Cloud-based Contact Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

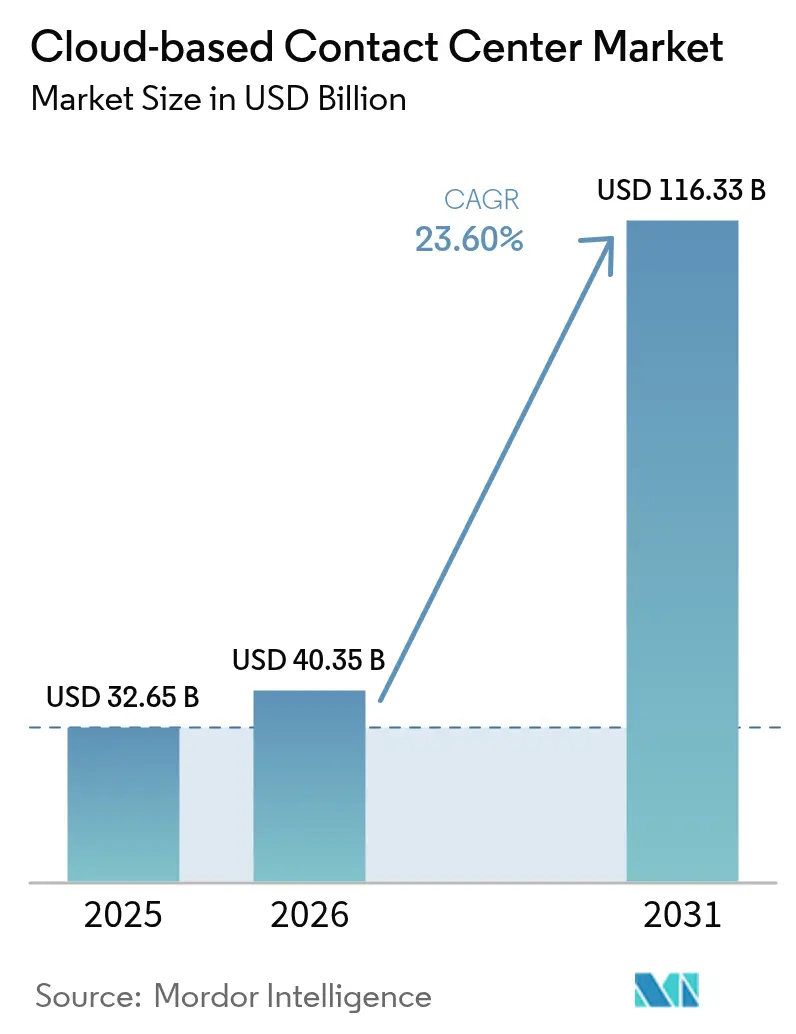

| Market Size (2026) | USD 40.35 Billion |

| Market Size (2031) | USD 116.33 Billion |

| Growth Rate (2026 - 2031) | 23.60% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud-based Contact Center Market Analysis by Mordor Intelligence

The cloud-based contact center market size is expected to grow from USD 32.65 billion in 2025 to USD 40.35 billion in 2026 and is forecast to reach USD 116.33 billion by 2031 at 23.6% CAGR over 2026-2031. Heightened demand stems from enterprises replacing static on-premise infrastructure with agile platforms that scale alongside omnichannel traffic, real-time analytics, and permanent remote workforces. Organizations now treat contact centers as revenue generators that surface actionable customer intelligence, leading providers to embed AI at each interaction layer. Public cloud elasticity accelerates adoption among large enterprises, while subscription pricing removes cost barriers for small and medium businesses. Competitive intensity is rising as hyperscalers bundle CCaaS with broader cloud estates, compressing prices yet expanding innovation velocity.

Key Report Takeaways

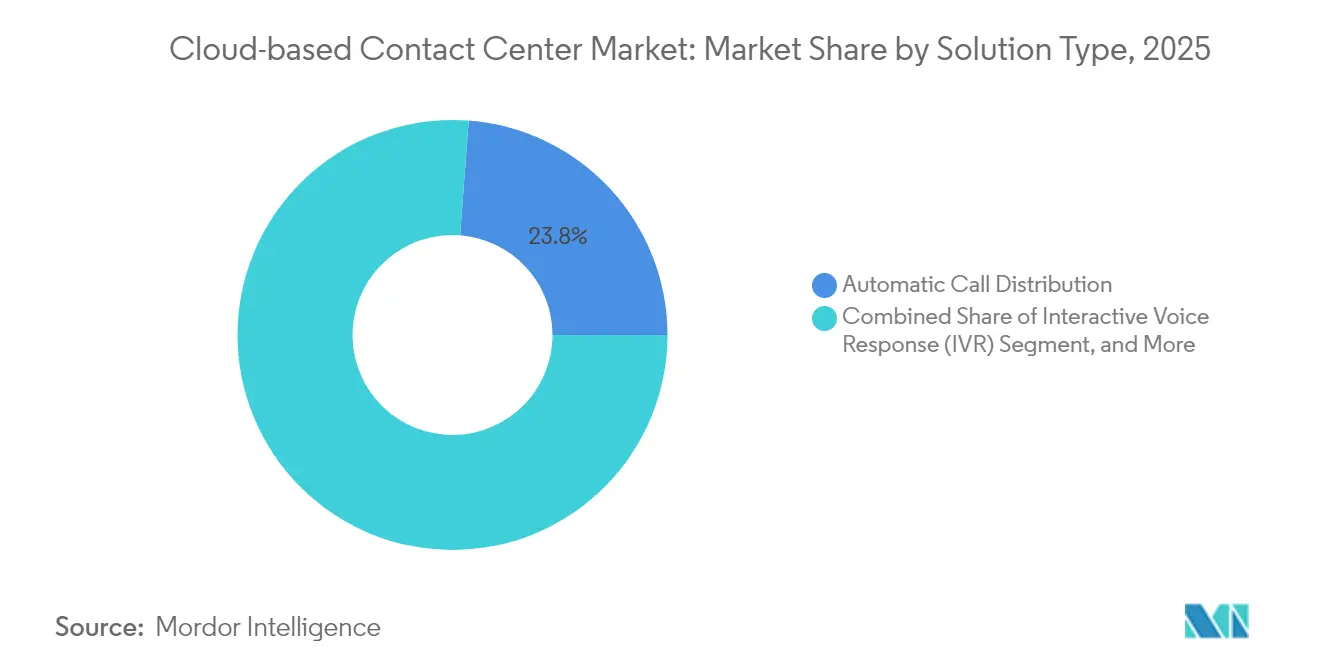

- By solution type, Automatic Call Distribution led with 23.80% of the cloud-based contact center market share in 2025, while Analytics and Reporting is projected to expand at an 18.1% CAGR to 2031.

- By deployment model, the public-cloud segment commanded 51.20% share of the cloud-based contact center market size in 2025; hybrid-cloud architectures are advancing at a 21.1% CAGR through 2031.

- By service, professional services accounted for 44.90% of the cloud-based contact center market size in 2025, whereas managed services posted the fastest 17.1% CAGR through 2031.

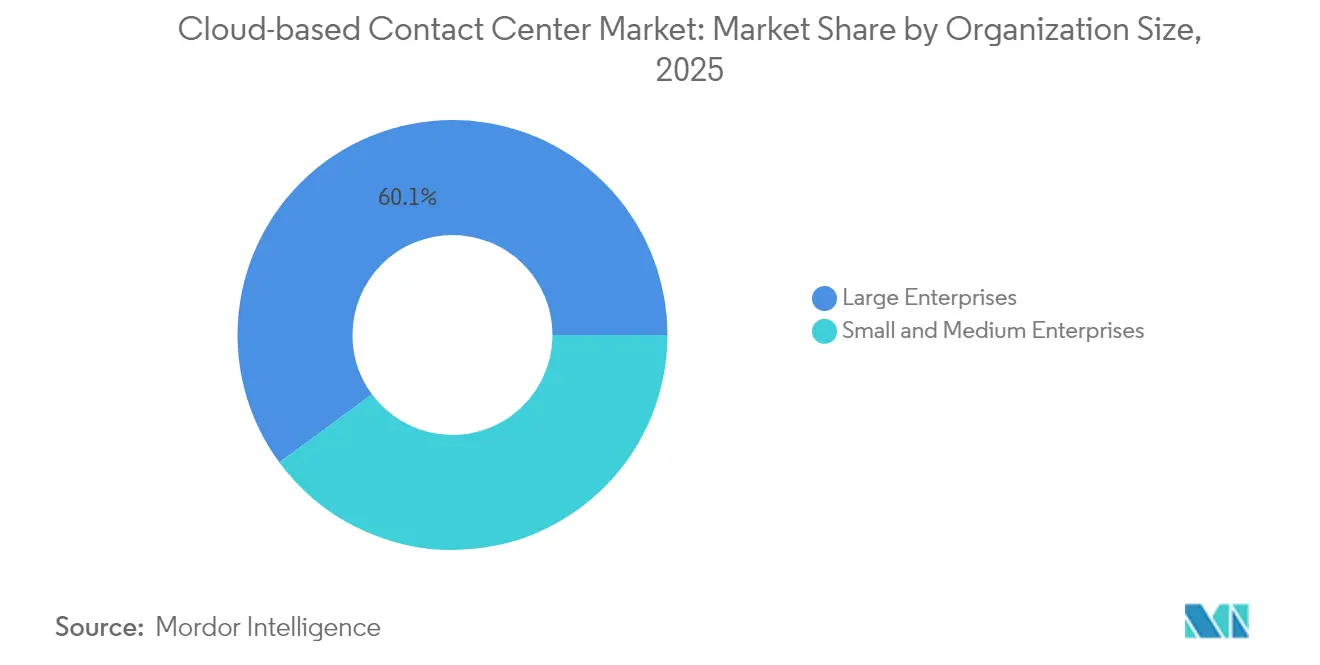

- By organization size, large enterprises held 60.10% of the cloud-based contact center market share in 2025; SMEs are projected to grow at a 18.3% CAGR to 2031.

- By end-user industry, BFSI led with 18.40% revenue share in 2025; healthcare and life sciences registers the strongest 19.9% CAGR through 2031.

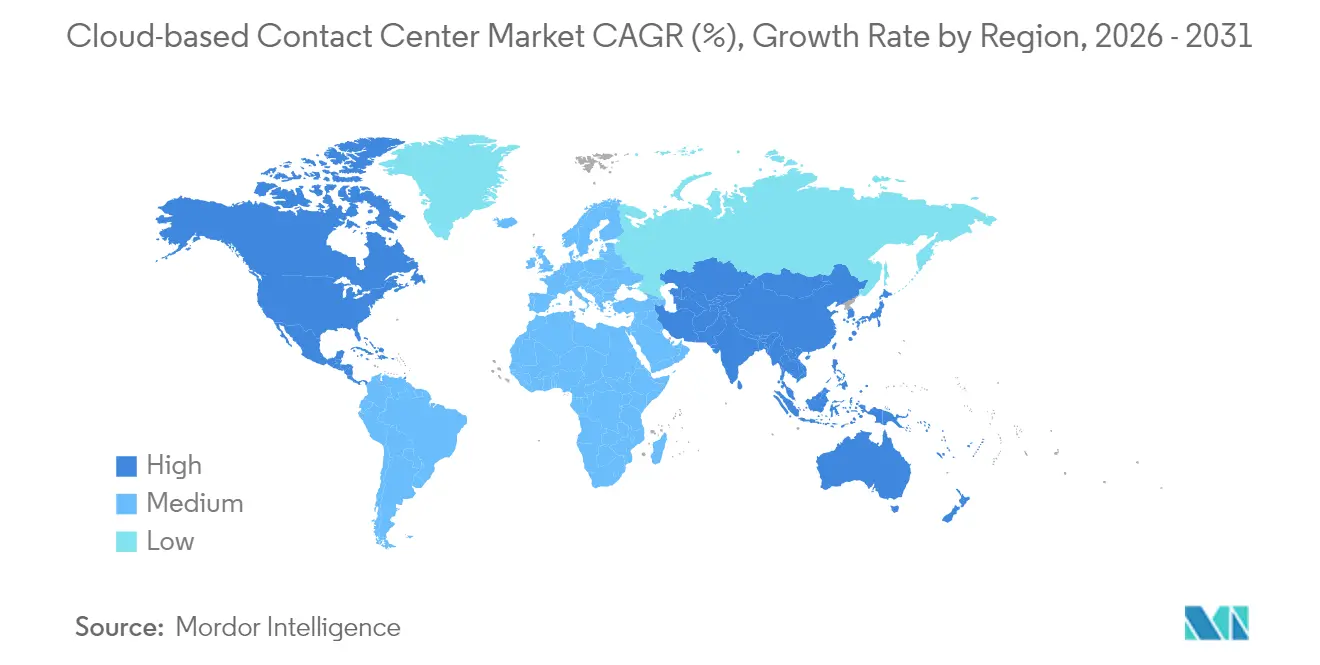

- By geography, North America dominated with 37.80% revenue share in 2025, while Asia-Pacific is set to rise at a 15.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud-based Contact Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in remote and hybrid work adoption | +4.2% | North America; Europe | Short term (≤ 2 years) |

| Rapid shift to omnichannel engagement | +5.8% | Global; APAC leading | Medium term (2-4 years) |

| Lower cap-ex and faster deployment | +3.6% | Emerging markets; SME focus | Short term (≤ 2 years) |

| AI-driven agent-assist at cloud scale | +6.4% | North America; APAC | Medium term (2-4 years) |

| 5G network slicing for ultra-low latency CX | +2.1% | Urban APAC | Long term (≥ 4 years) |

| Industry-specific compliant CCaaS platforms | +1.8% | North America; EU; healthcare and BFSI | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Shift to Omnichannel Customer Engagement

Contact volumes now begin on social channels, pivot to chat, and conclude over voice, demanding a unified agent desktop that legacy equipment cannot deliver economically. Cloud platforms integrate new channels in weeks, not quarters: Genesys Cloud added WhatsApp voice notes so agents can exchange audio messages without leaving workflow screens. Omnichannel alignment also collapses data silos, letting analytics reveal lifetime value signals in real time. Five9’s Deepgram-powered speech recognition improves alphanumeric transcription accuracy two-fold, raising self-service containment and cutting transfers. Enterprises that harmonize channels convert contact centers into proactive insight engines, boosting revenue as every interaction informs personalized outreach. The trend gains urgency in APAC, where mobile-first consumers expect fluid channel hopping, spurring double-digit regional adoption.

AI-Driven Agent-Assist Use-Cases Requiring Cloud Scale

Generative AI workloads need GPUs and elastic compute that exceed on-premise budgets. AWS Connect’s real-time summarization and Five9’s Genius AI Suite show how cloud economics democratize deep-learning models that guide agents mid-conversation [1]Five9, “Five9 Expands Global Footprint with New Data Centers in India,” five9.com . McKinsey reports 72% of CX leaders believe AI will materially reshape operations, yet human call volumes decline slowly, pushing blended models that elevate rather than replace agents. Continuous cloud updates refresh models weekly, keeping intent detection current with slang and product launches. Financial upside is clear: automated self-service averages USD 0.10 per contact versus USD 8 for live support, freeing spend for strategic CX investments.

Lower Cap-Ex and Faster Deployment Than On-Premise

Subscription pricing converts contact-center outlays from capital to operating budgets—vital for SMEs with thin cash reserves. Nearly 49% of small and mid-size businesses have adopted or plan CCaaS deployments, citing go-live timelines under 90 days. Five9’s new Indian data centers cut last-mile latency and remove the burden of local hardware procurement. Mid-tier centers with 50-250 seats report 40% higher first-contact resolution once migrated, proof that speed plus feature breadth inverts the legacy value equation. The democratization cycle accelerates growth among underserved firms previously priced out of advanced CX tooling.

Cyber-Security and Data-Privacy Concerns

Customer interaction data is a magnet for cybercriminals and regulators, making zero-trust frameworks mandatory. Upcoming GDPR+ amendments incorporate AI transparency, forcing providers to surface model logic for every automated decision. Although hyperscalers invest billions in security, risk-averse organizations, especially hospitals, still view on-premise servers as safer. The perception gap lengthens sales cycles, subtracting 2.8 percentage points from forecast CAGR. Providers answer by offering regional data residency, customer-managed keys, and SOC-2 Type II attestations to calm compliance officers. As audits confirm parity—or superiority—of cloud defenses, resistance is expected to fade beyond 2026.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security and data-privacy concerns | -2.8% | EU; healthcare | Short term (≤ 2 years) |

| Cloud-service downtime and vendor lock-in | -1.9% | Mission-critical sectors worldwide | Medium term (2-4 years) |

| Complex migration of legacy IVR and CRM | -2.1% | North America; Europe | Medium term (2-4 years) |

| Cross-border data-sovereignty burdens | -1.4% | EU; APAC financial services | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cyber-security & Data-privacy Concerns

Enterprise security apprehensions regarding cloud-based contact centers stem from legitimate concerns about data exposure and regulatory compliance, particularly as customer interaction data represents high-value targets for cybercriminals and regulatory scrutiny. The implementation of zero trust architecture becomes mandatory for cloud contact center deployments, with organizations requiring comprehensive security frameworks that exceed traditional perimeter-based protection models. GDPR, TCPA, HIPAA, and PCI-DSS compliance requirements create complex security obligations that some organizations perceive as easier to manage with on-premise infrastructure, despite cloud providers' typically superior security capabilities.

Complex Migration of Legacy IVR & CRM Integrations

Legacy system integration complexity creates significant barriers to cloud contact center adoption, particularly for large enterprises with extensive on-premise infrastructure investments and customized workflows that resist standardization. The migration of Interactive Voice Response systems and Customer Relationship Management integrations requires careful planning to avoid service disruptions, with many organizations underestimating the technical complexity and resource requirements for successful transitions. Established enterprises often maintain decades-old telephony infrastructure with custom integrations that cloud platforms cannot easily replicate, creating migration projects that extend beyond anticipated timelines and budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Analytics Drive Intelligence Revolution

Analytics and Reporting applications are forecast to grow at an 18.1% CAGR, reflecting demand for actionable insights that elevate customer lifetime value. In 2025 Automatic Call Distribution still held a 23.80% cloud-based contact center market share, anchoring routing logic that funnels queries to the right expertise. The convergence of speech analytics, sentiment scoring, and KPI dashboards turns every interaction into a dataset that steers marketing, product, and service decisions. Five9 offers 140 pre-built reports alongside AI-generated recommendations, making enterprise-grade analytics accessible to firms with limited data staffs.

Workforce Engagement Management (WEM) adoption is accelerating as planners connect agent well-being to CX outcomes. NICE’s Employee Engagement Manager automates shift bidding and performance nudges, improving retention and boosting sales by 20% among engaged teams. Integrating WEM with analytics lets supervisors predict staffing around promotional spikes or outages. Dialer tools, while still relevant for campaigns, see tempered growth as compliance caps outbound volumes. Overall, providers that unify routing, analytics, and WEM into one pane gain stickier deployments and upsell paths.

By Deployment Model: Hybrid Cloud Gains Strategic Momentum

Public cloud offerings captured 51.20% of the cloud-based contact center market size in 2025 as enterprises targeted quick wins and global reach. Yet hybrid architecture, projected to expand at 21.1% CAGR, is the strategic sweet spot for regulated industries balancing sovereignty with innovation. Cisco notes 82% of enterprises now run hybrid estates, segmenting workloads by sensitivity and latency . Hybrid lets banks keep core call recording on private nodes while leveraging public regions for burst analytics, satisfying auditors without sacrificing agility.

Multi-cloud permutations add another control layer: if one provider suffers an outage, traffic reroutes seamlessly. Huawei Cloud’s 106% hybrid-cloud growth in APAC illustrates regional appetite for sovereign nodes paired with global feature catalogs. Private cloud lingers for defense and critical infrastructure, but lifecycle economics increasingly favor managed hybrid stacks where vendors shoulder patching, scaling, and compliance paperwork. Decision frameworks thus pivot from blanket prohibitions to workload-by-workload placement.

By Service: Managed Services Accelerate Operational Outsourcing

Professional services represented 44.90% of 2025 revenue because initial migrations demand design, integration, and change-management expertise. As environments stabilize, managed services flourish, growing 17.1% annually as clients hand day-to-day tuning to specialists. Providers bundle KPI monitoring, bot retraining, and compliance reporting into fixed-fee contracts that outperform in-house teams on cost and uptime. Alvaria’s Employee Experience Management suite folds WEM telemetry into managed engagements, giving customers continuous workforce optimization without extra licenses .

Training and support services remain a pillar because every quarterly release adds capabilities that staff must master. Vendors increasingly deliver on-demand micro-learning and AI-based coaching that shortens proficiency curves. Overall, service depth becomes a key differentiator: technology parity is narrowing, so vendors that guarantee ROI through white-glove operations capture renewals and referrals.

By Organization Size: SMEs Drive Democratic Access Revolution

Large enterprises still account for 60.10% revenue, aided by scale and integration teams that exploit full platform breadth. Yet SMEs, expanding at 18.3% CAGR, are the growth engine as pay-as-you-go pricing removes entry hurdles. Cloud solutions auto-scale from five to 500 agents, letting retailers add seasonal seats in days. NICE defines SMEs as firms under 500 employees, and within that cohort, contact centers of 50-250 seats register the largest efficiency gains post-migration.

For startups, CCaaS is often the first telephony investment, skipping PBX ownership entirely. For mid-market firms, cloud unlocks AI features from tone analysis to predictive routing previously reserved for Fortune 500 budgets. Vendor competition centers on simplified onboarding, pre-built CRM connectors, and marketplace apps that let non-technical users add capabilities. As SME adoption widens, regional channel partners and MSPs become critical to penetrate local language and compliance nuances.

By End-User Industry: Healthcare Leads Digital Transformation

BFSI institutions held an 18.40% slice of 2025 revenue because stringent Know-Your-Customer and fraud controls make omnichannel transparency essential. However, healthcare and life sciences grow fastest at a 19.9% CAGR as telehealth normalizes and patient-experience scores influence reimbursements. IBM’s work with Rhode Island’s Department of Health shows CCaaS platforms can quintuple case investigation speed, demonstrating public-sector value .

Retail and e-commerce firms deploy CCaaS to weave physical and digital storefronts into seamless journeys, converting browsing signals into real-time offers. Logistics providers rely on voice and SMS alerts that shave minutes off delivery windows. Government adoption is rising as budgets migrate from cap-ex hardware refreshes to opex subscriptions, enhancing citizen engagement while meeting secure-by-default mandates. Across industries, vertical-specific compliance certifications and out-of-box integrations now drive vendor shortlisting more than generic feature counts.

Geography Analysis

North America contributed 37.80% of 2025 revenue, buoyed by mature broadband, early cloud buy-in, and proactive customer-experience budgeting. Hyperscalers operate dense regional data-center footprints, delivering sub-50 ms latency that powers real-time transcription and sentiment analytics. Market maturity means net-new logo growth slows, so providers focus on AI upsells and outcome-based renewals. Consolidation is underway as private-equity firms acquire niche CCaaS vendors to build end-to-end CX suites.

Asia-Pacific is on track for a 15.2% CAGR through 2031, propelled by smartphone ubiquity, government cloud-first edicts, and expanding fiber coverage. Five9’s dual Indian data centers exemplify investments that respect data-localization rules while assuring performance. Developed markets like Japan demand advanced AI orchestration, whereas Southeast Asian SMEs prioritize cost and multilingual bots. Regional telcos partner with CCaaS providers, bundling SIP trunks, 5G slices, and CPaaS APIs to accelerate uptake among emerging digital merchants.

Europe balances opportunity with regulatory rigor. GDPR plus emerging AI-governance laws drive hybrid deployments anchored in local zones. Providers that certify ISO 27001 and offer in-region disaster recovery gain advantage. Economic headwinds push enterprises toward opex models that stretch budgets without new datacenter builds. Growth pockets exist in Central and Eastern Europe where legacy estates persist, and in public-sector digitization funds earmarked for post-pandemic citizen-service modernization. Elsewhere, Latin America, Middle East, and Africa record high double-digit adoption albeit from lower bases, paced by telecom infrastructure rollouts and fintech booms.

Competitive Landscape

Market structure is moderately concentrated: NICE, Genesys, and Five9 together generate more than USD 4 billion in annual recurring revenue, yet their combined share remains below 35%, leaving room for challengers. Hyperscalers like AWS Connect bundle per-minute pricing with broader cloud portfolios, squeezing license rates and forcing incumbents to accelerate feature releases. Genesys’ USD 1.5 billion injection from Salesforce and ServiceNow underscores investment appetite for AI-infused CX stacks.

Differentiation pivots on depth of AI, vertical blueprints, and an ecosystem that shortens time-to-value. Vendors roll out domain-specific language models—healthcare, banking, retail—to raise accuracy without manual tuning. Strategic alliances proliferate: Verint and Five9 launched cloud-to-cloud integrations that fuse workforce management with omnichannel routing. Meanwhile, AI-native disruptors tout usage-based fees and 30-day onboarding, winning greenfield SME deals.

Pricing pressure coexists with rising switching costs as platforms entrench through proprietary data lakes and analytics dashboards. To hedge lock-in fears, buyers insist on open APIs and bring-your-own-model capabilities. Provider roadmaps now spotlight responsible-AI toolkits, customer-managed encryption keys, and carbon-aware routing, aligning with environmental, social, and governance procurement criteria. Overall, sustainable leadership demands continuous innovation, robust compliance posture, and services that translate technology into measurable business outcomes.

Cloud-based Contact Center Industry Leaders

Avaya Contact Center (Ayaya Group)

RingCentral Inc.

Genesys Telecommunications Laboratories Inc.

3CLogic Inc.

Five9 Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Five9 opened data centers in Delhi and Mumbai after receiving India’s Unified License, broadening reach while ensuring domestic call compliance.

- January 2025: LivePerson expanded its partnership with Google Cloud to infuse generative AI into its Connected Experience Platform, enabling personalized, anticipatory support.

- December 2024: Uniphore and Konecta targeted USD 500 million revenue over five years by co-developing industry-specific generative-AI CX solutions for U.S. and U.K. clients.

- September 2024: Verint and Five9 introduced cloud-to-cloud integration that marries Verint analytics with Five9 routing to automate customer experience workflows.

Global Cloud-based Contact Center Market Report Scope

Cloud-based contact centers refer to network services where the technology is owned and operated by a cloud services provider. This study categorizes these centers by type, service (including professional and managed services), end-user industry, and geography.

The cloud contact center market is segmented by type (automatic call distribution, agent performance optimization, dialers, interactive voice response, computer telephony integration, and analytics and reporting), services (professional services and managed services), end-user industry (banking, financial services, and insurance(BFSI), it and telecom, media and entertainment, retail, logistics and transport, healthcare, and other end-user industries), geography (North America, Europe, Asia, Australia and New Zealand, Latin America, and Middle East and Africa). The market size and forecasts are provided in terms of value USD for all the above segments.

| Automatic Call Distribution (ACD) |

| Interactive Voice Response (IVR) |

| Predictive / Progressive Dialers |

| Computer Telephony Integration (CTI) |

| Analytics and Reporting |

| Workforce Engagement Management |

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Multi-Cloud |

| Professional Services |

| Managed Services |

| Training and Support Services |

| Small and Medium Enterprises ( less than 1,000 seats ) |

| Large Enterprises ( Greater than or equal to 1,000 seats ) |

| Banking, Financial Services and Insurance |

| IT and Telecommunications |

| Retail and e-Commerce |

| Healthcare and Life Sciences |

| Logistics and Transportation |

| Media and Entertainment |

| Government and Public Sector |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Israel |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Solution Type | Automatic Call Distribution (ACD) | ||

| Interactive Voice Response (IVR) | |||

| Predictive / Progressive Dialers | |||

| Computer Telephony Integration (CTI) | |||

| Analytics and Reporting | |||

| Workforce Engagement Management | |||

| By Deployment Model | Public Cloud | ||

| Private Cloud | |||

| Hybrid Cloud | |||

| Multi-Cloud | |||

| By Service | Professional Services | ||

| Managed Services | |||

| Training and Support Services | |||

| By Organization Size | Small and Medium Enterprises ( less than 1,000 seats ) | ||

| Large Enterprises ( Greater than or equal to 1,000 seats ) | |||

| By End-User Industry | Banking, Financial Services and Insurance | ||

| IT and Telecommunications | |||

| Retail and e-Commerce | |||

| Healthcare and Life Sciences | |||

| Logistics and Transportation | |||

| Media and Entertainment | |||

| Government and Public Sector | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Israel | |

| Saudi Arabia | |||

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the cloud-based contact center market by 2031?

The cloud-based contact center market is expected to reach USD 116.33 billion by 2031.

Which region will grow fastest over the forecast period?

Asia-Pacific is forecast to post a 15.2% CAGR through 2031, the highest among all regions.

Which deployment model is gaining momentum among regulated industries?

Hybrid-cloud configurations are expanding at a 21.1% CAGR as firms balance agility with data sovereignty.

Why are SMEs adopting cloud-based contact centers rapidly?

Subscription pricing, quick deployment, and built-in AI features remove infrastructure and cost barriers for SMEs.

Page last updated on: