Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

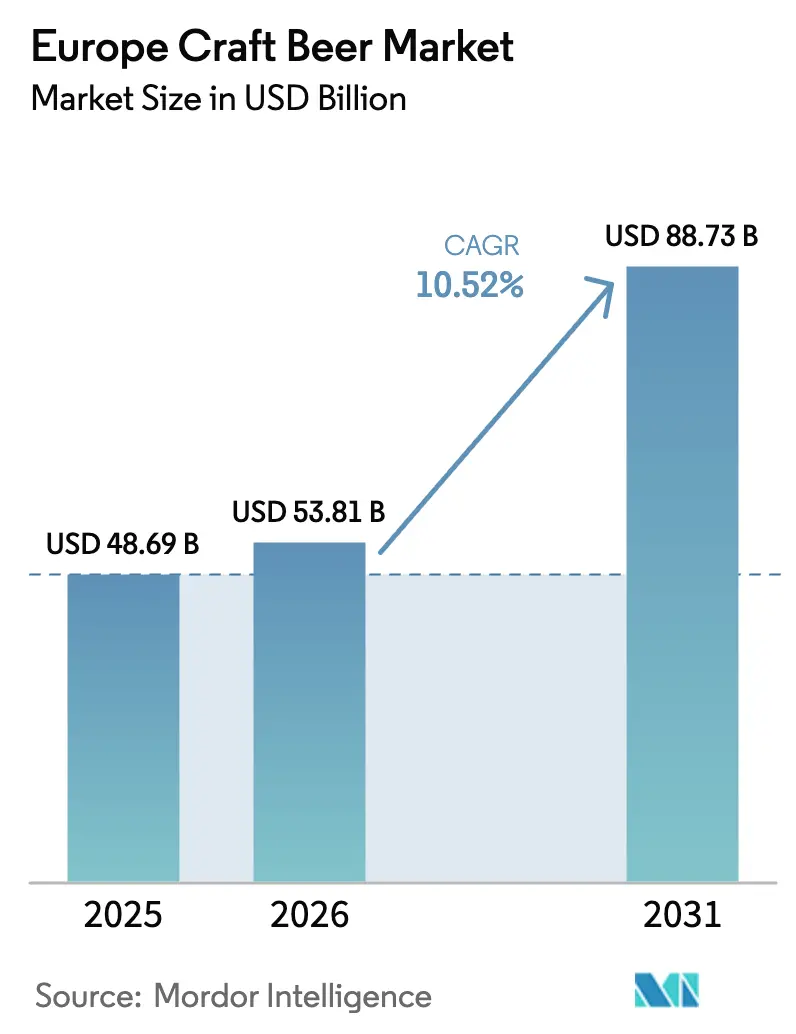

| Base Year Market Size (2025) | USD 48.69 Billion |

| Market Size (2026) | USD 53.81 Billion |

| Market Size (2031) | USD 88.73 Billion |

| Growth Rate (2026 - 2031) | 10.52% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Craft Beer Market Analysis by Mordor Intelligence

The Europe craft beer market size is expected to grow from USD 48.69 billion in 2025 to USD 53.81 billion in 2026 and is forecast to reach USD 88.73 billion by 2031 at 10.52% CAGR over 2026-2031. Premiumization is actively driving category value upward, supported by continuous flavor experimentation and the rapid growth of non-alcoholic styles. As mainstream lager volumes stabilize, these trends are reshaping the market. Cans have emerged as the dominant packaging choice, as they effectively reduce logistics costs and meet increasingly strict sustainability regulations. Retailers are actively creating craft-only aisles to replicate the exploratory experience of pubs, while breweries are expanding taprooms to strengthen hyperlocal demand. However, cost inflation and disparities in excise duties continue to challenge profitability. Larger brewers are addressing these challenges by acquiring smaller brands to enhance their authenticity. At the same time, agile microbreweries are capitalizing on opportunities by focusing on direct-to-consumer channels, ensuring they remain competitive in the evolving market landscape.

Key Report Takeaways

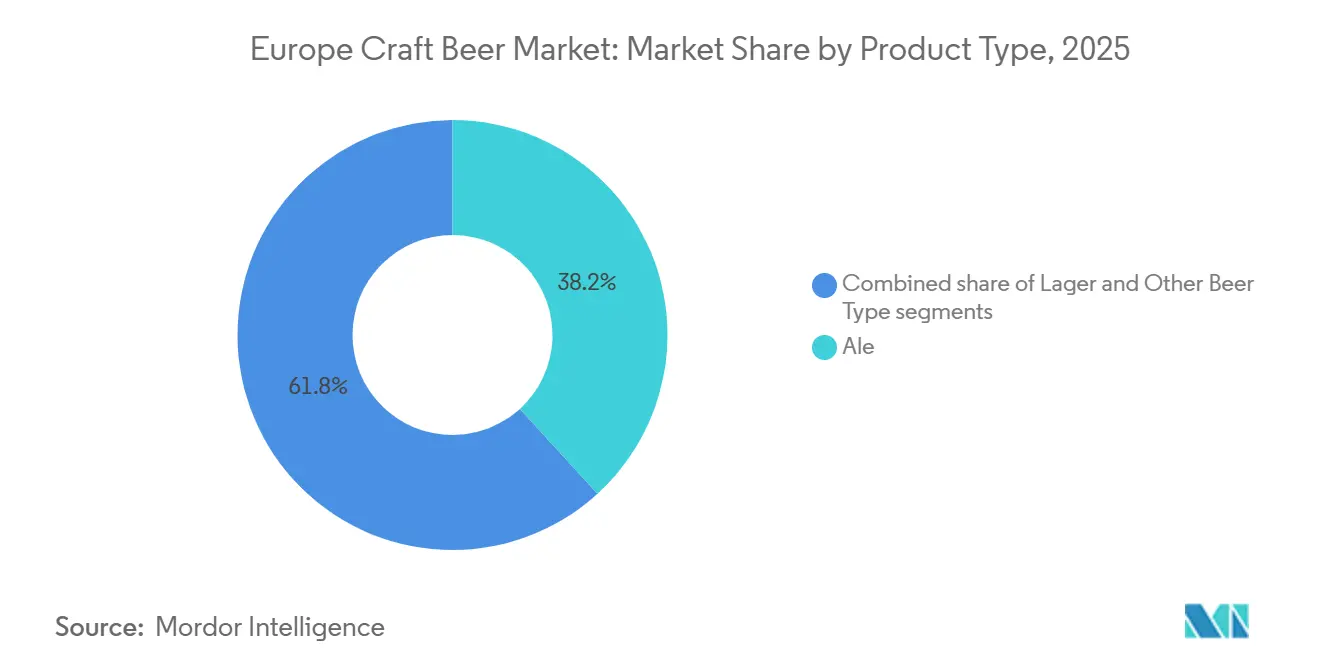

- By product type, ale led with 38.23% of the Europe craft beer market share in 2025, while lager is advancing at a 10.83% CAGR through 2031.

- By end user, men captured 68.31% of value in 2025, yet women are forecast to expand at an 11.23% CAGR to 2031.

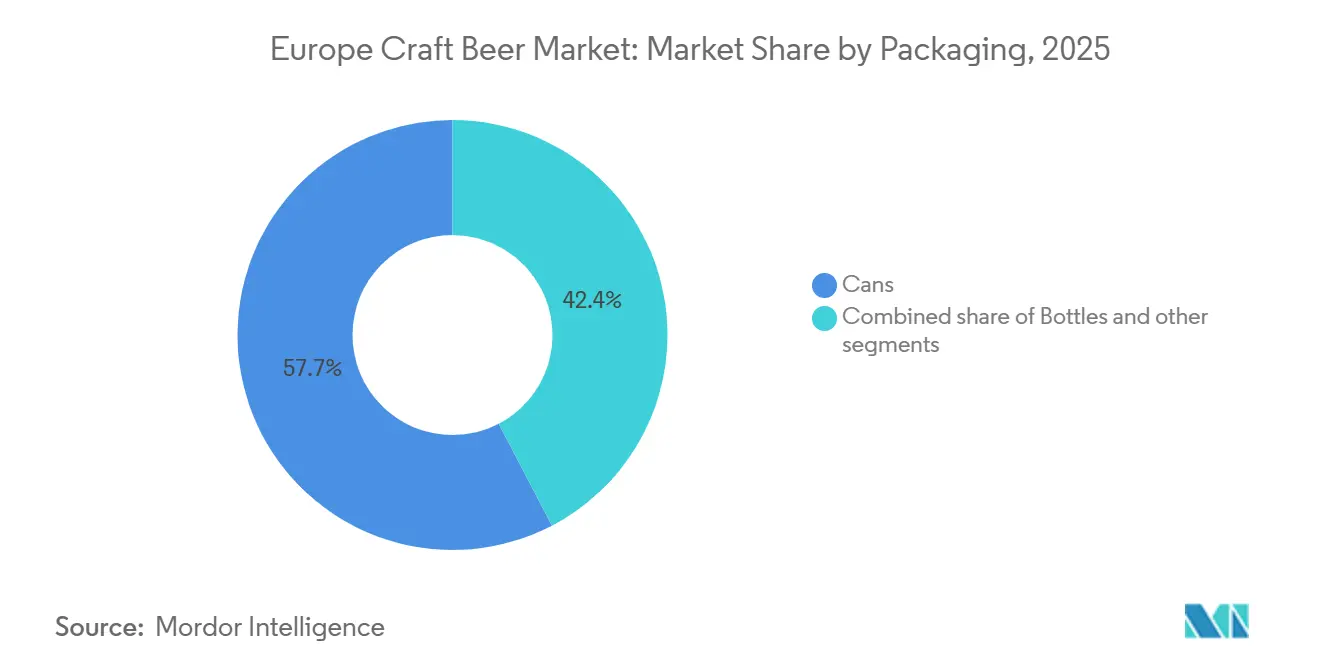

- By packaging, cans accounted for 57.65% of value in 2025 and are growing at a 10.67% CAGR through 2031.

- By distribution channel, on-trade held 62.04% value share in 2025, whereas off-trade is projected to post an 11.68% CAGR to 2031.

- By geography, the United Kingdom commanded 34.64% value in 2025, while Germany is the fastest-growing country at a 10.87% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Craft Beer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer preference for premium and artisanal beverages | +1.8% | Regional, with strongest uptake in UK, Belgium, Netherlands | Medium term (2-4 years) |

| Growing number of microbreweries and brewpubs across European countries | +1.5% | France, Spain, Italy (emerging); UK, Germany (mature saturation) | Long term (≥ 4 years) |

| Increasing demand for innovative flavors and experimental brewing styles | +1.2% | Urban centers across UK, Germany, Scandinavia; spillover to Eastern Europe | Short term (≤ 2 years) |

| Premiumization trend encouraging higher spending on specialty beverages | +1.0% | UK, Germany, France, Belgium, Netherlands | Medium term (2-4 years) |

| Increasing consumer interest in locally produced and authentic products | +0.9% | Regional strongholds: Bavaria, Yorkshire, Flanders; expanding to Poland, Spain | Long term (≥ 4 years) |

| Strong tourism and beer festival culture supporting craft beer awareness | +0.8% | Germany (Oktoberfest), Belgium (Beer Weekend), UK (GBBF), Czech Republic | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising consumer preference for premium and artisanal beverages

In Europe, a surge in consumer preference for premium and artisanal beverages has significantly propelled the craft beer market. Drinkers are increasingly favoring small-batch, flavorful brews over the traditional mass-produced lagers. Emphasizing authenticity, local sourcing, and craftsmanship, consumers are gravitating towards breweries that spotlight their origin stories, innovative recipes, and superior ingredients. This trend reflects a broader shift in consumer behavior, where quality and uniqueness are prioritized over quantity. With rising disposable incomes and a culture leaning towards experiential drinking, many are opting for pricier specialty beers. This includes IPAs, barrel-aged varieties, and seasonal releases, which offer distinct and memorable drinking experiences. Notably, urban millennials are at the forefront of this trend, showcasing a keen interest in diverse flavors and limited-edition launches. They are actively supporting taprooms, microbreweries, and beer festivals in major European cities, further driving the growth of the craft beer market.

Growing number of microbreweries and brewpubs across European countries

The growing number of microbreweries and brewpubs across European countries acted as a major driver for the Europe craft beer market, as it significantly expanded local production capacity and product diversity. This proliferation enabled more experimentation with beer styles, ingredients, and flavor profiles, catering to consumers seeking unique and regionally distinctive offerings. France emerged as one of the key examples, with over 2,500 microbreweries in 2024 and production reaching 24 million hectoliters, positioning the country as the fifth-largest beer producer in Europe[1]Source: Brasseurs de France, “Brewers' Harvest 2025! 14th edition!”, brasseurs-de-france.com. This rapid expansion illustrated how microbreweries helped shift the market away from standardized lagers toward differentiated craft products. In the United Kingdom, the momentum continued, with the total number of active breweries reaching 1,641 by the end of March 2025, as reported by the Society of Independent Brewers Association[2]Source: Society of Independent Brewers Association, “Number of Microbreweries in the UK”, siba.co.uk. This dense brewery network, spanning rural areas, towns, and major cities, strengthened local supply, shortened distribution chains, and fostered closer connections between brewers and consumers.

Increasing demand for innovative flavors and experimental brewing styles

Increasing demand for innovative flavors and experimental brewing styles acted as a strong driver for the market, as consumers moved beyond traditional lagers and pilsners toward more distinctive taste experiences. Brewers responded by developing a wide range of styles, including hop-forward IPAs, sour ales, barrel-aged beers, and fruit- or spice-infused variants, which appealed to curious and trend-driven drinkers. Limited editions and seasonal releases created a sense of novelty and urgency, encouraging repeat purchases and higher engagement with brands. Collaboration brews between local and international breweries further expanded flavor possibilities and helped transfer brewing knowledge across markets. This innovation wave also aligned with food-pairing trends in gastronomy, where complex craft beers complemented premium dining and street-food concepts. As a result, experimental brewing became a key differentiation tool for small and mid-sized breweries, allowing them to stand out against mainstream beer producers and capture value in premium price segments.

Strong tourism and beer festival culture supporting craft beer awareness

Strong tourism and a vibrant beer festival culture played a crucial role in supporting craft beer awareness across Europe, as visitors sought local, authentic drinking experiences that highlighted regional brewing traditions. Beer-focused events, city beer weeks, and brewery tours exposed international tourists to a wide variety of craft styles, helping small and independent producers gain visibility beyond their home markets. In major destinations such as Spain, a robust tourism base further amplified this effect; Spain’s travel and tourism sector was forecasted to reach EUR 260.5 billion in GDP contribution in 2025, equal to almost 16% of the national economy, underscoring the scale of potential exposure for local craft breweries through hospitality channels[3]Source: The World Travel & Tourism Council, “Spain's tourism sector could exceed €260 billion by 2025, according to WTTC”, wttc.org. As tourists discovered distinctive beers during their trips, they often translated this interest into repeat purchases and word-of-mouth promotion in their home countries. Beer festivals also acted as innovation showcases, where brewers tested new recipes, gathered consumer feedback, and built brand loyalty in a highly engaging environment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production and raw material costs impacting profitability of small breweries | -1.5% | Regional, acute in UK, Germany, France due to energy costs | Short term (≤ 2 years) |

| Limited distribution networks restricting market reach of independent brewers | -1.0% | Southern and Eastern Europe (Spain, Italy, Poland); rural UK, France | Medium term (2-4 years) |

| Strict alcohol taxation and regulatory compliance requirements across countries | -0.8% | High-tax jurisdictions: UK, Ireland, Netherlands, Finland | Long term (≥ 4 years) |

| Operational complexity due to small-batch and artisanal production methods | -0.5% | Regional, acute in Spain, Italy | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High production and raw material costs impacting profitability of small breweries

High production and raw material costs significantly constrained the profitability of small breweries in the Europe craft beer market. Rising prices of key inputs such as malt, hops, specialty yeasts, and energy increased per-unit production costs, which were harder to absorb at low volumes. Small brewers lacked the purchasing power and long-term supplier contracts enjoyed by large multinationals, so they often paid higher prices and faced more volatile input costs. Investment in quality equipment, packaging, and compliance with stringent food safety and environmental regulations further added to fixed cost burdens. Because many craft beers used premium or experimental ingredients, their recipes were inherently more expensive to produce than standard lagers. Passing these costs on to consumers via higher prices risked narrowing the customer base, especially in price-sensitive markets or economic downturns. Limited access to financing also restricted the ability of small breweries to modernize, scale up, or improve efficiency, keeping unit costs elevated.

Limited distribution networks restricting market reach of independent brewers

Limited distribution networks restricted the market reach of independent brewers in Europe, limiting their ability to compete with large, established beer companies. Many craft breweries relied on local taprooms, nearby bars, and small retailers, which constrained volume growth and brand visibility. Access to national retail chains and export channels often required scale, consistent supply, and strong negotiating power, which smaller brewers frequently lacked. In several markets, long-term agreements between major breweries and distributors or on-trade outlets further reduced shelf and tap space available for craft products. Logistics costs for cold-chain, small-batch, and geographically dispersed deliveries also made broader distribution less economical for independents. As a result, many promising craft brands remained regionally concentrated despite strong consumer interest.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Lager Narrows the Gap with Ale

Ale accounted for the largest share of the Europe craft beer market in 2025, representing 38.23% of total market revenue. The dominance of ale can be attributed to its wide variety of styles, flavors, and brewing techniques that appeal strongly to craft beer consumers seeking diversity and authenticity. Many craft breweries prioritize ale production due to shorter fermentation times and greater flexibility for experimentation with ingredients and flavor profiles. Consumer preference for bold, aromatic, and specialty beers has further strengthened the position of ales across both on-trade and off-trade channels. Additionally, the strong presence of pale ales, IPAs, and specialty seasonal variants has supported consistent demand across key European markets.

Lager is emerging as the fastest-growing segment in the Europe craft beer market and is projected to expand at a CAGR of 10.83% through 2031. The growth of craft lager is largely driven by increasing consumer demand for lighter, more refreshing beer options that offer both quality and drinkability. Craft brewers are increasingly introducing premium and specialty lagers that combine traditional brewing methods with modern flavor innovation. The segment is also benefiting from the transition of mainstream beer consumers toward craft alternatives without significantly changing taste preferences. Improved brewing technologies have enabled smaller breweries to produce high-quality lagers more efficiently, supporting wider product availability.

By End User: Women Drive Incremental Growth

Men accounted for the largest share of the Europe craft beer market by end user in 2025, contributing 68.31% of total market value. This substantial share reflects the traditionally higher beer consumption rates among male consumers across many European countries. Craft beer brands have historically targeted male demographics through product positioning, flavor intensity, and marketing strategies centered on heritage and brewing craftsmanship. Established social drinking cultures and strong participation of men in beer festivals, pub gatherings, and tasting events have further reinforced this dominance. Additionally, men tend to exhibit higher brand loyalty within the craft segment, supporting consistent repeat purchases. The broad acceptance of diverse ale and specialty beer styles among male consumers continues to underpin their leading contribution to overall market revenue.

Women represent the fastest-growing end-user segment in the Europe craft beer market and are projected to expand at a CAGR of 11.23% through 2031. This accelerated growth is driven by changing social norms, rising disposable incomes, and increasing participation of women in premium beverage consumption. Craft breweries are introducing lighter, fruit-infused, low-alcohol, and aesthetically branded options that appeal to evolving female preferences. Marketing strategies are also becoming more inclusive, moving away from traditionally male-focused branding toward gender-neutral and experience-driven positioning. Growing interest in artisanal, locally produced, and premium beverages among women is further stimulating demand.

By Packaging: Cans Consolidate Leadership Through Sustainability

In 2025, cans captured a dominant 57.65% market share and are expected to grow at a strong 10.67% CAGR from 2026 to 2031. Their growth stems from superior light and oxygen barriers, which preserve product quality, and their logistical efficiency, which reduces costs. Aluminum's impressive 75% average recycling rate in the EU aligns with breweries' efforts to disclose carbon footprints, allowing brands to showcase measurable environmental benefits to eco-conscious consumers. Lightweight can formats further enhance sustainability by cutting freight emissions and minimizing breakage costs. These advantages enable smaller producers to expand their retail presence while maintaining product quality and reducing operational expenses.

Advancements in liner technology now protect delicate hop oils, addressing previous concerns about flavor loss that once made glass the preferred choice. Custom shrink-sleeves and advanced digital printing techniques provide a boutique aesthetic, effectively challenging the perception that only bottles convey a premium image. Although returnable bottle schemes still exist, deposit-return legislation increasingly favors cans due to their ease of sorting and recycling. Consequently, craft breweries are increasingly installing canning lines in new facilities, reinforcing the dominance of cans and positioning them as a key driver in the next phase of growth for Europe's craft beer market.

By Distribution Channel: Off-Trade Gains as Retail Premiumizes

On-trade distribution accounted for the largest share of the Europe craft beer market in 2025, holding 62.04% of total market value. The strong performance of this segment is primarily driven by the deep-rooted pub and bar culture across many European countries, where consumers prefer experiencing craft beer in social settings. Brewpubs, taprooms, restaurants, and specialty bars play a crucial role in promoting craft beer by offering fresh brews and a wide variety of styles on tap. Consumers often associate on-trade venues with product discovery, tasting experiences, and brand engagement, which strengthens sales within this channel. In addition, collaborations between breweries and hospitality operators help expand product visibility and encourage trial among new consumers.

Off-trade distribution is projected to be the fastest-growing segment in the Europe craft beer market, expanding at a CAGR of 11.68% through 2031. The growth of this segment is supported by increasing availability of craft beer across supermarkets, specialty retail stores, and online platforms. Changing consumption patterns, including at-home drinking and convenience-driven purchasing behavior, are encouraging consumers to buy craft beer for personal consumption. Retailers are also expanding shelf space for craft brands, enabling wider product accessibility and brand exposure. The rise of e-commerce and direct-to-consumer sales channels has further accelerated off-trade growth by improving product reach beyond traditional venues.

Geography Analysis

The United Kingdom accounted for the largest share of the Europe craft beer market in 2025, contributing 34.64% of total market value. The country’s leadership position is supported by a well-established craft brewing culture and a high concentration of microbreweries and independent brewers. Strong consumer acceptance of premium and locally produced beer has encouraged continuous product innovation and brand diversification. The widespread presence of pubs, taprooms, and beer festivals has also played a significant role in promoting craft beer consumption across different consumer groups. In addition, the mature retail and hospitality infrastructure enables efficient product distribution and strong brand visibility.

Germany is projected to be the fastest-growing country in the Europe craft beer market, registering a CAGR of 10.87% through 2031. Growth in the German market is largely driven by evolving consumer preferences beyond traditional beer styles toward more diverse and innovative craft offerings. While Germany has a long-standing brewing heritage, younger consumers are increasingly exploring specialty beers, limited editions, and modern flavor profiles. The rise of independent breweries and craft-focused taprooms is further supporting market expansion. Increasing exposure to international craft beer trends and collaborations between local and global brewers are also contributing to accelerated growth.

Other European countries, including Spain, Italy, and France, are also demonstrating steady development within the Europe craft beer market. These countries are experiencing rising consumer interest in premium and locally produced beverages, supported by growing tourism and expanding urban hospitality sectors. The increasing number of small and independent breweries has strengthened product diversity and regional identity in craft beer offerings. Consumers in these markets are gradually shifting from mass-produced beer toward specialty and artisanal alternatives, encouraging innovation among brewers. Retail expansion and improved availability through supermarkets and specialty stores are further supporting market penetration.

Competitive Landscape

The European craft beer market operates with a fragmented structure, but consolidation is increasing as major brewing companies actively acquire craft brands. At the same time, independent breweries are driving innovation by adopting advanced technologies and implementing direct-to-consumer strategies. Although acquisition activities are on the rise, the market remains relatively unconcentrated. Heineken exemplifies a dual strategy by both developing its own craft brands organically and strategically acquiring independent breweries to expand its portfolio. Key players shaping the market include BrewDog PLC, Heineken Holding N.V., Anheuser-Busch InBev, Mikkeller A/S, and Molson Coors Beverage Company.

European Union directives have standardized regulations, significantly transforming the competitive dynamics of the craft beer market. These directives have introduced unified certification systems, which simplify compliance processes for smaller producers, reducing their administrative and operational challenges. Additionally, tax rate reductions across various member states have provided smaller breweries with notable financial benefits. By implementing these regulatory measures, the EU has created a more equitable competitive environment, empowering independent breweries to compete more effectively against larger, corporate-owned craft beer operations.

Craft breweries are actively leveraging opportunities at the intersection of sustainability and direct consumer engagement to differentiate themselves from mass-market alternatives. They are prioritizing environmental sustainability and creating unique consumer experiences to stand out in the market. For example, indoor hop cultivation technology allows craft breweries to achieve supply chain independence while producing higher-quality raw materials. Spanish breweries have demonstrated the effectiveness of this approach by achieving higher alpha acid content in hops grown indoors compared to those cultivated using traditional field methods. This innovation highlights how craft breweries are combining sustainability with quality to gain a competitive edge.

Europe Craft Beer Industry Leaders

Anheuser-Busch InBev

Molson Coors Beverage Company

BrewDog Plc

Heineken Holding N.V

Mikkeller A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Fierce Beer entered an exclusive collaboration with ASDA, becoming the sole Scottish brewery invited to contribute to ASDA’s “Collab Collection.” The partnership includes the launch of the Fierce West Coast IPA (6.2% ABV), now available in over 350 ASDA stores nationwide, expanding the brand’s retail footprint and visibility in the UK market.

- October 2025: Augustiner‑Bräu’s Helles lager is being introduced on draught in the UK for the first time through a long‑term exclusive import and distribution agreement with James Clay & Sons. This development marks a strategic expansion of Augustiner’s presence in the British market, offering Munich’s historic and highly regarded lager style to UK on‑trade venues.

- June 2025: HEINEKEN opened a global research and development center in the Netherlands to drive brewing innovations and advance next-generation product development. The EUR 45 million investment highlights HEINEKEN's role as a pioneer in the beer industry and its commitment to maintaining leadership in the Dutch food technology sector.

- May 2025: BrewDog, the Scottish craft brewery, has revamped the branding of its core beer lineup. This update includes well-loved variants like Punk IPA, Hazy Jane, Lost Lager, and Elvis Juice. The signature BrewDog brandmark and its color palette remain consistent, but each beer now features a unique aesthetic, boosting its shelf presence and recognizability.

Europe Craft Beer Market Report Scope

Craft beers are the ones that are prepared in a brewery that produces small amounts of beer, typically less than large breweries, and are often independently owned. Such breweries are generally perceived and marketed as having an emphasis on new flavors, and varied brewing techniques. The Europe craft beer market is segmented by product type, end user, paclaging type, distribution channel, and geography. Based on the product type, the market is segmented into ale, lager and other beer types. Based on end user, the market is segmented into men and women. Based on packaging type, the market is segmented into bottles, cans and others. Based on distribution channel, the market is segmented into on-trade and off-trade. Based on geography, the market is segmented into United Kingdom, Germany, France, Italy, Spain, Russia, Sweden, Belgium, Netherlands, Poland and Rest of Europe. For each segment, the market sizing and forecasts have been done on the basis of value (in USD billion) and Volume (Liters).

By Product Type

| Ale |

| Lager |

| Other Beer Types (Specialty Beers) |

By End User

| Men |

| Women |

By Packaging

| Bottles |

| Cans |

| Others |

By Distribution Channel

| On-Trade |

| Off-Trade |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Russia |

| Sweden |

| Belgium |

| Poland |

| Netherlands |

| Rest of Europe |

| By Product Type | Ale |

| Lager | |

| Other Beer Types (Specialty Beers) | |

| By End User | Men |

| Women | |

| By Packaging | Bottles |

| Cans | |

| Others | |

| By Distribution Channel | On-Trade |

| Off-Trade | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe craft beer market in 2026?

It is valued at USD 53.81 billion, on track to reach USD 88.73 billion by 2031.

Which country is expanding fastest?

Germany is projected to post the highest CAGR at 10.87% between 2026 and 2031, driven by non-alcoholic craft variants and export demand.

Why are cans overtaking bottles in Europe’s craft segment?

Deposit-return laws, lighter weight that cuts freight costs, and innovations like Carlsberg’s snap-pack make cans the most sustainable and economical option.

What is the biggest growth opportunity by consumer group?

Women, forecast to rise at an 11.23% CAGR, offer the largest incremental value through flavored stout and lower-ABV styles.

Which distribution channel is set to grow the quickest?

Off-trade retail, supported by craft-dedicated supermarket aisles and e-commerce, is expected to expand at an 11.68% CAGR through 2031.

Page last updated on: