Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

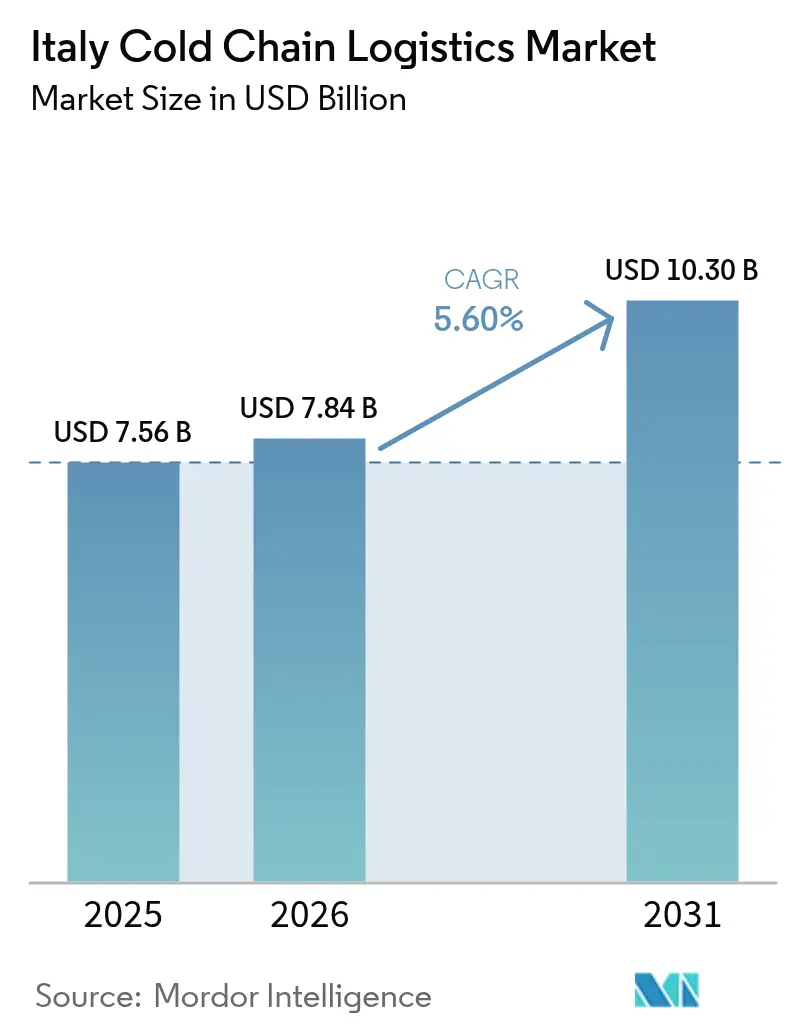

| Base Year Market Size (2025) | USD 7.56 Billion |

| Market Size (2026) | USD 7.84 Billion |

| Market Size (2031) | USD 10.30 Billion |

| Growth Rate (2026 - 2031) | 5.60% CAGR |

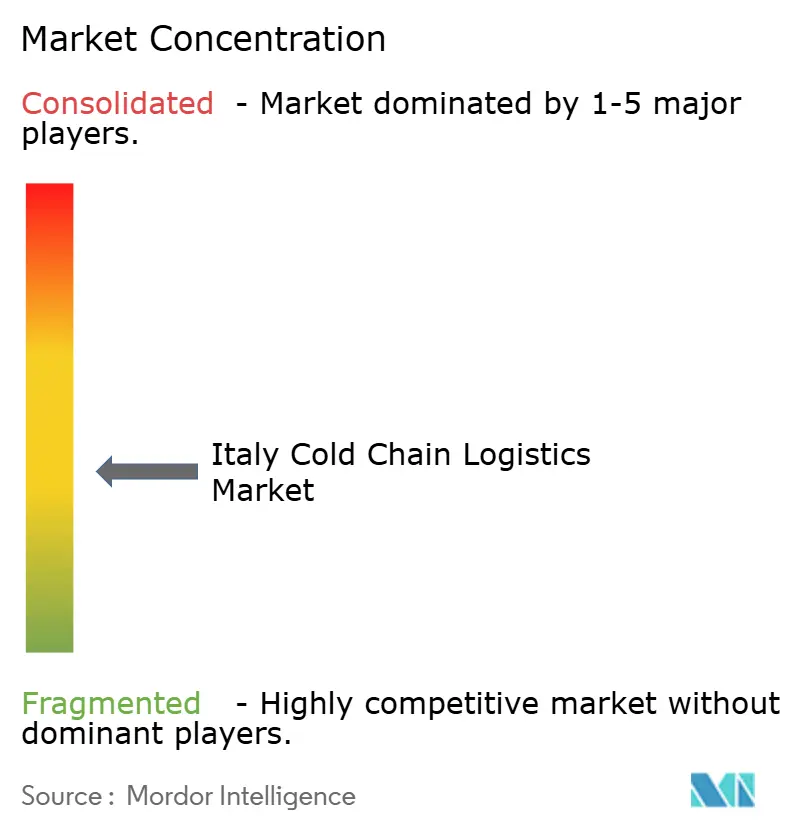

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Cold Chain Logistics Market Analysis by Mordor Intelligence

The Italy cold chain logistics market size is expected to grow from USD 7.56 billion in 2025 to USD 7.84 billion in 2026 and is forecast to reach USD 10.30 billion by 2031 at a 5.60% CAGR over 2026-2031.

Robust public-sector financing under the EU Recovery and Resilience Facility (RRF) is modernizing temperature-controlled warehousing, while supermarket consolidation is prompting in-house distribution networks that lift service standards and margins. Blockchain-verified temperature records are now mandatory in high-value pharmaceutical and premium food movements, accelerating digital adoption across the Italy cold chain logistics market. Renewable refrigerant retrofits reduce energy costs and align with net-zero targets, helping operators justify capital expenditure despite tight margins. Planned LNG-powered reefer services between mainland and island ports signal modal diversification that will gradually ease the historic road-transport dependency of the Italy cold chain logistics market.

Key Report Takeaways

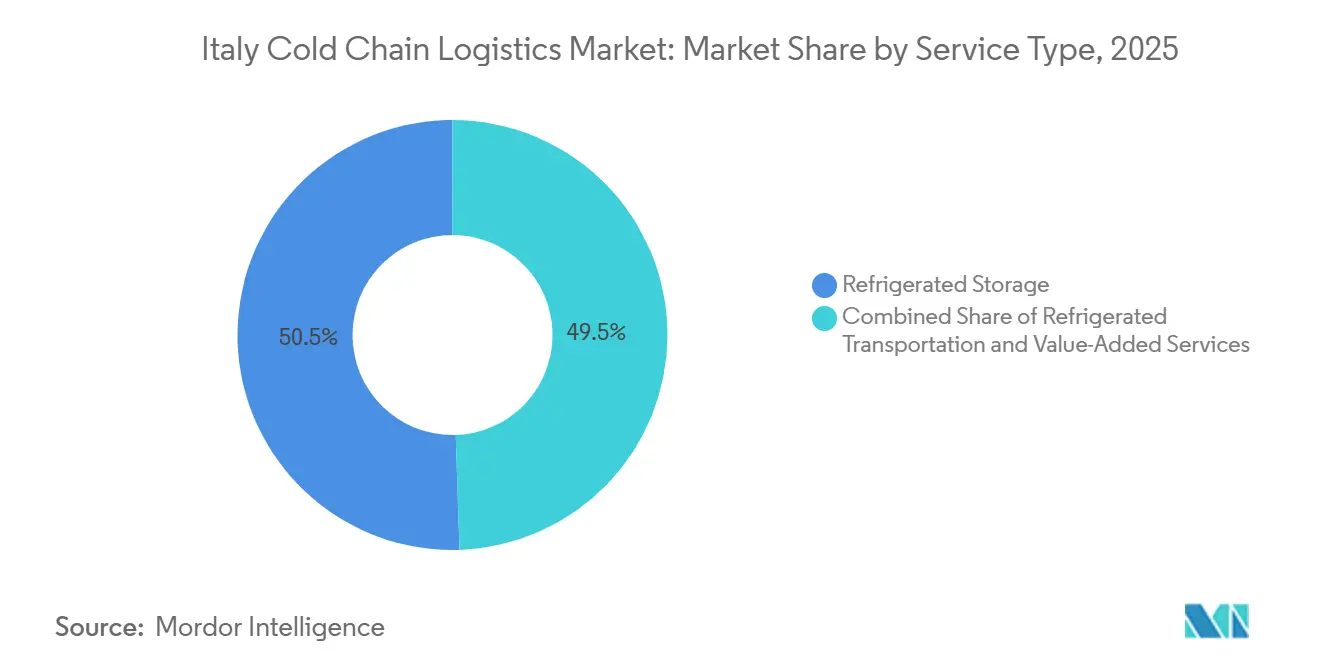

- By service type, refrigerated storage led the Italy cold chain logistics market share with 50.51% market share in 2025. Value-added services is projected to expand at a 7.15% CAGR through 2031.

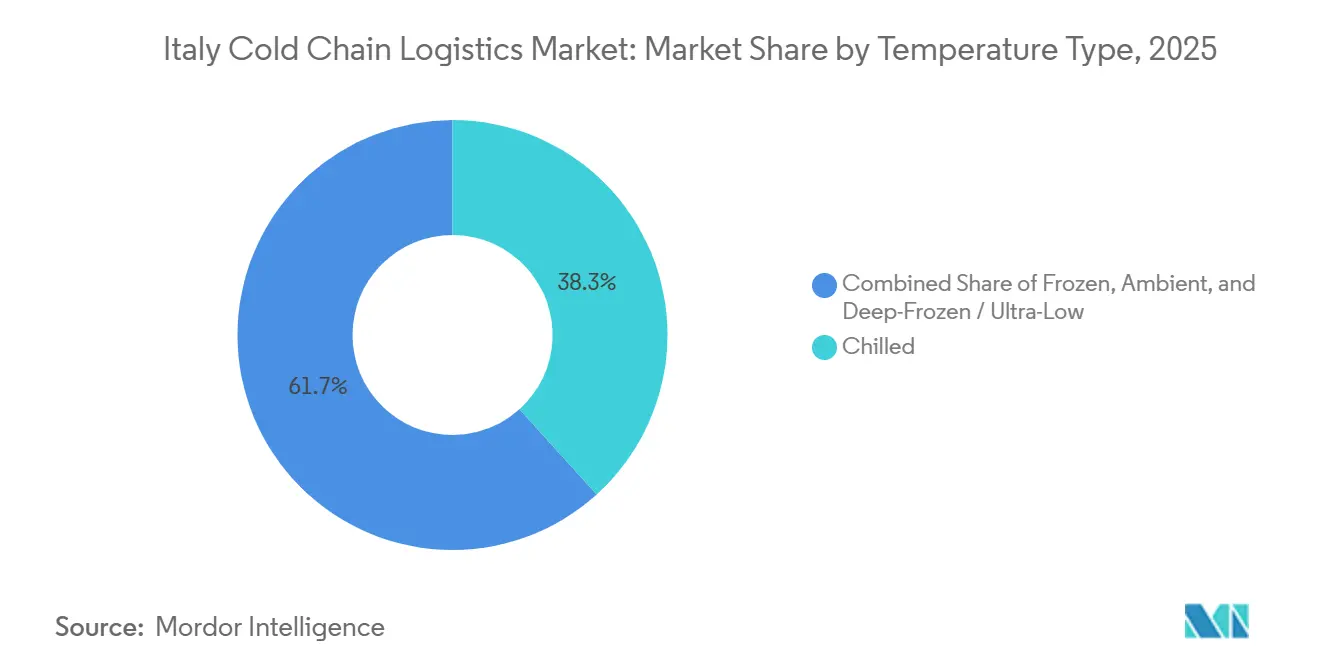

- By temperature type, chilled accounted for a 38.29% share of the Italy cold chain logistics market size in 2025, while frozen is advancing at a 6.17% CAGR through 2031.

- By application, dairy and frozen desserts held 22.45% share of the Italy cold chain logistics market size in 2025, whereas pharmaceuticals and biologics is forecast to grow at a 6.92% CAGR to 2031.

- By region, Northern Italy accounted for 31.03% of the 2025 value; Central Italy recorded the highest projected CAGR of 7.80% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of organised retail & supermarket cold chains | +1.1% | National, with a concentration in Northern Italy's urban centers | Medium term (2-4 years) |

| Rising export of premium frozen ready meals within the EU | +0.7% | Northern Italy, Central Italy, with export corridors to EU markets | Long term (≥ 4 years) |

| EU RRF grants driving energy-efficient cold-store retrofits | +0.9% | National, with priority allocation to Southern Italy and the Islands | Medium term (2-4 years) |

| Blockchain-based temperature-traceability adoption | +0.6% | National, with early adoption in the pharmaceutical and premium food segments | Long term (≥ 4 years) |

| Expansion of LNG-powered reefer maritime routes | +0.5% | Coastal regions, particularly Genoa, Naples, and Sicilian ports | Long term (≥ 4 years) |

| National food-waste reduction targets are prompting cold distribution | +0.8% | National, with emphasis on retail and foodservice cold chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth of Organised Retail & Supermarket Cold Chains

Consolidated grocery banners are scaling proprietary cold hubs to protect margins and product freshness. Conad’s 3,300-store network deploys multi-temperature cross-docks that cut dwell time and shrinkage. Esselunga invested EUR 231 million (USD 251.79 million) in new automated frozen chambers and shuttle systems during 2024 to support its e-commerce push, raising the competitive bar for third-party providers[1]Esselunga, “ENG 2024 1H v_3,” esselunga.it . Supermarkets now demand end-to-end temperature visibility, compelling logistics partners to add IoT sensors and blockchain reporting. Sustainability mandates from Coop Italia require renewable energy sourcing at distribution centers, further inflating capital requirements. As retailers internalize critical lanes, outsourced operators must pivot to value-added packaging, labeling, and compliance services to stay relevant.

Rising Export of Premium Frozen Ready-Meals within the EU

Italian manufacturers leverage Mediterranean cuisine branding to grow frozen ready-meal exports, requiring faultless cold transit across EU corridors. Barilla’s Emilia-Romagna site now dedicates lines to frozen pasta bound for Germany and France, obliging carriers to offer GDP-certified reefer fleets. Ferrero’s dessert division applies blockchain stamps that validate temperature history, differentiating products on northern European shelves. The single-market framework removes customs frictions yet enforces strict hazard-analysis records, favoring established Italy cold chain logistics market participants able to guarantee seamless traceability. Continued export momentum widens revenue pools for cross-border service specialists.

EU RRF Grants Driving Energy-Efficient Cold-Store Retrofits

Operators adopting trans-critical CO₂ systems secure grants covering up to 40% of capex, shortening payback periods and cutting power bills. Southern warehouses in Campania and Sicily receive priority funding, helping rebalance historic geographic gaps. Grant eligibility hinges on documented kWh savings, pushing firms toward holistic rebuilds rather than piecemeal fixes. The policy links climate objectives with competitiveness, positioning early movers to win long-term, emission-constrained contracts in the Italy cold chain logistics market.

Blockchain-Based Temperature-Traceability Adoption

Pharmaceutical shippers now require immutable temperature logs that meet EU Good Distribution Practice. IBM Food Trust pilots with Recordati feature real-time alerts that enable route corrections before excursion thresholds are breached. Operators report 20% lower spoilage claims after deploying blockchain-anchored sensors, offsetting the cost of licensing. Premium food exporters mimic pharma standards to reinforce brand authenticity and combat counterfeits. Falling device costs will expand the adoption of biologics into mainstream dairy and meat chains over the forecast period. Logistics firms lacking digital reporting risk disqualification from high-value tenders, compressing legacy player market shares in the Italy cold chain logistics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing ammonia-based cold-store infrastructure safety risks | -0.8% | National, with a concentration on older Northern Italy facilities | Medium term (2-4 years) |

| Limited refrigerated rail capacity on key north–south corridors | -0.6% | National, particularly the Bologna-Naples corridor | Short term (≤ 2 years) |

| Port inspection bottlenecks are increasing dwell time for perishables | -0.5% | Coastal regions, particularly Genoa, Naples, and Sicilian ports | Short term (≤ 2 years) |

| Elevated cargo-insurance premiums for temperature excursions | -0.4% | National, with a higher impact on the pharmaceutical and premium food segments | Medium term (2-4 years |

| Source: Mordor Intelligence | |||

Ageing Ammonia-Based Cold-Store Infrastructure Safety Risks

Many depots erected in the 1980s still rely on ammonia systems nearing the end of their lifespans. Leak incidents trigger costly evacuations, stricter labor-inspector audits, and rising insurance deductibles. Operators must choose between EUR-million-level refits or full-system replacement with natural refrigerants that comply with EU F-Gas rules. Consolidators with stronger balance sheets are acquiring sub-scale warehouses, funding safety upgrades, and unlocking economies of scale. Smaller firms unable to finance compliance risk exit, marginally tempering overall Italy cold chain logistics market growth.

Limited Refrigerated Rail Capacity on Key North–South Corridors

Civil works on the Bologna-Bari and Florence-Empoli lines curtailed reefer slot availability for eight months in 2025, forcing cargo back onto trucks[2]Kuehne+Nagel, “Civil works on rail networks in Italy expected to cause delays,” mykn.kuehne-nagel.com . Passenger-train prioritization further narrows freight windows, hindering modal-shift targets. Until upgrades are delivered in 2027-2028, intermodal operators face transit unreliability that discourages contract commitments from food exporters. Road haulage therefore retains a dominant role, sustaining greenhouse-gas output and exposure to fuel-price volatility across the Italy cold chain logistics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Value-Added Diversification Supports Margins

Refrigerated storage held a dominant 50.51% share of the Italy cold chain logistics market size in 2025, supported by high entry barriers tied to land availability and construction cost. Value-added Services, including kitting, relabeling, and quality inspections, grow at a 7.15% CAGR, signaling customer willingness to outsource non-core tasks that accelerate time-to-shelf. The segment benefits from stable occupancy by grocery, meat, and dairy customers that sign multi-year leases. Within this category, public warehouses capture volume from SMEs, whereas private facilities operated by multinationals prioritize security and customized layouts. Integrators bundle these services with storage, lifting wallet share while reducing churn.

Refrigerated transportation endures driver shortages and volatile diesel prices. Fleet owners deploy route-optimization and invest in biomethane or electric reefer units to temper operating costs and meet emission caps. Road remains compulsory for the final 200 km legs, but rail and short-sea are gaining interest for trunk hauls, aided by LNG-capable vessels and temperature-controlled intermodal swap bodies. Air freight secures high-margin pharma lifts, offsetting its single-digit volume share. The competitive mosaic underscores how technology and asset flexibility determine profitability inside the Italy cold chain logistics market.

By Temperature Type: Chilled Leadership Meets Frozen Acceleration

The frozen range (-18 °C to 0 °C) is advancing at a 6.17% CAGR through 2031 in Italy cold chain logistics market size, outpacing overall demand as consumers embrace convenience meals with long shelf life. Chilled operations, while still forming 38.29% of 2025 revenue, contend with shorter inventory cycles and stricter lead-time expectations from fresh produce growers. Supermarket private-label frozen assortments widened by 9% SKUs during 2025, prompting logistics providers to build extra sub-zero chambers with high-density racking. Operators hedge by designing multi-temperature halls capable of dynamic allocation between chilled and frozen pallets, enhancing asset utilization.

Deep-frozen/ultra-low facilities cater to vaccine and cell-therapy pipelines, where -70 °C freezers and redundant power supply justify premium rates. Ambient-controlled rooms round out pharmaceutical portfolios, housing blister packs or APIs sensitive to heat but not requiring refrigeration. Pfizer’s updated COVID-19 vaccine formula tolerates 2-8 °C storage, easing distribution but still demanding a validated chain of custody[3]Pfizer Inc., “Positive CHMP opinion for LP.8.1-adapted COVID-19 vaccine,” pfizer.com . Temperature-specific expertise, therefore, differentiates operators and enables higher margin tiers within the Italy cold chain logistics market for specialized services.

By Application: Pharma Growth Recasts Compliance Norms

Dairy and frozen desserts accounted for 22.45% of the Italy cold chain logistics market size in 2025, anchored by a robust domestic cheese and gelato sector. Pharmaceuticals and biologics, clocking a 6.92% CAGR, drive process upgrades such as GDP certification, controlled-temperature vehicle fleets, and 24/7 monitoring centers. Shippers remunerate reliability, cushioning margin compression elsewhere. Volumes track household consumption patterns and peak tourism months.

Fruits and vegetables depend on rapid cross-docking and pre-cooling near farms, especially in Puglia and Sicily export clusters. Meat and poultry players extend shelf life via modified-atmosphere packaging, requiring low-variation temperature trucks. Ready-to-eat meals reap e-grocery momentum, amplifying last-mile refrigerated van demand. The diverse payload mix insulates the Italy cold chain logistics market from single-sector cyclicality.

Geography Analysis

Northern Italy’s industrial heartland secured 31.03% of the 2025 revenue in Italy cold chain logistics market share, benefiting from Milan and Turin consumption centers, dense motorway grids, and ports of Genoa and Trieste. Central Italy posts a 7.8% CAGR to 2031, catalyzed by RRF rail upgrades and Rome’s growing foodservice scene. Kuehne + Nagel’s USD 374 million Mantova campus uses 700 robots and rooftop photovoltaics to shave kilowatt draw, setting a new efficiency benchmark. Alpine rail tunnels facilitate the export of cheese, pork, and vaccines to Germany and Austria without border friction. However, congestion on the A4 and fuel emissions legislation may cap road tonnage growth[4].Supply Chain 247, “Kuehne+Nagel opens massive logistics hub for Adidas in Italy,” supplychain247.com

Central Italy’s logistics network is maturing quickly. EU funds finance last-mile road repairs and broadband links, enabling IoT sensor connectivity in rural produce depots. Pharmaceutical wholesalers around Rome benefit from proximity to the National Medicines Agency, speeding product release. Intermodal terminals near Ancona integrate Ro-Ro ferry schedules with refrigerated rail wagons, diversifying routing options for the Italy cold chain logistics market.

Southern and island territories still lag in the number of GDP-certified cold rooms, but SEZ incentives are luring investors. Renewable-powered seawater heat pumps installed at Palermo port cold sheds cut electricity bills by 20%, showcasing climate-smart innovation. Seafood exporters from Mazara del Vallo rely on daily reefer charters to Genoa, aided by LNG propulsion that meets sulphur caps. Tourism-driven seasonality complicates capacity planning, forcing 3PLs to balance peak summer ice cream demand with winter lulls. Nevertheless, policy support and resource endowments position the south as a medium-term growth engine.

Competitive Landscape

The Italy cold chain logistics market remains moderately fragmented. The top five operators control roughly 42% of revenue, leaving space for regional specialists that leverage personal relationships with cheese cooperatives and produce growers. International players are deepening their roots through acquisitions: Planzer bought Sifte Berti in January 2025, adding 7 depots and 200,000 m² of multi-temperature space. DSV’s EUR 14.3 billion (USD 15.44 billion) purchase of DB Schenker will rationalize overlapping reefer lanes and introduce shared control towers that heighten service density.

Retailers also enter the fray: NewPrinces’ planned EUR 200 million (USD 236 million) logistics upgrade following its Carrefour Italia takeover will install automated storage and pick-by-voice systems, tightening end-to-end control. Start-ups such as GreenChill deploy solar-powered micro-warehouses for last-mile grocery, challenging incumbents on agility.

Technology is the clear battleground: Operators lacking blockchain dashboards, AI-driven demand planners, and trans-critical CO₂ chillers face the threat of margin erosion and potential contract losses. To address these challenges, mid-sized firms are increasingly collaborating by leveraging shared user networks. This approach allows them to pool capital expenditures and enhance their competitiveness in securing national bids.

Italy Cold Chain Logistics Industry Leaders

Stef Italia

Lineage Logistics (Italy)

Safim Logistics

DHL Supply Chain Italy

Frigoscandia SpA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: DHL announced an expanded dedicated Airfreight Cold Chain Network to enhance its Life Sciences and Healthcare logistics capabilities. The expansion includes dedicated temperature-controlled routes (starting with Brussels–Cincinnati), more GDP-compliant hubs, and a branded Boeing 777 freighter to strengthen global pharma cold-chain transport infrastructure.

- December 2025: CEVA Logistics agreed to acquire Italian project logistics specialist Fagioli Group (100% stake), expanding its footprint in logistics services that include heavy and specialized transports.

- June 2025: Aenova Group invested in a refrigerated logistics warehouse in Italy, operational by 2026, for biologics and temperature-sensitive medicines, enabling integrated cold-chain distribution for pharmaceutical clients.

- May 2025: CEVA Logistics in Italy renewed and extended its contract with Magneti Marelli Parts and Services for another six years, managing storage and distribution at its large San Pietro Mosezzo logistics hub.

Italy Cold Chain Logistics Market Report Scope

By Service Type

| Refrigerated Storage | |

| Refrigerated Transportation | Road |

| Rail | |

| Sea | |

| Air | |

| Value-Added Services |

By Temperature Type

| Chilled (0-5°C) |

| Frozen (-18-0°C) |

| Ambient |

| Deep-Frozen / Ultra-Low (less than-20°C) |

By Application

| Fruits and Vegetables |

| Meat and Poultry |

| Fish and Seafood |

| Dairy and Frozen Desserts |

| Bakery and Confectionery |

| Ready-to-Eat Meals |

| Pharmaceuticals and Biologics |

| Vaccines and Clinical Trial Materials |

| Chemicals and Specialty Materials |

| Other Perishables |

By Italian Region (Value)

| Northern Italy |

| Central Italy |

| Southern Italy |

| Islands (Sicily and Sardinia) |

| By Service Type | Refrigerated Storage | |

| Refrigerated Transportation | Road | |

| Rail | ||

| Sea | ||

| Air | ||

| Value-Added Services | ||

| By Temperature Type | Chilled (0-5°C) | |

| Frozen (-18-0°C) | ||

| Ambient | ||

| Deep-Frozen / Ultra-Low (less than-20°C) | ||

| By Application | Fruits and Vegetables | |

| Meat and Poultry | ||

| Fish and Seafood | ||

| Dairy and Frozen Desserts | ||

| Bakery and Confectionery | ||

| Ready-to-Eat Meals | ||

| Pharmaceuticals and Biologics | ||

| Vaccines and Clinical Trial Materials | ||

| Chemicals and Specialty Materials | ||

| Other Perishables | ||

| By Italian Region (Value) | Northern Italy | |

| Central Italy | ||

| Southern Italy | ||

| Islands (Sicily and Sardinia) | ||

Key Questions Answered in the Report

How fast is the Italy cold chain logistics market expected to grow between 2026 and 2031?

It is projected to register a 5.6% CAGR, rising from USD 7.84 billion in 2026 to USD 10.30 billion by 2031

Which service category captures the largest share of cold-chain spending?

Refrigerated Storage leads with 50.51% of 2025 revenue, reflecting high barriers to entry and long-term customer contracts.

What is the fastest-growing regional market for temperature-controlled logistics?

Central Italy has the highest forecast momentum, with a 7.8% CAGR through 2031, boosted by EU-funded infrastructure upgrades.

Why are blockchain solutions gaining traction in Italian temperature-controlled transport?

Pharmaceutical and premium food shippers require immutable temperature records for compliance and brand protection, making blockchain an industry standard.

How is energy inflation affecting logistics operators?

Electricity and gas price spikes of 24–27% force operators to adopt renewable power and energy-efficient refrigeration.

How are EU sustainability policies influencing refrigeration investments?

RRF grants subsidize natural-refrigerant systems and energy-efficient retrofits, cutting operating costs and aligning operators with Green Deal targets.

Page last updated on: