Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

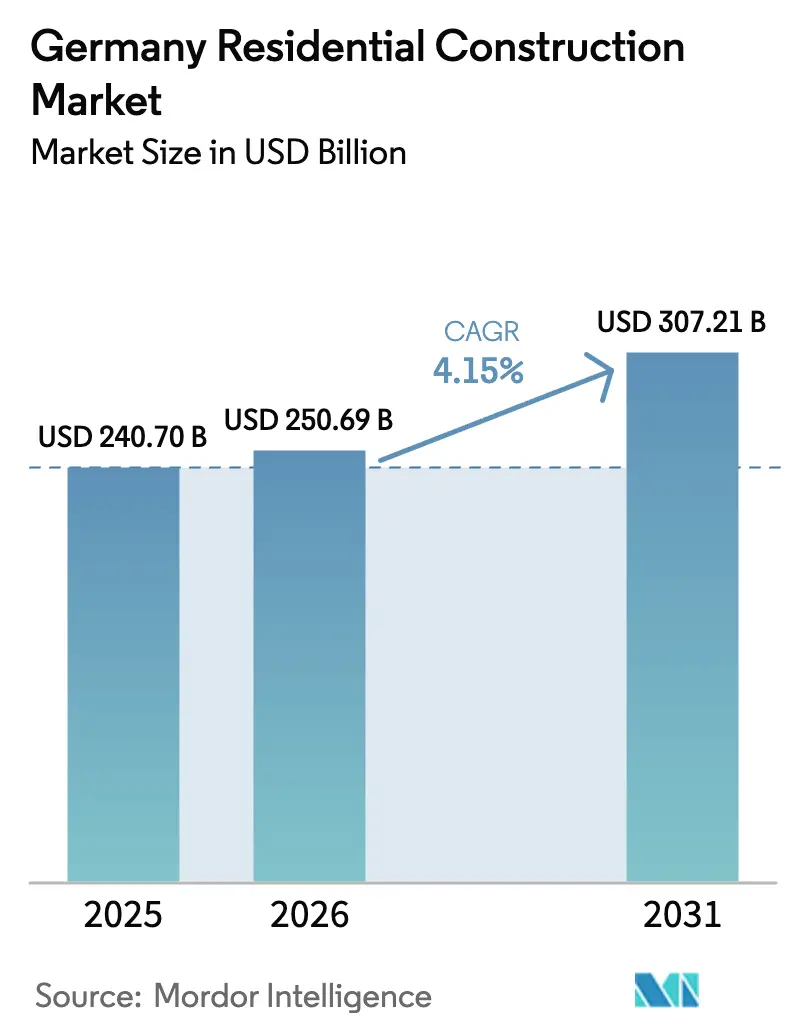

| Base Year Market Size (2025) | USD 240.70 Billion |

| Market Size (2026) | USD 250.69 Billion |

| Market Size (2031) | USD 307.21 Billion |

| Growth Rate (2026 - 2031) | 4.15% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Residential Construction Market Analysis by Mordor Intelligence

The Germany Residential Construction Market size market is expected to grow from USD 240.70 billion in 2025 to USD 250.69 billion in 2026 and is forecast to reach USD 307.21 billion by 2031 at 4.15% CAGR over 2026-2031. Renovation dominates as owners upgrade buildings to meet EU energy rules, while modular construction gains traction as a cost-effective response to labor shortages. Price inflation in construction inputs—3.2% year over year in February 2025—continues to squeeze developer margins[1]Federal Statistical Office, “Construction Price Indices February 2025,” destatis.de. At the same time, robust ESG-linked capital flows and a persistent housing shortfall underpin long-run demand, encouraging large players such as Vonovia to double annual capital spending and target 70,000 new units by 2028.

Key Report Takeaways

- By construction type, new construction captured 44.40% of the Germany residential construction market share in 2025; renovation is projected to expand at a 4.31% CAGR to 2031.

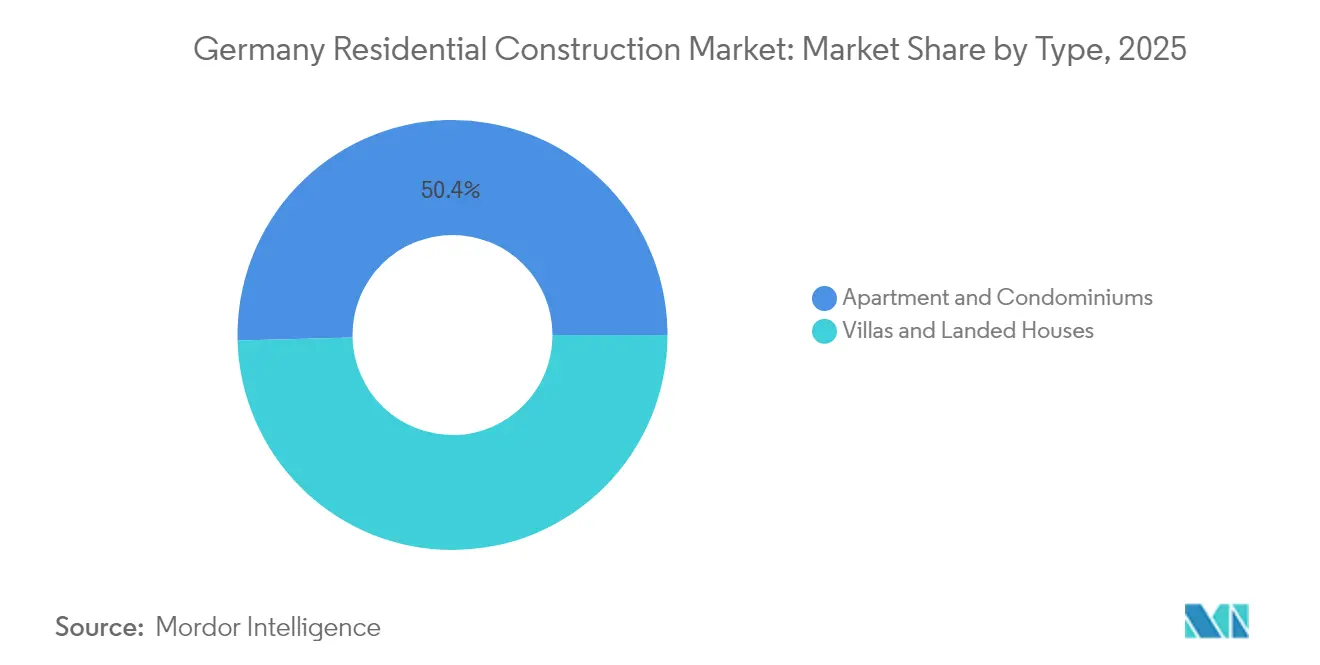

- By residential product, apartments led with 50.40% of the Germany residential construction revenue share in 2025, while villas and landed houses are forecast to post the fastest 4.36% CAGR through 2031.

- By construction method, traditional techniques accounted for 91.30% of the Germany residential construction market value in 2025, whereas modular approaches are advancing at a 4.49% CAGR.

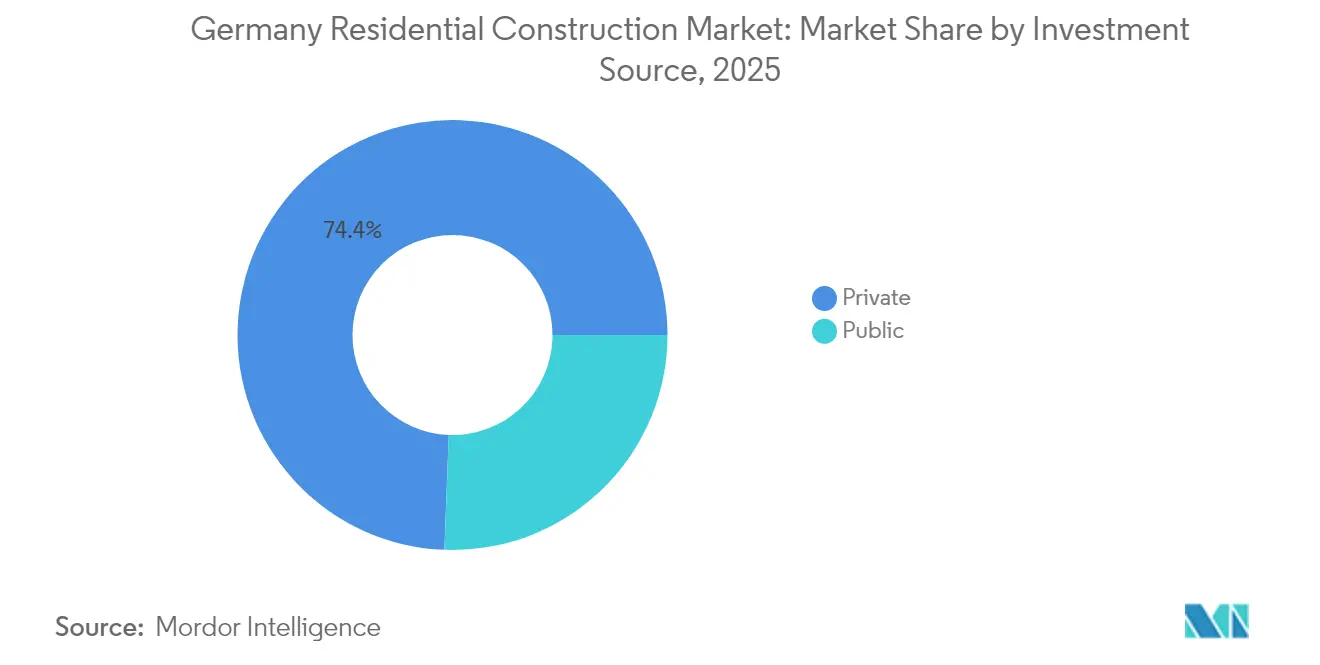

- By investment source, the private segment held 74.40% of Germany residential construction market in 2025 , but public funding is the fastest-growing flow at 5.11% CAGR on the back of social-housing budgets.

- By region, Berlin held a commanding 59.20% of Germany residential construction market share in 2025; Rest of Europe is the growth leader at a 4.54% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Residential Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging housing stock spurring renovation demand | +1.2% | National; strongest in Berlin, Munich, Frankfurt | Long term (≥ 4 years) |

| Government incentives to ease housing shortage | +0.9% | National; metro focus | Medium term (2-4 years) |

| Surge in ESG-linked real-estate funds | +0.7% | National; Berlin, Hamburg, Frankfurt | Medium term (2-4 years) |

| Digitally enabled off-site modular construction | +0.6% | National; early-stage urban rollout | Long term (≥ 4 years) |

| Expansion of Baukindergeld & similar family-housing subsidies | +0.5% | National, targeted at first-time buyers | Short term (≤ 2 years) |

| Growing issuance of green covered bonds for residential projects | +0.4% | National, concentrated in major financial centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging housing stock spurring renovation demand

Roughly two-thirds of German dwellings were built before 1980, and owners now face tightening EU energy-performance thresholds. That legacy has tilted activity toward upgrades, with the Germany residential construction market increasingly driven by insulation, heat-pump installation, and smart-meter retrofits[2]Kiel Institute, “Energy-Efficiency Retrofit Payoff in German Housing,” kielinstitute.org. Renovated units command rent premiums—illustrated by Berlin’s 14% jump in new-build asking rents from 2022 to 2023, a gap that renovated stock can capture. The pressure is national but most acute in large cities where buildable land is scarce, reinforcing renovation’s centrality to volume and value growth.

Government incentives to ease housing shortage

Federal policy has shifted decisively toward direct financial support, lifting social-housing allocations to more than EUR 20 billion (USD 22.07 billion) by 2028 and offering 5% first-year depreciation on new starts launched between October 2023 and September 2029. KfW’s climate-friendly construction credit line disbursed EUR 762 million (USD 840.97 million) in low-interest loans during 2024, supporting over 83,000 units since March 2023. State programs such as Bavaria’s income-based subsidy complement the federal push. Although the 400,000-unit annual completion target was missed in 2023, policy momentum signals continuing stimulus for the Germany residential construction market.

Surge in ESG-linked real-estate funds seeking green assets

Capital flows follow regulatory carrots: Berlin Hyp’s EUR 500 million (USD 551.82 million) Green Mortgage Pfandbrief was 6 times oversubscribed, with nearly one-third of orders placed by dedicated environmental investors. Deutsche Bank, backed by an EIB mezzanine guarantee, offered EUR 600 million (USD 662.18 million) of mortgages with 0.2 percentage-point discounts to energy-efficient borrowers[3]European Investment Bank, “EIB Guarantees Deutsche Bank Green Housing Loans,” eib.org. Preferential financing is splitting the market into ‘green premium’ and ‘brown discount’ tiers, encouraging developers to embed high-performance standards in new projects and deep retrofit scopes.

Digitally enabled off-site modular construction adoption

Factory-made housing modules cut build times up to 70% and mitigate a chronic trade-labor gap that drove 2025 wage agreements above 4%. GOLDBECK reports turnkey costs as low as EUR 2,000 per m² (USD 2,207.28 per m²) for standardized multifamily shells, creating a cost buffer against volatile material prices. Wider adoption hinges on code harmonization and bank underwriting standards, yet public procurement rules are beginning to favor modular bids for social-housing tenders, reinforcing its medium-term growth path in the Germany residential construction market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating construction material costs | -1.1% | Nationwide; sharpest in urban sites | Short term (≤ 2 years) |

| Skilled-labor scarcity and wage inflation | -0.8% | Nationwide; Berlin, Munich, Hamburg strongest | Medium term (2-4 years) |

| Strict energy-efficiency norms raising upfront capex | -0.6% | National, stricter enforcement in urban areas | Long term (≥ 4 years) |

| Municipal land-release bottlenecks despite federal push | -0.5% | Concentrated in Berlin, Munich, Frankfurt, Hamburg | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating construction material costs

Input prices climbed 3.2% year over year in February 2025, with roofing and electrical work posting even higher increases. Tight cement and steel supply—both exposed to high energy and CO₂ costs—widens the budget gap for long-duration projects. Developers respond by forward-buying or specifying engineered-wood systems, yet SME builders lack hedging capacity. Elevated materials inflation remains the most immediate drag on the Germany residential construction market.

Skilled-labor scarcity and wage inflation

Germany’s construction workforce shrank by 6% between 2019 and 2024, even as the building plan pipeline expanded. Union wage deals lifted compensation by more than 4% in 2025, outpacing productivity gains. The tight labor pool accelerates prefabrication adoption and heightens competition for electricians and HVAC installers, imposing cost pressures that offset some public-policy tailwinds.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Apartments Drive Volume, Villas Capture Growth

Apartments and condominiums held 50.40% of Germany residential construction market value in 2025, supported by density targets in metro zoning plans. Institutional landlords favour the segment for portfolio scale, and management efficiencies keep operating costs predictable. Demand resilience is mirrored in Vonovia’s 485,000-unit nationwide portfolio, which recorded stable occupancy above 96% in 2024.

Detached villas and landed houses, though smaller in absolute size, are expanding at a 4.36% CAGR to 2031, the highest among dwelling categories. Remote-work acceptance and improving suburban broadband encourage households to trade commute convenience for living space. KfW’s “Jung kauft Alt” loan, offering up to EUR 150,000 (USD 165,546) for families refurbishing older detached homes, supports this shift. Builders are capturing higher per-unit margins in this segment, helping offset material and wage inflation.

By Construction Type: Renovation Dominance Reflects Infrastructure Reality

Renovation projects accounted for 55.60% of Germany residential construction market expenditure in 2025 and are set to grow 4.31% annually through 2031. Energy-saving directives under the EU “Fit for 55” package make retrofit subsidies more lucrative than ever. The BEG (Federal Funding for Efficient Buildings) program bankrolls heat-pump upgrades and façade insulation with grants covering up to 20% of eligible costs.

New-build delivery remains vital, yet tight land supplies in city cores, higher financing costs, and lengthy permitting push developers to favour renovating existing stock. For pre-1980 buildings, deep retrofit can run to 60% of new-build cost, but it still avoids land-purchase outlays and can be phased unit-by-unit, smoothing cash-flow risk in the Germany residential construction market.

By Construction Method: Traditional Techniques Face Modular Disruption

Conventional on-site processes still commanded 91.30% of 2025 output, reflecting entrenched supply chains and regulatory design norms. Nevertheless, modern modular and prefabricated methods are scaling at a 4.49% CAGR as developers pursue schedule certainty and labour savings. KLEUSBERG’s hybrid timber-steel modules cut CO₂ emissions while keeping grid-shell spans flexible for tight urban footprints.

Financiers begin to recognise the lower construction-period risk in factory builds, improving loan-to-cost ratios for modular projects. Should code harmonisation continue, modular market penetration could lift Germany residential construction market size for prefabricated systems to high-single-digit share by decade-end.

By Investment Source: Private Capital Leads, Public Funding Accelerates

Private capital financed 74.40% of 2025 project volume, underpinned by pension funds and open-ended Spezialfonds targeting stable rental yields. ESG linkages provide a growing portion of this pool, with green-label buildings commanding lower premium amortisation.

Public funding, boosted by social-housing outlays rising beyond EUR 20 billion by 2028, records the briskest 5.11% CAGR. DKB’s EUR 500 million Social Housing Bond funnels low-cost debt to municipal providers serving over 5 million residents. While procurement timelines slow execution, guaranteed land access and subsidy alignment make public projects structurally counter-cyclical, adding resilience to the Germany residential construction market.

By Region: Berlin Retains Leadership, Rest-of-Germany Gains Pace

Berlin represented 59.20% of Germany residential construction market size in 2025, underpinned by EUR 2.35 billion (USD 2.59 billion) of residential transactions in Q1 2025 alone. Government and international business expansion sustain absorption across income brackets. Median asking rents climbed 14% between 2022 and 2023, reinforcing developer margins.

Secondary cities—Hamburg, Frankfurt, Leipzig, and Dresden—together post a faster 4.54% CAGR through 2031 as improved transport links and lower land prices attract both residents and investors. Hamburg’s HafenCity “Grasbrook” district will deliver 3,000 new apartments with 35% subsidised. These projects signal a broadening geographic opportunity set for the Germany residential construction market.

Geography Analysis

Berlin leads the pack, combining political capital status with deep employer diversity. Transaction volume of USD 2.5 billion in Q1 2025—triple the prior-year level—shows confidence despite elevated financing costs. Large portfolios change hands, exemplified by Vonovia’s disposal of 4,500 units for EUR 700 million, freeing capital for new schemes. Yet strict rent caps and energy mandates lift compliance costs, encouraging scale players over smaller developers.

Munich remains Germany’s most expensive housing market at EUR 8,787 per m² (USD 9,697.68 per m²) in 2024. Land scarcity and rigorous zoning limit supply, yielding low elasticity near 2%. Price appreciation persists, pushing spill-over demand into suburbs, where villa builders tap remote-working households. Social-housing budgets are essential for affordability, but bureaucratic complexity elongates project gestation.

Hamburg and Frankfurt form the growth spine of the Rest-of-Germany segment. HafenCity’s Moringa tower integrates recyclable materials and rooftop gardens, illustrating how sustainability standards diffuse beyond Berlin. Frankfurt’s financial-services strength draws foreign capital into multifamily towers, maintaining vacancy below 3%. Combined, these cities diversify the Germany residential construction market and ease concentration risk.

Competitive Landscape

The Germany residential construction market is moderately concentrated. Vonovia, Deutsche Wohnen, and HOCHTIEF leverage vertical integration from landbanking to asset management, securing cost advantages and underwriting ESG investments at scale. Vonovia intends to double annual capital expenditure to EUR 2 billion (USD 2.20 billion) by 2028, targeting virtually climate-neutral stock by 2045. Deutsche Wohnen pilots heat-pump retrofits across 2,000 units, while HOCHTIEF adds AI-driven project-scheduling tools to quell labour bottlenecks.

Challengers focus on modular efficiency: GOLDBECK’s factory network delivers shell-and-core modules nationwide at EUR 2,000 per m² (USD 2,207.28 per m²), almost 20% below average site-built costs. KUKA’s robotic systems automate wall-panel assembly, enabling 70% cycle-time cuts and reducing reliance on scarce trades.

Strategic partnerships proliferate. STRABAG teams with PropTech start-ups for predictive maintenance solutions, while Berlin Hyp underwrites green construction loans that price 15–25 basis points inside conventional spreads. The ability to combine climate compliance, digital construction, and affordable-housing delivery defines competitive edge across the Germany residential construction market.

Germany Residential Construction Industry Leaders

HOCHTIEF AG

Ed. Züblin AG

GOLDBECK GmbH

Max Bögl Group

Deutsche Wohnen SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Vonovia SE posted a 15.1% rise in adjusted EBITDA to EUR 698.5 million (USD 770.893 million) and confirmed plans to invest EUR 1.2 billion (USD 1.32 billion) in upgrades and new construction during 2025.

- March 2025: Vonovia completed 3,747 units in 2024 and will break ground on around 3,000 more in 2025 while reaffirming its 70,000-unit long-term goal.

- December 2024: Partners Group agreed to acquire Empira Group, adding a EUR 14 billion (USD 15.45 billion) residential development pipeline.

- December 2024: HERO Software secured EUR 40 million (USD 44.14 million) Series B funding to expand its construction SaaS footprint in the DACH region.

Germany Residential Construction Market Report Scope

Residential construction includes construction on single-family or two-family dwellings that are occupied or used or are intended to be occupied or used, primarily for residential purposes.

A complete background analysis of the Germany Residential Construction Market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact, is covered in the report.

The Germany Residential Construction Market is segmented by type (apartments & condominiums, and landed houses & villas), by construction type (new construction and renovation). The report offers market size in value terms in USD for all the above segments.

By Type

| Apartment & Condominiums |

| Villas and Landed Houses |

By Construction Type

| New Construction |

| Renovation |

By Construction Method

| Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc) |

By Investment Source

| Public |

| Private |

By City

| Berlin |

| Munich |

| Frankfurt |

| Hamburg |

| Rest of Germany |

| By Type | Apartment & Condominiums |

| Villas and Landed Houses | |

| By Construction Type | New Construction |

| Renovation | |

| By Construction Method | Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc) | |

| By Investment Source | Public |

| Private | |

| By City | Berlin |

| Munich | |

| Frankfurt | |

| Hamburg | |

| Rest of Germany |

Key Questions Answered in the Report

What is the current size of the Germany residential construction market?

It was valued at USD 250.69 billion in 2026 and is forecast to reach USD 307.21 billion by 2031 at a 4.15% CAGR.

Why does renovation dominate over new builds?

Roughly two-thirds of German homes pre-date 1980, and EU energy rules make upgrading existing stock cheaper and faster than erecting new buildings, giving renovation 55.60% market share in 2025.

How large is Berlin’s share of national residential construction?

Berlin accounted for 59.20% of Germany residential construction market value in 2025, driven by robust transaction volumes and population inflows.

What role does modular construction play?

Modern modular methods are growing at a 4.49% CAGR and can cut build times by up to 70%, but they still represented just 8.70% of activity in 2025.

Which funding source is expanding the fastest?

Public capital—via social-housing budgets and subsidised loan programs—is rising at 5.11% CAGR, outpacing the private segment’s growth.

How are ESG standards affecting project financing?

Green-labeled projects access cheaper debt, exemplified by Berlin Hyp’s oversubscribed green bond and Deutsche Bank’s discounted mortgages, creating a financing premium for sustainable developments.

Page last updated on: