Gelato Market Size and Share

Market Overview

| Study Period | 2026 - 2031 |

|---|---|

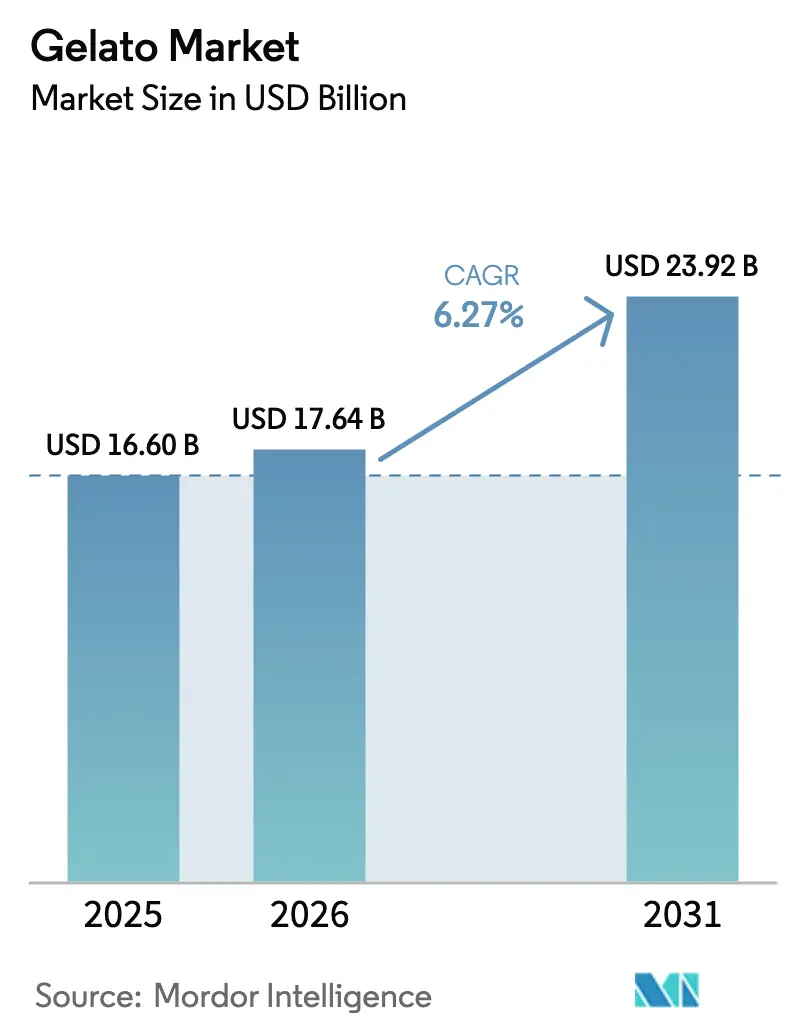

| Market Size (2026) | USD 17.64 Billion |

| Market Size (2031) | USD 23.92 Billion |

| Growth Rate (2026 - 2031) | 6.27% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gelato Market Analysis by Mordor Intelligence

The Global Gelato market size was valued at USD 16.6 billion in 2025 and estimated to grow from USD 17.64 billion in 2026 to reach USD 23.92 billion by 2031, at a CAGR of 6.27% during the forecast period (2026-2031). This upward trajectory underscores gelato's transformation from a seasonal treat to a coveted year-round dessert, fueled by a growing consumer preference for artisanal quality and unique flavors that set gelato apart from traditional ice cream. Gelato's dual identity as a cherished European tradition and a rising global trend makes it appealing globally. Notably, authentic Italian gelato, often certified and driven by tourism, is making significant inroads into international markets.

Key Report Takeaways

- By product type, dairy-based gelato held a share of 84.65% in the global gelato market in 2025, while dairy-free/plant-based gelato is anticipated to record a CAGR of 7.18% through 2031.

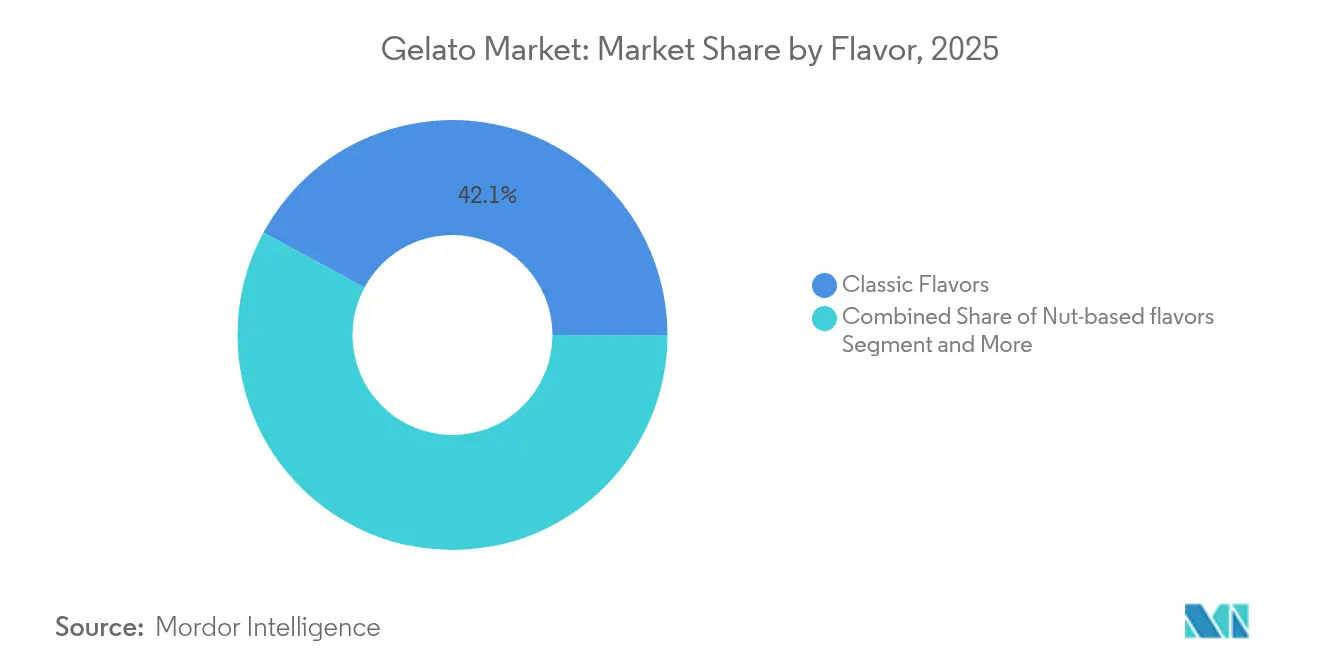

- By flavor, classic flavors like chocolate and vanilla command a 42.10% market share in 2025, and gourmet and limited edition flavors are set to grow at a robust 9.69% CAGR through 2031.

- By production method, industrial gelato production commands a 57.95% market share in 2025, and Artisanal gelato production is fueling a market growth at a 5.62% CAGR through 2031.

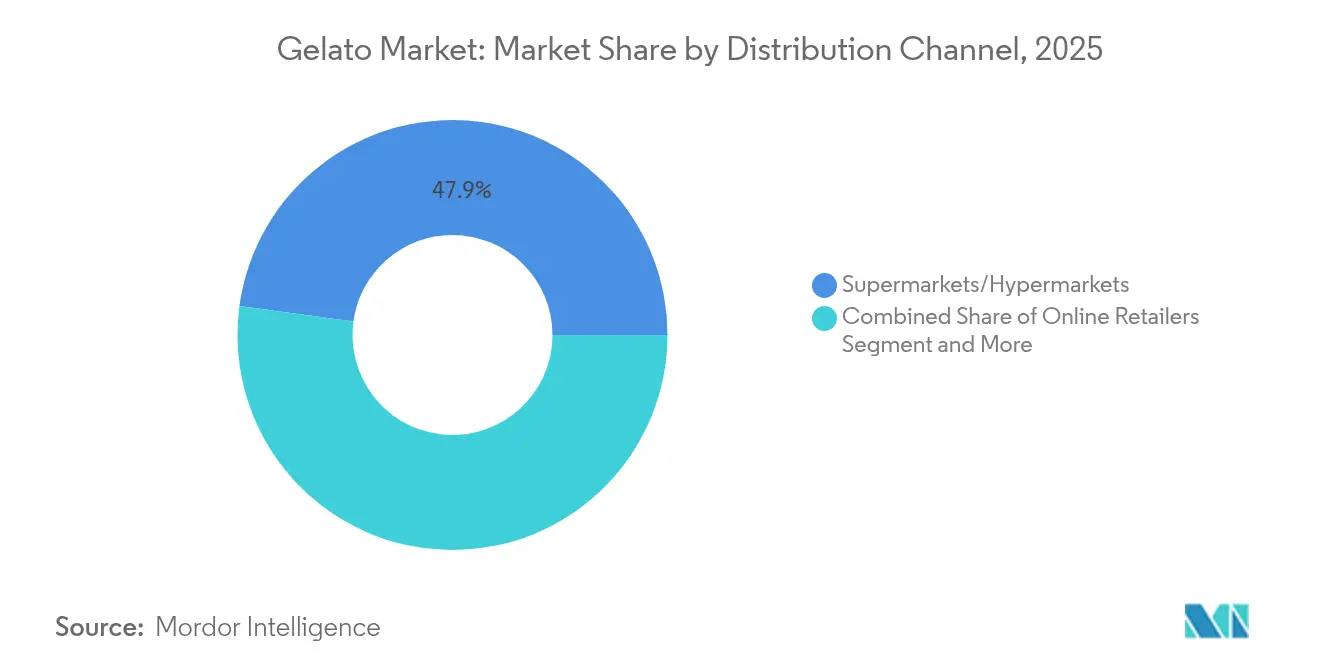

- By distribution channel, supermarkets and hypermarkets capture a 47.85% market share in 2025, and online retailers are projected to grow with a CAGR of 9.18%, through 2031.

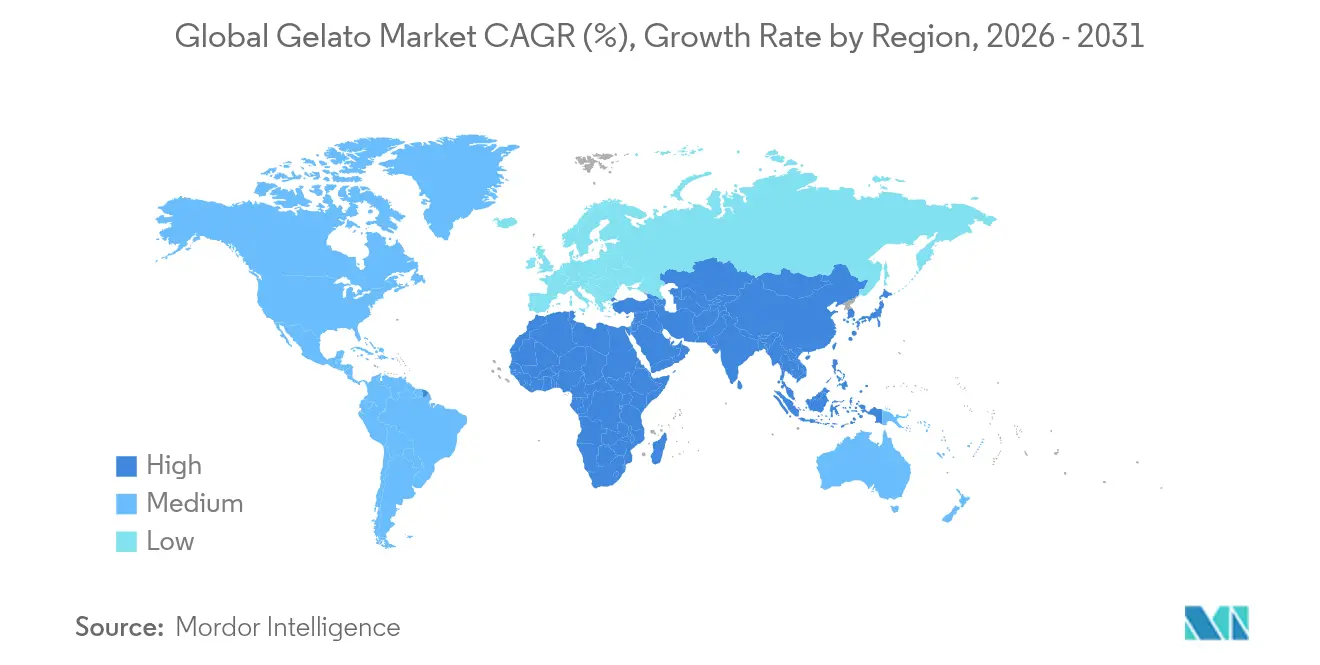

- By region, Europe commands a dominant 43.20% market share in 2025, and Asia-Pacific is rapidly climbing the ranks, with a projected CAGR of 7.49% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gelato Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer appetite for premium artisanal desserts | +1.5% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Expansion of supermarket/private-label gelato ranges | +1.2% | North America & Europe, expanding to APAC | Short term (≤ 2 years) |

| Rapid uptake of vegan & dairy-free gelato SKUs | +0.8% | Global, led by North America & Northern Europe | Medium term (2-4 years) |

| IoT-enabled batch freezers boosting in-store productivity | +0.6% | Europe & North America, early adoption in APAC | Long term (≥ 4 years) |

| Night-time delivery apps driving after-dark consumption | +0.4% | Urban centers globally, concentrated in Europe & APAC | Short term (≤ 2 years) |

| Tourism-driven "authentic Italian gelato" certification exports | +0.3% | Global, with emphasis on emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Appetite for Premium Artisanal Desserts

The consumption of premium, artisanal gelato has surged with increase in consumers' willingness to invest in genuine, artisanal experiences. This trend isn't confined to traditional European markets; even in Southeast Asia, a notable 77% of consumers express a willingness to pay a premium for gourmet ingredients in their frozen desserts[1]Gaynor Selbey, Food Ingredients First, 'Cargill Indulgence Study' , June 2025, www.foodingredientsfirst.com. Artisanal gelato garners attention not just for its rich flavors but also for its perceived health advantages, boasting a lower fat content compared to conventional ice cream and a commitment to natural ingredients. This premium positioning, rooted in authentic craftsmanship, offers a competitive edge that's challenging for industrial producers to mimic, firmly establishing artisanal gelato as a unique category, distinct from mere premium ice cream. This surge in demand for artisanal gelato is also supported by health-conscious consumers seeking lower-fat and more natural dessert options, as well as the influence of food media and social trends that celebrate culinary craftsmanship and experiential dining.

Expansion of Supermarket/Private-Label Gelato Ranges

Supermarket chains are swiftly broadening their private-label gelato selections, responding to surging consumer demand and aiming to boost profit margins. Major chains and hypermarkets are prominently showcasing high-quality private-label gelato, including artisanal and non-dairy varieties. This allows shoppers to effortlessly blend these gourmet treats into their routine grocery hauls. Such a move not only democratizes access to upscale gelato but also positions retailers to capitalize on the premiumization trend with unique store-brand offerings. Additionally, supermarket chains are collaborating with manufacturers to diversify their product lines. A case in point: Auchan Portugal, teaming up with the local brand O Gelado, has rolled out a new vegan banana-coconut ice cream SKU in 2025. Auchan Portugal also states that its private-label products constitute 40% of its sales in 2024,[2]Expresso, '40% of our revenue comes from our own brand,' says the general director of Auchan Portugal', March 2025, expresso.pt with a notable 85% sourced from local Portuguese suppliers. This strategy is a direct response to consumer desires for convenience, value, and quality. Through this private-label expansion, retailers are not just providing premium gelato at competitive prices but are also cultivating customer loyalty with exclusive offerings absent from competitor shelves. The rapid growth of supermarkets and private-label gelato selections is transforming the market, driven by retailers' aspirations to offer premium dessert options.

Rapid Uptake of Vegan & Dairy-Free Gelato SKUs

Driven by a shift towards plant-based diets and ethical consumption, the global gelato market is witnessing a robust rise in the adoption of vegan and dairy-free offerings. As brands innovate with bases like oat, almond, and coconut, they're catering to a growing demand for indulgent yet cleaner-label alternatives. This surge in popularity is not just a fleeting trend; heightened awareness around lactose intolerance, animal welfare, and environmental concerns has thrust vegan gelato into the mainstream, branding it as a guilt-free luxury. Major players, from Magnum's pea-protein line to artisanal gelaterias like Van Leeuwen in the U.S. and Europe's Amorino (which recently transitioned all its sorbets and gelatos to vegan and gluten-free), are rolling out enticing flavors like cashew-based chocolate fudge and turmeric-spiced gelatos. With rising dietary restrictions and environmental consciousness influencing buying decisions, vegan gelato is set to dominate freezer cases in retail and HoReCa channels. This trend not only accelerates the premiumization of gelato but also supports higher price points, allowing both established and emerging brands to carve out a distinct identity in the market.

IoT-Enabled Batch Freezers Boosting In-Store Productivity

IoT-enabled batch freezers are transforming in-store gelato production, enhancing operational efficiency and ensuring quality. These advancements are shifting gelato retail from a traditional artisan craft to a modern, tech-driven food service. These state-of-the-art freezers, outfitted with sensors, monitor key metrics like temperature, humidity, motor performance, and batch cycle times. This capability facilitates real-time data capture and cloud connectivity. As a result, store managers and technicians can oversee operations remotely, anticipate maintenance needs, and avert spoilage. Such real-time insights minimize the need for manual temperature checks and reactive maintenance, leading to reduced downtime and ensuring each batch aligns with brand-specific texture and flavor standards. Furthermore, features like digital controls, self-cleaning cycles, and programmable batch schedules in IoT batch freezers enable businesses to streamline production workflows. This ensures a swift delivery of consistent, high-quality gelato during peak demand, all while minimizing labor strain. Strategically, the enhanced data insights—such as trends in machine energy usage and mean time between failures (MTBF)—empower gelato retailers to adopt predictive maintenance and fine-tune supply planning. This not only curbs food waste but also hastens return on investment (ROI). These freezers allow gelato retailers to harmoniously merge tradition with technology, elevate in-store productivity, uphold premium quality, and sustainably expand production in a fiercely competitive landscape.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile dairy & sugar commodity prices | -0.8% | Global, with acute impact in price-sensitive markets | Short term (≤ 2 years) |

| Strong seasonality in temperate climates | -0.6% | North America & Europe, moderate impact in APAC | Medium term (2-4 years) |

| Shortage of skilled gelato artisans | -0.4% | Europe & North America, emerging in APAC | Long term (≥ 4 years) |

| Energy-intensive cold-chain under decarbonisation mandates | -0.3% | Europe & North America, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Dairy & Sugar Commodity Prices

Global gelato producers grapple with a significant challenge: the volatility of dairy and sugar prices. These fluctuations not only influence production costs but also the overall stability of the gelato market. Gelato's hallmark is its use of high-quality, fresh dairy and premium sugars, making it particularly vulnerable to shifts in these commodity markets. Notably, only about 9% of the international dairy market's total production is traded globally[3]Food and Beverage Expo, Chennai Trade Centre, December 2024, www.fnbexpo.biz. This limited trading volume renders prices highly sensitive to various shocks, be it from supply-demand imbalances, policy shifts, or broader economic changes. Also, farmgate milk prices, closely tied to commodity prices for products like butter and skimmed milk powder, often face short-term lags and divergences. These discrepancies arise from seasonality and supply chain inefficiencies, posing challenges for gelato producers who depend on consistent, high-quality milk and cream. On the sugar front, global prices are similarly volatile. They're swayed by factors like weather events, trade policies, and government actions, including import restraints. Such dynamics can result in abrupt changes to input costs. Moreover, gelato's perishability and the critical need for efficient cold-chain logistics intensify the repercussions of cost volatility. Any supply chain disruption or price surge can swiftly impact retail prices or profit margins. While market players pivot towards innovation, diversification, and sustainable sourcing to counter these challenges, the specter of volatile dairy and sugar prices looms large, influencing the trajectory of gelato producers globally.

Strong Seasonality in Temperate Climates

Gelato parlors and artisanal producers in temperate climates face significant challenges from strong seasonal demand fluctuations, making it difficult to achieve steady, year-round revenue. During the warmer spring and summer months, gelato sales surge as consumers seek cold, refreshing desserts, but as temperatures drop in autumn and winter, demand plummets, resulting in underutilized production capacity and uneven income streams. This seasonality is especially tough for smaller producers who often lack diversified product portfolios, making it harder to attract customers in the colder months. To adapt, many expand their offerings to include warm desserts, seasonal beverages, and comforting flavors that appeal to winter preferences, as well as rotate their menus to feature ingredients that are seasonally available—such as floral and fruity flavors in spring, tropical tastes in summer, spiced options in fall, and rich, indulgent profiles in winter. While this approach drives product innovation and marketing creativity, it also adds operational complexity and may not be feasible for all businesses due to resource constraints. The impact of seasonality extends throughout the supply chain, as suppliers and distributors must adjust to erratic order volumes and fluctuating demand for cold-chain logistics, often leading to inefficiencies and higher costs during off-peak periods. Producers in regions with harsh winters also face the risk of product spoilage or waste, since unsold gelato is difficult to store long-term without compromising quality, potentially resulting in financial losses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Flavor: Gourmet Innovation Outpaces Classic Preferences

In 2025, Classic flavors like chocolate and vanilla command a 42.10% market share. Their dominance is rooted in widespread consumer familiarity and unwavering demand, resonating across diverse age groups and global markets. Bolstered by well-entrenched supply chains and stable ingredient costs, these classic flavors enjoy a universal allure, streamlining their mass production and distribution. Serving as foundational offerings, these classics empower gelato producers to cement their market presence, paving the way for ventures into bolder, innovative flavor territories.

Through 2031, gourmet and limited edition flavors are set to grow at a robust 9.69% CAGR, fueled by consumers' thirst for unique experiences and the allure of innovative flavor combinations spotlighted on social media. Belgian gelato artisans, like Carpigiani, are pushing boundaries with inventive offerings such as beeswax gelato, stinging nettle pesto, smoked fiordilatte, and a unique blue cheese paired with pear. Nut-based flavors are riding the wave of premium ingredients and a health-centric orientation. Meanwhile, fruit flavors leverage their seasonal nature and a clean-label appeal, striking a chord with health-conscious consumers. Options that are functional and reduced in sugar cater to specific dietary needs, yet retain an indulgent allure. This creates niche markets that not only command premium pricing but also foster customer loyalty through their specialized positioning.

By Production Method: Artisanal Craft Gains Premium Positioning

In 2025, industrial gelato production commands a 57.95% market share, leveraging economies of scale, stringent quality control, and efficient distribution to penetrate markets at competitive prices. By harnessing advanced equipment, standardized formulations, and an optimized supply chain, industrial methods not only cut production costs but also uphold food safety standards. This large-scale production approach facilitates seasonal inventory management and fosters private-label collaborations with major retail chains, ensuring consistent product availability.

Artisanal gelato production is fueling a premium market growth at a 5.62% CAGR through 2031. This surge underscores consumers' readiness to invest more for genuine craft experiences and richer flavor profiles. While the sector grapples with a demand for 15,000-20,000 front-of-house staff, it continues to thrive, introducing innovative flavors like 'Reverse' Stracciatella and health-centric options such as plant-based and sugar-free gelatos, appealing to a broad consumer base. Artisanal methods allow for tailored creations, seasonal ingredient use, and distinctive flavor innovations. These attributes set them apart from industrial processes, cementing a sustainable premium stance that justifies elevated margins, even with the challenges of heightened operational intricacies and a demand for skilled labor. Institutions like Carpigiani Gelato University, ICIF, and Gelateneo play a pivotal role in nurturing these artisanal skills, ensuring quality consistency on a global scale. Moreover, technology is enhancing artisanal methods without overshadowing them. For instance, blockchain tracking systems are pioneering pay-per-use equipment models, lightening the capital load for smaller producers while upholding stringent quality benchmarks.

By Distribution Channel: Online Acceleration Transforms Retail Dynamics

In 2025, supermarkets and hypermarkets capture a 47.85% market share, thanks to their established cold-chain infrastructure, extensive consumer reach, and prowess in developing private labels. These advantages not only allow for competitive pricing but also ensure consistent product availability. Such channels adeptly harness impulse buying, enjoy promotional leeway, and seamlessly integrate into broader grocery shopping habits, bolstering regular customer visits. Meanwhile, traditional retail channels leverage product sampling, eye-catching merchandising, and the allure of immediate gratification, all of which play pivotal roles in influencing consumers' premium gelato choices.

Driven by a rising consumer appetite for convenience and premium frozen desserts, online retailers are swiftly carving out a dominant position, with a CAGR of 9.18% in the global gelato market. The surge of e-commerce platforms and food delivery services has empowered consumers to enjoy gelato from home, sidestepping the seasonal and geographical constraints of traditional gelato parlors. Catering to modern lifestyles, online sales are booming, offering a smooth purchasing journey with enticing options like same-day or scheduled deliveries, especially favored by urbanites and busy families. Technological strides in low-temperature storage and transport bolster this trend, safeguarding gelato's quality during transit. Consequently, online platforms are not just amplifying the reach of artisanal and premium gelato brands; they're also leveling the playing field for smaller producers, granting them access to new customer segments in a fiercely competitive market.

By Product Type: Plant-Based Innovation Challenges Dairy Dominance

Dairy-based gelato continues to hold the position as the largest segment with 84.65% share in 2025, firmly rooted in tradition and consumer preference for its creamy texture, rich mouthfeel, and authentic Italian heritage. This segment is characterized by its reliance on high-quality milk and cream, often sourced locally or from specialty dairies, which appeals to consumers seeking premium dessert experiences. The enduring popularity of dairy-based gelato is further supported by a wide array of classic and innovative flavors, ranging from traditional chocolate and pistachio to unique regional specialties. Despite growing health consciousness, consumers remain loyal to dairy gelato for its taste and indulgent qualities, and producers have responded with offerings such as low-fat, organic, and functional variants to cater to evolving dietary preferences.

In contrast, the dairy-free or plant-based gelato segment is emerging as the fastest-growing category, growing at 7.18% CAGR through 2031, driven by shifting consumer lifestyles, rising rates of lactose intolerance, and the increasing adoption of vegan and flexitarian diets worldwide. This segment leverages plant-based milks such as almond, coconut, oat, and cashew to replicate the creamy texture and flavor complexity of traditional gelato, while also introducing innovative flavors and functional benefits like lower sugar or added protein. The rapid expansion of dairy-free gelato is fueled by a growing demand for clean-label, allergen-free, and environmentally sustainable products, with younger consumers and urban populations showing particular enthusiasm for these alternatives. Also, ongoing advancements in food technology and ingredient sourcing continue to improve the quality and accessibility of dairy-free gelato, positioning this segment as a formidable challenger to dairy’s dominance and a key driver of future market growth.

Geography Analysis

In 2025, Europe commands a dominant 43.20% market share. Italy's rich cultural heritage and Germany's expanding retail landscape, supported the growth of the segment. Europe's lead is bolstered by a long-standing artisanal gelato tradition, a strong consumer preference for authentic, locally-sourced ingredients, and a vibrant tourism sector that ensures year-round consumption. Highlighting the premium nature of European gelato, Princess Cruises, endorsed by the Italian Chamber of Commerce's Ospitalità Italiana, made history as the first cruise line to offer authentic Italian gelato on board. Even as European markets face challenges like a shortage of 15,000-20,000 front-of-house staff and rising raw material costs, they thrive, buoyed by a premium positioning and a strong tourism influx. Furthermore, there's a noticeable uptick in organic, vegan, and functional gelato innovations, underscoring shifting consumer preferences and driving growth and diversification.

Asia-Pacific is rapidly climbing the ranks, with a projected CAGR of 7.49% through 2031. Countries like China, Japan, India, and South Korea are witnessing a surge in demand, driven by rising disposable incomes, swift urbanization, and a growing affinity for Western culinary trends. In Southeast Asia, consumers are becoming more discerning: 77% are open to splurging on gourmet ingredients, and 45% indulge in ice cream daily. The region's tropical climate supports year-round consumption, and a growing middle class, with increasing disposable income and improved cold-chain infrastructure, is driving market expansion beyond just urban centers. The region's enthusiasm for premium and innovative flavors—such as matcha, black sesame, and tropical fruit infusions—has led manufacturers to set up new sales points in shopping malls, supermarkets, and online platforms, further boosting market growth and diversification.

North America, South America, and the Middle East & Africa present a tapestry of opportunities, each influenced by distinct economic, infrastructural, and cultural factors. North America features a robust retail landscape and a consumer base familiar with premium frozen desserts. Yet, the region's temperate climate introduces seasonality challenges, pushing for strategic year-round marketing. In South America, Brazil and Argentina shine, with their growing middle class and rising tourism driving a thirst for authentic gelato experiences. Meanwhile, the Middle East & Africa, amidst their economic growth and urbanization, are nurturing a taste for premium frozen desserts. However, these regions face challenges: infrastructure limitations and climate issues necessitate a customized approach to cold-chain management and marketing strategies tailored to the seasons.

Competitive Landscape

The gelato market, with a moderate fragmentation level of 5 out of 10, fosters competitive dynamics that benefit both established multinationals and emerging artisanal producers through distinct positioning strategies. Major players like Unilever, Nestlé, and Ferrero harness scale advantages in ingredient sourcing, distribution, and marketing. In contrast, smaller artisanal producers carve out premium segments, emphasizing craft authenticity and localized flavor innovations. Unilever's move to spin off its EUR 7.9 billion ice cream division, which boasts brands like Ben & Jerry's and Magnum, by the end of 2025, hints at potential industry consolidation. This standalone entity aims for operational flexibility and growth.

Moreover, technological advancements, including IoT-driven production, blockchain supply chain tracking, and automated quality control, are reshaping the industry. These innovations not only streamline labor but also uphold consistency standards. Equipment manufacturers like Carpigiani and Technogel are at the forefront, introducing compact batch freezers, pay-per-use models, and integrated pasteurization systems, making professional-grade gelato production more accessible.

As consumer preferences shift towards health-conscious indulgence, opportunities arise in plant-based formulations, functional ingredients, and optimized packaging. New entrants are harnessing direct-to-consumer models, subscription services, and social media to bolster brand awareness and loyalty, sidestepping traditional retail investments. This strategy intensifies competitive pressure on established players, urging them to rethink distribution and consumer engagement tactics.

Gelato Industry Leaders

Unilever PLC

SONNENBLUME SAS (SUSO)

Hackney Gelato Limited

Remeo Gelato

Crosta & Mollica Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Valsoia, a plant-based brand from Italy, has launched four new frozen desserts in Malta, touting them as creamy, flavorful, and crafted from premium plant-based ingredients. The new lineup features Valsoia's pistachio, stracciatella, and lemon cake gelatos, all in pint sizes, alongside their no-added-sugar fruit cups.

- June 2025: ITC Hotels has unveiled Yura, its inaugural in-house gelato brand, setting a new benchmark in India's premium-luxury hospitality scene. With a focus on sustainability and innovation, Yura seeks to transform the landscape of artisanal frozen desserts.

- January 2025: Unilever has unveiled its 2025 ice cream lineup, rolling out an array of flavours under its renowned brands, such as Talenti, Breyers, Popsicle, Good Humor, Magnum, and Klondike. The latest additions include bakery-inspired gelato, s’mores-themed delights, and character-branded frozen treats. Notably, Talenti Gelato Layers is broadening its horizons with three new bakery-inspired flavours, all presented in the brand’s signature clear jar. One standout, the chocolate chip cookie batter flavour, artfully melds chocolate chip cookie gelato with shortbread cookie pieces, cookie batter, vanilla gelato, and a chocolate cookie base.

Global Gelato Market Report Scope

| Dairy-Based Gelato |

| Dairy-Free/Plant-Based Gelato |

| Classic Flavors (Chocolate, Vanilla) |

| Nut-based Flavors |

| Fruit Flavors |

| Gourmet & Limited Edition |

| Functional & Reduced Sugars |

| Industrial Gelato |

| Artisinal Gelato |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Speciality Stores |

| Food Service/HoReCa |

| Online Retailers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Dairy-Based Gelato | |

| Dairy-Free/Plant-Based Gelato | ||

| By Flavor | Classic Flavors (Chocolate, Vanilla) | |

| Nut-based Flavors | ||

| Fruit Flavors | ||

| Gourmet & Limited Edition | ||

| Functional & Reduced Sugars | ||

| By Production Method | Industrial Gelato | |

| Artisinal Gelato | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Speciality Stores | ||

| Food Service/HoReCa | ||

| Online Retailers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size and projected growth of the global gelato market through 2031?

The global gelato market is valued at USD 17.64 billion in 2026 and is projected to reach USD 23.92 billion by 2031, registering a CAGR of 6.27% during the forecast period (2026-2031). This growth is driven by premium artisanal dessert trends and plant-based innovation.

How are plant-based and dairy-free gelato segments disrupting traditional dairy-based market dynamics?

In 2025, dairy-based gelato commands an 84.65% market share, yet plant-based alternatives are surging ahead, boasting the fastest segment growth at a robust 7.18% CAGR projected through 2031. Companies such as Perfect Day and Mwah! are unveiling formulations, both dairy-identical and cashew-based, that not only mimic the classic texture but also present enhanced nutritional benefits.

Which regions are leading and which are growing fastest in the gelato market?

Europe, particularly Italy, remains the largest and most mature market, holding a dominant share due to its deep-rooted gelato culture. North America is also significant, while Asia-Pacific is emerging as the fastest-growing region, driven by urbanization, rising incomes, and Westernized dietary habits.

How is gelato different from regular ice cream?

Gelato, crafted with natural ingredients and boasting a lower fat content, offers a denser texture and more intense flavor than standard ice cream, thanks to its reduced air and stabilizer content. This makes it particularly appealing to health-conscious consumers.

How do supermarket private-label expansions influence market share dynamics?

Major retailers including Albertsons, AWG Brands, and Weis Markets launched premium private-label lines in 2024, creating positive impact on CAGR forecast through competitive pricing and exclusive positioning.

Page last updated on: