Calcium Gluconate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 111.26 Billion |

| Market Size (2031) | USD 142.16 Billion |

| Growth Rate (2026 - 2031) | 5.02% CAGR |

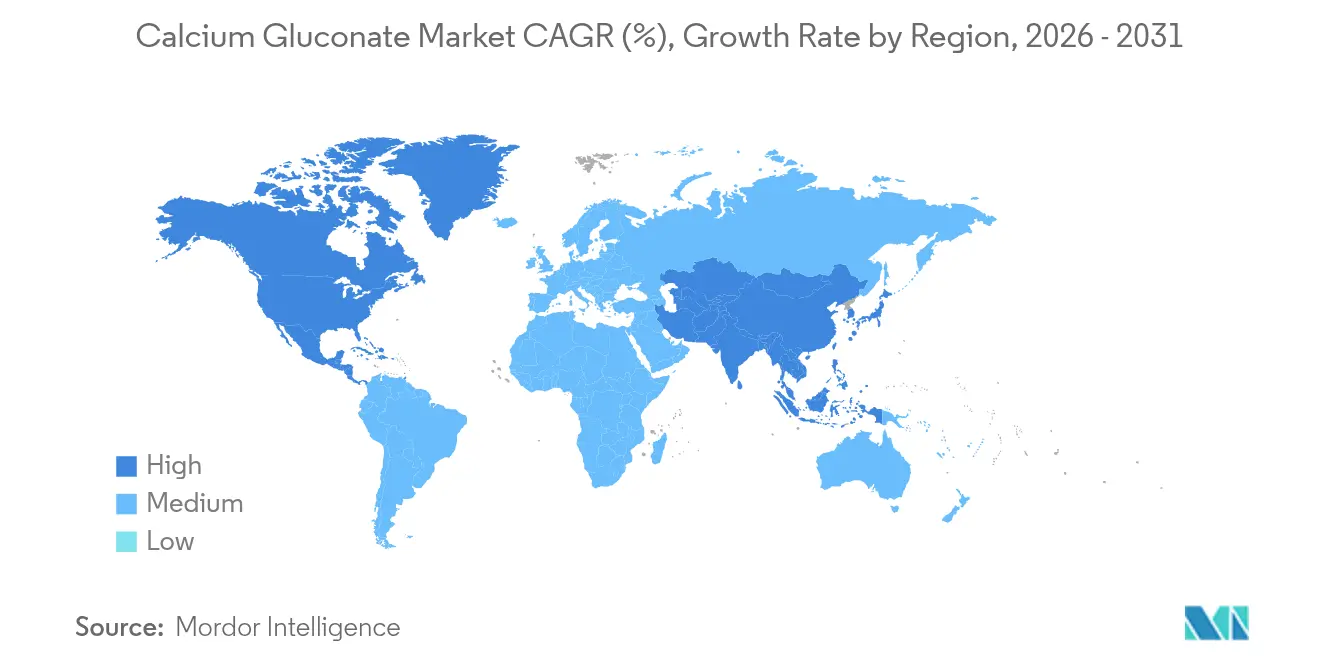

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Calcium Gluconate Market Analysis by Mordor Intelligence

The calcium gluconate market size is expected to grow from USD 105.94 billion in 2025 to USD 111.26 billion in 2026 and is forecast to reach USD 142.16 billion by 2031 at 5.02% CAGR over 2026-2031. The pharmaceutical sector drives this growth, as calcium gluconate provides superior bioavailability compared to other calcium salts, making it essential for intravenous treatment of hypocalcemia in both human and veterinary medicine. The market expansion is supported by developments in personal care delivery systems, increased demand for clean-label food fortification, and government nutrition initiatives. The Asia-Pacific region dominates consumption patterns due to widespread dietary calcium deficiency, while North America experiences the highest growth rate, driven by strong fortification policies and an aging population seeking easily absorbable calcium supplements. Market stability is maintained by vertically integrated manufacturers who control the entire production process from gluconic acid fermentation to final dosage formulation, reducing raw material supply risks. However, increasing production costs, the emergence of alternative chelates, and strict regulations for injectable products moderate the market's growth potential.

Key Report Takeaways

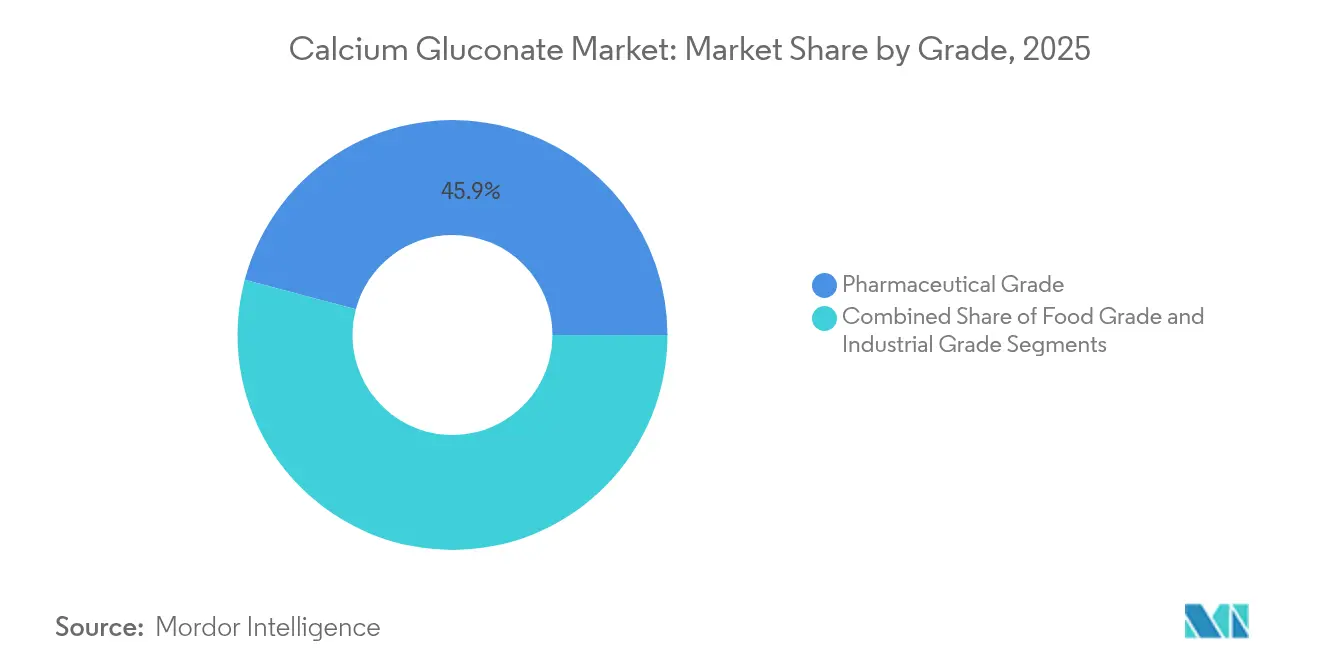

- By grade, pharmaceutical-grade products held 45.86% of the calcium gluconate market share in 2025 and are forecast to post a 6.05% CAGR by 2031.

- By form, powder variants captured 55.62% of the calcium gluconate market size in 2025, whereas liquid solutions are projected to expand at 6.63% through 2031.

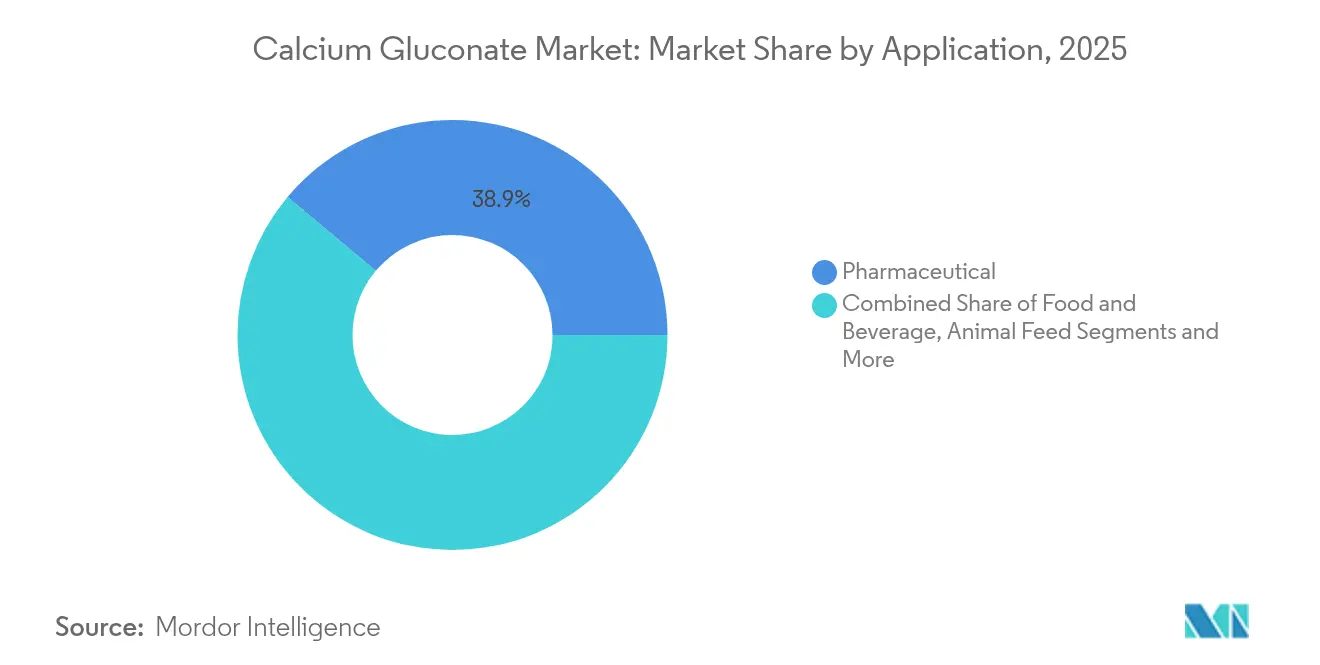

- By application, personal care is the fastest-growing segment at 6.32% CAGR, while pharmaceutical uses remained the largest revenue contributor in 2025 with 38.92% revenue share.

- By geography, Asia-Pacific commanded 33.05% of 2025 revenue; North America is set to grow at 6.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Calcium Gluconate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Calcium Deficiency Disorders | +1.2% | Global, concentrated in Asia-Pacific and developing regions | Medium term (2-4 years) |

| Growing Geriatric Population Worldwide | +0.9% | North America & Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Expanding Nutraceutical and Dietary Supplement Markets | +0.8% | Global, led by North America and Europe | Medium term (2-4 years) |

| Government Nutrition Initiatives and Fortification Policies | +0.7% | Global, with emphasis on developing countries | Long term (≥ 4 years) |

| Surging Demand in Veterinary Medicine | +0.5% | Global, concentrated in agricultural regions | Short term (≤ 2 years) |

| Increasing Adoption in Food and Beverage Fortification | +0.4% | North America, Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Calcium Deficiency Disorders

Calcium deficiency contributes significantly to disability-adjusted life years and cardiovascular risks globally, particularly in regions with low socioeconomic status. Healthcare facilities extensively use injectable calcium gluconate to treat severe hypocalcemia and hyperkalemia, as it enables immediate ionic calcium absorption without requiring gastric acid, unlike carbonate forms. Medical practitioners increasingly recognize calcium's fundamental role in managing hypertension, which drives substantial growth in both prescription and over-the-counter demand. The calcium gluconate market continues to expand as preventive healthcare intensifies its focus on addressing micronutrient deficiencies, supported by the compound's well-established clinical efficacy and comprehensive safety profile. Widespread telehealth platforms improve supplement accessibility, while comprehensive Asian community screening programs increase awareness about calcium deficiency among populations. Systematic public health initiatives, including educational campaigns and nutritional supplementation programs, continue to support the substantial expansion of the calcium gluconate market across developed and developing regions.

Growing Geriatric Population Worldwide

The aging population drives the increasing demand for bioavailable calcium across global markets, particularly in developed regions with significant elderly populations. According to Eurostat data, in 2024, individuals aged ≥ 65 years comprised 24% of Italy's population and 21.6% of the European Union average, highlighting a demographic shift toward an older population requiring enhanced calcium supplementation.[1]Source: Eurostat, "Population structure and ageing", ec.europa.eu Physicians prefer calcium gluconate for postmenopausal women requiring higher calcium intake, as it causes fewer gastrointestinal side effects compared to calcium carbonate, making it suitable for long-term use. The FDA, in January 2024, issued a boxed warning about denosumab-induced hypocalcemia has emphasizing the need for calcium supplementation, administered as intravenous calcium gluconate in clinical settings, particularly in hospitals and specialized care facilities.[2]Source: Food and Drug Administration, "Prolia (denosumab): Drug Safety Communication - FDA Adds Boxed Warning for Increased Risk of Severe Hypocalcemia in Patients with Advanced Chronic Kidney Disease", fda.gov In the United States, geriatric home-health programs use liquid calcium gluconate in pre-filled syringes for rapid correction, contributing to market demand and improving patient care outcomes. The trend of increased life expectancy also drives the growth of orthopedic procedures using calcium gluconate-infused bone cements, expanding consumption across healthcare facilities and contributing to market growth in primary and specialized care settings.

Expanding Nutraceutical and Dietary Supplement Markets

Calcium gluconate maintains a strong market presence due to research validating its bioavailability and safety profile. The market experiences growth in chewable dairy-based supplements, reflecting consumer demand for convenient consumption formats. Research demonstrates higher absorption rates and fewer side effects compared to conventional calcium supplements, increasing its appeal to both manufacturers and consumers. In June 2024, Seen Nutrition launched dairy-sourced calcium chews as an alternative to traditional supplements. These products minimize gastrointestinal issues typically linked to synthetic calcium supplements while providing better absorption through improved formulations. The format meets the needs of health-conscious consumers seeking nutrition in accessible forms. The market expands as consumers understand calcium's wider health benefits, including its importance in muscle function and cardiovascular health. Studies show that calcium supplementation helps reduce osteoporosis risk and maintains bone density during aging. Current regulations support health claims for calcium-fortified products, creating new opportunities in functional foods and beverages. The trend toward personalized nutrition drives demand for bioavailable calcium forms like gluconate, particularly among individuals with digestive sensitivities. This aligns with consumers' preventive approach to meeting nutritional requirements. Additionally, advances in formulation technology enable improved taste profiles and stability across various product applications.

Government Nutrition Initiatives and Fortification Policies

Government regulations on mandatory food fortification address widespread micronutrient deficiencies across population segments. The FDA mandates comprehensive calcium fortification requirements in soy beverages and dairy alternatives, generating substantial and consistent demand for food-grade calcium gluconate in the food processing industry. The United Kingdom's mandatory wheat flour fortification program creates steady and significant demand from bakery manufacturers and processors nationwide. These extensive regulatory requirements reduce market volatility and enable comprehensive long-term supply agreements, stabilizing manufacturer margins throughout the supply chain network. In developing economies, Kenya is implementing extensive fortification programs in school meals to improve bone health among adolescents. In October 2024, the Ministry of Education launched Kenya's National School Meals Coalition and released a detailed Operational Plan to expand the School Meals Programme (SMP) to universal coverage.[3]Source: The Rockefeller Foundation, "Ministry of Education Launches National School Meals Coalition, the Kenya Chapter", rockefellerfoundation.org The well-established nature of fortification regulations, combined with growing public health awareness and nutritional requirements, drives continuous and sustainable growth in the calcium gluconate market across multiple food industry segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Production and Purification Costs | -0.8% | Global, particularly affecting smaller manufacturers | Short term (≤ 2 years) |

| Competition from Alternative Calcium Supplements | -0.6% | North America & Europe, expanding globally | Medium term (2-4 years) |

| Regulatory Hurdles for Injectable Formulations | -0.4% | Global, with varying regional requirements | Long term (≥ 4 years) |

| Limited Consumer Awareness in Emerging Markets | -0.3% | Asia-Pacific, South America, Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Production and Purification Costs

The production of calcium gluconate involves complex fermentation processes and extensive purification steps to meet pharmaceutical-grade standards. The manufacturing process includes D-glucose oxidation to gluconic acid, neutralization with calcium sources, and subsequent crystallization and purification. These steps require significant energy consumption, advanced processing equipment, and specialized technical expertise, creating substantial entry barriers for new manufacturers while requiring established producers to maintain scale efficiencies. The costs of raw materials, particularly glucose and calcium sources, vary with agricultural commodity prices, affecting production economics and overall profitability. The requirement for GMP-certified facilities in pharmaceutical-grade production increases capital investments, operational costs, and restricts manufacturing capacity growth. Additionally, pharmaceutical applications require rigorous quality control testing and documentation, as each batch must meet strict purity standards for elemental calcium content, microbial limits, and heavy metal contamination. The complexity of maintaining consistent product quality across batches while adhering to regulatory requirements further adds to the manufacturing challenges.

Competition from Alternative Calcium Supplements

The calcium gluconate market faces increasing competition from alternative calcium salts that demonstrate higher solubility and bioavailability characteristics. In beverage fortification applications, calcium lactate citrate and calcium lactate malate provide enhanced solubility properties, making them more suitable for liquid supplement formulations. Products containing calcium bisglycinate, manufactured by companies such as Cypress Minerals and Innophos, demonstrate bioavailability up to four times higher than conventional calcium salts, attracting consumers who prioritize optimal nutrient absorption. The expanding market for chelated calcium reflects increased consumer awareness and understanding of absorption differences among various calcium forms. Calcium citrate maintains a significant presence in the osteoporosis treatment segment, particularly in oral supplements, creating competitive pressure in this application area. The superior absorption properties of these alternative forms enable manufacturers to implement premium pricing strategies, which creates pricing challenges for calcium gluconate manufacturers who must primarily compete on cost rather than performance attributes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Pharmaceutical Dominance Drives Quality Standards

Pharmaceutical-grade calcium gluconate accounts for 45.86% of the market revenue in 2025, driven by its critical role in acute-care medical protocols. The segment projects a CAGR of 6.05% through 2031, supported by rising hospital admissions and emergency care needs. Suppliers ensure product quality through vertical integration, controlling processes from gluconic-acid fermentation to aseptic vial filling. This integrated approach maintains product standards and reduces contamination risks. The veterinary pharmaceutical sector demonstrates increased demand from expanding dairy operations and livestock healthcare requirements, sustaining high utilization of pharmacopoeial-grade production facilities.

Food-grade calcium gluconate, operating under Codex standards, experiences increased adoption in bakery premixes, beverage bases, and meat alternatives. The segment expands through rising consumer awareness of calcium fortification benefits. Market growth continues as fortified products expand their retail presence, supporting steady production volumes and creating manufacturer opportunities. The industrial grade segment focuses on specific applications, mainly concrete additives and specialty chemical production where chelation properties take precedence over purity requirements. These applications include water treatment and metal surface treatments. This market segmentation allows manufacturers to address varying purity needs while maintaining distinct pricing structures, supporting efficient resource allocation and market stability.

By Form: Powder Practicality Versus Liquid Bioavailability

Powder format accounts for 55.62% of calcium gluconate shipments in 2025. This dominance stems from its efficient transportation capabilities, compatibility with tablet manufacturing processes, and superior shelf stability without causing issues. The format's cost-effectiveness supports large-scale fortification programs, including national flour initiatives, school meal supplementation, and public health campaigns. The market maintains stability through annual supply agreements with global grain millers. In animal feed applications, the powder format is crucial for uniform mixing during pellet production. The format also enables manufacturers to develop customized formulations for various end-user needs.

The liquid solutions segment is advancing at 6.63% CAGR. Healthcare sector requirements for ready-to-use formulations primarily drive this growth. Single-dose ampoules minimize preparation errors during emergencies, while infusion centers use premixed bags to improve operational efficiency. The format is essential in intensive care units, pediatric wards, and emergency departments where quick administration is necessary. Nutraceutical manufacturers utilize the format's favorable taste profile to provide alternatives to traditional pills. The segment's growth is further supported by hospitals' adoption of just-in-time inventory systems and increased demand for convenient dosage forms in home healthcare. Recent improvements in packaging and preservation technologies have enhanced product shelf life and sterility maintenance.

By Application: Pharmaceutical Leadership Meets Personal Care Innovation

Pharmaceutical applications dominated calcium gluconate sales in 2025, accounting for 38.92% of the market. The segment expanded due to broader clinical applications, including hypocalcemia treatment, calcium channel blocker overdose management, and cardioprotection during high-dose chemotherapy. The compound's proven efficacy in treating hypocalcemia has secured its inclusion in emergency medicine protocols and standard hospital formularies. In veterinary medicine, calcium gluconate is crucial for treating parturient paresis in dairy cattle, with veterinarians preferring it over calcium chloride due to its non-irritating properties. The pharmaceutical segment maintains market strength through regulatory compliance and GMP manufacturing standards, enabling premium pricing. The rising incidence of calcium-related disorders and an aging population further reinforce the segment's market position.

The personal care segment exhibits the highest growth rate at 6.32% CAGR during the forecast period, supported by technological advancements. Mibelle Biochemistry's EpiCalsome™ technology employs nano-vesicles for calcium delivery, enhancing epidermal junction strength and wound healing properties. This development has increased research activities in calcium-based skincare formulations. Premium skincare brands use calcium gluconate in scalp serums and anti-aging masks as a bioactive ingredient rather than a texturizer. The compound's influence on cellular signaling and skin barrier function has expanded its use in dermatological products. Food and beverage fortification and feed additive segments show consistent growth, while the construction industry uses the compound as a set-retarder in specialty cement applications, highlighting calcium gluconate's industrial versatility. The compound's applications across multiple industries support ongoing market growth and technical development.

Geography Analysis

Asia-Pacific held 33.05% of global revenue in 2025. The region's chronic dietary deficiencies prompt physicians and nutritionists to recommend prescription and over-the-counter supplementation programs. The nutritional gaps across developing nations require comprehensive supplementation strategies. China's fermentation facilities supply both domestic and export markets, ensuring the availability of food fortification and injectable formulations. The country's manufacturing infrastructure supports production capabilities to meet regional and international demand. India's public health initiatives, including fortification programs in school lunches, utilize domestic pharmaceutical manufacturing to control costs. These programs address calcium deficiency among school-age children and reflect the government's focus on nutritional improvement.

North America shows the highest growth rate at 6.18% CAGR through 2031, driven by the FDA's fortification regulations for plant-based milk alternatives. Consumer transition to plant-based diets requires enhanced calcium fortification in alternative products. The Dietary Guidelines for Americans include fortified soy beverages in the dairy category based on their nutrient profile. These guidelines emphasize products with higher calcium, and other nutrients, while limiting saturated fat and added sugars. The region's aging population increases supplement use, particularly among those aged 65 and above seeking bone health support. Hospital purchasing groups maintain long-term contracts for preservative-free injectable formulations. The United States-Canada trade benefits from aligned USP monographs, enabling efficient sterile manufacturing across North American markets.

Europe maintains demand through pharmaceutical and bakery fortification channels. The United Kingdom's mandatory calcium fortification in wheat flour supports population-wide calcium intake through staple foods. German hospitals provide demand for calcium gluconate ampoules in emergency care, particularly for hypocalcemia and cardiac emergencies. Latin America and Africa show growth potential, with Brazil's beverage industry developing gluconate-fortified sports drinks. Nigerian dairy cooperatives are evaluating injectable solutions for livestock care to address calcium deficiency in dairy cattle. Despite distribution challenges in these regions, increased investment in consumer education and market development indicates expansion opportunities. The emphasis on preventive healthcare and nutritional supplementation suggests growth potential in these emerging markets.

Competitive Landscape

The calcium gluconate market maintains moderate concentration, with key players including Jungbunzlauer and Corbion operating integrated production chains. These companies convert raw glucose into high-purity gluconate and finished dosages. Their control over fermentation yields and purification resins ensures batch uniformity, which appeals to pharmaceutical buyers requiring consistent elemental calcium levels. The companies maintain strategic plants in China and Austria to optimize logistics for regional demand, while implementing dual-sourcing programs to ensure supply security for multinational customers.

Jungbunzlauer utilizes its proprietary Aspergillus niger strain to reduce fermentation cycle time, resulting in lower utility costs and minimal waste effluent. Corbion specializes in downstream granulation technologies to improve powder flow, enabling faster compression speeds for tablet manufacturers. BASF maintains application laboratories to develop fortification recipes with dairy and beverage companies, integrating its ingredient specifications into final product formulations to secure repeat orders.

Mid-sized companies focus on specialized market segments. For instance, Somerset Therapeutics provides bar-coded pre-filled syringes to ambulatory-surgery centers. Evonik develops amine co-products to enhance gluconate set-retarder properties for construction composites. Balchem's acquisition of Kappa Bioscience combines vitamin K2 with calcium gluconate, enabling bundled offerings for orthopedic supplement brands. These specialized market approaches increase competitive dynamics while maintaining overall market concentration, supporting price stability and continued product innovation in the calcium gluconate market.

Calcium Gluconate Industry Leaders

-

Jungbunzlauer AG

-

Corbion N.V.

-

Spectrum Chemical Manufacturing Corp.

-

Tomita Pharmaceutical Co., Ltd.

-

Jiaan Biotech

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Haleon extended its Caltrate brand to the Philippines to address widespread calcium deficiency in expectant mothers. This expansion is part of Haleon's broader strategy to replicate its success in China by raising awareness about calcium deficiency and providing solutions. In the Philippines, Haleon is reaching out to gynecologists to educate them on the importance of calcium supplementation during pregnancy and offering bone density tests in clinics and stores.

- November 2024: Evonik is expanding its specialty-amine production capacity in Nanjing, China, to meet the growing demand for construction and automotive additives, specifically for polyurethane and epoxy curing agents. This expansion, at their existing site, aims to enhance their amine portfolio and strengthen their competitive position in the Chinese market and globally.

Global Calcium Gluconate Market Report Scope

Global calcium gluconate market is segmented by application (which includes food & beverage, pharmaceuticals, personal care products, and animal feed); and by geography (which includes North America, Europe, Asia-Pacific, South America, and the Middle East and Africa).

| Pharmaceutical Grade |

| Food Grade |

| Industrial Grade |

| Powder |

| Liquid |

| Food and Beverage |

| Pharmaceutical |

| Personal Care Products |

| Animal Feed |

| Construction and Industrial Additives |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Grade | Pharmaceutical Grade | |

| Food Grade | ||

| Industrial Grade | ||

| By Form | Powder | |

| Liquid | ||

| By Application | Food and Beverage | |

| Pharmaceutical | ||

| Personal Care Products | ||

| Animal Feed | ||

| Construction and Industrial Additives | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the calcium gluconate market by 2031?

The calcium gluconate market is forecast to reach USD 142.16 billion by 2031, growing at a 5.02% CAGR over 2026-2031.

Which region is growing the fastest in the calcium gluconate market?

North America is expanding at a 6.18% CAGR through 2031, propelled by fortification policies and an aging population that seeks highly absorbable calcium.

How big is the pharmaceutical-grade segment within the calcium gluconate market?

Pharmaceutical-grade products accounted for 45.86% of revenue in 2025 and are on track for a 6.05% CAGR, underscoring their dominance in therapeutic applications.

Why do hospitals prefer calcium gluconate over calcium chloride for hypocalcemia emergencies?

Calcium gluconate delivers ionic calcium quickly yet causes less tissue irritation and boasts a safer hemodynamic profile, making it the standard intravenous choice in many emergency protocols.

Page last updated on: