Cocoa Bean Extract Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

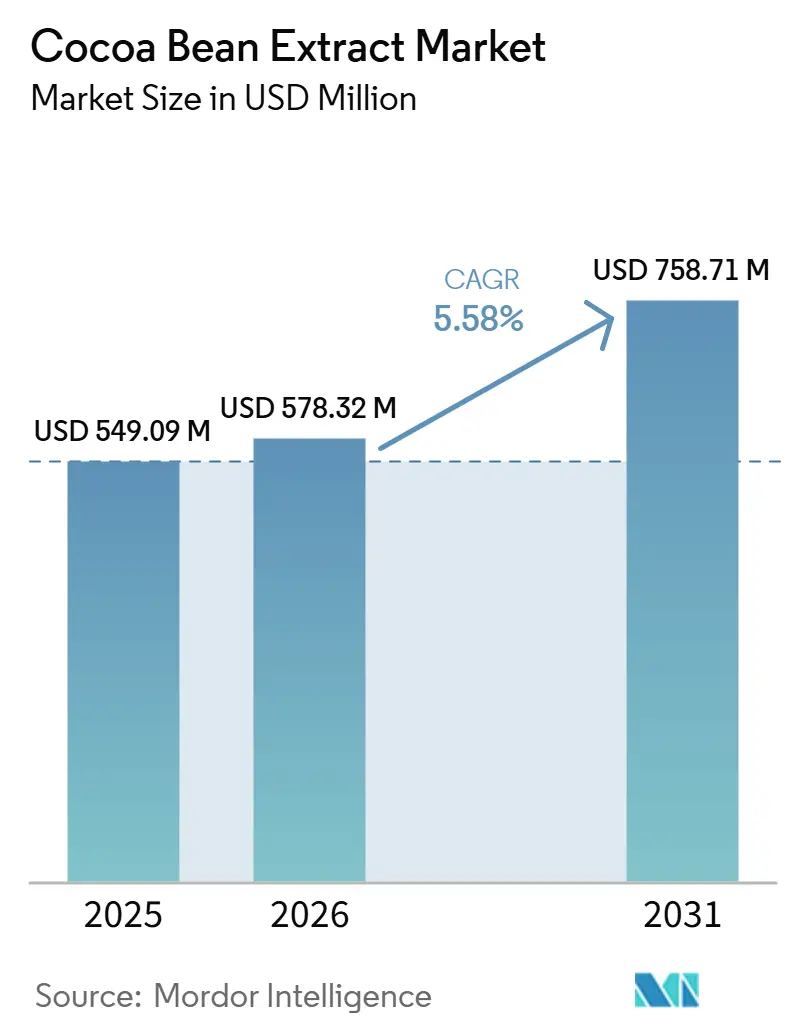

| Market Size (2026) | USD 578.32 Million |

| Market Size (2031) | USD 758.71 Million |

| Growth Rate (2026 - 2031) | 5.58% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cocoa Bean Extract Market Analysis by Mordor Intelligence

The cocoa bean extract Market size is expected to increase from USD 549.09 million in 2025 to USD 578.32 million in 2026 and reach USD 758.71 million by 2031, growing at a CAGR of 5.58% over 2026-2031. Driven by clinical validation, cocoa flavanols are increasingly sought after for their benefits in cardiovascular health, skin protection, and sports recovery. This shift in demand is moving away from traditional confectionery products and towards dietary supplements, functional beverages, and cosmeceuticals. In 2024, the United States Food and Drug Administration issued a qualified health claim, bolstering the case for cocoa flavanols. This followed an earlier endorsement from the European Food Safety Authority. Both authorities set a daily flavanol threshold, granting brand owners a solid regulatory footing to market heart-health benefits in North America and Europe. Bean prices saw a dramatic rise earlier in the year before stabilizing later, prompting processors to focus on higher-margin bioactive extracts, which are more resilient to such price swings. Furthermore, producers boasting integrated sourcing and traceability systems are capitalizing on sustainability narratives and premium certifications, enabling them to clinch reformulation contracts with brands in beverages, supplements, and personal care.

Key Report Takeaways

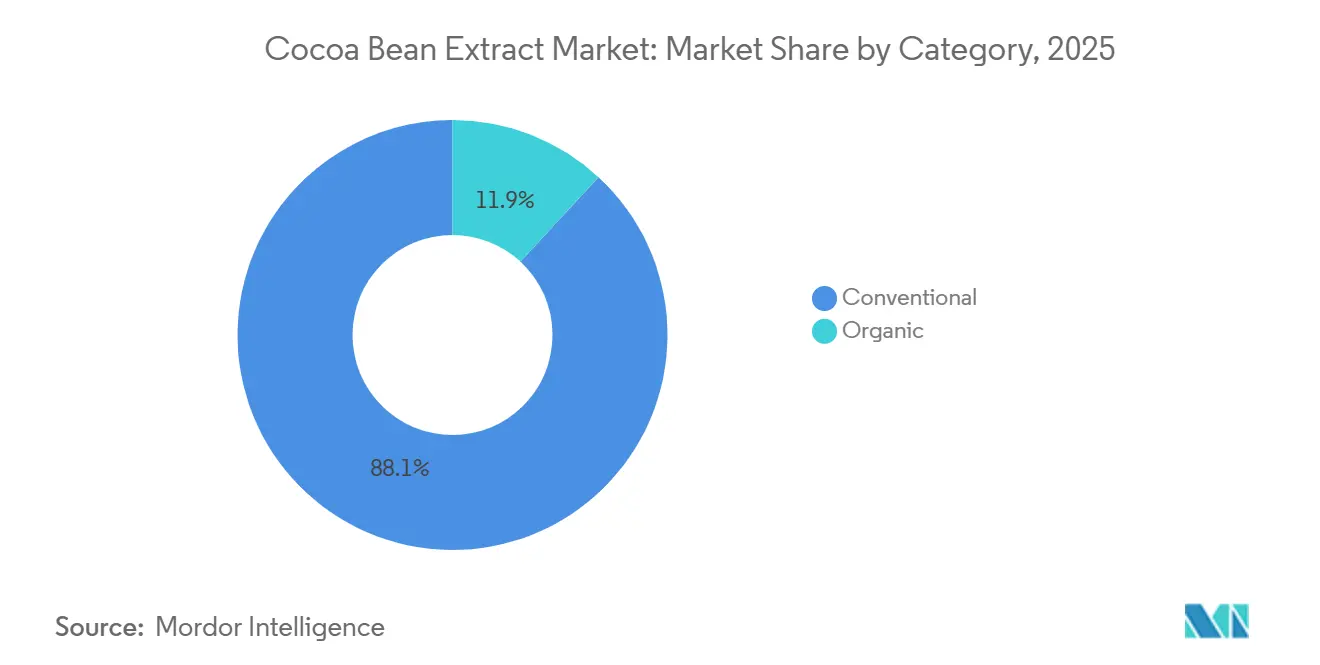

- By category, conventional products held 88.12% of the cocoa bean extract market share in 2025, whereas organic variants are forecast to expand at a 6.71% CAGR through 2031.

- By product form, powder extracts led with 67.82% revenue contribution in 2025, while liquid formats are projected to advance at a 6.42% CAGR to 2031.

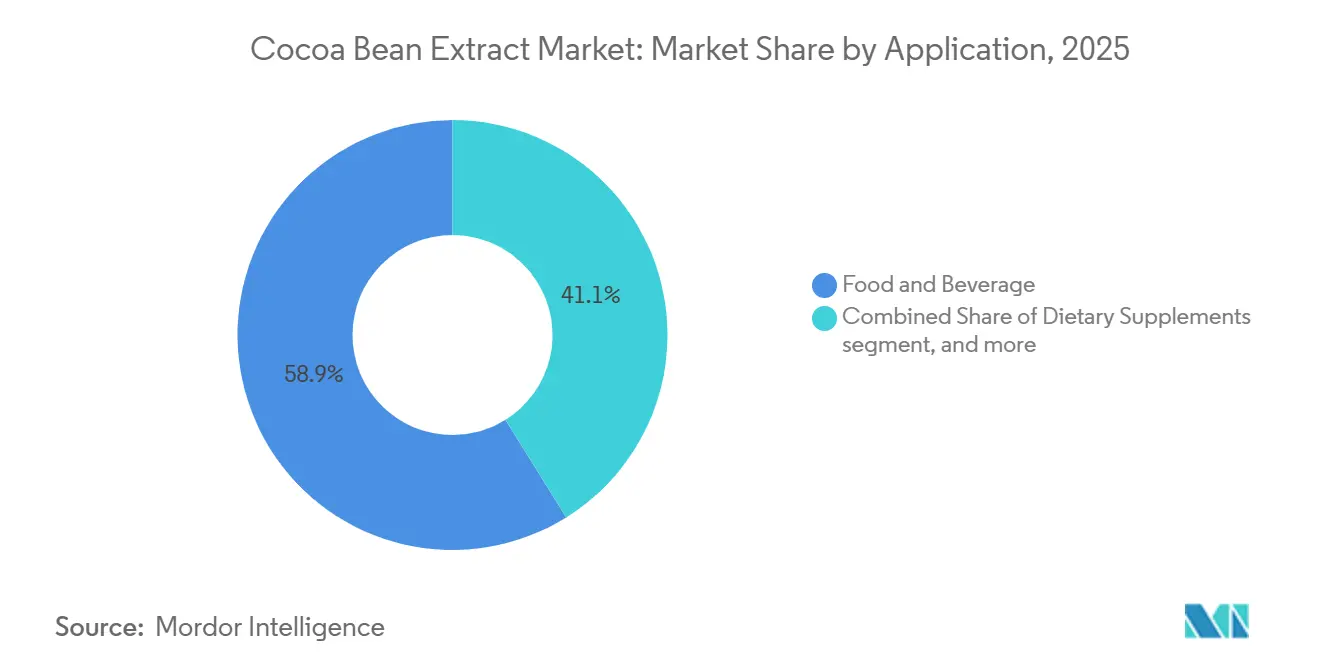

- By application, food and beverage accounted for 58.88% of demand in 2025, yet dietary supplements are expected to post the fastest growth at a 6.78% CAGR over the forecast window.

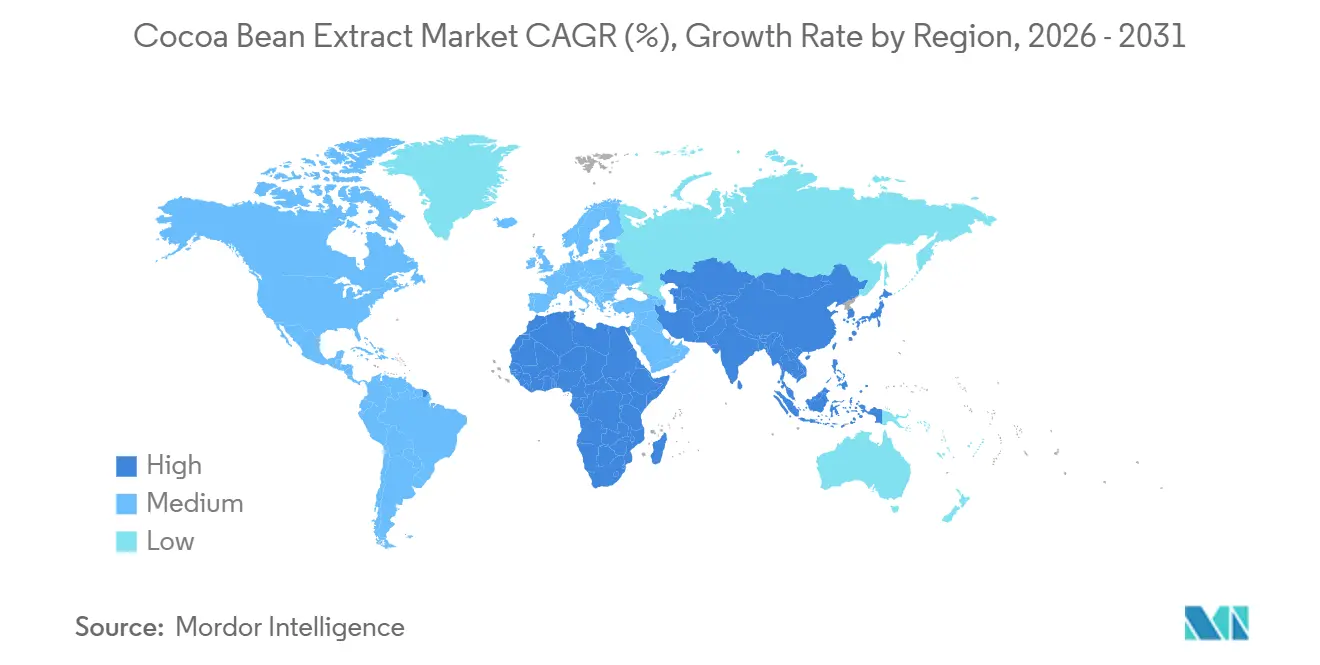

- By geography, Europe dominated with a 35.72% share in 2025, whereas Asia-Pacific is anticipated to register the quickest expansion at a 6.77% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cocoa Bean Extract Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer awareness of cocoa flavanols and polyphenols | +1.2% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Rising prevalence of lifestyle diseases driving preventive nutrition | +1.0% | Global, concentrated in North America, Europe, and urban Asia-Pacific | Long term (≥ 4 years) |

| Shift away from artificial flavors and synthetic antioxidants | +0.8% | North America and Europe, spillover to Asia-Pacific | Short term (≤ 2 years) |

| Expanding dietary supplement and sports nutrition applications | +0.9% | North America, Europe, and emerging Asia-Pacific markets | Medium term (2-4 years) |

| Growing application in cosmetics and personal care | +0.5% | Europe, North America, and premium Asia-Pacific segments | Medium term (2-4 years) |

| Increased adoption of plant-based extract technologies | +0.4% | Global, led by Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Consumer awareness of cocoa flavanols and polyphenols

Clinical validation is reshaping cocoa's image from a mere confectionery delight to a potent cardiovascular nutraceutical. The Cocoa Supplement and Multivitamin Outcomes Study (COSMOS), a rigorous randomized controlled study, tracked a large group of participants over several years. Findings revealed that a daily dose of cocoa flavanols significantly reduced cardiovascular deaths among dedicated participants. These results bolster the qualified health claim from the U.S. Food and Drug Administration (FDA) in 2024 and the endorsement from the European Food Safety Authority (EFSA). Such validations pave the way for cocoa's inclusion in dietary supplements and functional foods. Yet, the FDA's cautious "very limited evidence" tag on its claim underscores regulatory prudence. This caution curtails marketing language and mandates further post-market surveillance studies by producers. The polyphenol content in cocoa extracts, notably epicatechin, catechin, and procyanidins, fluctuates based on factors like bean origin, fermentation time, and extraction methods. Such variability poses quality assurance hurdles, giving an edge to vertically integrated suppliers with advanced traceability. Barry Callebaut's patent applications for techniques that enhance flavanol retention highlight a strategic move towards bioactive preservation and competitive edge.

Rising prevalence of lifestyle diseases driving preventive nutrition

According to the World Health Organization, cardiovascular disease is the leading global cause of death, claiming millions of lives each year. Meanwhile, the prevalence of type 2 diabetes has significantly increased since the year 2000. In response to this epidemiological burden, consumer spending is shifting from reactive pharmaceuticals to preventive supplements. This trend is further intensified by aging populations in Europe and North America, alongside a rising health consciousness among the middle class in the Asia-Pacific region. Cocoa extracts straddle the line between indulgence and functionality, serving as a palatable entry point for consumers wary of unfamiliar botanicals. However, standardizing dosage presents a challenge. While most clinical benefits are observed with a daily intake of specific amounts of flavanols, standard dark chocolate bars typically offer much lower quantities. This gap necessitates the use of concentrated extracts, which eliminate sugar and fat. Such formulation needs underscore the projected growth in dietary supplements, with capsule and powder formats allowing for precise dosing without added calories.

Shift away from artificial flavors and synthetic antioxidants

Clean-label mandates in North America and Europe are reshaping the formulation of packaged foods and beverages. Under the European Union's Farm to Fork strategy, a goal has been set to significantly reduce chemical pesticide use by the end of the decade. This move indirectly nudges manufacturers towards sourcing ingredients from simpler supply chains. In bakery and snack applications, cocoa extracts are now substituting synthetic antioxidants, such as butylated hydroxyanisole and butylated hydroxytoluene. These natural cocoa extracts not only provide a comparable shelf-life extension but also come with a compelling natural origin narrative. Both the United States Department of Agriculture's National Organic Program and the European Union's Organic Regulation impose stringent certification standards on organic cocoa extracts. These standards mandate traceability to certified farms and ban the use of synthetic solvents during processing. While compliance costs are significantly higher than conventional sourcing, the retail market offers a silver lining. Organic extracts enjoy a substantial price premium, effectively counterbalancing the input inflation. This interplay sheds light on the projected growth for organic variants. In contrast, conventional formats, holding the majority market share, remain dominant, largely due to their appeal in cost-sensitive mass-market food applications.

Expanding dietary supplement and sports nutrition applications

Cocoa extracts are becoming increasingly popular in pre-workout and recovery formulations due to their ability to boost nitric oxide levels, which enhances blood flow and oxygen delivery to muscles. A recent study published in the Journal of the International Society of Sports Nutrition highlighted that cocoa flavanols significantly improved endurance athletes' performance compared to a placebo. This development is driving new product launches in the sports nutrition market, where cocoa extracts compete with beetroot powder and citrulline malate for their nitric oxide-related benefits. The segment's growth reflects both clinical validation and formulation flexibility, as cocoa extracts easily integrate into protein powders, energy gels, and ready-to-drink shakes without the earthy taste associated with beetroot. Regulatory pathways remain supportive; this year, the United States Food and Drug Administration granted Generally Recognized as Safe status to cacao pulp and juice, signaling acceptance of innovative cocoa-derived ingredients [1]Source: U.S. Food & Drug Administration, “FDA Announces Qualified Health Claim for Cocoa Flavanols in High Flavanol Cocoa Powder and Reduced Risk of Cardiovascular Disease,” fda.gov. However, heavy metal contamination, particularly cadmium in beans sourced from Latin America, necessitates rigorous testing protocols. The European Commission has set strict limits for cadmium in cocoa powder, indirectly influencing extract sourcing practices [2]Source: Netherlands Ministry of Foreign Affairs, “What requirements must cocoa meet to be allowed on the European market?,” cbi.eu.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate change-induced crop yield unpredictability | -0.9% | Global, concentrated in West Africa and Southeast Asia | Long term (≥ 4 years) |

| Complex and divergent regulatory frameworks across regions | -0.6% | Global, with friction points between North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Rising incidence of cocoa crop diseases | -0.5% | West Africa, Latin America | Short term (≤ 2 years) |

| High cost and complexity of advanced extraction processes | -0.4% | Global, particularly impacting small and mid-sized processors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Climate change-induced crop yield unpredictability

Cocoa cultivation thrives within a specific climate: temperatures ranging from 18 to 32 degrees Celsius and annual rainfall between 1,500 and 2,000 millimeters. A study from Wageningen University in 2024 warned that under a 2-degree warming scenario, Ivory Coast, the world's largest cocoa producer, might see its suitable cocoa-growing area shrink significantly by the middle of the century. Temperatures exceeding 32 degrees Celsius cause heat stress, which hampers pod formation and increases vulnerability to pests. Erratic rainfall adds to the challenges; for example, Ghana's crop for the 2024 to 2025 season experienced a notable decline due to delayed rains during the critical flowering phase. These supply disruptions directly impact extract pricing, as raw bean costs make up a substantial portion of total production expenses. While the International Cocoa Organization reported a slight surplus for the 2024 to 2025 season, it anticipates deficits for the following season, putting pressure on processors who cannot hedge effectively [3]. Leading buyers are now sourcing from countries like Ecuador, Peru, and Indonesia. However, these regions also face climate-related challenges, such as droughts caused by El Niño and flooding during monsoon seasons.

Complex and divergent regulatory frameworks across regions

Health claim approval pathways vary significantly across jurisdictions, compelling manufacturers to tailor formulations and labeling to specific regions. The European Food Safety Authority mandates randomized controlled trials with a minimum of 200 participants for Article 13.5 health claims, a requirement that can cost manufacturers millions. While the United States Food and Drug Administration allows for a "qualified claim" route with less stringent evidence requirements, it also necessitates disclaimer language, potentially undermining the marketing message. The Asia-Pacific region showcases even greater fragmentation: China's National Health Commission views cocoa extracts as novel foods, necessitating pre-market approval, whereas India's Food Safety and Standards Authority allows their inclusion in dietary supplements sans pre-clearance, yet imposes restrictions on health claims. This regulatory maze inflates compliance costs for multinational brands by an estimated 15 to 20% and postpones global product launches by 12 to 18 months. Meanwhile, smaller ingredient suppliers, lacking the expertise to navigate these diverse regulations, find themselves losing ground to larger, vertically integrated companies like Cargill and Olam, which boast in-house regulatory teams in crucial markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Category: Organic Premiums Offset Volume Constraints

Conventional cocoa bean extracts accounted for 88.12% of market revenue in 2025, driven by cost advantages and established supply chains catering to mass-market food and beverage applications. Organic extracts, while holding a smaller market share, are projected to grow at an annual rate of 6.71% through 2031, surpassing the overall market growth rate by 113 basis points. This growth is attributed to premium pricing as organic extracts command 40% to 50% higher prices in retail channels and supportive regulatory initiatives, such as the European Union's Farm to Fork strategy and the United States Department of Agriculture's Organic Action Plan, which emphasize certified supply chains.

However, the supply of organic cocoa beans remains limited, with certified acreage accounting for less than 5% of global cocoa cultivation. This production is concentrated in countries like the Dominican Republic, Peru, and Madagascar, where smallholder farmers face certification costs ranging from USD 2,000 to USD 5,000 per farm and endure multi-year transition periods. The growth of the organic segment depends on addressing a structural challenge: while consumer willingness to pay premiums exceeds supply availability, the high costs and lengthy certification processes discourage adoption among farmers in West Africa, which produces 70% of the world's cocoa beans.

By Product Form: Bioavailability Drives Liquid Extract Gains

Powder extracts accounted for 67.82% of the market share in 2025, primarily due to their stability, low moisture content, and compatibility with capsule and tablet formats, which dominate dietary supplement channels. Liquid extracts, while holding the remaining share, are projected to grow at an annual rate of 6.42% through 2031. This growth is driven by their application in beverages, where water dispersibility and rapid dissolution are critical. According to the Journal of Agricultural and Food Chemistry, researchers observed that liquid cocoa extracts achieved higher peak plasma epicatechin concentrations compared to powdered extracts, even when dosed identically. This is attributed to pre-dissolved polyphenols in liquid extracts, which bypass gastric breakdown. As a result, functional beverage manufacturers are increasingly adopting liquid formats, particularly in ready-to-drink coffee, tea, and sports hydration products, where rapid onset and sensory integration are key to consumer preferences.

While powder extracts dominate cost-sensitive applications, their production processes, such as spray-drying and freeze-drying, result in higher costs compared to liquid concentrations. However, powder extracts offer a significant advantage in terms of shelf stability, with a lifespan that doubles that of liquid extracts. This extended shelf life reduces inventory risks for manufacturers, particularly those with global distribution networks. In the cosmetics and personal care sector, where steady growth is anticipated, powder formats are preferred. They are easily incorporated into products such as dry face masks, exfoliating scrubs, and pressed powders. This preference is driven by the need to maintain very low moisture content to prevent microbial growth. Addressing a key challenge in the beverage industry, Barry Callebaut recently secured a patent for a lipid-encapsulated cocoa powder extract. This innovation involves coating polyphenol particles with sunflower lecithin, ensuring instant dissolution in plant-based milk alternatives. This development eliminates sedimentation and enhances water dispersibility in cold beverages, further expanding the utility of powder extracts in the beverage market.

By Application: Nutraceuticals Outpace Confectionery

In 2025, food and beverage applications are projected to account for 58.88% of the demand for cocoa bean extracts. However, dietary supplements are anticipated to grow at an annual rate of 6.78% through 2031, emerging as the fastest-growing end-use segment for cocoa ingredients. This trend reflects a shift from indulgence-focused consumption to an emphasis on functional health benefits. Traditional chocolate confectionery, a primary use for cocoa, often faces challenges with inconsistent flavanol levels due to processing methods such as alkalization and roasting, which can significantly degrade polyphenols. These inconsistencies limit the ability of chocolate products to consistently deliver health benefits.

In contrast, dietary supplements utilize standardized extracts that ensure minimum flavanol levels per serving, strengthening their health-related claims. Furthermore, clinical studies, such as the Cocoa Supplement and Multivitamin Outcomes Study trial, have demonstrated notable health benefits, including a significant reduction in cardiovascular deaths among regular users. This evidence highlights the growing appeal of cocoa-based dietary supplements for health-conscious consumers. High-cocoa chocolate products, however, are unable to make similarly reliable health claims, as they lack the standardized flavanol content that supplements provide.

Geography Analysis

Europe remains the leading segment in the cocoa bean extract market, capturing 35.72% of revenue in 2025. This dominance is driven by Germany, the United Kingdom, and the Netherlands, where well-established dietary supplement channels and strict clean-label regulations converge. The European Food Safety Authority's endorsement of cocoa flavanol health claims has bolstered the positioning of cocoa-based ingredients. Additionally, the European Union's Farm to Fork strategy encourages manufacturers to focus on certified organic and fair-trade extracts. Germany's dietary supplement market, with its strong per-capita consumption of cardiovascular health products, is expected to grow significantly by 2025, further driving demand for cocoa-based formulations. Meanwhile, the United Kingdom faces regulatory challenges post-Brexit as the Food Standards Agency develops independent health claim pathways, potentially requiring product reformulations to meet both United Kingdom and European Union guidelines. The Netherlands plays a key role as a processing hub, with facilities like Barry Callebaut's Wieze plant and Cargill's Amsterdam cocoa plant handling substantial cocoa bean volumes annually. However, growth in European demand is expected to slow through 2031 due to market saturation and competition from alternative polyphenol sources like grape seed and green tea extracts.

The Asia-Pacific region is the fastest-growing segment, projected to expand at an annual rate of 6.77% through 2031. This growth is driven by increasing health awareness among the middle class in China and India, along with the expanding retail distribution of imported dietary supplements. In 2024, China's National Health Commission classified cocoa extracts as novel foods, requiring pre-market safety assessments. While this initially delayed product launches, approvals are now accelerating as manufacturers submit dossiers demonstrating safe use histories in Europe and North America. India's dietary supplement market, growing annually according to the Food Safety and Standards Authority of India, shows strong demand for cardiovascular and cognitive health products, where cocoa flavanols align with clinical evidence. These factors are expected to sustain the region's rapid growth trajectory.

Other regions, including North America, South America, the Middle East, and Africa, are also contributing to the cocoa bean extract market. In North America, the United States leads due to its robust dietary supplement industry and a regulatory environment that supports structure-function claims. The Food and Drug Administration's endorsement of cocoa flavanols as a qualified health claim, albeit with limited evidence, has boosted sales in mainstream outlets like Costco and Whole Foods. Canada requires pre-market licensing for supplements through the Natural and Non-prescription Health Products Directorate, a stricter process compared to the United States, but cocoa extracts have successfully gained approvals for their antioxidant benefits. Mexico's supplement market is growing steadily, driven by urbanization and a rising prevalence of diabetes, which is encouraging increased spending on preventive health products. In South America, led by Brazil and Colombia, moderate growth is observed due to economic challenges and a retail environment that struggles to support premium supplements. However, Colombian processors are focusing on domestic extract production to achieve value-added margins instead of exporting raw beans. In the Middle East and Africa, countries like the United Arab Emirates and South Africa are emerging as import hubs, attracting European and North American brands that cater to expatriates and affluent local consumers, signaling potential for future growth in these regions.

Competitive Landscape

The cocoa bean extract market exhibits moderate concentration, characterized by a bifurcated structure. Upstream processing is led by major companies such as Barry Callebaut, Cargill, and Olam International, while downstream formulation and distribution remain fragmented among specialty ingredient suppliers, contract manufacturers, and private-label providers. Olam's acquisition of Archer Daniels Midland's cocoa business for USD 1.3 billion in March 2026 consolidated 600,000 tonnes of annual processing capacity across eight factories located in Europe, North America, and Asia. This strategic acquisition positions Olam to vertically integrate its extract production processes and capture additional value beyond the commodity cocoa market.

Barry Callebaut announced a significant investment of EUR 250 million in its Wieze, Belgium facility in February 2026. This investment is specifically targeted at developing high-flavanol extract lines designed for pharmaceutical and cosmetic clients, signaling a strategic shift toward producing value-added bioactive ingredients. There are ongoing opportunities in improving bioavailability and creating targeted delivery systems for cocoa extracts. For example, Barry Callebaut's 2025 patent filing for lipid-encapsulated cocoa powder extracts aims to address the issue of poor water dispersibility in cold beverages, which has been a major obstacle to the adoption of cocoa extracts in the ready-to-drink functional beverage market.

Smaller players, such as Prova and Natra, are focusing on their expertise in formulation to remain competitive. These companies offer custom blends that combine cocoa extracts with complementary botanicals such as beetroot or green tea, enabling brand owners to create proprietary complexes that stand out in the market. However, the high costs associated with regulatory compliance, which are estimated to account for 15 to 20 percent of revenue for operations spanning multiple regions, provide a distinct advantage to larger players that have dedicated in-house regulatory affairs teams to manage these requirements efficiently.

Cocoa Bean Extract Industry Leaders

Barry Callebaut AG

Cargill, Incorporated

Olam International Limited

Archer Daniels Midland Company

Nestlé S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Barry Callebaut invested EUR 250 million in a chocolate factory located in Wieze. Additionally, a EUR 125 million Masterplan has been designed for the factory in Halle. These investments are aimed at future-proofing the production facilities, emphasizing their importance in delivering high-quality customer experiences and enhancing operational efficiency.

- September 2025: Barry Callebaut and Maersk have inaugurated a 40,000-metric-tonne cocoa bean warehouse in Port Klang, Malaysia, aimed at strengthening supply chain resilience for cocoa extract production in the Asia-Pacific region.

- December 2024: Israeli startup Celleste Bio, an AI-driven, cell-based cocoa producer, has secured a USD 4.5 million investment round led by Mondelēz. Celleste Bio combines agtech and biotechnology with AI models, enabling them to extract cells from cocoa plants. These cells, multiplied in bioreactors, yield the equivalent of cocoa butter and powder from just one or two beans, a feat that traditionally requires four tonnes of cocoa pods.

Global Cocoa Bean Extract Market Report Scope

The cocoa bean extract market refers to products derived from Theobroma cacao beans through processes such as fermentation, drying, roasting, grinding, pressing, and extraction. These extracts are valued for their cocoa flavor and naturally occurring bioactive compounds, including flavonoids, theobromine, catechins, procyanidins, and other antioxidant components. The market is segmented by category into organic and conventional; by product form into powder extract and liquid extract; by application into food and beverage, dietary supplements, cosmetics and personal care, and pharmaceuticals; and by geography into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market sizing has been done in value terms in USD and volume in Tons for all the abovementioned segments.

| Organic |

| Conventional |

| Powder Extract |

| Liquid Extract |

| Food and Beverage |

| Dietary Supplements |

| Cosmetics and Personal-Care |

| Pharmaceuticals |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Category | Organic | |

| Conventional | ||

| By Product Form | Powder Extract | |

| Liquid Extract | ||

| By Application | Food and Beverage | |

| Dietary Supplements | ||

| Cosmetics and Personal-Care | ||

| Pharmaceuticals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is cocoa bean extract demand growing in supplements?

Dietary-supplement demand is slated to rise at a 6.78% CAGR from 2026 to 2031, outpacing food and beverage channels.

Which region will add the most incremental volume by 2031?

Asia-Pacific, led by China and India, is projected to deliver the largest absolute growth, expanding at a 6.77% CAGR.

Why are manufacturers shifting from chocolate to extracts?

Standardized extracts allow precise 200-500 milligram flavanol doses without sugar or fat, aligning with cardiovascular-health claims.

What is the main threat to supply stability?

Climate-driven yield swings and crop diseases such as swollen-shoot virus in West Africa risk cutting bean availability and lifting costs.

How do liquid extracts compare with powders in bioavailability?

Clinical data show liquid formats achieve about 23% higher peak plasma epicatechin levels than matched-dose powders.

Page last updated on: