Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

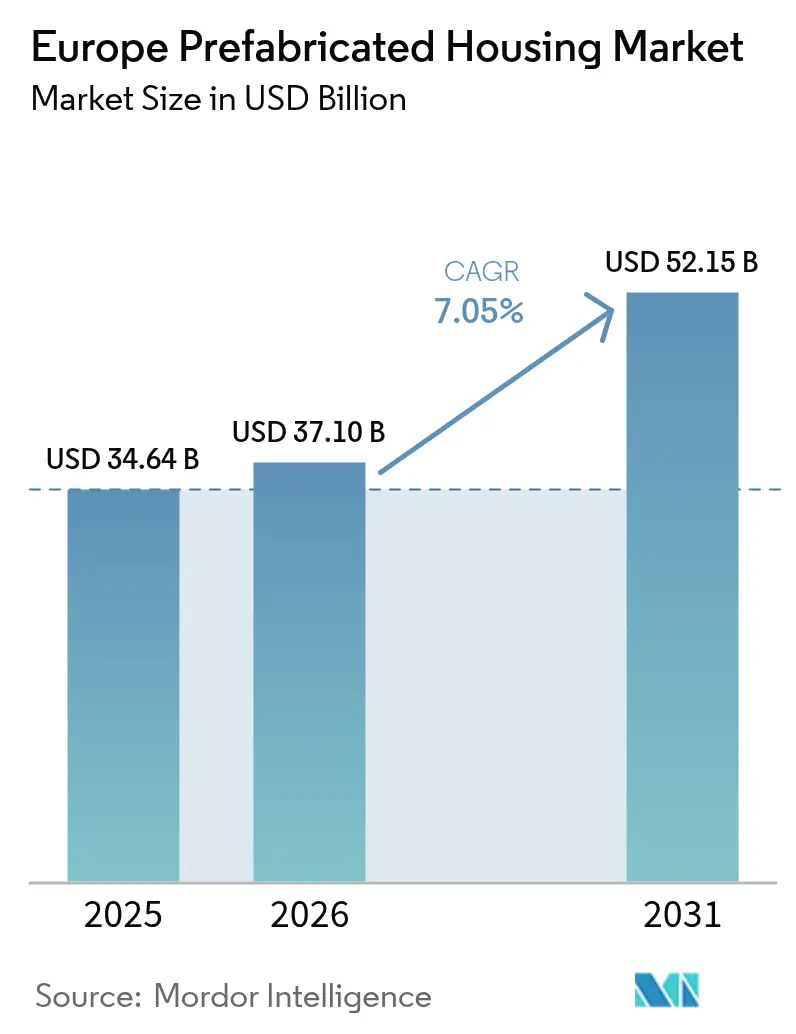

| Base Year Market Size (2025) | USD 34.64 Billion |

| Market Size (2026) | USD 37.10 Billion |

| Market Size (2031) | USD 52.15 Billion |

| Growth Rate (2026 - 2031) | 7.05% CAGR |

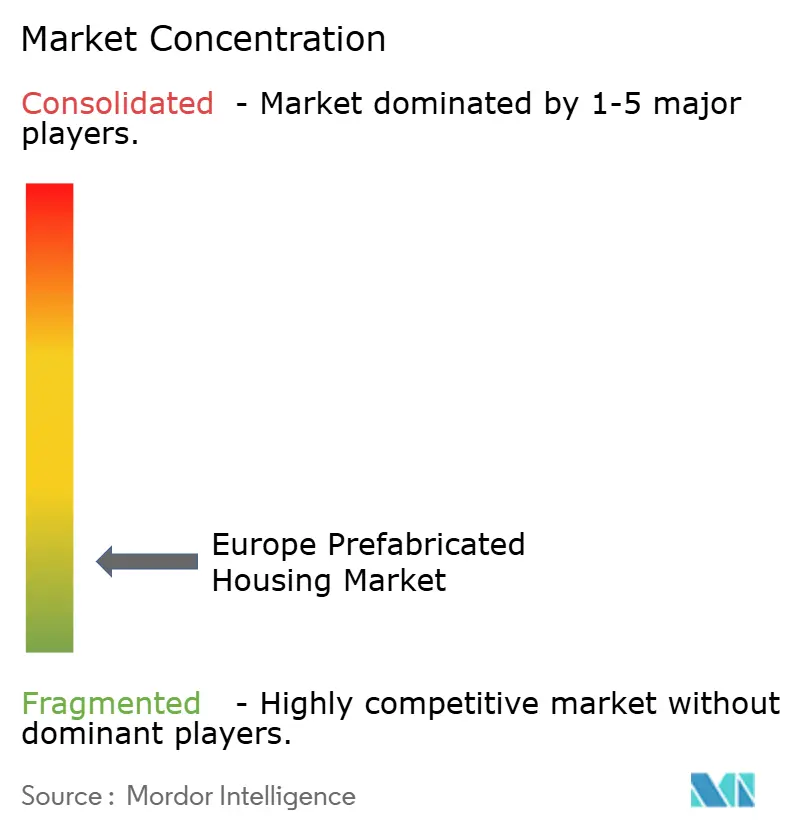

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Prefabricated Housing Market Analysis by Mordor Intelligence

The Europe prefab housing market size is projected to be USD 34.64 billion in 2025, USD 37.10 billion in 2026, and reach USD 52.15 billion by 2031, growing at a CAGR of 7.05% from 2026 to 2031. Robust public-sector programs, deft carbon-accounting rules, and a chronic skilled-labor shortfall are tilting procurement away from cast-in-situ methods toward serial, off-site manufacturing across the continent. Automation levels already surpass 80% in leading German factories, cutting cycle times and stabilizing quality while positioning early adopters to capture share as wage inflation erodes conventional builders’ cost base[1]“Company Overview and Factory Automation,” Gropyus, gropyus.com . Regulatory catalysts such as Germany’s Bau-Turbo law, the EU Renovation Wave, and the forthcoming Carbon Border Adjustment Mechanism strengthen the business case for low-carbon mass-timber modules and volumetric systems. Private-equity interest is accelerating consolidation, while supranational lenders channel capital into affordable-housing pipelines that specify modular procurement.

Key Report Takeaways

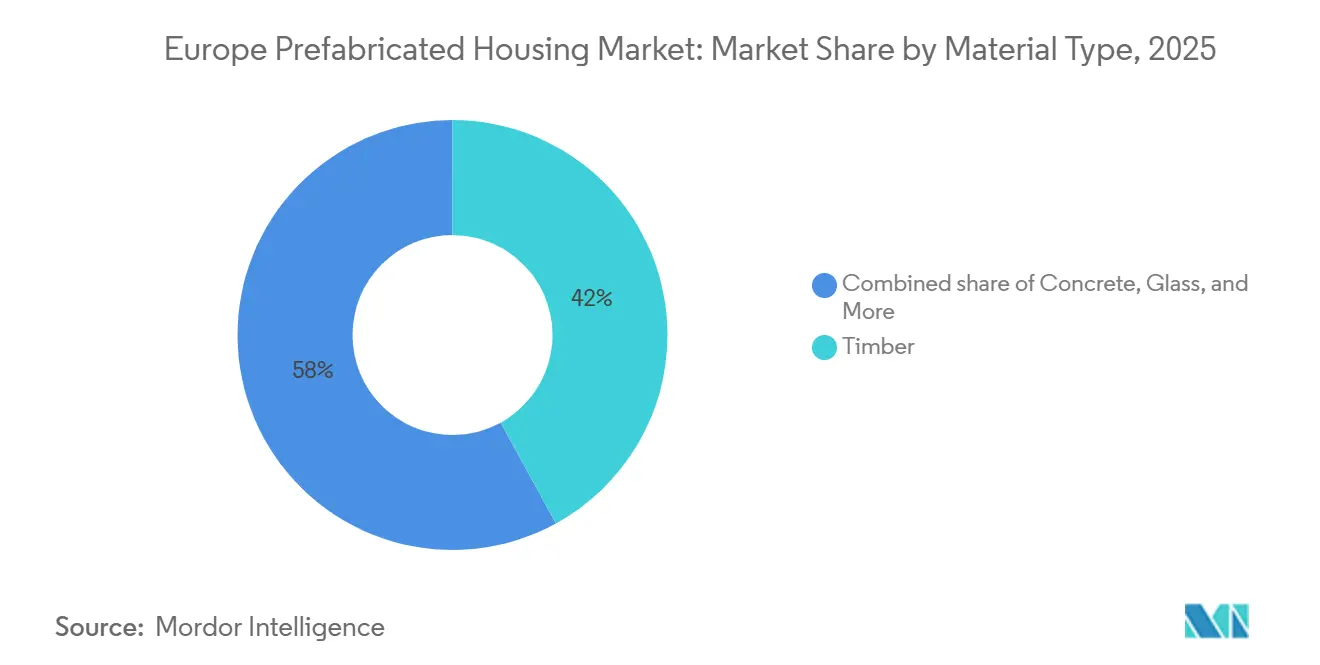

- By material, timber led with 42% of the Europe prefab housing market share in 2025; cross-laminated timber is projected to expand at a 9.40% CAGR to 2031.

- By housing type, single-family units commanded a 61% share of the European prefab housing market size in 2025, while multi-family demand is advancing at an 8.70% CAGR through 2031.

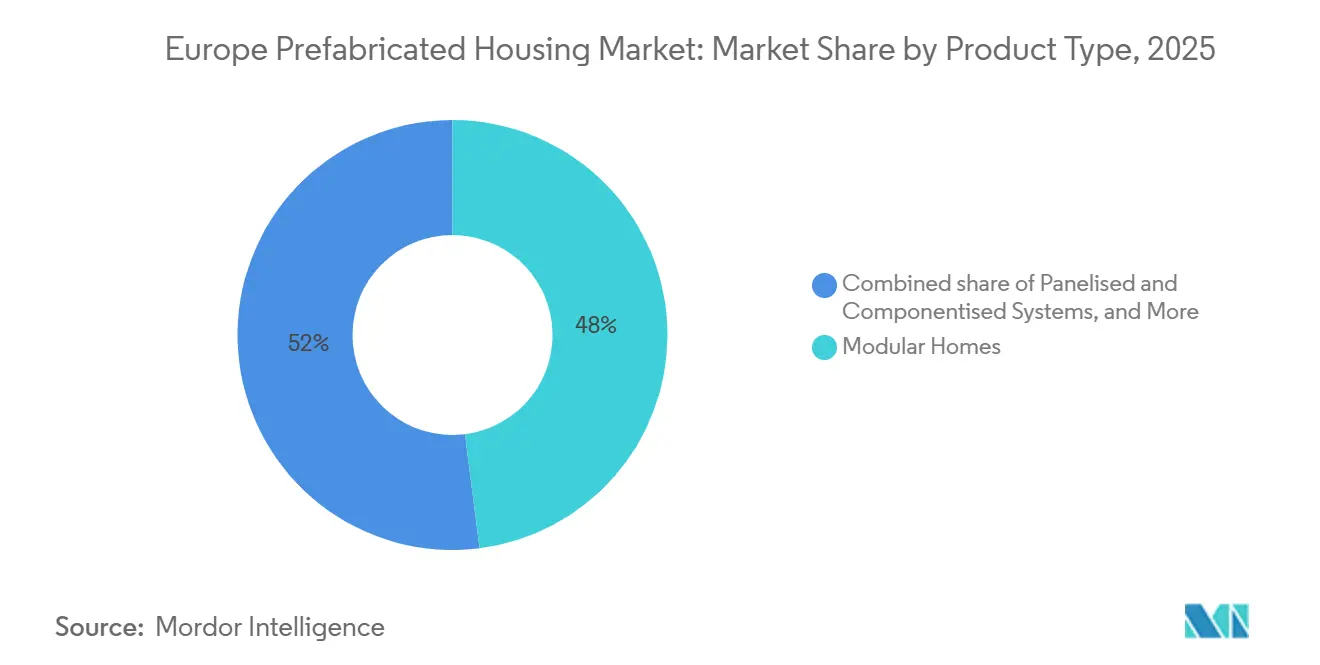

- By product type, modular homes captured 48% of 2025 volume and Panelized & Componentized Systems are set to grow the fastest at 9.90% CAGR as factory automation deepens.

- By geography, Germany contributed 35% revenue in 2025; the Netherlands is the fastest-growing country with a 9.20% CAGR forecast for 2026-2031 on the back of near-instant type-approval frameworks.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Prefabricated Housing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 2.2 million-unit affordable-housing deficit fuels public-private serial-construction programs | +1.5% | Pan-European, acute in Spain, UK, France, Germany | Short term (≤ 2 years) |

| EU Renovation Wave 2030 target accelerates demand for energy-positive prefab retrofits | +1.2% | EU-wide, strongest in Germany, France, Netherlands | Medium term (2-4 years) |

| Advanced robotics & AI-controlled factories counteract 30% skilled-labor gap | +1.0% | Germany, Sweden, Netherlands, Central Europe | Medium term (2-4 years) |

| Carbon Border Adjustment Mechanism credits boost demand for low-carbon mass-timber modules | +0.9% | EU-wide, Nordic & Alpine regions | Long term (≥ 4 years) |

| Insurance-premium discounts for off-site homes spur homeowner adoption | +0.6% | UK, Germany, Netherlands, Nordic markets | Short term (≤ 2 years) |

| NATO rapid-deployment contracts for modular barracks | +0.4% | Poland, Baltics, Romania, Central Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

2.2 Million-Unit Affordable-Housing Deficit Fuels Public-Private Serial-Construction Programs

Governments in Spain, the UK, France, and Germany are pivoting to modular frameworks to close acute housing gaps. Spain’s PERTE funnels EUR 1.3 billion (USD 1.42 billion) over a decade to deliver up to 20,000 industrialized units annually and establish a Construction Industrialization City at Valencia port. The UK’s Guinness Partnership and ilke Homes shipped 51 turnkey houses to Gloucestershire in 2024, showcasing 20% lower operational energy than masonry builds. European Investment Bank loans of USD 1.46 billion underwrite similar pipelines in Portugal and Prague, signaling lender confidence that serial construction can compress delivery time by 60% and cut costs by 25%. Rotterdam, meanwhile, commissioned 2,000 interim modular homes to address migrant inflows, blending bio-based panels with steel frames for speed. Such programs translate policy urgency into bankable long-run order books for prefab manufacturers.

EU Renovation Wave 2030 Target Accelerates Demand for Energy-Positive Prefab Retrofits

The Renovation Wave obliges member states to retrofit 35 million buildings by 2030, doubling the historical pace and generating immediate pull-through for industrialized façades and roof elements that deliver net-zero performance within weeks. Ecoworks and Oikos Group formed a partnership in 2024 to mass-produce such elements, targeting Germany’s 10 million post-war apartments, a potential USD 1.09 trillion retrofit pool (EUR 1 trillion)[2]“ecoworks and Oikos Group Form Strategic Partnership,” Ecoworks, ecoworks.tech. The collaboration blends 2,000 manufacturing employees with cloud-based design software, unlocking serial renovation as a growth adjacency for single-family specialists. Tenants benefit from minimal displacement, while landlords such as Vonovia validate the model by piloting climate-neutral overlays across legacy stock. As carbon budgets tighten toward 2030, retrofit-specific prefab lines secure priority in public tenders and green-finance allocations.

Advanced Robotics & AI-Controlled Factories Counteract 30% Skilled-Labor Gap

Construction labor shortfalls exceed 30% in several EU states, prompting a capital shift toward robotic lines that sustain 24/7 output. Gropyus’s Richen facility deploys 50 robots and 120 tools, achieving 86% automation and 3,500-unit annual capacity. KUKA and Kleusberg will introduce robotic weld cells capable of 2,000 meters per week by 2027, initially for steel-frame schools and offices. ABB and AUAR plan 10 micro-factories that fabricate a home’s core shell in under 12 hours, aligning with decentralized housing programs. Finnish firm ADMARES claims 141 robots across 26 lines, though throughput remains demand-constrained. Automated warehousing from Westfalia enhances just-in-time timber feed, reducing buffer stock and cycle variability. As apprenticeship pipelines thin, robotic capacity becomes a strategic moat for early movers in the Europe prefab housing market.

Carbon Border Adjustment Mechanism Credits Boost Demand for Low-Carbon Mass-Timber Modules

From 2028, CBAM assigns carbon levies to high-emission prefab imports and rewards compliant mass-timber systems. The rule dovetails with EU Taxonomy thresholds that cap primary-metal share at 30% in new buildings. Mayr-Melnhof invested EUR 175 million (USD 190.8 million) in a 140,000 m³ CLT plant to capture the upswing, locking PEFC supply for green-bond eligibility. Setra’s Vision-III-TT CNC line cuts panels up to 20 × 3.1 meters with millimeter precision, shrinking waste and easing volumetric repeatability. Honka’s Fusion+ CLT logs blend log aesthetics with engineered performance for premium buyers. ETH Zurich is advancing heat-resistant adhesives that mitigate char fall-off, a critical hurdle for insurers. Together, these innovations refine a materials pathway that simultaneously meets climate policy and customer preference.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Twin peaks in 2025-26 steel & timber prices erode prefab cost competitiveness | -1.3% | EU-wide, acute in Germany, France, Spain, Italy | Short term (≤ 2 years) |

| Divergent national fire-safety and warranty codes cause 6-12 month approval delays | -0.8% | Pan-European, especially UK, France, Germany, Nordics | Medium term (2-4 years) |

| Heightened insurer scrutiny raises premiums for CLT high-rise projects | -0.5% | Urban hubs: Germany, UK, France, Netherlands, Sweden | Medium term (2-4 years) |

| ESG-taxonomy gaps for hybrid concrete-timber modules restrict green-finance access | -0.4% | EU-wide, larger effect in Germany, France, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Twin Peaks in 2025-26 Steel & Timber Prices Erode Prefab Cost Competitiveness

Raw-material inflation narrowed prefab’s historic 20-25% cost edge over masonry. EUROFER recorded a 1.1% drop in EU steel consumption for 2024 and another 0.2% in 2025, yet energy costs kept prices high and import penetration rose to 27% [3]“EU Steel Market Outlook 2024-2025,” EUROFER, eurofer.eu. Aecom’s Tender Price Index jumped from 145.8 in Q1 2024 to an expected 155.8 by Q1 2026, driven largely by steel frames priced up to GBP 299 per m² . CLT spot levels climbed EUR 60 per m³, pushing the index to 110, while glulam exceeded EUR 600 per m³. Destatis data show prefab-house construction costs rose 0.5% in 2024, compared with 2.9% for conventional builds, indicating the gap is shrinking. Producers either absorb volatility or cede bids, complicating growth trajectories in the Europe prefab housing market.

Divergent National Fire-Safety and Warranty Codes Cause 6-12 Month Approval Delays

Lack of harmonized CLT standards forces manufacturers to navigate a patchwork of national rules, extending permitting cycles. Eurocode 5 revisions are still pending harmonization, leaving insurers and authorities to apply conservative fire and moisture criteria. The Netherlands grants near-instant permits under Van Wijnen’s Kiwa system, but most EU states still require bespoke tests, adding legal fees and design drag. Post-Brexit divergences oblige dual certification for UK projects, inflating compliance overhead. Until convergence, fragmented codes clip speed advantages central to the Europe prefab housing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Timber Dominance Driven by Carbon Accounting

Timber controlled 42% of material inputs in 2025, the largest share within the Europe prefab housing market, underpinned by climate policy and abundant regional forestry. The Europe prefab housing market size assigned to timber products is poised to expand as cross-laminated timber posts a 9.40% CAGR to 2031, outpacing concrete, glass, and metal alternatives. Mayr-Melnhof’s new CLT facility, certified by PEFC, exemplifies capital allocation that captures CBAM credits and green-bond demand. In Bavaria and Baden-Württemberg, where forest cover is dense, prefab shares exceeded 40% of new approvals in 2024, proving culture and resource access sway material choice.

Concrete remains indispensable for foundations and long-span applications, as illustrated by K-Prefab’s 45,000 m² Lund apartment project slated for 2026. Metal frames secure relevance in commercial modular buildings, despite Taxonomy limits on primary metal content. Innovations such as Setra’s large-format CNC systems and ETH Zurich’s fire-resistant adhesives continue to refine timber’s structural envelope, while volatile lumber prices challenge cost models. Yet combined policy, finance, and performance dynamics keep timber on track to widen its footprint in the Europe prefab housing market.

By Housing Type: Multi-Family Acceleration Amid Urbanization

Single-family homes captured 61% of 2025 demand, making them the dominant segment of the European prefab housing market. SchwörerHaus, WeberHaus, Bien-Zenker, and Hanse Haus target this space with customizable energy-positive designs that also qualify for insurance discounts. However, multi-family developments are forecast to grow at an 8.70% CAGR between 2026 and 2031, the fastest among housing types, as municipalities densify urban cores and pursue social-housing quotas.

German approvals for prefab multi-family buildings climbed to 8.2% in 2024, up from 7.0% in 2023, reflecting pilots such as Lindbäcks Bygg’s 55-apartment CLT block in Växjö. Spain’s PERTE and Rotterdam’s 2,000-unit framework further illustrate how policy momentum widens the opportunity pool. As modular factories perfect volumetric repeatability, developers meet strict timeline targets while embedding PV and heat-pump packages that satisfy nearly zero-energy building mandates, reinforcing share gains for multi-family prefab within the Europe prefab housing market.

By Product Type: Volumetric Modules Gain on Automation

Modular homes accounted for 48% of product volume in 2025, the highest within the Europe prefab housing market share. Yet volumetric modules, which ship as fully finished room-scale units, are projected to grow fastest at 9.90% CAGR through 2031. Gropyus’s 86%-automated line finishes a unit within 12 hours, while ABB-AUAR micro-factories replicate the model across 10 upcoming sites.

Panelized and componentized systems hold sway in retrofits and custom single-family builds because they adapt to irregular plots and phased construction. Manufactured homes built to national codes fill the value segment, epitomized by DFH’s five-brand portfolio that now benefits from Capmont’s capital injection. Emerging hybrid systems, exemplified by Peikko and CREE Buildings, aim to blend long spans with low embodied carbon, positioning the Europe prefab housing industry for more architectural flexibility without sacrificing ESG alignment.

Geography Analysis

Germany delivered 35% of regional revenue in 2025, underlining its status as anchor market for the Europe prefab housing market. Bau-Turbo legislation condenses permitting from five years to two months, and private-equity investors demonstrated conviction when Capmont acquired Deutsche Fertighaus Holding in 2025. Bavaria and Baden-Württemberg continue to lead national prefab penetration thanks to timber affinity and streamlined local rules, while federal climate targets spur ecoworks-Oikos retrofit lines that unlock a USD 1.09 trillion opportunity.

The Netherlands records the steepest growth trajectory at 9.20% CAGR for 2026-2031. Van Wijnen’s Kiwa type-approval trims permits to near real-time issuance, enabling developers to compress schedules dramatically. Rotterdam’s bio-based temporary housing program and VDL Groep’s ownership of De Meeuw add supply-side depth. Municipal inconsistency and VAT quirks still hamper rooftop-extension schemes, yet policy ambition outweighs friction, expanding addressable demand in the Europe prefab housing market.

Elsewhere, the UK, Spain, France, and Italy chart varied adoption curves. The UK’s MMC schemes achieve EPC-B as standard, with ilke Homes’ 51-unit Drybrook project validating energy savings. Spain’s PERTE funnels over USD 1.42 billion toward industrialized frameworks and is backed by the Oceanika flex-living CLT complex scheduled for 2025 completion. France’s Bouygues and Eiffage leverage modular arms for suburban student housing, and Italy sees nascent pilots in the north despite a masonry preference. Nordic countries—Sweden, Denmark, Norway—maintain leadership in timber prefab, with Skanska’s BoKlok brand and Lindbäcks Bygg setting benchmarks even as Skanska exits direct manufacturing. Eastern Europe emerges as both supplier and customer: TeraSteel’s new Romania plant adds 1.8 million m² sandwich-panel capacity, linked by rail and port to Ukraine and Turkey. Together, these dynamics paint a mosaic of adoption speeds that feed into the long-run expansion of the Europe prefab housing market.

Competitive Landscape

SchwörerHaus shipped 1,600 houses and USD 542 million (EUR 500 million) revenue in 2024, while WeberHaus operates an experiential center to reinforce brand pull. Diversified conglomerates such as Goldbeck, Skanska, Bouygues, and Eiffage wield multi-country reach; Goldbeck posted USD 4.69 billion (EUR 4.3 billion) turnover in 2024 and now targets commercial modules.

Private-equity funds accelerate consolidation. Capmont’s acquisition of DFH secures five brands under one operational roof, positioning the investor to standardize design libraries and bulk-source materials. BESIX’s stake in Bao Living scales digital materials passports, and Semodu’s planned 40,000 m² Bavarian plant pursues automotive-style throughput via heavy robotics.

Skanska divested its Gullringen factory yet retains the BoKlok brand under a licensing model, decoupling capital-heavy manufacturing from high-margin development. Peikko’s alliance with CREE Buildings broadens hybrid timber-concrete offerings and accesses a licensed contractor network, while Kleusberg widens its defense portfolio on NATO frameworks. Automation deployments at Gropyus, KUKA-Kleusberg, and ABB-AUAR will likely create a two-tier market in which scale and robotics secure margin resilience, forcing smaller traditional assemblers either to consolidate or retreat.

Europe Prefabricated Housing Industry Leaders

SchwörerHaus KG

Hanse Haus GmbH

WeberHaus GmbH & Co.

Bien-Zenker GmbH

ScanHaus Marlow GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Bundesverband Deutscher Fertigbau outlined four prefab trends—open living zones, adaptable layouts, embedded smart-home tech, and timber sustainability—to shape 2026 demand.

- February 2026: TeraSteel inaugurated a EUR 20 million (USD 21.8 million) sandwich-panel factory in Romania, adding 1.8 million m² capacity for export to Central and Eastern Europe.

- October 2025: Spain launched a EUR 1.3 billion (USD 1.42 billion) PERTE for industrialized housing, targeting 20,000 units annually and a prefab R&D hub at Valencia port.

- May 2025: Capmont closed the acquisition of Deutsche Fertighaus Holding, integrating five brands across three plants and 1,500 employees.

Europe Prefabricated Housing Market Report Scope

Prefabrication is the method of construction where components of a building structure are assembled either in a manufacturing or production site, transporting complete or partial assemblies to the site where the structure should be present. This work is carried out in two stages: manufacturing components in a place other than the final location and their erection in position.

The report covers a complete background analysis of the European prefabricated housing market. It includes the economic assessment and contribution of economic sectors, market overview, market size estimation for key segments, emerging market segments, market dynamics, geographical trends, and the impact of the COVID-19 pandemic.

The European prefabricated housing market is segmented by type (single-family and multi-family) and country (Germany, United Kingdom, France, and Rest of Europe). The report offers the European prefabricated housing market size and forecasts in value (USD) for all the above segments.

By Material Type

| Concrete |

| Glass |

| Metal |

| Timber |

| Other Materials |

By Housing Type

| Single-Family |

| Multi-Family |

By Product Type

| Modular Homes |

| Panelized & Componentized Systems |

| Manufactured Homes |

| Other Prefab Types |

By Country

| Germany |

| United Kingdom |

| France |

| Spain |

| Italy |

| Netherlands |

| Sweden |

| Denmark |

| Norway |

| Rest of Europe |

| By Material Type | Concrete |

| Glass | |

| Metal | |

| Timber | |

| Other Materials | |

| By Housing Type | Single-Family |

| Multi-Family | |

| By Product Type | Modular Homes |

| Panelized & Componentized Systems | |

| Manufactured Homes | |

| Other Prefab Types | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Netherlands | |

| Sweden | |

| Denmark | |

| Norway | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe prefab housing market in 2026?

The Europe prefab housing market size stands at USD 37.10 billion in 2026.

What CAGR is forecast for Europe’s prefab housing between 2026 and 2031?

The market is projected to grow at a 7.05% CAGR over 2026-2031.

Which material dominates European prefab construction?

Timber holds the top position with a 42% share in 2025, and cross-laminated timber is the fastest-growing substrate.

Which country is the fastest-growing prefab market in Europe?

The Netherlands leads with a projected 9.20% CAGR from 2026 to 2031 owing to type-approval frameworks that slash permit times.

Why are volumetric modules gaining popularity?

Factory automation enables volumetric units to arrive fully finished, cutting on-site work and supporting defense, healthcare, and social-housing timelines.

Page last updated on: