Micro Mobile Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

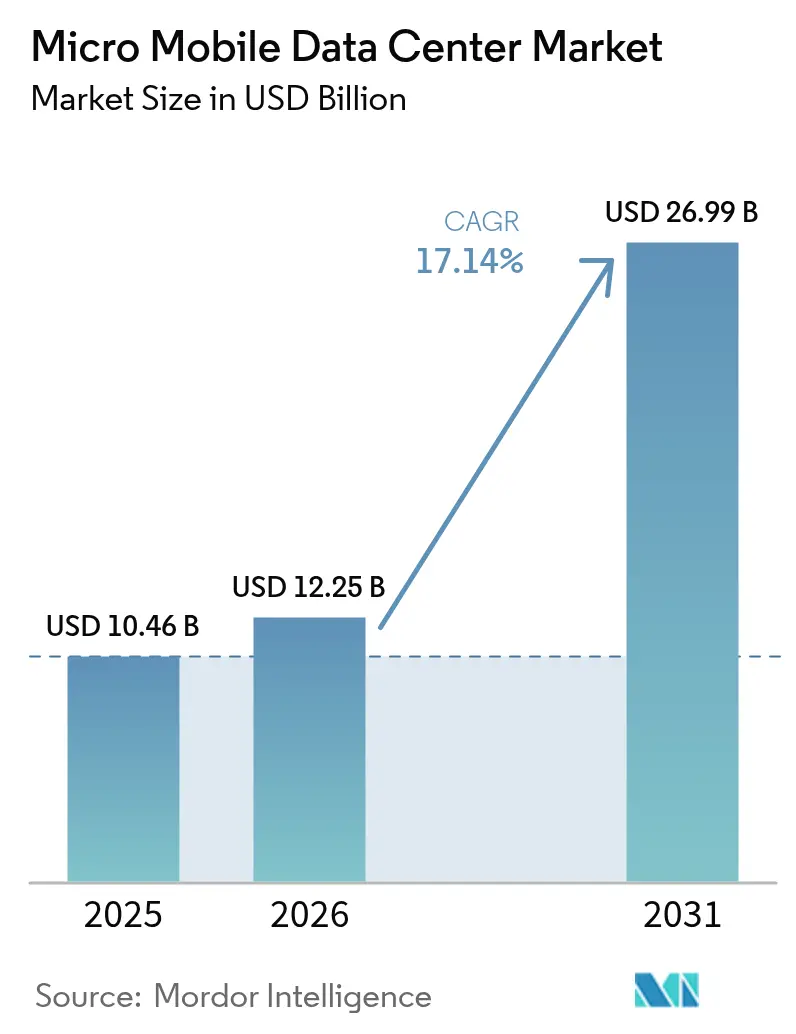

| Market Size (2026) | USD 12.25 Billion |

| Market Size (2031) | USD 26.99 Billion |

| Growth Rate (2026 - 2031) | 17.14% CAGR |

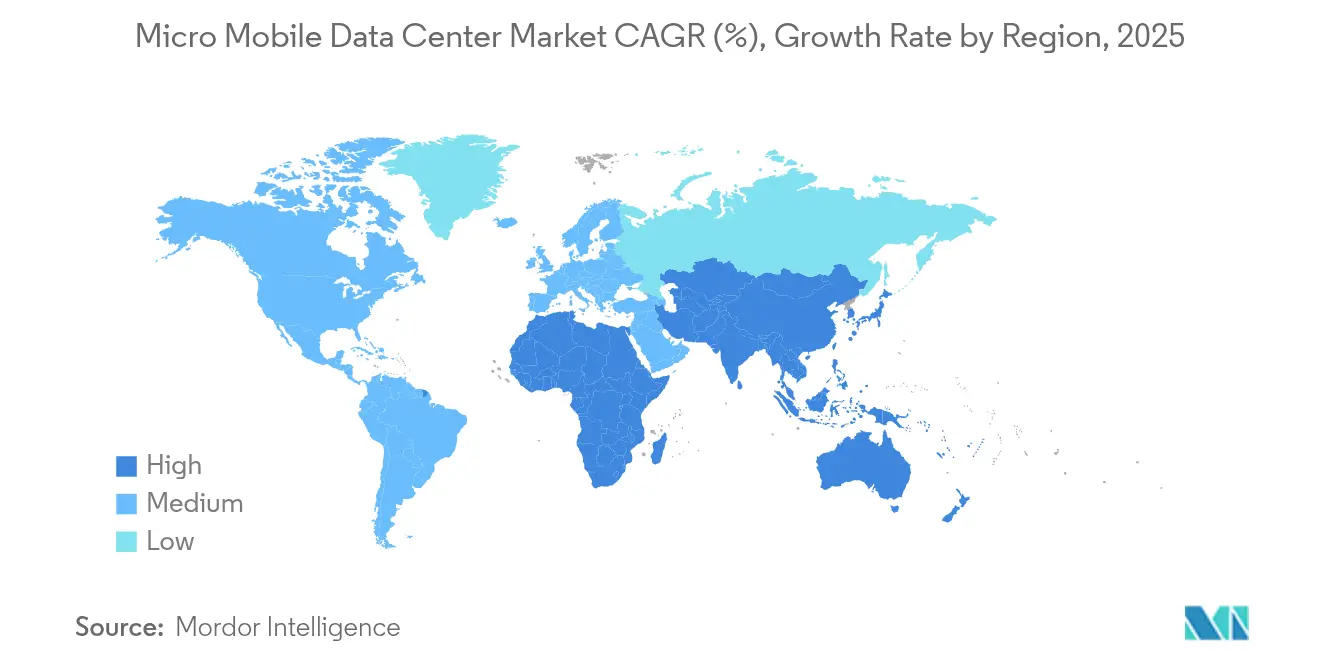

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Micro Mobile Data Center Market Analysis by Mordor Intelligence

micro mobile data center market size in 2026 is estimated at USD 12.25 billion, growing from 2025 value of USD 10.46 billion with 2031 projections showing USD 26.99 billion, growing at 17.14% CAGR over 2026-2031. Most of this momentum comes from enterprises pushing compute resources closer to data-generation points to avoid latency, meet real-time analytics needs, and lower backhaul costs. Rapid 5G roll-outs, soaring IoT traffic, and mounting resiliency requirements after high-profile hyperscaler outages are amplifying demand, while modular designs and edge-as-a-service offers shorten deployment times and reduce upfront capital outlays. North America retains leadership on the strength of hyperscaler investment and an advanced telecom backbone, yet Asia-Pacific is growing the fastest as governments back smart-city programs and digital-economy goals. Vendors are responding with pre-integrated, remotely managed systems that simplify life-cycle operations and appeal strongly to resource-constrained SMEs, which already generate a majority of installations.

Key Report Takeaways

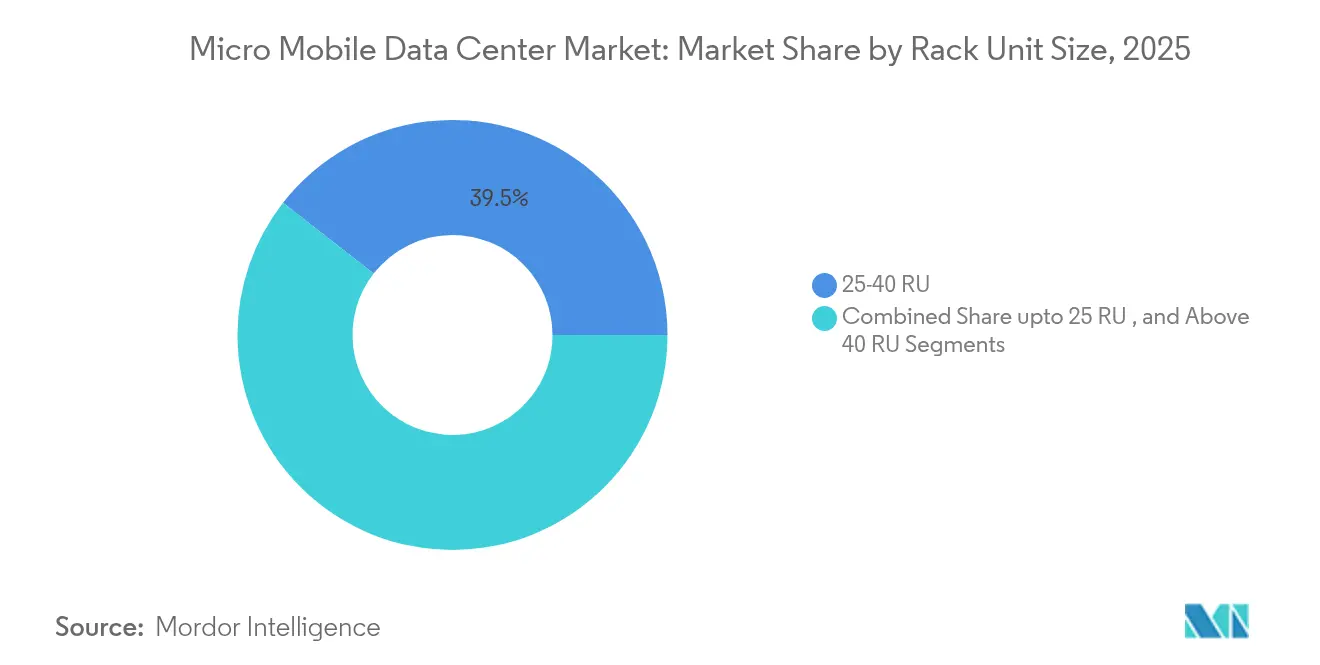

- By rack unit size, the 25-40 RU category captured 39.45% of the micro mobile data center market share in 2025 and is on track for a 18.6% CAGR through 2031.

- By form factor, rack-mounted pods led with 50.55% revenue share in 2025; containerized modules are projected to record the strongest 19.4% CAGR.

- By application, edge computing nodes accounted for 42.15% of the micro mobile data center market size in 2025, while high-density networks will advance at an 17.9% CAGR over 2026-2031.

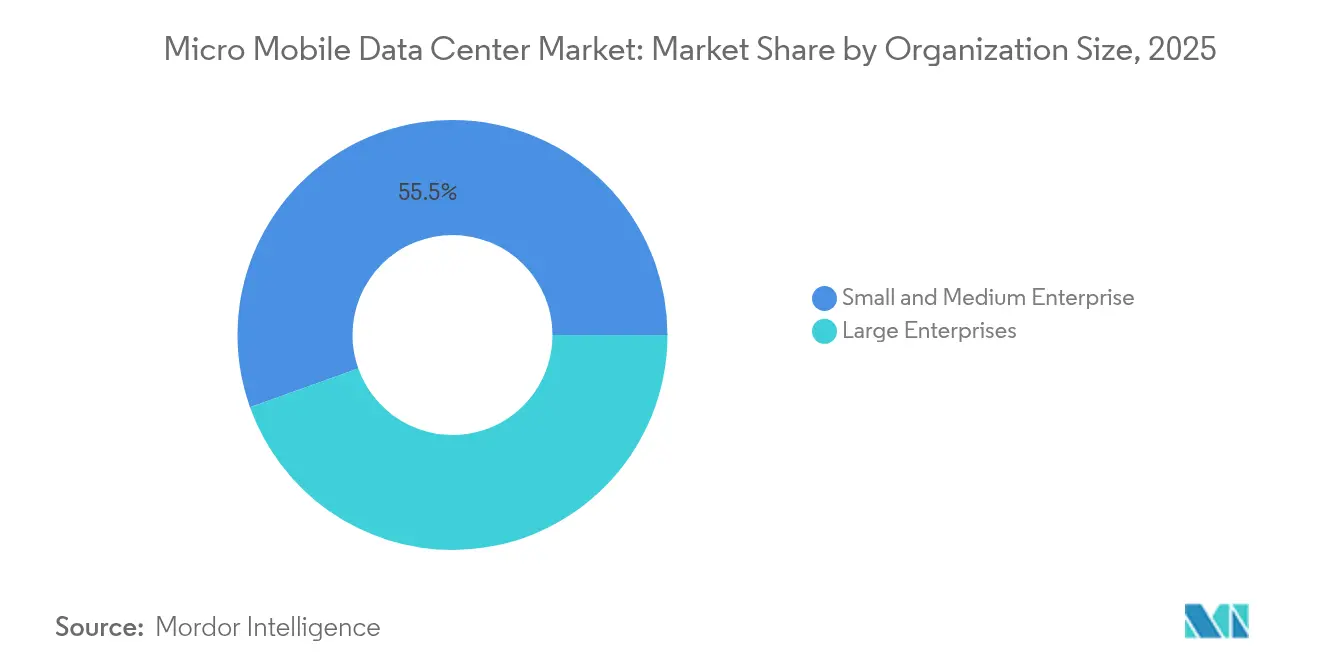

- By organization size, SMEs held 55.45% share of the micro mobile data center market size in 2025 and are expanding at a 21.2% CAGR through 2031.

- By end-user vertical, IT and telecommunications captured 31.75% of the micro mobile data center market in 2025; healthcare and life sciences will post the fastest 18.85% CAGR.

- By geography, North America commanded 34.65% of 2025 revenue, whereas Asia-Pacific will register an 18.1% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Micro Mobile Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Edge‐computing push from 5G roll-outs | +3.5% | Global, with concentration in North America, East Asia, Western Europe | Medium term (2-4 years) |

| Exponential IoT data at endpoints | +2.8% | Global, with emphasis on industrial hubs in Asia-Pacific and Europe | Medium term (2-4 years) |

| Rapid retail omni-channel digitization | +2.3% | North America, Europe, developed Asia-Pacific markets | Short term (≤ 2 years) |

| Heightened resilience needs after hyperscaler outages | +1.9% | Global, with emphasis on financial centers | Short term (≤ 2 years) |

| Military demand for rugged off-grid compute | +1.5% | North America, Europe, Middle East | Medium term (2-4 years) |

| ESG-driven micro-grid pairing for renewables | +1.2% | Europe, North America, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Edge-Computing Push from 5G Roll-Outs

Fifth-generation networks are raising throughput to 10 Gbps and pushing latency below 1 ms, making centralized processing impractical for immersive realities, autonomous mobility, and industrial automation. Carriers are therefore co-locating micro mobile data center market nodes at cell-site edges to host network-function virtualization and multi-access edge computing stacks. Real-time video analytics, AR retail fitting rooms, and cooperative vehicle guidance now execute locally, trimming transport costs and guaranteeing deterministic performance. Spending on edge infrastructure jumped 15.4% to USD 232 billion in 2024, spearheaded by telecom operators eager to monetize 5G capacity.[1] Mathew Schwartz, “2024 Was the Breakout Year for Edge Computing,” bankinfosecurity.com

Exponential IoT Data at Endpoints

Billions of smart sensors in factories, hospitals, and city streets churn out torrents of telemetry that cannot all traverse the WAN. Compact, ruggedized enclosures installed beside manufacturing lines or inside smart-lighting poles let algorithms infer, filter, and compress raw feeds before optionally syncing with the cloud. Localized processing also satisfies data-sovereignty and privacy codes in regulated industries. FS.com observes that edge micro sites improve security by retaining sensitive payloads on premises until policy checkpoints are met.[2]FS Technology, “How to Build a High-Performance Edge Data Centre?” FS.com

Rapid Retail Omni-Channel Digitization

Retailers are adopting store-level micro nodes to synchronize inventory, drive computer-vision checkout, and personalize digital signage in real time. The blend of 5G, Wi-Fi 7, and AI inference at the shelf delivers frictionless “buy-online-pick-up-in-store” flows and immersive in-aisle promotions. Cambridge Management Consulting notes that back-of-house deployments let chains consume cloud services without heavy capital outlay while keeping latency-sensitive interactions below 20 ms.[3]Cambridge Management Consulting, “Future of Retail: How Edge Compute Will Help Create a 24-7 Augmented Retail Experience,” cambridgemc.com

Heightened Resilience Needs After Hyperscaler Outages

Successive hyperscale disruptions in 2024 prompted large enterprises to diversify compute footprints. Edge installations now anchor multi-cloud strategies, instantly absorbing transaction loads when primary regions fail. Tripp Lite reports rising demand for pre-cabled micro enclosures that reach site in three days and slot into disaster-recovery playbooks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Talent scarcity in edge-qualified facility ops | -1.8% | Global, with acute impact in rapidly growing markets | Medium term (2-4 years) |

| Fragmented regulatory codes for modular DCs | -1.2% | Regional variations across North America, EU, Asia-Pacific | Medium term (2-4 years) |

| Lithium-ion thermal-runaway concerns | -0.9% | Global, with stricter impact in densely populated areas | Short term (≤ 2 years) |

| Copper and rare-earth supply-chain volatility | -0.7% | Global, with pronounced impact on manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Talent Scarcity in Edge-Qualified Facility Operations

Running hundreds of distributed enclosures demands personnel who grasp IT, electrical, and mechanical disciplines. Schneider Electric’s open courseware has enrolled more than 1 million learners to bridge the projected need for 2.3 million data-center staff by 2025. Yet recruitment lags, slowing roll-outs in emerging markets.

Lithium-Ion Thermal-Runaway Concerns

A May 2025 fire in Hillsboro, Oregon exposed response gaps when densely packed cells ignite. Regulators are drafting new ventilation, gas-detection, and separation mandates that lengthen permitting cycles, especially in urban cores. Early-warning off-gas sensors promoted by Honeywell are gaining traction to contain incidents before cascading failure

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rack Unit Size: 25-40 RU Dominates Enterprise Deployments

The 25-40 RU accounted for 39.45% of the micro mobile data center market and is forecast to advance at 18.6% CAGR. Enterprises favor this footprint because it bundles compute, power, and cooling in a cabinet that is both compact enough for branch sites and spacious enough to accommodate future workload expansion. Compact UPS systems with integrated lithium-ion packs from Delta boost density while trimming floor-space requirements.

Smaller sub-25 RU enclosures excel in areas where real estate is scarce, such as highway toll booths or offshore rigs, but often struggle with airflow and limited spare capacity. Configurations above 40 RU serve aggregation layers or telecom central offices demanding GPU clusters for AI inference. Suppliers expect hybrid designs, where two 30 RU frames travel as a pair to balance resilience and scalability in the micro mobile data center market.

By Form Factor: Rack-Mounted Pods Enable Flexible Scaling

Rack-mounted pods accounted for 50.55% of revenue and will maintain lead status thanks to standardized depth and width that align with existing server infrastructure. Customers scale one pod at a time, synchronizing cash spend with application demand and shrinking stranded capacity. Supermicro’s rack-scale architecture even lets operators disaggregate NVMe storage and recombine resources on the fly to optimize utilization.

Containerized modules deliver rapid bulk capacity for event venues or remote mining, often arriving factory-sealed with outside-air economizers. Wall-mount nodes satisfy convenience-store chains and quick-service restaurants, where floor space is premium. Vendors now add shock sensors, dust filters, and tamper switches to withstand harsh field conditions, expanding addressable workloads across the broader micro mobile data center market.

By Application: Edge Computing Nodes Drive Market Growth

Edge computing nodes seized 42.15% of 2025 demand, equal to USD 4.4 billion, and anchor the highest installed base of micro mobile data center market nodes. They host AI-assisted quality inspection on assembly lines, distribute public safety camera analytics, and crunch LIDAR feeds for autonomous shuttles. Adding FPGA and GPU accelerators improves inference latency without saturating uplinks.

High-density network functions will log the fastest 17.9% CAGR. Telcos virtualize routing, firewalls, and user-plane functions inside steel-walled pods stationed at aggregation sites, cutting CapEx compared to custom appliances. Remote-office, disaster-recovery, and backup workloads remain essential, giving enterprises granular control during connectivity failures.

By Organization Size: SMEs Embrace Edge Computing Advantages

SMEs commanded 55.45% of the micro mobile data center market in 2025 and are scaling at 21.2% CAGR through 2031. Subscription-based, pre-configured racks let smaller firms obtain high-availability compute without building specialized facilities or recruiting full-time engineers. Financing bundles hardware, monitoring, and break-fix services under monthly operating budgets. Zella DC sees local clinics, law firms, and logistics depots adopting turnkey pods to lower latency and satisfy data-sovereignty policies.

Large enterprises deploy identical blueprints across hundreds of branches to simplify security audits, firmware patching, and life-cycle refreshes. Edge-as-a-service models also resonate with their need for consumption-based pricing when launching temporary pop-up sites or seasonal events.

By End-User Vertical: Healthcare Adoption Accelerates

IT and telecommunications led spending at 31.75% in 2025 because cell-site MEC and content-delivery caches demand short-haul latency. Precise timing, hardened enclosures, and zero-touch provisioning are critical design features. Edge nodes also run private 5G cores that orchestrate industrial devices.

Healthcare climbs fastest at a 18.85% CAGR through 2031 as imaging repositories, bedside monitoring, and robotic surgery insist on sub-millisecond responses. Micro nodes process protected health information locally, keeping sensitive scans on campus to comply with HIPAA and GDPR. Retail, e-commerce, government, and defense follow, each tailoring ruggedness, encryption, or environmental controls to mission requirements within the micro mobile data center market.

Geography Analysis

North America held 34.65% of total revenue in 2025 thanks to dense 5G roll-outs, hyperscaler investment in edge POPs, and supportive data-sovereignty statutes for healthcare and finance. The United States dominates, with Northern Virginia, Silicon Valley, and Texas generating heavy demand for campus-adjacent edge nodes that complement megascale builds. Federal initiatives such as microreactor pilots underscore commitment to off-grid power strategies for strategic workloads.

Asia-Pacific will post the highest 18.1% CAGR to 2031 as China, India, Japan, and South Korea accelerate smart-manufacturing and connected-mobility programs. State grants and spectrum allocations encourage telcos and cloud providers to host proximate compute for real-time IoT analytics. Vantage’s second Cyberjaya campus and NTT DATA’s Jakarta build illustrate a regional shift toward distributed models capable of respecting local data-residency laws.

Europe continues steady expansion led by Germany, the United Kingdom, and France. Strict GDPR rules require localized processing, so factories, hospitals, and fintechs invest in zone-specific clusters instead of shipping data across borders. Equinix’s IBX network in Frankfurt, London, and Paris bridges regional hubs to cloud on-ramps while hosting sub-5 ms edge workloads. Emerging adoption in the Middle East, Africa, and South America starts from smaller bases but is buoyed by smart-city budgets and 5G corridor projects, opening fresh terrain for micro mobile data center market suppliers.

Regulatory Landscape

Compliance for micro mobile data centers is being shaped by faster-moving standards and region-specific critical-infrastructure rules that affect distributed, small-footprint deployments. On the technical side, the Telecommunications Industry Association updated TIA-942-C in 2024, adding clearer requirements relevant to edge and micro data center infrastructure, while ITU-T issued Recommendation L.1307 (2024) focused on energy efficiency in micro data centers used for edge computing. For security and governance, ISO/IEC 22237-6:2024 reinforces physical security expectations for data center infrastructure, which becomes more operationally complex when scaled across hundreds of remote sites.

Policy fragmentation continues to constrain developers because permitting and operating obligations vary by jurisdiction, particularly for power, cooling, and resilience choices used in modular units. In the European Union, NIS2 and related critical-entity and financial-sector frameworks (CER and DORA) increase cybersecurity and incident reporting requirements for operators and key suppliers supporting digital infrastructure. In the United States, environmental and infrastructure policy is increasingly state-driven for data centers, including water-use and rulemaking timelines. For example, North Carolina Senate Bill S730 directs the Department of Environmental Quality to adopt permanent rules by September 1, 2026, while a July 2025 federal action to accelerate permitting targets very large data center projects affects how developers package compliance and documentation, including when deploying edge nodes as part of broader programs.

Value Chain Analysis

The value chain for micro mobile data centers starts with component suppliers for compute, storage, and networking, along with power electronics (UPS, switchgear, batteries) and thermal systems (DX, liquid, or hybrid cooling). From there, enclosure OEMs and integrators pre-wire, test, and certify rack-mounted pods or containerized modules. Distribution typically runs through IT channel partners, telecom equipment providers, and system integrators or MSPs that bundle configuration, installation, and managed services, before landing with end users such as telecom operators (MEC and network functions), enterprises (branch, retail, industrial), and government and defense customers that prioritize ruggedization and rapid commissioning.

Factory prefabrication is the main differentiator across the value chain because it moves labor from the jobsite into controlled manufacturing, tightening QA and compressing deployment cycles relative to conventional builds. It also helps offset the field labor scarcity that shows up in distributed operations. The most common constraints are long lead times for high-density power and cooling subassemblies and limited availability of edge-qualified operations talent. Siting decisions often favor existing telecom central offices, 5G aggregation points, and utility-adjacent locations to reduce fiber buildout and streamline power access. Industry initiatives such as the Open Compute Project Open Systems for AI (launched January 2025) also push vendors toward pre-qualified, modular building blocks that can be used in repeatable edge blueprints.

Competitive Landscape

The micro mobile data center market is moderately concentrated, featuring infrastructure majors, telecom suppliers, and niche edge specialists. Schneider Electric, Dell Technologies, Hewlett Packard Enterprise, and Vertiv fold micro offerings into end-to-end portfolios that span racks, power, cooling, and management software. Huawei blends radio access know-how with integrated edge-cloud stacks for carriers. Pure-plays such as Zella DC, EdgeConneX, and HIRO Micro Data Centers differentiate themselves through localized cooling, sealed enclosures, or service models designed for underserved metropolitan areas.

Strategic alliances pair complementary capabilities. Supermicro collaborates with GPU vendors to pre-qualify AI inference kits, while Microamp partners with Thales and Druid Software to integrate AES-256 encryption into millimeter-wave private 5G bundles, targeting defense customers. Edge-as-a-service is now featured in telecom operators’ catalogs, converting hardware CapEx to consumption-based fees and expanding SME reach.

Innovation centers on liquid and refrigerant-based cooling, lithium-ion safety systems rated to UL9540A, and zero-touch orchestration that rolls out firmware and security patches across thousands of micro sites. Vertiv’s 24% year-on-year revenue jump in Q1 2025 underscores surging demand for modular architectures, encouraging new manufacturing capacity in South Carolina. Vendors increasingly bundle analytics that predict component failure, lowering truck rolls and improving service-level adherence across the wider micro mobile data center market.

Micro Mobile Data Center Industry Leaders

Schneider Electric SE

Dell EMC Inc.

Huawei Technologies Co. Ltd

Hewlett Packard Enterprise Development LP

Eaton Corporation PLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Telecom-led edge rollouts and standardized far-edge network functions create a clear whitespace for turnkey micro mobile data center platforms that reduce integration effort across multi-site deployments. Nokia's February 2026 agreement to deploy data center networking solutions across Telefonica's edge data centers in Spain, covering 17 new edge nodes (with 12 already deployed), points to demand for repeatable edge stacks that can be replicated per node. In parallel, far-edge packet core and user-plane function deployments create another pull-through channel for compact, pre-integrated enclosures, reinforced by an Intel, Dell, and Nokia preview of an edge-based UPF device at Mobile World Congress 2026 designed for 5G far-edge environments.

A second opportunity area is co-locating prefabricated micro data centers with existing power infrastructure to reduce site development friction and address energy and interconnection constraints. In July 2026, Nvidia, Prologis, EPRI, and InfraPartners announced a collaboration to pilot prefabricated micro data centers (5-20 MW) at US utility substation sites, with five pilot projects targeted for development by the end of 2026. This expands a pathway for standardized, power-adjacent deployments that can also support edge AI inference. On the service layer, edge-as-a-service and managed offerings for SMEs remain a practical adoption lever, given SMEs represent the majority of installations in the market context, leaving room for vendors and integrators to bundle subscription pricing, remote operations, and compliance-aligned security and battery-safety monitoring into a single procurement motion.

Recent Industry Developments

- June 2026: Schneider Electric and Foxconn announced a strategic partnership to co-develop reference architectures for AI data centers, aligning Foxconn manufacturing capabilities with Schneider Electric power, cooling, and infrastructure systems. The collaboration supports more standardized, repeatable building blocks that can influence micro and modular deployments where power density and rapid rollout are central requirements.

- May 2026: Hewlett Packard Enterprise and Schneider Electric launched the HPE Micro Datacenter, a turnkey edge solution pairing HPE compute and storage with Schneider Electric's SmartBunker FX enclosure. The combined offer lowers integration effort for distributed sites and strengthens vendor ability to sell pre-validated edge bundles into SME and branch deployments.

- May 2025: Vertiv opened a new manufacturing plant in South Carolina focused on modular systems as demand for modular architectures increased. The added production footprint improves supply availability for prefabricated micro data center configurations and supports shorter delivery cycles for edge and resilience-driven projects.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The micro mobile data center market is defined as compact, self-contained data center infrastructure that can be deployed near the point of use, with integrated power, cooling, cabling, and connectivity to support edge computing needs in multiple environments.

Scope exclusions: Traditional large-scale fixed data center builds and general enterprise IT hardware that is not part of a complete micro mobile data center package are excluded.

Segmentation Overview

- By Rack Unit Size

- Up to 25 RU

- 25 - 40 RU

- Above 40 RU

- By Form Factor

- Containerized Modules

- Rack-Mounted Pods

- Wall-Mounted / Micro-Edge Nodes

- By Application

- Instant / Retrofit Data Center

- Edge-Computing Nodes

- High-Density Networks

- Remote Office and Branch Office

- Mobile and Tactical Computing

- Disaster Recovery and Backup

- By Organization Size

- Small and Medium Enterprises

- Large Enterprises

- By End-user Vertical

- IT and Telecommunication

- BFSI

- Retail and E-commerce

- Healthcare and Life Sciences

- Government and Defense

- Energy and Utilities

- Manufacturing and Industrial

- Education

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Netherlands

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Singapore

- Australia

- Malaysia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- UAE

- Saudi Arabia

- Turkey

- Israel

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by grounding our understanding of demand for edge deployments and small-footprint infrastructure, and then narrowing it down to micro mobile data center form factors. Public sources, such as the International Telecommunication Union (ITU), the International Energy Agency (IEA), the US Energy Information Administration (EIA), the US International Trade Commission data portals, and standards bodies such as ISO and IEC, are used to sanity-check macro signals that influence deployments.

We also review company filings, investor presentations, product documentation, and reputable technology press to confirm what is typically bundled in a micro mobile data center and how buyers describe use cases like remote operations and emergency response. For additional context, we selectively use paid subscriptions for company financials and intelligence, patent databases, and import/export shipment-level trade views to validate supplier activity and component flows. These sources are not exhaustive, and many other public references were used to collect data points, confirm assumptions, and resolve definition gaps.

Primary Interviews and Surveys

Primary work is used to pressure-test the desk assumptions that tend to swing market value, such as what buyers count as a complete unit, typical capacity ranges, and how often deployments are expanded after pilots. We speak with a mix of manufacturers, system integrators, channel partners, and end users across APAC, EMEA, and the Americas so the final sizing reflects practical purchasing behavior and not only published shipment narratives.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 15% | APAC: 43% |

| Mid tier: 52% | Functional/Unit leaders: 36% | EMEA: 30% |

| Smaller Players: 15% | Managers: 49% | Americas: 27% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where data center and edge infrastructure demand is reconstructed by region and then filtered to micro mobile deployments using adoption and use-case shares confirmed in interviews. The model is kept practical by tying value to observable inputs, such as rollout pace of edge computing sites, average deployment cycle time for compact units, typical rack unit ranges used in the field, power and cooling configuration mixes, and the share of deployments linked to verticals like telecom, manufacturing, and government.

Once the demand pool is shaped, we corroborate totals with selective bottom-up checks, such as sampled average selling price bands multiplied by estimated unit volumes and channel feedback on annual run rates. Where bottom-up inputs are missing for smaller geographies, gaps are handled through proxy indicators like relative edge site additions and import intensity before the numbers are normalized back to the global total.

For forecasting, scenario analysis is applied around a base case that reflects consensus expectations from primary respondents, and then adjusted by region using drivers like latency-sensitive application growth, site-level power constraints, and capex timing. Assumptions are kept consistent across years by using the same unit economics logic and only updating variables that change, such as pricing progression and adoption curves.

Data Validation & Update Cycle

Validation is done by comparing modeled outputs against independent signals, including shipment and trade directionality, announced deployment programs, and the implied unit economics seen in real procurement cycles. Variance checks are run at region level and again at the global roll-up, and any outliers are reviewed before the final numbers are signed off.

Reports are refreshed annually, and interim updates are triggered when material events occur, such as sudden changes in supply availability, major policy shifts affecting data infrastructure, or sharp pricing moves in key components. Before delivery, a fresh analyst pass is completed so clients receive the latest updated view with consistent assumptions across the time series.

Mordor Intelligence's Micro Mobile Data Center Market Size Measured Against Other Published Estimates

Published market sizes for micro mobile data centers often differ because the product definition is not applied in the same way and because the timing of the base year varies across studies. Differences also come from how each estimate treats packaged infrastructure versus adjacent edge hardware and services, and from whether pricing is tracked as installed value or as shipment value.

In practical terms, the spread usually shows up when one source counts broader edge data center spend, or when it assumes faster price increases for integrated power and cooling without checking how projects are contracted. Another common gap comes from mixing rack-level micro data centers with larger containerized builds, and from using a different currency timing for conversion when regional demand is volatile.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 12.25 B (2026) | |

| Industry Research Group A | USD 6.34 B (2025) | Uses an earlier base year and a broader edge-computing framing, which can understate installed-value packages when only shipment-level pricing is applied. |

| Global Consultancy B | USD 6.44 B (2025) | Applies a wider segmentation lens that can blend micro mobile units with adjacent micro data center categories, and it may rely on longer-dated pricing assumptions for bundled power and cooling. |

The table shows that timing and what is counted as a complete deployable unit explain most of the gap. When the definition is kept to integrated, turnkey infrastructure with cloud connectivity and then checked against deployment signals, the estimate stays traceable to real demand drivers, which is the choice applied here by Mordor Intelligence.

Key Questions Answered in the Report

What is driving the rapid expansion of the micro mobile data center market?

Low-latency 5G services, exploding IoT data, and the need for resilient, distributed compute resources are propelling a 17.14% CAGR through 2031.

Which rack size is most popular for edge deployments?

The 25-40 RU category accounts for 39.45% of 2025 revenue and balances density with a footprint that fits retail back rooms, factories, and telecom sites.

How are SMEs benefiting from micro mobile data centers?

SMEs leverage turnkey, subscription-based enclosures that cut upfront capital, simplify management, and support local processing of sensitive data, leading to a 21.2% CAGR in this segment.

Why are lithium-ion batteries raising concerns in edge sites?

Thermal-runaway incidents, including a May 2025 fire in Oregon, have prompted stricter safety rules and wider adoption of off-gas detection and advanced ventilation.

Why are lithium-ion batteries raising concerns in edge sites?

Asia-Pacific is forecast to expand at an 18.1% CAGR as governments push smart-city and Industry 4.0 programs that depend on localized processing.

How concentrated is vendor competition?

The market scores 6 on a 1-10 scale; leading infrastructure providers control just over 60% of revenue, with smaller specialists rapidly closing the gap.

Page last updated on: