Central And Eastern Europe Cold Chain Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

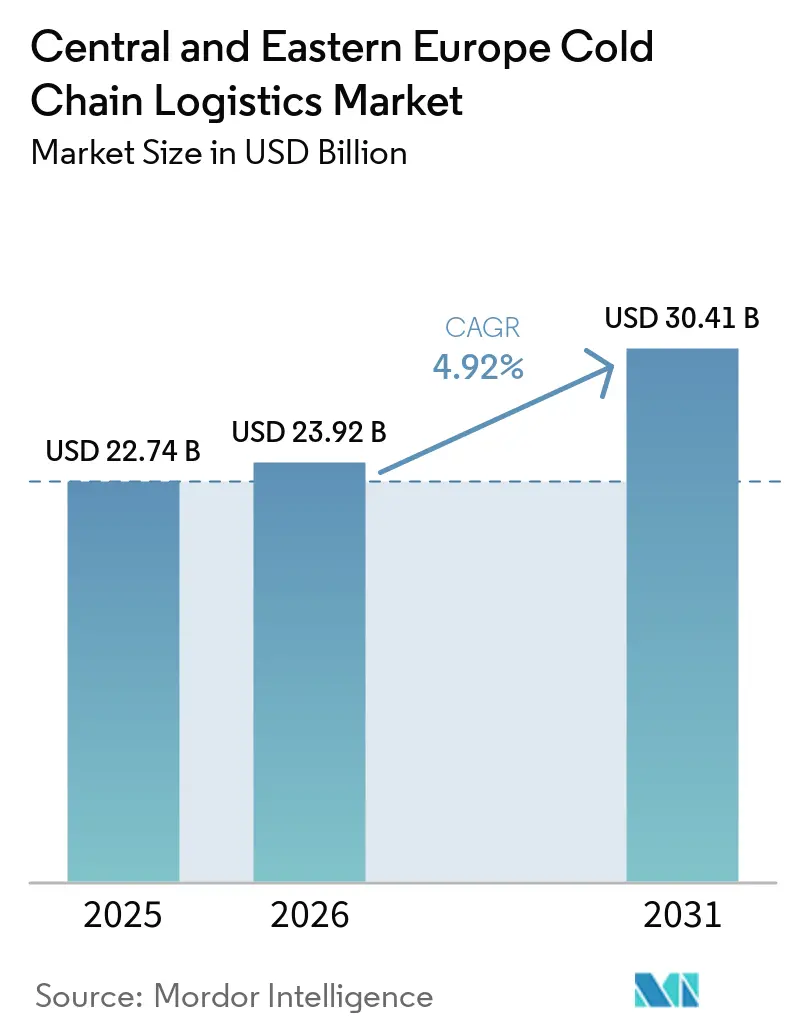

| Base Year Market Size (2025) | USD 22.74 Billion |

| Market Size (2026) | USD 23.92 Billion |

| Market Size (2031) | USD 30.41 Billion |

| Growth Rate (2026 - 2031) | 4.92% CAGR |

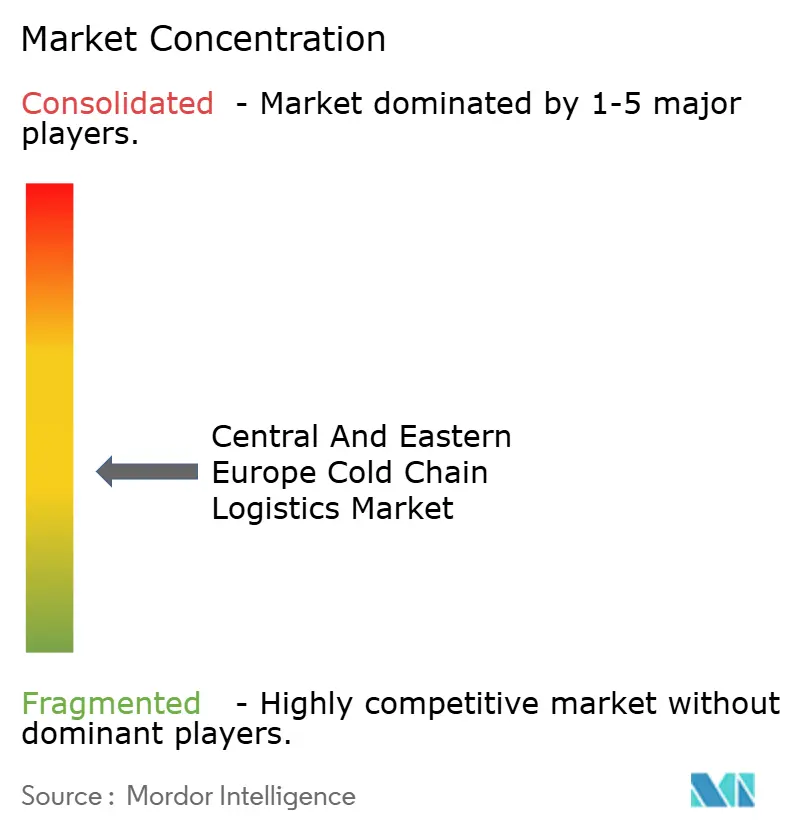

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Central And Eastern Europe Cold Chain Logistics Market Analysis by Mordor Intelligence

The Central and Eastern Europe Cold Chain Logistics Market size is projected to grow from USD 22.74 billion in 2025 to USD 23.92 billion in 2026, and to reach USD 30.41 billion by 2031, growing at a 4.92% CAGR from 2026 to 2031.

Expansion is underpinned by the region’s role as a low-cost protein processing hub exporting to Western Europe and a proving ground for decarbonized refrigerated transport designed to meet EU Carbon Border Adjustment Mechanism (CBAM) requirements. Rising ESG-linked capital inflows are funding automated freezers even as grid constraints delay commissioning, while 5G-enabled IoT telemetry lowers spoilage and insurance costs for pharmaceutical cargo. Hydrogen and battery-electric reefer pilots along TEN-T rail corridors improve intermodal efficiency, and quick-commerce platforms in tier-2 cities are reshaping last-mile refrigerated delivery economics. Collectively, these forces reinforce the competitiveness of the Central and Eastern Europe cold chain logistics market in global protein and biologics supply networks.

Key Report Takeaways

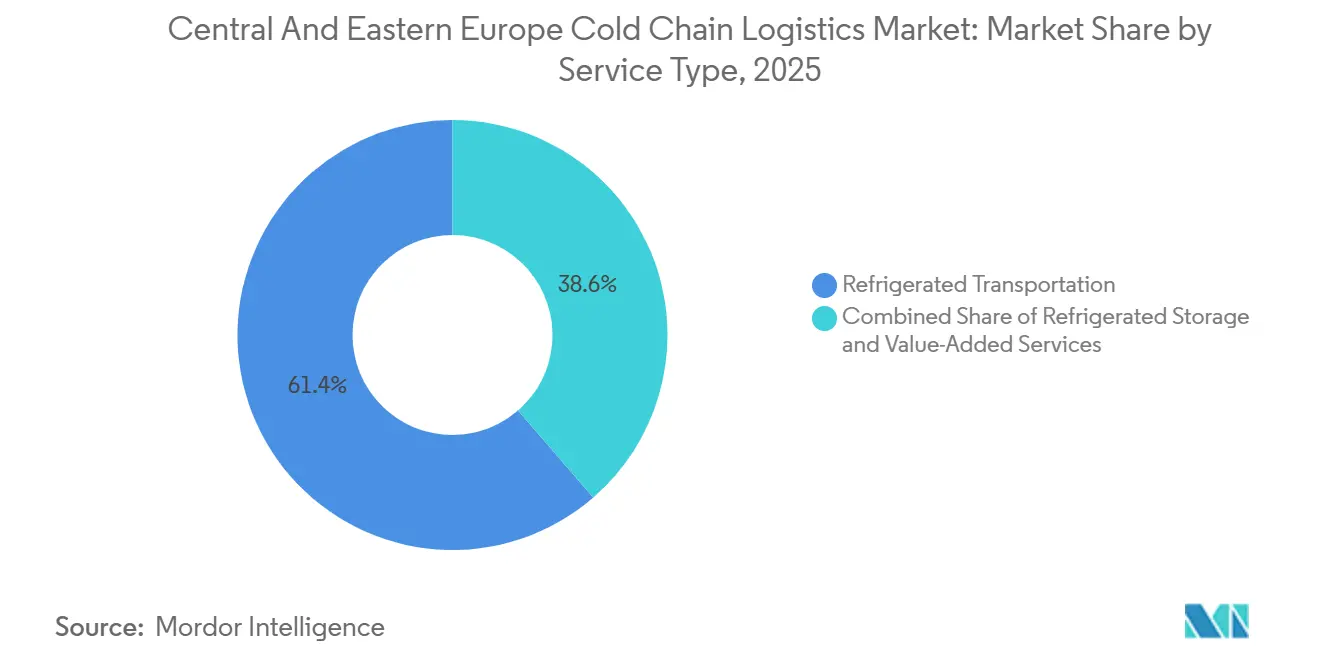

- By service type, refrigerated transportation led with 61.37% of the Central and Eastern Europe cold chain logistics market share in 2025, while value-added services are forecast to expand at a 5.58% CAGR to 2031.

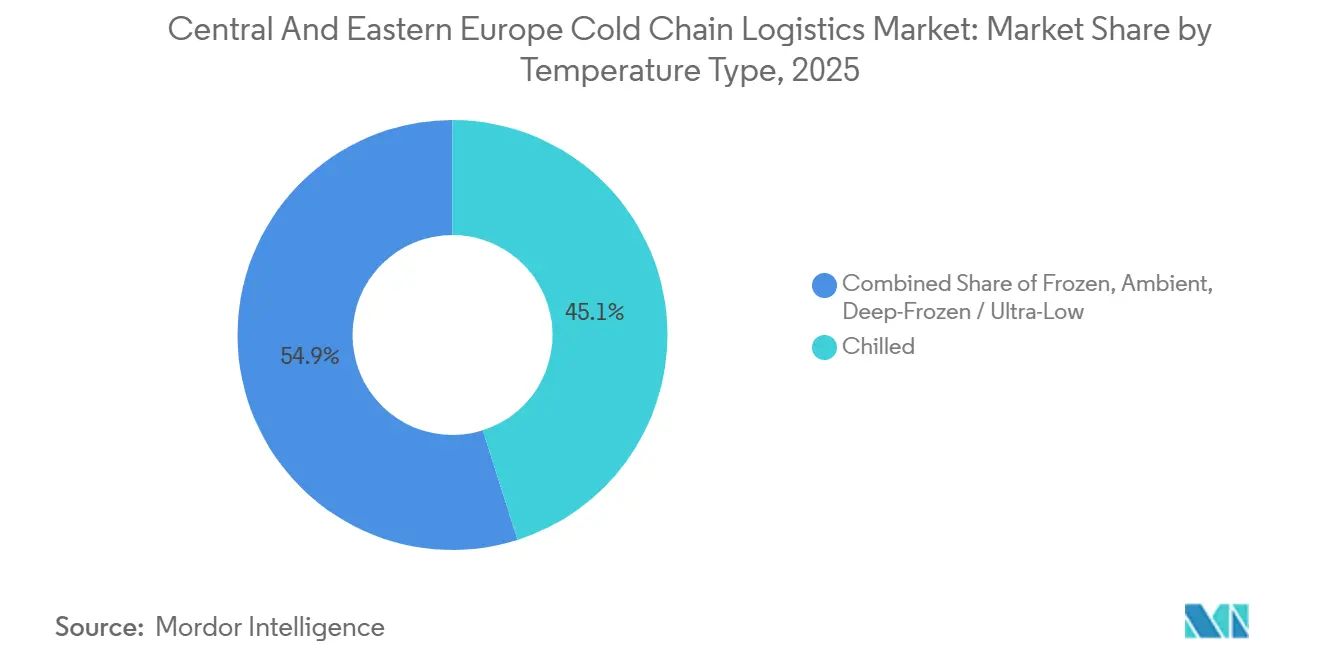

- By temperature type, the chilled segment captured 45.10% share of the Central and Eastern Europe cold chain logistics market size in 2025, whereas the frozen segment is projected to record a 6.11% CAGR through 2031.

- By application, meat and poultry held 20.68% of the Central and Eastern Europe cold chain logistics market share in 2025, while pharmaceuticals and biologics are advancing at a 6.73% CAGR during 2026-2031.

- By geography, Romania accounted for 33.72% of the Central and Eastern Europe cold chain logistics market size in 2025, while Poland is on track for a 5.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Central And Eastern Europe Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CBAM-driven shift to low-carbon cold logistics solutions | +0.9% | EU-wide, CEE export corridors | Medium term (2-4 years) |

| Export boom of CEE animal protein demanding ultra-low temp capacity | +1.1% | Romania, Poland, Hungary | Short term (≤ 2 years) |

| Hydrogen and battery-electric reefer corridors backed by EU subsidies | +0.8% | Poland, Czech Republic, Slovakia | Long term (≥ 4 years) |

| 5G and IoT telemetry lowering spoilage and insurance premiums | +0.7% | Regional urban centers | Medium term (2-4 years) |

| Tier-2 city dark-store quick-commerce fueling micro-fulfillment demand | +0.6% | Poland, Czech Republic, Romania | Short term (≤ 2 years) |

| ESG capital inflow for speculative high-bay freezer developments | +0.8% | Poland, Czech Republic | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

CBAM-Driven Shift to Low-Carbon Cold Logistics Solutions

The EU CBAM, moving to full enforcement in 2026, is prompting operators to retrofit fleets with natural refrigerants and electric transport refrigeration units to avoid embedded-carbon penalties. Refrigerant costs support the switch: hydrofluorocarbon prices surged 1,000% since 2014, while CO₂ and propane alternatives stabilized between EUR 5-15 per kg. Poland, the EU’s largest road-freight market at 385 billion tonne-kilometres in 2022, is piloting CBAM-compliant battery-electric reefers on TEN-T corridors that will soon feature mandatory ultra-fast chargers every 100 km. Romanian protein processors are installing renewable-powered cold stores to curb Scope 3 emissions linked to methane-intensive meat supply chains. Western European retailers embed carbon-intensity thresholds in CEE supplier contracts, cementing first-mover advantages for decarbonized operators[1]“High-GWP Refrigerants Face Soaring Prices,” Green Cooling Initiative, green-cooling-initiative.org.

Export Boom of CEE Animal Protein Demanding Ultra-Low Temp Capacity

Low-cost labor and proximity to Western Europe have positioned CEE as a go-to cutting and packaging base, and Romania’s Black Sea access accelerates frozen meat exports to the Middle East. NewCold’s 9-hectare high-bay freezer project in Romania raises storage density by 12.5% and reduces energy use by 40% compared with conventional facilities. African Swine Fever disruptions in Asia redirected pork demand toward European exporters, straining legacy capacities by 2024. With cold warehouses only 8-10% of Poland’s 35 million m² logistics stock, speculative developments chase demand spikes. Blast-freezers near Baltic ports now support fish exports, while AutoStore’s multi-temperature cube allows frozen and chilled SKUs under one roof, cutting footprints by up to 75%.

Hydrogen and Battery-Electric Reefer Corridors Backed by EU Subsidies

The Connecting Europe Facility earmarked EUR 7 billion (USD 8.23 billion) for rail and alternative-fuel infrastructure, 80% of which targets electrified TEN-T freight capable of supporting hydrogen and battery-electric reefers. Scania aims for 50% zero-emission truck sales by 2030, aligning OEM roadmaps with subsidy windows. UPS accelerated adoption by acquiring Frigo-Trans and pledging electric TRU retrofits eligible for 40% cost rebates. Rail Baltica will add refrigerated railcars by 2030, reducing road reliance for north-south protein and pharma flows. Intermodal cold hubs in Poland’s Lodz region integrate on-site solar arrays and battery storage, minimizing grid draw during charging peaks[2]“Scania, Mercedes-Benz, MAN, the only EU truck brands on track to decarbonise, study,” Transport & Environment, transportenvironment.org .

5G and IoT Telemetry Lowering Spoilage and Insurance Premiums

Widespread 5G roll-outs in CEE enable real-time temperature, humidity, and shock monitoring with 1-10 ms latency, a critical upgrade from 4G systems’ 50-100 ms. DHL’s CRYOPDP acquisition brings 600,000 specialized pharma moves under a platform that cuts claims by double digits through continuous telemetry. Romanian e-commerce growth to EUR 10 billion (USD 11.76 billion) by 2025 is spurring consumer-facing apps that display live temperature data, enhancing brand trust. Insurers now offer up to 25% premium discounts for GDP-compliant telematics, improving margins on high-value biologics. Predictive maintenance algorithms flag compressor anomalies 48-72 hours in advance, preventing multimillion-dollar losses.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inflationary spike in insulated-panel and refrigeration component costs | -0.8% | CEE-wide projects | Short term (≤ 2 years) |

| Fragmented smallholder supply base limits back-haul consolidation | -0.6% | Hungary, Slovakia, Romania | Long term (≥ 4 years) |

| Grid-capacity and power-permit bottlenecks for energy-intensive sites | -0.9% | Poland, Czech Republic | Medium term (2-4 years) |

| Multi-jurisdiction VAT and ICS2 e-customs complexity inflating costs | -0.5% | Cross-border operators | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Inflationary Spike in Insulated-Panel and Refrigeration Component Costs

Polyurethane insulation panels have risen 35-45% since 2022 as feedstock and energy volatility hit suppliers, squeezing developer margins. Steel tariffs on non-EU imports add further cost pressure and extend component lead times to 20-26 weeks. The 48% F-gas quota cut for 2025-2026 tightened refrigerant supply, lifting equipment prices by up to 30%. Smaller firms lacking fixed-price contracts face project cancellations or forced exits, fuelling consolidation. Labor scarcity for certified HVAC technicians inflates wage bills by 20-35%, compounding capital cost overruns[3]“New European F-Gas Regulation – Impacts and Compliance,” Generalgas, generalgas.eu .

Fragmented Small holder Supply Base Limits Back-Haul Consolidation

Agricultural parcels in Hungary and Slovakia average under 5 hectares, producing disaggregated pickup points that hinder full-truck-load consolidation. Empty-run ratios often exceed 35% versus Western Europe’s sub-20% benchmarks, raising per-kilometer costs. Technology platforms aggregating smallholder output remain nascent, and cooperative models struggle to scale due to governance challenges. As a result, logistics providers absorb higher costs or forgo rural lanes altogether, limiting cold chain penetration into peripheral regional economies[4]“New European F-Gas Regulation – Impacts and Compliance,” Generalgas, generalgas.eu .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Transportation Dominance Reflects Export Orientation

Refrigerated Transportation commanded 61.37% of the Central and Eastern Europe cold chain logistics market share in 2025, underlining the region’s outward-facing supply chains. Poland’s 385 billion tonne-kilometres of road freight in 2022 underscores modal dependence on trucks for meat and pharma exports. Rail’s share is rising through EUR 7 billion (USD 8.23 billion) TEN-T upgrades that support battery-electric and hydrogen reefers, reducing embedded carbon and ensuring CBAM readiness. The Central and Eastern Europe cold chain logistics market size for transportation is projected to grow alongside subsidy-driven fleet renewal, creating opportunities for OEM operator partnerships in zero-emission platforms.

Value-Added Services hold smaller revenue today but clock the fastest CAGR at 5.58% because shippers seek kitting and blockchain-verified provenance to differentiate in saturated food categories. Storage still plays a pivotal buffering role, with automated freezers reducing energy costs via density gains, yet its share lags as exporters favor velocity over dwell time. Air cargo remains niche but critical for cell-therapy materials and high-value biologics requiring stringent time-temperature compliance. Sea freight is winning volume from air on cost and carbon grounds, with passive packaging innovations extending hold times. Ultimately, competitive advantage in this segment pivots on intermodal agility, carbon footprint transparency, and the ability to layer premium value-added workflows onto core haulage.

By Temperature Type: Frozen Segment Accelerates on Pharma Demand

The Chilled segment accounted for 45.10% of the Central and Eastern Europe cold chain logistics market size in 2025, mirroring strong dairy and fresh-meat flows to Western Europe. However, the Frozen segment is forecast to notch a robust 6.11% CAGR fueled by vaccine distribution and frozen poultry exports to the Middle East. Frozen’s rise lifts the Central and Eastern Europe cold chain logistics market size attached to ultra-low temperature assets, intensifying competition for scarce grid capacity because freezers consume up to 40% more power than chillers. AutoStore’s multi-temperature automation cuts energy use by 40%, addressing opex pain points for operators pivoting into frozen lines.

Deep-Frozen storage below –20 °C supports cell and gene therapies, attracting premium yields that offset higher capex, while ambient-controlled services round out mixed loads and strengthen back-haul economics. Regulatory divergence also shapes opportunity sets: good distribution practice mandates force continuous monitoring in pharma lanes, whereas HACCP rules allow more operational latitude in food sectors, enabling differentiated risk-pricing models. Temperature hybridization combining chilled, frozen, and ambient in one automated cube emerges as a capital-efficient route to serve varied product mixes without multiple standalone facilities.

By Application: Pharmaceuticals Outpace Traditional Food Segments

Meat and Poultry retained 20.68% of the Central and Eastern Europe cold chain logistics market share in 2025, buoyed by Poland’s and Romania’s processing clusters. Yet Pharmaceuticals and Biologics are on track for a 6.73% CAGR as Western Europe’s capacity squeeze pushes contract manufacturing eastward, enlarging the Central and Eastern Europe cold chain logistics market size attached to high-margin healthcare cargo. GLP-1 drug logistics demand stringent 2-8 °C control and flawless documentation, commanding rates several multiples above protein freight. Vaccines and clinical-trial materials, often shipped at –20 °C to –80 °C, amplify demand for ultra-low temperature storage and specialized active or passive packaging.

Fruits and Vegetables still drive reliable volume but have slimmer margins due to retailer price pressure; operators seek efficiency through cross-docking and route optimization. Fish and Seafood capitalize on Baltic port enhancements that cut transit to Western Europe by 24 hours, supporting freshness premiums. Dairy benefits from private-label expansion among discounters that now demand vendor-managed inventory, reinforcing call-off flexibility. Ready-to-Eat meals ride quick-commerce momentum in secondary urban centers, requiring micro-fulfillment cold rooms near consumers. Chemicals and specialty materials occupy a niche but critical slice where ultra-deep-frozen capabilities yield high returns for limited square footage. The coexistence of commodity protein volumes and high-value biologics compresses asset allocation decisions: operators must balance throughput-driven food contracts against precision-driven pharma lanes without compromising either service model.

Geography Analysis

Romania captured 33.72% of the Central and Eastern Europe cold chain logistics market size in 2025, propelled by dense meat-processing plants clustered near the Black Sea and an export focus toward Middle Eastern buyers. Ahold Delhaize’s EUR 2.5 billion (USD 2.94 billion) Profi acquisition locks Western European retail demand into Romanian supply chains, guaranteeing throughput for new automated freezers. Trendyol’s planned Bucharest logistics hub adds e-commerce pull, while the domestic online sector heads toward EUR 10 billion (USD 11.76 billion) sales, supporting last-mile chilled delivery. Grid limitations around Bucharest pose risks, lengthening connection lead times beyond two years, yet developers offset delays with rooftop PV and thermal batteries.

Poland is the fastest-growing geography, expected to post a 5.43% CAGR through 2031 on the back of EUR 7 billion (USD 8.23 billion) TEN-T rail upgrades and a 35-million m² warehouse base that already integrates cold docks. Lineage and Panattoni anchor multimodal hubs in Lodz, embedding rail spurs and EV truck chargers. Domestic policy favors zero-emission fleets, dovetailing with EU subsidies that cover up to 40% of incremental electric-TRU costs. Nonetheless, warehouse vacancy crept to 8.5% in some outer submarkets, flagging overbuild risk in non-prime zones.

The Czech Republic, Slovakia, and Hungary form a second-tier growth triangle. Czech retail parks added 80,000 m² in 2024, with another 220,000 m² due by 2026, driving chilled distribution demand. Slovakia attracted LPP’s 25,400 m² fulfillment center, signaling apparel-led cold-light requirements for quick-commerce. Hungary’s Danube corridor sees auto-industry-linked cold flows but suffers back-haul inefficiencies due to fragmented smallholders. Baltic states round out the Rest of CEE; Rail Baltica’s 2030 completion will integrate refrigerated wagons with EU mainlines, opening new north-south lanes. Geographic dispersion of regulations from F-gas quotas to VAT rules creates planning complexity but also route-based arbitrage that savvy providers exploit to optimize total landed cost for shippers.

Competitive Landscape

The Central and Eastern Europe cold chain logistics market shows moderate concentration as scale and technology requirements spur consolidation. Global integrators such as DHL and UPS bought CRYOPDP, Frigo-Trans, and BPL to secure biologics lanes with premium yields. Regional champions Raben Group and Dachser SE differentiate through sustainability, rolling out electric semi-trailers and rooftop solar arrays that cut Scope 1 emissions and meet retailer carbon scorecards. Asset-heavy developers Lineage and NewCold bet on automated high-bay freezers financed by ESG investors eager for energy-efficiency stories; their facilities reach up to 40 m height, packing four times the pallet density of conventional warehouses.

Digital capability is the emerging battleground. Lineage’s partnership with Cognizant embeds Agentic AI chatbots that answer customer queries and orchestrate inventory moves in real time. Rohlik Group spun off Veloq to commercialize AI fulfillment tech, promising 60-minute grocery deliveries in Prague, Budapest, and Vienna. Start-ups leverage 5G IoT sensors to offer usage-based insurance, undercutting traditional premiums by 20-25% for operators with proven telemetry data. Hydrogen reefer pilots attract consortiums that blend OEMs, fuel suppliers, and logistics firms in subsidy-backed demonstrations along Polish and Czech routes.

Competitive pressure also comes from real-estate developers such as Prologis and P3 that integrate cold boxes within broader logistics parks, bundling long-term leases with renewable energy add-ons. Quick-commerce entrants create demand fragmentation that incumbents counter with co-packing, kitting, and blockchain provenance to lock in customers for longer contract terms. As capex intensifies and compliance costs rise, small operators below 10,000 pallets risk marginalization, accelerating a consolidation wave that is likely to lift the combined top-five share toward 70% by 2031.

Central And Eastern Europe Cold Chain Logistics Industry Leaders

Raben Group

DHL Group

DSV A/S

DACHSER

Kuehne+Nagel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: DHL Supply Chain and Pepco expanded their long-standing collaboration to strengthen Pepco’s distribution operations across Europe.

- April 2026: In Gluchow, Central Poland, DHL Supply Chain inaugurated a logistics facility, designating it as a global hub for Oriflame. The move brings on board over 100 personnel tasked with overseeing inventory and managing B2C distribution.

- July 2025: Lineage Logistics expanded its Cognizant partnership to roll out Agentic AI across CEE cold stores, targeting inventory accuracy gains and service-desk automation.

- May 2025: Raben Group surpassed EUR 2.15 billion (USD 2.52 billion) revenue, opened new contract-logistics hubs in Lithuania and Greece, and deployed electric refrigerated trailers across CEE.

Central And Eastern Europe Cold Chain Logistics Market Report Scope

| Refrigerated Storage | Public Warehousing |

| Private Warehousing | |

| Refrigerated Transportation | Road |

| Rail | |

| Sea | |

| Air | |

| Value-Added Services |

| Chilled (0-5 °C) |

| Frozen (-18-0 °C) |

| Ambient |

| Deep-Frozen / Ultra-Low (less than-20 °C) |

| Fruits and Vegetables |

| Meat and Poultry |

| Fish and Seafood |

| Dairy and Frozen Desserts |

| Bakery and Confectionery |

| Ready-to-Eat Meals |

| Pharmaceuticals and Biologics |

| Vaccines and Clinical Trial Materials |

| Chemicals and Specialty Materials |

| Other Applications |

| Poland |

| Slovakia |

| Czech Republic |

| Hungary |

| Romania |

| Rest of CEE |

| By Service Type | Refrigerated Storage | Public Warehousing |

| Private Warehousing | ||

| Refrigerated Transportation | Road | |

| Rail | ||

| Sea | ||

| Air | ||

| Value-Added Services | ||

| By Temperature Type | Chilled (0-5 °C) | |

| Frozen (-18-0 °C) | ||

| Ambient | ||

| Deep-Frozen / Ultra-Low (less than-20 °C) | ||

| By Application | Fruits and Vegetables | |

| Meat and Poultry | ||

| Fish and Seafood | ||

| Dairy and Frozen Desserts | ||

| Bakery and Confectionery | ||

| Ready-to-Eat Meals | ||

| Pharmaceuticals and Biologics | ||

| Vaccines and Clinical Trial Materials | ||

| Chemicals and Specialty Materials | ||

| Other Applications | ||

| By Country | Poland | |

| Slovakia | ||

| Czech Republic | ||

| Hungary | ||

| Romania | ||

| Rest of CEE | ||

Key Questions Answered in the Report

How large will Central and Eastern Europe’s cold chain logistics sector be by 2031?

The Central and Eastern Europe cold chain logistics market size is forecast to reach USD 30.41 billion by 2031.

Which temperature segment is growing the fastest in the region?

The Frozen segment is projected to advance at a 6.11% CAGR between 2026-2031 thanks to vaccine and frozen protein exports.

Why is Romania so dominant in CEE refrigerated logistics?

Romania holds one-third of regional value because its meat-processing clusters and Black Sea port access anchor high-volume protein exports.

How is EU policy shaping investment in refrigerated transport?

CBAM and Alternative Fuels rules drive subsidies toward battery-electric and hydrogen reefers, accelerating zero-emission fleet roll-outs.

What strategies help logistics firms manage energy-cost inflation?

Operators deploy automated high-bay freezers, on-site renewable power, and IoT analytics to cut electricity use and avoid peak tariffs.

Page last updated on: