United Kingdom Pharmaceutical Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

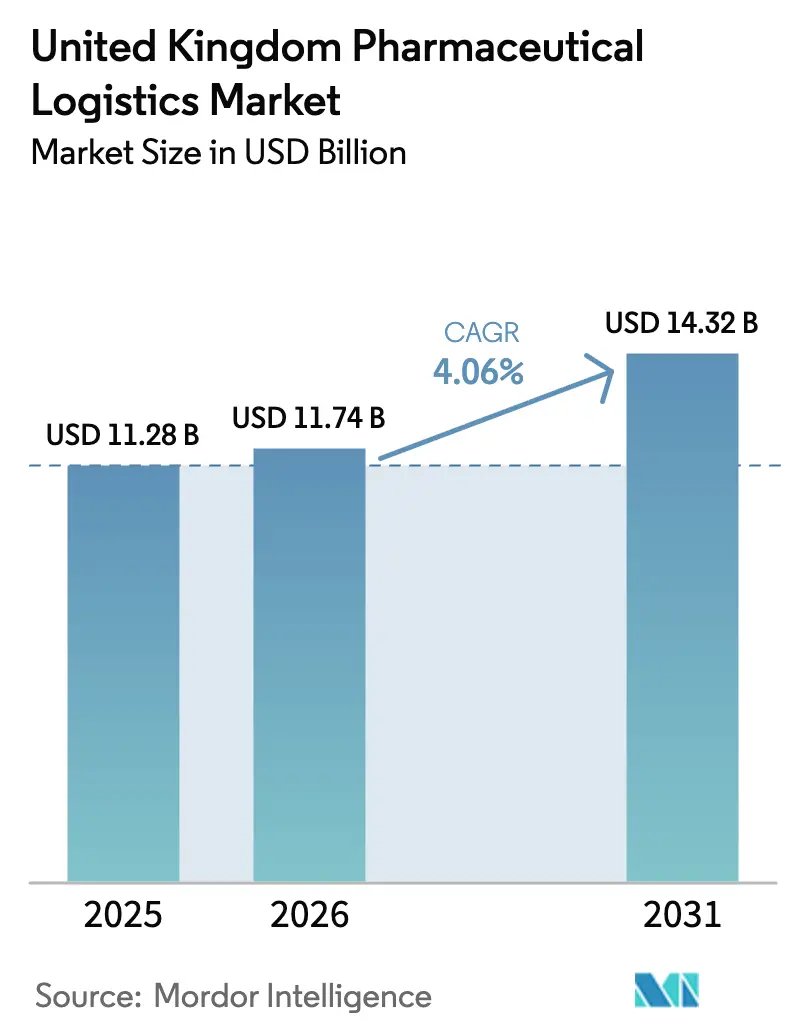

| Base Year Market Size (2025) | USD 11.28 Billion |

| Market Size (2026) | USD 11.74 Billion |

| Market Size (2031) | USD 14.32 Billion |

| Growth Rate (2026 - 2031) | 4.06% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United Kingdom Pharmaceutical Logistics Market Analysis by Mordor Intelligence

The United Kingdom Pharmaceutical Logistics market size is expected to grow from USD 11.28 billion in 2025 to USD 11.74 billion in 2026 and is forecast to reach USD 14.32 billion by 2031 at 4.06% CAGR over 2026-2031.

Sustained demand for advanced therapy medicinal products (ATMPs), rapid digitalization of National Health Service (NHS) prescription fulfillment, and Brexit-driven supply-chain localization underpin growth, while persistent talent shortages and energy cost inflation temper operating margins. Domestic logistics investment has accelerated since the Windsor Framework mandated UK-wide marketing authorizations and stricter safety declarations for medicines imported from the European Union, prompting carriers to upgrade customs-handling and compliance systems[1]“UK-Wide Licensing for Human Medicines,” UK Government, GOV.UK. Cold-chain capacity additions continue across England and Scotland to support cell and gene therapy pipelines, and integrated digital platforms have emerged as competitive differentiators by providing end-to-end shipment visibility for NHS stakeholders.

Key Report Takeaways

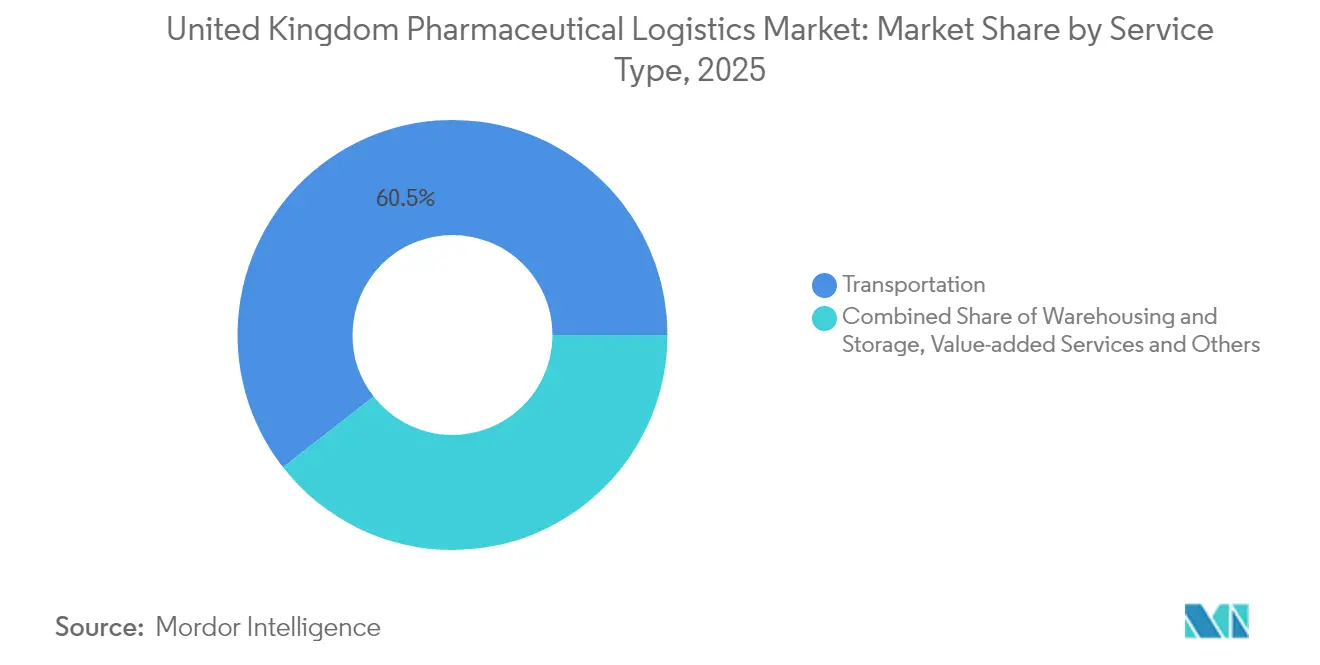

- By service type, transportation captured 60.55% of the UK pharmaceutical logistics market share in 2025; value-added services are advancing at a 4.78% CAGR through 2031.

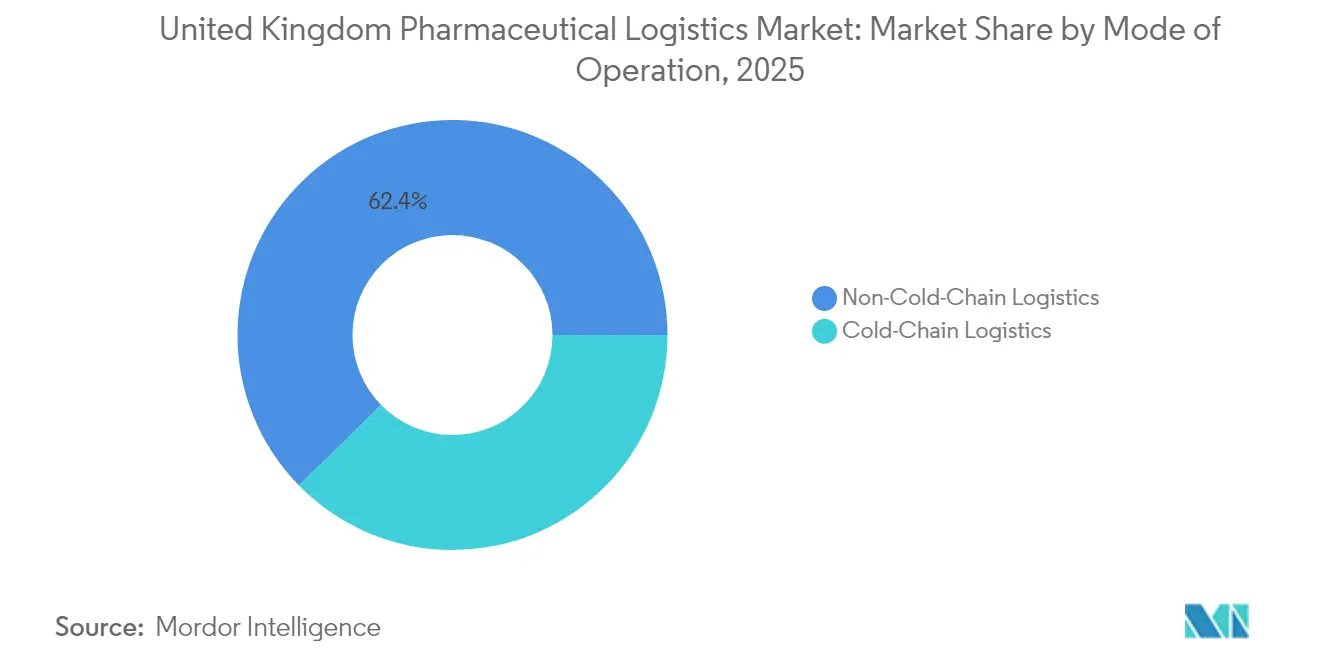

- By mode of operation, non-cold-chain services held 62.35% of the UK pharmaceutical logistics market size in 2025, while cold-chain is forecast to grow at 5.62% CAGR between 2026 and 2031

- By product type, prescription drugs accounted for 36.65% share of the UK pharmaceutical logistics market in 2025 and cell and gene therapies are projected to expand at a 4.36% CAGR through 2031.

- By geography, England remained the dominant revenue contributor in 2025, whereas Northern Ireland is expected to register the fastest growth as dual-market access capabilities mature under the Windsor Framework.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Pharmaceutical Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing online pharmacy & e-commerce growth | +0.8% | UK-wide; urban centers | Medium term (2-4 years) |

| Strict MHRA GDP compliance | +0.6% | UK-wide | Short term (≤ 2 years) |

| NHS personalised-medicine initiatives | +0.7% | UK-wide; pilot programs in England | Medium term (2-4 years) |

| Brexit-driven domestic logistics investment | +0.9% | UK-wide; emphasis on Northern Ireland | Long term (≥ 4 years) |

| Growth in ATMP clinical trials (ultra-cold chain) | +0.5% | England and Scotland research hubs | Long term (≥ 4 years) |

| Expansion of NHS pharmacy home-delivery services | +0.4% | UK-wide; rural areas priority | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Online Pharmacy and E-commerce Growth

NHS partnerships with Uber and Royal Mail illustrate a systemic pivot toward direct-to-patient delivery, enabling real-time prescription tracking and cutting dispensing errors through electronic verification[2]“Soft Market Research for an Electronic Medicines Tracking System,” UK Government, GOV.UK. AI-assisted demand forecasting now underpins stock-replenishment cycles, shrinking inventory buffers and freeing warehouse space for higher-value biologics. These digital workflows elevate data-security requirements, pushing carriers to integrate secure APIs and two-factor authentication for patient data interchange. Last-mile complexity is rising because controlled drugs and temperature-sensitive biologics must meet both security and GDP parameters during doorstep hand-off. The result is growing uptake of IoT-enabled lockboxes and time-stamped delivery validation tools, making digitally native logistics providers attractive partners for NHS trusts pursuing home-care expansion.

Strict MHRA GDP Compliance

Brexit has ended automatic recognition of EU GDP certificates, obliging every inbound shipment to demonstrate UK compliance documentation and triggering systems retrofits among carriers. Transition from Parallel Distribution Notices to Parallel Import Licences requires data-capture upgrades across warehouse management systems, adding near-term cost but sharpening competitive advantages for large operators with mature quality-management frameworks. MHRA’s point-of-care manufacturing guidance furthers complexity; logistics firms must add validated clean-room transfer protocols to carry freshly compounded personalized doses directly from hospital labs to bedside within narrow stability windows. Compliance spend is cascading into workforce training, with carriers expanding GDP curricula to include cyber-security and data-integrity modules that address electronic chain-of-custody mandates.

NHS Personalised-Medicine Initiatives

The NHS 10-Year Plan integrates pharmacogenomic testing and electronic prescribing, requiring logistics nodes to interoperate with ePMA systems for patient-specific inventory pulls. Hospital-at-home pilots in England rely on scheduled courier visits equipped with temperature-validated pouches for biologics infusion kits, intensifying demand for trained staff in secure last-mile execution. Sample-collection logistics add reverse-flow challenges, as genomic swabs must meet 2-8 °C thresholds en route to sequencing labs. These personalized-medicine pathways spawn micro-fulfillment facilities near clinical clusters, allowing 24-hour cycle times from prescription to delivery. Consequently, integrated digital twins that model time-temperature exposure are becoming a procurement criterion in NHS contract tenders.

Brexit-Driven Domestic Logistics Investment

The Windsor Framework’s customs reforms incentivize in-country storage and regional fulfillment centers, particularly around Belfast and Liverpool, to minimize clearance delays[3]“Government Ramps Up Work to Secure Supplies of Medicines,” UK Government, GOV.UK. Pharmaceutical manufacturers are colocating secondary packaging lines with distribution hubs, trimming cross-channel lead times and lowering spoilage risks for high-value biologics. The Critical Imports and Supply Chains Strategy directs GBP 400 million (USD 509.21 million) to logistics digitalization, unlocking grants for automated document-scrubbing and AI-enabled risk screening. Carriers able to self-declare consignments via new Safety & Security declarations gain two-hour clearance privileges at Dover and Felixstowe, improving on-time performance metrics. Over the long run, these nearshoring moves are expected to raise baseline domestic freight volumes by mid-single digits annually.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Talent shortage of GDP-compliant drivers | -0.3% | UK-wide; acute in Scotland and Wales | Short term (≤ 2 years) |

| Rising energy & fuel costs | -0.4% | UK-wide; cold-chain operations most affected | Medium term (2-4 years) |

| Limited pharmaceutical cargo capacity at regional airports | -0.2% | Northern England, Scotland, Wales | Short term (≤ 2 years) |

| Cyber-security risks in connected cold-chain systems | -0.15% | UK-wide; high in urban fulfillment nodes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Talent Shortage of GDP-Compliant Drivers

Immigration curbs post-Brexit reduced the heavy-goods-vehicle workforce pool, and GDP qualifications add an extra training layer of 6-12 months, delaying talent replenishment. Salary premiums for certified drivers rose 14% year-over-year in 2024, squeezing smaller carriers that operate thin margin refrigerated fleets. Rural pharmacies report missed delivery windows during seasonal peaks, compelling NHS trusts to engage multi-stop consolidation services that lengthen lead times. While apprenticeship grants have been introduced, uptake remains modest due to long qualification pathways. Over time, semi-autonomous truck pilots could mitigate dependency, yet regulatory hurdles push commercial deployment beyond the forecast horizon.

Rising Energy & Fuel Costs

Diesel and electricity tariffs climbed 30-40% between 2024 and 2025, inflating cold-chain cost structures where refrigeration can represent 45% of total operating expense. Logistics UK has lobbied for fuel-duty relief, but fiscal headroom remains tight. Some carriers retrofit trailers with solar panels to offset auxiliary-power-unit draw; payback periods, however, exceed five years under current price regimes. Ultra-low-temperature freezers consume up to 20 kWh daily per unit, forcing warehouses to renegotiate power contracts or pass surcharges to shippers. Energy hedging tools are gaining traction, yet volatility risks persist, prompting carriers to prioritize high-margin biologics lanes over commoditized ambient freight.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Transportation Services Anchor a Digitally Evolving Portfolio

Transportation maintained 60.55% share of the UK pharmaceutical logistics market in 2025, translating to a UK pharmaceutical logistics market size contribution of USD 6.83 billion. Road freight leads due to its geographic reach across 1,250+ NHS hospital and community-pharmacy delivery points, allowing same-day replenishment cycles for critical medicines. The sub-segment leverages GPS-enabled telematics that feed shipment-status data directly into NHS Electronic Prescription Service dashboards, heightening transparency. Value-added services, albeit smaller, are rising at a 4.78% CAGR as clients seek inventory optimization analytics, relabeling, and returns-management functions within one contract, notably under NHS digitalization mandates.

Technology investments continue to reshape service-type economics. AI-driven route-optimization trims average empty mileage by 8%, offsetting fuel-cost volatility. Air freight, though <8% of value, is pivotal for ATMP imports from the United States and rapid vaccine deployment, but runway curfews at regional airports constrain uplift. Warehousing, particularly temperature-controlled space, experiences single-digit growth as sterile-manufacturing expansion pads demand for validated clean-storage chambers. The convergence of transportation and value-added services into platform models signals an evolving competitive dynamic where carriers monetize data as much as miles traveled.

By Mode of Operation: Cold-Chain’s Rapid Catch-Up

The non-cold-chain segment contributed 62.35% of the UK pharmaceutical logistics market share in 2025, yet cold-chain’s 5.62% CAGR narrows the gap toward 2031. Within cold-chain, dry-ice and liquid-nitrogen shippers dominate ATMP lanes, requiring validated weight-loss monitoring during transit. Enforced digital lane mapping for cryogenic consignments has catalyzed investment in IoT probe networks, an arena where integrated platforms confer service reliability advantages. Non-cold-chain operators increasingly retrofit assets with passive insulation kits to extend service portfolios and mitigate seasonality.

Rising biologics penetration fuels cold-store real-estate demand, driving pre-let transactions near Oxford-Cambridge life-science clusters. High power density designs become standard, featuring redundancy in HVAC and backup generators to secure GDP compliance amid grid instability. Conversely, ambient networks digitize inventory controls to hold service parity, employing barcode and RFID scanning that sync with NHS stock-replenishment portals. The boundary between cold-chain and ambient operations blurs as predictive analytics inform lane assignments based on seasonal risk profiles, making hybrid skill sets a hiring priority.

By Product Type: Prescription Drugs Steady, ATMPs Ascendant

Prescription drugs preserved a 36.65% slice of the 2025 UK pharmaceutical logistics market size, driven by chronic-disease volumes under NHS prescriptions. Service levels remain high, with next-day delivery expectations for 95% of tracked SKUs. Cell and gene therapies posted the highest 4.36% CAGR outlook, albeit from a low volume base, underscoring the intensifying need for ultra-cold supply chains linked to academic hospitals. Over-the-counter drugs benefit from click-and-collect and mail-order channels, yet margin compression persists because e-commerce giants negotiate bulk rates.

Biologics and biosimilars command premium pricing that justifies dedicated 2-8 °C lanes equipped with dual-probe validation. Vaccine logistics stabilizes post-pandemic but remains strategically significant as the UK maintains stockpiles for future outbreaks. Clinical trial materials expand alongside the MHRA’s streamlined regulatory regime, which is expected to cut start-up timelines by 40% and therefore elevate shipment frequency. Medical devices and diagnostics see modest but consistent growth, correlated with telehealth uptake that shifts distribution closer to households. Collectively, product-type diversification compels carriers to cultivate multi-temperature capabilities and nuanced regulatory acumen.

Geography Analysis

England dominated the UK pharmaceutical logistics market in 2025, supported by dense healthcare infrastructure and proximity to Heathrow, which handles over 50% of the nation’s pharma air cargo. London–South-East corridors integrate extensive warehouse parks equipped with cross-dock cold rooms that funnel ATMP imports to specialist hospitals in under six hours. The UK pharmaceutical logistics market share concentration in this region is reinforced by AstraZeneca’s GBP 650 million (USD 827.46 million) expansion in Liverpool and Cambridge, which adds regional freight volumes across biologics lanes.

Scotland represents the second-largest cluster, buoyed by government life-science grants and university partnerships in Glasgow and Edinburgh that lure ATMP trial sponsors. Cold-chain infrastructure near Edinburgh Airport is scaling through modular freezer farms that integrate renewable-energy micro-grids to mitigate power-cost risk. Wales exhibits smaller absolute volumes but the highest per-capita e-commerce penetration for medicines, spurring last-mile couriers to pilot electric vans across hilly rural routes. Regional NHS digital-health initiatives also stimulate warehousing demand for telehealth kits.

Northern Ireland’s dual-access status positions it as a strategic logistics bridge. Belfast Harbor invests in GDP-certified container handling to streamline EU inbound flows, yet complex customs declarations under the Windsor Framework extend paper-processing times. Carriers that install automated declaration engines secure faster throughput and capture share. Ireland-to-Great Britain lanes carry increased ambient payloads for generics, but cold-chain expansion lags until infrastructural upgrades at Belfast International Airport conclude. Overall, geographic diversification strategies hinge on balancing infrastructure readiness, regulatory frictions, and demand density.

Competitive Landscape

The UK pharmaceutical logistics market features moderate concentration. DHL Supply Chain integrates robotics-enabled pick-and-pack lines in its Rugby hub, trimming cycle times for biologics shipments and integrating directly with NHS e-procurement portals. UPS Healthcare’s 2024 acquisition of Frigo-Trans added 430 specialized trailers, enhancing cold-chain reach from Germany to Northern England and elevating the firm’s cross-border compliance offerings. Kuehne Nagel deploys an AI-enhanced Control Tower in East Midlands that visualizes real-time lane performance and carbon footprints, aligning with NHS net-zero targets.

Specialists such as Movianto target clinical-trial logistics, operating GMP-compliant secondary packaging suites that add value in blinded-trial material preparation. Cool Cargo and Life Couriers UK focus on last-mile cryogenic transport, using small-format liquid nitrogen shippers and hand-carry protocols for autologous cell therapies. Digital entrants deploy platform models that match pharmacy demand with spare courier capacity, tapping into crowdsourced fleets under stringent onboarding checks.

Price competition remains rational due to high regulatory entry barriers. Integrated service portfolios and proven GDP audit histories differentiate incumbents, while cyber-security capabilities now factor into bidding scores for NHS tenders. Strategic partnerships proliferate; for instance, DHL and AstraZeneca signed a multi-year pact to co-develop ultra-cold storage pods colocated at manufacturing sites. Looking ahead, consolidation is likely as mid-tier players seek scale to absorb compliance and technology costs.

United Kingdom Pharmaceutical Logistics Industry Leaders

-

DHL Supply Chain

-

Life Couriers UK (Formerly Vision Logistics)

-

Kammac

-

Cencora, Inc.

-

UPS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: CEVA Logistics set aside GBP 150 million (USD 188.48 million) to boost its pharmaceutical cold-chain network, adding GDP-compliant sites in Manchester and Edinburgh equipped with real-time temperature tracking for delicate medicines.

- August 2024: DHL Supply Chain bought a specialist pharma-logistics firm for about GBP 85 million (USD 106.80 million), gaining extra regulatory know-how and chilled storage across several prime UK hubs.

- July 2024: Kuehne + Nagel teamed with a British drug maker on a GBP 120 million (USD 150.78 million) venture to build dedicated cold-chain warehouses and custom transport fleets serving England and Scotland.

- June 2024: UPS Supply Chain Solutions unveiled a GBP 95 million (USD 119.37 million) healthcare expansion, including new distribution centers in Birmingham and Glasgow featuring advanced monitoring and serialization tools.

United Kingdom Pharmaceutical Logistics Market Report Scope

Pharmaceutical logistics involves manufacturing, processing, and shipping materials and resources. Pharmaceutical Logistics companies also undertake activities related to handling finished products for customers.

Transporting healthcare products requires sophisticated logistics to ensure the integrity of pharmaceutical shipments. This involves specialized equipment, dedicated storage facilities, standardized handling procedures, and strong collaboration among cold chain partners. Logistics companies play a crucial role in the operations of pharmaceutical firms.

The United Kingdom Pharmaceutical Logistics market is segmented by product (generic drugs, branded drugs), by mode of operation (cold chain transport, non-cold chain transport), by application (bio pharma, chemical pharma), by mode of transport (air, rail, road, and sea) The report offers market size and forecast for United Kingdom Pharmaceutical Logistics Market in value (USD) for all the above segments.

| Transportation | Road Freight |

| Air Freight | |

| Sea Freight | |

| Rail Freight | |

| Warehousing and Storage | |

| Value-added Services and Others |

| Cold-Chain Logistics |

| Non-Cold-Chain Logistics |

| Prescription Drugs |

| OTC Drugs |

| Biologics and Biosimilars |

| Vaccines and Blood Products |

| Clinical Trail Materials |

| Cell and Gene Therapies |

| Medical Devices and Diagnostics |

| Veterinary Medicine |

| Others |

| By Service Type | Transportation | Road Freight |

| Air Freight | ||

| Sea Freight | ||

| Rail Freight | ||

| Warehousing and Storage | ||

| Value-added Services and Others | ||

| By Mode of Operation | Cold-Chain Logistics | |

| Non-Cold-Chain Logistics | ||

| By Product Type | Prescription Drugs | |

| OTC Drugs | ||

| Biologics and Biosimilars | ||

| Vaccines and Blood Products | ||

| Clinical Trail Materials | ||

| Cell and Gene Therapies | ||

| Medical Devices and Diagnostics | ||

| Veterinary Medicine | ||

| Others |

Key Questions Answered in the Report

What is the projected value of the UK pharmaceutical logistics market in 2031?

The market is forecast to reach USD 14.32 billion by 2031, growing at a 4.06% CAGR.

Which service type leads UK pharmaceutical logistics revenues?

Transportation services dominate with 60.55% share as of 2025, reflecting the criticality of nationwide road-freight coverage.

How fast is the cold-chain segment expanding?

Cold-chain logistics is expected to grow at 5.62% CAGR from 2026 to 2031, the fastest among operation modes.

What factor most constrains UK pharma logistics capacity? A shortage of GDP-qualified drivers remains the principal bottleneck, negatively impacting CAGR by 0.3%.

A shortage of GDP-qualified drivers remains the principal bottleneck, negatively impacting CAGR by 0.3%.

Which product category is rising quickest?

Cell and gene therapies, though still niche, are forecast to expand at 4.36% CAGR through 2031, propelled by ATMP clinical trials.

How does Brexit influence logistics investment?

Regulatory independence under the Windsor Framework has spurred domestic warehousing and customs-automation spending, supporting long-term network resilience.

Page last updated on: