Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

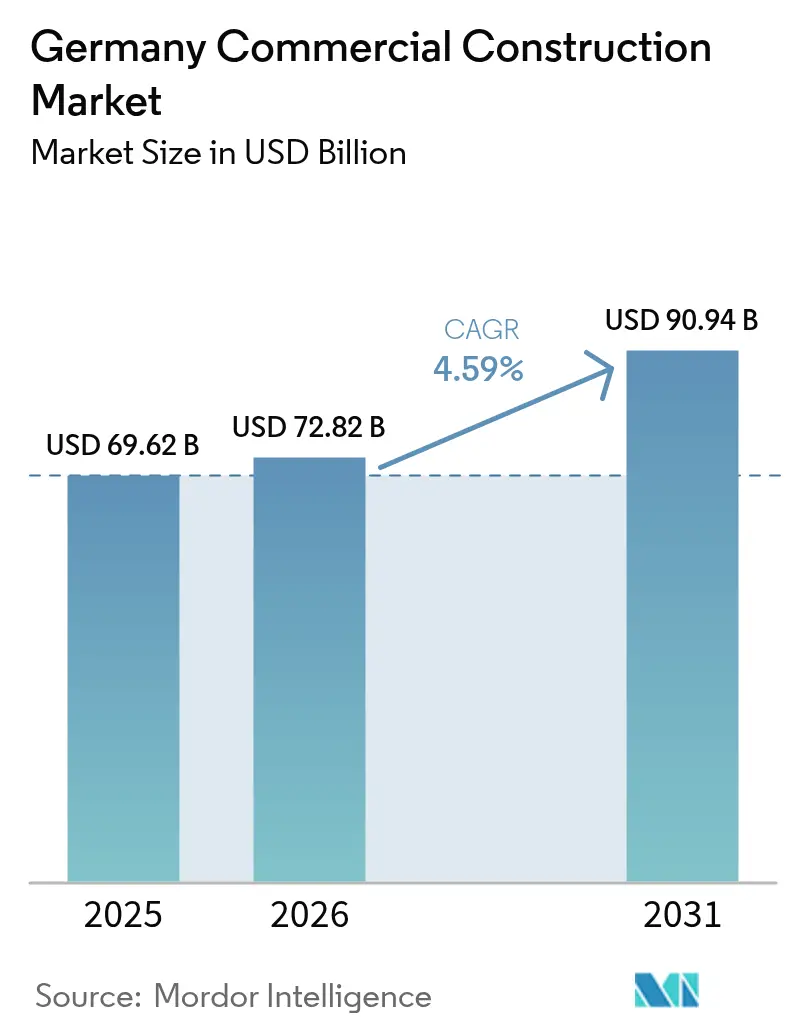

| Base Year Market Size (2025) | USD 69.62 Billion |

| Market Size (2026) | USD 72.82 Billion |

| Market Size (2031) | USD 90.94 Billion |

| Growth Rate (2026 - 2031) | 4.59% CAGR |

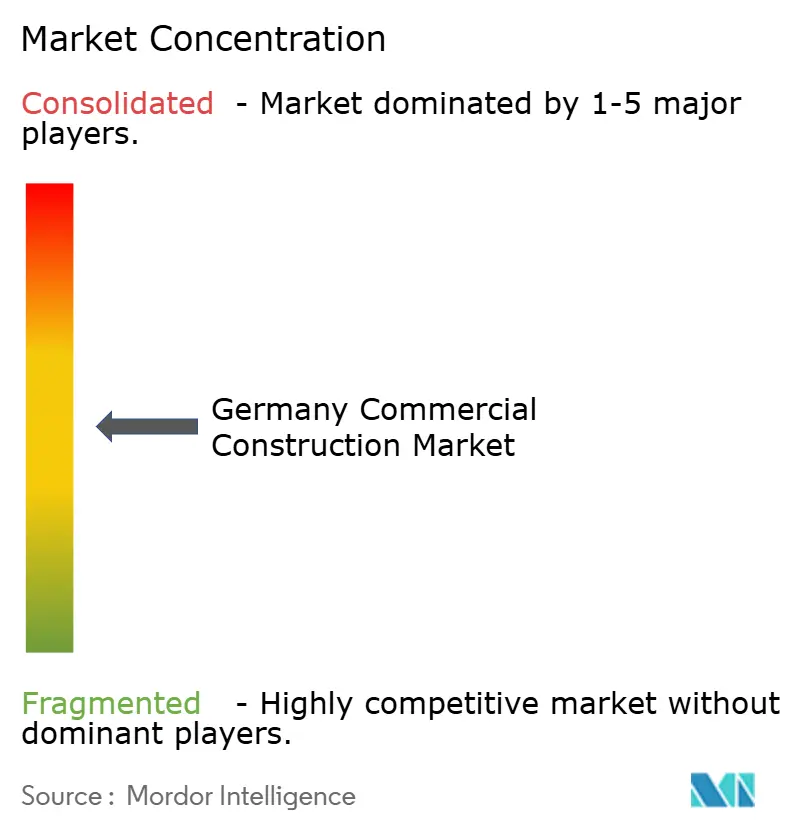

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Commercial Construction Market Analysis by Mordor Intelligence

Germany Commercial Construction Market size in 2026 is estimated at USD 72.82 billion, growing from 2025 value of USD 69.62 billion with 2031 projections showing USD 90.94 billion, growing at 4.59% CAGR over 2026-2031. Rising public spending, led by a USD 550 billion climate and infrastructure fund, anchors the sector’s steady outlook. Private investors remain active in logistics assets, while international technology firms channel fresh capital into hyperscale data-center projects. Legislative incentives for energy-efficient buildings strengthen renovation pipelines, even as volatile material prices and persistent labor shortages weigh on project margins. Strategic shifts toward modular building and digital project controls help large contractors contain costs and improve delivery speed, positioning the Germany commercial construction market for balanced, resilience-driven expansion.

Key Report Takeaways

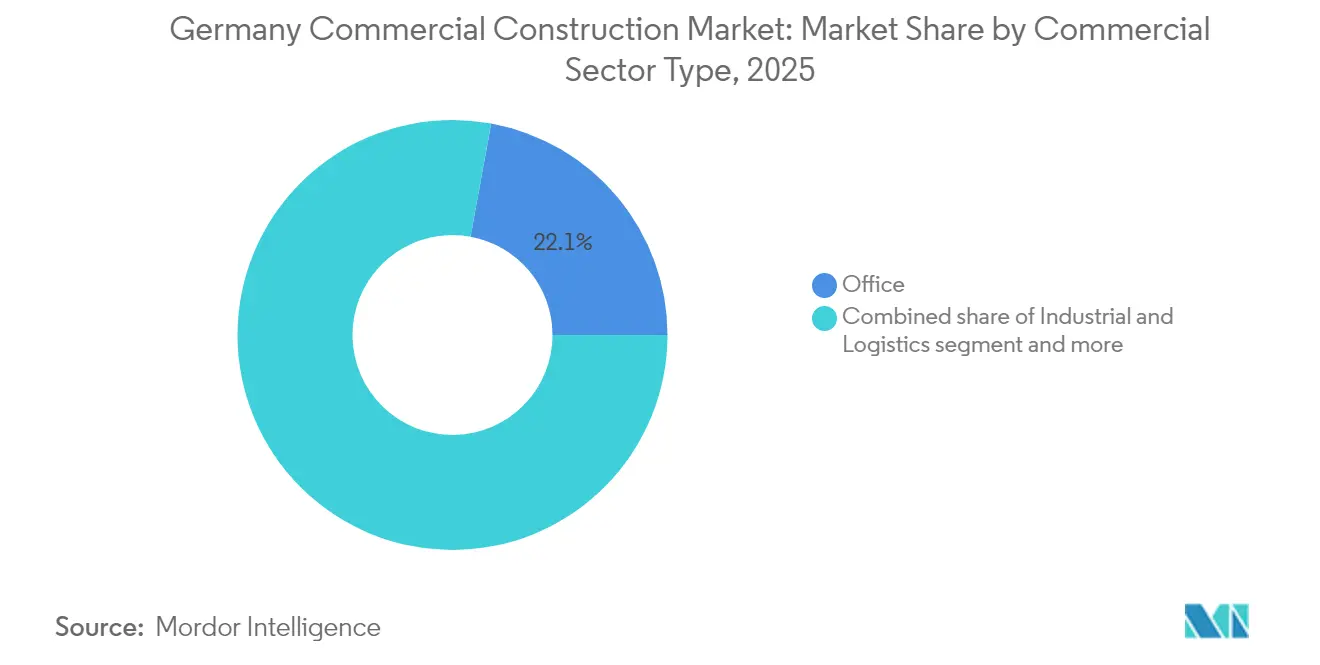

- By commercial sector type, office construction held 22.12% of the Germany commercial construction market share in 2025; industrial and logistics facilities are forecast to expand at a 5.02% CAGR through 2031.

- By construction type, new projects accounted for 71.55% share of the Germany commercial construction market size in 2025 and renovation work is advancing at a 4.78% CAGR to 2031.

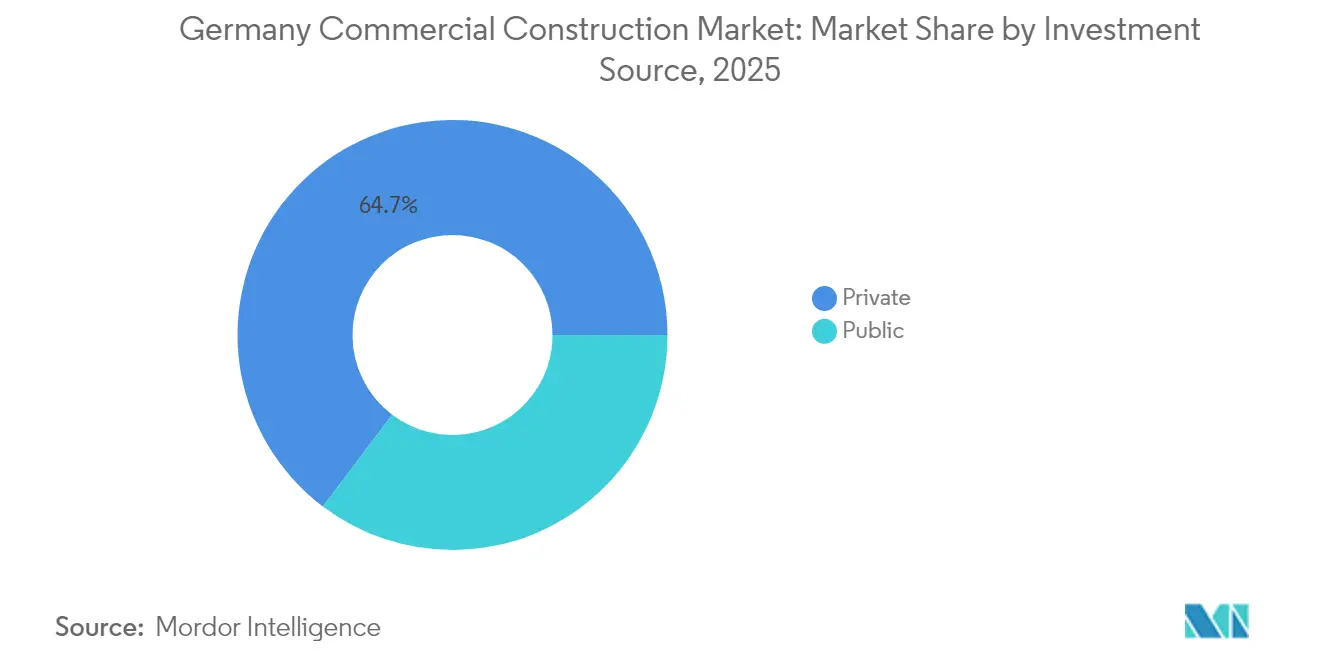

- By investment source, private funding captured 64.70% share of the Germany commercial construction market size in 2025, while public sector outlays are projected to rise at a 5.12% CAGR over the forecast period.

- By city, Berlin led with 23.55% revenue share in 2025; Frankfurt is projected to record a 4.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Commercial Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-efficiency retrofit incentives (BEG & related schemes) | +0.8% | National, urban centers | Medium term (2-4 years) |

| Rapid growth in data-center construction for cloud and AI workloads | +0.7% | Frankfurt, Berlin, Munich corridors | Short term (≤ 2 years) |

| Expansion of last-mile logistics and urban warehousing | +0.6% | Berlin, Hamburg, Frankfurt metros | Short term (≤ 2 years) |

| Increasing institutional capital allocation to German commercial real estate | +0.4% | National, tier-1 cities | Medium term (2-4 years) |

| Industrialised building methods gaining traction | +0.3% | National, early social-housing uptake | Long term (≥ 4 years) |

| Corporate shift to flexible workspace driving adaptive-reuse projects | +0.2% | Berlin, Munich, Hamburg districts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Energy-efficiency retrofit incentives drive market transformation

Germany’s streamlined BEG grant scheme now covers up to 45% of eligible renovation costs, lowering capital hurdles for mid-sized property owners. Contractors with HVAC, façade, and smart-building expertise see fuller backlogs as compliance becomes a tenant-attraction tool in tight urban sub-markets. Building owners prioritize envelope upgrades and heat-pump integration to lock in lower operating costs. The retrofit wave supports a nationwide shift toward net-zero goals and improves the Germany commercial construction market’s earnings visibility. Momentum is expected to persist through 2028, when stricter EU taxonomy rules take effect[1]Bundesamt für Wirtschaft und Ausfuhrkontrolle Staff, “BEG Investment Grant Guidelines 2024,” BAFA, bafa.de.

Rapid growth in data-center construction reshapes infrastructure priorities

Microsoft earmarked USD 3.52 billion for German AI infrastructure, while Amazon committed USD 8.58 billion to its sovereign-cloud region near Berlin. Frankfurt’s power-dense corridor remains the nucleus, yet secondary sites in Berlin and Munich are scaling. Projects demand redundant grids, liquid-cooling, and renewable energy tie-ins to meet the 2027 100% clean-power mandate. Specialized contractors with mission-critical credentials gain a pricing premium, reinforcing the Germany commercial construction market’s pivot toward technology-centric assets.

Expansion of last-mile logistics and urban warehousing fuels new builds

E-commerce penetration above 20% and consumer expectations for same-day delivery push developers toward infill hubs around Berlin and Hamburg. DACHSER’s USD 48.4 million warehouse in Unna illustrates a typical facility that blends rooftop solar arrays with high-bay automation. Demand stability helps offset softer retail-mall pipelines, and the quick-turn profile of logistics buildings smooths cashflows for mid-tier contractors. The segment’s scalability sustains the Germany commercial construction market’s base load of activity over the next two years.

Industrialised building methods gain institutional acceptance

Manufacturers such as Goldbeck deploy factory-finished modules that cut site hours by 70% and trim costs 25%, easing labor-pressure points. Early uptake centers on standardized offices and logistics sheds. Banks now finance modular projects on par with conventional builds, signalling mainstream credibility. Over the long term, wider adoption will moderate schedule risk and improve margins, underpinning steady growth in the Germany commercial construction market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile construction-material prices tied to energy markets | −0.5% | Nationwide, energy-intensive regions | Short term (≤ 2 years) |

| Acute skilled-labour shortage and wage inflation | −0.4% | Nationwide, severe in Bavaria and Baden-Württemberg | Medium term (2-4 years) |

| EU taxonomy carbon-intensity limits raising financing hurdles | −0.3% | Nationwide, large developments | Medium term (2-4 years) |

| Lengthy permitting timelines in smaller municipalities | −0.2% | Rural and secondary cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Construction-material price volatility constrains project economics

Germany’s materials index climbed 3.2% year over year in February 2025 as energy costs remained elevated. Developers struggle to lock in lump-sum contracts, adding contingency allowances that push some projects beyond feasibility thresholds. Roofing and electrical packages show the steepest inflation, prompting substitution toward prefabricated elements where possible. Although hedging strategies soften the blow, persistent volatility pressures the Germany commercial construction market’s near-term margin outlook.

Labor shortage intensifies despite wage increases

Despite April 2025 wage hikes—4.2 % in the west and 5.0 % in the east—covering 930,000 workers, Germany’s commercial construction sector still faces 183,000 unfilled positions. Acute shortages of BIM- and energy-system technicians are delaying critical path tasks, forcing contractors to stagger start dates or walk away from bids to stay within capacity. The market, therefore, cannot accelerate even when demand is strong. Automation and international talent pipelines offer relief, but only over the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Commercial Sector Type: Logistics facilities outpace traditional offices

Office construction held 22.12% of the Germany commercial construction market share in 2025, yet demand is evolving as hybrid work models reduce average floor-space needs and intensify expectations for energy-efficient buildings. At the same time, industrial and logistics facilities are on track for a 5.02% CAGR to 2031, reflecting the surge in e-commerce fulfilment and the re-design of supply chains that now favor last-mile hubs close to consumers. These projects call for automated racking, low-carbon materials, and on-site renewable power, moving the segment well beyond conventional warehouse design. Smaller segments—healthcare, education, and mixed-use schemes—benefit from demographic shifts and public spending but expand at a slower pace than logistics, underscoring Germany’s growing role as a European distribution node.

DACHSER’s USD 48.4 million facility in Unna, equipped for 22,000 pallets and slated to create 290 jobs, shows the scale and complexity that new logistics builds now demand. Photovoltaic roofs and recyclable construction materials are standard specifications, making environmental certification a baseline rather than a premium feature. Retail construction faces structural headwinds as shoppers migrate online, prompting developers to rethink malls as experience-led destinations or repurpose them for alternative commercial uses. Contractors that master smart-building integration and energy-retrofit skills are best positioned to capture the shifting mix of work, keeping the Germany commercial construction market resilient even as traditional office and retail pipelines adjust.

By Construction Type: Renovation gathers speed alongside data-center green-field work

New builds retained 71.55% of total spending in 2025, yet renovation activity posts a brisk 4.78% CAGR to 2031 as owners chase BEG grants. The Germany commercial construction market size for retrofit projects now aligns with regulatory deadlines that require EPC level A by 2033 for many commercial properties. Contractors skilled in envelope insulation, HVAC retrofits, and smart metering enjoy repeat workstreams. Data-center green-field projects remain capital-heavy and technologically demanding, keeping new-build volumes elevated despite carbon-budget scrutiny.

Renovations also support adaptive-reuse plays, especially in city cores where land prices limit green-field feasibility. Investors convert ageing offices into mixed-use blocks that blend co-working, retail, and micro-fulfilment. Circular construction practices reclaim steel and façade elements, lowering scope 3 emissions and reinforcing sustainability credentials within the Germany commercial construction market.

By Investment Source: Public spending accelerates yet private capital dominates

Private funding supplied 64.70% of project value in 2025, maintaining its primacy as the Germany commercial construction market’s main engine. The federal USD 110 billion allocation for climate-centric builds, however, propels public outlays at a forecast 5.12% CAGR to 2031. Public tenders favor low-carbon concrete and lifecycle-cost metrics, nudging contractors toward ESG-aligned supply chains. Large-scale rail upgrades, such as the Munich line, awarded to ACS, drain specialised resources, tightening the supply in smaller projects.

Private investors target logistics and data-center segments where rental escalations and covenant strength support valuations. Sale-and-leaseback deals free corporate capital while securing long-term income for funds. Public-private partnerships surface in social-infrastructure builds, merging government credit with private construction agility, an emerging hallmark of the Germany commercial construction market.

Geography Analysis

Berlin accounted for 23.55% of the Germany commercial construction market in 2025, underpinned by government complexes and a vibrant technology ecosystem. The city’s pipeline increasingly involves adaptive reuse as investors reposition outdated stock into ESG-ready space. Vacancy at 7% suggests supply absorption risk, yet prime rents hold firm because tenants prize efficient buildings.

Frankfurt, although smaller, is on track for a 4.86% CAGR to 2031. Hyperscale data-center clusters leverage the city’s low-latency fiber backbone and robust power grids. Financial institutions refurbish towers to meet strict carbon ceilings, boosting high-value retrofit demand. The Germany commercial construction market responds with a widening cadre of mission-critical contractors that specialise in concurrent engineering and off-site fabrication.

Munich and Hamburg sustain mature, diversified project flows. Munich channels automotive and semiconductor expansions into high-tech labs and clean rooms, while Hamburg’s port logistics drive large sheds with rail inter-modal links. The USD 12.1 billion SuedLink transmission project, crossing multiple regions, injects civil works demand along its route. Smaller cities absorb spill-over as firms search for lower land costs, demonstrating the Germany commercial construction market’s polycentric spread.

Competitive Landscape

The Germany commercial construction market features moderate concentration where two multinational groups, STRABAG SE and HOCHTIEF AG, anchor bidding on complex schemes. STRABAG’s record backlog and 2,643 BIM 5D seats spotlight its digital-delivery edge, while its pledge to reach climate neutrality by 2040 secures eligibility for green public tenders. HOCHTIEF integrates North American affiliates Flatiron and Dragados to access mega-project know-how, reinforcing risk diversification across geographies.

Mid-tier firms such as Goldbeck and BAM Deutschland exploit agility in modular builds and design-build contracts. Goldbeck’s factory network underwrites short lead times that appeal to logistics developers on tight schedules. Regional specialists thrive in façade engineering, smart-building systems, and timber-hybrid structures, areas where incumbents still scale capabilities. The resulting ecosystem keeps pricing competitive yet encourages collaboration when bespoke skills are required.

Strategic moves focus on vertical integration and carbon footprint reduction. Contractors source green cement, lock in long-term power-purchase agreements for renewable electricity, and deploy AI-enabled scheduling software to trim idle time. Joint ventures form around data-center and rail packages that combine civil, MEP, and digital controls. Continuous upskilling in energy-modelling widens service scope, ensuring the Germany commercial construction market adapts to regulatory and client demands.

Germany Commercial Construction Industry Leaders

Strabag SE

HOCHTIEF

Ed. Züblin AG

GOLDBECK GmbH

BAM Deutschland AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Amazon announced a USD 11 billion German expansion, including USD 9.68 billion for AWS facilities near Frankfurt, projected to lift the firm’s local workforce to 40,000.

- May 2025: The German cabinet approved a USD 550 billion climate and infrastructure fund, reserving USD 110 billion for climate-linked construction.

- April 2025: ACS Group subsidiary HOCHTIEF secured a large Munich rail contract valued in the high hundreds of millions of USD.

- March 2025: Baden-Württemberg introduced simplified rules for wood structures and low-carbon cement to cut costs and accelerate approvals.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the German commercial construction market as the value of work put in place for new-builds and major renovations across income-generating premises, office towers, retail centers, hospitality facilities, private healthcare and education buildings, logistics hubs, and mixed-use developments. The spending captured spans design, core shell, interior fit-out, and essential services installations.

Scope Exclusion: public infrastructure and purely residential housing are kept outside this frame.

Segmentation Overview

- By Commercial Sector Type

- Office

- Retail

- Industrial and Logistics

- Others

- By Construction Type

- New Construction

- Renovation

- By Investment Source

- Public

- Private

- By City

- Berlin

- Munich

- Frankfurt

- Hamburg

- Rest of Germany

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed project managers at tier-one general contractors, municipal planning officers in Berlin, Munich, and Hamburg, as well as lenders backing green-building portfolios. These conversations clarified typical cost per square meter, pipeline timing, and vacancy-driven refurb cycles, letting us fine-tune desk-based estimates and cross-check trend inflections.

Desk Research

We first assembled cost and output indicators from open sources such as Destatis construction production indices, Eurostat building-permit dashboards, the German Federal Environment Agency's energy renovation filings, and city-level pipeline trackers maintained by Hauptverband der Deutschen Bauindustrie. Company filings, investor decks, and reputable dailies like Handelsblatt supplemented project-level intelligence. Subscription assets, chiefly D&B Hoovers for contractor financials and Dow Jones Factiva for deal news, helped size private investments. The sources listed here are illustrative; many further publications were referenced while validating inputs and assumptions.

Market-Sizing & Forecasting

We modeled spending by anchoring top-down national construction value-add data to the commercial share implied by building-permit counts and space completions. We then tempered the total with a bottom-up roll-up of sampled project values and contractor billings. Key market fingerprints, office completions measured in square meters, retail footfall-linked fit-out cycles, foreign direct investment into real estate, commercial building energy-retrofit subsidies, and logistics vacancy rates feed a multivariate regression that projects demand through the forecast period. Scenario analysis overlays account for financing costs and carbon-reduction policy shifts. Gaps in bottom-up samples are bridged using average project cost multipliers derived from primary interviews.

Data Validation & Update Cycle

Results pass variance checks against historical series, cost inflation trackers, and peer ratios before a senior analyst signs off. The model refreshes every twelve months, with interim updates triggered by material policy or macro shocks, ensuring clients always receive our latest view.

Why Mordor's Germany Commercial Construction Baseline Commands Reliability

Published figures often diverge because firms mix residential or institutional spend, rely solely on macro outlays, or update less frequently. By isolating revenue-generating premises and blending permit, pipeline, and cost data that we verify directly with market participants, our baseline stays grounded and current.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 69.6 B (2025) | Mordor Intelligence | - |

| USD 108.0 B (2024) | Regional Consultancy A | Includes institutional and industrial assets; macro spend proxies with limited bottom-up checks |

| USD 114.2 B (2025) | Trade Journal B | Converts permit values using broad price indices; minimal stakeholder validation |

The comparison shows how wider scopes and lighter validation inflate numbers. By focusing on clearly defined commercial assets and double-checking every assumption, Mordor Intelligence delivers a balanced, transparent baseline decision-makers can trust.

Key Questions Answered in the Report

What is the current size of the Germany commercial construction market?

The market generated USD 72.82 billion in 2026 and is projected to reach USD 90.94 billion by 2031.

Which commercial sector type leads in market share?

Office construction remains the largest segment, holding 22.12% of sector spending in 2025.

Where is the fastest growth expected geographically?

Frankfurt is forecast to expand at a 4.86% CAGR through 2031, outpacing other major German cities.

What public funding is driving future projects?

A federal climate-and-infrastructure fund worth about USD 550 billion is earmarking at least USD 110 billion for climate-related construction.

How significant are renovation projects versus new builds?

New construction still dominates with 71.55% share, but renovation work is growing at a 4.78% CAGR as owners pursue energy-efficiency upgrades.

Which constraint most threatens near-term growth?

Volatile material prices, already adding 3.2% to building costs year over year, pose the sharpest risk to project margins.

Page last updated on: