Lager Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

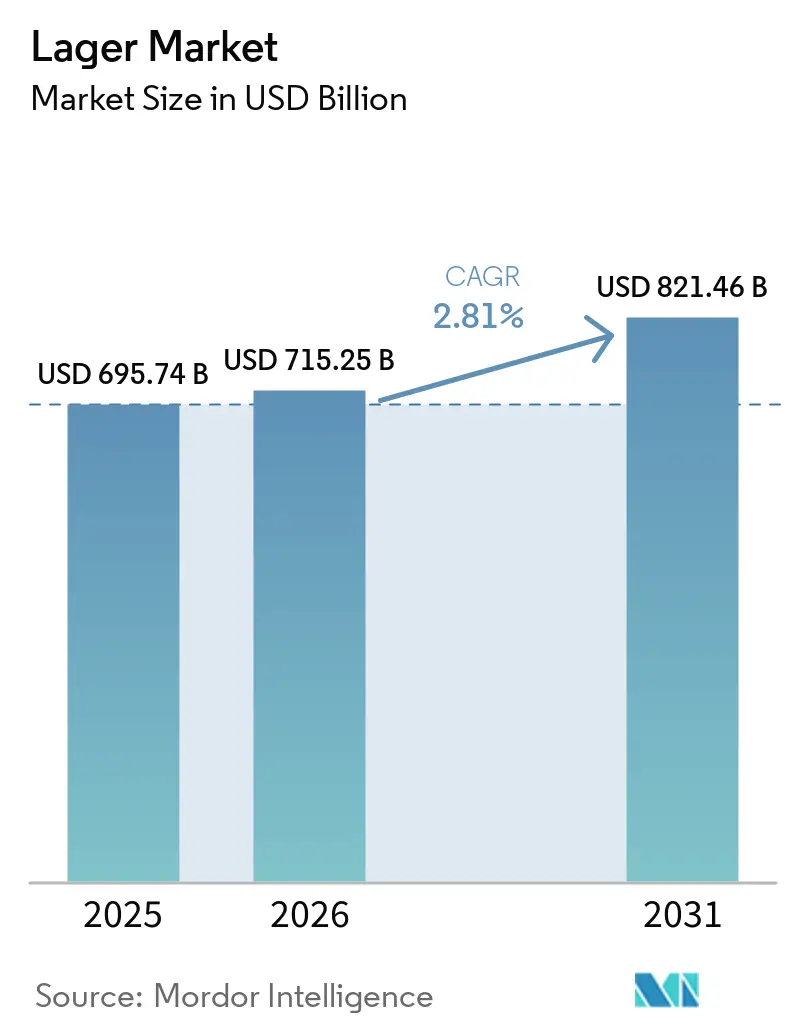

| Market Size (2026) | USD 715.25 Billion |

| Market Size (2031) | USD 821.46 Billion |

| Growth Rate (2026 - 2031) | 2.81% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lager Market Analysis by Mordor Intelligence

The global lager market size expected to grow from USD 695.74 billion in 2025 to USD 715.25 billion in 2026 and is forecast to reach USD 821.46 billion by 2031 at 2.81% CAGR over 2026-2031. The global lager market is driven by its widespread consumer appeal, offering a light, crisp taste with lower bitterness that caters to varied preferences across regions. Increasing urbanization and rising disposable incomes, especially in emerging economies, are contributing to higher on-trade consumption in bars, restaurants, and social settings. Furthermore, strong brand recognition and extensive distribution networks of major brewers improve product accessibility and visibility globally. Innovations such as premium, craft-inspired, and low- or no-alcohol lagers are attracting health-conscious and younger consumers. Additionally, increased marketing efforts, event sponsorships, and the growth of modern retail channels continue to support consistent market growth.

Key Report Takeaways

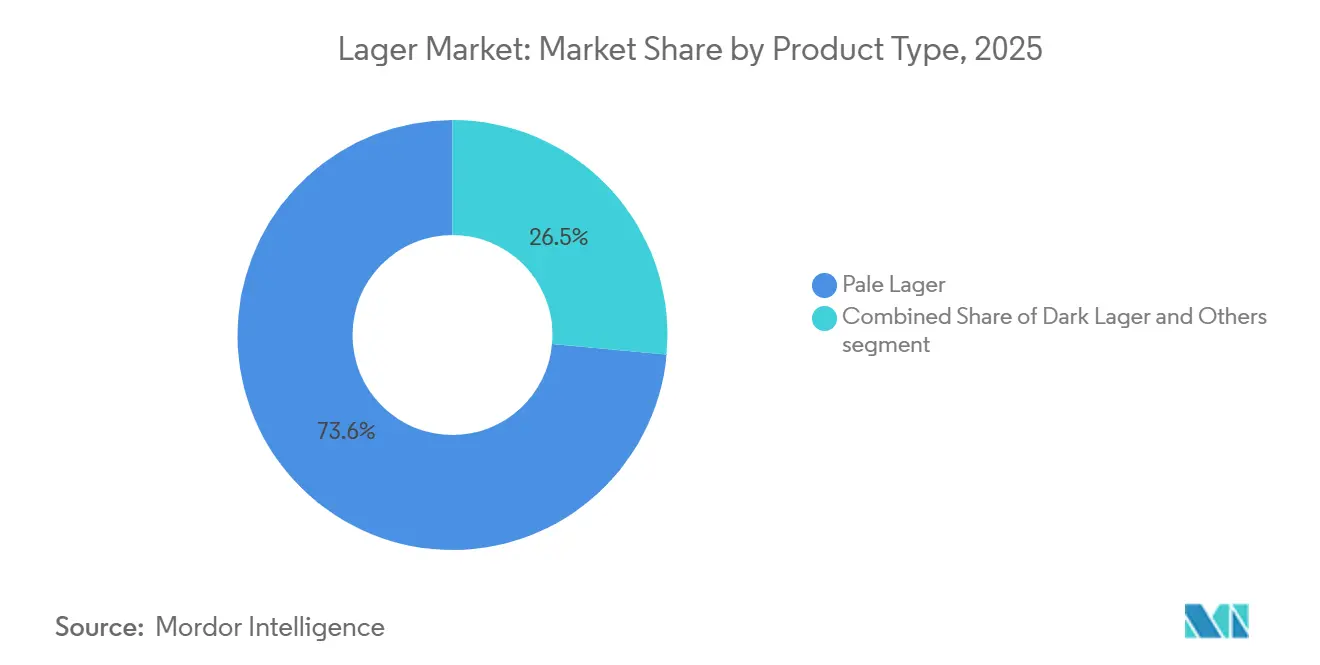

- By product type, pale lager led with 73.55% of the 2025 lager market share, while dark lager is expanding at a 3.45% CAGR through 2031.

- By category, standard lager accounted for 59.33% of the 2025 share, whereas premium lager is forecast to advance at a 4.44% CAGR over 2026-2031.

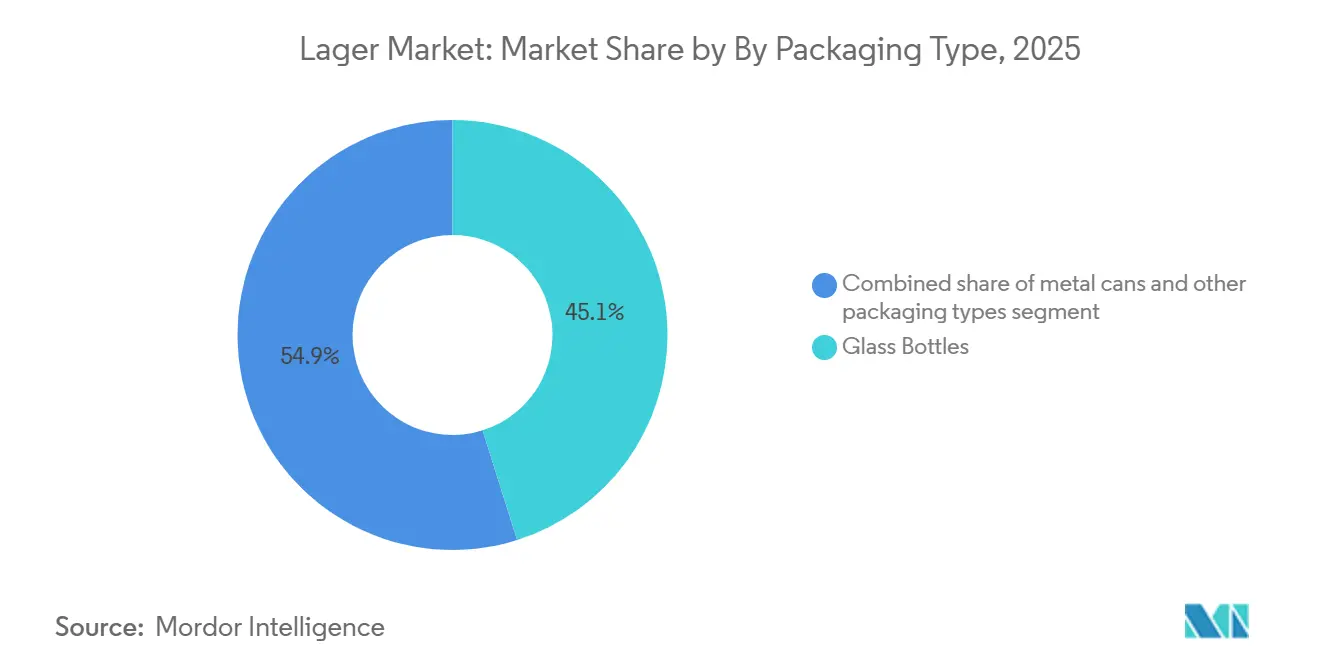

- By packaging, glass bottles held 45.14% share in 2025, yet metal cans are set to grow at a 3.81% CAGR during the forecast period.

- By distribution, off-trade captured 61.05% in 2025, while on-trade is recovering at a 3.76% CAGR over 2026-2031.

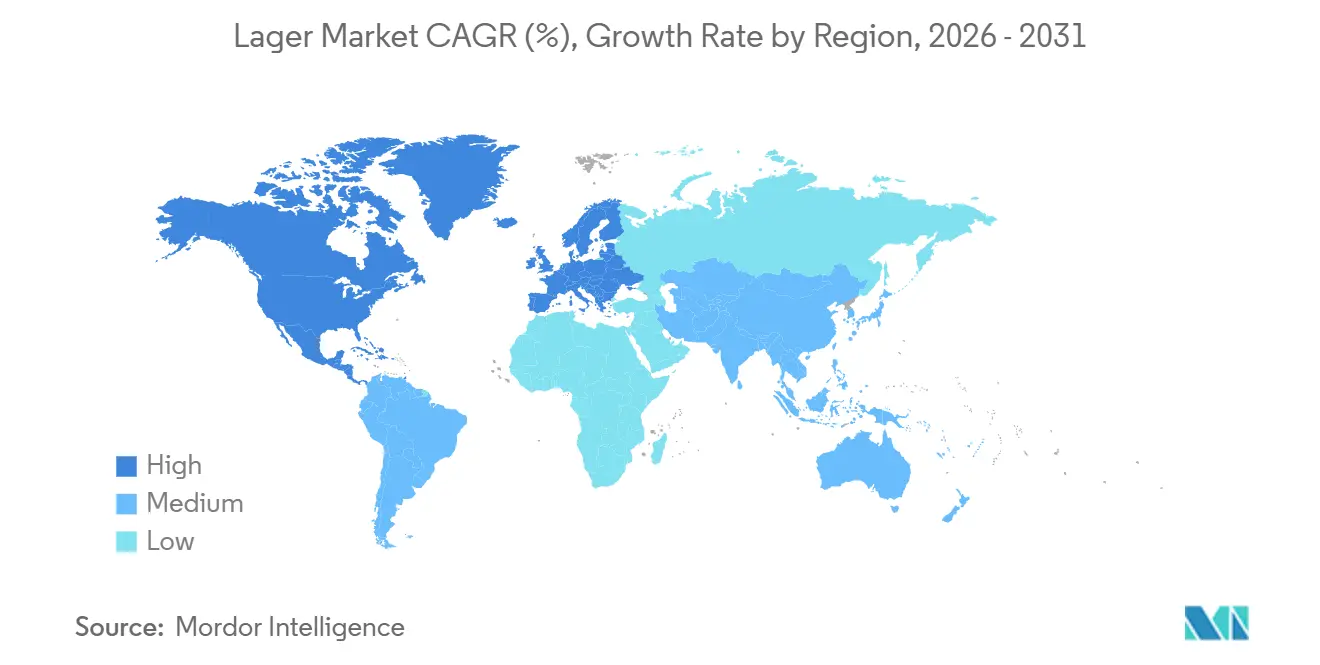

- By geography, Europe controlled 44.64% of the 2025 value; however, Asia-Pacific is projected to rise at a 5.05% CAGR, the fastest globally.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Lager Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise of craft and specialty lagers | +0.3% | North America, Europe (Germany, United Kingdom, Belgium), Australia | Medium term (2-4 years) |

| Product innovation and flavor diversification | +0.4% | Global, with early adoption in North America, Western Europe, Japan | Short term (≤ 2 years) |

| Expansion of low and non-alcoholic lagers | +0.5% | Europe (United Kingdom, Germany, Netherlands), North America, Middle East | Short term (≤ 2 years) |

| Premiumization and brand storytelling | +0.6% | Global, strongest in Asia-Pacific (China, India), Europe, urban centers | Medium term (2-4 years) |

| Growth of microbreweries and craft beer brands | +0.2% | North America (United States, Canada), Europe (United Kingdom, Germany, Belgium), Australia | Long term (≥ 4 years) |

| Advancements and innovation in brewing technologies | +0.3% | Global, led by Europe and North America; spillover to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise of craft and specialty lagers

Craft and specialty lagers are reshaping consumer expectations by combining traditional brewing techniques with innovative ingredients, offering margin opportunities that mass-market brands find challenging to replicate. Brewers are revitalizing heritage styles such as Czech pilsners, German helles, and Vienna lagers, while incorporating modern techniques like dry-hopping and barrel-aging to achieve premium pricing. This trend is particularly evident in North America and Western Europe, where consumers associate craft origins with authenticity and quality. The growing preference for specialty lagers also benefits major brewers acquiring craft labels, enabling them to tap into premiumization without impacting core volumes. For example, Asahi's 2024 acquisition of Octopi Brewing aimed to localize production and reduce logistics costs. In Europe, craft brewers are utilizing Protected Geographical Indication (PGI) certifications to reinforce authenticity and support price premiums, especially in countries like Germany and Belgium, where brewing traditions are deeply rooted. The rise of craft lagers reflects a shift in value rather than volume, as consumers opt for higher-quality options within the lager category rather than moving away from it entirely.

Product innovation and flavor diversification

Product innovation remains a key strategy for maintaining shelf space and capturing additional consumption occasions as baseline lager demand stagnates. Heineken's USD 47.82 million R&D center, inaugurated in 2024, is dedicated to yeast strain optimization and sensory profiling, aiming to reduce time-to-market for limited-edition products. Flavor diversification is expanding beyond traditional lager boundaries, incorporating fruit infusions (such as citrus and tropical flavors), botanical blends (like elderflower and hibiscus), and hybrid formats (e.g., lager-spritz combinations). These innovations are designed to appeal to younger consumers and female demographics, who have traditionally preferred wine and spirits. The pace of innovation is accelerating as retailers prioritize shelf space based on product velocity and novelty, compelling brewers to update SKUs every 6-12 months to avoid delisting. Additionally, flavor diversification serves a strategic role by fragmenting the competitive landscape, complicating direct price comparisons, and allowing brewers to experiment with higher price points under the framework of premiumization. Regulatory compliance is also a critical factor. EU labeling regulations now require ingredient disclosure and nutritional information, increasing formulation complexity. However, this also presents an opportunity for brands to differentiate through transparency and clean-label positioning, provided they are willing to invest in these areas.

Expansion of low‑ and non‑alcoholic lagers

Low and non-alcoholic lagers are the fastest-growing subsegment within the beer category, driven by health-conscious consumers, stricter drink-driving regulations, and cultural shifts toward moderation. According to the AACR Cancer Progress Report 2024, fewer than half of Americans are aware that alcohol consumption can increase cancer risk. The report further highlights that approximately 5.4% of all cancer cases diagnosed in the United States are attributed to alcohol consumption. This has prompted government campaigns promoting alcohol-free alternatives[1]Source: American Association for Cancer Research, “How Does Alcohol Consumption Impact Cancer Risk?,” aacr.org. Additionally, technological advancements in dealcoholization methods, such as vacuum distillation, reverse osmosis, and arrested fermentation, have significantly improved taste profiles, addressing the "wort-like" flavor issues found in earlier versions. The Middle East presents a distinct growth opportunity, as cultural and religious norms favor non-alcoholic beverages while consumers still seek the social experience associated with beer consumption. This has driven demand for zero-alcohol lagers that closely replicate the taste of full-strength variants. Furthermore, premiumization trends are also evident, with non-alcoholic lagers retailing at 70-90% of the price of full-strength beers, allowing brewers to maintain margins while expanding their addressable markets.

Growth of microbreweries and craft beer brands

The growth of microbreweries and craft beer brands is a significant driver of the global lager market, as these entities are influencing consumer preferences by offering innovative, high-quality, and locally inspired lager options. Craft brewers are increasingly experimenting with ingredients, brewing methods, and flavor profiles, elevating lager from a mass-produced beverage to a premium, artisanal product category. This shift is appealing to younger consumers and urban drinkers who seek unique taste experiences while appreciating the smooth and approachable qualities of lager. Furthermore, the expansion of microbreweries is enhancing local distribution and on-trade consumption, contributing to increased market penetration. For example, the Brewers Association reported that the number of small and independent breweries operating in the United States reached 9,778 in 2025, underscoring the strong growth of craft brewing and its global impact on lager innovation and demand[2]Source: Brewers Association, “The 2025 Year in Beer,” brewersassociation.org.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising awareness of alcohol-related health risks | -0.4% | Global, most acute in Europe (United Kingdom, Nordics), North America, Australia | Short term (≤ 2 years) |

| Competition from non-alcoholic and low-alcohol alternatives | -0.3% | Europe (United Kingdom, Germany, Netherlands), North America, Middle East | Medium term (2-4 years) |

| Regulatory restrictions on alcohol | -0.3% | Europe (United Kingdom, Scotland, Ireland), North America, select Asia-Pacific markets | Medium term (2-4 years) |

| Shifting consumer preferences toward spirits and RTD cocktails | -0.5% | North America (United States, Canada), Australia, urban centers globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising awareness of alcohol‑related health risks

Public health campaigns highlighting the links between alcohol consumption and health risks such as cancer, cardiovascular disease, and liver damage are reducing the social acceptability of regular drinking, particularly among younger demographics who emphasize wellness and longevity. The United Kingdom's Chief Medical Officer updated drinking guidelines to recommend a maximum of 14 units per week, emphasizing that any level of alcohol consumption carries some risk[3]Source: Department of Health (United Kingdom), “UK Chief Medical Officers’ Low Risk Drinking Guidelines,” assets.publishing.service.gov.uk. This has influenced consumer behavior, encouraging moderation and abstinence. The health-risk narrative has been especially impactful in Northern Europe and Australia, where government-funded campaigns and medical endorsements hold significant influence. Younger consumers, including Gen Z and younger Millennials, are increasingly adopting "sober curious" lifestyles, perceiving lager as incompatible with their fitness, mental health, and productivity goals. This demographic shift poses a challenge to the long-term viability of the lager market, as consumption habits formed in early adulthood often persist over time. In response, brewers are investing in functional beverages and beyond-beer alternatives, such as hard seltzers, kombucha, and CBD-infused drinks.

Regulatory restrictions on alcohol

Regulatory restrictions on alcohol serve as a significant constraint on the global lager market. Governments in many countries enforce stringent policies governing production, distribution, marketing, and consumption. These measures often include higher excise duties, restricted sales hours, age limitations, advertising prohibitions, and licensing requirements, all of which increase operational costs for breweries and limit consumer access to products. Additionally, public health initiatives in several regions are intensifying compliance standards and promoting reduced alcohol consumption through awareness campaigns and warning labels. These regulatory challenges not only hinder market expansion but also pose entry barriers for new participants and smaller breweries, ultimately slowing the growth of the lager market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dark Lager Gains as Consumers Rediscover Malt

Pale lager accounted for 73.55% of the market in 2025, reflecting its widespread appeal, ease of consumption, and alignment with mass-production efficiencies. This dominance is attributed to its light flavor profile, which appeals to a broad consumer base, and its suitability for large-scale production and distribution. However, dark lager is the fastest-growing product type, with a CAGR of 3.45% projected through 2031. This growth is driven by consumer interest in richer, malt-forward profiles that offer differentiation from the more common pale variants.

Dark lagers, including Munich dunkels, schwarzbiers, and Vienna-style lagers, are gaining traction due to the craft movement's focus on heritage styles and complex flavors. These styles are often marketed as premium products, appealing to consumers seeking unique and high-quality beer options. Brewers are positioning these as premium alternatives to standard pale lagers. Meanwhile, pale lagers continue to dominate the category, supported by global brands such as Budweiser, Heineken, Corona, and Tsingtao, which capitalize on economies of scale, extensive distribution networks, and strong brand recognition to maintain their market share.

By Category: Premium Lager Outpaces Standard

In 2025, standard lager accounted for 59.33% of the category share, catering to price-sensitive consumers and high-volume on-premise accounts. The affordability of standard lagers makes them a preferred choice for consumers seeking value for money, especially in markets where economic constraints influence purchasing decisions. Additionally, their widespread availability and established presence in both retail and on-premise channels contribute to their dominance in the category. Brewers are focusing on optimizing production efficiency and streamlining SKU portfolios. Meanwhile, luxury lagers, though a niche subsegment, are experiencing growth in on-premise channels where consumers prioritize experiences over price sensitivity. These products, often presented as limited-edition releases in embossed glass bottles and priced above USD 10 per unit, target affluent urban consumers and special occasions.

Premium lager is projected to grow at a CAGR of 4.44% through 2031, driven by increasing consumer preference for products associated with higher quality and sophistication. Factors such as brand heritage, premium packaging, and the perception of superior quality play a significant role in attracting consumers. The growing disposable incomes in regions like Asia-Pacific, particularly in China and India, further fuel demand for premium lagers, as consumers increasingly associate these products with status and lifestyle aspirations. The premiumization strategy requires disciplined distribution practices, including selective retail partnerships, controlled on-premise placements, and consistent above-the-line marketing efforts to preserve brand equity and avoid dilution through discounting. Additionally, brewers are incorporating sustainability initiatives, such as carbon-neutral brewing and regenerative agriculture, to justify premium pricing and align with consumer preferences for environmental responsibility.

By Packaging Type: Metal Cans Gain on Sustainability and Portability

Glass bottles accounted for 45.14% of the packaging market share in 2025, driven by their association with on-premise traditions and consumer perceptions of quality. Glass bottles are particularly favored in settings such as restaurants, bars, and hotels, where presentation and ritual play a significant role in enhancing the consumer experience. Additionally, in markets like Germany, deposit-return schemes that support refillable glass bottles further bolster their usage. The premium image associated with glass packaging also appeals to consumers seeking high-quality products, making it a preferred choice for many beverage manufacturers targeting the premium segment.

Metal cans are the fastest-growing packaging format, with a CAGR of 3.81% projected through 2031. This growth is primarily driven by sustainability mandates, as aluminum cans have a 61% lower lifecycle carbon footprint compared to PET bottles in high-recycling scenarios, according to lifecycle assessments. Their lightweight and durable nature enhances supply chain efficiency, while their portability makes them ideal for off-trade and outdoor consumption occasions. These attributes, combined with their recyclability, make aluminum cans a preferred choice for brewers and beverage manufacturers aiming to meet net-zero commitments and cater to environmentally conscious consumers.

By Distribution Channel: On-Trade Rebounds as Hospitality Recovers

Off-trade channels accounted for 61.05% of distribution in 2025, reflecting a structural shift toward at-home consumption. The growth of off-trade is driven by factors such as the convenience of purchasing from retail outlets, the increasing adoption of e-commerce platforms, and the rising preference for at-home consumption due to lifestyle changes. Additionally, the availability of a wide variety of products in retail stores and the cost-effectiveness of off-trade purchases compared to on-trade options further support its expansion. E-commerce, a subset of off-trade, is growing rapidly in Asia-Pacific and North America, facilitating direct-to-consumer sales and subscription-based models.

On-trade is recovering, with a projected CAGR of 3.76% through 2031, driven by the increasing hospitality venues, rising tourism, and consumers' preference for social experiences outside the home. On-premise sales typically achieve 30-50% higher margins than retail sales due to lower price sensitivity and the premium consumers pay for ambiance and service. The resurgence of on-trade is also supported by the growing demand for experiential dining and drinking, as well as the increasing focus of hospitality venues on enhancing customer experiences through improved service and unique offerings. Moreover, brewers are increasingly investing in hybrid models, such as branded retail experiences and taprooms attached to breweries, to engage with both channels. These approaches enable brewers to build direct consumer relationships, bypass traditional wholesale intermediaries, and improve margin capture.

Geography Analysis

Europe accounted for 44.64% of the market share in 2025, driven by a strong beer-drinking culture, a well-established brewing heritage, and high per capita consumption in countries such as Germany and the Czech Republic. Consumers are increasingly favoring premium and craft lagers, supported by the growing number of microbreweries and innovations in flavors and brewing techniques. The expansion of low- and no-alcohol lagers is also gaining momentum due to rising health awareness and strict drink-driving regulations. Additionally, the widespread availability of lagers across supermarkets, pubs, and festivals, along with strong tourism and social drinking occasions, continues to support steady demand.

Asia-Pacific is the fastest-growing region, with a 5.05% CAGR projected through 2031, driven by rapid urbanization, rising disposable incomes, and a growing young population in countries like China and India. Lager remains the most popular beer type due to its light and refreshing profile, which aligns with warmer climates and evolving consumer preferences. The increasing westernization of lifestyles, the expansion of modern retail channels, and the rising presence of international and regional breweries are further fueling demand. Additionally, the growth of on-trade consumption through bars, restaurants, and nightlife culture is accelerating market expansion in key urban centers.

In North America, South America, and the Middle East & Africa, the lager market is supported by a combination of premiumization trends, expanding middle-class populations, and growing social drinking occasions. In the United States and Canada, demand is driven by craft lager innovation and a shift toward premium and flavored variants. In Brazil and Mexico, increasing urbanization and a strong beer culture are boosting consumption volumes. Meanwhile, in parts of the Middle East & Africa, market growth is more selective due to regulatory constraints. However, rising tourism, expatriate populations, and the gradual development of hospitality sectors are supporting demand in regions where alcohol consumption is permitted.

Competitive Landscape

The global lager market is highly consolidated, with Anheuser-Busch InBev, Heineken, and Carlsberg accounting for a significant share of total volume and an even larger proportion of market value. These companies leverage economies of scale, extensive brand portfolios, and established distribution networks to influence pricing strategies and drive product innovation. Their competitive strategies focus on two key areas: optimizing costs and efficiencies in core mass-market lagers, and expanding into premium, low- and no-alcohol variants, as well as adjacent beverage categories, to improve margins in a mature volume environment.

Strategic acquisitions remain critical for strengthening market positions, particularly through investments in craft brewing capabilities and diversification into non-alcoholic beverage segments. Additionally, the adoption of advanced brewing technologies and digital process optimization tools enables large brewers to ensure consistent quality, enhance operational efficiency, and maintain a competitive advantage that smaller players often struggle to match. Emerging opportunities are visible in niche segments such as dark lagers, premium on-trade experiences, and underserved emerging markets where distribution infrastructure is still developing.

Craft brewers are gaining momentum by emphasizing direct-to-consumer models, distinctive branding, and sustainability-focused initiatives that appeal to younger consumers. However, their overall scale remains limited compared to industry leaders. Regional brewers, on the other hand, rely on strong local brand equity and cost advantages to defend their domestic markets. Despite these strengths, they often face challenges in expanding globally due to limited resources and lower international brand recognition.

Lager Industry Leaders

Anheuser-Busch InBev SA/NV

Heineken N.V.

Carlsberg Group

Molson Coors Beverage Company

China Resources Snow Breweries Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Kati Patang Lifestyle Limited introduced Freedom Lager – Motoverse Edition, designed to celebrate motorcycling culture. Freedom Lager is a light-bodied lager brewed with locally sourced, non-GMO Indian corn, offering a crisp and refreshing taste. It is crafted for explorers and reflects a shared spirit of discovery, independence, creativity, and cultural connection.

- October 2025: Conan launched a new 8% ABV strong lager in India, starting with its introduction in Delhi. The product is positioned as a premium option within the strong beer segment, highlighting a smoother taste and the use of imported ingredients, including German malt and American hops, to distinguish itself from traditionally harsher strong lagers. The brand aims to cater to evolving consumer preferences for higher-quality, high-alcohol beverages and seeks to leverage the growing premiumization trend in India’s beer market.

- February 2025: BrewDog Wingman touchdown lager was launched, which was asserted to be crafted with Simcoe and Citra hops to deliver a crisp, citrusy 4.8% ABV. This seasonal lager was released in special NFL-themed cans for Super Bowl LIX. Its limited-edition nature and bold branding underscore the synergy between beverage launches and major cultural events.

- November 2024: Wrexham Lager Beer Co. launched its product in the United States. Specifically, the beer is now available at Total Wine & More stores in 29 states. This marks the first time Wrexham Lager has been sold in the US.

Global Lager Market Report Scope

| Pale Lager |

| Dark Lager |

| Others |

| Standard Lager |

| Premium Lager |

| Luxury Lager |

| Glass Bottle |

| Metal cans |

| Other Packaging Types |

| On-Trade |

| Off-Trade |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| United Arab Emirates | |

| Nigeria | |

| Morocco | |

| Egypt | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Pale Lager | |

| Dark Lager | ||

| Others | ||

| By Category | Standard Lager | |

| Premium Lager | ||

| Luxury Lager | ||

| By Packaging Type | Glass Bottle | |

| Metal cans | ||

| Other Packaging Types | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| United Arab Emirates | ||

| Nigeria | ||

| Morocco | ||

| Egypt | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the global lager market?

The lager market size is USD 715.25 billion in 2026 and is projected to reach USD 821.46 billion by 2031.

Which region will grow fastest for lager through 2031?

Asia-Pacific leads with a 5.05% CAGR owing to rising incomes in China and India and growing demand for premium imports.

What product type is gaining share most rapidly?

Dark lager is forecast to expand at a 3.45% CAGR as consumers look for richer, malt-forward styles.

Why are brewers shifting toward metal cans?

Cans cut logistics emissions, meet circular-economy targets, offer premium graphics, and are growing at a 3.81% CAGR in packaging.

Page last updated on: