Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

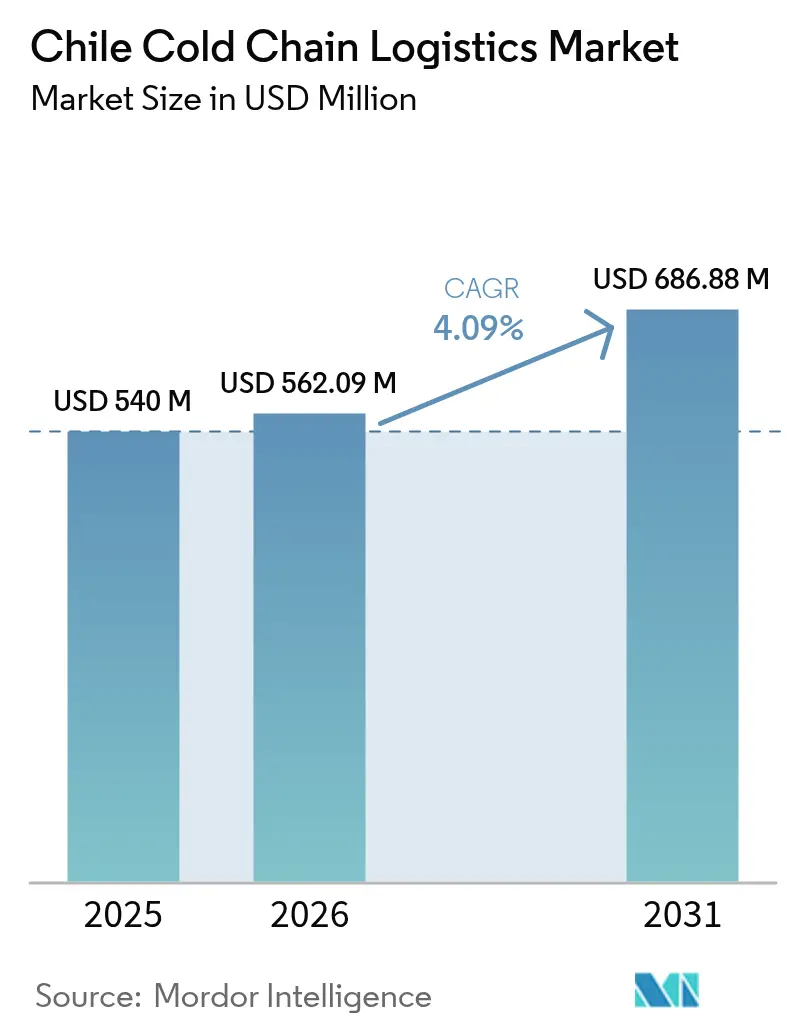

| Base Year Market Size (2025) | USD 540 Million |

| Market Size (2026) | USD 562.09 Million |

| Market Size (2031) | USD 686.88 Million |

| Growth Rate (2026 - 2031) | 4.09% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chile Cold Chain Logistics Market Analysis by Mordor Intelligence

The Chile Cold Chain Logistics Market size was valued at USD 540 million in 2025 and estimated to grow from USD 562.09 million in 2026 to reach USD 686.88 million by 2031, at a CAGR of 4.09% during the forecast period (2026-2031).

Rising export volumes of high-value perishables, resilient domestic demand for frozen foods, renewable-energy incentives for temperature-controlled warehouses, and digital traceability mandates combine to sustain capital flows into temperature-controlled storage, transport, and value-added services. Global buyers reward exporters that document uninterrupted cold conditions from field to ship, prompting investments in IoT monitoring, ammonia-based refrigeration, and portside reefer capacity. Operators also improve energy efficiency through photovoltaic rooftops and battery storage to mitigate peak-season power tariffs, while micro-fulfillment hubs shorten last-mile delivery for e-grocery in Santiago, Valparaíso, and Concepción. Low market concentration enables regional specialists to coexist with multinationals pursuing acquisitions to build nationwide networks.

Key Report Takeaways

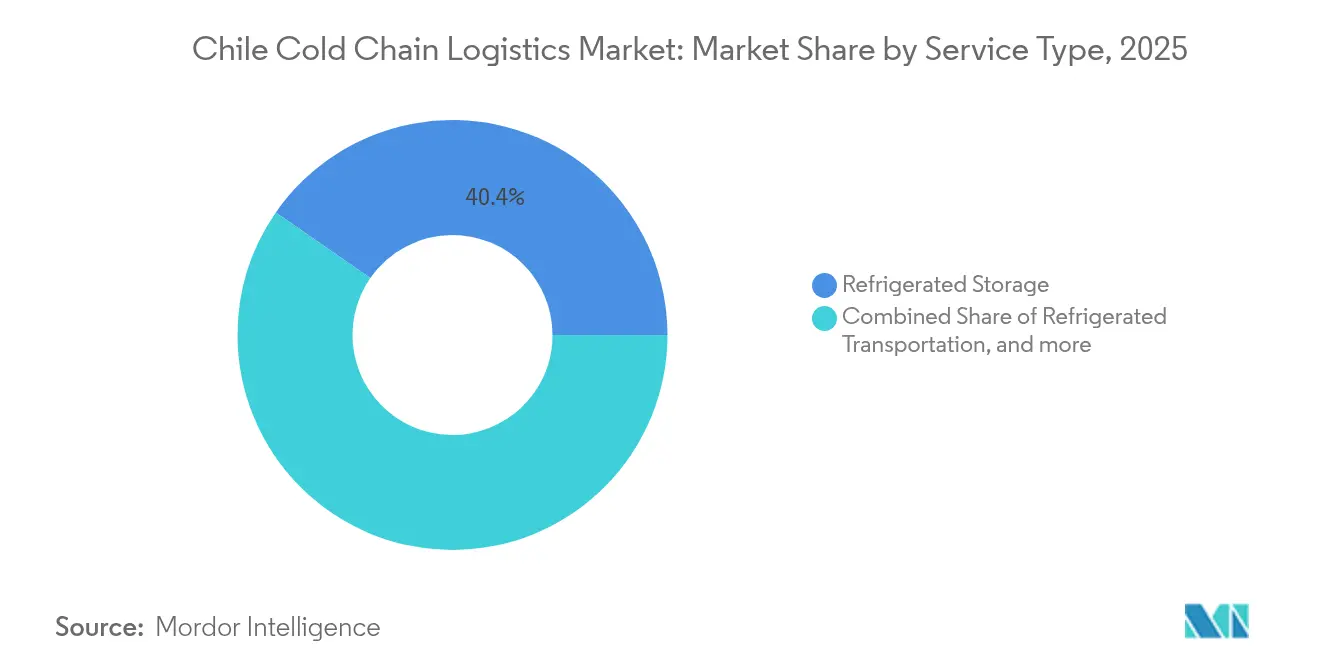

- By service type, refrigerated storage led with 40.35% of Chile cold chain logistics market share in 2025; value-added services are forecast to expand at a 4.12% CAGR through 2031.

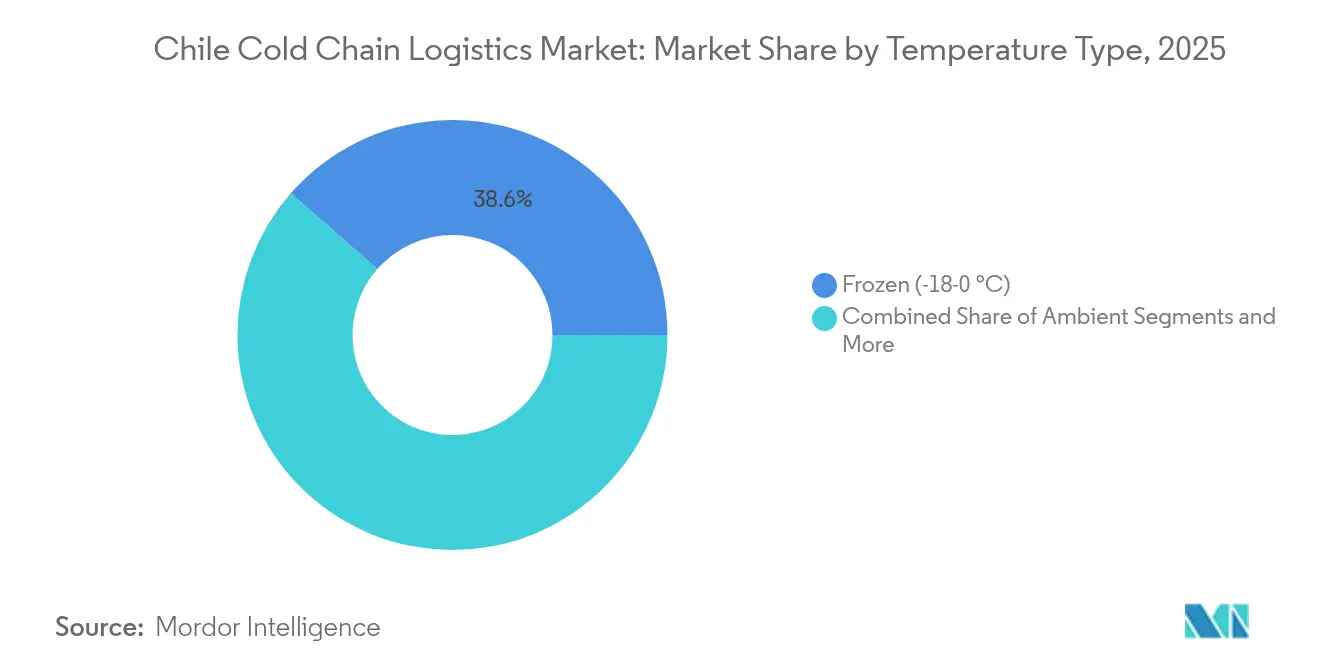

- By temperature type, the frozen (-18 to 0 °C) band captured 38.55% of Chile cold chain logistics market share in 2025, while deep-frozen/ultra-low segments below -20 °C are projected to advance at a 4.68% CAGR to 2031.

- By application, fruits & vegetables accounted for 20.55% of the Chile cold chain logistics market size in 2025; vaccines & clinical-trial materials are set to grow at a 5.06% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Chile Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging fresh-fruit export volumes | +1.2% | Valparaíso, O’Higgins, Maule | Medium term (2-4 years) |

| Expansion of the salmon export industry | +0.8% | Los Lagos, Aysén | Long term (≥ 4 years) |

| Growing domestic frozen-food demand | +0.6% | Santiago, Valparaíso, Concepción | Short term (≤ 2 years) |

| Government incentives for PV-powered cold warehouses | +0.4% | Atacama, Antofagasta, nationwide | Long term (≥ 4 years) |

| Micro-fulfillment cold hubs for e-grocery | +0.3% | Santiago, Valparaíso, Concepción | Medium term (2-4 years) |

| Blockchain-based export-traceability mandates | +0.2% | National export corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Fresh-Fruit Export Volumes

Cherry output is projected to reach 500,000 tons in marketing year 2024/25, up 6.8% year-on-year, reinforcing capital commitments to pre-cooling tunnels, controlled-atmosphere rooms, and 2,700 new reefer plugs installed at San Antonio port[1]F.A.S., “Chile Stone Fruit Annual,” fas.usda.gov. Table-grape exports are also poised to grow 7.8% to 570,000 tons, expanding the Chile cold chain logistics market as operators adopt modified-atmosphere liners and 0.5 °C cold-treatment regimes that add USD 1,000–2,000 to container costs yet guarantee market access in China. Blockchain pilots document each temperature checkpoint, preserving reputational premium in Asia. These dynamics stimulate suppliers of insulated containers, reefer vessels, and IoT probes, locking in mid-term revenue visibility.

Expansion of the Salmon Export Industry

Chile shipped 782,076 tons of salmon worth USD 6.37 billion in 2024 as processors optimized outbound logistics from Puerto Montt to Santiago airport, underpinning cold-chain service demand. Vertical integration drives investments in blast freezers and –35 °C plate freezers, while UNIDO-supported ammonia systems at Marine Farm cut energy use by 10% and trimmed 1.23 million kg CO₂, illustrating regulatory-aligned cost savings. Government scrutiny of farming density pushes operators toward efficiency, rewarding logistics partners that offer telemetry, hygienic design, and contingency power.

Growing Domestic Frozen-Food Demand

Urban households increased freezer ownership and online grocery orders during the pandemic, prompting logistician Loginsa to manage 75,000 SKUs across 22 sites until its 2024 sale to Ransa. National food waste of 5.18 million tons in 2021—48% fruits and 16% vegetables—highlights the scope for real-time temperature monitoring to extend shelf life. Retail chains are enlarging frozen aisles, stimulating multiclient warehouses that guarantee –18 °C across peak-season load spikes. This steady domestic pull complements export-centric revenue, flattening seasonal utilization curves.

Government Incentives for PV-Powered Cold Warehouses

The Energy Savings Insurance program underwrites photovoltaic retrofits for small and medium facilities, unlocking project financing of USD 36 million annually. High solar-insolation zones in Atacama and Antofagasta adopt rooftop arrays and 2-hour lithium BESS to shave peak tariffs, an approach endorsed by White & Case analysis showing 6 GW of BESS in the pipeline. Enel Chile’s goal of 100% renewable electricity by 2040 reinforces confidence in green power availability, while insurance-backed savings contracts hedge performance risk.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| First-mile challenges across Andean terrain | –0.7% | Rural fruit belts, Andean corridors | Long term (≥ 4 years) |

| Limited reefer-truck availability | –0.5% | National, acute in southern regions | Medium term (2-4 years) |

| Peak-season electricity tariff spikes | –0.4% | Industrial clusters nationwide | Short term (≤ 2 years) |

| Shortage of natural-refrigerant technicians | –0.3% | Urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

First-Mile Challenges Across Andean Terrain

Chile’s 4,300-km length and steep altitudes complicate time-sensitive haulage from interior orchards to coastal pack houses, adding fuel, transit hours, and spoilage risk[2]International Transport Forum, “Logistics Observatory for Chile,” itf-oecd.org. Quarantine zones now cover one-fifth of cherry groves, forcing detours that raise cost per pallet and crowd the limited reefer supply. Public-private plans such as USD 5 billion “Chile Over Rails” freight upgrades promise relief by 2027, yet climate-driven droughts and landslides still threaten continuity.

Limited Reefer-Truck Availability

Seasonal export peaks absorb nearly all 300-hp tractor units fitted with dual-zone reefers, squeezing fisheries and pharma shippers competing for capacity. Deployment of CO₂ transcritical systems lags amid high ambient temperatures, and ammonia trailers demand technicians who are scarce and expensive. Smaller haulers wrestle with capex hurdles and insurance premiums, perpetuating a capacity pinch that curbs swift market-share gains for chilled categories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Storage Dominates, Value-Added Gains Momentum

Refrigerated storage contributed 40.35% to the Chile cold chain logistics market share in 2025, underpinning large-scale cherry and salmon export cycles that rely on palletized inventories awaiting vessel slots. Consolidators such as Ice Star now operate eight nationwide depots exceeding 3 million ft³, while public warehouses lease modular cells to smaller packers seeking flexible space. The Chile cold chain logistics market size linked to storage expands modestly as capacity additions match crop growth, yet operators differentiate through ammonia retrofits, solar rooftops, and HACCP-certified handling protocols.

Value-added services capture shippers eager for end-to-end solutions encompassing ripeness profiling, RFID tagging, and export paperwork. At a projected 4.12% CAGR, this niche outpaces headline growth by integrating data analytics and blockchain records that pre-populate customs forms. IoT integration enables remote alarms that reduce incident-related cargo claims and justify premium rates. M&A activity favors firms with bespoke packing lines, pushing segment operators to form alliances with automation vendors.

By Temperature Type: Frozen Leads, Ultra-Low Surges

The frozen band between -18 and 0 °C accounted for 38.55% of Chile's cold chain logistics market share in 2025, anchored by salmon fillets and frozen berries destined for North America and Europe. Blast freezers in Puerto Montt achieve -35 °C core temperature within 4 hours, curbing histamine formation and securing higher export grades. The Chile cold chain logistics market size in the deep-frozen/ultra-low bracket is forecast to climb fastest at 4.68% CAGR as vaccination campaigns, mRNA trials, and biologic import flows demand -20 °C to -80 °C stability, especially for Santiago-based depots supplying regional hospitals.

Chilled 0 to 5 °C assets remain critical for fresh grapes, peaches, and avocados with voyage times of 20-30 days to Shanghai. Ambient zones handle processed foods but contribute minimal incremental revenue. Natural refrigerant uptake varies: CO₂ is favored in southern climates, while low-charge ammonia dominates in central valleys, contingent on technician availability and safety compliance.

By Application: Produce Still Largest, Pharma Tops Growth Charts

Fruits & vegetables held 20.55% share of the Chile cold chain logistics market size in 2025, reflecting counter-seasonal shipping windows that align with Northern Hemisphere winter demand. Controlled-atmosphere reefer containers and rapid-cool tunnels reduce respiration and maintain firmness, sustaining exporter premiums. However, volume growth moderates as orchard acreage stabilizes, prompting brokers to explore higher-margin segments.

Vaccines & clinical-trial materials are poised for a 5.06% CAGR through 2031, leveraging Santiago’s clinical-research footprint and Ministry of Health immunization programs. Specialized 2 to 8 °C lanes and dry-ice services attract global CROs that require GxP-compliant handlers. Meat & poultry, fish & seafood, and ready-to-eat meals post steady mid-single-digit expansion as consumer lifestyles shift toward convenience and protein diversification.

Geography Analysis

Metropolitan Santiago anchors the Chile cold chain logistics market with the densest concentration of 3PL hubs, pharmaceutical depots, and cross-docks linking central valleys to ports and airports. DP World’s 2,700 reefer connections at San Antonio port support record cherry throughput, mitigating bottlenecks during December peaks. Inland rail upgrades promise to trim door-to-dock times by 20% once the “Chile Over Rails” spine doubles freight volumes to 21 million tons by 2027.

Los Lagos and Aysén form a salmon-centric logistics corridor where low ambient temperatures complement blast-freezing economics. Processors relocate closer to Route 5 intersections, shaving hours off truck legs to Santiago airport and Valparaíso por. Emerging clusters of PV-powered cold stores in Atacama and Antofagasta leverage 2,900 kWh/m² annual solar resource, lowering levelized energy costs for mining-catered food services.

Longitudinal extremes challenge uniform service delivery; the Andean cordillera restricts east-west corridors, forcing reliance on a limited number of paved passes subject to snow closures. The proposed USD 10 billion Bioceanic Corridor would diversify inland routes, enhancing resilience if funding materializes.

Climate variability causes irrigation stress in Coquimbo while intensifying rain events in Biobío, compelling adaptive design of refrigerated warehouses to withstand both heatwaves and floods.

Competitive Landscape

Low concentration defines the Chile cold chain logistics market. IceStar’s June 2024 acquisition of Mega Frio Chile added eight sites and signaled an appetite for horizontal integration. Emergent Cold LatAm simultaneously scaled to 157 million ft³ region-wide, positioning itself for multi-country service contracts.

Technology adoption differentiates competitors: IoT sensor suites broadcast live dashboards that let shippers intervene before deviations breach setpoints, reducing spoilage and insurance claims. CEVA Logistics’ FORPLANET initiative deploys sustainable fuels and 1,000 low-carbon trucks, catering to exporters seeking ESG-aligned partners. DHL, Kuehne + Nagel, and DSV leverage global pharma certifications, yet local independents retain share through bespoke fruit-handling know-how and flexible pricing.

Future rivalry centers on ultra-low storage, blockchain integration, and renewable-powered depots. Training alliances with technical institutes aim to expand the pool of natural-refrigerant specialists, while venture funding flows to startups offering AI route optimization and automated pallet shuttles. Given overlapping investments and moderate economies of scale, market leadership is expected to change hands primarily through mergers rather than through organic displacement.

Chile Cold Chain Logistics Industry Leaders

Megafrio Chile

Frio Romeral Limitada

Empresas Taylor

Transportes Nazar

Friofort SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Global Cold Chain Alliance released its 2025 Top 25 refrigerated logistics providers list, offering benchmarks for Chilean firms

- January 2025: UNK expanded to Mexico after securing Corfo funding, bringing IoT temperature-humidity monitoring to 50 clients across 200 Chilean and Mexican sites

- January 2025: DP World projected 75% growth in cherry volumes via San Antonio, citing newly installed MoorMaster units and extra reefer plugs.

- November 2024: CEVA Logistics launched the FORPLANET low-carbon sub-brand, achieving 26,000 tons emissions avoidance through sustainable fuels

Chile Cold Chain Logistics Market Report Scope

The technology and mechanism that allows for the secure delivery of temperature-sensitive goods and items along the supply chain are known as cold chain logistics. Any product that is perishable or is branded as such would almost certainly need cold chain management. A complete background analysis of Chile's cold chain logistics market, including the assessment of the economy and contribution of sectors in the economy, a market overview, market size estimation for key segments, emerging trends in the market segments, market dynamics and geographical trends, and COVID-19 impact, is covered in the report.

Chile's cold chain logistics market is segmented by service (storage, transportation, and value-added services), temperature type (chilled, frozen, and ambient), and end-user (horticulture ((fresh fruits and vegetables), dairy products (milk, ice cream, butter, etc.); meat, fish, and poultry; processed food products; pharma, life sciences, chemicals; and other end users). The report offers market size and forecasts for all the above segments in value (USD).

By Service Type

| Refrigerated Storage | Public Warehousing |

| Private Warehousing | |

| Refrigerated Transportation | Road |

| Rail | |

| Sea | |

| Air | |

| Value-Added Services |

By Temperature Type

| Chilled (0–5 °C) |

| Frozen (-18–0 °C) |

| Ambient |

| Deep-Frozen / Ultra-Low (less than-20 °C) |

By Application

| Fruits & Vegetables |

| Meat & Poultry |

| Fish & Seafood |

| Dairy & Frozen Desserts |

| Bakery & Confectionery |

| Ready-to-Eat Meals |

| Pharmaceuticals & Biologics |

| Vaccines & Clinical Trial Materials |

| Chemicals & Specialty Materials |

| Other Applications |

| By Service Type | Refrigerated Storage | Public Warehousing |

| Private Warehousing | ||

| Refrigerated Transportation | Road | |

| Rail | ||

| Sea | ||

| Air | ||

| Value-Added Services | ||

| By Temperature Type | Chilled (0–5 °C) | |

| Frozen (-18–0 °C) | ||

| Ambient | ||

| Deep-Frozen / Ultra-Low (less than-20 °C) | ||

| By Application | Fruits & Vegetables | |

| Meat & Poultry | ||

| Fish & Seafood | ||

| Dairy & Frozen Desserts | ||

| Bakery & Confectionery | ||

| Ready-to-Eat Meals | ||

| Pharmaceuticals & Biologics | ||

| Vaccines & Clinical Trial Materials | ||

| Chemicals & Specialty Materials | ||

| Other Applications | ||

Key Questions Answered in the Report

What is the 2026 value of the Chile cold chain logistics market?

The market stands at USD 562.09 million in 2026.

How fast will Chile’s cold chain logistics grow through 2031?

It is forecast to expand at a 4.09% CAGR to reach USD 686.88 million.

Which service type currently holds the largest share?

Refrigerated storage leads with 40.35% share in 2025.

Which application segment is growing the fastest?

Vaccines and clinical-trial materials are projected to grow at 5.06% CAGR.

Why are renewable-energy incentives important for cold warehouses in Chile?

They lower operating costs and hedge against peak-season electricity tariffs.

How concentrated is the competitive landscape?

The top five players control less than 35% of capacity, indicating moderate fragmentation.

Page last updated on: