Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.43 Billion |

| Market Size (2026) | USD 1.47 Billion |

| Market Size (2031) | USD 1.71 Billion |

| Growth Rate (2026 - 2031) | 3.05% CAGR |

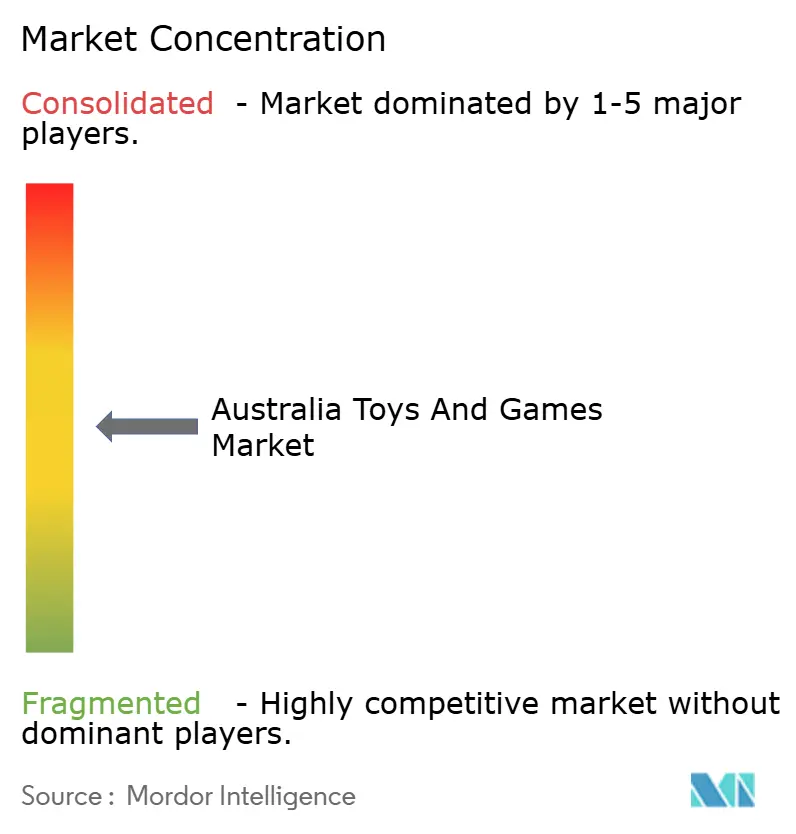

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Toys And Games Market Analysis by Mordor Intelligence

The Australia toys and games market size is expected to grow from USD 1.43 billion in 2025 to USD 1.47 billion in 2026 and is forecast to reach USD 1.71 billion by 2031 at 3.05% CAGR over 2026-2031. Measured household confidence supports discretionary spending on toys even as living-cost pressures remain evident, and educational items together with adult collectibles act as buffers during cyclical downturns. Government STEM funding, early-childhood policy focus, and enhanced e-commerce logistics further amplify demand, while eco-design mandates are reshaping packaging and materials choices. Competitive intensity remains elevated because global leaders adapt portfolios to local licensing opportunities, and online marketplaces extend nationwide reach despite rising compliance scrutiny. Overall, the Australia toys market benefits from a confluence of demographic growth in family households, omnichannel retail maturation, and policy-aligned learning priorities that sustain volume and value advancement.

Key Report Takeaways

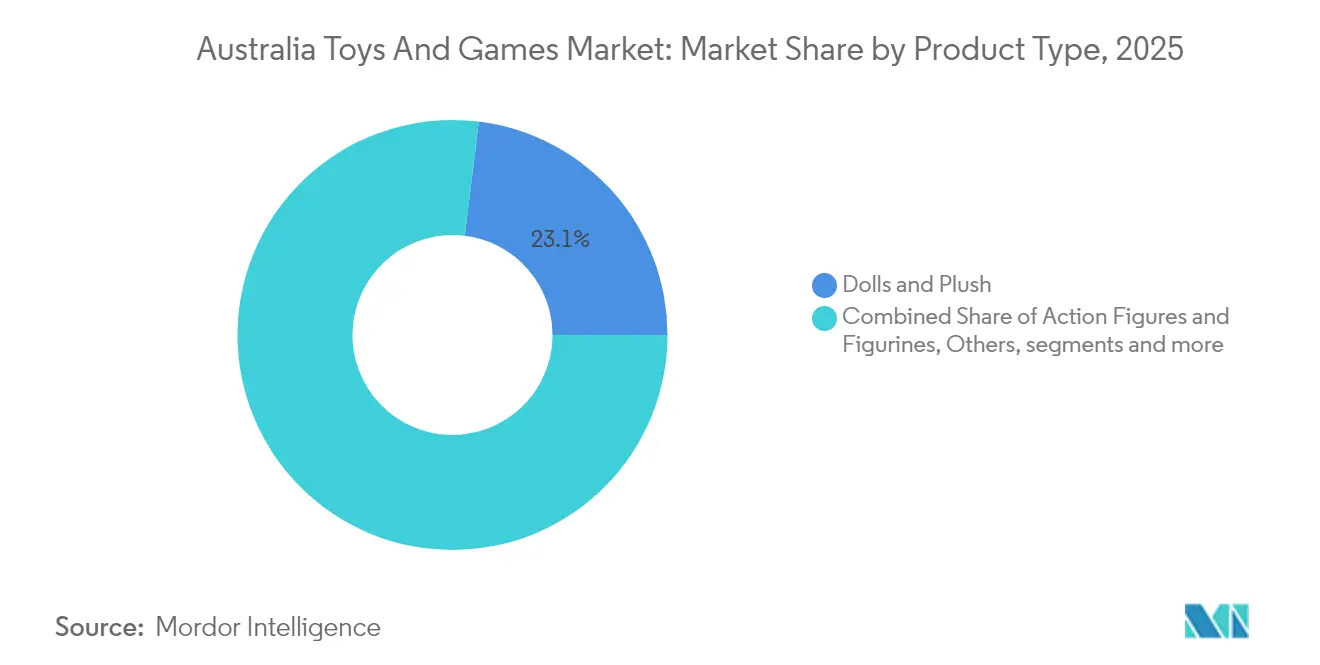

- By product type, dolls and plush led with 23.05% of Australia toys market share in 2025, whereas educational and STEM toys are on track for a 5.12% CAGR to 2031.

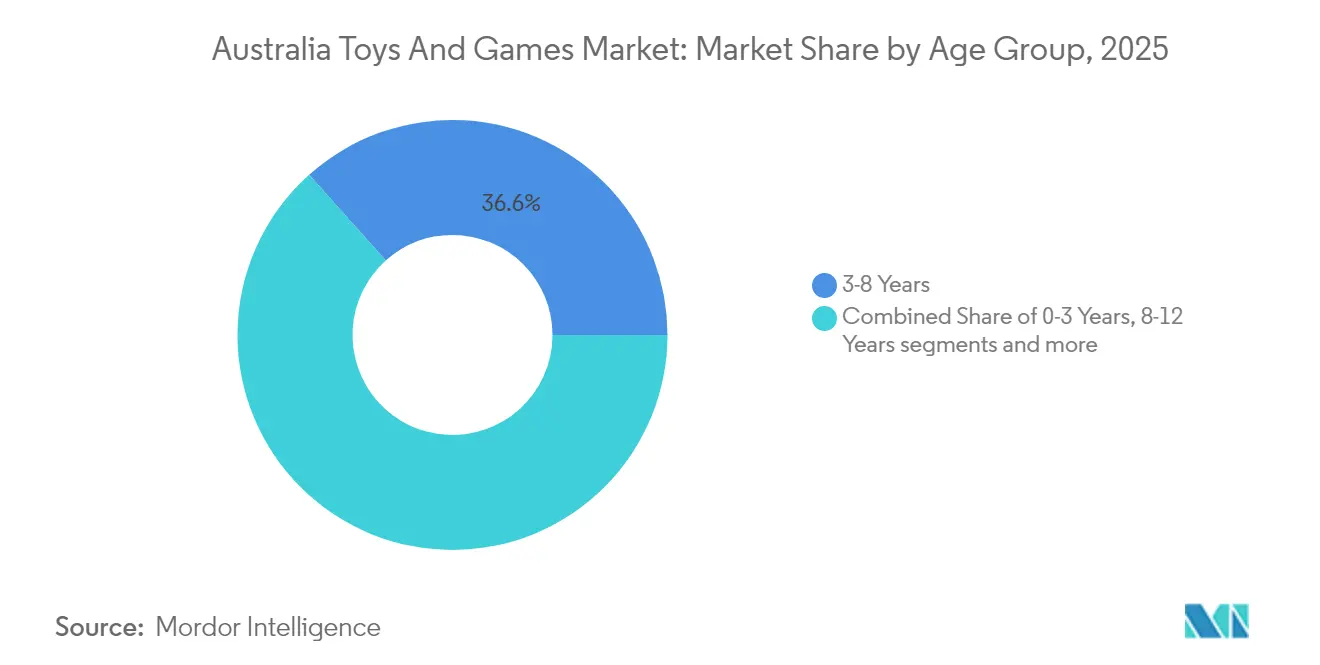

- By age group, 3-8 years accounted for 36.62% share of the Australia toys market size in 2025, while 8-12 Years is projected to expand at a 5.78% CAGR through 2031.

- By distribution channel, online retail commanded 35.13% of the Australia toys market size in 2025 and is advancing at a 4.72% CAGR to 2031.

- By state, New South Wales held a 29.85% revenue share in 2025; Queensland is forecast to grow at a 5.95% CAGR over the same period.

- The LEGO Group, Mattel Inc., Hasbro Inc., Moose Toys, and Spin Master Corp. collectively held a dominant position in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Toys And Games Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable income and gifting culture | +0.8% | National, with higher impact in NSW and Victoria | Medium term (2-4 years) |

| Expansion of licensed merchandise franchises | +0.6% | National, with concentration in urban centers | Long term (≥ 4 years) |

| Growth in e-commerce and omnichannel retail | +0.7% | National, with rural areas showing highest growth | Short term (≤ 2 years) |

| Increasing demand for educational and STEM toys | +0.5% | National, with government program alignment | Medium term (2-4 years) |

| Government funding for early-childhood STEM programs | +0.3% | National, with targeted regional implementation | Long term (≥ 4 years) |

| Adult collectible and hobby community expansion | +0.4% | Urban centers, particularly Sydney and Melbourne | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Income and Gifting Culture

Household spending resilience supports the Australia toys market as discretionary budgets expand even when essentials outpace wage growth. Elevated gifting traditions across multicultural calendars add several mini seasons beyond Christmas, sustaining revenue consistency throughout the year. Younger adults aged 25-29 maintain toy purchases despite trimming other discretionary categories, indicating enduring emotional attachment to childhood experiences. Premium products flourish during peak events such as Chinese New Year, Diwali, and Eid, encouraging manufacturers to broaden culturally relevant assortments. As retailers refine loyalty programs, gifting remains a strategic anchor for average-order-value growth across physical and digital channels.

Expansion of Licensed Merchandise Franchises

Intellectual-property franchises deepen engagement in the Australia toys market by coupling streaming content with merchandise drops, creating recurring sales beyond initial launches. Bluey’s global reach across 50 countries demonstrates local IP scalability, and Moose Toys leverages this momentum through worldwide production agreements. Mattel’s 2025 acquisition of DC Comics rights re-positions the firm for category leadership while limiting competitors’ access to high-equity characters, raising entry barriers. Strong national IP protection laws reassure licensors and spur further collaborations, especially as cross-platform storytelling aligns with parents’ preference for recognizable educational narratives. Licensing also enables quick merchandise refreshes that coincide with new series seasons, keeping shelf assortments dynamic and driving impulse purchases.

Growth in E-commerce and Omnichannel Retail

Online expenditure of USD 45 billion, spotlights digital momentum nationally. In the Australia toys market, marketplace participation by 93% of consumers places Amazon and eBay at the heart of discovery journeys, while rising players such as Temu attract value-driven shoppers. Rural households register the fastest digital adoption due to limited physical store density, reinforcing nationwide fulfillment networks. Mobile transactions exceeding 30% of digital orders accelerate bite-sized purchasing behavior, benefiting low-ticket toy categories. However, safety compliance failures on unvetted platforms prompt regulatory crackdowns that may reroute demand toward compliant sellers.

Increasing Demand for Educational and STEM Toys

Federal STEM policy under Australia’s National Science Statement 2024 reclassifies many learning toys as skill-building assets rather than leisure items [1]Department of Industry, Science and Resources, “National Science Statement 2024,” industry.gov.au.. Source: Department of Industry, Science and Resources, “National Science Statement 2024,” industry.gov.au. Parallel early-childhood frameworks for ages 0-5 embed developmental benchmarks into daycare procurement, lifting institutional volume. Parents in growth corridors such as Camden and Wollondilly view construction sets, coding kits, and robotics as investments in future employability, bolstering unit value. These products maintain positive growth during downturns, given their perceived academic benefit. Suppliers increasingly pair physical kits with app-based curricula, reinforcing sustained engagement and subscription upsell opportunities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from digital entertainment and screen time | -0.9% | National, with higher impact in urban areas | Short term (≤ 2 years) |

| Rising safety certification and compliance costs | -0.6% | National, affecting all market participants | Medium term (2-4 years) |

| Price sensitivity amid economic uncertainties | -0.4% | National, with greater impact on lower-income households | Short term (≤ 2 years) |

| Sustainability scrutiny and packaging-waste regulations | -0.3% | National, with state-specific implementation variations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition from Digital Entertainment and Screen Time

Children aged 12-13 spend more than 3 weekday hours on screens, climbing past 4 hours on weekends, siphoning attention from traditional toys. Free-to-play mobile titles channel discretionary dollars into micro-transactions rather than one-off purchases, while console ecosystems from Nintendo and Sony deepen loyalty through subscription models. The restraint is sharpest among tweens and teens but cascades into younger cohorts as tablets become learning aids. Hybrid experiences that fuse augmented reality with physical pieces partially offset this shift, suggesting opportunity spaces for adaptable brands. Retailers respond by curating interactive in-store demos that rekindle tactile engagement among digitally native shoppers.

Rising Safety Certification and Compliance Costs

Enhanced enforcement by the Australian Competition and Consumer Commission triggers mounting fines for non-compliance, with penalties of USD 49,500 levied for button-battery testing failures [2]Australian Competition and Consumer Commission, “Button Battery Enforcement Outcomes,” accc.gov.au. . From March 2025, a revised infant-toy standard mandates additional choking-hazard assessment. Meanwhile, the Australian Packaging Covenant Organization introduces eco-modulation fees from FY27, effectively taxing non-recyclable materials. Smaller importers struggle to absorb testing expenses and sustainable redesign investment, ceding shelf space to multinationals with global quality frameworks. Longer lead times for safety validation also compress launch calendars, pushing brands toward evergreen ranges rather than rapid-fire novelties.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Educational Toys Command Premium Momentum

Educational and STEM Toys represent the fastest-expanding category, advancing at a 5.12% CAGR to 2031 and steadily increasing their contribution to the Australia toys market. Unit demand rises as parents perceive coding robots, science kits, and math games as tools that improve school performance, aligning with national curriculum updates. Simultaneously, regulatory attention to STEM proficiency elevates these items from nice-to-have gifts into planned household purchases, supporting higher price points. Dolls and Plush maintain a 23.05% revenue lead in 2025 by capturing emotional attachment and inclusive storylines, while Construction Sets enjoy loyal adult collectors who extend the lifespan of core franchises. Games and Puzzles thrive by bridging cross-generational social play, harnessing stay-at-home habits that persisted after the pandemic period.

Outdoor and Sports Toys experience muted growth because urban households lack expansive play areas, yet demand endures among health-minded parents integrating physical activity into daily routines. Vehicles and Remote-Control items remain relevant by embedding Bluetooth or Wi-Fi controls, offering a bridge between tactile manipulation and smartphone familiarity. Video-Game Hardware sits at the convergence of entertainment and toy retail, with handheld consoles sold alongside board games at omnichannel outlets. The residual “Others” classification gathers sustainable bamboo skittles, sensory autism aids, and AI-driven companions that foreshadow new niches within the Australia toys market.

By Age Group: Upper Childhood Segment Accelerates

The 3-8 Years bracket delivered 36.62% of the 2025 value, reinforcing its status as the core purchasing demographic; however, the 8-12 Years segment is on course for a 5.78% CAGR that outpaces every other band. Parents target higher-order cognitive skill kits and franchise collectibles as children transition to more complex interests, lifting average selling prices. The 0-3 Years cohort benefits from the projected 11% uplift in the under-15 population by 2041, ensuring a stable base for developmental toys in metro and peri-urban districts. Teens gravitate toward hobby-grade models, tabletop games, and limited-edition figurines that satisfy expressive identity needs even as screen alternatives compete aggressively.

Adults and hobby collectors now account for a meaningful slice of the Australia toys market, mirroring global evidence that 19% of sales originate from over-18 customers. Vintage Barbie, Star Wars memorabilia, and LEGO Architecture sets resonate with this clientele, unlocking margin-rich SKUs. Specialty retailers schedule after-hours events to showcase high-value releases, fostering community engagement that further shields this segment from digital cannibalization.

By Distribution Channel: Digital Dominance Continues

Online Retail controlled 35.13% of the Australia toys market size in 2025 and is expanding at a 4.72% CAGR to 2031, driven by fast delivery promises and aggressive promotional cycles. Marketplace algorithms expose micro-brands to nationwide audiences, yet growing enforcement around product safety will likely concentrate traffic among verified storefronts. Specialty Toy Stores preserve relevance through experiential merchandising and curated ranges that cater to collectors and STEM-focused parents. Department and Discount Stores commit heavily to click-and-collect.

Supermarkets address convenience spending for low-ticket impulse buys, particularly pocket-money plush lines and blind-box collectibles situated near checkouts. Direct-to-consumer subscriptions enter the scene, bundling monthly STEM projects with progress-tracking apps that reinforce recurrence revenue. While Temu’s rapid Australian ascent spotlights value positioning, its 100% compliance failure rate in independent testing may channel consumers back toward established e-commerce leaders that guarantee regulated sourcing.

Geography Analysis

New South Wales generated 29.85% of national toy revenue in 2025 as Greater Sydney’s dense family population and mature omnichannel retail network support high product turnover. Continued suburban infill and a projected rise to 9.9 million residents by 2041 underpin long-run volume growth, although elevated living costs are steering younger renters toward value lines. Cultural diversity broadens the calendar of gifting events, allowing retailers to smooth quarterly sales without deep discounting.

Queensland is the fastest-growing state, advancing at a 5.95% CAGR to 2031 as interstate migration brings young families into Brisbane, Gold Coast, and Sunshine Coast corridors. Additional demand flows from tourism spending, which peaks during school holidays and amplifies seasonal volume for outdoor and licensed ranges. The state’s focus on STEM education aligns with institutional purchases of science kits and coding sets for community programs, reinforcing premium sub-segment momentum.

Victoria, Western Australia, South Australia, Tasmania, ACT, and Northern Territory provide the remaining share and display mixed growth profiles. Victoria leverages Melbourne’s large tertiary sector and multicultural depth to support premium and language-learning lines, while Western Australia’s mining wealth encourages higher average selling prices. Smaller states depend on targeted assortments and rising e-commerce penetration to overcome limited store footprints, a trend intensified by national logistics upgrades that shorten rural delivery windows.

Regulatory Landscape

Australia's toy and game safety framework is enforced primarily through the Australian Competition and Consumer Commission (ACCC) under the Australian Consumer Law, with mandatory safety standards covering categories such as toys for children up to and including 36 months, aquatic toys, and toys containing lead and other elements. A notable update is the commencement of the Consumer Goods (Aquatic Toys) Safety Standard 2026 on 26 June 2026, with a transition window that permits compliance with either the earlier or updated standard until 25 June 2028.

Mandatory requirements commonly reference voluntary technical benchmarks such as AS/NZS ISO 8124.1, and the ACCC has also been running reviews of multiple children's product safety standards (including toy-related standards) during 2025 to assess effectiveness and potential alignment with international approaches. Suppliers carry the compliance obligation throughout the supply process, and enforcement mechanisms center on surveillance, recalls, and penalties rather than a broad pre-market approval system for general toy imports.

Value Chain Analysis

Australia's toys and games value chain is heavily import-led, with global brand owners and local distributors sourcing large volumes of finished products from manufacturing hubs such as China and Vietnam, then routing shipments through national freight and warehousing networks before reaching omnichannel retailers. Scale logistics partnerships shape downstream availability, exemplified by DHL Supply Chain Australia's long-term warehousing agreement with Mattel and the relocation of operations to a 31,000 sq m facility in Truganina, Victoria, which supports faster replenishment to major metro corridors and national e-commerce fulfillment.

Compliance and testing act as gating steps in the chain, particularly for products intended for children under 36 months and for higher-risk categories such as aquatic toys, magnets, and products with regulated substances. The ACCC's ongoing review of mandatory standards, alongside the June 2026 update to the aquatic toy safety standard and its multi-year transition period, increases the operational importance of documentation, lab testing, and traceability across importers, marketplaces, and brick-and-mortar retailers, with larger suppliers better able to absorb certification lead times and redesign cycles.

Competitive Landscape

Five multinational brands, The LEGO Group, Mattel Inc., Hasbro Inc., Moose Toys, and Spin Master Corp., hold a commanding position through deep IP catalogs, advanced compliance systems, and efficient omnichannel distribution. Mattel’s 2025 recovery of DC Comics rights bolsters its local action-figure portfolio, while LEGO sustains cross-generational appeal with architecture and adult collector sets. Spin Master’s 18.8% 2024 revenue surge reflects an innovation pipeline that balances preschool, construction, and digital-hybrid lines.

Market disruption followed Toys ‘R’ Us Australia’s mid-2025 collapse, releasing almost USD 30 million in sales that competitors quickly absorbed. Rising regulatory costs also shift share toward large incumbents because fines such as the ACCC’s recent USD 49,500 button-battery penalties weigh more heavily on small importers. At the same time, platform retailers face closer oversight, which is likely to concentrate compliant sellers and increase bargaining power for established brands.

Sustainability rules offer another competitive lever. Early movers redesign packaging to satisfy APCO’s eco-modulation fees taking effect from FY27, positioning themselves for potential cost advantages and stronger consumer trust. Strategic priorities across the leader group include licensing acquisitions, connected-play technology, and direct-to-consumer launches that capitalize on growing adult collector demand while preserving scale efficiencies in core children’s segments.

Australia Toys And Games Industry Leaders

The LEGO Group

Mattel Inc.

Hasbro Inc.

Moose Toys

Spin Master Corp.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Specialty retail consolidation and network expansion are creating new routes to market for premium and collector-led assortments. In May 2026, Kennedy Consolidated acquired the 25-store Australian LEGO Certified Stores portfolio from Alquemie Group, which reflects ongoing investment in established toy retail formats and supports store refreshes, enhanced merchandising, and cross-channel programs that lift conversion for high-ticket adult and family buyers.

Licensing-led releases and channel partnerships are also widening assortment breadth and improving regional access. The Australian Toy Association's sell-out Australian Toy, Hobby and Licensing Fair in 2026 reinforced the role of licensed properties in retail planning, while partnerships such as the April 2026 Gyroor Australia and Toyworld national supply arrangement through the Associated Retailers Limited (ARL) network point to more technology-integrated toys reaching suburban and regional consumers. At the same time, tighter safety oversight, including the new aquatic toy mandatory standard commencing 26 June 2026 and broader ACCC reviews of children's standards, creates room for compliant sellers to differentiate through verified testing and safer product design, particularly on online channels where scrutiny of unvetted listings has intensified.

Recent Industry Developments

- May 2026: Kennedy Consolidated acquired Alquemie Group's Australian LEGO Certified Stores portfolio, spanning 25 stores. The transaction reshaped control of a major premium specialty channel and provides a platform for tighter execution across store operations, merchandising, and omnichannel initiatives around a single global brand.

- May 2026: Moose Toys expanded its master toy partnership with Netflix, adding new toy lines tied to kids and family entertainment properties. The move deepened Moose Toys' licensing pipeline and supports more frequent franchise-linked product drops that can lift visibility across Australian retail and e-commerce shelves.

- October 2024: Kuehne+Nagel announced it would operate a new distribution center for the LEGO Group in Australia. The added logistics capability strengthens replenishment and fulfillment capacity for both retail partners and direct channels, supporting faster delivery and better inventory availability across Australia and New Zealand.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers toys and games sold in Australia, counted as the value of products purchased by consumers through online and offline channels across the country.

Scope exclusions: We exclude second-hand resale between consumers and non-toy categories that are sometimes bundled into recreational goods totals.

Segmentation Overview

- By Product Type

- Action Figures and Figurines

- Dolls and Plush

- Construction and Building Sets

- Games and Puzzles

- Outdoor and Sports Toys

- Vehicles and Remote Control

- Educational and STEM Toys

- Video-Game Hardware and Software

- Others

- By Age Group

- 0-3 Years

- 3-8 Years

- 8-12 Years

- 12-18 Years

- Adults and Hobby Collectors

- By Distribution Channel

- Specialty Toy Stores

- Online Retail

- Department and Discount Stores

- Supermarkets and Hypermarkets

- Others

- By Geography

- New South Wales

- Victoria

- Queensland

- Western Australia

- South Australia

- Tasmania

- Australian Capital Territory

- Northern Territory

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with public signals that describe category momentum and where sales are being captured. We use sources such as the Australian Bureau of Statistics retail trade releases (including the toy and game retailing classification within broader recreational goods), Australian Government trade statistics portals for imports and exports, and tariff code guidance published by the Australian Border Force.

To make the model usable, company annual reports, retailer updates, and investor decks are used to confirm pricing direction, promo intensity, and channel mix shifts. Peer reviewed consumer and child development journals are also checked to understand changes in play patterns that can shift product mix over time. For filling gaps on company revenue splits, shipment indicators, and patent activity, we also refer to a few paid databases focused on company financials and intelligence, import and export shipments, and patent filings. The sources listed here are illustrative, and many other public releases and documents are reviewed to collect, cross-check, and clarify data points.

Primary Interviews and Surveys

Primary work was used to convert the desk inputs into assumptions that match how the category is actually sold in Australia, especially where public data is grouped into broader retail buckets. We spoke with a mix of brand and distributor contacts, retail category managers, and logistics or sourcing professionals across Australia to confirm demand seasonality, promotional depth, and the share sold online versus in-store.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 13% | |

| Mid tier: 49% | Functional/Unit leaders: 30% | |

| Smaller Players: 17% | Managers: 57% |

Market-Sizing & Forecasting

The core market size is built using top-down and bottom-up logic. The top-down side is anchored on Australia-specific retail turnover signals and trade-based supply indicators, which help reconstruct category demand. Once the country demand pool is set, it is split into toys and games using product mix shares and channel shares that were validated through interviews and public retail commentary.

To keep the numbers aligned to buying behavior, we track inputs such as toy and game import volumes by relevant product codes, average selling price movements during peak periods (especially year-end), online penetration of specialty and mass retail, and changes in household spending pressure that can shift consumers toward lower ticket items. We also include practical market fingerprints like seasonality around major gifting windows and the impact of licensing cycles, which tends to change the mix even when total units stay similar. Selective bottom-up checks are then run using sampled brand and distributor revenue splits, retailer category sizing discussions, and ASP-to-unit approximations for a few high-visibility subcategories. Where gaps remain, we apply conservative distribution margins and coverage factors, and re-test them with primary inputs.

For forecasting, we use scenario analysis supported by simple regression-style relationships between category spend and a few macro drivers, then adjust the curve using expert views on pricing, promotion intensity, and channel shifts. When signals disagree, the assumption is pushed back to respondents for a second pass before the final forecast line is set.

Data Validation & Update Cycle

Outputs are checked in several steps so the final totals do not depend on one dataset or one assumption. We compare the modeled market value against independent signals like retail turnover direction, import cost trends, and known peak-season lift patterns, then investigate outliers before sign-off.

If a variance is too large, the inputs are revisited, interview notes are re-checked, and follow-up calls are triggered with the relevant channel or product experts. Each report is refreshed annually, and interim updates are made when a material event changes demand, supply, or pricing assumptions. Before delivery, a final review pass is completed so the published view reflects the most recent data releases and validation checks.

Mordor Intelligence's Australia Toys and Games Market Estimate Compared With Other Published Estimates

Published market values for toys and games in Australia can differ across sources, even when they describe the same end market. The differences usually come from what is included in the basket, whether values are reported at retail or at earlier points in the value chain, and how pricing and seasonality are handled for the base year.

The biggest gap drivers in this category tend to be whether collectible hobbies and gaming hardware are counted as part of toys, how online marketplace sales are treated versus specialty retail, and whether import values are used directly without normalizing to consumer prices. Some publishers also apply aggressive price growth through the forecast window, while others keep prices flatter and let units do most of the work, which changes market value quickly. When retail classification data is used, it is also necessary to separate toy and game selling from broader recreational goods totals, and that separation is one reason the 2025 value is set at USD 1.43 B (2025) using a retail-spend lens and import-value normalization checks applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.43 B (2025) | |

| Industry Association A | USD 1.29 B (2025) | Often reflects narrower retail channels and may exclude online marketplace sales and some game categories, which can understate total consumer spend during peak seasons. |

| Trade Journal B | USD 1.58 B (2025) | May blend adjacent categories such as collectibles or select electronics-linked items, and may apply higher ASP uplift assumptions without consistent checks against retail turnover and trade signals. |

The comparison shows that the spread is mainly created by category boundaries and price handling, not by a single arithmetic difference. By keeping the scope focused on toys and games sold to consumers in Australia and by cross-checking retail and trade indicators, the final number stays traceable to clear inputs and can be repeated as new data comes in.

Key Questions Answered in the Report

What is the current size of the Australia toys market?

The Australia toys market size stands at USD 1.47 billion in 2026 and is expected to climb to USD 1.71 billion by 2031 at a 3.05% CAGR.

Which product segment is growing fastest?

Educational and STEM Toys are expanding at a 5.12% CAGR to 2031, driven by STEM policy support and parental demand for developmental play.

How important is e-commerce to toy sales in Australia?

Online Retail already represents 35.13% of the category revenue in 2025 and is forecast to grow at 4.72% CAGR, making it the pivotal channel for future expansion.

Which state offers the highest growth potential?

Queensland is projected to deliver a 5.95% CAGR by 2031 as lifestyle-driven migration fuels household formation and toy spending.

How are safety regulations affecting manufacturers?

Stringent ACCC enforcement and new infant-toy standards increase compliance costs, favoring large players with established testing infrastructure.

What opportunities exist in the adult collector space?

Collectors contribute an expanding premium segment, and limited-edition releases targeting over-18 buyers offer high margins with relatively low volume risk.

Page last updated on: