Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

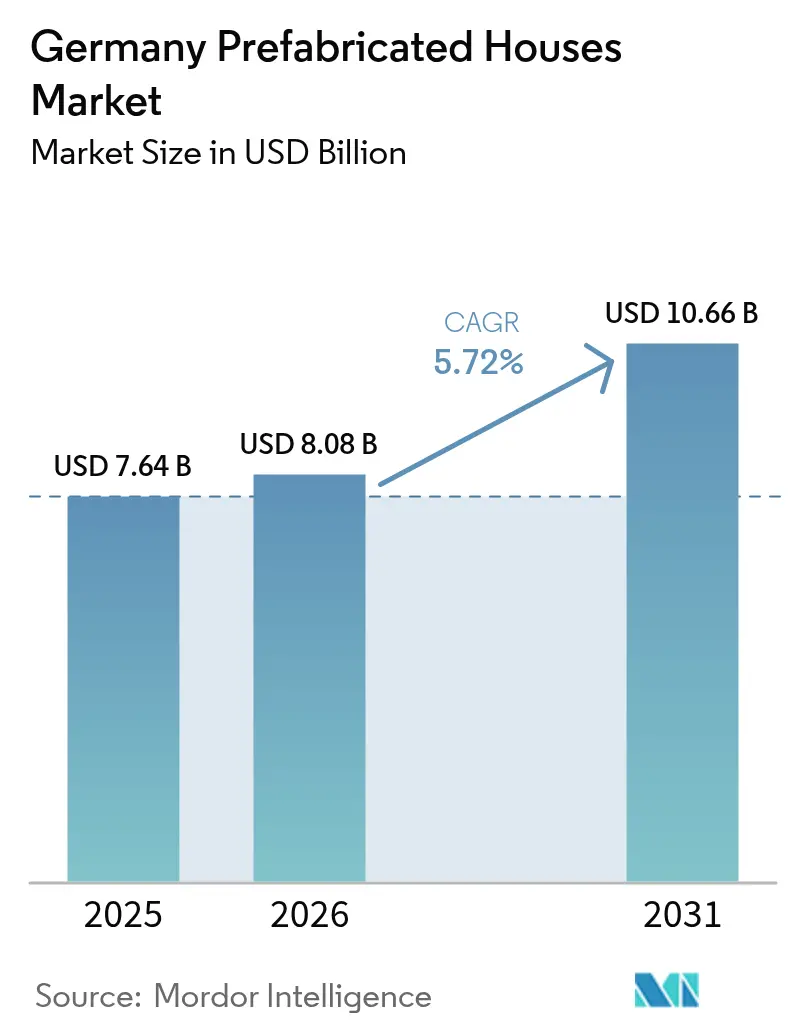

| Base Year Market Size (2025) | USD 7.64 Billion |

| Market Size (2026) | USD 8.08 Billion |

| Market Size (2031) | USD 10.66 Billion |

| Growth Rate (2026 - 2031) | 5.72% CAGR |

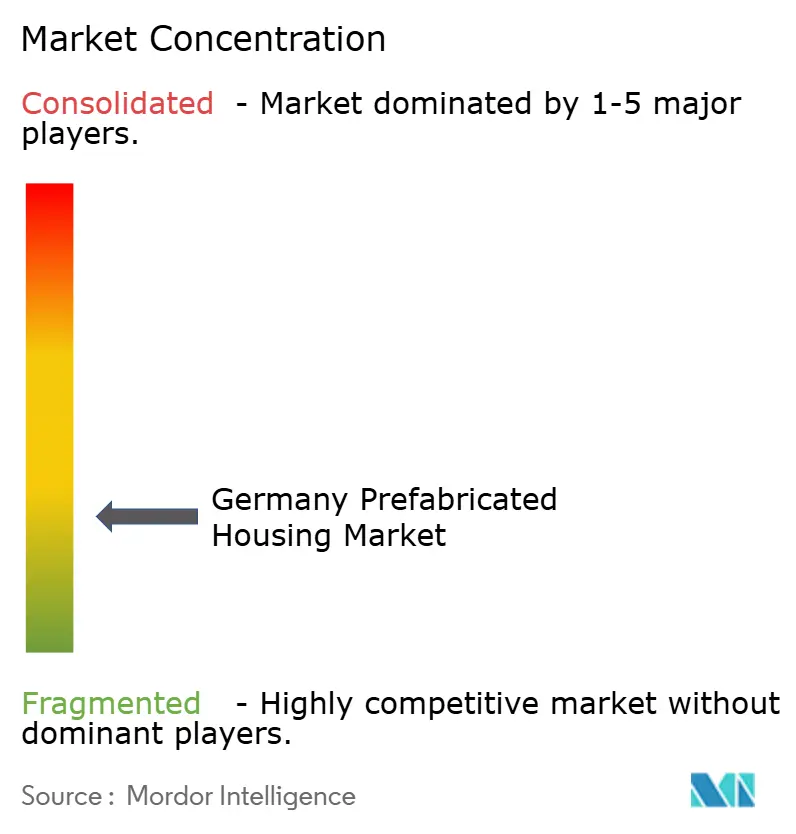

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Prefabricated Houses Market Analysis by Mordor Intelligence

The Germany prefabricated housing market size was valued at USD 7.64 billion in 2025 and estimated to grow from USD 8.08 billion in 2026 to reach USD 10.66 billion by 2031, at a CAGR of 5.72% during the forecast period (2026-2031). Demand is fueled by an 800,000-unit national housing gap, escalating renewable-energy rules under GEG 2024, and KfW’s USD 1.21 billion (converted from EUR 1.1 billion at 1 EUR = 1.1 USD) commitment to climate-friendly new construction programs. Factory-built solutions cut delivery times to 35 days versus 16 months for conventional builds, a speed advantage that resonates with municipal procurement officers pressed to meet social-housing deadlines. Energy-efficient design baked in at the production stage positions prefab homes to capture a disproportionate share of KfW and BEG subsidies, while widespread labor shortages in the traditional trades nudge contractors toward highly automated plants. Meanwhile, digital design standards such as DIN SPEC 91400 and the rapid maturation of 3D-printed concrete modules are broadening material choices, giving consumers and developers alike more options without lengthening project timelines[1]Clean Energy Wire, “Germany Boosts Funding for Energy-Efficient Homes,” cleanenergywire.org.

Key Report Takeaways

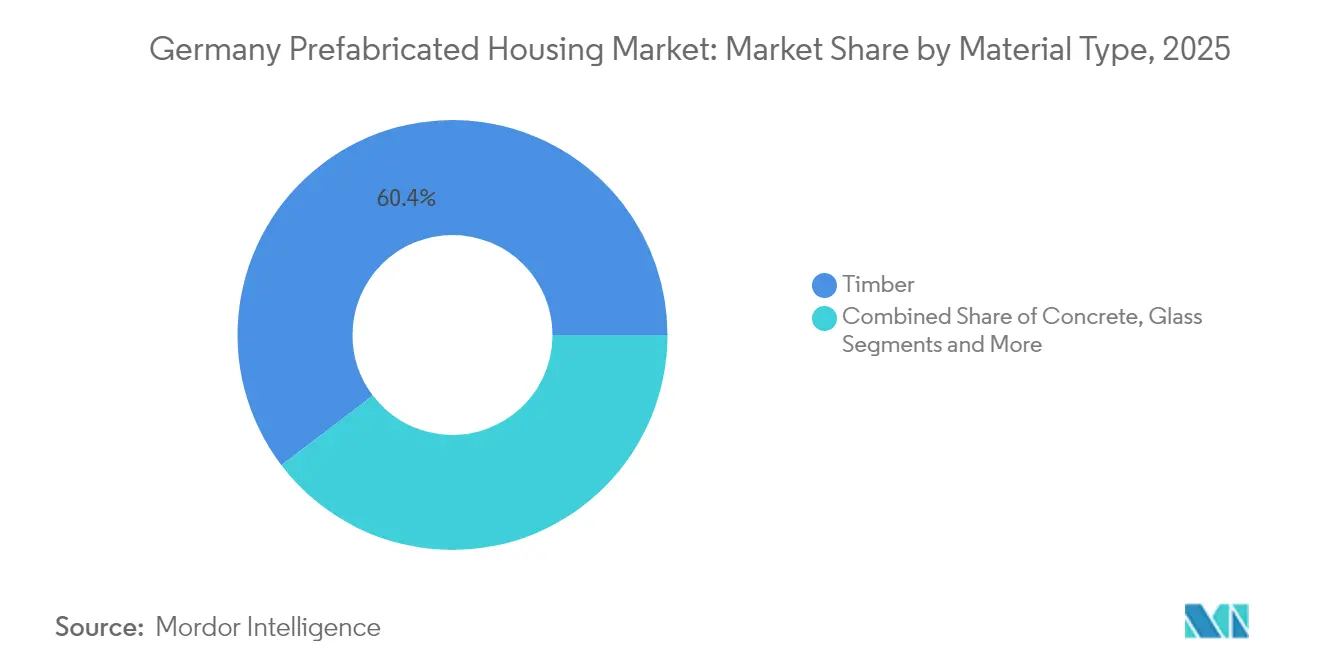

- By material type, timber led with 60.35% of the Germany prefabricated housing market share in 2025; concrete is projected to expand at a 6.28% CAGR to 2031.

- By type, single-family units captured 71.20% share of the Germany prefabricated housing market in 2025, while multi-family units are forecast to grow at a 6.02% CAGR through 2031.

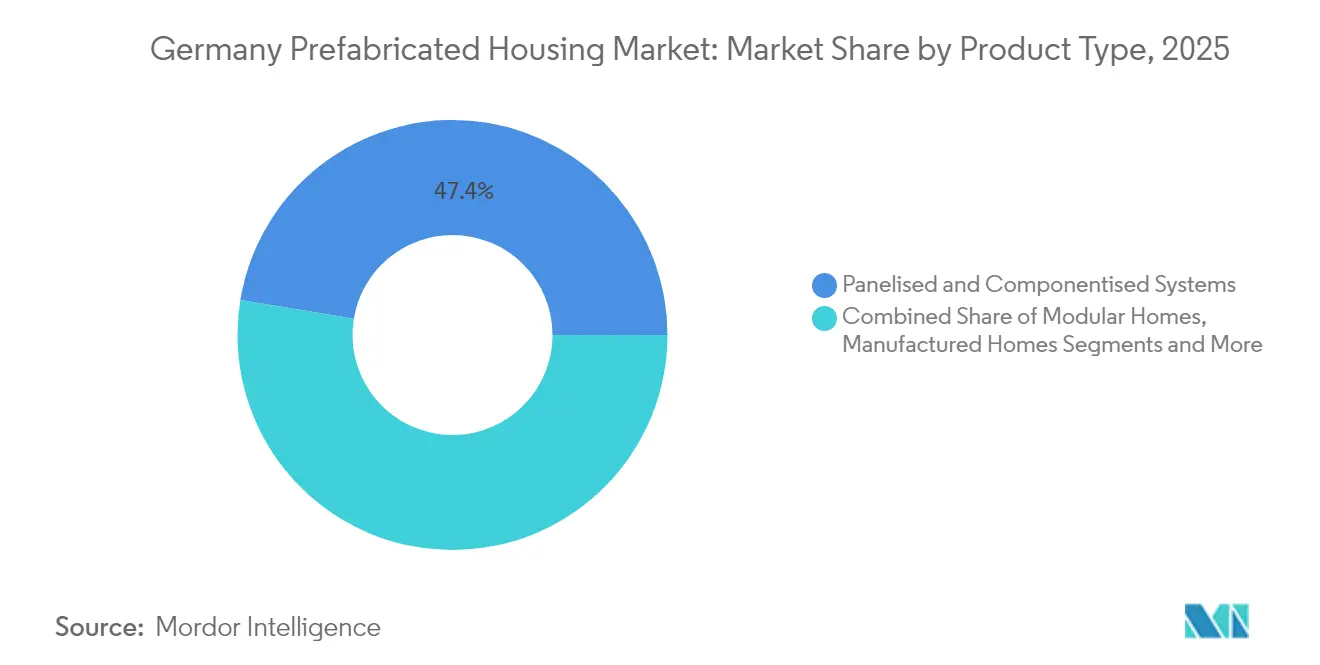

- By product type, panelised and componentised systems held 47.40% of the Germany prefabricated housing market share in 2025; modular homes will advance at a 6.22% CAGR over the forecast period.

- By key cities, Berlin accounted for 16.85% of the Germany prefabricated housing market size in 2025, whereas Frankfurt records the highest projected CAGR at 6.45% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Prefabricated Houses Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic 800,000-unit housing deficit promotes serial-construction tenders | +1.8% | Berlin, Hamburg, Munich, Frankfurt, Cologne | Long term (≥ 4 years) |

| KfW / BEG subsidies accelerate demand for energy-efficient prefab homes | +1.2% | National—strongest in Baden-Württemberg and Bavaria | Short term (≤ 2 years) |

| Factory automation & robotics offset skilled-labor shortages | +0.9% | North Rhine-Westphalia, Baden-Württemberg | Medium term (2-4 years) |

| CO₂-pricing, timber-quota targets & GEG 2024 favour low-carbon wood modules | +0.8% | Forest-rich regions nationwide | Long term (≥ 4 years) |

| BIM-centred design plus 3D-printed parts shorten planning cycles | +0.7% | Munich, Stuttgart, Hamburg | Medium term (2-4 years) |

| Bundeswehr & disaster-relief contracts spur rapid-deploy volumetric units | +0.4% | Defense sites and emergency zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Chronic 800,000-unit housing deficit promotes serial-construction tenders

Germany’s urban centers collectively miss annual completion targets by tens of thousands of units, a shortfall that has prompted cities such as Cologne and Hamburg to specify prefab formats in social-housing tenders. Serial construction frameworks cut costs by 22% and slash delivery schedules by well over a year, yielding predictable outcomes that satisfy value-for-money audits. The evolution from lowest-price bids toward life-cycle-value scoring further tilts procurement rules toward industrialized builders able to guarantee energy-performance metrics upfront. Policy signals are now explicit: Berlin’s latest statewide guidelines set a 30% prefab allocation for new municipal projects, locking in market visibility for suppliers. Developers who ignore serial bidding risk exclusion from a pipeline likely to exceed USD 35 billion in public-sector spending to 2030[2]Federal Ministry for Housing, Urban Development and Building, “GEG 2024 Implementation Guide,” bmwsb.bund.de.

KfW / BEG subsidies accelerate demand for energy-efficient prefab homes

Germany’s flagship KfW and BEG programs now cover up to 70% of eligible renewable-heating costs, driving middle-income buyers toward factory-produced dwellings that integrate heat pumps and solar arrays before leaving the plant. Loan volumes for energy-efficiency upgrades rose 17% in 2024, confirming that homeowners view subsidies as decisive. Prefab makers fold these incentives into turnkey offers, which lowers the effective entry price and allows rapid disbursement once on-site work is verified. Urban municipalities further sweeten the proposition by reducing permit fees for projects that meet KfW Efficiency House 40 standards. Continued political backing appears strong for 2025, but future budgets could tighten, making cost-optimized production essential to maintain momentum.

Factory automation & robotics offset skilled-labor shortages

Roughly 175,000 construction vacancies across Germany have lifted trade wages and lengthened site schedules, prompting producers to deploy multi-robot cells that saw, nail, and finish wall panels with negligible human input. Plants equipped with ZeroLabor platforms can reduce shop-floor headcount by 70% without compromising throughput. Robotics also boosts dimensional accuracy, lowering re-work rates and warranty claims that erode profit margins. Industrial regions such as Baden-Württemberg lead adoption because they already host automation suppliers and possess grid capacity for energy-hungry robotic lines. As labor demographics worsen, investors increasingly value prefab factories not merely as manufacturing assets but as hedges against a scarce workforce.

CO₂-pricing, timber-quota targets & GEG 2024 favour low-carbon wood modules

Starting in 2024, every new heat source must achieve a 65% renewable mix, and the CO₂ price per metric ton is set to climb steadily, making embodied emissions a cost line in feasibility models. Timber walls store carbon rather than emit it, conferring an immediate accounting benefit over steel or concrete alternatives. Baden-Württemberg’s March 2025 rule updates cement legal certainty by aligning fire-rating thresholds for multi-story timber structures with those of conventional builds. Municipalities rich in forestry assets further nudge adoption through regional quota systems that require a minimum wood share in public projects. Builders specializing in timber modules thus secure a regulatory moat, while those anchored in mineral-based materials must rush to develop low-carbon mixes or risk obsolescence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Double-digit cost inflation for prefab inputs since 2022 erodes price edge | -1.4% | Nationwide—sharper where imports dominate | Short term (≤ 2 years) |

| Shortfall of certified timber-frame assemblers & crane crews | -0.8% | Rural and mid-tier cities | Medium term (2-4 years) |

| Divergent state building codes (16 Länder LBOs) delay approvals | -0.6% | National, with particular complexity in cross-state projects | Long term (≥ 4 years) |

| "Catalogue-house" image & resale-value doubts curb urban uptake | -0.5% | Urban centers: Berlin, Hamburg, Munich, Frankfurt, Cologne | Long term (≥ 4 years) |

| Tight road-escort rules boost logistics costs for oversized modules | -0.4% | National, with higher impact on rural delivery routes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Double-digit cost inflation for prefab inputs since 2022 erodes price edge

Timber, insulation foam, and structural steel rose more than 10% per year from 2022 to 2024, squeezing profit margins across the German prefabricated housing market. Factory efficiency cannot fully neutralize such spikes because raw materials account for over half of ex-works cost. Municipal buyers operating under fixed-price frameworks sometimes postpone awards when bids exceed budget ceilings, delaying revenue recognition for manufacturers. The strain is most visible in the affordable segment, where final selling prices hover near upper limits set by social programs. Suppliers respond by forward-buying inventories and adopting digital twins to engineer out material waste, tactics that lessen but do not eliminate upward cost pressure.

Shortfall of certified timber-frame assemblers & crane crews

While robotics covers many shop-floor tasks, final assembly still requires licensed crews capable of precision work and crane signaling. Rural zones often lack such talent, forcing companies to dispatch teams hundreds of miles, inflating logistics budgets, and risking schedule overruns. Certification programs lag behind market growth, producing only a fraction of the specialists required each year. The bottleneck also complicates warranty service, since unfamiliar subcontractors may not adhere strictly to factory guidelines. Some manufacturers invest in mobile training academies and augmented-reality guidance systems that aim to compress learning curves, yet a structural gap remains until vocational programs scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Timber Dominance Faces Concrete Innovation Challenge

Timber secured a commanding 60.35% of the German prefabricated housing market share in 2025, underscoring the material’s long-standing cultural resonance and its regulatory advantages under GEG 2024. Concrete, while holding a smaller base, is on track to post the fastest 6.28% CAGR through 2031, buoyed by 3D-printing breakthroughs that slash labor hours and emit fewer greenhouse gases than conventional mixes. Timber’s leadership rests on established saw-mill networks, predictable moisture behavior, and end-of-life recyclability, all of which dovetail with rising environmental product declarations demanded by lenders. GOLDBECK’s Blue Concrete, formulated to cut embodied carbon by 35%, demonstrates how mineral materials can claw back relevance when sustainability metrics tighten.

In this competitive landscape, the German prefabricated housing market size for concrete modules could exceed USD 2.46 billion by 2031 if its current momentum holds. Wood remains entrenched because Baden-Württemberg, Bavaria, and Thuringia continue to subsidize timber innovation clusters, translating policy into factory orders. Yet hybrid systems combining engineered wood beams with printed concrete cores are emerging to meet greater fire-rating demands in multi-story projects. Manufacturers that develop flexible lines able to pivot between pure timber, pure concrete, and hybrid bills of materials will insulate themselves from commodity price whiplash while winning specification slots in diverse project briefs.

By Type: Multi-Family Growth Accelerates Urban Density Solutions

Single-family homes commanded 71.20% of the German prefabricated housing market share in 2025, mirroring suburban aspirations and mortgage conditions tailored to detached properties. Multi-family units, however, are forecast to expand at a 6.02% CAGR as land scarcity in inner-city postcodes compels vertical living formats. The German prefabricated housing market size for multi-family blocks is projected to double by 2030, assisted by serial-build contracts that guarantee long production runs. Berlin’s latest 1,500-unit deal with GOLDBECK sets a repeatable blueprint: standardized modules at USD 2,200 per m²—half the price of bespoke masonry—without sacrificing architectural variation.

Shifting demographics also amplify apartment demand; single-person households surpassed 42% nationwide in 2025, according to Destatis. Municipal zoning changes increasingly permit greater plot ratios when builders opt for off-site fabrication that minimizes neighborhood disruption. Meanwhile, single-family producers are diversifying into accessory dwelling units to hedge against slowing greenfield releases. Companies able to straddle both segments through platform-based design libraries stand to stabilize order books and smooth seasonality swings inherent in consumer-driven detached housing.

By Product Type: Modular Systems Challenge Panelised Leadership

Panelised and componentised kits held 47.40% of the German prefabricated housing market share in 2025, reflecting decades-old production infrastructure and the ease of flat-bed trucking across the Autobahn network. Modular homes are on pace for a 6.22% CAGR through 2031, outpacing every other product class. Rapid on-site setting—often completed within one business week—makes volumetric boxes attractive in urban zones where crane time is limited to night shifts. MOD21’s new plant aims for 100,000 m² yearly output, translating into roughly 1,400 city-ready apartments and cementing Germany’s profile as a European modular export hub.

While panels remain popular for bespoke single-family builds that require architectural flexibility, modular solutions increasingly win institutional contracts where speed, cost certainty, and energy-performance guarantees outweigh granular customization. Integration of plug-and-play utility cores means entire bathrooms and mechanical rooms leave the factory 95% complete, reducing call-back risks. Panel suppliers are responding by offering semi-volumetric hybrids—closed panels with pre-installed windows and services—blurring traditional product boundaries. Over the forecast window, share shifts will hinge on hauling regulations, as upcoming EU axle-load standards could alter cost dynamics between flat packs and volumetric stacks.

Geography Analysis

In 2025, Berlin is setting the standard in serial construction mandates, claiming a notable 16.85% share of the German prefabricated housing market. The city streamlines the process by packaging land leases with tender invitations, cutting down bid timelines, and giving suppliers specializing in modular social housing a clear roadmap of upcoming projects. With plenty of brownfield sites available, Berlin ensures efficient logistics by allowing modules to be staged nearby without disrupting traffic. While rising land prices might slow demand for detached homes, multi-family prefab projects are expected to remain strong, backed by city-level subsidies for energy-positive buildings.

Hamburg’s port infrastructure offers unrivaled entry for oversized wall panels and volumetric boxes arriving from Scandinavian yards, reinforcing its steady annual completion target of 10,000 new dwellings. The city’s climate-adaptation blueprint now links building permits to heat-island modeling, indirectly favoring prefab designs that incorporate high-performance envelope systems. Developers citing Hamburg’s Wärmeschutzverordnung scorecard increasingly specify factory-installed triple-glazed units to secure faster sign-off. Meanwhile, Munich illustrates affluent-market dynamics where buyers prioritize build quality and sustainability over sticker price. High land costs push average dwelling footprints downward, boosting demand for innovative stacked-townhouse prefab configurations that maximize utility on constrained parcels.

The Rest of Germany contributes a mosaic of mid-sized cities—Stuttgart, Leipzig, Dresden—each with distinct regulatory quirks arising from the federal Länder structure. Divergent energy-code enforcement compels national manufacturers to maintain adaptable spec sheets, adding back-office complexity but also creating competitive barriers to entry. Leipzig’s new digital cadastral system, live since April 2025, reduces site-plan approval from 12 to 5 weeks for designs uploaded in BIM Level 3 format, a boon for tech-savvy prefab firms. Combined, secondary cities collectively surpass Munich in volume and will account for an expanding share of the German prefabricated housing market as federal highway upgrades cut inter-state transit times, permitting plants to serve multiple growth nodes efficiently.

Competitive Landscape

The prefab housing market in Germany is moderately fragmented. Legacy brands like SchwörerHaus and WeberHaus lean on reputational equity built over four decades, yet their largely panelised portfolios face mounting competition from automation-first newcomers. MOD21 and DENNERT have commissioned robotic saw lines and vision-guided fastening stations capable of continuous three-shift operation, elevating plant utilization rates to 85%—nearly 20 points above the artisanal industry average.

Strategic alliances between equipment builders and housing producers are reshaping the supplier landscape. KUKA partnered with Randek to integrate six-axis robots into turnkey wall-line packages, allowing mid-tier firms to leapfrog labor constraints without incurring full R&D burdens. Meanwhile, GOLDBECK’s Blue Buildings roadmap blends proprietary low-CO₂ concrete with serial volumetric design, positioning the company to win carbon-budget-capped public tenders across Europe. International entrants—particularly Scandinavian timber specialists—use Hamburg as a beachhead, capitalizing on favorable shipping economics and cultural affinity for wood buildings.

Financing profiles are also evolving. Vonovia’s 2025 merger with Deutsche Wohnen creates a landlord controlling more than 500,000 units, granting it negotiating clout in long-run supply contracts and the balance-sheet strength to co-invest in dedicated factory lines. Smaller regional players hedge risk via consortium purchasing groups, pooling order books to secure steel and timber at pre-agreed rates. Across the board, digital twins and cloud-based defect-tracking platforms are becoming table stakes, as warranty transparency increasingly influences consumer choice.

Germany Prefabricated Houses Industry Leaders

SchwörerHaus KG

Hanse Haus GmbH

WeberHaus GmbH & Co.

Bien-Zenker GmbH

DFH Haus Holding AG (Massa / Allkauf)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Stadtwerke München wrapped up a USD 27.5 million prefabricated project in Neuhausen-Nymphenburg that delivers 114 apartments, rooftop solar arrays, and an on-site kindergarten. The build is part of a USD 220 million plan to add 3,000 company-owned homes for staff by 2030, signaling a wider move toward employer-backed housing solutions.

- March 2025: Baden-Württemberg introduced streamlined Technical Building Regulations that cut red tape for factory-built homes and give clear legal status to timber systems, a change expected to speed prefab approvals across Germany’s third-largest state and inspire copy-cat reforms elsewhere.

- February 2025: GOLDBECK won a USD 330 million mandate to supply 1,500 modular social-housing units in Berlin—Germany’s biggest single order for off-site construction—using the firm’s low-carbon “Blue Buildings” platform.

- December 2024: MOD21, a unit of Poland’s ERBUD group, announced a USD 55 million expansion that includes a new German timber-module plant capable of turning out about 2,600 apartments a year, bringing fresh foreign capital and capacity into the market.

Germany Prefabricated Houses Market Report Scope

Prefabricated homes, often referred to as prefab homes, are primarily manufactured in advance off-site, then delivered and assembled on-site. This report covers market insights, such as market dynamics, drivers, restraints, opportunities, technological innovation, its impact, Porter's five forces analysis, and the impact of COVID-19 on the market. In addition, the report provides company profiles to understand the competitive landscape of the market.

Germany's prefabricated housing market is segmented by type (single-family and multi-family). The report offers market size and forecasts in value (USD billion).

By Material Type

| Concrete |

| Glass |

| Metal |

| Timber |

| Other Materials |

By Type

| Single-Family |

| Multi-Family |

By Product Type

| Modular Homes |

| Panelised & Componentised Systems |

| Manufactured Homes |

| Other Prefab Types |

By Key Cities

| Berlin |

| Hamburg |

| Munich |

| Cologne |

| Frankfurt |

| Rest of Germany |

| By Material Type | Concrete |

| Glass | |

| Metal | |

| Timber | |

| Other Materials | |

| By Type | Single-Family |

| Multi-Family | |

| By Product Type | Modular Homes |

| Panelised & Componentised Systems | |

| Manufactured Homes | |

| Other Prefab Types | |

| By Key Cities | Berlin |

| Hamburg | |

| Munich | |

| Cologne | |

| Frankfurt | |

| Rest of Germany |

Key Questions Answered in the Report

How large is the Germany prefabricated housing market in 2026?

The sector is valued at USD 8.08 billion in 2026, with expectations of USD 10.66 billion by 2031 on a 5.72% CAGR trajectory.

Which material dominates German prefab homes today?

Timber holds 60.35% share in 2025, benefiting from GEG 2024 compliance advantages and extensive forestry supply chains.

What is driving the surge in modular construction across German cities?

Serial-construction tenders tied to an 800,000-unit housing gap, faster delivery speeds, and subsidy alignment are propelling modular adoption.

Why is Frankfurt outpacing other cities in growth?

Financial-sector job creation and superior logistics for module transport give Frankfurt a forecast 6.45% CAGR through 2031.

How are manufacturers coping with skilled-labor shortages?

Leading firms are deploying robotics and automated lines that cut factory labor needs by up to 70%, while also funding mobile training for on-site crews.

Do rising material costs threaten prefab’s cost advantage?

Double-digit inflation squeezes margins, but lifecycle savings from energy efficiency and quicker occupancy continue to make prefab competitive, especially in subsidized programs.

Page last updated on: