Germany Pharmaceutical Cold Chain Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

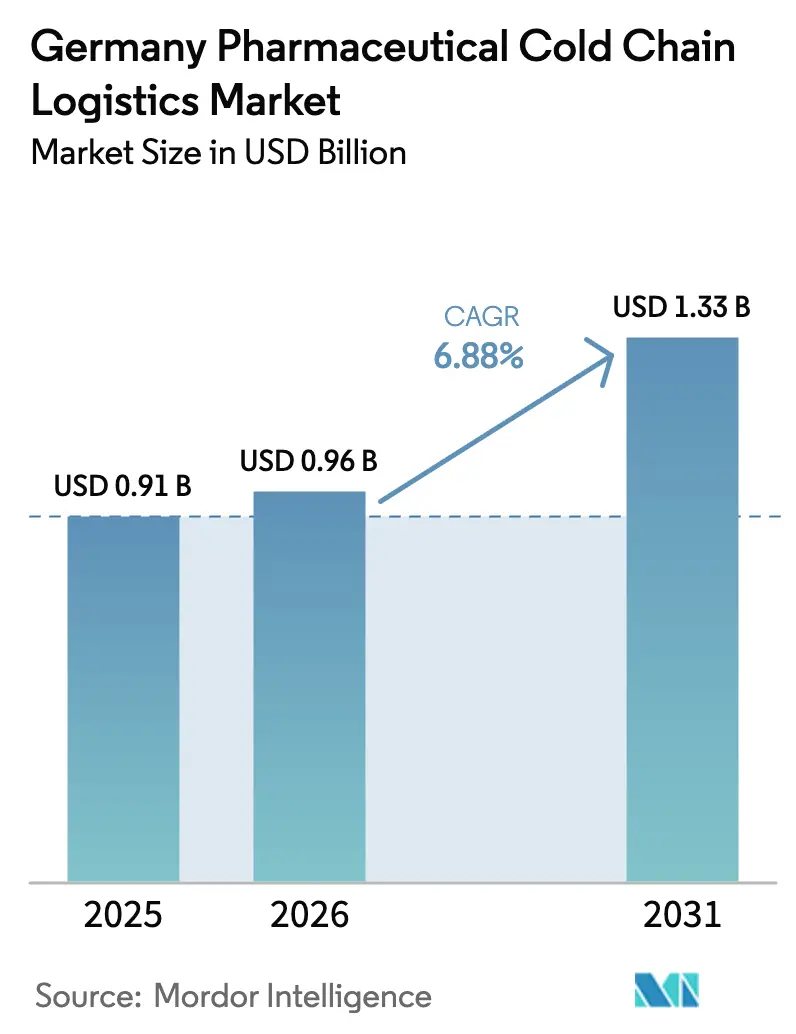

| Base Year Market Size (2025) | USD 0.91 Billion |

| Market Size (2026) | USD 0.96 Billion |

| Market Size (2031) | USD 1.33 Billion |

| Growth Rate (2026 - 2031) | 6.88% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Pharmaceutical Cold Chain Logistics Market Analysis by Mordor Intelligence

The Germany Pharmaceutical Cold Chain Logistics Market size is expected to grow from USD 0.91 billion in 2025 to USD 0.96 billion in 2026 and is forecast to reach USD 1.33 billion by 2031 at 6.88% CAGR over 2026-2031.

Robust growth reflects Germany’s role as a European manufacturing and distribution nucleus, with biopharma volumes driving multi-temperature capacity and validated lanes across key industrial corridors. mRNA capacity built during the pandemic is being repurposed for oncology and rare-disease pipelines, which pushes demand for ultra-cold capabilities and stricter GDP adherence. Direct-to-patient programs are expanding from chronic therapies to complex biologics, which shifts volumes from wholesale channels to residential deliveries with real-time monitoring. Competitive pressure from Eastern European networks is intensifying, yet German incumbents are reinforcing premium positions through GDP certification, IoT-enabled traceability, and purpose-built biopharma routes. A tighter regulatory stance on distribution quality elevates cold-chain integrity from a cost center to a compliance obligation in the Germany pharmaceutical cold-chain logistics market.

Key Report Takeaways

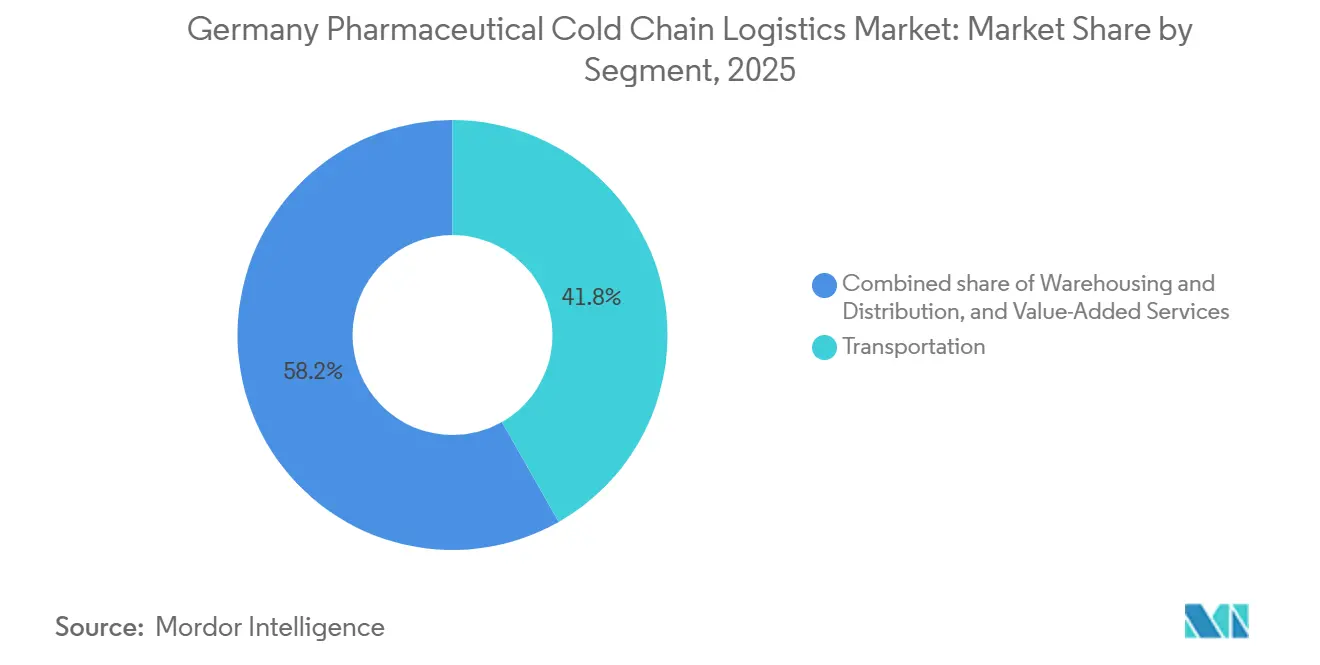

- By service type, transportation held 41.78% of the Germany pharmaceutical cold chain logistics market share in 2025, while value-added services recorded the fastest growth at 6.87% CAGR through 2031.

- By temperature type, the chilled segment led with 48.12% market share in 2025, and the frozen segment is the fastest-growing at a 7.24% CAGR to 2031.

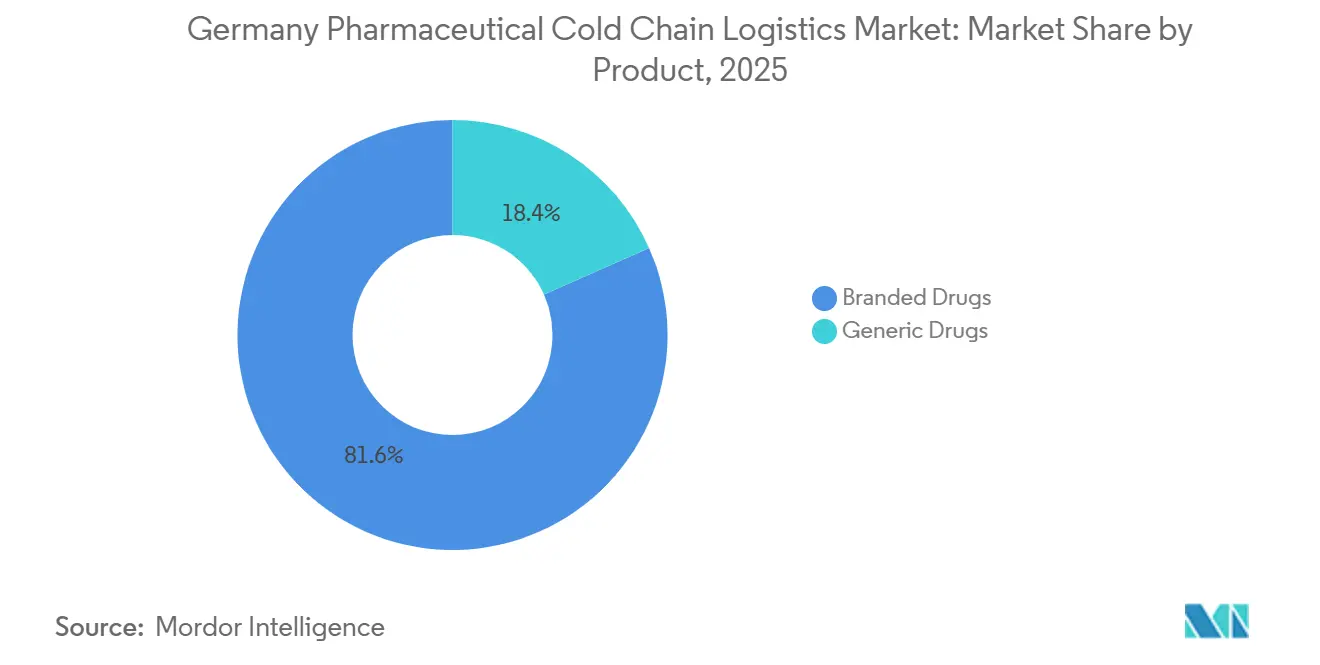

- By product, branded drugs held 81.64% of the Germany pharmaceutical cold chain logistics market size in 2025 and are projected to expand at a 7.67% CAGR through 2031.

- By application, biopharma accounted for a 68.97% share of the Germany pharmaceutical cold chain logistics market size in 2025, and specialized pharma is advancing at an 8.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Pharmaceutical Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Biopharma Manufacturing in Bavaria and Baden-Württemberg | +1.2% | Southern Germany core, spillover to Rhineland-Palatinate and Hesse | Medium term (2-4 years) |

| Germany as Central European Pharmaceutical Distribution Hub | +1.5% | National, with concentration in Frankfurt Rhine-Main, Hamburg, and Berlin | Long term (≥ 4 years) |

| Growing Direct-to-Patient Home Delivery Programs | +1.1% | Urban cores initially, expanding nationwide | Medium term (2-4 years) |

| Increasing Clinical Trial Activity for Cell and Gene Therapies | +1.4% | University hospital clusters (Berlin, Heidelberg, Munich, Regensburg) | Medium term (2-4 years) |

| Premium Pricing Tolerance for Temperature-Assured Logistics | +0.8% | Global, strongest in high-value biopharma corridors | Long term (≥ 4 years) |

| Rising mRNA Vaccine Production Following Pandemic Infrastructure | +0.9% | Bavaria (Mainz), North Rhine-Westphalia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion of Biopharma Manufacturing in Bavaria and Baden-Württemberg

Eli Lilly’s EUR 2.3 billion (USD 2.5 billion) plant in Aley, operational by 2027, underscores how western and southern corridors are scaling biologics and incretin therapy output that moves under 2-8°C protocols from fill-finish to dispensing. Roche’s continued capital commitment in Germany adds further momentum across Baden-Württemberg and adjacent states, reinforcing a dense cluster of global players that value regulatory speed and specialized labor. This clustering reduces inter-facility transfer time, strengthens reverse-logistics loops, and creates multi-depot density that GDP-certified carriers convert into efficient milk runs and full-truckload lanes. Proximity to Frankfurt and Stuttgart intermodal gateways improves route control and reduces ambient risk during transshipment for high-value biologics. The result is a more consolidated outbound flow from the south and west that improves asset utilization for carriers and stabilizes service-level performance in the Germany pharmaceutical cold chain logistics market.

Germany as a Central European Pharmaceutical Distribution Hub

DHL’s expanded Life Sciences & Healthcare campus in Florstadt adds 100,000 square meters of GDP-compliant space and more than 140,000 pallet positions across multi-temperature zones, which strengthens Germany’s position as a central European pharma hub served by Frankfurt Airport. The site supports APIs, hazardous materials, and raw materials within GMP conditions, aligning with strict European and international standards for life sciences customers across the region. Germany’s multimodal backbone, including the Rhine-Main-Danube corridor and high-speed rail, links North Sea gateways to Alpine manufacturing and helps consolidate pharmaceutical flows. For specialized therapies that need sub-24-hour delivery and chain-of-identity controls, Germany’s hub-and-spoke architecture enables overnight staging and same-morning hospital or home-care dispatch. This integrated network effect is a structural advantage that sustains the Germany pharmaceutical cold chain logistics market over the long term.

Growing Direct-to-Patient Home Delivery Programs

Direct-to-patient programs are moving beyond chronic therapies to complex temperature-controlled consignments that require validated packaging, active monitoring, and trained couriers. The SMA Apotheken Programm coordinates national home delivery of gene therapy treatments for spinal muscular atrophy, including preparation, stock control, and interaction checks through an integrated portal that supports both patients and providers. Eurotranspharma Deutschland operates a bi-temperature network within single vehicles that can deliver at +2°C to +8°C and +15°C to +25°C, which supports multi-SKU residential drops without over-reliance on passive packaging. As carriers validate residential identity checks and exception handling, manufacturers gain confidence to re-balance from wholesale-pharmacy-hospital loops to point-of-care delivery. This shift creates new operational patterns around appointment scheduling and proof-of-delivery in the Germany pharmaceutical cold chain logistics market.

Increasing Clinical Trial Activity for Cell and Gene Therapies

Germany’s pipeline of cell and gene therapy trials is building repeatable logistics lanes that carriers can qualify across clinical sites, which reduces per-shipment irregularity. Bayer has advanced both a cell therapy and a gene therapy for Parkinson’s disease into later-stage European trials that include German centers, which require controlled movement of sensitive material under tight time windows. The Berlin Center for Gene and Cell Therapies will add 4,600 square meters of GMP capacity for ATMPs by 2028, supported by EUR 76.5 million (USD 83.2 million) in funding over ten years, and will be operated by ProBioGen [1]Editorial team, “ProBioGen to Lead GMP Manufacturing Operations at Berlin Center for Gene and Cell Therapies (BC GCT),” ProBioGen AG, probiogen.de. Germany’s national strategy for gene and cell-based therapies aims to streamline pathways via the Paul-Ehrlich-Institut and strengthen GMP capabilities at academic centers, which supports consistent clinical-supply operations. As autologous and allogeneic modalities scale, cryogenic handoffs and chain-of-identity tracking solidify as baseline requirements in the Germany pharmaceutical cold chain logistics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Energy Costs Impacting Refrigeration Economics | -0.6% | National, acute in high-refrigeration warehouses (Hamburg, Bremen) | Short term (≤ 2 years) |

| Driver Shortage for GDP-Certified Cold Chain Transportation | -0.4% | National, severe in eastern states and rural routes | Medium term (2-4 years) |

| Infrastructure Limitations in Former East German Regions | -0.3% | Saxony, Thuringia, Brandenburg, Mecklenburg-Vorpommern | Long term (≥ 4 years) |

| Intense Price Competition from Eastern European Logistics Providers | -0.5% | Cross-border lanes to Poland, Czech Republic; domestic underbidding | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Energy Costs Impacting Refrigeration Economics

Cold storage and active refrigerated transport depend on energy-intensive systems, so price volatility tightens margins and limits the ability to add surge capacity quickly. Producer price movements underscore cost sensitivity within German manufacturing, which influences the cost base for temperature-controlled operations and related services. Sites with high refrigeration density, such as port-adjacent warehouses, face peak-load challenges during seasonal extremes that raise contingency costs. Carriers respond with route and load consolidation, but residual exposure persists for shipments that require dedicated capacity or short-notice dispatch. These pressures can delay upgrades to -20°C and -70°C infrastructure, which in turn affects service breadth in the Germany pharmaceutical cold chain logistics market.[2]Editorial team, “Producer prices in January 2026: -3.0% on January 2025,” German Federal Statistical Office (Destatis), destatis.de

Driver Shortage for GDP-Certified Cold Chain Transportation

GDP-compliant pharmaceutical transport requires trained drivers and handlers, and staffing gaps reduce effective capacity during peak demand. Germany’s labor market has reported shortages in many skilled occupations, which filters into specialized logistics roles that require compliance training and audited SOPs. The shortage weighs more on rural and eastern routes, where network density is lower, and bench strength is thin. Carriers are investing in training and retention, but certification pathways take time and resources to scale. The result is intermittent service strain that can limit same-day or sub-24-hour flexibility in the Germany pharmaceutical cold chain logistics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Integrated Logistics Reshape Value Distribution

Transportation held 41.78% of segment value in 2025, which anchors the current mix even as value-added services post the fastest 6.87% CAGR through 2031. Road distribution remains the backbone for domestic flows across production nodes in Bavaria, North Rhine-Westphalia, and Hesse, while air freight bridges time-critical biologics and clinical materials through Frankfurt. Ocean and rail have a smaller role for domestic movements, yet they contribute to import-export corridors and upstream API consolidation. Warehousing and distribution absorb a growing share due to multi-zone GDP facilities, validated cold rooms, and continuous monitoring that many pharma clients outsource. DHL’s Florstadt campus illustrates how integrated warehousing with 2-8°C, -20°C, and down to -70°C zones supports a wider service envelope for biopharma and clinical research customers. GEODIS’s GDP certification for ocean freight in Hamburg strengthens multimodal continuity from vessel to GDP warehouse, which reduces handoff risk for inbound or transshipment flows. The Germany pharmaceutical cold chain logistics market benefits when carriers can wrap transport, storage, and compliance-heavy add-ons into single contracts that reduce audit overhead for shippers.

Transportation will remain central as value-added services scale because manufacturers want fewer handoffs with richer compliance coverage. This is most visible in temperature excursion management, controlled returns, and clinical sample handling that sit adjacent to core transport. Eurotranspharma’s bi-temperature distribution shows how fleet-level design can support mixed consignments in one route plan, which reduces the need for passive packaging on every parcel. As more contracts expand to end-to-end scope, carriers that integrate storage, labeling, relabeling, and batch-certified kitting gain traction in the Germany pharmaceutical cold chain logistics industry. The shift favors operators with audited IT systems and telemetry that demonstrate GDP adherence in real time. These attributes underpin price resilience against low-cost bids in the Germany pharmaceutical cold chain logistics market.

By Temperature Type: Frozen Growth Outpaces Chilled Dominance

Chilled shipments at 2-8°C commanded 48.12% of segment revenue in 2025, which reflects the prevalence of vaccines, insulins, and many biologics in professional and home-care settings. Frozen is the fastest-growing category at 7.24% CAGR through 2031, propelled by ultra-cold mRNA programs and specialized therapies that require -20°C or below for stability. The Germany pharmaceutical cold chain logistics market is expanding the sub-zero footprint, which includes validated -70°C capacity for investigational therapies and some commercial pipelines. DHL’s multi-temperature capabilities at Florstadt demonstrate how warehousing platforms are futureproofing with ultra-cold readiness, supported by controlled clean-room processes. Carriers are adopting IoT sensors and qualified packaging to keep thermal performance consistent from pick-up through the last mile. These features are now key evaluation criteria in procurement for pipelines that cannot tolerate wider temperature ranges in the Germany pharmaceutical cold chain logistics market.

Chilled will continue to dominate by revenue, yet frozen complexity will shape investment priorities because it requires cryogenic containers, qualified dry ice processes, and specialized SOPs. Fleet and site upgrades are being sequenced to where trial density and specialty volumes are highest, including Frankfurt Rhine-Main and Berlin. The Germany pharmaceutical cold chain logistics industry also sees active 15-25°C control on ambient-tolerant products to mitigate seasonal spikes. As climate variability raises excursion risk, more shippers prefer active control rather than relying only on passive systems for longer routes. This reinforces an infrastructure mix that balances consolidation on 2-8°C with dedicated frozen capacity for high-value products in the Germany pharmaceutical cold chain logistics market.

By Product: Branded Drugs Anchor Value

Branded drugs accounted for 81.64% of segment value in 2025 and are projected to grow at 7.67% through 2031, which anchors premium service demand across hospital and home-care channels. Specialty biologics and gene therapies require GDP protocols with validated lanes and rigorous batch-level documentation that raise service complexity. The branded dominance shapes carrier strategy toward higher service-level commitments, granular tracking, and hospital-direct delivery. Domestic clusters around Bavaria and Hesse, supported by Frankfurt’s air hub, channel many of these products into time-defined routes with active monitoring. The Germany pharmaceutical cold chain logistics market allocates the highest capital intensity to branded flows where excursion tolerance is low, and penalty risk is high.

Generics contribute meaningful refrigerated volumes for vaccines and insulins, but their cost orientation keeps pressure on per-pallet economics and route consolidation. As biosimilars expand, some shipments move under conditions like branded biologics, which narrows the operational difference while preserving a spread in service pricing. Procurement teams segment tenders by risk class, which helps align service levels to stability profiles and serialize traceability. Incumbent carriers leverage established GDP audits and qualified packaging catalogs to simplify onboarding for branded portfolios. This alignment sustains the premium tier and reinforces the revenue mix in the Germany pharmaceutical cold chain logistics market.

Geography Analysis

Western and southern corridors such as Bavaria, Baden-Württemberg, North Rhine-Westphalia, and Hesse concentrate manufacturing and distribution that feed national and European flows. Bavaria and Hesse benefit from proximity to Frankfurt Airport and the Florstadt campus, which anchors cross-border connectivity for APIs and finished products. North Rhine-Westphalia connects through Cologne-Bonn and Düsseldorf airports with inland waterways that support resilient multimodal routes. Southern nodes that include Roche’s German footprint and cross-border Swiss manufacturing contribute steady biologics volumes to Germany’s hub network. Eli Lilly’s EUR 2.3 billion (USD 2.7 billion) Alzey investment will add outbound volumes for chilled transport once commercial operations begin in 2027. Roche’s ongoing capital program in Germany complements this outlook and supports dense route planning across clinics and hospital pharmacies. The Germany pharmaceutical cold chain logistics market continues to scale capacity where outbound biologics and specialty therapies cluster.

Eastern states, including Saxony, Thuringia, Brandenburg, Mecklenburg-Vorpommern, and Saxony-Anhalt, show thinner depot density and fewer GDP warehouses, which raises per-stop costs and excursion risk on longer runs. Leipzig and Dresden support limited cold storage nodes, but many rural destinations depend on longer hauls from western hubs. The 2026 federal transport budget allocates EUR 28.22 billion (USD 33.19 billion) for transport infrastructure, with EUR 2.04 billion (USD 2.39 billion) for municipal traffic improvement and EUR 1.85 billion (USD 2.17 billion) for federal waterways, which supports long-term network quality even if investment per capita varies across regions - USD 30.68 billion, USD 2.22 billion, and USD 2.01 billion, respectively. Stricter temperature-control expectations will likely push smaller or regional carriers to adopt continuous telemetry, which adds cost and can accelerate consolidation. As clinical sponsors demand sub-2% excursion rates, procurement often concentrates volumes with national carriers that keep validated lanes across all states. These dynamic preserves quality performance but can shift volumes away from under-capitalized providers in the Germany pharmaceutical cold chain logistics market.

Hamburg and Bremen remain key maritime gateways where pharmaceutical imports are transferred to inland GDP facilities. GEODIS’s GDP certification for ocean freight in Hamburg supports seamless regulatory alignment from vessel to warehouse for sensitive consignments. Berlin is developing as a focal point for cell and gene therapy logistics on the back of the BC GCT and the city’s academic medical infrastructure. Its location also links western corridors to Poland and the Czech Republic, which supports cross-border flows into Central and Eastern Europe[3]Patricia Teixeira Mendes, “GEODIS in Germany Receives GDP Certification for Pharmaceutical Ocean Freight Logistics,” GEODIS, geodis.com. The Germany pharmaceutical cold chain logistics market benefits from this bridge role as EU GDP harmonization extends service reach into adjacent member states. Frankfurt and Leipzig airports help stage overnight shipments and next-morning delivery windows for high-priority therapies. Carrier investments follow these geography patterns to keep utilization high and excursion risk low across corridors that matter most.

Competitive Landscape

Top Companies in Germany Pharmaceutical Cold Chain Logistics Market

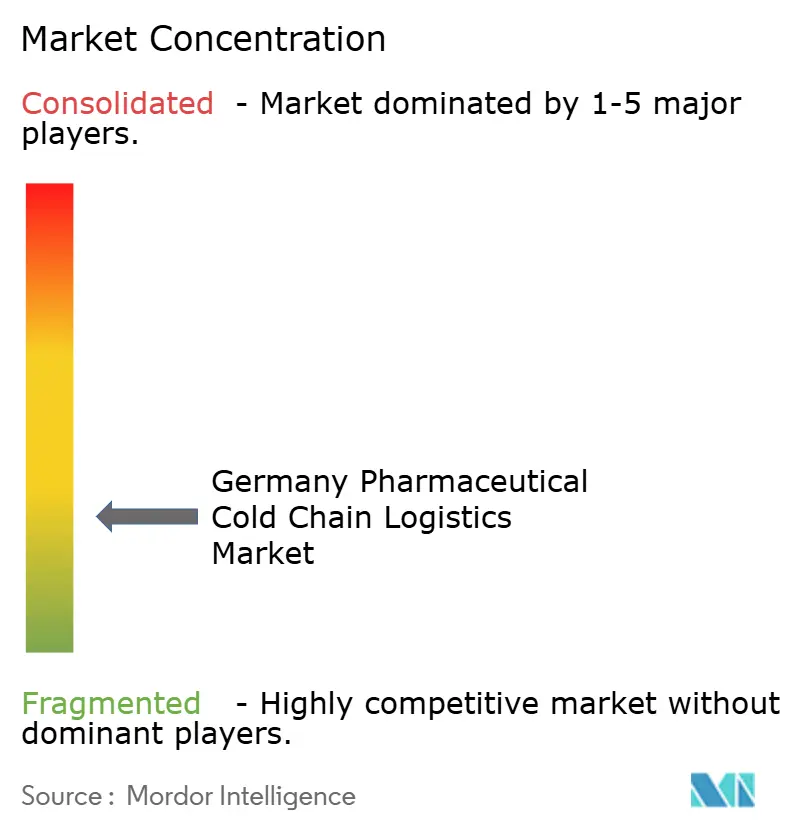

While the market remains fragmented overall, GDP-compliant and biopharma segments are increasingly consolidated among certified players. Global integrators such as DHL Supply Chain and GEODIS have expanded GDP-compliant capabilities that combine warehousing, distribution, and value-added services into auditable end-to-end solutions. DHL’s Florstadt campus expansion highlights a multi-temperature platform that can process APIs and hazardous materials under GMP controls, which appeals to biopharma and clinical research customers across Europe. GDP-certified ocean freight in Hamburg further supports multimodal continuity for sensitive cargo. Integrators differentiate through auditable IT, IoT telemetry, and consistent SOPs that streamline customer audits and deviation management. The German pharmaceutical cold chain logistics market rewards these integrated plays with longer contracts and price stability relative to spot transport.

Specialist carriers strengthen last-mile capabilities with bi-temperature fleets and pharmacy-dense route networks. Eurotranspharma Deutschland’s GDP certification and dual-temperature vehicle operations reflect this specialization and enable efficient distribution of mixed consignments across 2-8°C and 15-25°C ranges without switching vehicles. These features reduce passive-packaging dependence and improve efficiency for multi-SKU deliveries. Carriers with validated hospital-direct and home-delivery processes can support increasing direct-to-patient volumes. This position supports premium pricing where pharmaceutical clients prioritize risk mitigation in the Germany pharmaceutical cold chain logistics market.

Regulatory expectations continue to shape competitive dynamics. Regular GDP oversight by competent authorities keeps pressure on auditable systems and trained personnel, and national dialogues on regulatory updates reflect the push for timely access and consistent standards. Companies that invest in continuous temperature records and quality dashboards gain preference in tenders that scrutinize audit readiness. The Germany pharmaceutical cold chain logistics market, therefore, sees a gradual tilt toward incumbents with embedded compliance and a scalable technology stack. Niche players retain room to differentiate in cryogenic logistics and specialized hospital services where agility matters.

Germany Pharmaceutical Cold Chain Logistics Industry Leaders

Trans-o-flex (ThermoMed)

DHL

GDP Network Solutions GmbH

Transmed Transport GmbH

Kuehne + Nagel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: GEODIS in Germany received GDP certification from Bureau Veritas for its ocean freight service in Hamburg, which complements earlier CEIV Pharma certification for its Frankfurt air freight team.

- May 2025: DHL’s Florstadt Life Sciences & Healthcare campus expanded to 100,000 square meters with multi-temperature zones and an integrated clean room, serving biopharma, specialty pharma, and clinical research customers.

Germany Pharmaceutical Cold Chain Logistics Market Report Scope

The Germany Pharmaceutical Cold Chain Logistics Market Report is Segmented by Service Type (Transportation [Road, Air, Sea, Rail], Warehousing & Distribution, and Value-Added Services), by Temperature Type (Chilled, Frozen, and Ambient), by Product (Generic Drugs, and Branded Drugs), and by Application (Biopharma, Chemical Pharma, and Specialized Pharma). The Market Forecasts are Provided in Terms of Value (USD Billion).

| Transportation | Road |

| Air | |

| Sea | |

| Rail | |

| Warehousing & Distribution | |

| Value-Added Services |

| Chilled |

| Frozen |

| Ambient |

| Generic Drugs |

| Branded Drugs |

| Biopharma |

| Chemical Pharma |

| Specialized Pharma |

| By Service Type | Transportation | Road |

| Air | ||

| Sea | ||

| Rail | ||

| Warehousing & Distribution | ||

| Value-Added Services | ||

| By Temperature Type | Chilled | |

| Frozen | ||

| Ambient | ||

| By Product | Generic Drugs | |

| Branded Drugs | ||

| By Application | Biopharma | |

| Chemical Pharma | ||

| Specialized Pharma |

Key Questions Answered in the Report

How big is the Germany Pharmaceutical Cold Chain Logistics Market?

The Germany Pharmaceutical Cold Chain Logistics Market size is expected to reach USD 0.91 billion in 2025 and grow at a CAGR of 6.88% to reach USD 1.33 billion by 2031.

Which service and temperature segments are leading and growing fastest in Germany?

Transportation led with 41.78% share in 2025 while value-added services recorded the fastest growth at 6.87% CAGR, and chilled at 2-8°C held 48.12% share while frozen is the fastest-growing at 7.24% CAGR.

How is Germany’s infrastructure shaping pharmaceutical distribution for sensitive therapies?

Expanded multi-temperature GDP campuses near Frankfurt and certified ocean freight in Hamburg support end-to-end continuity for biologics and trials, reinforcing Germany’s role as a central European hub.

What is driving the surge in specialized cold chain needs such as ultra-cold and cryogenic?

Growth in mRNA platforms and cell and gene therapies is increasing demand for -20°C to -70°C capabilities, chain-of-identity tracking, and hospital-direct delivery protocols.

Where in Germany is cold chain demand most concentrated and why?

Western and southern corridors such as Bavaria, Baden-Wurttemberg, North Rhine-Westphalia, and Hesse concentrate manufacturing and hub capacity, which drives consolidated outbound flows and validated lanes.

What role do direct-to-patient programs play in shaping last-mile cold chain?

Programs that coordinate home delivery of temperature-sensitive therapies require validated packaging, active monitoring, trained couriers, and identity verification, which shifts volumes from wholesale channels to residential nodes.

Page last updated on: