United States Hardware Stores Retail Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

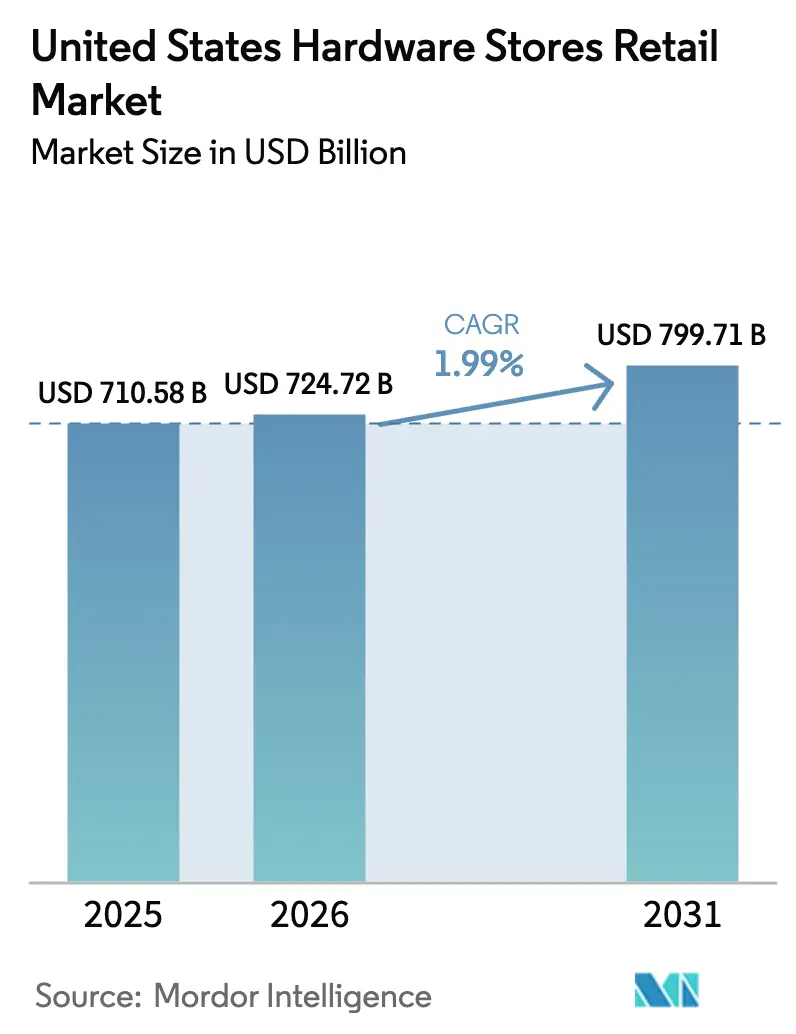

| Base Year Market Size (2025) | USD 710.58 Billion |

| Market Size (2026) | USD 724.72 Billion |

| Market Size (2031) | USD 799.71 Billion |

| Growth Rate (2026 - 2031) | 1.99% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Hardware Stores Retail Market Analysis by Mordor Intelligence

The United States hardware stores retail market size in 2026 is estimated at USD 724.72 billion, growing from 2025 value of USD 710.58 billion with 2031 projections showing USD 799.71 billion, growing at 1.99% CAGR over 2026-2031. Renovation spending outpaces new‐build activity as elevated mortgage rates convince many homeowners to remodel rather than relocate, channelling discretionary dollars toward big-ticket kitchen, bathroom, and energy-efficiency upgrades. Population gains in the South, wildfire-resilience mandates in the West, and expanding energy codes nationwide keep baseline demand intact even when broader construction indicators soften[1]“Home Building Geography Index,” National Association of Home Builders, nahb.org. . Large retailers leverage scale to lock in commodity supply and pass along price fluctuations more effectively than independents, while social-media-fueled DIY trends support weekend traffic and higher-margin impulse purchases. The United States hardware stores retail market benefits from a dual engine of professional contractor demand and consumer-driven projects that together mute cyclical volatility.

Key Report Takeaways

- By product type, building materials led with 36.05% of the United States hardware stores retail market share in 2025; Smart-Home Hardware is projected to expand at a 10.03% CAGR through 2031.

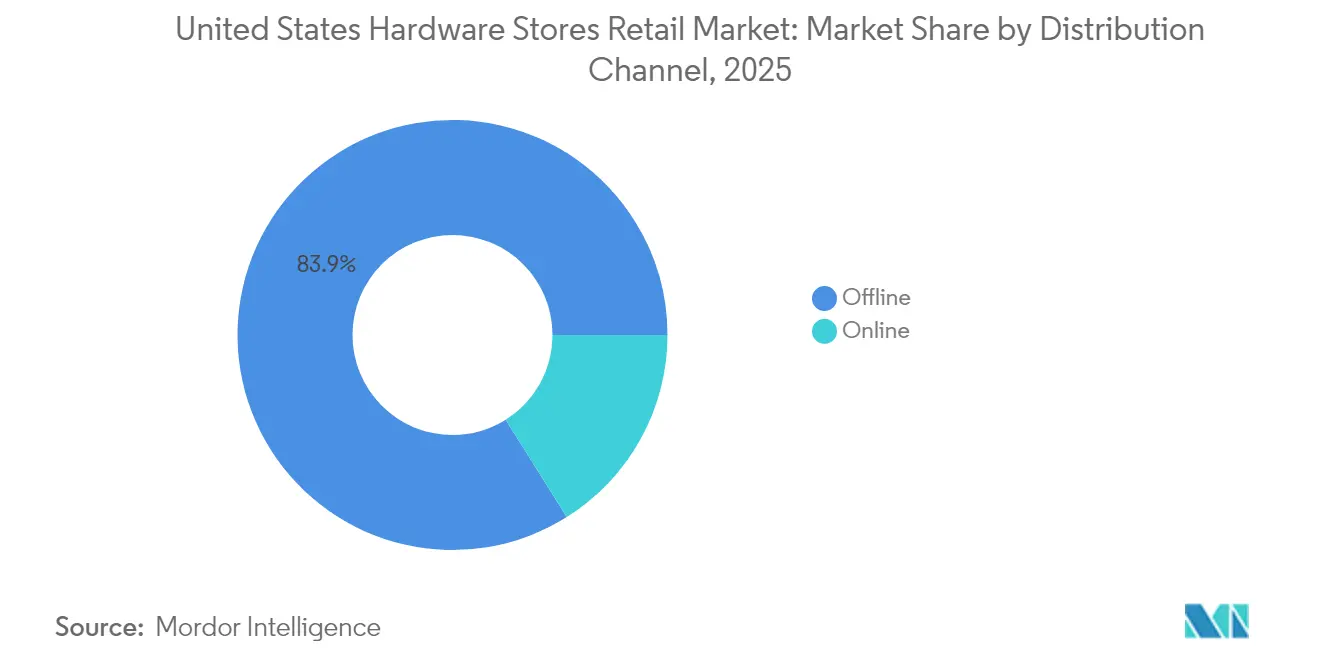

- By distribution channel, offline outlets accounted for 83.92% of the United States hardware stores retail market size in 2025, while online sales are rising at a 13.42% CAGR to 2031.

- By store format, big-box home centers captured 58.88% share of the United States hardware stores retail market size in 2025; online-only platforms recorded the quickest growth at an 11.05% CAGR.

- By region, the South commanded 34.12% of the United States hardware stores retail market share in 2025, whereas the West is advancing at a 6.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Hardware Stores Retail Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Big-ticket home-renovation boom post-2024 | +0.8% | National, concentrated in high home-equity markets | Medium term (2-4 years) |

| DIY culture amplified by social-media tutorials | +0.4% | National, stronger in younger demographics | Short term (≤ 2 years) |

| Energy-efficient building code updates | +0.3% | National, led by California and Northeast states | Long term (≥ 4 years) |

| Rapid wildfire-resilient construction mandates | +0.2% | West Coast, expanding to Mountain states | Medium term (2-4 years) |

| Aging-in-place retrofits for seniors | +0.2% | National, concentrated in established suburbs | Long term (≥ 4 years) |

| Insurance-driven demand for fortified roofs | +0.1% | Gulf Coast, Southeast, expanding nationally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Big-Ticket Home-Renovation Boom Post-2024

Elevated mortgage rates averaging 6.5% through 2024 have fundamentally altered homeowner behaviour, creating a captive audience for renovation projects as moving becomes financially prohibitive[2]“U.S. Economic, Housing and Mortgage Outlook,” Freddie Mac, freddiemac.com. . This rate environment has generated what industry analysts term "mortgage rate lock-in," where homeowners with sub-4% rates from 2020-2021 defer selling, redirecting discretionary spending toward home improvements instead. The Joint Center for Housing Studies projects renovation spending will reach USD 509 billion in 2025, representing a 6.4% upward revision from earlier forecasts. Kitchen and bathroom upgrades dominate this spending surge, with homeowners increasingly viewing these projects as long-term investments rather than discretionary expenses. The trend particularly benefits hardware retailers through higher average transaction values and increased frequency of professional-grade product purchases.

DIY Culture Amplified by Social-Media Tutorials

Social media platforms have democratized home improvement knowledge, with YouTube and TikTok tutorials generating unprecedented confidence among novice DIY enthusiasts, particularly millennials and Gen Z homeowners. This cultural shift represents more than entertainment it translates directly into retail sales as tutorial viewers purchase materials and tools to replicate projects they observe online. The phenomenon has created viral trends around specific techniques and products, driving sudden demand spikes that challenge traditional inventory planning. Hardware retailers report increased sales of specialty tools and materials previously reserved for professional contractors, as social media content normalizes complex projects. The trend extends beyond individual projects to encompass broader lifestyle aspirations, where DIY capability signals personal competence and financial savvy. Retailers increasingly partner with social media influencers and create their own content to capture this audience, recognizing that digital engagement often precedes physical store visits.

Energy-Efficient Building Code Updates

The 2024 International Energy Conservation Code (IECC) implementation across multiple states has created mandatory demand for energy-efficient building materials, insulation systems, and HVAC components that meet stricter performance standards. These regulatory changes operate differently from market-driven trends they create non-negotiable compliance requirements that sustain demand regardless of economic conditions. California's Title 24 updates and similar state-level initiatives have established precedents that other jurisdictions follow, creating predictable waves of regulatory adoption. The codes particularly benefit hardware retailers through increased sales of high-performance insulation, energy-efficient windows, and smart building controls that command premium pricing. Professional contractors increasingly rely on retail channels to source compliant materials quickly, as project timelines compress under regulatory deadlines. The trend accelerates as federal tax credits align with state building codes, creating dual incentives for energy-efficient upgrades that hardware retailers are positioned to fulfil.

Rapid Wildfire-Resilient Construction Mandates

Western states have implemented increasingly stringent wildfire-resistant construction requirements, creating specialized demand for fire-rated roofing materials, ember-resistant vents, and defensible space landscaping products [3]“ISO Wildfire-Mitigation Rules,” Verisk Analytics, verisk.com. . California's Chapter 7A requirements and similar Oregon mandates represent regulatory responses to escalating wildfire losses that now exceed USD 57 billion annually in insured damages. These regulations create captive markets for specialized products that traditional hardware stores previously stocked minimally, forcing rapid assortment expansion and supplier relationship development. The mandates extend beyond new construction to encompass retrofits in high-risk zones, generating recurring revenue streams as existing structures require compliance upgrades. Insurance companies increasingly require wildfire-resistant features for policy renewals, creating additional market pressure beyond regulatory compliance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pro-contractor consolidation bypassing retail | -0.4% | National, strongest in commercial construction markets | Long term (≥ 4 years) |

| Volatile lumber & steel pricing | -0.3% | National, acute in import-dependent regions | Short term (≤ 2 years) |

| Skilled-labor shortages slowing DIY completions (under-the-radar) | -0.2% | Tier-2/3 cities and suburban areas | Medium term (2–4 years) |

| Rising retail crime/shrink rates on small hardware items (under-the-radar) | -0.2% | Urban centers and high-footfall retail zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Pro-Contractor Consolidation Bypassing Retail

Large-scale professional contractors increasingly establish direct relationships with manufacturers and distributors, circumventing traditional retail channels to secure volume pricing and guaranteed supply allocation. This trend accelerates as contractor consolidation creates entities with sufficient scale to negotiate manufacturer-direct terms previously reserved for major retailers. The shift particularly impacts high-volume, low-margin products where contractors can achieve 15-25% cost savings through direct sourcing arrangements. Regional contractor networks and buying cooperatives further amplify this trend, pooling smaller operators' purchasing power to access wholesale pricing. Hardware retailers respond by emphasizing value-added services, specialized products, and emergency availability that direct channels cannot replicate, but the structural shift toward disintermediation remains a persistent headwind for traditional retail models.

Volatile Lumber & Steel Pricing

Commodity price volatility, exacerbated by tariff policies and supply chain disruptions, creates planning challenges that compress retailer margins and deter large project commitments from price-sensitive customers. Steel prices increased 15-25% and lumber rose 17.2% year-over-year through early 2025, driven by tariff implementations and retaliatory trade measures. These price swings create inventory valuation challenges for retailers, who must balance carrying costs against stockout risks while maintaining competitive pricing. Professional contractors increasingly demand fixed-price quotes with extended validity periods, transferring price risk to retailers who lack manufacturers' hedging capabilities. The volatility particularly impacts project-based sales, where material cost uncertainty can delay or cancel large renovations, reducing both immediate revenue and future maintenance-related purchases.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Building Materials Drive Core Demand

Building Materials commanded 36.05% market share in 2025, reflecting their fundamental role in both new construction and renovation projects across residential and commercial applications. This segment's dominance stems from recurring replacement cycles and regulatory compliance requirements that sustain baseline demand regardless of economic conditions. Smart-Home Hardware emerges as the fastest-growing segment at 10.03% CAGR through 2031, driven by consumer adoption of connected devices and integration with home automation systems. Door Hardware maintains steady demand through security upgrade cycles and aesthetic renovation trends, while Kitchen and Toilet Products benefit from bathroom and kitchen remodeling projects that represent the highest-value home improvement categories.

The segment's evolution reflects broader technological integration, where traditional hardware increasingly incorporates smart features and connectivity options that command premium pricing. Lowe's partnership with OpenAI for its "Mylow" AI advisor demonstrates how retailers leverage technology to guide product selection and cross-selling within this category. Other Product Types capture specialized applications and emerging categories that don't fit traditional classifications, representing innovation opportunities for retailers willing to experiment with new product lines and supplier relationships.

By Distribution Channel: Offline Dominance Faces Digital Disruption

Offline channels maintained 83.92% market share in 2025, demonstrating the enduring importance of physical touchpoints for product evaluation, immediate availability, and professional contractor relationships. This dominance reflects hardware retail's tactile nature, where customers need to assess product quality, compatibility, and specifications before making purchase decisions. However, Online channels accelerate at a 13.42% CAGR through 2031, driven by convenience, expanded product assortments, and improved logistics capabilities that reduce delivery times for urgent projects. The online growth particularly benefits specialized products and hard-to-find items that physical stores cannot economically stock. Successful retailers increasingly adopt omnichannel strategies that blur traditional distribution boundaries, offering services like buy-online-pickup-in-store, curbside delivery, and virtual consultations that combine digital convenience with physical fulfillment. Home Depot's investment in supply chain automation and Lowe's Total Home Strategy exemplify how major players integrate digital and physical capabilities to capture growth across both channels while defending against pure-play online competitors.

By Store Format: Big-Box Efficiency Versus Specialized Service

Big-Box Home Centers captured 58.88% market share in 2025, leveraging their vast product assortments, competitive pricing, and integrated professional services to dominate both DIY and contractor segments. These formats benefit from economies of scale in purchasing, logistics, and marketing that smaller competitors cannot match, while their size enables comprehensive one-stop shopping experiences that reduce customer acquisition costs. Online-Only Platforms represent the fastest-growing format at 11.05% CAGR through 2031, targeting specialized needs and niche products that physical stores cannot economically serve. Traditional Hardware Stores and Lumber & Building-Material Yards maintain relevance through personalized service, local market knowledge, and specialized expertise that big-box formats struggle to replicate consistently. The format evolution reflects changing customer expectations, where convenience and expertise matter more than pure price competition. Farm & Ranch Supply Stores and Warehouse Clubs serve distinct customer segments with tailored assortments and service models, while the recent consolidation of True Value and Do it Best demonstrates how smaller formats must achieve scale to remain competitive.

Geography Analysis

The South's market leadership at 34.12% share in 2025 reflects sustained demographic and economic advantages that create durable demand for hardware retail across both residential and commercial applications. Population growth in states like Texas, Florida, and North Carolina drives new construction activity that generates contractor purchases and subsequent homeowner maintenance needs. The region's business-friendly regulatory environment and lower construction costs attract both residents and businesses, creating multiplier effects that sustain hardware demand across economic cycles. Hurricane preparedness requirements increasingly drive specialized product demand, with insurance companies offering 20-55% premium discounts for FORTIFIED construction standards that require specific materials and installation techniques.

The West's 6.9% CAGR through 2031 reflects unique regulatory and demographic drivers that create premium product opportunities despite slower construction activity. California's stringent building codes and wildfire regulations mandate specialized materials that command higher margins, while high home values justify expensive retrofit projects that generate substantial per-transaction revenue. The region's technology adoption leadership creates early-mover advantages for smart home products and connected building systems that eventually expand to other markets. Aging-in-place demographics particularly impact Western markets, where high housing costs encourage seniors to retrofit existing homes rather than relocate, driving demand for accessibility modifications and safety equipment.

The Northeast and Midwest maintain steady demand through renovation cycles and infrastructure replacement needs, with older housing stock requiring more frequent maintenance interventions than newer construction in growth regions. These markets emphasize energy efficiency upgrades and weatherization projects that align with state-level climate initiatives and utility rebate programs. Regional construction activity data shows the Middle Atlantic division recording 22% year-over-year growth in single-family starts during 2024, indicating pockets of strength that support localized hardware demand despite broader market maturity.

Competitive Landscape

The United States hardware retail market is deeply consolidated, with a small number of dominant players controlling the majority of industry revenue. This concentrated structure creates significant barriers to entry, making it difficult for smaller or new entrants to compete effectively. Larger retailers benefit from economies of scale in areas such as procurement, logistics, and digital investments, giving them a sustained competitive edge. These advantages are hard for independent or regional players to replicate. As a result, market leaders are shifting focus toward serving professional contractors and B2B customers, who typically generate higher-value transactions and more consistent demand than the DIY segment.

Strategic consolidation is gaining momentum as companies opt for acquisitions over organic growth to expand their capabilities and market presence. A notable example is Home Depot’s USD 18.25 billion acquisition of SRS Distribution, which strengthens its position in the professional contractor supply chain. This move supports vertical integration by linking wholesale distribution with retail operations. At the same time, technology adoption is becoming a major differentiator among top players. Lowe’s partnerships with OpenAI and NVIDIA are helping it deliver tailored shopping experiences and proactive maintenance solutions, increasing customer loyalty and operational efficiency.

New growth opportunities are also emerging in specialized niches that are less dependent on scale and more on localized expertise. Segments such as aging-in-place home modifications, smart home installation services, and regional contractor marketplaces offer room for innovation. These areas require service depth and customization, playing to the strengths of firms that can adapt to specific customer needs. Unlike the traditional big-box model, success here relies on a blend of service capabilities and local market knowledge. As consumer expectations evolve, these white-space areas are expected to become key growth drivers in the next phase of the market.

United States Hardware Stores Retail Industry Leaders

The Home Depot

Lowe’s Companies, Inc.

Menards

Ace Hardware Corp.

True Value Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Lowe's completed its acquisition of Artisan Design Group (ADG) for USD 1.325 billion on June 2, 2025, financing the deal with cash on hand. This acquisition strengthens Lowe's presence in the interior finishes market by integrating ADG's design, distribution, and installation services into its Pro division.

- December 2024: Home Depot completed its USD 18.25 billion acquisition of SRS Distribution, creating the largest professional building products distributor in North America with over 780 locations. This transaction fundamentally reshapes the professional contractor market by combining Home Depot's retail presence with SRS's specialized distribution network, enabling comprehensive coverage of both residential and commercial construction projects.

- November 2024: True Value Company completed its bankruptcy-driven sale to Do it Best Corp for an undisclosed amount, consolidating two major hardware cooperatives and affecting over 4,500 independent retailers. The merger creates the largest hardware cooperative in North America, providing enhanced buying power and operational efficiency for member stores competing against big-box retailers.

- September 2024: Do it Best Corp and United Hardware merged their operations to create an expanded cooperative serving over 3,800 member retailers across North America. The combination provides enhanced distribution capabilities and technology resources to independent hardware stores facing increasing competition from national chains.

United States Hardware Stores Retail Market Report Scope

Hardware store retail refers to the business of selling a variety of tools, equipment, and supplies used in construction, maintenance, and repair tasks. The US hardware stores retail market is segmented by product type and distribution channel. By product type, the market is segmented into door hardware, building materials, kitchen and toilet products, and other product types. By distribution channel, the market is segmented into offline and online. The report offers market sizing and forecasts in value (USD) for all the above segments.

| Door Hardware |

| Building Materials |

| Kitchen and Toilet Products |

| Other Product Types |

| Offline |

| Online |

| Big-Box Home Centers |

| Traditional Hardware Stores |

| Lumber & Building-Material Yards |

| Farm & Ranch Supply Stores |

| Warehouse Clubs |

| Northeast |

| Midwest |

| South |

| West |

| By Product Type | Door Hardware |

| Building Materials | |

| Kitchen and Toilet Products | |

| Other Product Types | |

| By Distribution Channel | Offline |

| Online | |

| By Store Format | Big-Box Home Centers |

| Traditional Hardware Stores | |

| Lumber & Building-Material Yards | |

| Farm & Ranch Supply Stores | |

| Warehouse Clubs | |

| By Region (U.S.) | Northeast |

| Midwest | |

| South | |

| West |

Key Questions Answered in the Report

Which product category generates the most revenue?

Building Materials lead with 36.05% share, reflecting core demand for structural staples.

What channel is growing fastest?

Online sales are expanding at a 13.42% CAGR, outpacing the mature offline base.

Why are renovations supporting sales despite high rates?

Elevated mortgage rates discourage relocation, so homeowners invest in upgrades, boosting large-ticket transactions.

Which region shows the quickest growth through 2031?

The West is forecast to grow at 6.9% CAGR, driven by wildfire-resilience mandates and smart-home adoption.

Who dominates the competitive landscape?

Home Depot and Lowe’s together hold roughly 77% of revenue, giving them significant pricing and supply-chain leverage.

Page last updated on: