Germany Scaffolding Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

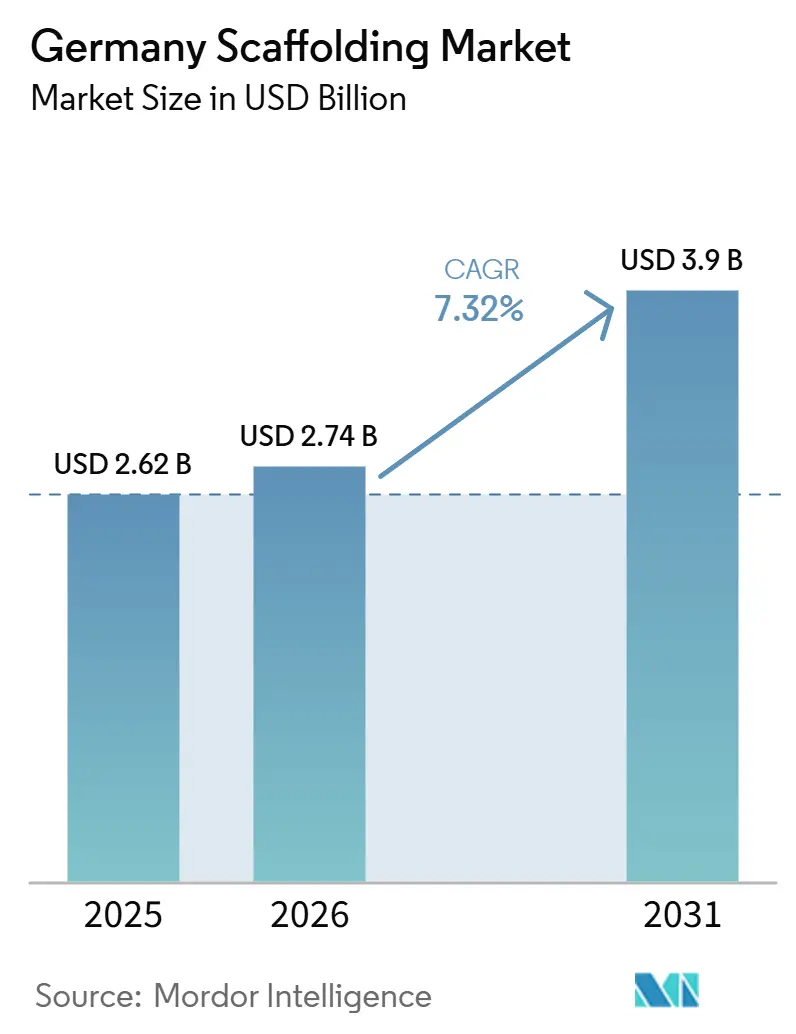

| Base Year Market Size (2025) | USD 2.62 Billion |

| Market Size (2026) | USD 2.74 Billion |

| Market Size (2031) | USD 3.9 Billion |

| Growth Rate (2026 - 2031) | 7.32% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Scaffolding Market Analysis by Mordor Intelligence

The Germany Scaffolding Market size is projected to be USD 2.62 billion in 2025, USD 2.74 billion in 2026, and reach USD 3.9 billion by 2031, growing at a CAGR of 7.32% from 2026 to 2031.

Public investment is now doing more of the heavy lifting for the Germany scaffolding market, with the federal government planning USD 141.9 billion of total investment in 2026, including USD 63.8 billion from the Special Fund for Infrastructure and Climate Neutrality, which is supporting transport, rail, bridge, and climate-linked construction programs that require large volumes of access systems and temporary structures. The growth path of the Germany scaffolding market is also tied to a widening renovation gap, because Germany’s building energy renovation rate was only 0.7% in 2025, while climate goals require a much faster pace of upgrades across existing stock, which keeps façade work, insulation retrofits, and restoration activity relevant well beyond the current cycle. Competitive positioning in the Germany scaffolding market is moving toward certified systems, faster assembly formats, and digital planning tools that help contractors meet documentation, design, and project coordination requirements on increasingly complex sites. Public works demand is creating room for growth in civil engineering and infrastructure maintenance, while the same environment is pushing suppliers to balance higher utilization with rising compliance and operating demands. Cost pressure still matters because construction prices in Germany remained elevated in late 2025, which limits margin expansion even as the Germany scaffolding market moves onto a stronger volume base.

Key Report Takeaways

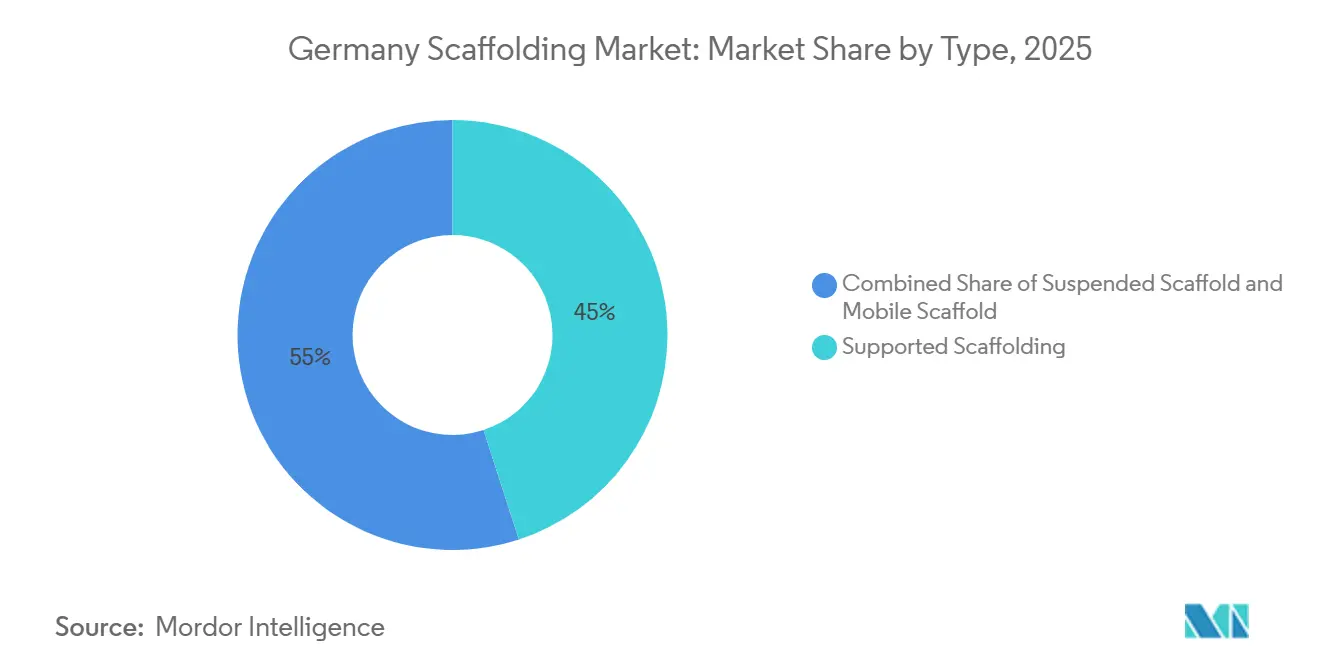

- By type, supported scaffolding held 45% of Germany scaffolding market share in 2025, while suspended scaffolding is projected to expand at an 8.8% CAGR through 2031.

- By system, modular / ringlock systems accounted for 38% of Germany scaffolding market size in 2025, while the segment is also projected to record the fastest CAGR of 7.6% through 2031.

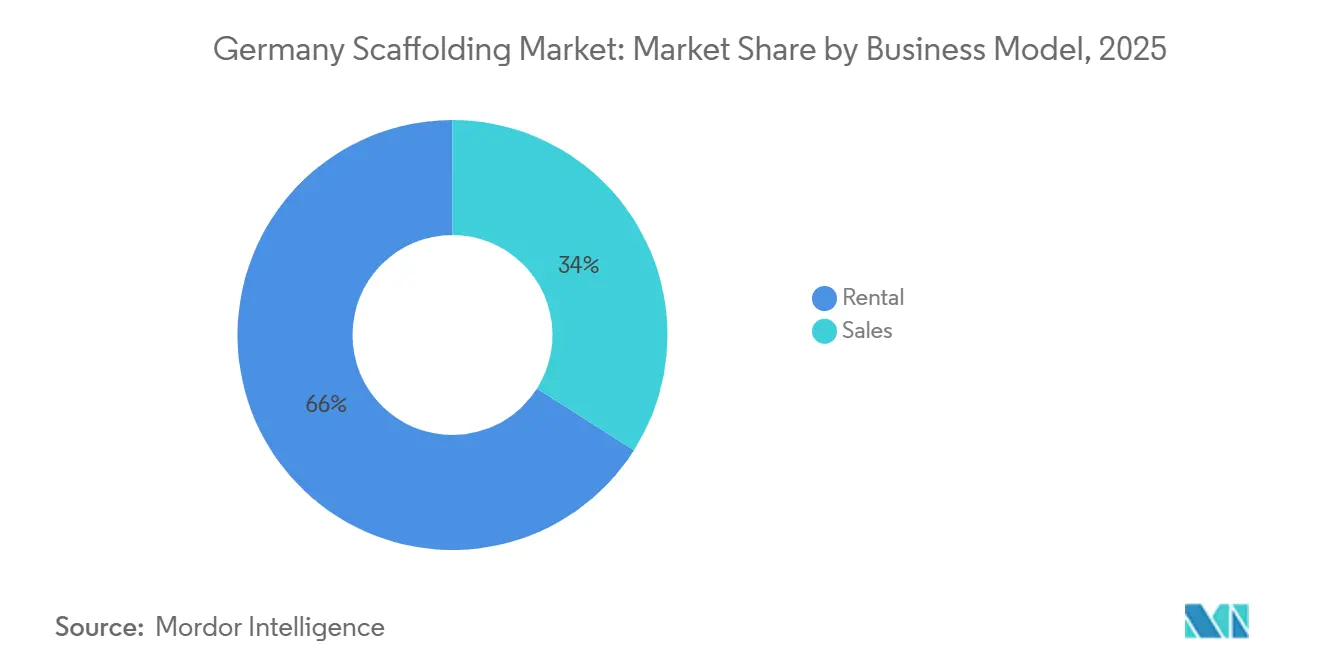

- By business model, rental captured 66% of Germany scaffolding market share in 2025 and is also forecast to post the fastest CAGR of 7.9% through 2031.

- By material type, steel held 61% of Germany scaffolding market share in 2025, while aluminum is expected to record the fastest CAGR of 7.8% through 2031.

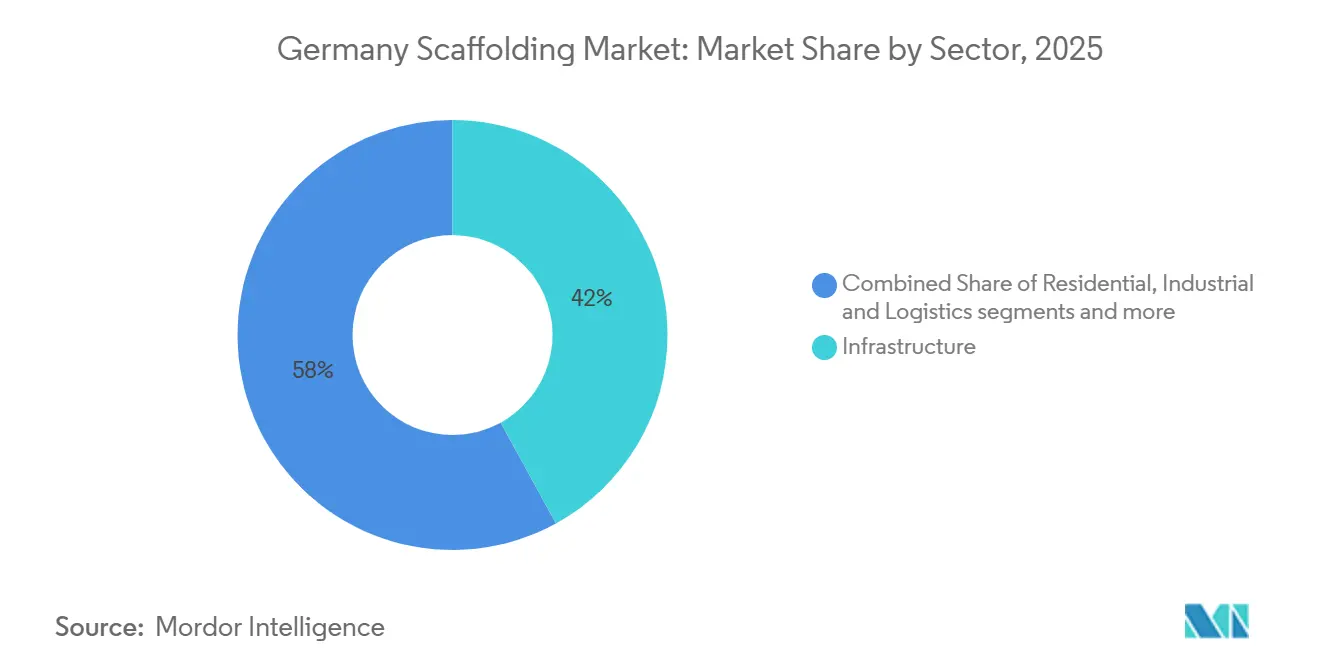

- By sector, infrastructure accounted for 42% of Germany scaffolding market size in 2025 and represented the largest contributor to Germany scaffolding market share, while it is also projected to post the fastest CAGR of 8.2% through 2031.

- By geography, West Germany led with 31% of Germany scaffolding market share in 2025, while East Germany is forecast to expand at the fastest CAGR of 8.1% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Scaffolding Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure Renovation and Energy Transition Projects Drive Scaffolding Demand | +2.2% | National, with strong relevance in East Germany, North Germany, and federal transport corridors | Medium term (2-4 years) |

| Strong Safety Regulations Support Adoption of Certified Scaffolding Systems | +1.5% | National, with early consolidation in Bavaria, North Rhine-Westphalia, and Saxony | Short term (≤ 2 years) |

| Refurbishment and Heritage Restoration Projects Increase Scaffolding Utilization | +1.1% | National, with high density in West Germany and South Germany | Medium term (2-4 years) |

| Rental Model Expansion Boosts Access Among Contractors and Industrial Users | +0.9% | National, especially in East Germany and historic urban cores in North and West Germany | Long term (≥ 4 years) |

| Modular / Ringlock System Adoption Enables Faster Project Execution | +0.8% | National, with faster adoption in large civil and industrial sites | Medium term (2-4 years) |

| Digital Planning and BIM Integration Improve Scaffolding Management Efficiency | +0.5% | National, with the highest relevance in the public sector and large engineered projects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Infrastructure Renovation and Energy Transition Projects Drive Scaffolding Demand

The Germany scaffolding market is drawing direct support from the federal investment cycle, now moving into execution, as 2026 funding plans include large allocations for transport, rail, and climate-related infrastructure, where scaffold access is required across multiple stages of civil work and maintenance. Germany’s 2026 funding structure includes large commitments for rail maintenance subsidies and bridge and tunnel maintenance, and these programs support recurring demand for supported, suspended, and project-specific access structures rather than short one-off jobs[1]Federal Ministry of Finance, “Special Fund for Infrastructure and Climate Neutrality,” Federal Ministry of Finance, bundesfinanzministerium.de. The same pattern extends to energy transmission, where grid expansion creates work not only at power-related assets but also at converter stations, substations, tunnel sections, cable access points, and other heavy civil interfaces that require controlled work-at-height systems over long construction schedules. Amprion’s Elb crossing tunnel contract, valued at USD 330 million and announced in March 2026, shows how power-grid construction is feeding specialized demand for access solutions in technically complex environments[2]Amprion, “Amprion Verpflichtet Die Firmen BEMO Tunnelling Und ÖSTU-STETTIN Für Den Bau Der Elbquerung ElbB,” Amprion Press Release, amprion.net. In the Germany scaffolding market, this matters because public infrastructure projects tend to span long timelines, require strict safety compliance, and create repeat work for firms that can deploy certified systems at scale across several regions.

Strong Safety Regulations Support Adoption of Certified Scaffolding Systems

The Germany scaffolding market operates within one of Europe’s more structured safety environments. That setting continues to favor formal operators that can document compliance, deploy tested systems, and support inspection-heavy projects without disruption. Public construction in Germany is also moving more firmly toward Building Information Modeling (BIM), which increases the value of suppliers that can integrate digital planning, material coordination, and site documentation into routine scaffolding delivery[3]Bundesministerium für Wohnen, Stadtentwicklung und Bauwesen, “BIM Deutschland,” BMWSB, bmwsb.bund.de. This shift not only raises the technical bar for engineered projects but also changes procurement behavior, as contractors and clients seek fewer handoff risks, clearer documentation, and better traceability from design through dismantling. The effect on the Germany scaffolding market is a gradual shift away from purely price-led competition toward qualification-led selection, especially in public works, infrastructure repair, industrial shutdowns, and sites with complex geometry. As that happens, larger system suppliers and capable regional scaffolding companies are better positioned to win work, because compliance, documentation, and system certification are becoming part of day-to-day commercial differentiation rather than an afterthought.

Refurbishment and Heritage Restoration Projects Increase Scaffolding Utilization

The Germany scaffolding market is also supported by work that does not depend entirely on new-build cycles, especially façade restoration, energy retrofits, and preservation of older building stock in dense urban areas and historically sensitive locations. Germany’s energy renovation rate was only 0.7% in 2025, well below the pace needed to meet climate objectives, and this gap implies a long runway for external envelope work, insulation upgrades, and access requirements for roofs and façades. Heritage projects add another layer to the Germany scaffolding market because they often require custom layouts, suspended configurations, lower load concentrations, and slower but more controlled installation methods, which support premium pricing. The same demand pattern appears across older public buildings, monuments, civic structures, and urban renovation projects, where scaffold design must adapt to narrow streets, preservation rules, and restricted anchoring conditions. As a result, the Germany scaffolding market benefits from a stream of technically demanding contracts that may be smaller than major infrastructure packages, but often carry longer installation periods and more specialized engineering requirements.

Rental Model Expansion Boosts Access Among Contractors and Industrial Users

Rental remains central to the Germany scaffolding market because many contractors prefer access to a compliant fleet without tying up capital in ownership, maintenance, inspection routines, and periodic upgrades, given project visibility that can still shift from quarter to quarter. This model is especially attractive for smaller renovation firms, occasional industrial users, and contractors moving between façade work, maintenance contracts, and short civil packages where utilization is not consistent enough to justify large owned inventories. The rental-heavy structure of the Germany scaffolding market also helps spread advanced systems more quickly, because specialist providers can invest in modular fleets, digital tracking, and logistics capabilities that smaller buyers would struggle to carry on their own balance sheets. That creates a practical advantage for high-specification products, since better systems become accessible to a wider customer base through day-rate and project-rate pricing rather than upfront equipment purchase. Over time, this makes the Germany scaffolding market more service-oriented, with providers competing not only on fleet availability but also on planning support, delivery speed, system mix, training, and the ability to handle documentation for larger jobs.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Labor Costs and Skilled Erector Shortages Constrain Market Growth | -1.8% | National, most acute in Hamburg, Munich, Frankfurt, and Berlin | Short term (≤ 2 years) |

| Raw Material Price Volatility Pressures Manufacturer and Contractor Margins | -1.2% | National, with high exposure in steel-intensive regions and large fleet operators | Medium term (2-4 years) |

| Environmental Compliance Requirements Increase Operational Costs | -0.7% | National, with a higher burden on older fleet operators | Medium term (2-4 years) |

| High Upfront Fleet and Maintenance Costs Limit Investment Capacity | -0.5% | National, especially restrictive for small and medium-sized enterprises in rural markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Labor Costs and Skilled Erector Shortages Constrain Market Growth

Labor availability is one of the clearest operating limits for the Germany scaffolding market, because stronger project pipelines do not automatically translate into faster execution when skilled erection crews remain difficult to secure across major construction hubs. The wider construction sector is missing around 250,000 qualified workers, and the pressure is especially visible in trades that require physical intensity, strict safety practice, and hands-on site experience. The March 2025 skilled labor report from the Germany Property Federation also warned that labor shortages could slow the translation of investment momentum into completed projects, which matters directly for a service-heavy field like scaffolding, where labor is inseparable from revenue delivery. For the Germany scaffolding market, that means firms may see healthy order books and still struggle with throughput, bidding discipline, and margin protection when crew availability becomes the real bottleneck. The practical result is that growth can remain positive. At the same time, project timing stretches out, subcontracting increases, and only the more organized operators can capture the full benefit of the demand upswing.

Raw Material Price Volatility Pressures Manufacturer and Contractor Margins

Material cost pressure continues to weigh on the Germany scaffolding market, because steel remains the dominant base material and fleet-intensive operators are exposed both when buying new systems and when replacing worn components across heavily used inventories. Germany’s construction prices for residential buildings rose 3.2% year over year in November 2025, while metalwork prices rose 2.2%, indicating that cost escalation was still flowing through the value chain even as activity conditions began to stabilize. This pressure is difficult to manage in the Germany scaffolding market because long-duration contracts and fixed-price tenders do not always allow full cost pass-through once a project is underway. Aluminum offers weight and handling benefits, but it is also sensitive to broader energy and supply conditions, so it does not eliminate cost risk, even when it improves productivity and site flexibility. For many operators, the outcome is a narrower spread between top-line growth and actual earnings improvement, which means the Germany scaffolding market can expand in value. In contrast, many suppliers still face tight operating economics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Supported Scaffolds Account for the Largest Share, While Suspended Scaffolds Accelerate

Supported scaffolding accounted for 45% of the Germany scaffolding market value in 2025, making it the largest type segment. Its lead came from the wide range of jobs that still need stable, ground-based access platforms, including façade insulation work, bridge parapet repairs, tunnel portal finishing, and industrial plant maintenance. Supported systems remain the standard choice because they are practical, cost-predictable, and well aligned with Germany safety and performance requirements. Mobile scaffolding continued to serve a smaller but steady role in commercial maintenance and short interior access work, where quick repositioning is more important than heavy load capacity. This kept supporting scaffolding at the center of routine demand across the Germany scaffolding market.

Suspended scaffolding is forecast to record the fastest CAGR of 8.8% through 2031. Growth is being supported by bridge deck soffit maintenance, high-rise glass façade work in Frankfurt, Hamburg, and Munich, and more complex restoration projects in dense urban areas. Federal support for bridge and tunnel maintenance, including USD 3.6 billion in 2026 funding, is also helping to drive demand for suspended systems higher. Wind repowering adds another layer of demand, because taller turbine structures increasingly need more specialized access during construction and maintenance. The Frankfurt Langer Franz Rathausturm project clearly shows this shift, since the scaffold had to be hung from window openings rather than using standard ground support.

By System: Modular / Ringlock Formats Reshape Project Delivery Efficiency

Modular / ringlock systems accounted for 38% of the Germany scaffolding market value in 2025, making them the largest system segment. They are also the fastest-growing segment, with a projected CAGR of 7.6% through 2031. Contractors are choosing these systems because they allow faster assembly, more consistent layouts, and better performance on structured civil and industrial projects. Their standardized design also supports the approval requirements needed for many federally tendered contracts. This combination of speed, consistency, and compliance has made modular / ringlock systems the leading format in the market.

The competitive environment in this segment is also becoming more active. PERI expanded its PERI UP scaffolding system in June 2025 with new modules, which shows that suppliers are still adding functionality rather than treating the segment as mature. Doka’s entry into the Germany scaffolding market in November 2024 also increased pressure in a category previously led mainly by Layher and PERI. Frame and H-frame systems still hold value in standard residential work, while tube & coupler systems remain important in industrial projects with irregular geometry. Digital planning is also pushing adoption higher because standardized modular systems work more easily with Building Information Modeling (BIM), and automated quantity planning.

By Business Model: Rental Access Reshapes Contractor Economics

Rental accounted for 66% of the Germany scaffolding market value in 2025, making it the largest business model segment. It is also the fastest-growing category, with a projected CAGR of 7.9% through 2031. This reflects a clear shift in contractor behavior, as more firms are choosing to rent scaffold fleets rather than own them. Rental helps them avoid the full burden of certification, maintenance, and upgrades at a time when compliance requirements are becoming more demanding. That is why rental continues to strengthen its position across the Germany scaffolding market.

The July 2024 transition law added more pressure on firms that erect scaffolding for third parties without formal certification, making specialist rental providers even more attractive. Germany had around 217 registered scaffolding rental service providers as of April 2026, and the actual market capacity is higher when the rental divisions of integrated manufacturers are included. The sales segment still held 34% of market value in 2025 and remained important for large Engineering, Procurement, and Construction (EPC) contractors and public utilities with long-duration programs. Even so, rental fleets are being upgraded toward modular / ringlock systems, which command stronger rates and support longer project cycles. This means rental operators are improving revenue quality even without major workforce growth.

By Material Type: Steel Anchors the Base, Aluminum Accelerates

Steel accounted for 61% of the Germany scaffolding market value in 2025, making it the largest material segment. Its position remains strong because steel offers high load-bearing performance, broad supply availability, and deep compatibility with Germany scaffold standards. Large public works and rail and bridge maintenance programs continue to rely on steel because it performs well under heavy and repeated use. This is especially relevant across projects run by major transport and infrastructure operators, where durability and long service life matter more than lower weight. Steel, therefore, remains the base material across much of the Germany scaffolding market.

Aluminum is forecast to grow at the fastest CAGR of 7.8% through 2031. Its lighter weight makes it more suitable for energy-efficiency refurbishments, heritage restoration, and pharmaceutical plant work, where load limits and access geometry are more restrictive. Layher’s Allround Lightweight series reflects how suppliers are bringing aluminum into formats that existing fleets can adopt more easily. From 2026, the European Union Carbon Border Adjustment Mechanism is also expected to increase cost pressure on imported steel and aluminum, which may support greater interest in domestic and recycled-content materials. Timber and plywood still serve a specialist role in heritage work. At the same time, plastic and fiberglass systems remain relevant in chemical and pharmaceutical settings where ignition-sensitive conditions limit the use of metal systems.

By Sector: Infrastructure Spending Defines the Growth Trajectory

Infrastructure accounted for 42% of the Germany scaffolding market value in 2025, making it the largest segment. It is also the fastest-growing sector, with a projected CAGR of 8.2% through 2031. This makes Germany stand out from many other Western European markets, where residential construction usually carries more weight. Infrastructure growth is being driven by the Special Fund for Infrastructure and Climate Neutrality, which totals USD 550 billion. Within the 2026 federal budget alone, this included USD 3.6 billion for bridge and tunnel maintenance and USD 17.9 billion in rail subsidies.

Energy grid expansion is further supporting the infrastructure segment. Amprion’s Elb crossing cable tunnel, valued at USD 330 million and due to begin construction from late 2026, and 50Hertz’s SuedOstLink overhead line work both need supported and suspended scaffold across distributed civil worksites. This gives infrastructure demand greater depth than a simple transport story. It also creates future maintenance cycles, since each new bridge or motorway renewal can lead to long-term follow-on access work. Residential demand remains limited by Germany’s low 0.67% annual energy renovation rate in 2025, while commercial and industrial activity continues to support a steady secondary demand base.

Geography Analysis

West Germany accounted for 31% of Germany's scaffolding market in 2025, making it the largest regional cluster, as it combines dense construction activity, industrial concentration, and a large installed base of maintenance-heavy assets. The region benefits from continuous demand across North Rhine-Westphalia, Hessen, Baden-Württemberg, and Rhineland-Palatinate, where chemical, automotive, logistics, and public building projects create a steady flow of scaffold work rather than a narrow set of one-time contracts. Historic restoration also strengthens utilization in the west, since long-duration work on legacy structures and urban landmarks tends to support more predictable project calendars for regional operators. The Germany scaffolding market, therefore, starts from a strong Western base where industrial maintenance, civic restoration, and transport renewal overlap within a relatively compact geography.

East Germany is the fastest-growing regional pocket in the Germany scaffolding market, with an 8.1% CAGR through 2031, driven by infrastructure catch-up, digital build-out, and energy transition projects arriving together rather than in isolation. Dresden’s Campuslinie transport project, launched in June 2026 with an investment of USD 356.4 million, illustrates the scale of work now supporting bridge construction and related access demand in the east. Coal transition activity in Saxony also supports the Germany scaffolding market through new energy projects and related civil works. At the same time, fiber expansion across multiple eastern sites adds another layer of access demand that is less tied to the traditional building cycle. The east stands out because it is combining transport upgrades, grid-related construction, local redevelopment, and utility-linked work within the same investment window. That mix gives East Germany a stronger growth profile than its current size alone would suggest.

South Germany remains important to the Germany scaffolding market because Bavaria and Baden-Württemberg combine large civil projects, industrial capacity, and early adoption of advanced modular systems. The April 2025 bauma event in Munich also reinforced the south’s role as a sourcing and product-launch region, with innovations from major suppliers feeding into active deployment across infrastructure and industrial jobs. North Germany adds a different demand pattern through port infrastructure, offshore wind support activity onshore, and transmission-related construction corridors, which gives the Germany scaffolding market a broader geographic spread than a single-region story would suggest. Taken together, these regional profiles show a market where the west holds the largest share, the east is growing fastest, and the south and north each add distinct demand streams that support national expansion.

Competitive Landscape

The Germany scaffolding market is moderately concentrated at the system-supply level and clearly more fragmented at the contracting and rental level, where hundreds of certified regional firms operate beside a smaller group of major manufacturers and engineered system providers. Layher Holding GmbH & Co. KG, PERI SE, Altrad through Plettac Assco GmbH, BrandSafway through Hünnebeck by BrandSafway, and Doka are the main named participants shaping product competition in the Germany scaffolding market. Layher remains influential because its Allround platform has long-standing familiarity in the field. At the same time, PERI benefits from offering formwork and scaffolding within a single engineering relationship on more complex jobs. The draft also indicates that no materially irrelevant companies were identified in the competitive set, meaning the listed manufacturers, rental businesses, and specialist erection contractors all fall within the defined scope of the Germany scaffolding market.

Strategic competition in the Germany scaffolding market is moving toward digital coordination, system compatibility, and adjacent value-chain partnerships rather than simple price-cutting alone. Hünnebeck by BrandSafway and alkus AG signed a supply partnership in August 2025 that expanded collaboration across formwork panel lines, demonstrating how established players are widening their solution offerings around the jobsite rather than staying within a narrow product boundary. PERI also documented a Germany pharmaceutical plant project in December 2025, where the PERI UP system and Building Information Modeling-based planning through the myPeri portal supported coordination between formwork and access requirements on a complex build. Doka’s 2024 entry into the segment added another global formwork-led competitor to the Germany scaffolding market, underscoring that engineered access is seen as a strategic adjacent business rather than a peripheral add-on. These moves show that leading suppliers are trying to deepen customer dependence through integrated planning, broader system ecosystems, and closer linkage between scaffold supply and wider site execution.

Digital differentiation is becoming more important in the Germany scaffolding market because public works and larger private projects increasingly reward suppliers that can support planning, logistics, documentation, and inspection workflows with fewer manual gaps. Layher’s Scaffold Information Management platform and PERI’s myPeri tools reflect the same shift toward project visibility, traceability, and digital handover, especially as Building Information Modeling processes gain ground. The market still leaves room for regional specialists. Still, firms without strong engineering support or digital capabilities face a higher risk of losing access to larger, more formal procurement channels. Industrial maintenance in North Rhine-Westphalia, digital rental services for small and medium-sized contractors, and suspended access for glass-heavy high-rise maintenance in Frankfurt, Munich. Hamburg remains the area where competition is likely to remain active across the Germany scaffolding market.

Germany Scaffolding Industry Leaders

Layher Holding GmbH & Co. KG

PERI SE

Doka Deutschland GmbH

ALTRAD Industrial Services GmbH

Brand Energy & Infrastructure Services GmbH (BrandSafway)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: CMC Group, backed by the Metrika fund, acquired a majority stake in CMC Arbeitsbühnen GmbH & Co. KG and Equipment Service GmbH in Germany. CMC Arbeitsbühnen had been the long-standing official dealer for CMC in the German access equipment space, while Equipment Service specialized in technical aftermarket support. After the deal, CMC Deutschland became the commercial and logistics hub for the DACH region, which includes Germany, Austria, and Switzerland. The acquisition strengthens CMC’s position in Germany for spider lifts and elevated access platforms used in construction and industrial maintenance.

- March 2026: Felbermayr acquired Hoffmann's lifting scaffold assets, including two 1,000-tonne lifting scaffold systems and a fleet of Sefiro heavy transport vehicles, to strengthen its Engineered Solutions division for complex industrial and civil engineering projects.

- February 2026: Belgian scaffolding manufacturer AFIX Group established AFIX GmbH near Munich and obtained DIBt approval for its AFIXFAST X52 modular scaffold system. The new subsidiary will serve as the company's sales, logistics, and rental hub for the DACH region (Germany, Austria, and Switzerland), marking its formal expansion into the German market.

Germany Scaffolding Market Report Scope

The Germany Scaffolding Report is Segmented by Type (Supported, Suspended, and Mobile Scaffold), System (Tube & Coupler, Cuplock, and More), Business Model (Sales and Rental), Material Type (Timber / Plywood, Steel, Aluminum, and More), Sector (Residential, Commercial, Industrial & Logistics, and Infrastructure), and Geography (North, West, South, and East Germany). The Market Forecasts are Provided in Terms of Value (USD).

| Supported Scaffold |

| Suspended Scaffold |

| Mobile Scaffold |

| Tube & Coupler |

| Cuplock |

| Modular / Ringlock |

| Frame / H-Frame |

| Sales |

| Rental |

| Timber / Plywood |

| Steel |

| Aluminum |

| Plastic / Fibreglass |

| Others |

| Residential |

| Commercial |

| Industrial & Logistics |

| Infrastructure |

| North Germany |

| West Germany |

| South Germany |

| East Germany |

| By Type | Supported Scaffold |

| Suspended Scaffold | |

| Mobile Scaffold | |

| By System | Tube & Coupler |

| Cuplock | |

| Modular / Ringlock | |

| Frame / H-Frame | |

| By Business Model | Sales |

| Rental | |

| By Material Type | Timber / Plywood |

| Steel | |

| Aluminum | |

| Plastic / Fibreglass | |

| Others | |

| By Sector | Residential |

| Commercial | |

| Industrial & Logistics | |

| Infrastructure | |

| By Geography | North Germany |

| West Germany | |

| South Germany | |

| East Germany |

Key Questions Answered in the Report

What is the 2026 value of the Germany scaffolding market?

The Germany scaffolding market stands at USD 2.74 billion in 2026 and is projected to reach USD 3.90 billion by 2031, growing at a 7.32% CAGR.

Which end-use segment leads demand in Germany?

Infrastructure is the largest sector, with a 42% share in 2025, supported by rail, bridge, tunnel, and energy transition-related construction programs.

Which scaffold type is growing fastest in Germany?

Suspended scaffolding is the fastest-growing type, with an 8.8% CAGR through 2031, driven by bridge work, high-rise maintenance, and constrained restoration projects.

Why does rental dominate scaffolding demand in Germany?

Rental held 66% of the market in 2025 because contractors value flexibility, lower capital commitment, and access to compliant fleets without owning and maintaining equipment.

Which region shows the strongest growth outlook?

East Germany is projected to grow the fastest at an 8.1% CAGR through 2031, supported by transport upgrades, energy transition projects, and digital infrastructure build-out.

What is shaping competition among major suppliers?

Competition is increasingly centered on modular systems, digital planning support, integrated jobsite offerings, and partnerships that connect scaffolding with wider construction workflows.

Page last updated on: