Consumer Electronics Retail Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

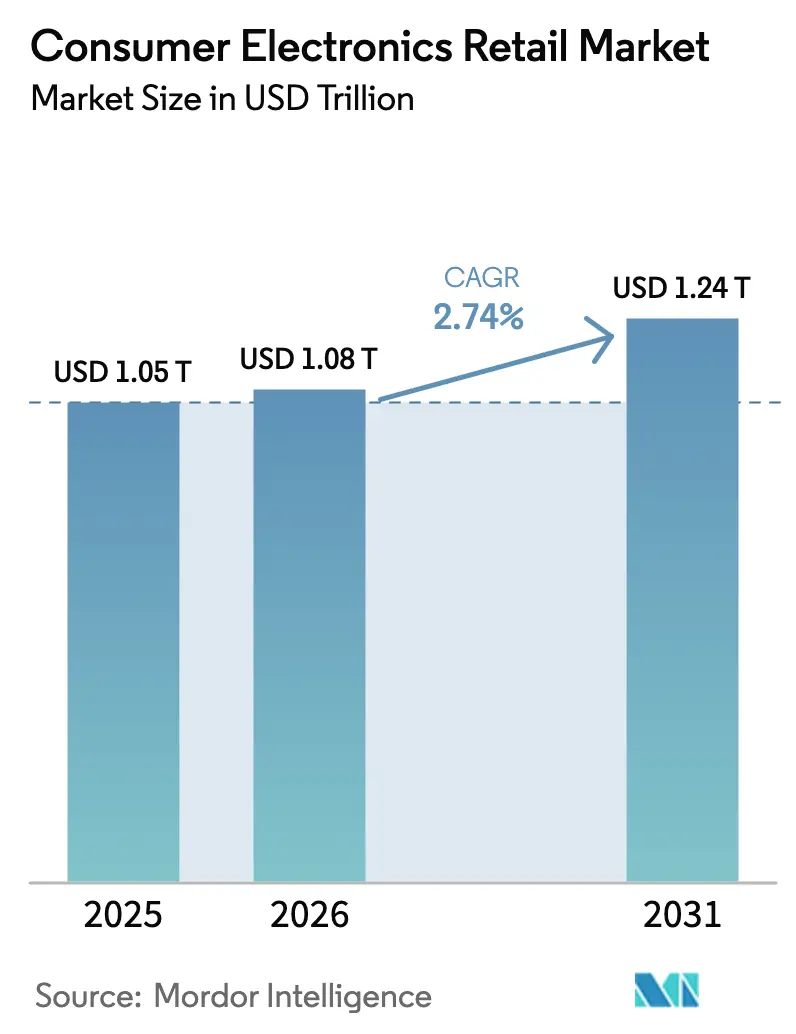

| Market Size (2026) | USD 1.08 Trillion |

| Market Size (2031) | USD 1.24 Trillion |

| Growth Rate (2026 - 2031) | 2.74% CAGR |

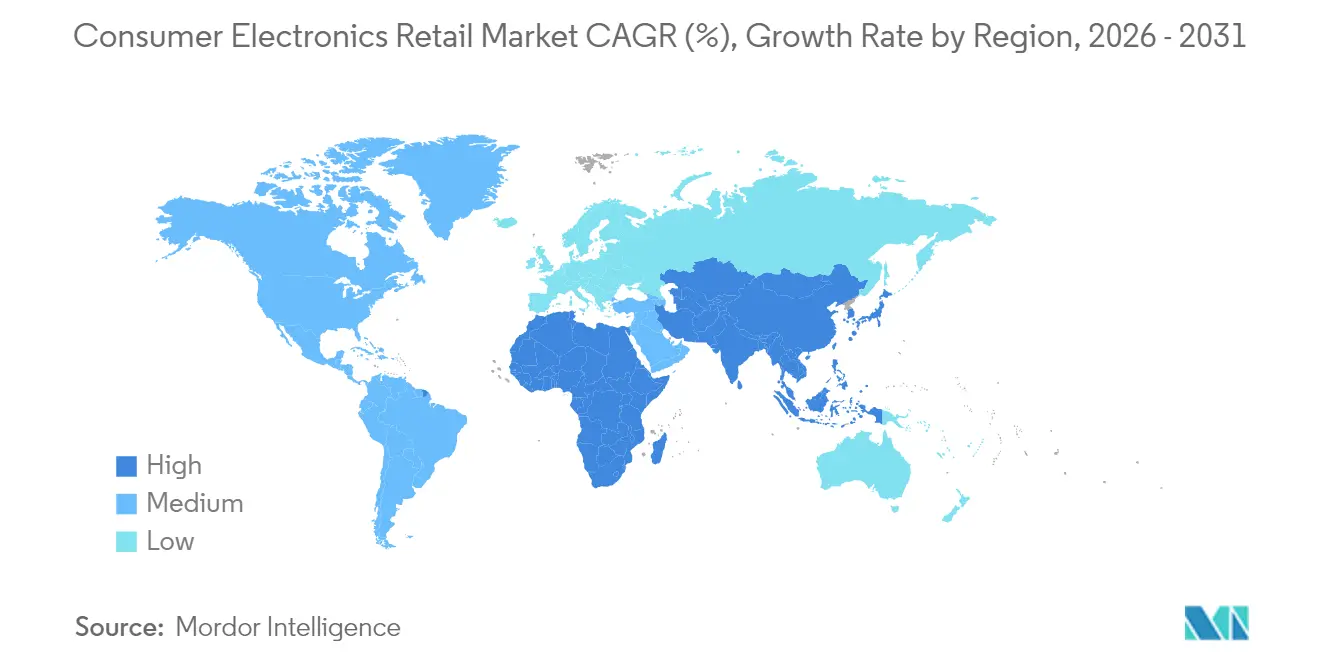

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Consumer Electronics Retail Market Analysis by Mordor Intelligence

Consumer Electronics Retail market size in 2026 is estimated at USD 1.08 trillion, growing from 2025 value of USD 1.05 trillion with 2031 projections showing USD 1.24 trillion, growing at 2.74% CAGR over 2026-2031. The measured CAGR masks a substantial channel realignment as direct-to-consumer storefronts, bundled smart-home ecosystems, and buy-now-pay-later (BNPL) financing schemes change where and how shoppers spend. At the same time, 5G upgrade cycles, experiential retail formats, and refurbished-device trade-in programs expand purchase occasions even as inflation limits discretionary budgets. Competitive intensity remains moderate: the top five retailers control just under 40% of worldwide sales, leaving meaningful white-space for region-focused specialists. Regionally, Asia-Pacific holds the largest share, yet Middle East & Africa is growing the fastest, proving that localized service, language support, and payment options remain critical to scale in emerging geographies. Inventory planning, meanwhile, stays vulnerable to chip supply swings, prompting retailers to deploy AI-based demand forecasts and multi-sourcing contracts to maintain shelf availability.

Key Report Takeaways

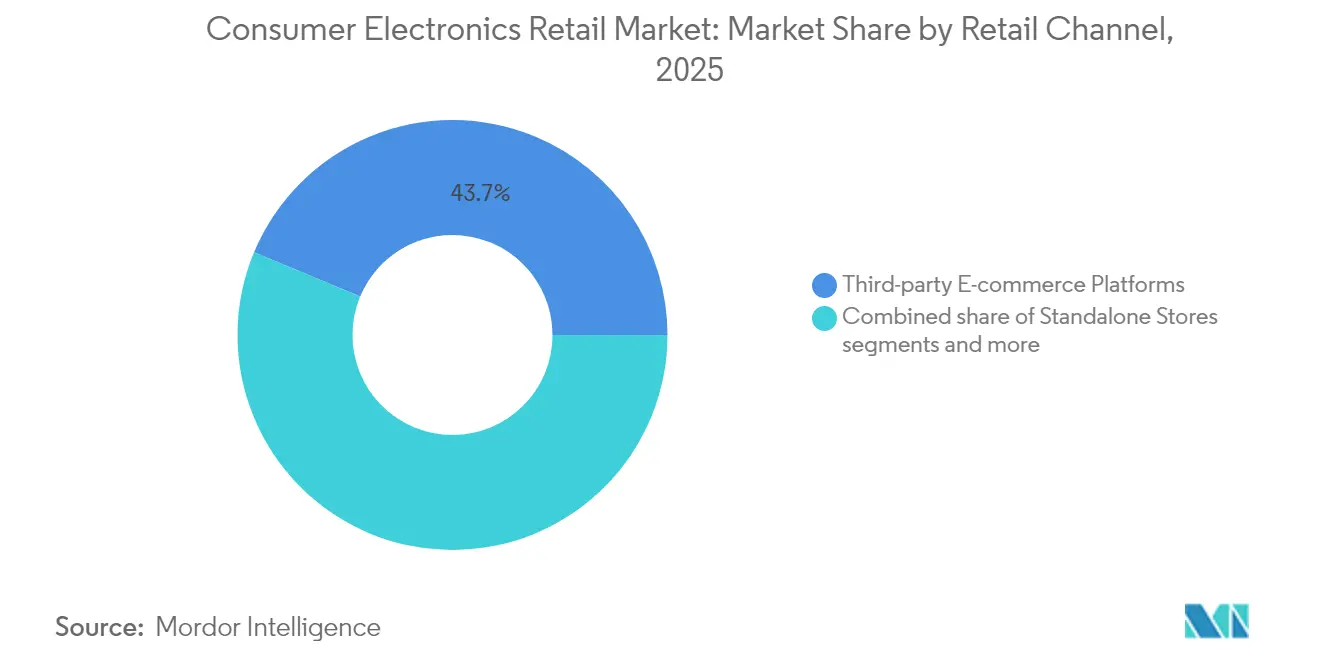

- By retail channel, third-party e-commerce platforms captured 43.72% of the Consumer Electronics Retail market share in 2025; brand-owned websites are projected to expand at a 9.92% CAGR to 2031.

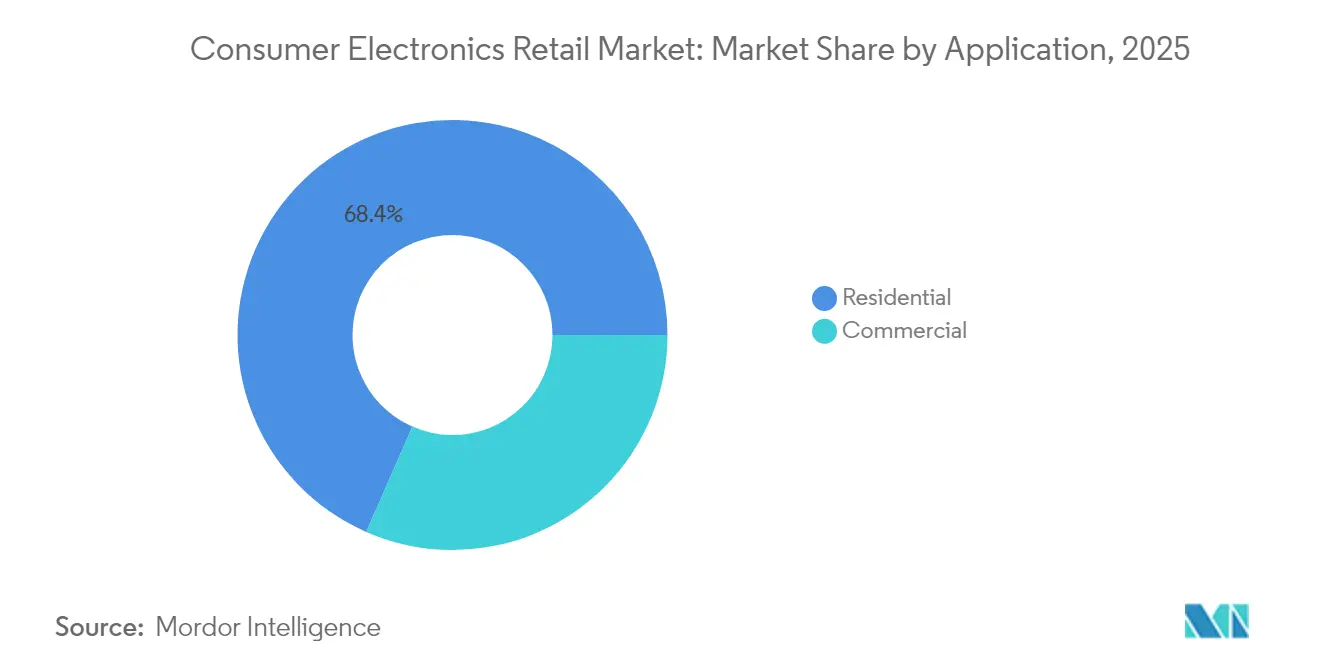

- By application, residential accounted for a 68.43% share of the Consumer Electronics Retail market size in 2025, while commercial is advancing at an 7.98% CAGR through 2031.

- By distribution channel, offline outlets held 56.71% of the Consumer Electronics Retail market size in 2025; online channels record the highest projected CAGR at 9.31% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Consumer Electronics Retail Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of direct-to-consumer (D2C) brand stores | +0.8% | Global, strongest in North America & APAC | Medium term (2-4 years) |

| Rising demand for smart home ecosystems | +0.7% | Global, led by North America & Europe | Long term (≥ 4 years) |

| Growth in "Buy Now, Pay Later" (BNPL) financing options | +0.6% | Global, highest penetration in North America & Europe | Short term (≤ 2 years) |

| Rapid 5G device replacement cycles | +0.5% | APAC core, spill-over to North America & Europe | Medium term (2-4 years) |

| Emergence of experiential retail formats (AR/VR demos) | +0.3% | North America & Europe, expanding to APAC | Long term (≥ 4 years) |

| Circular-economy trade-in & refurbished programs | +0.4% | Global, regulatory driven in Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Direct-to-Consumer Brand Stores

Manufacturers increasingly bypass traditional retail intermediaries to establish direct customer relationships, capturing higher margins while controlling brand experience across touchpoints. Xiaomi's expansion into Spain with dedicated Mi Stores in 2024 exemplifies this strategy, as the Chinese brand seeks to differentiate from commodity Android offerings through curated retail environments. This D2C pivot accelerates as brands recognize that traditional retailers often commoditize their products, limiting differentiation opportunities and margin capture. Best Buy's response includes strategic partnerships with brands like Ikea to create shop-in-shop experiences, acknowledging that pure-play electronics retailers must evolve beyond transactional relationships. The trend particularly benefits premium brands that can justify dedicated retail footprints, while mid-tier manufacturers explore pop-up formats and experiential showrooms to test market receptivity before committing to permanent locations.

Rising Demand for Smart Home Ecosystems

Interconnected device ecosystems drive multi-product purchasing behaviours, as consumers seek seamless integration across lighting, security, entertainment, and climate control systems. Samsung's SmartThings platform integration across appliances, mobile devices, and home automation products creates switching costs that lock customers into the ecosystem, generating recurring revenue through services and accessories[1]Samsung Electronics, “2024 Business Report,” samsung.com.. The Matter standard's adoption in 2024 reduces interoperability barriers, paradoxically intensifying competition as consumers gain confidence in cross-brand compatibility. LG's ThinQ platform demonstrates how traditional appliance manufacturers leverage connectivity to enter adjacent categories, with refrigerators becoming central hubs for grocery ordering and energy management. This ecosystem approach transforms one-time hardware sales into ongoing service relationships, fundamentally altering retailer value propositions from product-centric to solution-oriented offerings.

Growth in Buy Now, Pay Later Financing Options

BNPL services expand electronics affordability by fragmenting large purchases into manageable installments, particularly appealing to younger demographics with limited credit history. Affirm's partnership expansions with electronics retailers in 2024 demonstrate how BNPL providers target high-consideration categories where payment flexibility influences purchase decisions[2]Affirm Holdings, “2024 Investor Letter,” affirm.com.. Research indicates that 43% of Gen Z consumers prefer BNPL over traditional credit cards for electronics purchases, as these services avoid interest charges when payments are made on schedule. The trend particularly benefits retailers selling premium devices, as BNPL reduces psychological barriers to higher-priced items while maintaining cash flow through immediate payment from BNPL providers. However, regulatory scrutiny intensifies as consumer advocacy groups raise concerns about over-leveraging, potentially constraining future growth as compliance costs increase.

Rapid 5G Device Replacement Cycles

As 5G network coverage now reaches over 80% of the global population, users are accelerating the transition from 4G to 5G devices, upgrading their handsets far sooner than historical replacement cycles would suggest. This shift is being driven not only by faster network speeds but also by growing consumer demand for high-performance mobile experiences such as real-time gaming, HD streaming, and AI-driven applications, which place increasing strain on legacy 4G devices. According to forecasts by Ericsson, average monthly smartphone data consumption is expected to exceed 7 GB by 2025, placing further pressure on outdated hardware and encouraging users to adopt newer, 5G-enabled models[3]Ericsson AB, “Mobility Report 2024,” ericsson.com. . Retailers are capitalizing on this momentum by offering compelling trade-in incentives, such as elevated credit for old devices and seamless same-day data transfer services, effectively lowering upgrade barriers while enhancing customer convenience. These strategies not only boost new device sales but also create secondary revenue streams through the resale of refurbished units, contributing to circular economy initiatives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent global chip supply volatility | -0.9% | Global, most severe in APAC manufacturing hubs | Medium term (2-4 years) |

| Inflation-driven discretionary-spend pullback | -0.7% | Global, acute in Europe & South America | Short term (≤ 2 years) |

| Intensifying cross-border e-commerce price competition | -0.4% | Global, strongest impact in Europe & North America | Long term (≥ 4 years) |

| Growing regulatory scrutiny on e-waste compliance | -0.3% | Europe & North America, expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Global Chip Supply Volatility

Semiconductor shortages continue disrupting electronics retail inventory planning, as Hurricane Helene's impact on North Carolina's Spruce Pine quartz mining operations in 2024 highlighted critical supply chain vulnerabilities. This facility supplies approximately 70% of global high-purity quartz essential for semiconductor wafer production, demonstrating how geographically concentrated raw material sources create systemic risks. Artificial intelligence demands further strain on chip allocation, as data center processors command premium pricing and priority allocation over consumer electronics applications. Retailers respond by diversifying supplier relationships and implementing AI-driven demand forecasting to optimize inventory allocation across product categories. General Motors' deployment of AI-powered supply chain risk management systems exemplifies how major buyers proactively identify potential disruptions before they impact production schedules.

Inflation-driven Discretionary Spend Pullback

Persistent inflationary pressures constrain consumer electronics purchases as households prioritize essential goods over discretionary upgrades. Federal Reserve data indicate that consumer electronics spending declined 3.20% year-over-year in Q3 2024, as inflation-adjusted disposable income growth lagged price increases across multiple categories. This constraint particularly affects mid-tier products, as consumers either delay purchases or trade down to basic functionality devices, compressing retailer margins on volume-driven categories. Proposed tariff policies could exacerbate these pressures, with Peterson Institute estimates suggesting 25% tariffs on Chinese electronics could increase laptop prices by 45% and smartphone costs by 26%. Retailers adapt through expanded trade-in programs and financing partnerships, attempting to maintain transaction volumes despite affordability constraints.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Retail Channel: Third-Party Platforms Dominate, D2C Outpaces

Third-party e-commerce held 43.72% of the Consumer Electronics Retail market share in 2025, but brand-owned websites are projected to capture the highest 9.92% CAGR through 2031, reflecting brands’ appetite for direct data ownership. The Consumer Electronics Retail market size attributed to D2C sites is forecast to add more than USD 44.2 billion over the horizon, helping manufacturers offset wholesale margin erosion. Physical omni-channel chains respond with curbside pickup, same-day delivery, and subscription-based tech-support bundles to preserve traffic. D2C momentum does not spell extinction for marketplace giants; network effects still funnel small brands to Amazon for demand generation. Yet, escalating platform fees have triggered high-volume sellers to co-launch standalone sites supported by social-commerce traffic. Standalone mall stores face a shallower 3.22% CAGR as foot traffic migrates to mixed-use developments, but experiential anchors—VR gaming dens or smart-home mockups—can lift dwell time and attachment rates. Ultimately, channel coexistence evolves toward customer-journey orchestration: discovery may start on TikTok, comparison on a marketplace, and purchase at a brand app with in-store pickup.

By Application: Residential Retains Scale, Commercial Accelerates

Residential applications generated 68.43% of the Consumer Electronics Retail market size in 2025, underpinned by multi-device households and smart-home uptake. Nevertheless, the commercial segment is set to grow at 7.98% CAGR on the back of hybrid-work investments. Collaboration displays, conferencing bars, and security analytics servers headline procurement lists as enterprises retrofit spaces for flexible attendance. Commercial buyers operate on total-cost-of-ownership logic; thus, retailers extend managed-services contracts and financing to lock in three- to five-year refresh commitments, elevating lifetime value. Residential shoppers continue to prioritize ease and instant gratification; one-hour delivery windows on premium phones and consoles have proven to increase conversion by 17% for retailers offering the service. As macro conditions tighten, both segments gravitate toward trade-in rebates, establishing a circular inventory stream that lowers entry price and improves environmental credentials.

By Distribution Channel: Online Surges, Offline Reinvents

Online distribution channels surge at 9.31% CAGR through 2031, steadily gaining share against offline channels that maintain 56.71% market share in 2025 but grow at only 4.05% CAGR. This shift reflects permanent behavioural changes from pandemic-era shopping patterns, as consumers embrace digital research and purchase processes for electronics categories. Amazon's electronics segment growth demonstrates online platforms' advantages in selection breadth and price transparency, while traditional retailers invest heavily in omni-channel capabilities to remain competitive. Best Buy's successful "buy online, pick up in store" model illustrates how offline retailers can leverage physical assets to compete with pure-play digital platforms.

The channel evolution creates distinct competitive dynamics, with online platforms excelling in convenience and selection while offline stores provide hands-on product evaluation and immediate gratification. Experiential retail formats attempt to bridge this gap, using AR and VR demonstrations to replicate online information richness within physical environments. Walmart's electronics department redesign in 2024 exemplifies how traditional retailers integrate digital tools to enhance in-store experiences while maintaining their logistics and inventory advantages. Regulatory compliance factors increasingly influence channel strategies, as e-waste management requirements favor retailers with established reverse logistics capabilities for trade-in and recycling programs.

Geography Analysis

Asia-Pacific dominates the Consumer Electronics Retail market with a 36.05% share in 2025, leveraging manufacturing proximity, rising middle-class consumption, and rapid e-commerce adoption across key economies. China's "New Retail" integration of online and offline channels creates sophisticated omni-channel experiences that Western retailers are now emulating, while India's consumer durables sector grows at approximately 11% CAGR as EY projects the country to become the world's fourth-largest market by fiscal 2027. Indonesia's Electronic City invested USD 15 million in retail expansion during 2024, reflecting regional confidence in sustained demand growth despite global economic uncertainties. Southeast Asia's e-commerce momentum continues with Vietnam's market projected to reach USD 63 billion by 2030, driven by mobile-first shopping behaviours and improving logistics infrastructure.

Middle East & Africa emerges as the fastest-growing region at 7.61% CAGR through 2031, attracting significant foreign investment as retailers recognize untapped market potential. TJX Companies' USD 360 million acquisition of a 35% stake in the UAE's Brands for Less in 2024 signals major retailers' confidence in regional growth prospects, while Sharp's USD 30 million joint venture with Egypt's Elaraby Group for refrigerator manufacturing demonstrates how global brands establish local production to serve expanding markets. The region benefits from young demographics, increasing urbanization, and government digitization initiatives that drive electronics adoption across consumer and commercial segments.

North America and Europe face mature market dynamics with 4.14% and 3.47% CAGR, respectively, through 2031, as replacement cycles extend and consumers become more selective about upgrades. However, these regions lead in premium segment adoption and experiential retail innovation, with Best Buy's VR demonstration areas and Apple's expanded service offerings setting global standards for customer engagement. European markets particularly emphasize sustainability compliance, with WEEE (Waste Electrical and Electronic Equipment) directive requirements creating competitive advantages for retailers with established circular economy programs. South America's 4.93% CAGR reflects economic recovery and expanding middle-class access to consumer electronics, though currency volatility and import dependencies create ongoing challenges for consistent growth trajectories.

Competitive Landscape

The Consumer Electronics Retail market shows moderate fragmentation, with the top five players collectively holding a notable portion of global market share. This structure leaves substantial room for specialized retailers and regional leaders to capture niche segments through tailored offerings and local market understanding. Amazon leads globally, benefiting from the scalability of its marketplace model and robust logistics infrastructure. Meanwhile, Walmart remains a strong contender, utilizing its extensive physical store network and supply chain capabilities to compete effectively in electronics. Competitive dynamics vary widely by region and sales channel, influenced by factors such as consumer behaviour, regulatory environments, and market maturity.

Strategic differentiation in the market is shifting away from purely transactional retail models toward experiential and service-oriented formats. As online platforms become increasingly dominant in product pricing and convenience, brick-and-mortar retailers are investing in added-value services to retain customer loyalty. Best Buy’s Geek Squad and Apple’s Genius Bar exemplify this shift, offering technical support and post-sale engagement that create switching costs and deepen brand relationships. These service layers help traditional retailers defend against both direct-to-consumer brands and international e-commerce players that bypass conventional distribution systems. In this landscape, building emotional and service-based loyalty is becoming just as important as offering competitive pricing.

Technological innovation continues to accelerate, with AI-powered personalization, chat-based customer support, and augmented reality product demos now expected rather than exceptional. As digital tools become standard across leading platforms, the focus is turning toward execution excellence and seamless integration of online and offline experiences. Growth opportunities are also emerging in underserved geographies and niche product segments where customer needs remain unmet by mass-market players. Additionally, increasing regulatory pressure on sustainability is driving demand for services like certified refurbishing, recycling, and trade-in programs areas that require strong operational capabilities and compliance expertise. Retailers that can navigate these complexities while maintaining customer trust are likely to gain long-term competitive advantages.

Consumer Electronics Retail Industry Leaders

Amazon.com, Inc

Walmart Inc.

Best Buy Co., Inc.

JD.com Inc.

MediaMarktSaturn Retail Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: TJX Companies acquired a 35% stake in UAE-based Brands for Less for USD 360 million, marking the discount retailer's major expansion into Middle Eastern electronics and consumer goods markets. This strategic investment positions TJX to capitalize on the region's growing middle-class consumption and establishes a platform for further regional expansion.

- August 2024: Sharp Corporation formed a USD 30 million joint venture with Egypt's Elaraby Group to manufacture refrigerators and home appliances locally. This partnership enables Sharp to serve North African markets more cost-effectively while reducing import dependencies and currency exposure risks.

- July 2024: Electronic City Indonesia announced a USD 15 million retail expansion plan, opening 25 new stores across Java and Sumatra islands. The expansion reflects confidence in Indonesia's growing consumer electronics demand and aims to capture market share from online-only competitors through an omnichannel presence.

- June 2024: Xiaomi opened its first flagship Mi Store in Madrid, Spain, as part of a broader European retail expansion strategy. The 200-square-meter store features interactive product demonstrations and represents Xiaomi's push to establish direct customer relationships beyond its traditional online channels.

Global Consumer Electronics Retail Market Report Scope

A consumer electronics retailer is a business primarily focused on selling electronic devices designed for personal use, commonly through physical retail outlets. These retailers offer various products, including televisions, computers, smartphones, home appliances, and entertainment systems. The market forecast is segmented by retail channel, application, distribution channel, and geography. The market is segmented by Retail Channel into Standalone Stores, Shopping Malls, Brand-owned Websites, Third-party E-commerce Platforms, Omni-Channel Retailers, and Other Retails Channels. By applications, the market is segmented into residential and commercial applications. Lastly, by distribution channels, the market is segmented into offline and online. And by geography, the market is segmented into Asia-Pacific, North America, Europe, South America, Middle East & Africa, and the Asia-Pacific. The reports offer the market sizing and forecasts for the consumer electronics retailers market in value (USD) for all the above segments.

| Standalone Stores |

| Shopping Malls |

| Brand-owned Websites |

| Third-party E-commerce Platforms |

| Omni-Channel Retailers |

| Other Retail Channels |

| Residential |

| Commercial |

| Offline |

| Online |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Retail Channel | Standalone Stores | |

| Shopping Malls | ||

| Brand-owned Websites | ||

| Third-party E-commerce Platforms | ||

| Omni-Channel Retailers | ||

| Other Retail Channels | ||

| By Application | Residential | |

| Commercial | ||

| By Distribution Channel | Offline | |

| Online | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the Consumer Electronics Retail market in 2026?

The Consumer Electronics Retailers Market size is expected to reach USD 1.08 trillion in 2026 and grow at a CAGR of 2.74% to reach USD 1.24 trillion by 2031.

Which retail channel is growing the fastest for electronics?

Brand-owned websites lead growth with a projected 9.92% CAGR through 2031, driven by manufacturers seeking direct customer engagement.

What region delivers the highest growth rate for electronics sales?

Middle East & Africa is expected to post a 7.61% CAGR, benefiting from young demographics and expanding digital infrastructure.

How are retailers addressing chip supply shortages?

Retailers deploy AI forecasting, diversify supplier bases, and secure pre-paid allocation contracts to stabilize product availability.

Why is BNPL important to electronics retail?

BNPL lifts conversion rates by fragmenting large-ticket payments into interest-free installments, making premium devices accessible to credit-averse shoppers

Page last updated on: