Cosmetic And Fragrance Retail Chain Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

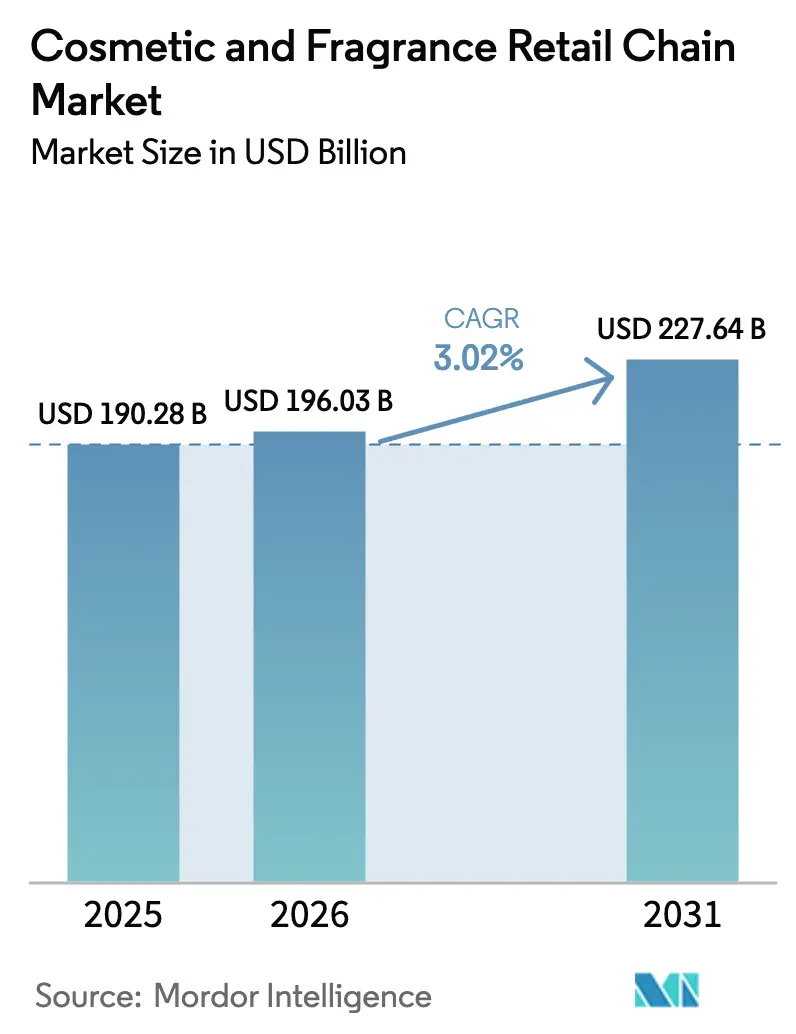

| Market Size (2026) | USD 196.03 Billion |

| Market Size (2031) | USD 227.64 Billion |

| Growth Rate (2026 - 2031) | 3.02% CAGR |

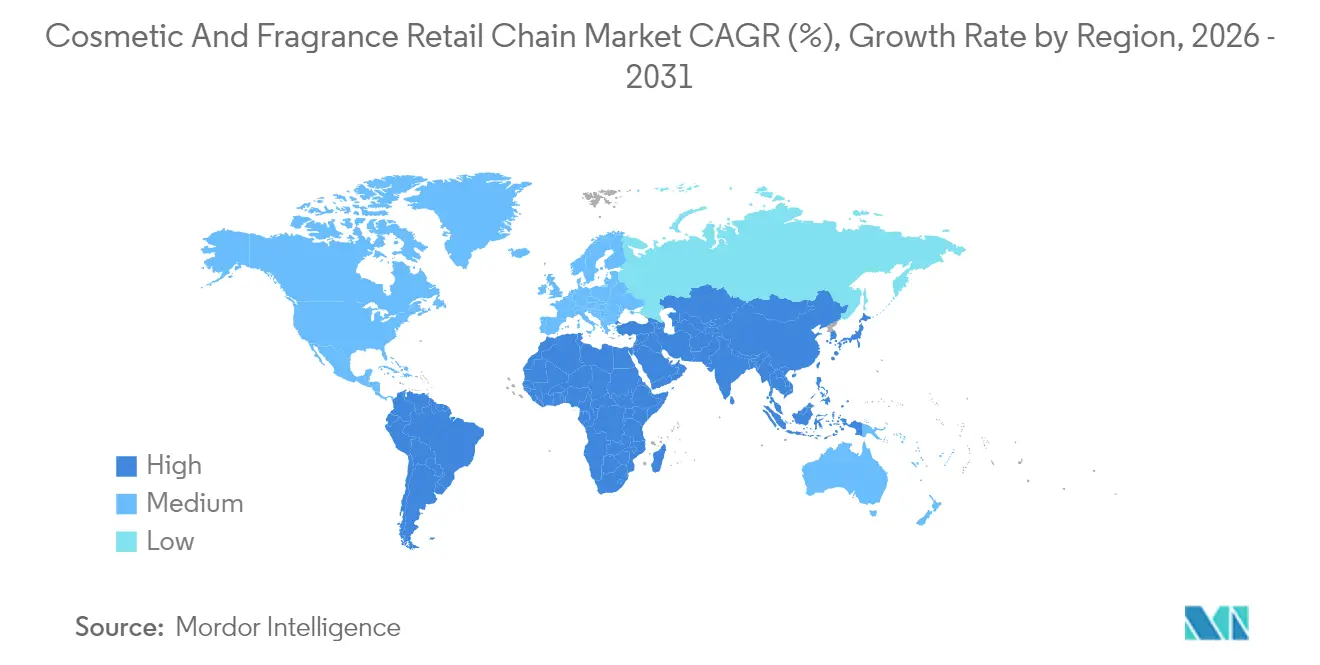

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cosmetic And Fragrance Retail Chain Market Analysis by Mordor Intelligence

The cosmetics and fragrance retail chain market size is expected to grow from USD 190.28 billion in 2025 to USD 196.03 billion in 2026 and is forecast to reach USD 227.64 billion by 2031 at 3.02% CAGR over 2026-2031. Sales momentum comes from experiential store formats that extend dwell time and raise basket values, omnichannel ecosystems that monetize first-party data, and AI-driven personalization tools that lift conversion rates. Leading chains refine loyalty programs into revenue-generating media platforms while investing in same-day delivery networks that widen urban catchment areas. Premiumization trends accelerate in emerging regions as middle-class consumers trade up to prestige brands, offsetting inflation-led down-trading in mature markets. At the same time, compliance with stricter sustainability rules and persistent gray-market leakage present margin headwinds, prompting retailers to optimize assortments and packaging initiatives.

Key Report Takeaways

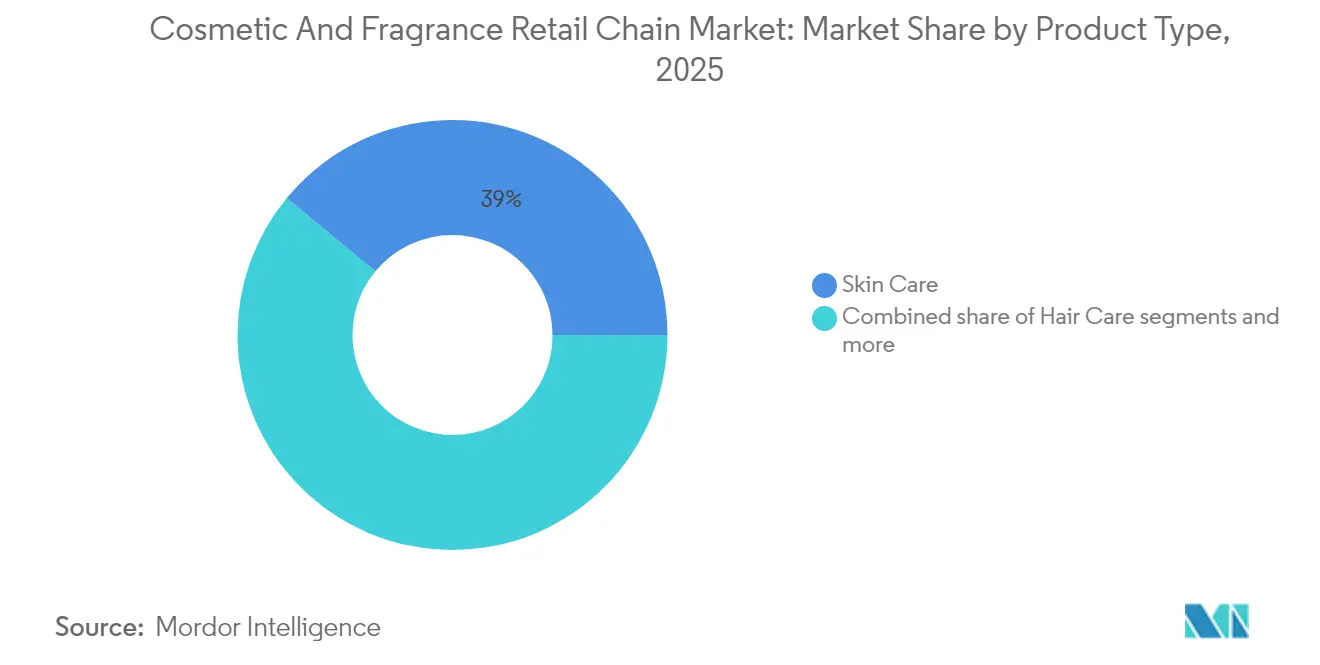

- By product type, skin care led with 39.02% revenue share of the cosmetics and fragrance retail chain market in 2025, while fragrances are expanding at an 7.95% CAGR to 2031.

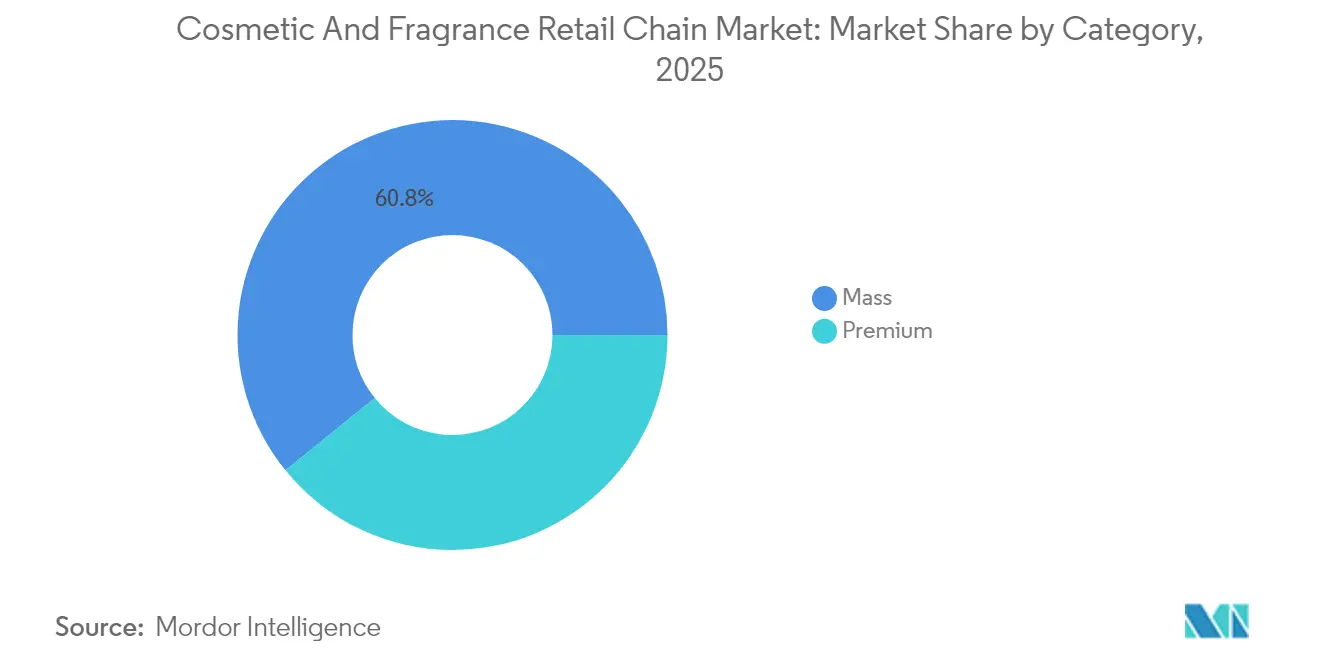

- By category, the mass segment held 60.84% of the cosmetics and fragrance retail chain market share in 2025; premium offerings are forecast to expand at a 10.05% CAGR through 2031.

- By end user, women accounted fora 59.72% share of the cosmetics and fragrance retail chain market size in 2025, whereas men’s grooming is growing at a 7.55% CAGR to 2031.

- By geography, Asia-Pacific captured 35.78% of the cosmetics and fragrance retail chain market share in 2025, and the Middle East & Africa is advancing at a 9.48% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cosmetic And Fragrance Retail Chain Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Experiential retail-tainment formats | +0.8% | North America & Europe core; APAC expansion | Medium term (2-4 years) |

| Omnichannel loyalty ecosystems | +0.6% | Global, strongest in developed markets | Long term (≥4 years) |

| Prestige shop-in-shop deals with mass retailers | +0.4% | North America dominant; selective EU adoption | Short term (≤2 years) |

| AI-enabled hyper-personalization & virtual try-on | +0.5% | Global with APAC and North America leadership | Medium term (2-4 years) |

| Cross-border e-commerce & same-day delivery | +0.3% | Global; urban concentration | Short term (≤2 years) |

| Emerging-market middle-class premium spend | +0.7% | APAC, MEA, South America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Experiential Retail-tainment Formats Driving Footfall

Chains redesign flagship locations into mini entertainment hubs that mix tutorials, café corners, and selfie zones to counter e-commerce substitution. Sephora’s Beauty Studio concept more than doubled average dwell time to 28 minutes and lifted basket values by 35% in Los Angeles and Shanghai stores in 2025[1]Tiffany Ap, “Sephora Greater China Head Steps Down,” Business of Fashion, businessoffashion.com. . A.S. Watson pumped USD 250 million into 6,000 Asia redesigns, layering QR-code-enabled discovery and O+O journeys that funnel app engagement. Chinese newcomer Harmay placed cinema-themed outlets inside Universal Studios Beijing, creating Instagrammable set pieces that amplify free social media reach. Immersive formats convert passive browsing into interactive discovery, encouraging impulse purchases across categories. They also feed loyalty apps with rich behavioural data that sharpens future targeting. As landlords seek foot-traffic magnets, retailers parlay these experience centers into favorable lease terms that reduce occupancy costs.

Omnichannel Loyalty Ecosystems

Modern loyalty programs evolve from discount engines into data-rich platforms that underpin retail media networks. Sephora’s Beauty Insider surpassed 38 million members by mid-2025 and now delivers 25% of total sales through personalized offers. Ulta Beauty’s Ultamate Rewards integrates credit cards, virtual consultations, and early-access drops, driving 95% of the revenue and tripling customer lifetime value for top-tier members. These ecosystems generate ad inventory for brands eager to pay premium CPMs for highly segmented audiences. Transactional data also guides dynamic pricing and localized merchandising, shrinking stockouts and markdowns. As privacy regulations tighten, chains owning opt-in data gain durable advantages over social-media marketing. The resulting switching costs lock shoppers into closed loops that competitors find hard to disrupt.

AI-Enabled Hyper-Personalization & Virtual Try-On

Retailers deploy computer vision and machine-learning models to recommend shades, map skin conditions, and simulate scents. Ulta’s GLAMlab Hair Try-On, built with Nvidia, raised conversion by 35% while cutting return rates by 40% in 2025 pilot stores. Sephora’s Skin IQ scanner now underpins 15-minute face readings that double skincare upsell versus manual consultations. AI engines parse tens of millions of anonymized profiles to forecast item-level demand, trimming overstock by 25% chain-wide. Virtual try-on bridges the sensory gap of online shopping, pushing high-consideration categories such as foundation and fragrance into the digital basket. Consistent experience across app, kiosk, and website delivers seamless journeys that build trust. As algorithms learn from continuous feedback loops, recommendation accuracy improves, sustaining engagement without heavy discounting.

Cross-Border E-Commerce & Same-Day Delivery

Beauty shoppers increasingly import niche SKUs via cross-border platforms, though rising tariffs and de minimis changes complicate landed costs. U.S. duties reached as high as 54% on selected skincare lines in 2025, compelling brands to consider first-sale rule structures for mitigation . Same-day delivery emerged as a hygiene factor in dense cities: DoorDash and Instacart powered two-hour windows for 2,500 Ulta and Watsons outlets, boosting average order value by 28%. Fulfillment requires micro-DC networks and algorithmic demand positioning, but increased ticket sizes offset logistics fees. Cross-border sellers also deploy bonded warehouses to expedite customs clearance, trimming lead times from 10 days to 48 hours. Retailers monetize speed as a premium service, charging USD 5–15 per drop without eroding margin. These capabilities blur geographic boundaries and accelerate category rotation for trend-hungry consumers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inflation-driven trading-down to mass & private label | −0.4% | Global; acute in price-sensitive markets | Short term (≤2 years) |

| Gray-market leakage undermining selective distribution | −0.3% | Europe & APAC core; emerging in Americas | Medium term (2-4 years) |

| Stricter sustainability regulations raising compliance cost | −0.2% | EU dominant; North America follow-on | Long term (≥4 years) |

| Online price transparency compressing gross margins | −0.3% | Global, strongest in developed economies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Inflation-Driven Trading-Down

Persistent cost-of-living pressures steer shoppers from prestige fragrances into value skincare and private-label bath goods. In 2025, private-label penetration at leading chains rose to 18% of category sales, capturing customers with 30-50% lower price points. Retailers launched tiered assortments that preserve volume but shave gross margin by roughly 150 basis points. Promotional stacking and buy-one-get-one events keep foot traffic stable yet risk brand dilution. Mass brands capitalize on the shift by touting dermatologist-backed claims that mimic prestige positioning at friendlier prices. Over time, trading down may ease as wages catch up, but the episode underscores revenue sensitivity to macro shocks. Chains hedge by flexing SKU depth and maintaining agile supply to pivot between tiers.

Stricter Sustainability Regulations

Europe’s Packaging and Packaging Waste Regulation mandates all cosmetic packaging be recyclable by 2030 and stipulates 30–35% recycled content in plastics[2]Bolla Sophie, “European Union Finalizes New Rules for Packaging and Packaging Waste Reduction,” USDA Foreign Agricultural Service, fas.usda.gov. . Retailers must redesign componentry, audit suppliers, and install traceability software, lifting cost-of-goods by an estimated 1–2% in the near term. Decorative double walls and false bottoms face outright bans, challenging luxury aesthetics that signal premium value. Health Canada’s allergen disclosure rules add yet more label real estate, pushing multilingual packs toward QR-code solutions. While scale players amortize investments across millions of units, small chains confront disproportionate compliance burdens that could trigger consolidation. Early movers, however, market eco-positive credentials to win sustainability-minded consumers and negotiate greener lease incentives with landlords.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Skin Care Anchors Revenue While Fragrance Accelerates

Skin care retained a 39.02% slice of the cosmetics and fragrance retail chain market share in 2025, underpinned by daily routine stickiness and science-driven launches that command premium pricing . The category’s resilience buffered chains during pandemic cycles and now fuels steady upgrade flows to serums and derm-actives. Innovation, such as RXRα-activating complexes, demonstrated 8.90% wrinkle reduction in clinical trials, justifying fresh price ladders that lift average selling prices. Fragrance, while smaller, is forecast to post an 7.95% CAGR, linking scent layering and limited-edition drops to collectability dynamics. Hair care’s loyal user base provides recurring revenue yet faces commoditization absent novel claims like microbiome-friendly formulas. Color cosmetics recover gradually as office attendance normalizes, though screen-time skincare blends blur traditional category lines. Deodorants stay flat but are strategic for cross-selling kits that raise basket size.

Second-order effects reinforce category interplay across channels. AI skin analyzers push regimen bundles that increase units per transaction while lowering return risk. Fragrance discovery kits in subscription boxes introduce niche houses, translating curiosity into full-size store purchases. Premium sample-size walls meet travel demand and encourage trial at lower entry costs. Category adjacencies spur store-within-store storytelling: for example, shower gels scented to match flagship perfumes. As virtual avatars proliferate, digital-first launches arrive online and then backfill into physical shelves, reversing historical cadence. Ultimately, product-type breadth enables chains to balance cyclical weaknesses and maintain customer engagement throughout the year.

By Category: Mass Commands Volume, Premium Drives Margin

The mass tier held 60.84% of the cosmetics and fragrance retail chain market size in 2025, proving its resilience during economic uncertainty. Large-scale sourcing, value pricing, and FMCG velocity keep shelves turning, but margins stay razor thin. Retailers counterbalance with exclusive launches that inject novelty without alienating budget shoppers. Premium beauty, on the other hand, enjoys a 10.05% forecast CAGR through 2031 as emerging-market affluence and luxury aspirations converge. Clean formulations, clinical claims, and eco-smart packaging validate price premiums that stretch gross profit north of 65%. Chains curate premium corners with enhanced lighting, concierge service, and AR mirrors to elevate perceived worth.

Dual-tier merchandising demands astute floor planning, so entry-level SKUs do not cannibalize prestige offerings. Data-driven clustering tailors product depth to neighborhood demographic mix, avoiding inventory drag. Retailers also create private-label bridges that marry premium sensorial aesthetics with mass price, blurring lines and cushioning trade-down effects. Digital channels add endless-aisle capacity to carry ultra-niche prestige lines without floor-space burden as premium shoppers expect white-glove fulfillment, same-day delivery, and luxe packaging to become non-negotiable. The divergent trajectories of mass and premium ensure continued portfolio diversification that hedges macro volatility.

By End User: Women Remain Core, Men Accelerate Adoption

Women represented 59.72% of spending in 2025, reflecting established beauty rituals and higher basket sizes. Retailers maintain dedicated storytelling zones for skincare routines, shade-matching stations, and fragrance wardrobing that cater to nuanced female needs. Yet, men’s grooming charts a 7.55% CAGR as stigma fades and social media normalizes skincare regimens. Dedicated men’s bays showcase minimalist packaging, straightforward claims, and quick-fix solutions appealing to time-pressed users. Unisex ranges gain traction, mirroring Gen Z’s fluid approach to beauty and easing assort-ment complexity for chains.

Growth in male segments sparks partnerships with barbershops and gym chains that embed retail corners within service venues, extending reach beyond traditional malls. Influencer marketing leans on male athletes and K-pop idols to promote sunscreen habits and fragrance layering. AI diagnostics adapt to thicker skin texture and facial-hair variables, personalizing recommendations for men who prefer data-backed guidance. Chains leverage men’s entry-level interest to upsell fragrance and hairstyling, increasing lifetime value. As female segments mature, men’s and gender-neutral portfolios offer blue-ocean potential without cannibalizing core female traffic.

Geography Analysis

Asia-Pacific delivered 35.78% of global revenue in 2025, with digital ecosystems like Douyin enabling domestic brands to scale rapidly to billion-yuan benchmarks. High mobile penetration synchronizes live-streamed tutorials with one-click conversion, shrinking the path to purchase. Korea’s beauty tourism lures nearly 800,000 medical visitors annually, who then stock up on skincare souvenirs that ripple through retail sales. China’s tier-2 and tier-3 cities power incremental store openings as coastal markets saturate, underpinning steady expansion. Meanwhile, Japan and Australia provide mature-market stability, buttressing regional EBIT margins. Local players such as Olive Young exemplify O+O excellence, compelling global peers to localize assortments and app UX.

Middle East & Africa posts the fastest 9.48% CAGR to 2031, fueled by youthful demographics and a cultural affinity for fragrance gifting traditions. GCC e-commerce adoption accelerates click-and-collect demand as extreme temperatures drive indoor mall traffic year-round. Duty-free hubs at Dubai and Doha airports amplify prestige perfume exposure, becoming trial funnels into domestic retail. North Africa’s expanding middle class seeks affordable luxuries, prompting value-tier launches from Western brands. Sustainable packaging resonates due to rising environmental awareness, but must coexist with ornate aesthetics favoured in gift culture. Political stability gains in markets like Saudi Arabia unlock real estate flagship-format at flagships, accelerating store penetration.

Europe and North America hold mature but innovation-driven positions, where experiential upgrades and sustainability mandates define competitive edge. EU PPWR standards impose recycled-content thresholds, compelling packaging redesigns that add differentiation for early adopters. In North America, the exit of Ulta shop-in-shops at Target in 2026 opens shelf space for private brands, repricing concessions across the channel. Prestige disciples gravitate to department-store revamps such as Saks-Neiman consolidation moves that promise broader assortments and cross-border shipping. Across both continents, data privacy frameworks pressure performance marketing budgets, reinforcing the value of retailer-owned media channels.

Competitive Landscape

The cosmetics and fragrance retail market is highly fragmented, offering ample room for regional specialists, digital-first brands, and niche players to gain meaningful traction. Market leadership is split among several key players, each with strength in specific regions and channels. Sephora, for example, holds a dominant position in North America and Europe, while A.S. Watson Group thrives across Asia through its various retail banners. This fragmentation allows newer entrants to compete effectively by focusing on unique customer experiences and differentiated brand identities. The competition is less about pricing and more about omnichannel strength, loyalty ecosystems, and immersive retail environments. Notable moves, such as Ulta Beauty's partnership with Space NK and the acquisition of Walgreens Boots Alliance by Sycamore Partners, underscore the importance of strategic expansion and consolidation.

Technology continues to shape the competitive landscape by enabling better personalization, faster delivery, and enhanced digital experiences. Retailers are investing heavily in AI tools, virtual try-on solutions, and real-time logistics infrastructure to improve conversion rates and customer loyalty. These tech-driven capabilities give larger players sustainable advantages, allowing them to deliver more consistent and tailored experiences. Meanwhile, white-space opportunities are emerging in areas like cross-border retail media, which leverages customer data for monetization, and sustainable retail formats focused on refill and reuse systems. These models address growing consumer demand for eco-conscious solutions while providing ongoing revenue potential. Expansion into underpenetrated markets also presents growth avenues for companies with established operational and brand expertise.

Emerging disruptors, including experiential Chinese retailers and social commerce-driven digital platforms, are reshaping how younger consumers engage with beauty brands. These challengers often focus on influencer partnerships and owned-brand portfolios to build loyalty and extend margins. Strategic trends across the industry now center on vertical integration via private label development and horizontal expansion through retail partnerships. Global retailers are also diversifying geographically, entering high-growth regions while reinforcing their positions in mature markets. The shift toward platform-based models is evident, as retailers move beyond selling products to monetizing customer relationships through data, services, and partnerships. This evolution favors players with scale advantages in analytics, supply chains, and brand collaborations, reinforcing long-term competitive moats.

Cosmetic And Fragrance Retail Chain Industry Leaders

Sephora (LVMH)

A.S. Watson Group (Watsons, Superdrug, Kruidvat, etc.)

Ulta Beauty

Douglas

Boots UK

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Saks and Neiman Marcus announced a potential USD 2.65 billion merger to create "Saks Global," combining luxury retail operations and potentially impacting beauty retail through enhanced buying power and operational synergies.

- August 2025: Walgreens Boots Alliance agreed to be acquired by Sycamore Partners for approximately USD 10 billion, marking a significant private equity investment in the pharmacy-beauty retail sector. The deal reflects investor confidence in the omnichannel pharmacy-beauty model despite recent operational challenges.

- August 2025: Target and Ulta Beauty announced the ending of their shop-in-shop partnership effective August 2026, with Target citing strategic focus on owned-brand beauty development. The partnership generated significant revenue for both parties but faced operational complexity and brand positioning challenges that ultimately led to its termination.

- July 2025: Ulta Beauty acquired Space NK, the UK-based premium beauty retailer, for undisclosed terms to accelerate international expansion and gain access to the European luxury beauty market. The acquisition provides Ulta with established retail infrastructure and brand relationships in the UK market while enabling Space NK to leverage Ulta's omnichannel capabilities and loyalty program expertise.

Global Cosmetic And Fragrance Retail Chain Market Report Scope

A cosmetic and fragrance retail chain refers to a network of stores selling cosmetics, fragrances, beauty supplies, and related items. These chains offer various brand-name products catering to personal grooming and beauty needs. The cosmetic and fragrance retail chain market is segmented by product type, category, end user, and geography. By product type, the market is segmented into consumer hair care, skin care, make-up products, deodorants, and fragrances, category; the market is segmented into mass and premium, end user, and the market is segmented into men, women, and unisex. The market is geographically segmented into Asia-Pacific, North America, Europe, South America, Middle East & Africa, and the Rest of the World. The reports offer the market sizing and forecasts for the cosmetic and fragrance retail chain market in value (USD) for all the above segments.

| Hair Care |

| Skin Care |

| Make-Up Products |

| Deodorants |

| Fragrances |

| Mass |

| Premium |

| Men |

| Women |

| Unisex |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product Type | Hair Care | |

| Skin Care | ||

| Make-Up Products | ||

| Deodorants | ||

| Fragrances | ||

| By Category | Mass | |

| Premium | ||

| By End User | Men | |

| Women | ||

| Unisex | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the value of the cosmetics and fragrance retail chain market in 2026?

The cosmetics and fragrance retail chain market size is valued at USD 196.03 billion in 2026.

How fast will sales grow through 2031?

Revenue is forecast to expand at a 3.02% CAGR, reaching USD 227.64 billion by 2031.

Which region contributes the most revenue?

Asia-Pacific leads, accounting for 35.78% of global revenue in 2025.

Which product category is expanding the quickest?

Fragrances show the fastest trajectory, advancing at an 7.95% CAGR through 2031.

What emerging technology is lifting conversion rates?

AI-powered virtual try-on and hyper-personalization tools are delivering conversion gains of up to 35%.

Page last updated on: