Glucuronolactone Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

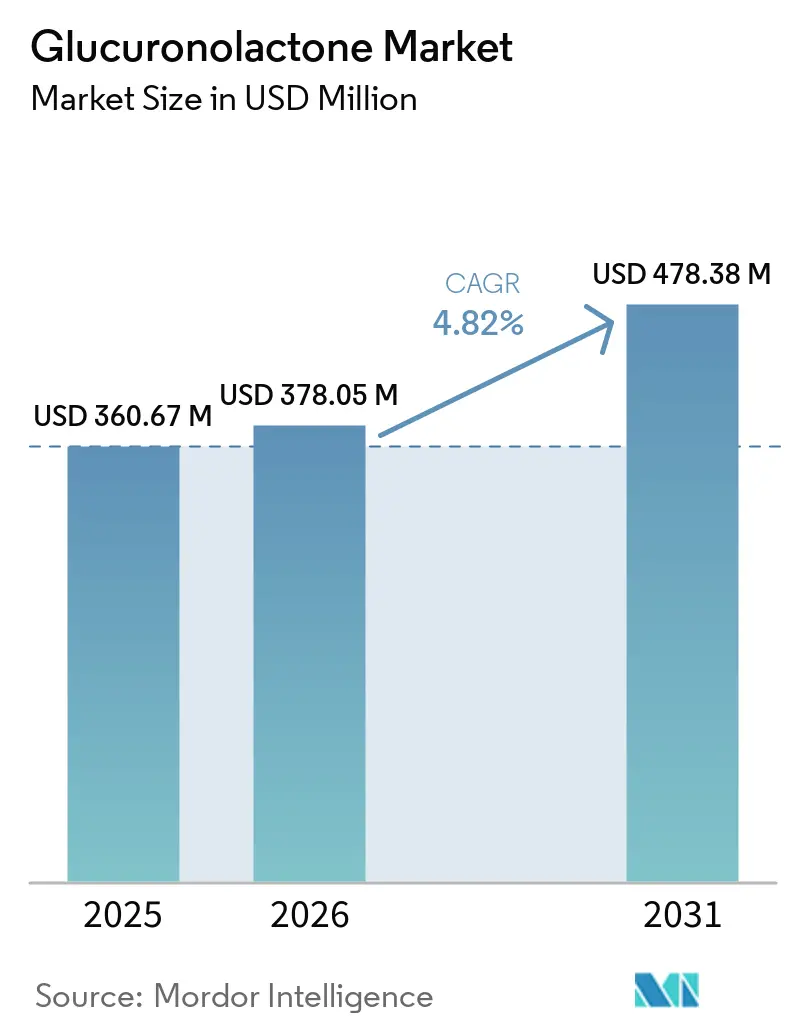

| Market Size (2026) | USD 378.05 Million |

| Market Size (2031) | USD 478.38 Million |

| Growth Rate (2026 - 2031) | 4.82% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Glucuronolactone Market Analysis by Mordor Intelligence

The glucuronolactone market size is expected to increase from USD 360.67 million in 2025 to USD 378.05 million in 2026 and reach USD 478.38 million by 2031, growing at a CAGR of 4.82% over 2026-2031, driven by sustained demand from energy drink producers and an expanding dietary supplement industry that has absorbed the compound's dual positioning as a detoxification aid and a performance enhancer. The compound's role in hepatic glucuronidation, binding, and elimination of metabolic waste products through the liver's Phase II detoxification pathway is increasingly cited in peer-reviewed literature as a functional differentiator from caffeine and B-vitamin-only formulas. A broad reformulation cycle in zero- and low-sugar beverages is also supporting the glucuronolactone market, as brand owners seek ingredients that align with cleaner labels and work well alongside taurine, caffeine, vitamins, and electrolytes. Supply conditions remain a key watch point, as tighter environmental enforcement in Shandong is raising compliance demands on producers, likely favoring larger suppliers with auditable operations and clear sustainability credentials.

Key Report Takeaways

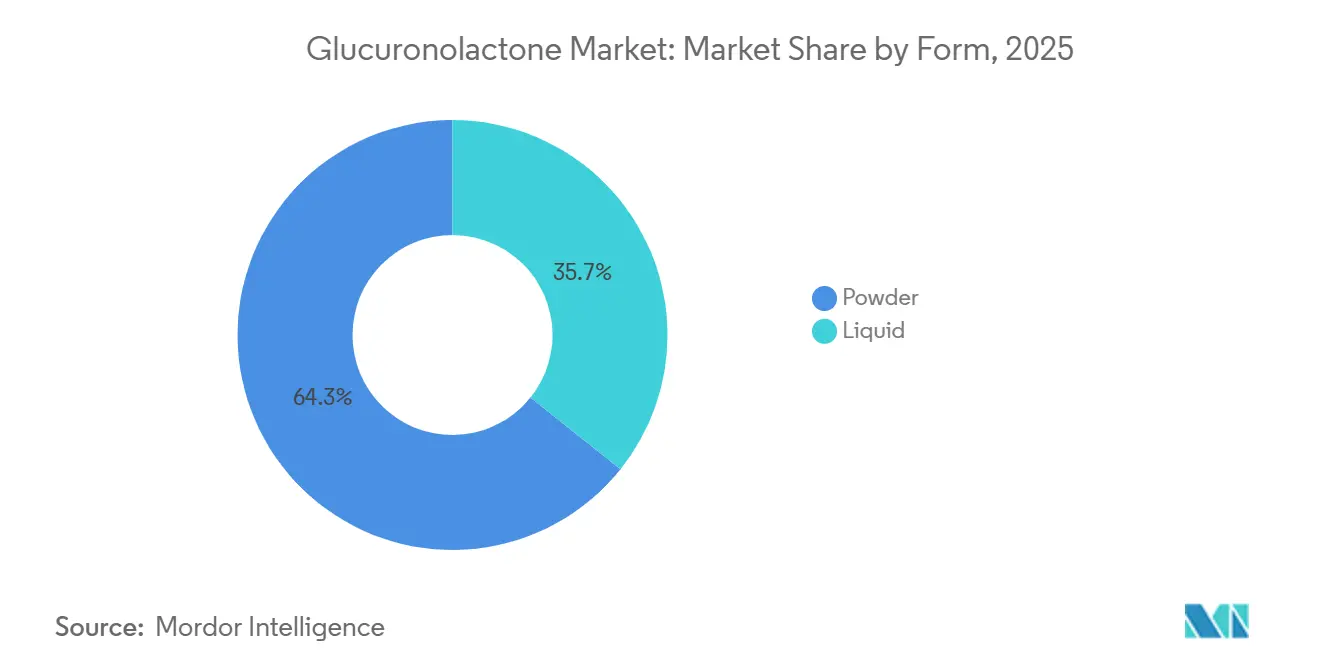

- By form, powder held 64.27% share in 2025, while liquid is forecast to expand at 6.06% CAGR during 2026-2031.

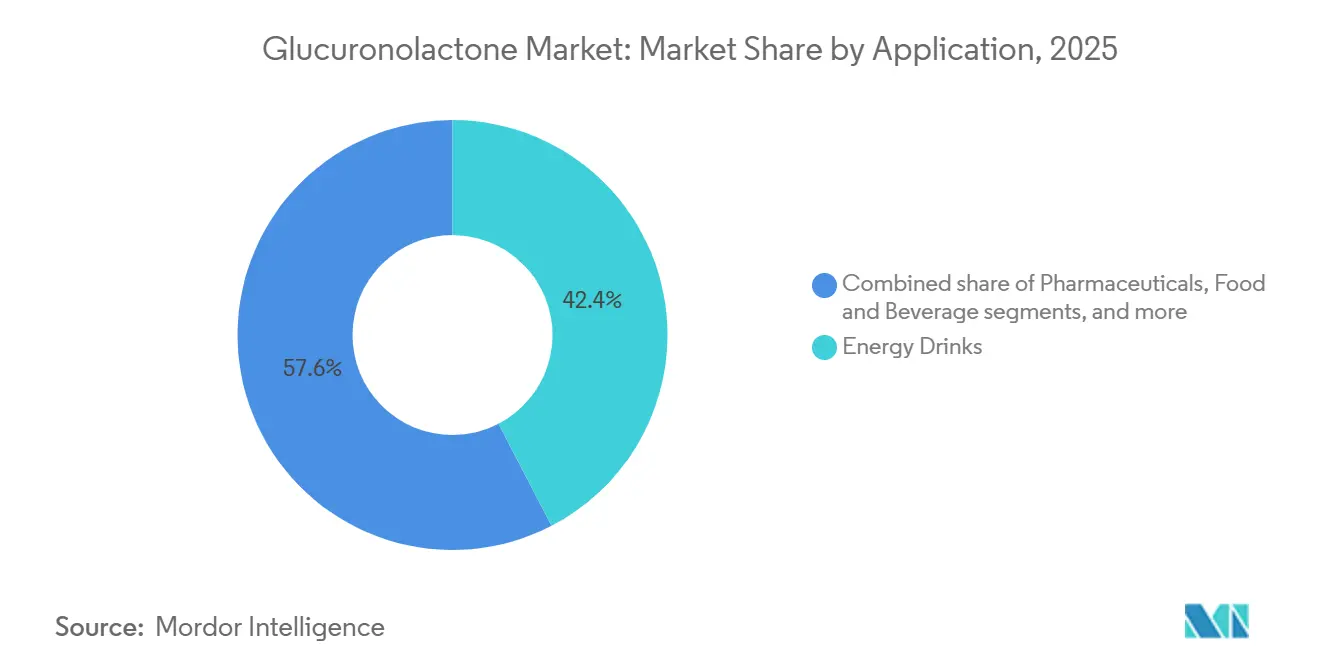

- By application, energy drinks accounted for 42.38% of the glucuronolactone market in 2025, while dietary supplements and nutraceuticals is projected to grow at 7.28% CAGR through 2031.

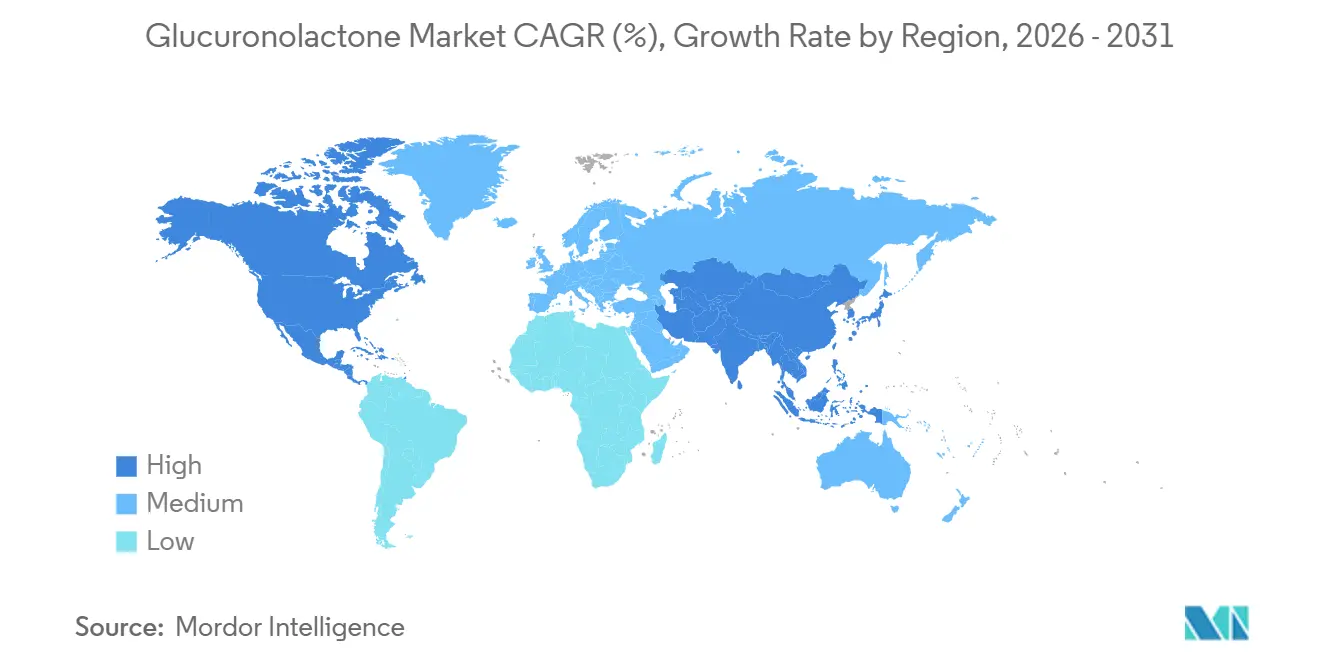

- By geography, North America held 37.08% of the glucuronolactone market share in 2025, while Asia-Pacific is set to record the highest CAGR of 6.25% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Glucuronolactone Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy drink and functional beverage expansion | +1.3% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Dietary supplement and liver-support uptake | +1.0% | Global; early gains in North America and Asia-Pacific | Medium term (2–4 years) |

| Rising demand for sports nutrition products | +0.6% | North America and Europe; spill-over to Asia-Pacific | Short term (≤ 2 years) |

| Innovation in low-sugar RTD formulations | +0.5% | North America and Europe | Medium term (2–4 years) |

| Gamer and nootropic product penetration | +0.4% | Asia-Pacific core; spill-over to North America and Europe | Medium term (2–4 years) |

| Growing application in cognitive health and mental focus | +0.4% | Global, strongest in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Energy drink and functional beverage expansion

The energy drink category continues to create the single largest volume pull for the glucuronolactone market. Brands are expanding their product portfolios to cater to distinct consumer occasions such as hydration, focus, and recovery. Glucuronolactone's multifunctional profile, including detoxification, energy enhancement, and liver protection, enables its integration across various formulations, thereby increasing its average inclusion rate per unit volume. The growing demand for functional beverages, including energy drinks, is further driving the market. These beverages are increasingly targeting health-conscious consumers by incorporating ingredients such as glucuronolactone to enhance performance and deliver functional benefits. Additionally, the rise of clean-label and natural ingredient trends has encouraged manufacturers to innovate and reformulate products, creating new opportunities for glucuronolactone in the functional beverage segment. The global expansion of energy drink brands into emerging markets, coupled with aggressive marketing strategies, is expected to sustain the growth of this segment, making it a critical driver for the glucuronolactone market.

Rising demand for sports nutrition products

The rising demand for sports nutrition products is significantly driving the growth of the glucuronolactone market. Sports nutrition products, including energy drinks, recovery beverages, and functional supplements, are increasingly incorporating glucuronolactone due to its multifunctional benefits. Known for its detoxification, energy-boosting, and liver-protective properties, glucuronolactone has become a key ingredient in formulations for athletes and fitness enthusiasts. This trend is further supported by the growing consumer focus on health, wellness, and performance optimization. Sports nutrition is also expanding the application of glucuronolactone beyond traditional pre-workout energy drinks. HOWTIAN Group, for instance, has positioned D-glucuronolactone as a critical component in post-training recovery protocols. Its ability to enhance hepatic clearance of toxins accumulated during high-protein diets and stimulant-heavy training regimens makes it an ideal ingredient for recovery-focused products. This positioning is particularly significant as it creates new opportunities for glucuronolactone in post-session beverages and powders, diversifying its use cases and increasing its market penetration.

Innovation in low-sugar RTD formulations

Low-sugar and zero-sugar beverage innovation is opening a new path for the glucuronolactone market. Dunkin’ Zero, Monster STORM, and Dong-A Pharmaceutical’s Eolbaksa Zero all launched in 2026, and these releases show that major brands across retail, quick service, and healthcare-adjacent channels are betting on sugar-reduced energy beverages. As brands from QSR chains (Dunkin' Zero, March 2026) to pharma-adjacent drinks companies (Dong-A Pharmaceutical's Eolbaksa Zero, March 2026) enter the zero- and low-sugar energy space, they need functional ingredients that maintain consumer-perceivable benefit credentials without relying on sugar-driven palatability. Glucuronolactone's neutral flavor profile and demonstrated co-formulant compatibility with caffeine and taurine, validated at 2,400 mg/liter by the European Food Safety Authority (EFSA), make it ideally suited for these cleaner formulations[1]Source: European Union, "Energy Drinks Consumption in Minors: EU and National Approaches," europarl.europa.eu. The ingredient benefits from a regulatory tailwind here: products meeting EFSA's low-concern threshold for glucuronolactone face fewer reformulation constraints than those reliant on higher-dose stimulants.

Growing application in cognitive health and mental focus

Beyond gaming, glucuronolactone is attracting attention in the broader cognitive health supplement segment, which covers working professionals, students, and aging populations. Growing applications in cognitive health and mental focus are driving the expansion of the glucuronolactone market, particularly within the premium wellness product segment. Increasingly, the nutrition literature highlights the role of glucuronolactone in formulations designed to enhance alertness, concentration, and memory support. Recent nutrition literature has focused on glucuronolactone-containing combinations in products linked to alertness, concentration, and memory support, drawing interest from formulators targeting professionals, students, and older adults. The compound's conversion to glucuronic acid in the liver, subsequently deployed in central nervous system detoxification, provides a mechanistic link between hepatic health and cognitive performance, positioning glucuronolactone as a cross-category ingredient spanning liver-support and brain-health stacks. This dual positioning is emerging as a strategic advantage for formulators targeting the premium supplement tier, where consumers already pay a price premium for multi-function ingredients.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns associated with high-dose consumption | -0.7% | Global | Short term (≤ 2 years) |

| China-centric supply concentration and environmental compliance risk | -0.6% | Global supply chain; upstream risk | Medium term (2–4 years) |

| Growth of substitute functional ingredients | -0.5% | Global, strongest in North America and Europe | Long term (≥ 4 years) |

| Regulatory scrutiny on energy drinks | -0.4% | Europe and North America | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

China-centric supply concentration and environmental compliance risk

Supply for D-glucuronolactone is heavily concentrated in Shandong province, China, a geography facing accelerating environmental compliance pressure. The Shandong Expanded Emerging Pollutant Controls (effective February 2026) add new monitoring and audit obligations for chemical manufacturers, while Central Environmental Inspection findings cited 7 chemical enterprises in Shandong for violations, including illegal expansion within protected river-management zones[2]Source: Ministry of Ecology and and Environment, "China’s Policies and Actions for Addressing Climate Change 2025 Annual Report," english.mee.gov.cn. For global buyers, this creates a dual risk: episodic supply disruption when non-compliant facilities are ordered to halt operations, and a sustained cost pass-through from producers investing in wastewater treatment and emissions controls. To mitigate these challenges, global buyers are exploring alternative sourcing options, particularly from Indian manufacturers such as Aadhunik Industries, Muby Chemicals, and Anmol Chemicals. However, diversification efforts remain limited, as China continues to dominate production, making it difficult to fully offset the risks associated with its supply concentration.

Regulatory scrutiny on energy drinks

Energy drink regulation remains a direct restraint, as this category still accounts for the largest share of applications in the glucuronolactone market. A regulatory wave across Europe is directly constraining the market that accounts for the largest share of glucuronolactone demand. Poland banned the sale of energy drinks to minors effective January 2024; Romania enacted a similar measure in 2024; Hungary and Bulgaria followed in mid- and late-2025, respectively; and the UK Department of Health and Social Care opened a consultation in September 2025 on banning sales to under-16s[3]Source: UK Department of Health and Social Care, “Banning the Sale of High-Caffeine Energy Drinks to Children,” gov.uk. These actions do not remove glucuronolactone from formulations, but they narrow the available consumer base for traditional high-caffeine delivery formats. Brands are responding by shifting toward adult-positioned beverages and sugar-reduced launches that soften the classic energy drink image. That helps demand hold up, but it also raises development costs and slows volume growth in some European markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Liquid Gains Speed as RTD Demand Expands

Powder held 64.27% of the glucuronolactone market share in 2025, reflecting its long-standing role in capsules, tablets, stick packs, and bulk premixes used by beverage manufacturers. The format remains favored because it is easier to ship, simpler to store, and more precise for dosing in pharmaceutical-grade and supplement production. The powder form offers extended shelf life and stability, making it a preferred choice for manufacturers aiming to maintain product quality over time. Its versatility in blending with other ingredients further enhances its adoption across applications such as energy drinks, dietary supplements, and functional foods. The powder segment also benefits from cost-effectiveness in large-scale production, which appeals to manufacturers seeking to achieve competitive pricing in the market.

Liquid is projected to grow at a 6.1% CAGR through 2031, placing it ahead of both the total glucuronolactone market and the powder segment. The faster growth stems from the strong shift toward ready-to-drink formats, especially zero-sugar energy beverages and functional shots. HOWTIAN Group, which produces 2,000 tons of D-glucuronolactone annually, explicitly promotes its liquid-compatible solubility and flavor neutrality as formulation advantages for Ready-to-Drink (RTD) beverage brands. The liquid-form advantage also extends to effervescent powders and stick-pack dissolvable formats targeted at sports recovery and gaming nutrition, both of which demand rapid dissolution.

By Application: Supplements Narrow the Gap With Energy Drinks

Energy Drinks accounted for 42.38% of the glucuronolactone market in 2025, and this leadership still reflects the ingredient’s deep integration with caffeine and taurine in mainstream formulations. The segment benefits from scale, as large beverage brands continue to expand distribution and refresh product lines across focus, hydration, and recovery occasions. Pharmaceuticals, Cosmetics and Personal Care, and Food and Beverages remain smaller applications, yet they add stability because their demand is tied to different performance claims and purchasing cycles. This mix keeps the glucuronolactone market from relying entirely on one end use, even though beverages still set the pace.

Dietary Supplements and Nutraceuticals is forecast to grow at 7.28% CAGR through 2031, making it the fastest-growing application in the glucuronolactone market size. Growth is supported by new delivery formats such as gummies, functional drinks, and effervescent tablets, which broaden consumer access and align with the premium side of the glucuronolactone industry. The rising consumer focus on health and wellness, coupled with increasing awareness of glucuronolactone's potential benefits, such as detoxification and energy enhancement, is driving demand in this segment. Additionally, the growing trend of personalized nutrition and the adoption of glucuronolactone in formulations targeting specific health concerns, such as liver health and cognitive function, are further fueling its growth.

Geography Analysis

North America held 37.08% of the glucuronolactone market share in 2025, which made it the largest regional demand center. The United States drives most of that volume through its large energy drink base, mature sports nutrition retail network, and steady demand for daily wellness supplements. The partnership between Anheuser-Busch and 1st Phorm showed how closely energy beverages and sports nutrition are moving together in the market. The region also keeps an advantage over Europe because the United States does not have a federal age restriction or caffeine cap for energy drinks, which preserves a wider addressable base.

Asia-Pacific is projected to grow at a 6.25% CAGR through 2031, making it the fastest-growing regional market and the leading growth engine for the glucuronolactone market. China remains central because it combines a major manufacturing base with rising domestic demand for energy drinks, supplements, and pharmaceutical-grade intermediates. India is emerging as a secondary supply node, with domestic nutraceutical demand growing and local chemical producers widening their specialty ingredient offerings. Japan adds a premium channel because strict compliance with functional food and supplement regulations supports higher-value, pharmaceutical-grade sales. South America and the Middle East and Africa still contribute a smaller share today, but export-oriented distribution networks already active in these regions suggest a better platform for future glucuronolactone market expansion.

Europe remains an important market for food, pharmaceutical, and specialty ingredient demand, but regulations are becoming increasingly restrictive. By 2025, several European countries had already restricted the sale of energy drinks to minors, and the UK consultation published in September 2025 pointed to further pressure ahead. This is pushing innovation toward adult-focused functional beverages that retain the ingredient stack while softening the energy drink label. Jungbunzlauer’s 2025 move into Illinois also showed that European-headquartered suppliers are shifting production footprints outward to reduce regional concentration risk

Competitive Landscape

The glucuronolactone market remains moderatelty fragmented, with Chinese producers competing aggressively on price, volume, and available purity grades. Suppliers such as HOWTIAN Group, Foodchem International, Anhui Fubore, Hefei TNJ Chemical, Fengchen Group, and Zouping Mingxing operate in a competitive landscape where no single player dominates across all end uses. HOWTIAN has strengthened its position by pairing pharmaceutical-grade supply with sustainability messaging and auditable operations, appealing to Western buyers seeking traceable sourcing. European-origin suppliers such as Jungbunzlauer, Roquette, and Merck KGaA compete from the premium end by offering broader application portfolios, regulatory support, and established customer relationships.

Jungbunzlauer’s November 2025 acquisition of an Illinois manufacturing facility marked a significant strategic move, providing the company with its first U.S. production site and supporting supply-chain localization. Its earlier acquisition of Alliance Gums and Industries in 2024 further demonstrated a broader plan to enhance formulation capabilities across beverage and nutrition applications. Smaller players such as Actylis and Niran Bio are focusing on service depth, regional access, and fine-chemical specialization rather than engaging in direct price wars. Certification standards such as ISO 22000 and FSSC 22000 are also becoming increasingly critical, raising the entry bar for suppliers lacking comprehensive food and supplement compliance infrastructure.

The primary opportunity for future competition lies in application-specific formulation work rather than expanding bulk commodity capacity. Controlled-release formats, premium recovery products, and multifunction supplement blends offer suppliers a better chance to differentiate themselves than relying solely on bulk sales. This is particularly important as buyer procurement power remains strong, keeping margins under pressure across much of the glucuronolactone market. Suppliers that combine purity assurance, documentation support, and formulation guidance are better positioned than those competing solely on price. Consequently, the market remains active and competitive, with limited technical differentiation today but clear potential for branded ingredient strategies in the future.

Glucuronolactone Industry Leaders

-

Jungbunzlauer Suisse AG

-

Roquette Frères

-

Merck KGaA (MilliporeSigma)

-

Foodchem International Corporation

-

Hubei Yitai Pharmaceutical Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Monster Energy launched new patriotic summer flavors, including Juice Monster Strawberry Lemonade and Ultra Red, White & Blue Razz, in celebration of America's 250th birthday. The brand uses glucuronolactone and caffeine in its energy drink lines to help reduce fatigue, enhance cognitive focus, and support metabolic detoxification.

- November 2025: Jungbunzlauer acquired a manufacturing facility in Thomson, Illinois, from International Flavors and Fragrances, marking the company's first U.S. production site. The site supports its broader specialty ingredient portfolio and forms part of its North American supply-chain localization strategy

- March 2024: Nutraceutical Corporation, a leading manufacturer and marketer of nutritional and dietary supplements, launched a new product line, "GlucoFlex," containing Glucuronolactone. This innovative supplement was designed to support joint health and overall wellness. The product was launched in response to increasing consumer demand for natural health solutions.

Global Glucuronolactone Market Report Scope

Glucuronolactone is a naturally occurring carbohydrate and a byproduct of glucose metabolism in the human liver. It is primarily known as a popular ingredient in energy drinks and dietary supplements, added to help combat fatigue and support cognitive performance.

The glucuronolactone market is segmented by form, application, and geography. Based on form, the market has been segmented into powder and liquid. By application, the market is segmented into energy drinks, dietary supplements and nutraceuticals, pharmaceuticals, cosmetics and personal care, and food and beverage. By geography, the market has been segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done based on value (USD).

| Powder |

| Liquid |

| Energy Drinks |

| Dietary Supplements and Nutraceuticals |

| Pharmaceuticals |

| Cosmetics and Personal Care |

| Food and Beverage |

| North America | United States |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Form | Powder | |

| Liquid | ||

| By Application | Energy Drinks | |

| Dietary Supplements and Nutraceuticals | ||

| Pharmaceuticals | ||

| Cosmetics and Personal Care | ||

| Food and Beverage | ||

| By Geography | North America | United States |

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the expected value of glucuronolactone market by 2031?

The glucuronolactone market is forecast to reach USD 478.38 million by 2031, up from USD 378.05 million in 2026, at a 4.82% CAGR over 2026-2031.

Which application leads current demand for glucuronolactone?

Energy drinks lead current demand, with a 42.38% share in 2025, because the ingredient remains a standard part of mainstream stimulant and functional beverage formulations.

Why is liquid glucuronolactone gaining traction?

Liquid is forecast to grow at 6.06% CAGR because zero-sugar ready-to-drink launches and functional shots are creating more demand for soluble, neutral-flavor ingredients.

Which region is the largest buyer today?

North America is the largest regional buyer, with 37.08% share in 2025, supported by a large U.S. energy drink base and well-developed sports nutrition retail channels.

Page last updated on: