Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 9.56 Billion |

| Market Size (2026) | USD 9.94 Billion |

| Market Size (2031) | USD 12.05 Billion |

| Growth Rate (2026 - 2031) | 3.92% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Cold Chain Logistics Market Analysis by Mordor Intelligence

The France Cold Chain Logistics Market size is estimated at USD 9.94 billion in 2026, and is expected to reach USD 12.05 billion by 2031, at a CAGR of 3.92% during the forecast period (2026-2031).

A shift towards ultra-low-temperature pharmaceutical corridors, electrification of pivotal port assets, and the gradual rollout of hydrogen pilots are counterbalancing challenges like refrigerant phase-downs and a shortage of drivers. While there's a surge in demand for temperature-validated biologics logistics, leading to increased capital spending on ISO-compliant storage, traditional dairy and produce lanes are facing margin compression due to inefficiencies from empty returns. Upgrades at the Port of Le Havre, along with mandates for real-time IoT monitoring, are giving integrated operators a competitive edge. At the same time, EU regulations on food waste and F-gases are pushing smaller firms to retrofit their systems at a premium, further driving consolidation in the French cold chain logistics landscape.

Key Report Takeaways

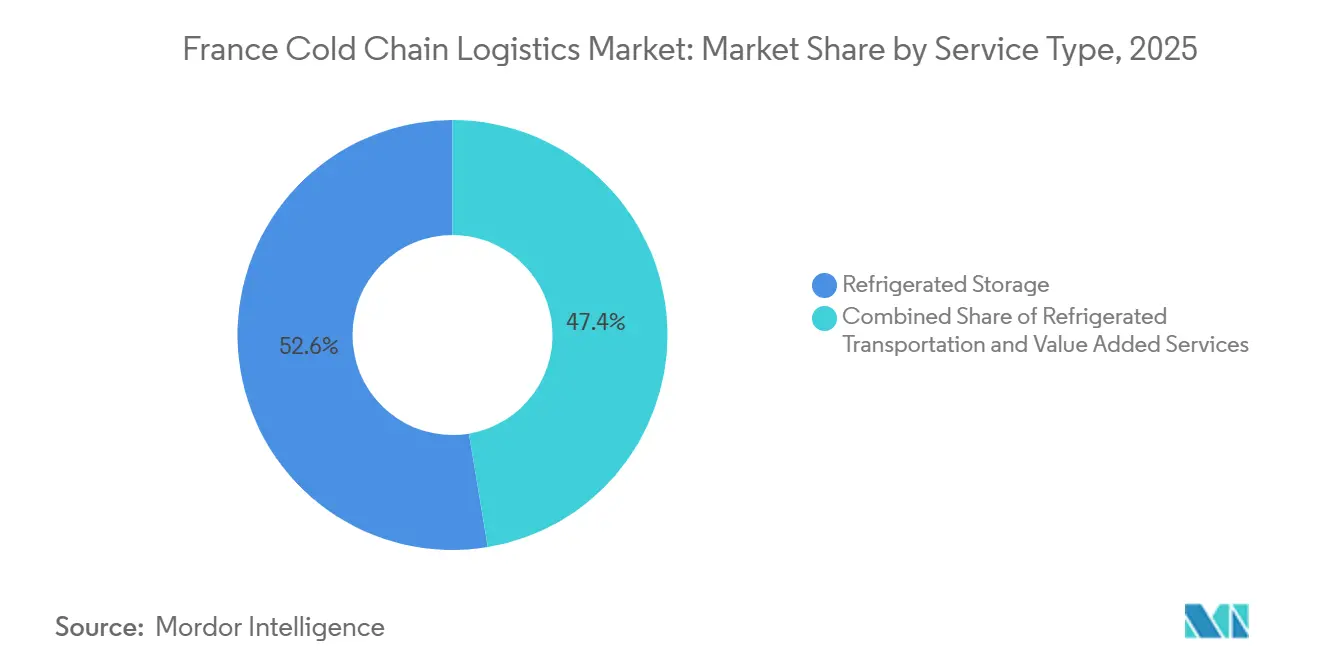

- By service type, refrigerated storage led the France cold chain logistics market share with 52.63% in 2025, while value-added services are projected to expand at the fastest rate, with a 7.14% CAGR through 2031.

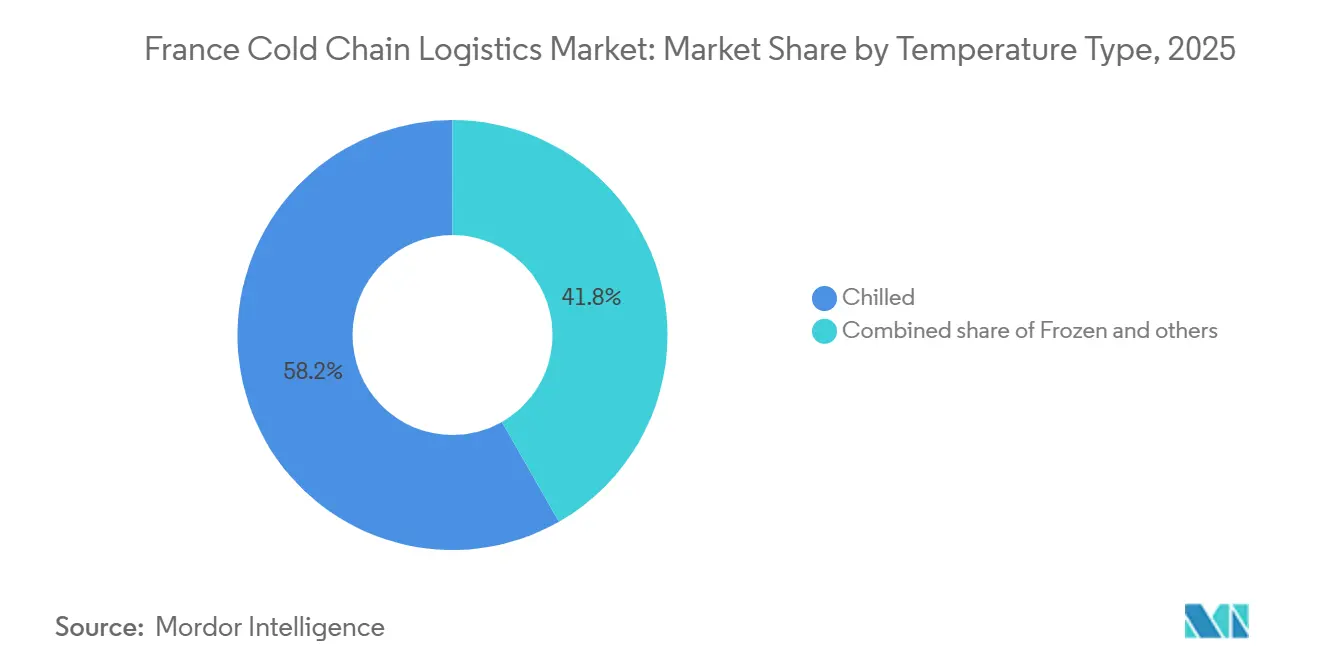

- By application, chilled applications commanded 58.24% of the France cold chain logistics market size in 2025, while frozen applications are forecast to post a 6.78% CAGR between 2026 and 2031.

- By sector, dairy & frozen desserts accounted for 29.76% of the France cold chain logistics market size in 2025, whereas pharmaceuticals & biologics are expected to register an 8.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | TIMELINE |

|---|---|---|---|

| Post-COVID e-grocery boom elevates last-mile refrigerated demand | +0.8% | National focus on Ile-de-France, Lyon, Marseille | Short term (≤ 2 years) |

| Biologics and mRNA vaccine pipeline scaling GDP-compliant logistics | +1.2% | Pharmaceutical clusters in Lyon, Paris, Strasbourg | Medium term (2-4 years) |

| EU and France-wide food-waste reduction mandates creating cold-chain gaps | +0.5% | Retail chains and food-service networks nationwide | Medium term (2-4 years) |

| Port of Le Havre reefer-plug expansion spurring import volumes | +0.4% | Northern France and Seine corridor | Short term (≤ 2 years) |

| AI-driven predictive maintenance cutting refrigeration OPEX | +0.6% | Large-scale cold-storage hubs nationwide | Medium term (2-4 years) |

| Hydrogen-powered forklifts and reefers gaining policy incentives | +0.3% | Paris region, Nord-Pas-de-Calais pilots | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-COVID E-grocery Boom Elevates Last-mile Refrigerated Demand

France leads Europe in online grocery growth, driven by rising demand for home delivery of fresh and frozen goods. The food and beverage e-commerce sector is expected to grow at double-digit rates through 2030, boosting demand for compact refrigerated vans suited to urban routes. Yet, low order density and high fuel costs are straining profitability. Retailers are testing hub-and-spoke models to improve efficiency, but these raise temperature control risks. Meanwhile, grocery and pharmaceutical chains maintain separate vehicle fleets due to differing standards, increasing capital costs. This is pushing France’s cold chain sector toward specialization grocery fleets expand for last-mile delivery, while GDP-certified vehicles focus on higher-margin pharmaceutical transport.[1]Organisation for Economic Co-operation and Development https://www.oecd.org/

Biologics and mRNA Vaccine Pipeline Scaling GDP-compliant Logistics

In 2025, the EU enforced stricter GDP rules requiring real-time temperature monitoring at 2-8°C, -20°C, and -70°C, electronic quarantines, and 10-year data storage. Compliance now depends on GPS-tracked trailers, tamper seals, Qualified Person oversight, and annual staff training. In France, hubs in Lyon and Paris are key for handling temperature-sensitive medicines, with noncompliance fines reaching USD 586,000. Certified leaders like DHL, UPS, and Kuehne + Nagel are gaining ground, while smaller firms struggle with costly validation and blockchain tracking. Rising demand for ultra-low temperatures, driven by mRNA therapies, is fueling high-spec warehouse development with redundant power and LNG backup systems, raising entry barriers in France’s cold chain logistics market.

EU and France-wide Food-waste Reduction Mandates Creating Cold-chain Gaps

EU rules require a 10% cut at processing and a 30% cut at retail and consumption by 2030, pushing French retailers to lengthen product shelf life via tighter temperature control[2]Road Freight Empty-Running Statistics 202 ec. europa.eu/eurostat. Fragmented regional distribution makes consistent handoffs difficult, prompting investment in IoT temperature logging and blockchain traceability. Retrofitting legacy fleets with telematics costs USD 540-1,080 per truck, so mid-tier operators defer upgrades, risking penalties. Longer inventory dwell times raise warehouse energy consumption, and RTE reported record summer peak demand in cold-storage zones during 2025. The France cold chain logistics market, therefore, juggles parallel pressures to cut waste and reduce power consumption, an operational paradox that favors integrated operators with renewable on-site generation.

Port of Le Havre Reefer-plug Expansion Spurring Import Volumes

Haropa Port has expanded to 3,900 reefer sockets along the Seine-axis, enabling shore power use and cutting vessel emissions. In early 2025, container traffic hit 1.51 million TEUs, driven by rising cold cargo imports from South America and Africa. However, limited hinterland storage is prolonging dwell times and increasing demurrage costs, offsetting efficiency gains. High inland grid and peak-tariff fees further deter smaller forwarders, prompting some to shift to Belgian and Dutch ports. Consequently, growth at Le Havre mainly benefits larger cold chain operators able to pre-book capacity and leverage bonded warehouses to navigate delays.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Grid-capacity bottlenecks for energy-hungry cold warehouses | -0.5% | Ile-de-France load pocket and Alpes load pockets | Short term (≤ 2 years) |

| Phase-down of HFC refrigerants inflating retrofit capex | -0.7% | Operators with legacy fleets nationwide | Medium term (2-4 years) |

| Empty-run share above 20% on international legs | -0.4% | France-Germany and France-Spain corridors | Short term (≤ 2 years) |

| Acute shortage of GDP-trained drivers and technicians | -0.6% | Lyon and Paris pharmaceutical hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid-capacity Bottlenecks for Energy-hungry Cold Warehouses

France’s cold chain sector, especially around suburban Paris and Lyon, faces severe grid constraints as RTE prioritizes renewables over new industrial links. This limits approvals for energy-intensive cold stores consuming 50-100 kWh per m² annually. Ultra-low temperature pharma sites require costly redundant power feeds, adding USD 216,000-324,000 upfront, pushing operators toward solar-plus-battery microgrids with decade-long paybacks. Peak tariffs run 3-4 times higher than off-peak rates, leaving little flexibility for continuous refrigeration. Some facilities pre-cool overnight, risking temperature swings, while grid scarcity delays permits and stalls new cold storage projects despite strong demand.

Phase-down of HFC Refrigerants Inflating Retrofit Capex

The EU’s steep HFC quota cuts-79% by 2027 and 85% by 2030 are pushing French cold chain operators to replace high-GWP refrigerants like R-404A with ammonia or CO₂ systems, costing over USD 54,000 per chamber with added safety upgrades. Smaller firms rely on reclaimed HFCs, but inconsistent purity and soaring R-404A prices (up to EUR 120/kg in 2024) strain margins under fixed shipper contracts. While natural refrigerants cut emissions sharply, they require scarce expertise in trans-critical CO₂ systems, causing installation delays. High upfront costs and technician shortages are slowing equipment upgrades just as demand for e-commerce perishables accelerates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Value-added Services Capture Pharma Premiums

Refrigerated Storage controlled 52.63% of the France cold chain logistics market share in 2025 and continues to anchor regional consolidation hubs that feed pan-European distribution[3]Nine-Month Revenue 2025 stef.com. This dominant share reflects France’s dense warehouse network that services food retail and pharmaceuticals from single locations. Road transport remains essential in hub-and-spoke models and absorbs the bulk of cross-border volume, yet France cold chain logistics market size value-added services such as kitting, relabeling, and compliance audits are winning the fastest growth at a 7.14% CAGR through 2031. Shippers pay premiums for end-to-end temperature validation, serialization support, and digital paperwork, margins that storage-only facilities cannot secure.

Hydrogen pilots under the FresH2 project could cut diesel exposure for truck fleets after 2028, lowering operating costs and improving ESG scores. Rail remains a second-tier option because reefer-wagon supply is thin, while air transport captures niche pharma shipments under tight lead times. Sea freight benefits from new plugs at Le Havre, but hinterland congestion dilutes port efficiency gains. The segment outlook therefore favors integrated players with diversified modal capacity inside the France cold chain logistics market.

By Temperature Type: Frozen Gains as Retailers Rebuild Safety Stock

Chilled logistics held 58.24% of the France cold chain logistics market share in 2025, powered by dairy, ready meals, and produce flows. Retailers have rebuilt frozen safety stocks since pandemic disruptions, leading the frozen category to a 6.78% forecast CAGR. Energy costs for -18°C storage run 30-40% higher than chilled, yet lower spoilage offsets part of the extra spend. Ultra-low zones below -70°C, primarily for biologics, command the highest yields but require capital-intensive redundant power and validation systems.

Plant-based frozen offerings are multiplying shelf facings, adding new SKUs that raise demand for -18°C transport legs. AI-based capacity planning, validated by MIT, cuts energy use and eases peak-load penalties, boosting adoption among operators pressured by grid constraints. Ambient-controlled lanes for bakery items remain a steady niche but offer thin margins. Investment decisions now hinge on balancing higher frozen returns against volatile energy prices, a dynamic that shapes capital allocation within the France cold chain logistics market.

By Application: Pharmaceuticals Outpace Traditional Food Segments

Dairy & Frozen Desserts represented 29.76% of application revenue in 2025, anchored by France’s status as Europe’s second-largest dairy producer. Pharmaceuticals & Biologics are projected to log an 8.21% CAGR through 2031 as mRNA vaccines and gene therapies proliferate. Fruits & Vegetables and Meat & Poultry remain mature, sub-4% growth lines constrained by flat consumption and retailer consolidation that compresses logistics rates.

Operators are converting chilled dairy warehouses into ultra-low pharmaceutical chambers to capture higher yields despite losing short-term volume. Meat & Poultry and Fish & Seafood face longer dwell times under waste-reduction rules, raising refrigeration costs without equivalent rate lifts. Chemicals and specialty materials need hazmat compliance plus temperature control, creating a niche for specialized fleets. Overall, the application mix polarizes between high-volume, low-margin food and low-volume, high-margin pharma within the France cold chain logistics market.

Geography Analysis

Ile-de-France hosts 35-40% of national cold storage, driven by proximity to Charles de Gaulle Airport’s pharma hub and dense e-grocery demand. Grid constraints in suburban zones limited new warehouse approvals in 2025, pushing operators toward rooftop solar and battery systems despite decade-long paybacks. Rhone-Alpes benefits from Lyon’s pharmaceutical cluster and its position on Alpine trade lanes, yet labor costs run higher because Swiss employers lure drivers across the border.

Northern France leverages the Port of Le Havre for reefer imports that feed Belgium and Germany, but inland storage is lagging, causing congestion that occasionally diverts cargo to Rotterdam. Grand Est and Brittany manage cross-border dairy and seafood flows, yet eastbound empty-return rates exceed 25%, squeezing margins. Southern France serves Mediterranean produce exports and tourism-driven catering, but seasonal peaks limit asset utilization, so operators prefer flexible leases over fixed capacity in these regions.

Regulatory intensity varies. Ile-de-France and Rhone-Alpes receive the strictest GDP audits given pharmaceutical density, while peripheral areas face lighter oversight, creating compliance arbitrage. The decentralized geography of the France cold chain logistics market raises network complexity; nationwide coverage requires redundant nodes, but concentrated footprints risk grid overload and wage inflation.

Competitive Landscape

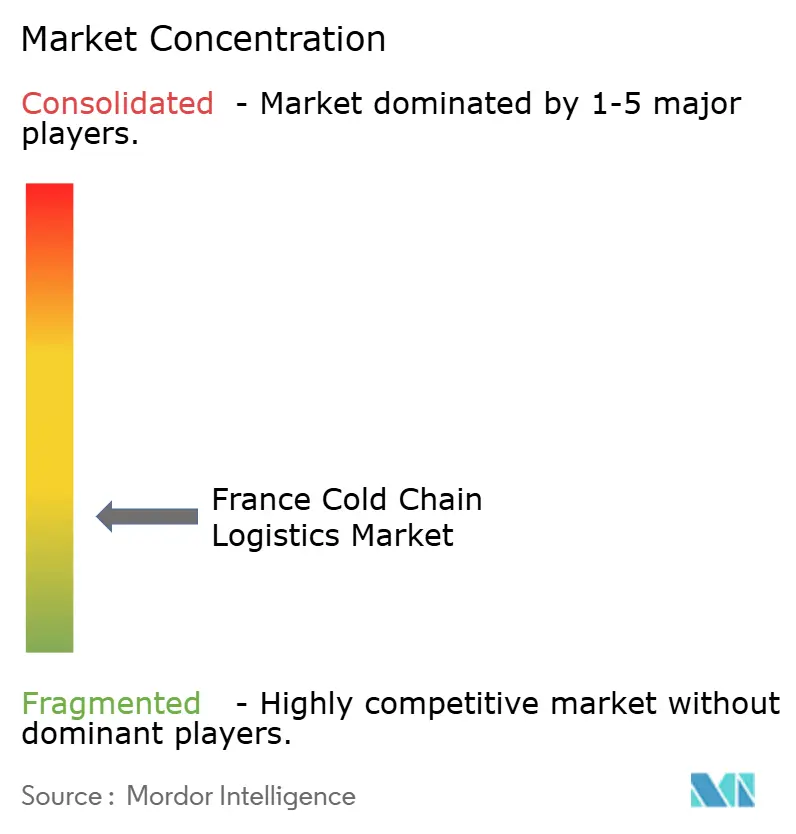

The France cold chain logistics market remains moderately fragmented. STEF controls the largest domestic network of 250 sites and 5,500 refrigerated vehicles, yet its share is below 15%, so international integrators and niche specialists still find room to grow. DSV’s 2025 integration of DB Schenker boosted cross-border capabilities, especially in pharma lanes. Kuehne + Nagel and DHL expanded GDP-certified depots in Lyon and Paris, tailoring solutions for clinical-trial staging. Strategy splits along scale lines: incumbents invest in alternative fuels and AI routing to retain share, whereas challengers acquire certified facilities rather than build from scratch.

Technology is the competitive fulcrum. IoT sensors provide real-time temperature visibility, blockchain underpins traceability, and digital twins optimize energy use, yet roll-out costs slow adoption by mid-tier firms. STEF’s deployment of hydrogen forklifts signals early compliance with future F-gas caps. Disruptors such as TSE Express Médical focus on customized biotech handling, capturing clients that prize agility over network breadth. ISO 9001:2015 and GDP certifications act as entry barriers, clustering pharmaceutical flows among operators that can fund audits and validation.

Cost pressure from refrigerant phase-downs and labor deficits is accelerating consolidation. Smaller warehouses without natural-refrigerant systems face retrofit bills that they cannot finance, prompting sale or leaseback deals. Meanwhile, e-grocery growth lures parcel specialists into chilled last-mile segments, increasing competitive overlap. Overall, rivalry intensifies along two fronts: sustainability leadership and pharmaceutical compliance excellence within the France cold chain logistics market.

France Cold Chain Logistics Industry Leaders

STEF

Kuehne + Nagel

Sofrilog

Olano Group

XPO

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: STEF finalized the integration of Christian Cavegn AG, extending frozen and fresh logistics coverage across Switzerland, which enhances cross-border capacity for French shippers.

- December 2025: GEODIS partnered with EDF to deploy on-site renewables and energy-optimization software across logistics facilities, targeting significant emissions reduction in cold-store operations.

- July 2025: XPO opened a new last-mile hub in Annecy to meet heavier-goods demand, improving 24-48-hour nationwide service for perishables.

- May 2025: DSV completed its acquisition of DB Schenker, expanding temperature-controlled contract logistics and transport solutions across France.

France Cold Chain Logistics Market Report Scope

By Service Type

| Refrigerated Storage | |

| Refrigerated Transportation | Road |

| Rail | |

| Sea | |

| Air | |

| Value-Added Services |

By Temperature Type

| Chilled (0–5 °C) |

| Frozen (-18 °C) |

| Ambient |

| Deep-Frozen / Ultra-Low (less than -20 °C) |

By Application

| Fruits & Vegetables |

| Meat & Poultry |

| Fish & Seafood |

| Dairy & Frozen Desserts |

| Bakery & Confectionery |

| Ready-to-Eat Meals |

| Pharmaceuticals & Biologics |

| Vaccines & Clinical Trial Materials |

| Chemicals & Specialty Materials |

| Other Perishables |

| By Service Type | Refrigerated Storage | |

| Refrigerated Transportation | Road | |

| Rail | ||

| Sea | ||

| Air | ||

| Value-Added Services | ||

| By Temperature Type | Chilled (0–5 °C) | |

| Frozen (-18 °C) | ||

| Ambient | ||

| Deep-Frozen / Ultra-Low (less than -20 °C) | ||

| By Application | Fruits & Vegetables | |

| Meat & Poultry | ||

| Fish & Seafood | ||

| Dairy & Frozen Desserts | ||

| Bakery & Confectionery | ||

| Ready-to-Eat Meals | ||

| Pharmaceuticals & Biologics | ||

| Vaccines & Clinical Trial Materials | ||

| Chemicals & Specialty Materials | ||

| Other Perishables | ||

Key Questions Answered in the Report

How large is the France cold chain logistics market in 2026 and what growth is expected?

The market is valued at USD 9.94 billion in 2026 and is projected to reach USD 12.05 billion by 2031, showing a 3.92% CAGR.

Which service type currently dominates French temperature-controlled logistics?

Refrigerated Storage leads, holding 52.63% share in 2025 thanks to the country’s dense warehouse network.

What is the fastest-growing application category through 2031?

Pharmaceuticals & Biologics are forecast to expand at an 8.21% CAGR as biologic therapies and mRNA vaccines scale.

Where are infrastructure bottlenecks most acute?

Grid-capacity constraints are most severe around Île-de-France and Rhône-Alpes, slowing new ultra-low-temperature warehouse approvals.

Page last updated on: