Garcinia Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 308.67 Million |

| Market Size (2030) | USD 840.85 Million |

| Growth Rate (2025 - 2030) | 9.45% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

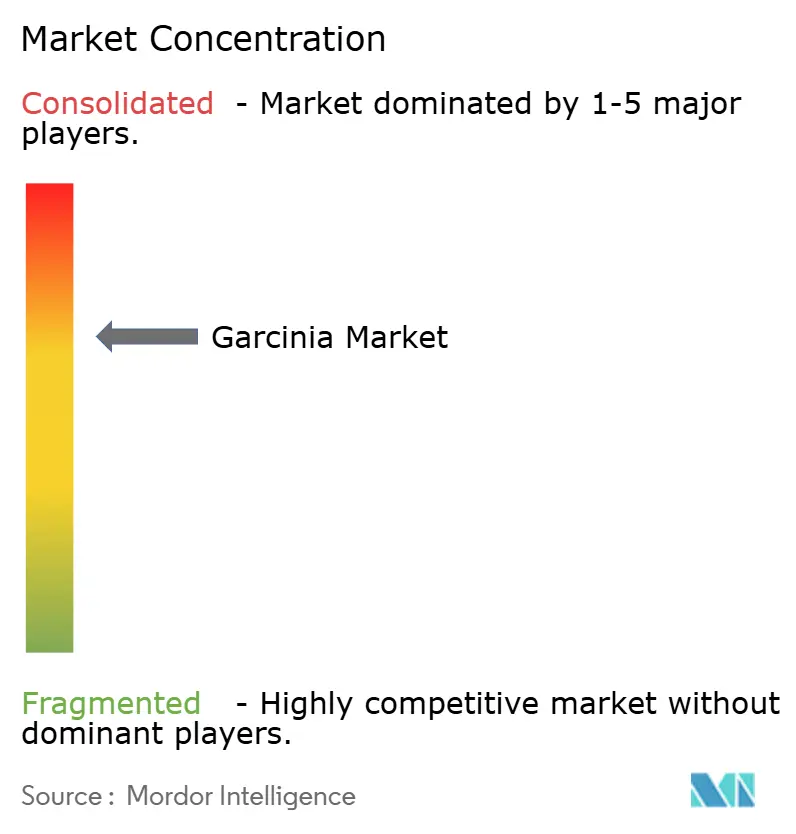

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Garcinia Market Analysis by Mordor Intelligence

The garcinia market size stands at USD 308.67 million in 2025 and is forecast to reach USD 840.85 million by 2030, growing at a 9.45% CAGR. The current expansion is supported by standardized hydroxycitric acid (HCA) benchmarks, rising demand for weight-management solutions, and retailer focus on clean-label botanicals. Formulation advances, such as patented micro-encapsulation, improve bioavailability and enable premium positioning across the garcinia market. Regulatory convergence in North America and Asia-Pacific encourages pharmaceutical-grade manufacturing standards, while supply chain digitization strengthens authenticity verification. At the same time, regulatory alerts on hepatotoxicity and competition from synthetic GLP-1 drugs temper short-term momentum, requiring proactive quality assurance and medical engagement strategies within the garcinia market.

Key Report Takeaways

- By form, powder held 43.23% of the 2024 garcinia market share, liquid formats record the highest projected 10.12% CAGR through 2030.

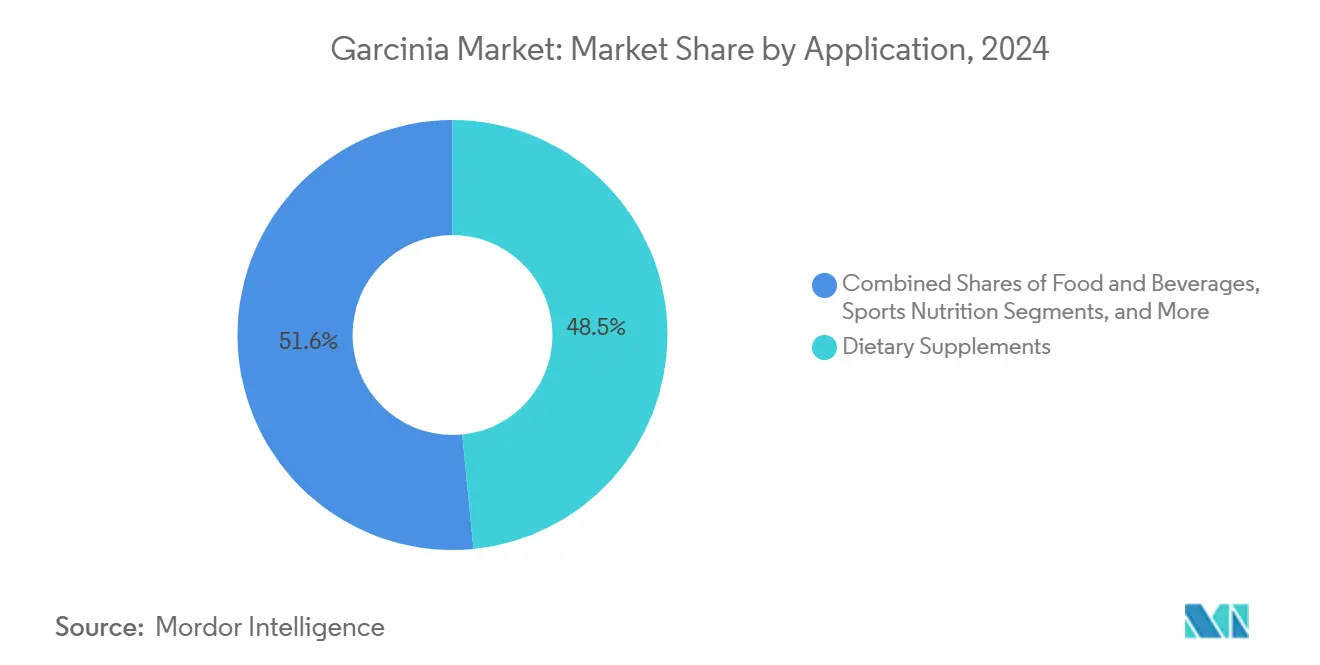

- By application, dietary supplements captured 48.45% of the 2024 garcinia market share, while food and beverage solutions advanced at an 11.12% CAGR.

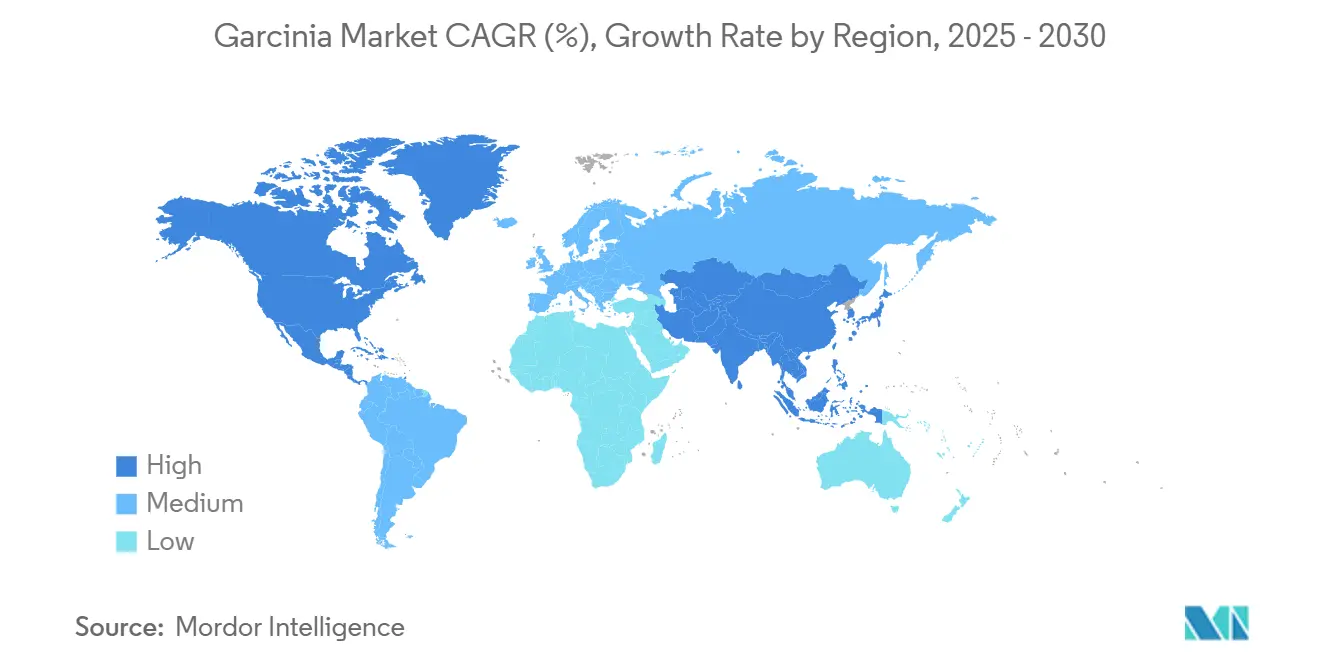

- By geography, North America accounted for 35.67% market share in 2024. Asia-Pacific posts the fastest 11.45% CAGR through 2030.

Global Garcinia Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mainstream popularity of HCA-standardised extracts | +1.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Growing obesity & weight-management supplement uptake | +2.1% | Global, strongest in North America & Asia-Pacific | Long term (≥ 4 years) |

| Retailer push for clean-label botanical ingredients | +1.4% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Pharma-grade purity standards adopted by nutraceutical OEMs | +1.2% | Global, led by developed markets | Long term (≥ 4 years) |

| Patented micro-encapsulation improving bio-availability | +0.9% | North America & Europe | Short term (≤ 2 years) |

| Expanded R&D into non-HCA metabolites such as garcinol & xanthones | +0.7% | Global, concentrated in research hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mainstream Popularity of HCA-Standardised Extracts

Hydroxycitric acid (HCA) content standardization marks a significant shift in the market, rectifying long-standing quality issues in garcinia supplements. Research highlights a troubling inconsistency: HCA concentrations in commercial products vary widely, with some suppliers offering as little as 4.6% and others as much as 55%. By standardizing HCA content, manufacturers can ensure consistent product efficacy and better align with regulatory standards. Thanks to advanced analytical methods, particularly validated UHPLC-PDA techniques, there's now an accurate way to quantify HCA and other bioactive compounds, bolstering quality assurance efforts. This push for pharmaceutical-grade standardization not only enhances product credibility but also offers a competitive edge to suppliers who prioritize robust analytical and quality control measures.

Growing Obesity & Weight-Management Supplement Uptake

Despite mixed clinical evidence surrounding the efficacy of garcinia, the global rise in obesity rates is fueling a growing demand for botanical solutions aimed at weight management. According to the Centers for Disease Control and Prevention data[1]Centers for Disease Control and Prevention, "Adult Obesity Facts", www.cdc.gov from 2024, obesity prevalance in the United States among adults aged 20-29 was 39.8%. Meta-analytical studies indicate that while the effects are modest, they are statistically significant: garcinia supplementation has been shown to reduce serum leptin levels by 5.01 ng/ml when compared to a placebo. This biochemical action lends credence to claims of appetite suppression. Yet, it's worth noting that clinical outcomes related to weight loss have varied across different studies. The market is buoyed by a consumer shift towards natural alternatives, especially among health-conscious individuals who view these botanicals as complementary to their lifestyle changes, rather than as replacements for pharmaceutical solutions. Nonetheless, the rise of potent GLP-1 receptor agonists, which can achieve weight reductions of 15-25%, presents a formidable challenge to the botanical supplement market.

Retailer Push for Clean-Label Botanical Ingredients

Food and beverage manufacturers are prioritizing clean-label formulations, leading to a surge in demand for natural botanical extracts as functional ingredients. This shift mirrors consumer preferences for recognizable, minimally processed components over synthetic additives. Garcinia extracts are capitalizing on this trend, serving as natural flavor enhancers and potential functional ingredients in beverages, confections, and dietary products. The clean-label movement emphasizes the need for transparent sourcing and thorough documentation of extraction processes. This creates challenges for smaller suppliers but offers a competitive edge to established players with strong supply chain management. Retailers are demanding detailed information on ingredient provenance, further driving the adoption of blockchain-based traceability systems and third-party certification programs.

Pharma-Grade Purity Standards Adopted by Nutraceutical OEMs

Regulatory pressures and consumer safety concerns have driven the nutraceutical industry to adopt pharmaceutical-grade manufacturing standards. Compliance with Current Good Manufacturing Practice (cGMP) is becoming a necessity across various jurisdictions. The Consumer Healthcare Products Association has set standardized Certificate of Analysis requirements for components in dietary supplements. These standards address issues like microbial contamination limits, heavy metal testing, and protocols for botanical authentication. Research underscores the importance of contamination control; for instance, studies have found significant bacterial loads in garcinia extracts, which then required tetracycline treatment for microbial reduction. By adhering to these stringent standards, established manufacturers fortify their competitive edge, while simultaneously raising the entry barriers for newcomers to the market.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory alerts on hepatotoxicity cases | -2.3% | Global, most severe in Europe & Australia | Short term (≤ 2 years) |

| Supply chain fraud/HCA content mis-labelling | -1.6% | Global, concentrated in unregulated markets | Medium term (2-4 years) |

| Rising scrutiny of carbon footprint for tropical botanicals | -0.8% | Europe & North America | Long term (≥ 4 years) |

| Competition from synthetic GLP-1 weight-loss drugs | -1.9% | Global, strongest in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Alerts on Hepatotoxicity Cases

Regulatory bodies worldwide are raising alarms over liver injuries linked to garcinia, reshaping the market landscape. In March 2025, France's ANSES released detailed advisories, highlighting 38 severe adverse effects tied to garcinia. These included not only liver complications but also psychiatric and cardiac issues, with one case tragically resulting in death due to acute hepatitis. Echoing these concerns, Australia's Therapeutic Goods Administration[2]Australian Government, "Medicines containing Garcinia gummi-gutta (Garcinia cambogia) or hydroxycitric acid (HCA)", www.tga.gov cautioned about the rare yet grave risks of liver injuries, pointing out instances severe enough to necessitate hospitalization and even liver transplants. Clinical reports, such as those by Ferreira, Victor, et al., have documented several cases of acute hepatitis and autoimmune hepatitis, some progressing to severe liver failure and transplantation after garcinia consumption. Such regulatory interventions pose formidable challenges for the market, hinting at potential product recalls, stringent labeling mandates, and a dip in consumer trust within the botanical supplement industry.

Supply Chain Fraud/HCA Content Mis-Labelling

Widespread adulteration and mislabeling challenge the integrity of the garcinia supply chain. Analytical studies highlight alarming discrepancies: some commercial supplements, despite claims, contain as little as 4.6% HCA. Research in botanical ingredient forensics uncovers sophisticated adulteration tactics, crafted to evade standard detection methods. Evaluations of garcinia-based weight-loss supplements consistently show a gap between experimental and declared HCA values, underscoring the issue of labeling fraud. These integrity challenges underscore the need for advanced analytical methods, third-party verification, and blockchain traceability. However, these solutions come at a cost, heightening operational expenses and diminishing consumer trust in botanical supplements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Powder Dominance Amid Liquid Innovation

In 2024, powder formulations command a dominant 43.23% market share, thanks to cost-effective manufacturing and a robust supply chain. These powders not only boast extended shelf stability and lower shipping costs but also seamlessly fit into various delivery formats, from capsules and tablets to bulk ingredient applications. On the other hand, liquid formulations are on a growth trajectory, expanding at a 10.12% CAGR through 2030. This surge is fueled by their enhanced bioavailability and a growing consumer preference for convenient dosing.

Liquid garcinia extracts, utilizing cutting-edge extraction and micro-encapsulation techniques, are boosting HCA bioavailability and absorption rates. Research underscores that liposomal encapsulation outperforms traditional powder methods in delivering bioactive compounds, bolstering premium market strategies. Furthermore, the liquid segment is branching out, embracing novel delivery systems like sublingual drops, functional beverages, and ready-to-drink options, broadening its appeal beyond conventional supplements. Yet, the intricacies of manufacturing and the need for cold-chain storage pose challenges, simultaneously fortifying the profit margins for seasoned liquid extract producers.

By Application: Supplements Lead While F&B Accelerates

In 2024, dietary supplements dominate the market, holding a 48.45% share, primarily driven by weight management trends and heightened consumer awareness. This segment enjoys the advantage of clear regulatory guidelines and well-established distribution channels, including specialty retailers, pharmacies, and e-commerce platforms. Meanwhile, the food and beverage sector is on a robust growth path, boasting an 11.12% CAGR, fueled by trends favoring clean-label ingredients and innovations in functional foods.

Sports nutrition stands out as a rapidly expanding niche, harnessing garcinia's appetite-suppressing qualities for weight management and cutting phases. In the cosmetics realm, garcinia's antioxidant benefits are being tapped for topical products, though it's worth noting that regulatory standards differ widely by region. While pharmaceutical uses of garcinia are currently limited, there's burgeoning interest, especially with new findings on non-HCA metabolites like garcinol and xanthones, which show promise in cancer and diabetes treatments. This broad diversification across various applications not only mitigates market concentration risks but also paves the way for premium positioning of specialized products.

Geography Analysis

In 2024, North America commands a dominant 35.67% market share, bolstered by FDA dietary supplement guidelines and heightened consumer awareness of garcinia's weight management benefits. The region boasts advanced distribution channels, spanning specialty supplement retailers, pharmacy chains, and direct-to-consumer e-commerce platforms. Yet, following reports of hepatotoxicity, regulatory scrutiny has intensified, potentially reshaping labeling and safety warnings. While the National Center for Complementary and Integrative Health underscores the ambiguous efficacy of garcinia, it also raises alarms about safety, notably liver toxicity. As the North American market matures, there's a noticeable shift towards premium innovations, such as micro-encapsulated delivery systems and standardized HCA content, allowing established players to bolster their profit margins.

Asia-Pacific is set to outpace others, charting an 11.45% CAGR through 2030, driven by bolstering manufacturing capabilities and shifting regulatory landscapes. In 2024, Indonesia rolled out comprehensive BPOM regulations[3]Indonesian Food and Drug Monitoring Agency, "Indonesia Unveils Regulation on Labeling of Health Supplements", www.pom.go.id, mandating standardized labeling for health supplements, including ingredient disclosures and allergen alerts. The region's proximity to garcinia sources, especially in India, Indonesia, and Thailand, not only facilitates cost-effective raw material procurement but also opens doors for vertical integration. Investments are pouring into pharmaceutical-grade manufacturing facilities, aligning with global cGMP standards, paving the way for export market ventures. Yet, navigating the regulatory maze is no small feat, with ASEAN nations showcasing a spectrum of nutraceutical frameworks, from India's food-centric regulations to Japan's specialized health product categories.

Europe grapples with regulatory challenges, especially in light of France's ANSES warning against garcinia, which could sway EU-wide regulatory stances. The European Food Safety Authority is in the midst of assessing garcinia's safety, a move that could have ramifications for compliance with the Novel Foods Regulation and health claim validations. Despite these hurdles, Europe continues to show a robust demand for standardized botanical extracts that meet pharmaceutical-grade purity, reinforcing premium positioning strategies. Meanwhile, South America and the Middle East & Africa, though characterized by nascent regulatory frameworks, are witnessing a surge in consumer awareness about botanical supplements, presenting ripe opportunities for market entrants emphasizing education and quality differentiation.

Competitive Landscape

The garcinia extract market demonstrates moderate concentration at 7 out of 10, indicating established players maintain significant positions while accommodating specialized entrants focused on extraction technology and quality differentiation. Market leaders, including Givaudan (through Naturex acquisition), Sabinsa Corporation, and Indena, leverage vertical integration strategies encompassing raw material sourcing, extraction processing, and finished product manufacturing. Givaudan's 2024 integrated report highlights sustainability commitments, including climate-positive targets before 2050 and responsible sourcing initiatives, reflecting industry trends toward environmental accountability.

Competition intensifies around analytical capabilities and quality assurance protocols, with leading suppliers investing in advanced UHPLC-MS/MS systems for multi-class bioactive constituent analysis and authentication. Strategic differentiation focuses on specialized extraction technologies, standardized HCA content, and novel delivery systems addressing bioavailability limitations. Patent protection around micro-encapsulation methods and phytosome formulations creates competitive moats for innovative manufacturers, though technology complexity requires substantial R&D investments.

White-space opportunities emerge in therapeutic applications beyond weight management, particularly given research advances in garcinol and xanthone compounds for cancer, diabetes, and bone health applications. Emerging disruptors leverage blockchain-based traceability systems and direct-to-consumer distribution models, challenging traditional supply chain structures while addressing authentication concerns that plague the broader botanical supplement industry.

Garcinia Industry Leaders

-

Givaudan SA

-

Sabinsa Corporation

-

Indena S.p.A.

-

OmniActive Health Technologies

-

Nutraceutical International Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Top Pure Natural Garcinia participated as an exhibitor at CPhI China, showcasing their high-quality Garcinia products to a global audience. The company utilized this platform to highlight their advanced extraction technology and the purity of their Garcinia extracts, aiming to expand their international market presence and establish new business partnerships.

- January 2025: Indonesia's BPOM implemented Regulation No. 3 of 2025 amending organizational structure and operational frameworks governing food and drug safety, including herbal supplements like garcinia cambogia, establishing enhanced regulatory oversight for botanical extract market participants

Global Garcinia Market Report Scope

| Powder |

| Liquid |

| Food and Beverages |

| Dietary Supplements |

| Cosmetics and Personal Care |

| Sports Nutrition Products |

| Pharmaceuticals |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Netherlands | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| Form | Powder | |

| Liquid | ||

| Application | Food and Beverages | |

| Dietary Supplements | ||

| Cosmetics and Personal Care | ||

| Sports Nutrition Products | ||

| Pharmaceuticals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Netherlands | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the garcinia market?

The garcinia market size is USD 308.67 million in 2025.

How fast is the garcinia market expected to grow?

The market is projected to rise to USD 840.85 million by 2030 at a 9.45% CAGR.

Which form is growing fastest?

Liquid extracts register the highest 10.12% CAGR through 2030.

Which region offers the strongest growth outlook?

Asia-Pacific is forecast to expand at 11.45% CAGR through 2030.

Page last updated on: