Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

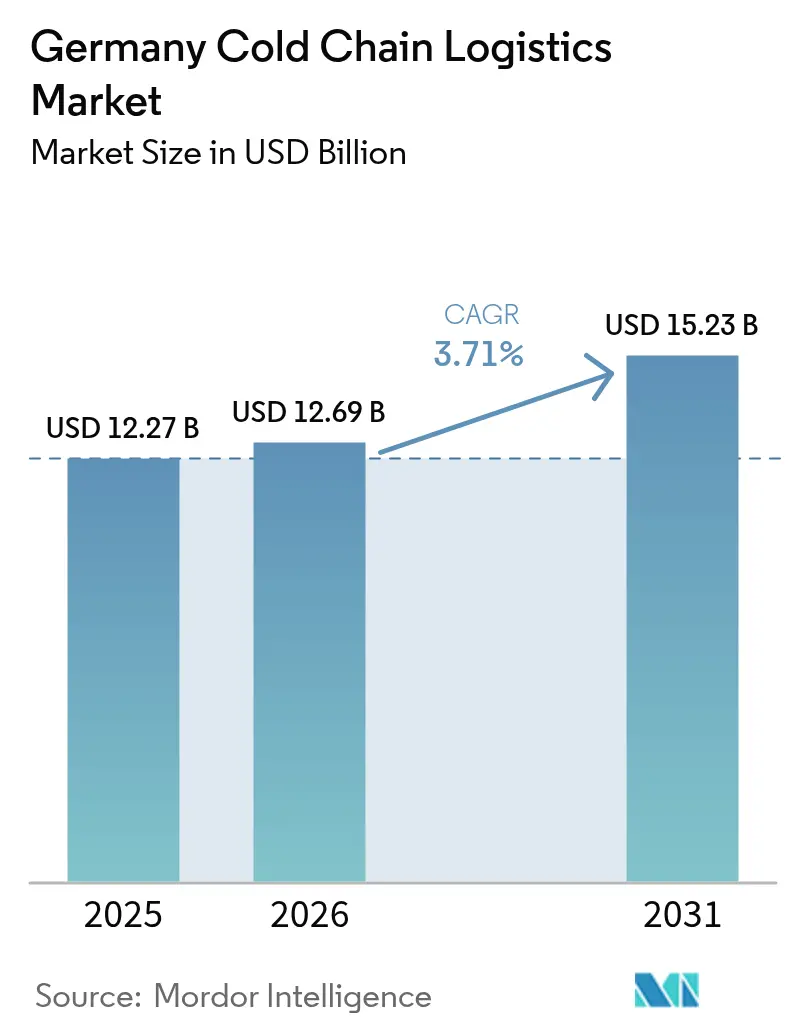

| Base Year Market Size (2025) | USD 12.27 Billion |

| Market Size (2026) | USD 12.69 Billion |

| Market Size (2031) | USD 15.23 Billion |

| Growth Rate (2026 - 2031) | 3.71% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Cold Chain Logistics Market Analysis by Mordor Intelligence

The Germany cold chain logistics market size is expected to increase from USD 12.27 billion in 2025 to USD 12.69 billion in 2026 and reach USD 15.23 billion by 2031, growing at a CAGR of 3.71% over 2026-2031.

Rising quick-commerce demand, EU-wide product-passport traceability rules, and deep-freeze automation schemes are reshaping competitive priorities. Operators are reallocating capital from basic haulage toward blockchain-enabled monitoring, AI-driven inventory planning, and rooftop-solar refrigeration that cushions energy-price volatility. Digital infrastructure spend now outpaces fleet expansion, reflecting a pivot in how the Germany cold chain logistics market creates value. Compliance pressures drive technology partnerships, while energy-efficient natural-refrigerant conversions gain momentum as HFC prices continue to rise.

Key Report Takeaways

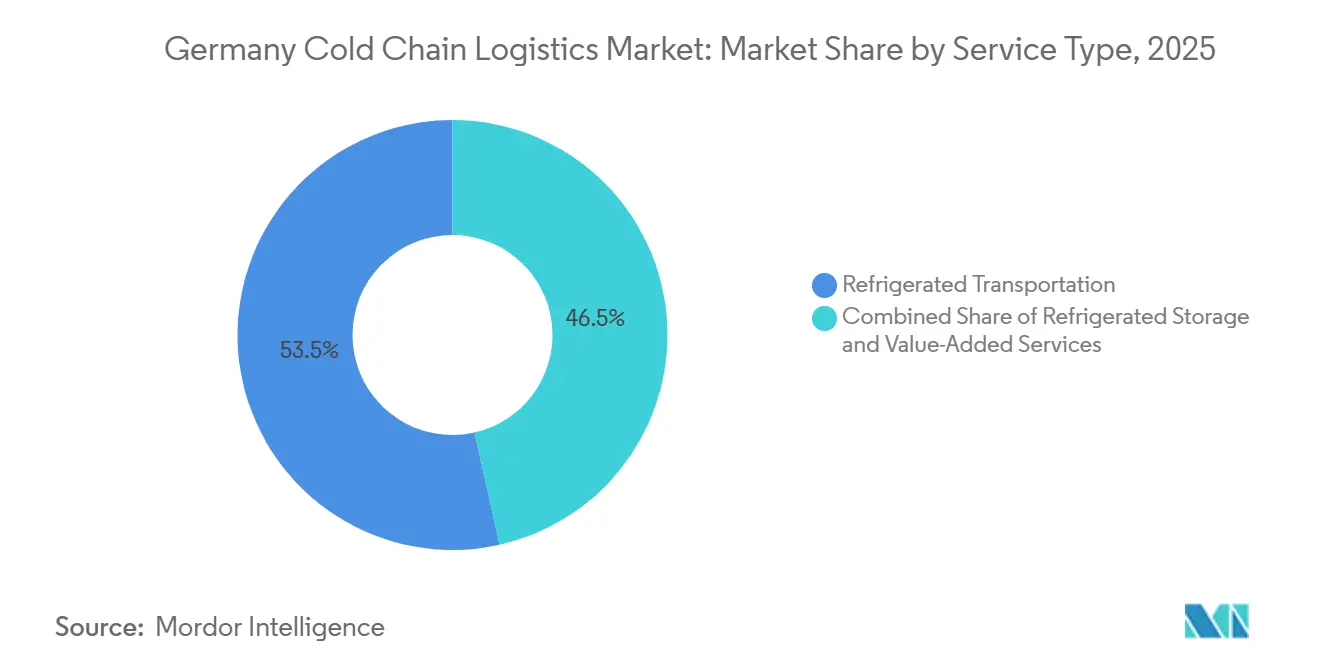

- By service type, refrigerated transport led with 53.51% of the Germany cold chain logistics market share in 2025, while value-added services are projected to expand at a 6.58% CAGR through 2031.

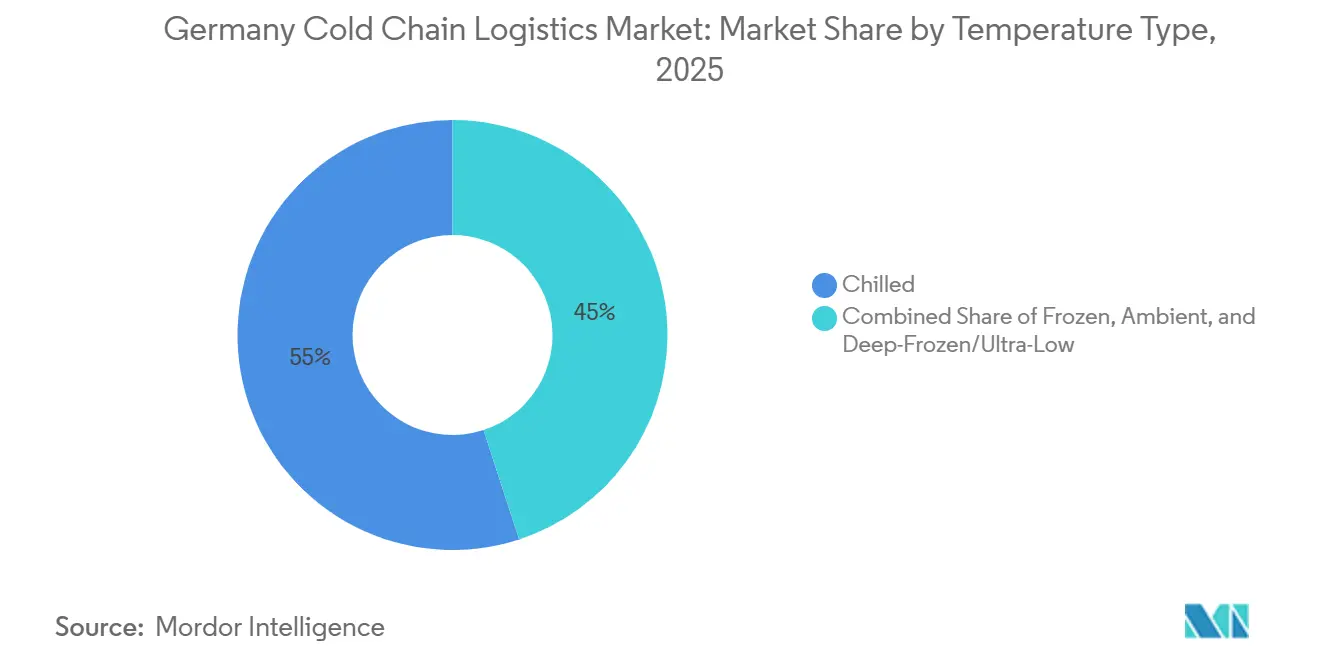

- By temperature type, chilled storage accounted for 55.02% of the Germany cold chain logistics market size in 2025, and the frozen segment is advancing at a 4.49% CAGR through 2031.

- By application, meat and poultry held a 32.47% share of the Germany cold chain logistics market size in 2025; pharmaceuticals and biologics record the highest projected CAGR at 6.01% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Meal-kit and 15-minute "q-commerce" fulfilment boom | +0.9% | National, concentrated in Berlin, Munich, Hamburg, Cologne metro areas | Short term (≤ 2 years) |

| EU Digital Product Passport traceability requirement | +1.1% | National, with EU-wide compliance mandate | Medium term (2-4 years) |

| Rooftop-solar powered refrigeration subsidy scheme | +0.4% | National, higher uptake in southern regions with better solar irradiance | Long term (≥ 4 years) |

| Cell-based meat pilot plants scaling in NRW and Bavaria | +0.3% | Regional, focused on North Rhine-Westphalia and Bavaria innovation clusters | Long term (≥ 4 years) |

| Mandatory temperature-logger GDP update (2025) for pharma | +0.8% | National, pharmaceutical distribution networks | Short term (≤ 2 years) |

| Deep-freeze robotics lowering energy per pallet hour | +0.6% | National, concentrated in large-scale cold storage facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Meal-kit and 15-minute Q-commerce Fulfilment Boom

Germany’s last-mile grocery segment processed EUR 2.8 billion (USD 3.29 billion) in 2026 revenue, operating across 85 cities and demanding micro-fulfilment hubs that maintain frozen, chilled, and ambient zones inside 200-400 m² footprints. AI-based demand forecasting has cut spoilage by 15-20%, while insulated e-cargo bikes sustain 2-8 °C for up to six hours, enabling emission-free urban delivery. The Germany cold chain logistics market now prioritizes energy-efficient refrigeration because power costs can reach 50% of an inner-city hub’s expenses. Retailers such as REWE retrofit stores with automated pick systems that process more than 100 orders per hour without breaching temperature thresholds[1]“Ecodesign for Sustainable Products Regulation,” European Commission, europa.eu.

EU Digital Product Passport Traceability Requirement

From 2026, all temperature-controlled food and pharma goods must carry a digital product passport tracking real-time location and temperature throughout the supply chain. German operators are investing EUR 150-200 million (USD 176.44-235.26 million) each year in RFID tags, IoT sensors, and blockchain platforms that automate compliance reporting and unlock data-driven route optimization. Early adopters cut energy use 8-12% by adjusting vehicle dispatch and warehouse set-points according to granular product data streams[2]“EU legislation to control F-gases,” Climate Directorate, climate.ec.europa.eu.

Mandatory Temperature-Logger GDP Update (2025) for Pharma

Revised GDP rules, effective January 2025, require continuous electronic temperature records for every refrigerated medicine moving through Germany. Logistics firms spent EUR 80-120 million (USD 94.10-141.15 million) on wireless sensors and cloud storage ahead of the deadline, replacing manual checks and slashing document-prep time by 60-70%. Integrators such as DHL Health Logistics now link monitoring dashboards with customer ERP systems, offering real-time visibility that commands premium pricing in the Germany cold chain logistics market.

Deep-Freeze Robotics Lowering Energy per Pallet Hour

Robotic deep-freeze systems cut energy consumption 30-40% and resolve technician shortages that left 60% of cold-store tech posts vacant in 2025. Installations by operators like Fiege Logistik save up to EUR 300,000 (USD 352,893) in electricity annually on 10,000-pallet sites and boost throughput 40-50% thanks to 24/7 unmanned picking. These gains help justify EUR 15-25 million (USD 17.64-29.40 million) capital outlays as HFC refrigerant prices jump 45-60% amid EU quota squeezes.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| HFC quota squeeze inflating refrigerant prices | -0.8% | National, affecting all refrigerated facilities and transport | Short term (≤ 2 years) |

| Severe ADR-qualified driver shortfall for reefer trucks | -0.9% | National, with acute shortages in long-haul corridors | Short term (≤ 2 years) |

| Rail-freight network works causing capacity pinch | -0.5% | National, concentrated on major north-south corridors | Medium term (2-4 years) |

| Rising insurance excesses after Listeria recall events | -0.3% | National, particularly affecting fresh food logistics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

HFC Quota Squeeze Inflating Refrigerant Prices

EU Regulation 2024/573 cut the HFC quota 40% for 2024-2027, pushing R404A prices to EUR 80-120 kg, more than double 2023 levels. Larger facilities now spend an extra EUR 150,000 (USD 176,446) a year refilling leaky systems. The Germany cold chain logistics market tilts toward natural refrigerants, yet conversion costs of EUR 500,000-2 million (USD 588,155-2.35 million) strain mid-size operators even after a 30-40% federal subsidy[3]“EU reports shortage of RAC technicians,” International Institute of Refrigeration, iifiir.org.

Severe ADR-Qualified Driver Shortfall for Reefer Trucks

ADR license retirements outstrip new certifications, leaving a 30-40% gap in drivers competent to haul temperature-controlled hazardous goods. Waiting lists for training stretch nine months, forcing carriers to pay 15-25% wage premiums and compelling the Germany cold chain logistics market to prioritize fleet automation, load consolidation, and modal shifts wherever rail or intermodal options exist[4]“Container handling statistics 2024,” Port of Hamburg Authority, hafen-hamburg.de .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Value-Added Services Capture Emerging Profit Pools

Refrigerated transport dominated the Germany cold chain logistics market with a 53.51% slice in 2025, but commoditization erodes margins as fuel costs climb and ADR drivers remain scarce. Value-added services, while smaller, are rising at a 6.58% CAGR and increasingly bundle compliance documentation, IoT sensor integration, and specialized packaging. This shift lifts average revenue per pallet as customers pay for end-to-end temperature visibility instead of isolated truck moves. Refrigerated storage modernizes through robotics that cut energy 20-30%, whereas airfreight retains a niche for high-value biologics requiring multilayer thermal protection.

Integrated providers now cross-sell services, enabling one-stop contracts that deepen customer stickiness in the Germany cold chain logistics market. DACHSER’s EUR 128 million (USD 150.56 million) Brummer takeover added 715,000 annual cross-border shipments and triggered immediate driver-recruit campaigns and tech retrofits. Similar acquisitions highlight the scale premium linked to nationwide GDP and forthcoming product-passport compliance.

By Temperature Type: Automation Propels Frozen Capacity

Chilled rooms held 55.02% of the Germany cold chain logistics market size in 2025 due to widespread fresh-food retail and pharma distribution, yet frozen capacity is expanding faster at 4.49% CAGR as robotic high-bay freezers spread. Each automated frozen pallet now consumes 30-40% less electricity, offsetting steep HFC costs. Operators also trial CO₂ cascade chillers that save 40% energy compared with legacy HFC systems.

Demand for ultra-low storage below -80 °C rises with mRNA vaccine and cell-based meat pilot runs, creating micro-segments inside the Germany cold chain logistics market where cryogenic nitrogen or deep-freezer pods must integrate with mainstream WMS software. Flexible facilities able to swap zones between chilled, frozen, and ambient temperatures on demand take investment priority.

By Application: Pharma Leads Growth as Compliance Tightens

Meat and poultry retained a 32.47% share in 2025, anchored by Germany’s EUR 40 billion processing industry, yet insurance costs balloon after a series of Listeria events. Pharmaceuticals and biologics surge at 6.01% CAGR, energized by mandatory GDP loggers and digital passports plus Bavarian biotech clusters exporting high-value biologics worth EUR 105.8 billion in 2024.

Fish and seafood volumes benefit from North Sea near-shoring and Bremerhaven’s 650,000 m³ of cold storage that supports 270,000 t throughput. Ready-to-eat meals and plant-based proteins add incremental pallets as Germany cold chain logistics market participants adapt to evolving dietary preferences.

Geography Analysis

North Rhine-Westphalia, Bavaria, and Baden-Württemberg collectively represent about 60% of the Germany cold chain logistics market in 2026. NRW combines population density with corridor connections to Benelux and France, while Bavaria hosts Munich’s pharma cluster that invested EUR 30-40 million (USD 35.28-47.05 million) in new GDP monitoring between 2024 and 2026. Baden-Württemberg’s automotive exports generate steady demand for temperature-controlled specialty chemicals and coatings.

Hamburg and Bremen run gateway ports that feed reefer containers inland. Hamburg moved 7.8 million TEU in 2024, with reefer boxes gaining share as Asian seafood and European pharma trade expand. Bremerhaven’s direct-quay Lineage facility added 40,000 pallet spots in 2024, underscoring coastal importance for the Germany cold chain logistics market.

Eastern states gain traction through EU infrastructure funds and lower wages. DHL Freight’s new 5,200 m² Berlin hub with 48 docks exemplifies investments flowing eastward. As q-commerce penetrates secondary cities, network planners add spoke warehouses within 150 km radii to uphold 15-minute delivery promises.

Competitive Landscape

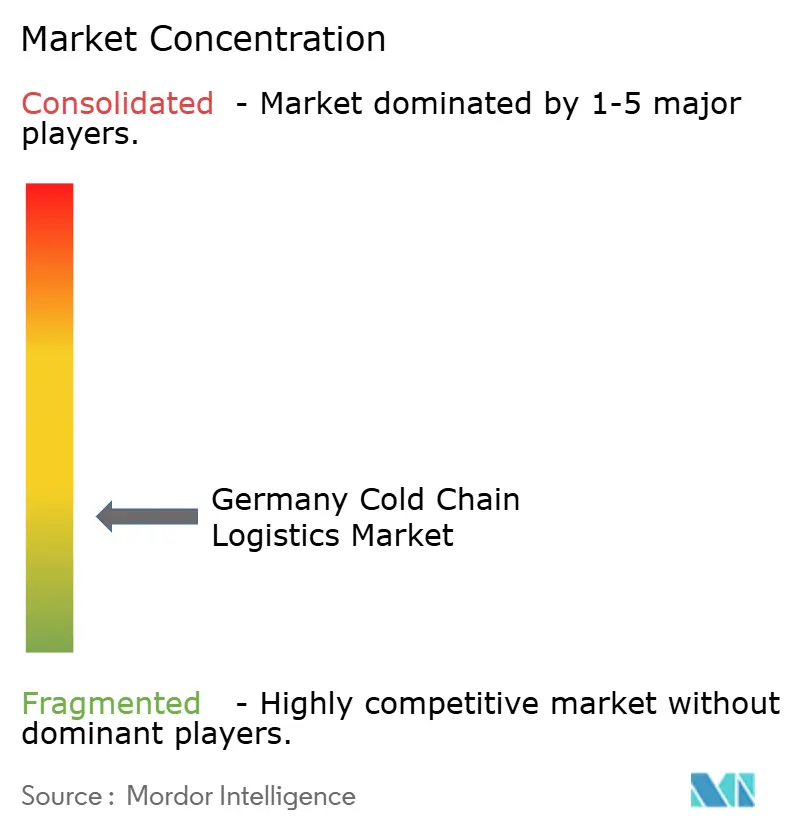

The Germany cold chain logistics market remains moderately fragmented. The top five players collectively control roughly 45-50% of value, leaving room for regionally focused specialists. DSV’s EUR 14.3 billion (USD 15.8 billion) Schenker purchase vaults it into the German top tier and allocates EUR 1 billion (USD 1.17 billion) for technology and capacity expansion through 2030. DHL Group earmarks EUR 2 billion (USD 2.35 billion) for pharma-grade capacity and multi-temperature fleets.

Kuehne+Nagel’s 21 deals since 2024 bolster end-to-end traceability offerings. Lineage Logistics leverages port-adjacent mega-freezers while Nagel-Group fills regional fresh niches. Emerging competitors focus on cell-based meat logistics and blockchain traceability, where small scale and specialized know-how still trump size.

Sustainability differentiates bids: As customers increasingly link supplier choices to ESG metrics, bids featuring rooftop photovoltaics, natural refrigerants, and electric fleet pilots gain an edge, highlighting sustainability's growing importance in tender evaluations and supplier selection.

Germany Cold Chain Logistics Industry Leaders

Kuehne + Nagel International AG

DHL Group

Lineage Logistics LLC

Dachser SE

DFDS Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: DSV closed its EUR 14.3 billion (USD 15.8 billion) Schenker acquisition, pledging EUR 1 billion (USD 1.17 billion) for German growth.

- April 2025: DHL Group committed EUR 2 billion (USD 2.35 billion) to expand DHL Health Logistics, adding GDP-certified hubs and temperature-controlled vehicles across Europe.

- March 2025: DHL acquired Cryopdp, a pharmaceutical logistics specialist offering temperature-controlled shipping and packaging services, enhancing its global life-sciences cold chain logistics capabilities.

- January 2025: DHL Freight opened a 5,200 m² Berlin-Marienfelde terminal equipped with electric trucks and onsite renewables.

Germany Cold Chain Logistics Market Report Scope

By Service Type

| Refrigerated Storage | |

| Refrigerated Transportation | Road |

| Rail | |

| Sea | |

| Air | |

| Value-Added Services |

By Temperature Type

| Chilled (0-5°C) |

| Frozen (-18 to 0°C) |

| Ambient |

| Deep-Frozen / Ultra-Low (less than-20°C) |

By Application

| Fruits and Vegetables |

| Meat and Poultry |

| Fish and Seafood |

| Dairy and Frozen Desserts |

| Bakery and Confectionery |

| Ready-to-Eat Meals |

| Pharmaceuticals and Biologics |

| Vaccines and Clinical Trial Materials |

| Chemicals and Specialty Materials |

| Other Perishables |

| By Service Type | Refrigerated Storage | |

| Refrigerated Transportation | Road | |

| Rail | ||

| Sea | ||

| Air | ||

| Value-Added Services | ||

| By Temperature Type | Chilled (0-5°C) | |

| Frozen (-18 to 0°C) | ||

| Ambient | ||

| Deep-Frozen / Ultra-Low (less than-20°C) | ||

| By Application | Fruits and Vegetables | |

| Meat and Poultry | ||

| Fish and Seafood | ||

| Dairy and Frozen Desserts | ||

| Bakery and Confectionery | ||

| Ready-to-Eat Meals | ||

| Pharmaceuticals and Biologics | ||

| Vaccines and Clinical Trial Materials | ||

| Chemicals and Specialty Materials | ||

| Other Perishables | ||

Key Questions Answered in the Report

What is the projected value of the Germany cold chain logistics market in 2031?

It is forecast to reach USD 15.23 billion by 2031, reflecting a 3.71% CAGR over 2026-2031.

Which service segment is growing fastest?

Value-added services are expanding at a 6.58% CAGR as customers demand compliance documentation, IoT tracking, and specialized packaging.

Why are frozen warehouses adopting robotics?

Automated deep-freeze systems cut energy use 30-40% and boost throughput 40-50%, offsetting labor shortages and higher refrigerant costs.

How does the EU Digital Product Passport affect operators?

From 2026, providers must capture and share real-time temperature and location data, driving EUR 150-200 million per year in digital upgrades.

Which application promises the highest growth?

Pharmaceuticals and biologics lead with a 6.01% CAGR, supported by stricter GDP monitoring and Germany’s strong export base. It is forecast to reach USD 15.23 billion by 2031, reflecting a 3.71% CAGR over 2026-2031.

Page last updated on: