Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

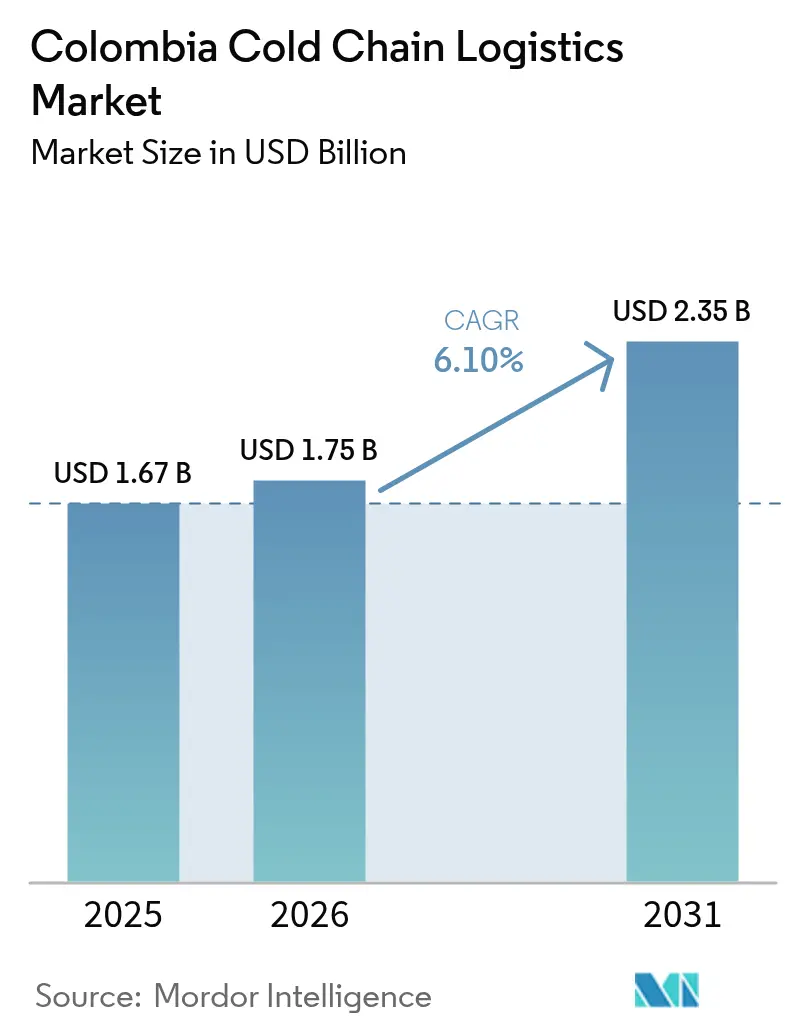

| Base Year Market Size (2025) | USD 1.67 Billion |

| Market Size (2026) | USD 1.75 Billion |

| Market Size (2031) | USD 2.35 Billion |

| Growth Rate (2026 - 2031) | 6.10% CAGR |

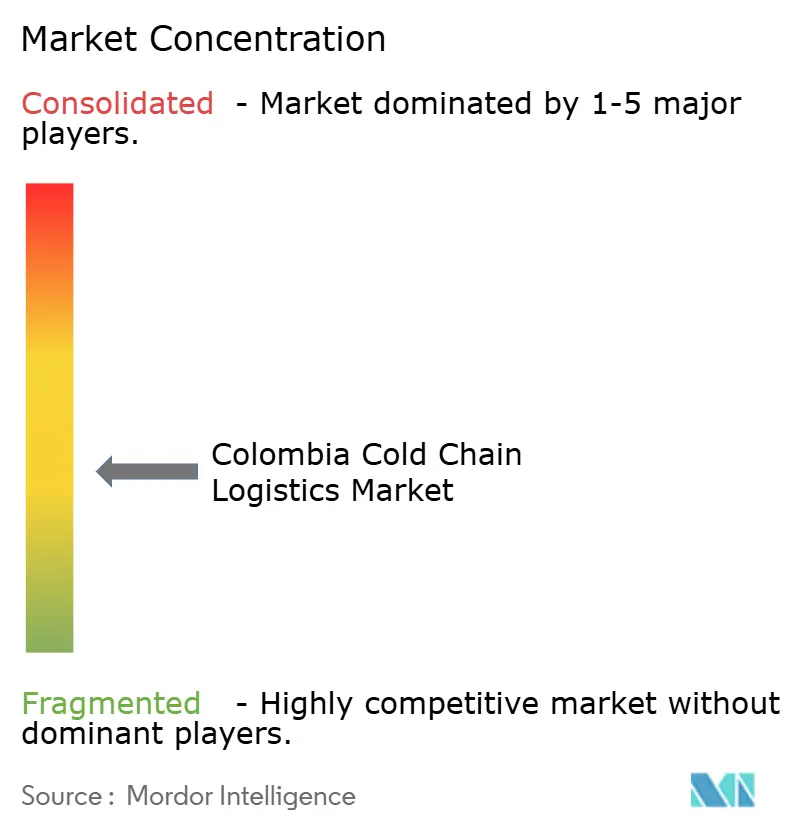

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Colombia Cold Chain Logistics Market Analysis by Mordor Intelligence

The Colombia cold chain logistics market size is expected to grow from USD 1.67 billion in 2025 to USD 1.75 billion in 2026 and is forecast to reach USD 2.35 billion by 2031 at a 6.10% CAGR over 2026-2031.

Accelerating urban demand for frozen convenience meals, fiscal incentives that reward energy-efficient refrigeration, and mandatory RFID traceability rules are reshaping operational economics, compliance thresholds, and service design across the Colombia cold chain logistics market. In parallel, a fast-expanding aquaculture export sector requires blast-freezing capacity capable of holding products at -18 °C to -25 °C during long inland hauls to Caribbean and Pacific ports. Competitive intensity rises as multinationals expand certified pharma campuses and regional specialists upgrade deep-frozen zones to capture cell- and gene-therapy volumes.

Key Report Takeaways

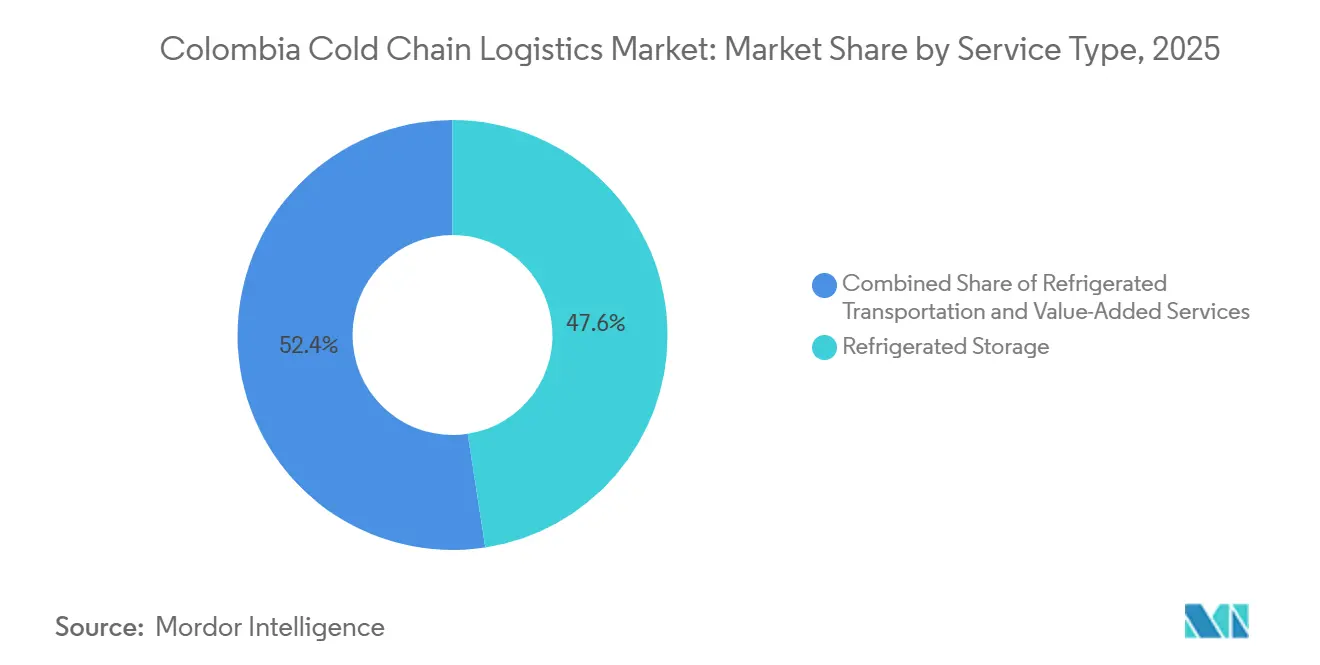

- By service type, refrigerated storage accounted for 47.6% of the Colombia cold chain logistics market share in 2025; value-added services are projected to expand at a 7.59% CAGR through 2031.

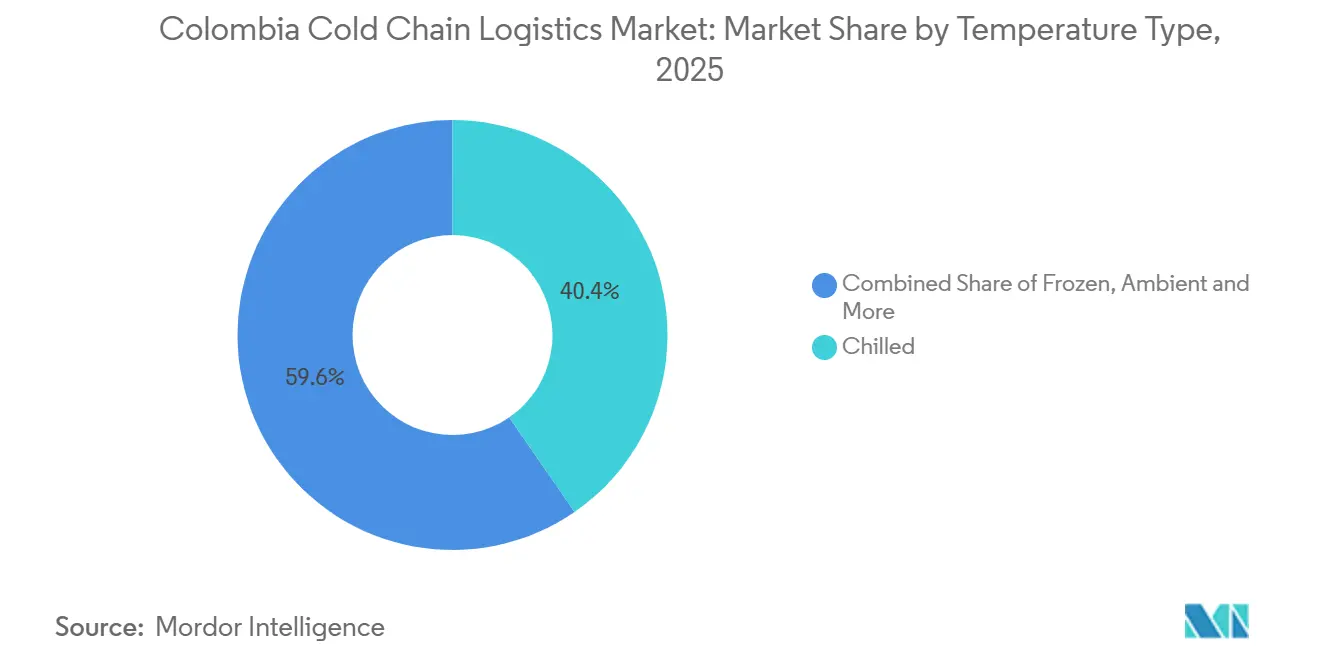

- By temperature type, chilled (0-5 °C) accounted for 40.4% of the Colombia cold chain logistics market size in 2025, and deep-frozen/ultra-low (-20 °C) is advancing at a 7.15% CAGR through 2031.

- By application, fruits and vegetables held a 28.41% share of the Colombia cold chain logistics market size in 2025, vaccines and clinical-trial materials are growing at a 9.06% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Colombia Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for frozen convenience meals among urban millennials | +1.3% | Bogota, Medellín, Cali, Barranquilla | Short term (≤ 2 years) |

| Aquaculture boom (particularly Atlantic salmon) lifting seafood‐export cold chains | +0.9% | Coastal and inland aquaculture zones | Medium term (2-4 years) |

| Tax credits for energy-efficient refrigeration under CONPES 4070 | +0.8% | National industrial corridors | Medium term (2-4 years) |

| Expansion of agro-industrial free-trade zones with mandatory temperature-controlled hubs | +1.0% | Bogota, Barranquilla, Cartagena, Cali | Long term (≥ 4 years) |

| Mandatory end-to-end RFID traceability rule (Decree 1079/2025) | +1.1% | Nationwide | Short term (≤ 2 years) |

| Emergence of cell- & gene-therapy imports requiring ultra-low-temperature logistics | +0.7% | Bogota, Medellín, Cali | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Frozen Convenience Meals Among Urban Millennials

Online grocery spending in major cities is surging, reinforcing the need for last-mile delivery slots that keep cargo at -18 °C. Dual-income households, reflected in a 54.7% female labor-force participation rate, favour ready-to-heat dishes that compress meal prep time[1]World Bank, “Population, total – Colombia,” data.worldbank.org . Quick-commerce platforms now retrofit dark stores with blast freezers and insulated totes to serve this segment. Retailers have doubled the number of frozen SKUs in metropolitan outlets, broadening assortments to include plant-based proteins and international cuisine. These shifts elevate pallet turns in urban cold rooms and magnify the technology premium for real-time monitoring systems in the Colombian cold chain logistics market.

Aquaculture boom (particularly Atlantic salmon) lifting seafood‐export cold chains

Annual production of 172,000 tons commands stringent -18 °C to -25 °C profiles from farm to vessel, particularly for rainbow trout and emerging Atlantic salmon trade lanes. Blast-freezing installations near Boyaca and Cundinamarca shorten the warm-chain window, while reefer container scarcity at coastal terminals creates peak-season congestion. Electronic phytosanitary certificates, adopted in 2024, cut customs dwell times and support the Colombia cold chain logistics market competitiveness in seafood. Investments leverage shared infrastructure with fruit exporters, unlocking utilization synergies for multi-temperature warehouses.

Tax Credits for Energy-Efficient Refrigeration Under CONPES 4070

Rebates erode the 15-20% capex premium of natural refrigerant assets, accelerating the adoption of ammonia and CO₂ that slash energy bills by up to 40%[2]UNEP, “Kigali Amendment to the Montreal Protocol,” unep.org . Electricity accounts for roughly 25% of a warehouse’s operating cost, so payback compresses from eight to five years under the incentive. Operators such as Ransa Colombia report 12% unit-cost savings after installing a 530 TR ammonia system. Compliance demands third-party energy audits, injecting transparency into the Colombia cold chain logistics market.

Expansion of Agro-Industrial Free-Trade Zones With Mandatory Temperature-Controlled Hubs

Colombia hosts 119 free-trade zones, several of which are newly obliged to include refrigerated warehousing for agro-exports. The Bogota zone alone spans 300 ha and anchors flower, pharma, and food clients that rely on just-in-time pre-cooling. Tax exemptions on imported refrigeration gear and zero income tax on export sales lure FDI, while integrated customs processes shorten port clearance cycles. These clusters concentrate demand for value-added services within the Colombia cold chain logistics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sparse intermodal (rail–road–port) reefer connectivity inflating transit times | -1.0% | Nationwide inland-to-coast corridors | Medium term (2-4 years) |

| High capex for natural-refrigerant conversions driven by F-gas phase-down | -0.9% | Industrial cold storage hubs | Long term (≥ 4 years) |

| Shortage of certified refrigeration technicians for advanced systems | -0.7% | Secondary urban nodes | Short term (≤ 2 years) |

| Peso volatility raising costs of imported reefer units & spare parts | -0.8% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Sparse intermodal (rail–road–port) reefer connectivity inflating transit times

Rail moves 1% of national freight, compelling cold chain operators to run diesel reefers for 18-20 h highway trips from Bogota to Barranquilla. Fuel-burn surges 25% compared with dry vans, while congested port gates without pre-cooling pads extend wait times during peak flower and avocado seasons. The USD 1.5 billion 2050 transport plan still tilts toward roads, limiting the potential for modal shift[3]BNamericas, “Colombia Presents US$1.5 bn Transport Plan,” bnamericas.com . These gaps erode the Colombia cold chain logistics market competitiveness for price-sensitive exports.

High capex for natural-refrigerant conversions driven by F-gas phase-down

Kigali mandates a 10% HFC cut by 2029, but ammonia or CO₂ systems carry 15-20% higher sticker prices and demand safety-critical design. Smaller warehouses struggle to accelerate depreciation on legacy HFC plants. Warm tropical climates add complexity to CO₂ trans critical efficiency, amplifying engineering and commissioning costs within the Colombia cold chain logistics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Integrated Solutions Outpace Basic Storage

Refrigerated storage generated 47.6% of the Colombia cold chain logistics market share in 2025 as exporters staged flowers, fruits, and pharmaceuticals for air and sea lanes. Multi-temperature chambers with 25,000-pallet capacity inside Bogota’s northern logistics parks illustrate the scale that anchors this segment. Yet value-added services, labeling, kitting, repacking, and customs documentation are outgrowing the core at a 7.59% CAGR through 2031. Shippers increasingly seek one-stop partners that couple storage with RFID audit streams to satisfy Decree 1079/2025. The Colombia cold chain logistics market size for integrated solutions, therefore, climbs even faster among pharmaceutical and seafood clients that outsource quality-assurance protocols to specialized 3PLs.

Second-tier functions such as order-level picking for dark-store networks and e-grocery fulfillment spur WMS adoption. Megafin Logistica’s Easy WMS instance sequences inventory by SKU life and thermal band, cutting picker travel by 30% and shrinking outbound dwell to under two hours. Cross-docking lanes shorten transit for flowers headed to Miami, reinforcing refrigerated transportation demand despite infrastructure shortfalls. Consequently, the Colombia cold chain logistics market share of providers offering end-to-end solutions is expected to widen as small, single-site storers cede accounts.

By Temperature Type: Ultra-Cold Applications Drive Fastest Expansion

Chilled cargo (0-5 °C) retained 40.4% of the Colombia cold chain logistics market share in 2025, led by dairy, produce, and certain biologics. However, the deep-frozen/ultra-low tier below -20 °C is scaling fastest at a 7.15% CAGR as cell-therapy vials and high-value seafood pull volumes into -80 °C lanes. Warehouse projects now dedicate separate wings with cryogenic redundancies and liquid-nitrogen back-ups to secure these profiles. Government vaccine freezer deployments provide a public anchor tenant, lowering risk for private investors who add incremental pallet positions under the same roof[4]Haier Biomedical, “Emergency Delivery to Colombia,” haierbiomedical.co.uk .

Frozen bands (-18 °C to 0 °C) still underpin the urban frozen-meal boom. Retailers recorded double-digit category growth, widening inventory rotation without undermining temperature integrity. Real-time IoT gateways flag door-open events that jeopardize uniformity in multi-temperature chambers, reinforcing predictive maintenance algorithms that now form standard operating practice across the Colombia cold chain logistics market.

By Application: Pharmaceuticals Surge Past Traditional Agriculture

Fruits and vegetables composed 28.41% of the 2025 sales of the Colombia cold chain logistics market size, thanks to avocado, banana, and flower exports. Yet vaccines and clinical-trial materials headline the future, booking a 9.06% CAGR through 2031. August 2024 legislation strengthening INVIMA’s regulatory scope forces stricter GDP compliance, elevating the technical entry bar. Multinationals respond by certifying Bogota and Medellin campuses under ISO 13485, cementing Colombia cold chain logistics market leadership in life-science distribution.

Fish and seafood volumes rise with aquaculture but require near-seamless air-chilled throughput to reach the United States and European buyers. Meat and poultry leverage domestic consumption tailwinds, while ready-to-eat meals benefit from urban e-commerce growth, each injecting diversity into throughput that lowers concentration risk for 3PLs. Dairy processors scale UHT and frozen dessert lines, extending shelf life and justifying regional cold-room rollouts in Valle del Cauca under MinAgricultura’s industrialization roadmap.

Geography Analysis

Bogota’s metropolitan zone houses the lion’s share of specialized cold storage, including Emergent Cold LatAm’s 25,000-pallet Red Polar hub and DHL’s GDP-rated campus in Cota. El Dorado International Airport processes 92% of flower exports, sustaining rapid pallet turnover and high asset utilization within the Colombia cold chain logistics market. Tocancipa’s Maersk complex adds 651 m² of reefer staging, bridging inland factories with Caribbean departures.

Medellin’s Antioquia region benefits from textile, coffee, and pharmaceutical clusters. The Guillermo Gaviria Echeverri Tunnel cuts freight time to Uraba ports in half, encouraging cool-chain transitions from road to short-sea feeder services. DHL Express has announced plans for a dedicated Medellin-United States flight within 24 months, elevating pharma export reliability.

Cali anchors sugar, processed food, and new pharma inflows. Emergent Cold LatAm’s greenfield facility enlarges pallet inventory and installs separate -40 °C zones for gene-therapy carriers. Barranquilla and Cartagena ports absorb rising seafood and fruit exports; the Conexion Norte highway prunes Cartagena-Medellin run-times by six hours, elevating corridor attractiveness for multi-product reefers. Secondary cities still lack certified technicians and large-scale cold rooms, signaling white-space expansion prospects for investors seeking first-mover gains in the Colombia cold chain logistics industry.

Competitive Landscape

The Colombia cold chain logistics market exhibits moderate fragmentation. The top five operators, DSV, Ransa Colombia, Frimac, Megafin Logistica, and Rentafrio, collectively control roughly 45-50% of installed pallet capacity, leaving space for niche specialists in ultra-cold and last-mile services. Strategic trajectories converge on vertical integration: DHL has earmarked EUR 200 million (USD 218 million) for Latin American healthcare campuses delivering GMP-aligned storage, serialization, and lane validation.

Emergent Cold LatAm strings Bogota, Cali, and Atlantic facilities into a 45,000-pallet national grid, backed by advanced WMS and ammonia installations. DSV layers order-level track-and-trace dashboards to satisfy Decree 1079/2025. Local challengers wield deep territory knowledge. Megafin Logistica capitalizes on agro-industrial relationships and invests in technician academies to reduce downtime.

Rentafrio focuses on modular solar-powered cold rooms in underserved coffee highlands, addressing technician scarcity through remote monitoring. Technology disruptors pilot blockchain traceability for salmon exports and AI-driven route optimization for e-grocery fulfillment, although high capex and compliance overheads temper rapid scaling.

Colombia Cold Chain Logistics Industry Leaders

Megafin Logistica Para Alimentos

Ransa Colombia (Colfrigos)

Rentafrio

Frimac

DSV Colombia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Emergent Cold inaugurated a new cold storage warehouse in Cartagena with over 9,000 pallet positions and 76,000 m³ of capacity as part of its investment plan ( USD 18 million) to strengthen refrigerated storage in the Caribbean region.

- April 2025: DHL Group earmarked USD 218 million for cold-chain improvements across Latin America. This includes facility and capability enhancements that impact DHL’s Colombian cold logistics services.

- April 2025: Emergent Cold LatAm announced construction of a new cold storage warehouse in Cali, one of Colombia’s key industrial hubs. The project’s first phase includes 7,000 pallet positions, expanding to 18,000 pallet positions when fully completed.

- March 2025: DHL Express announced plans for a new direct Medellin ↔ United States cargo route that will improve refrigerated product (flowers, pharma) export logistics within 24 months.

Colombia Cold Chain Logistics Market Report Scope

By Service Type

| Refrigerated Storage | |

| Refrigerated Transportation | Road |

| Rail | |

| Sea | |

| Air | |

| Value-Added Services |

By Temperature Type

| Chilled (0–5 °C) |

| Frozen (-18–0 °C) |

| Ambient |

| Deep-Frozen / Ultra-Low (less than-20 °C) |

By Application

| Fruits and Vegetables |

| Meat and Poultry |

| Fish and Seafood |

| Dairy and Frozen Desserts |

| Bakery and Confectionery |

| Ready-to-Eat Meals |

| Pharmaceuticals and Biologics |

| Vaccines and Clinical Trial Materials |

| Chemicals and Specialty Materials |

| Other Perishables |

| By Service Type | Refrigerated Storage | |

| Refrigerated Transportation | Road | |

| Rail | ||

| Sea | ||

| Air | ||

| Value-Added Services | ||

| By Temperature Type | Chilled (0–5 °C) | |

| Frozen (-18–0 °C) | ||

| Ambient | ||

| Deep-Frozen / Ultra-Low (less than-20 °C) | ||

| By Application | Fruits and Vegetables | |

| Meat and Poultry | ||

| Fish and Seafood | ||

| Dairy and Frozen Desserts | ||

| Bakery and Confectionery | ||

| Ready-to-Eat Meals | ||

| Pharmaceuticals and Biologics | ||

| Vaccines and Clinical Trial Materials | ||

| Chemicals and Specialty Materials | ||

| Other Perishables | ||

Key Questions Answered in the Report

How large will Colombia’s temperature-controlled logistics sector be by 2031?

The Colombia cold chain logistics market is forecast to reach USD 2.35 billion by 2031, expanding at a 6.10% CAGR from 2026.

Which service line is growing fastest in Colombian refrigerated supply chains?

Value-added services such as labeling, kitting, and regulatory documentation are projected to rise at a 7.59% CAGR, outpacing basic storage and transport.

What temperature band shows the highest growth momentum?

Deep-frozen and ultra-low applications below -20 °C are advancing at a 7.15% CAGR, driven by cell- and gene-therapy imports and premium seafood exports.

Why are fiscal incentives important in this market?

CONPES 4070 tax credits offset up to 20% of the premium for natural-refrigerant systems, cutting payback periods to five years and encouraging energy-efficient upgrades.

What infrastructure project most benefits cold logistics?

The USD 1.9 billion Antioquia–Bolivar highway cuts transit to Caribbean ports by six hours, lowering spoilage risk for perishables.

Which cities offer the strongest cold chain infrastructure today?

Bogota leads with extensive GDP-certified capacity, followed by Medellín and Cali, each benefiting from recent warehousing and airport investments that support pharmaceuticals and perishables.

Page last updated on: