Frozen Pizza Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

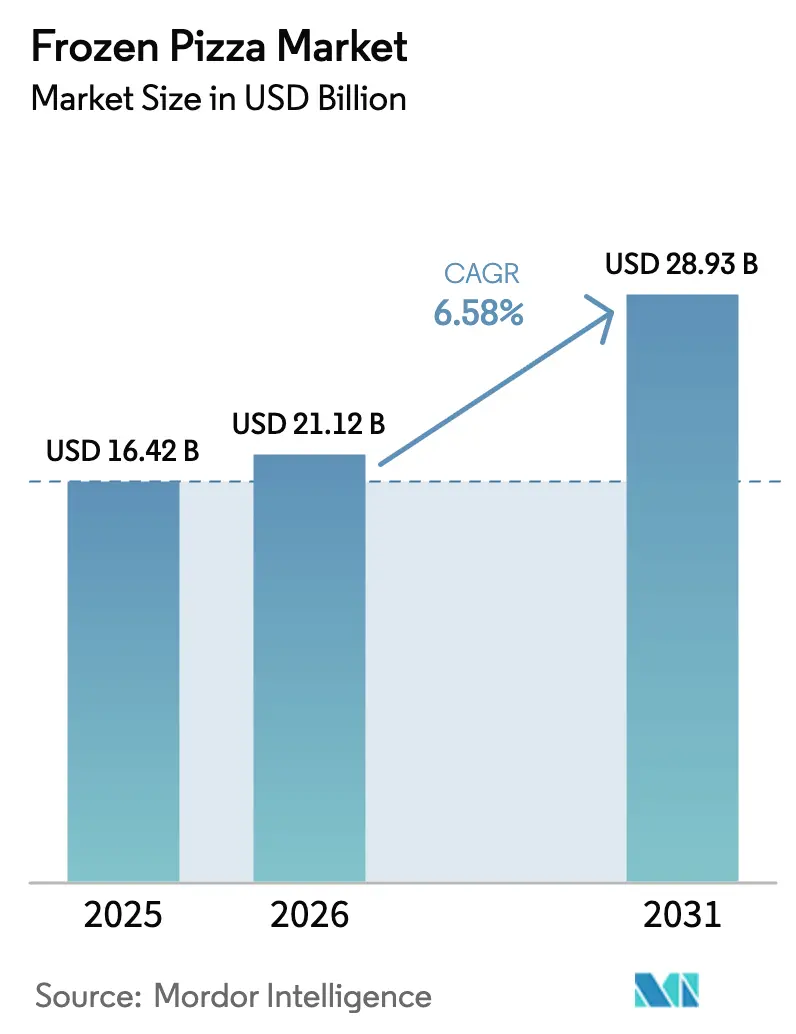

| Market Size (2026) | USD 21.12 Billion |

| Market Size (2031) | USD 28.93 Billion |

| Growth Rate (2026 - 2031) | 6.58% CAGR |

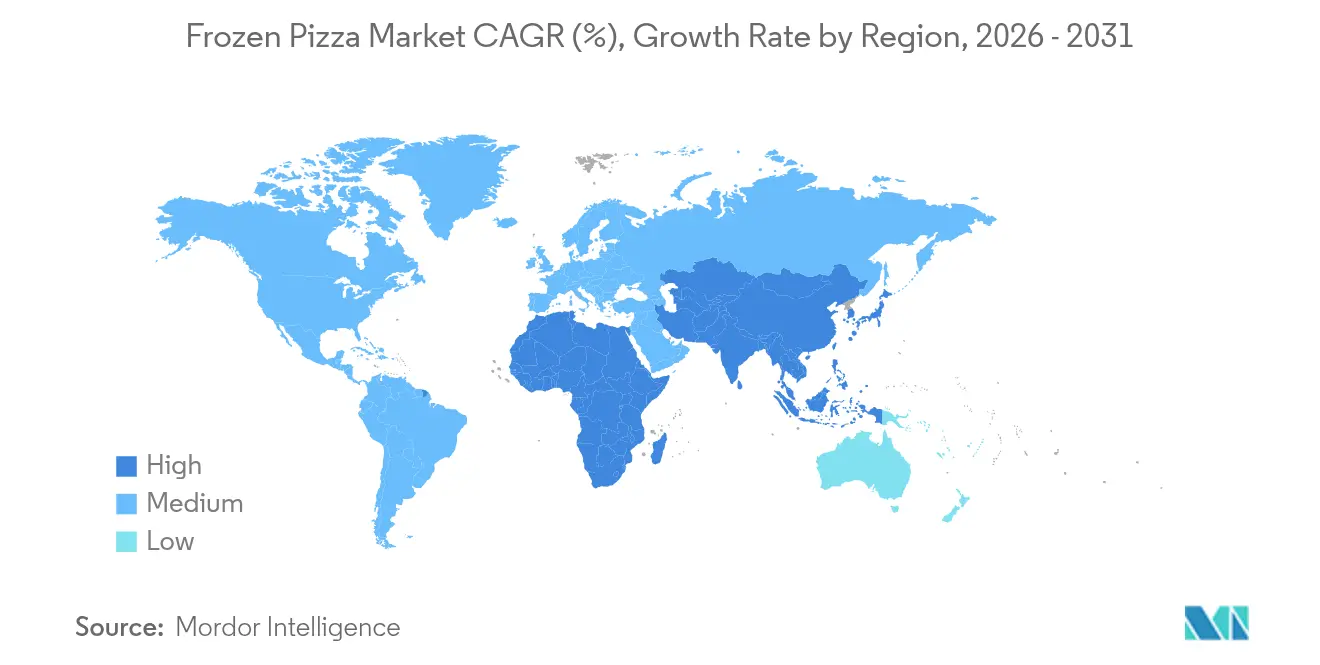

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Frozen Pizza Market Analysis by Mordor Intelligence

The frozen pizza market size is expected to increase from USD 16.42 billion in 2025 to USD 21.12 billion in 2026 and reach USD 28.93 billion by 2031, growing at a CAGR of 6.58% over 2026-2031. Household meal preparation is shifting toward ready-to-bake options as dual-income families seek convenient dinners that mimic restaurant quality. Premium crust formats, specialty toppings, and clean-label claims allow brands to charge higher unit prices without depressing volume. Rapid expansion of cold-chain logistics in emerging economies widens geographic reach and underpins long-term category growth. Retailers are broadening freezer assortments and experimenting with brisk on-the-go formats that compete directly with quick-service restaurants on speed. Consolidation remains limited, which encourages agile niche players to introduce differentiated offerings such as cauliflower crusts or hot-honey flavor profiles.

Key Report Takeaways

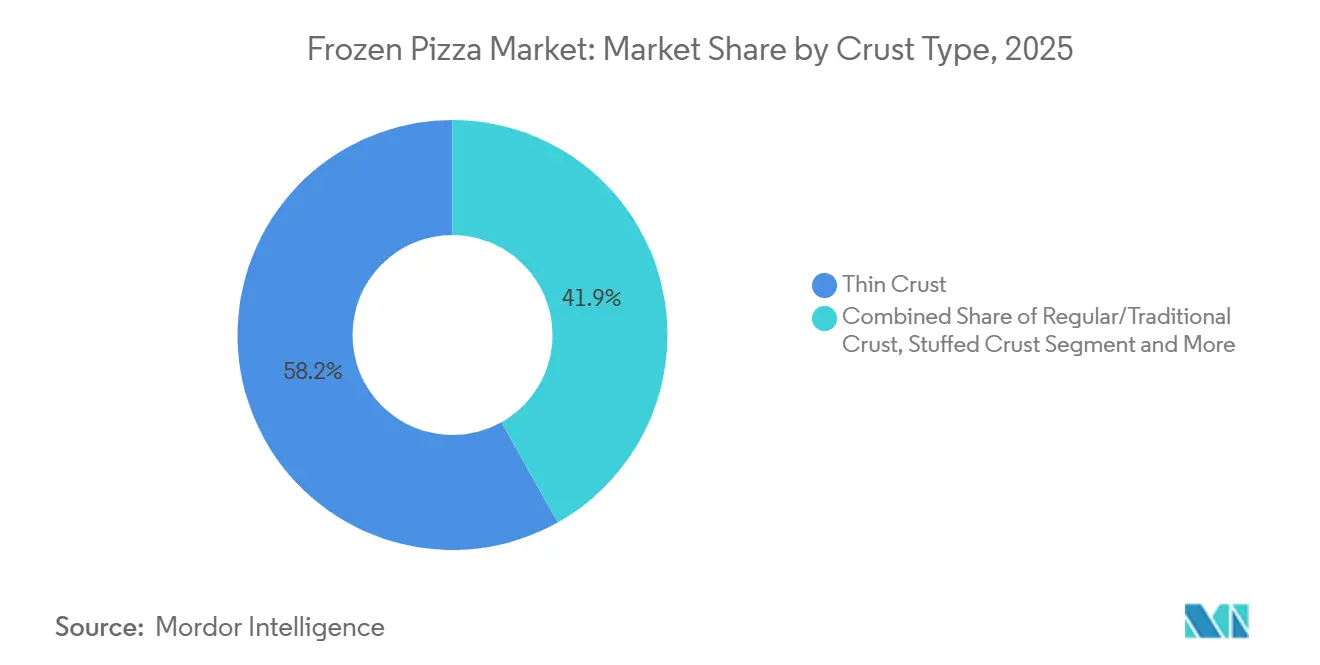

- By crust type, thin crust led with 58.15% of frozen pizza market share in 2025, while stuffed crust is forecast to expand at a 7.82% CAGR through 2031.

- By topping, meat-based combinations held 61.25% share of the frozen pizza market size in 2025, but vegan cheese toppings are projected to grow at an 8.11% CAGR to 2031.

- By category, conventional products accounted for 72.42% of 2025 volume, whereas free-from variants are advancing at a 7.94% CAGR through 2031.

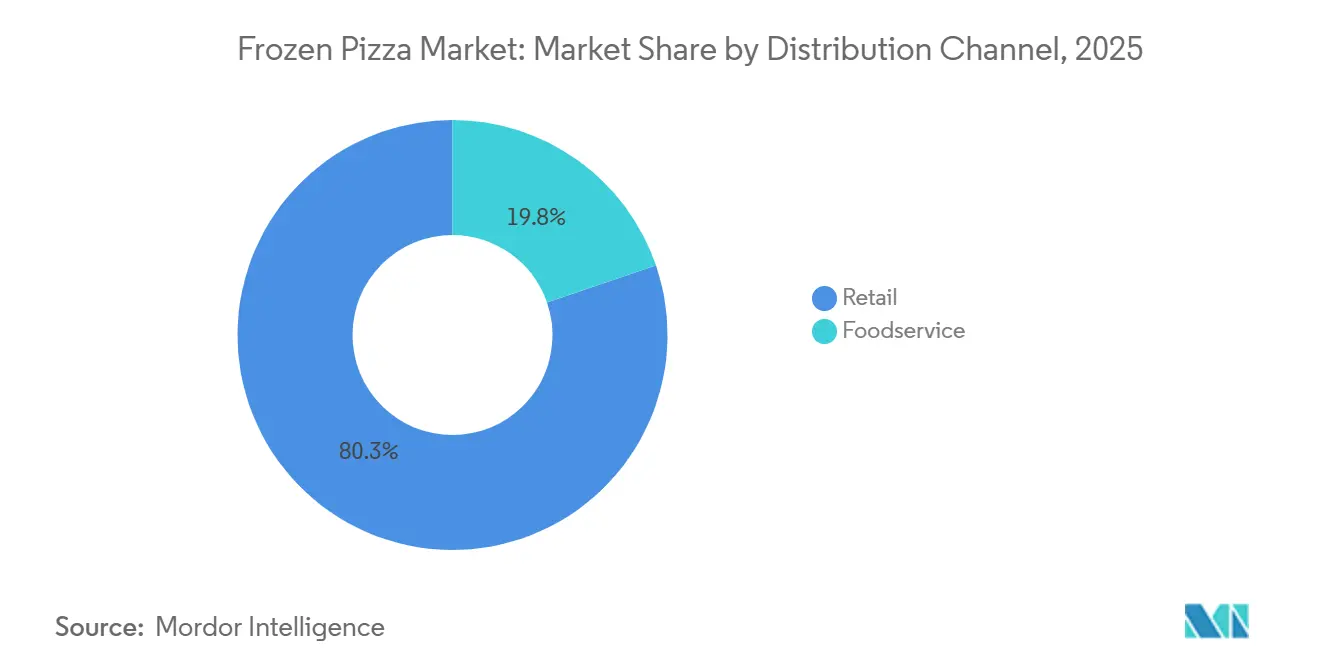

- By distribution channel, retail captured 80.25% share of the frozen pizza market size in 2025; foodservice is rebounding at an 8.05% CAGR to 2031.

- By geography, North America commanded 38.58% of 2025 revenue, while Asia-Pacific is anticipated to register the highest regional CAGR at 8.55% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Frozen Pizza Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand Fuels the Need for Convenient Meal Solutions | +1.2% | Global, with highest intensity in North America, Europe, and urban Asia-Pacific | Short term (≤ 2 years) |

| Rising Consumer Interest in Products with Longer Shelf Life | +0.8% | Global, particularly emerging markets with limited cold-chain infrastructure | Medium term (2-4 years) |

| Expansion of Vegan and Plant-based Pizza Offerings | +1.0% | North America, Europe, urban Asia-Pacific (China, India, Japan) | Medium term (2-4 years) |

| Western Food Culture Gains Popularity in Emerging Markets | +1.3% | Asia-Pacific (China, India, Southeast Asia), Latin America (Brazil, Mexico), Middle East | Long term (≥ 4 years) |

| Increased Appeal of Customizable and Diverse Topping Choices | +0.7% | Global, with premium segments in North America and Europe | Short term (≤ 2 years) |

| Greater Availability of Specialty and Gourmet Frozen Pizzas | +0.9% | North America, Europe, affluent urban centers in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand Fuels the Need for Convenient Meal Solutions

Changing meal preparation norms, influenced by dual-income households and busy professionals, have led 94% of consumers to rank convenience as their top priority when selecting frozen foods, according to the National Frozen & Refrigerated Foods Association. This shift surpasses basic reheating, as consumers now seek restaurant-quality flavors, accurate portion sizes, and easy cleanup. The National Frozen & Refrigerated Foods Association also reported a rise in frozen pizza sales during remote work periods. Despite the return to office environments, demand has stayed strong, signaling a permanent behavioral change rather than a temporary pandemic effect. In Japan and Germany, this trend is further driven by the growth of single-person households and aging populations. In 2024, Japan experienced a significant 50.7% year-on-year increase in smaller pack sizes and one-plate frozen meals, reaching USD 130 million, as per the USDA Foreign Agricultural Service[1]Source: USDA Foreign Agricultural Service, “Japan Frozen Food Market Report 2023-2024,” fas.usda.gov. Retailers are responding by expanding freezer aisle offerings and introducing grab-and-go formats, directly competing with quick-service restaurants on speed and cost.

Rising Consumer Interest in Products with Longer Shelf Life

Extended shelf life reduces food waste and shopping frequency, both of which resonate with cost-conscious and sustainability-minded buyers. Frozen pizza's 12-to-18-month freezer life contrasts sharply with refrigerated dough kits that expire within weeks, making it a pantry staple during supply-chain disruptions or extreme weather events. Advances in flash-freezing technology and modified-atmosphere packaging have improved texture retention, addressing historical complaints about soggy crusts or freezer burn. Emerging markets with nascent cold-chain networks—such as India, Indonesia, and Nigeria—are investing heavily in last-mile refrigeration, which will unlock frozen categories in regions where ambient-stable products previously dominated. This infrastructure build-out is expected to add 2 to 3 percentage points to regional CAGR over the next decade, as urban penetration rises and rural electrification projects come online.

Expansion of Vegan and Plant-Based Pizza Offerings

In 2024, 39% of U.S. consumers explored plant-based foods, signaling a shift from niche to mainstream. Flexitarians, rather than strict vegans, are driving this trend. Frozen pizza brands are leveraging this opportunity by introducing dairy-free mozzarella made from cashews, almonds, and fermented proteins, which replicate the melt and stretch of traditional cheese. The Good Food Institute reported an 8% increase in retail sales of plant-based cheese in 2024, surpassing the growth of the overall cheese category. Frozen pizza has emerged as the fastest-growing application, attributed to lower price sensitivity compared to fresh pizza. Additionally, the allergen-free positioning appeals to lactose-intolerant consumers and parents managing children's dietary restrictions. Daiya Foods and CAULIPOWER have secured placements in mainstream grocery stores, while major players like Nestle and General Mills are reformulating existing products to include plant-based options, reinforcing that this trend represents a structural shift rather than a passing fad.

Western Food Culture Gains Popularity in Emerging Markets

Urbanization, rising disposable incomes, and exposure to global media are accelerating Western food adoption in Asia, Latin America, and the Middle East. Pizza consumption in China has grown at double-digit rates as international chains expand beyond tier-1 cities and local brands introduce fusion toppings like Peking duck or spicy Sichuan flavors. Japan's frozen food market reached USD 12.5 billion in 2023, growing 3.4% year-on-year, with pizza and pasta categories leading household purchases as dual-income families seek time-saving solutions. In India, quick-commerce platforms are delivering frozen pizzas in under 15 minutes, competing directly with traditional takeout and enabling impulse purchases. Latin American consumers are embracing frozen pizza as a weekend treat, with Brazil and Mexico showing the strongest uptake. This geographic diversification reduces reliance on saturated North American and European markets, though it requires localized flavor profiles, halal certifications, and smaller pack sizes to match purchasing power and household structures.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health Concerns Surrounding Processed and Frozen Foods | -0.6% | Global, with highest scrutiny in North America and Europe | Short term (≤ 2 years) |

| More Rigorous Food Safety and Labeling Regulations | -0.4% | North America (FDA), Europe (EFSA), Asia-Pacific (FSSAI, local authorities) | Medium term (2-4 years) |

| Challenges Due to Limited Shelf Space in Retail Outlets | -0.3% | Global, particularly competitive in North America and Europe | Short term (≤ 2 years) |

| Allergens and Dietary Restrictions Reduce the Potential Consumer Base | -0.5% | Global, with highest impact in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health Concerns Surrounding Processed and Frozen Foods

Ultra-processed foods are under growing scrutiny from public-health advocates, who associate their high sodium, saturated fats, and artificial preservatives with chronic diseases. A single serving of frozen pizza typically contains 600 to 900 milligrams of sodium, up to 40% of the FDA's recommended daily intake, leading to calls for reformulation. Media attention on the dangers of ultra-processed foods has surged, with studies linking frequent consumption to obesity, cardiovascular diseases, and metabolic disorders. In response, brands are reducing sodium, removing artificial colors, and emphasizing "clean label" ingredients. However, these adjustments often affect taste or shelf stability, creating a reformulation challenge. In 2024, the U.S. Food and Drug Administration updated nutrition labeling regulations, requiring front-of-pack warnings for high sodium content, which could deter health-conscious consumers[2]Source: U.S. Food and Drug Administration, “Nutrition Labeling and Food Safety Regulations Update 2024,” FDA.GOV. Frozen pizza manufacturers face the challenge of balancing taste expectations with nutritional standards, a conflict that slows innovation and increases production costs.

More Rigorous Food Safety and Labeling Regulations

Regulatory agencies are tightening oversight of frozen foods, with the European Food Safety Authority introducing stricter limits on emulsifiers and stabilizers in 2024, while the FDA expanded allergen declaration requirements to include sesame and other emerging triggers. Compliance costs are rising as manufacturers invest in traceability systems, third-party audits, and facility upgrades to meet HACCP (Hazard Analysis and Critical Control Points) and ISO 22000 standards. Labeling complexity has increased, with mandatory disclosures for bioengineered ingredients, country-of-origin, and sustainability claims, all of which require legal review and packaging redesigns. Smaller brands struggle to absorb these costs, creating a barrier to entry that favors large incumbents with dedicated regulatory teams. Cross-border trade is further complicated by divergent standards, as products approved in the U.S. may require reformulation for European or Asian markets, limiting economies of scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Crust Type: Stuffed Crust Gains Despite Thin Crust Dominance

In 2025, thin-crust pizzas accounted for 58.15% of sales, highlighting a consumer preference for lighter, crispier textures that align with health-conscious eating habits and faster cooking times. However, stuffed-crust variants are expected to grow at a 7.82% CAGR through 2031, driven by indulgent eating occasions and effective marketing campaigns that promote cheese-filled edges as a premium feature. Korn Ferry research shows that stuffed-crust innovations generate hundreds of millions in additional revenue for major chains, confirming the format's commercial success. A Pizza Hut survey revealed that 28% of consumers prefer thin crust, compared to 20% who favor stuffed crust. Despite this, stuffed crusts command a 15% to 20% price premium, enhancing per-unit profitability. Traditional crusts remain a reliable category, appealing to budget-conscious families and institutional buyers. Meanwhile, alternative crusts, such as those made from cauliflower, chickpeas, and Greek yogurt, have experienced a remarkable 367% growth over four years, driven by the increasing popularity of gluten-free and low-carb diets, as reported by the American Culinary Federation.

Regional pizza styles are further diversifying the crust market. Detroit-style pizzas, recognized for their thick, rectangular shape and crispy edges, have grown 117% year-on-year. Similarly, Grandma pizza, known for its thin, square shape and olive oil base, has risen by 35%, according to the American Culinary Federation. These regional styles cater to consumers seeking authenticity and variety beyond the standard round pizza. In the frozen pizza segment, brands are introducing par-baked crusts that crisp up in home ovens, addressing past complaints of soggy textures and aiming to deliver pizzeria-quality results. As the market becomes increasingly competitive, crust innovation has become a critical area for differentiation, surpassing traditional variations in toppings and sauces.

By Topping: Vegan Cheese Accelerates as Meat-Based Holds Majority

In 2025, meat-based toppings accounted for 61.25% of sales, thanks to ingrained taste preferences and easy availability. Meanwhile, vegan and plant-based cheese alternatives are on an 8.11% CAGR rise through 2031, fueled by flexitarian diets, allergen avoidance, and environmental concerns, rather than a strict adherence to veganism. The Good Food Institute noted an 8% surge in plant-based cheese retail sales in 2024, with frozen pizza leading the charge, benefiting from price sensitivity and the ability to mask texture differences through baking. Vegetable-topped pizzas strike a balance, catering to health-conscious consumers and vegetarians, yet they don't match the rapid ascent of vegan cheese or the consistent demand for meat-based toppings.

Innovation in toppings is now a pivotal differentiator. Hot honey, for instance, has surged by 430% over four years, as consumers warm up to sweet and savory flavor profiles, according to the American Culinary Federation. Pepperoni cups, which curl and crisp when baked, have seen a five-fold increase in volume, underscoring the importance of texture and visual appeal in driving repeat purchases. Premium toppings like truffle oil, prosciutto, and burrata are transitioning from exclusive restaurant menus to supermarket freezer aisles. Specialty formats, priced between USD 11 to USD 14, are strategically targeting affluent households. Brands are also infusing global flavors such as Peking duck in China, paneer tikka in India, and chorizo in Mexico into their offerings, aiming to rival regional pizza chains. While this diversification in toppings increases SKU counts, it also empowers brands to secure shelf space and command premium prices.

By Category: Free-From Variants Outpace Conventional Growth

In 2025, conventional frozen pizzas dominated the market, capturing a substantial 72.42% share, thanks to their widespread appeal, competitive pricing, and well-established distribution channels. Meanwhile, "free from" variants, spanning gluten free, organic, clean label, and allergen free options, are on an upward trajectory, boasting a 7.94% CAGR through 2031. This surge is largely attributed to consumers becoming more discerning about ingredient transparency. Conagra Brands highlighted a notable shift: 62% of consumers now desire "elevated experiences" from their frozen food choices. This evolving demand has prompted manufacturers to not only reformulate recipes but also enhance packaging and emphasize provenance claims. Once a niche, gluten-free crusts crafted from cauliflower, chickpea, or rice flour have entered the mainstream arena. Notably, the popularity of cauliflower crust has skyrocketed, witnessing a staggering 367% surge over four years, as reported by the American Culinary Federation.

Parents, wary of pesticide residues and synthetic additives, are drawn to organic certifications. Simultaneously, millennials and Gen Z shoppers are gravitating towards clean-label products, which spotlight recognizable ingredients and minimal processing. While free from products command a retail premium of 20% to 40% over their conventional counterparts, boosting margins, they also restrict the addressable market volume. Brands face a challenging tightrope as they must reformulate to align with clean label standards, all while ensuring taste and shelf stability remain uncompromised. The production of gluten free and allergen free pizzas introduces complexities, especially with cross contamination risks. These variants often necessitate dedicated production lines or stringent sanitation measures to mitigate recall risks. Yet, despite these hurdles, the growth of free from products appears to be a structural trend, bolstered by enduring dietary restrictions and wellness movements.

By Distribution Channel: Foodservice Rebounds as Retail Dominates

Retail channels captured 80.25% of 2025 distribution, driven by supermarkets, hypermarkets, and the rapid expansion of online grocery platforms. Mass retailers like Walmart captured 45.4% of e-grocery share in 2023, leveraging store networks for same-day fulfillment and undercutting pure-play delivery services on fees. Convenience stores are also expanding frozen assortments, particularly in Japan, where approximately 60,000 locations stock single-serve frozen pizzas for on-the-go consumption. Online retail is the fastest-growing sub-channel, fueled by subscription services, direct-to-consumer brands, and quick-commerce platforms that promise delivery in under 15 minutes.

Foodservice is rebounding at 8.05% CAGR through 2031, recovering from pandemic-era closures and benefiting from ghost kitchens, delivery aggregators, and restaurant-to-retail brand extensions American Culinary Federation. Off-premise orders now account for 70% of pizza restaurant sales, blurring the line between foodservice and retail as chains like Chuck E. Cheese and Katie's Pizza launch frozen lines in Walmart and specialty grocers. Foodservice growth is concentrated in quick-service and fast-casual segments, where frozen dough and par-baked crusts reduce labor costs and improve consistency. Institutional buyers, schools, hospitals, corporate cafeterias are also increasing frozen pizza purchases as labor shortages make scratch preparation impractical. This channel convergence is reshaping competitive dynamics, as brands must now compete across retail shelves, delivery apps, and foodservice distributors simultaneously.

Geography Analysis

In 2025, North America accounted for 38.58% of global revenue, underscoring its mature market status, high per capita consumption, and well-established distribution networks spanning supermarkets, convenience stores, and foodservice operators. The frozen pizza segment in North America is marked by fierce competition from private labels, aggressive promotional pricing, and a focus on innovations like premium toppings, alternative crusts, and clean label reformulations. While Canada and Mexico share these market dynamics, Mexico stands out with its burgeoning middle class and an expanding cold chain infrastructure, both of which are hastening the embrace of Western convenience foods. Although North America's growth is slowing compared to emerging markets, its established brand equity, economies of scale, and consumers' readiness to pay a premium for specialty formats ensure it remains a lucrative profit center.

Asia Pacific is on track to grow at a robust 8.55% CAGR through 2031, driven by urbanization, the rise of dual-income households, and a growing affinity for Western food culture in nations like China, India, Japan, and across Southeast Asia. In 2023, Japan's frozen food market, valued at USD 12.5 billion, saw a 3.4% year-on-year growth. Notably, household consumption outpaced commercial foodservice for the first time, a shift attributed to aging demographics and smaller household sizes favoring single serve portions. In 2024, one plate frozen meals surged by 50.7% year-on-year, hitting USD 130 million, highlighting a pronounced shift towards convenience. Quick commerce platforms in India are booming, expanding at a staggering 48% CAGR from 2023 to 2028, and are now delivering frozen pizzas in under 15 minutes, challenging the dominance of traditional kirana stores. In China, pizza consumption is on the rise, with international chains venturing beyond tier one cities and local brands innovating with fusion toppings like Peking duck and spicy Sichuan flavors. Investments in cold chain infrastructure are pivotal, as advancements in last mile refrigeration are making previously ambient stable regions receptive to frozen categories.

Europe stands as a mature yet stable market, with Germany, the UK, France, and Italy leading in sales. European consumers, emphasizing quality, authenticity, and sustainability, are increasingly drawn to organic, locally sourced, and artisanal frozen pizzas. In 2024, the European Food Safety Authority tightened regulations on emulsifiers and stabilizers, prompting many brands to reformulate their products, a move that has escalated compliance costs[3]Source: European Food Safety Authority, “Food Additive Regulations and Emulsifier Standards 2024,” efsa.europa.eu. Picard, a prominent French frozen food retailer, has made strides in Japan, operating 47 stores and catering to affluent consumers eager to splurge on imported European delicacies, showcasing the potential of cross border brand extensions. South America, particularly Brazil, Argentina, and Colombia, presents a burgeoning market opportunity, driven by rising disposable incomes and urbanization. However, players must navigate challenges posed by economic volatility and currency fluctuations. Meanwhile, the Middle East and Africa, still in their infancy in this market, see growth primarily in urban hubs like Dubai, Riyadh, Johannesburg, and Lagos, spurred by demands from expatriate communities and affluent locals for international brands.

Competitive Landscape

The frozen pizza market exhibits low concentration, with a score of 3 out of 10, enabling niche players to capture share through specialized offerings such as cauliflower crusts, vegan cheese, and restaurant-to-retail brand extensions. Incumbents like Nestle, General Mills, Conagra Brands, and Dr. Oetker compete on scale, distribution reach, and brand equity, while smaller entrants like CAULIPOWER, Amy's Kitchen, and Cappello's differentiate through clean-label positioning, allergen-free certifications, and direct-to-consumer channels. Strategy patterns include premiumization, upgrading ingredients and packaging to justify higher price points, and channel diversification, where brands expand from retail into foodservice or vice versa. Restaurant-to-retail conversions are accelerating, with Chuck E. Cheese and Katie's Pizza launching frozen lines in Walmart and specialty grocers, leveraging brand equity built in foodservice to bypass traditional retail barriers.

Technology adoption is uneven, with leaders investing in e-commerce platforms, subscription models, and data analytics to predict flavor trends, while laggards rely on legacy distribution and promotional pricing. White-space opportunities include emerging markets with nascent cold-chain infrastructure, such as India, Indonesia, and Nigeria, where urbanization and rising incomes are creating new consumer cohorts. Plant-based and allergen-free segments remain underpenetrated, as many brands still treat them as niche rather than mainstream categories.

Emerging disruptors include quick-commerce platforms that compress delivery windows to under 15 minutes, threatening traditional retail and foodservice channels, and direct-to-consumer brands that use social media and influencer partnerships to build loyalty without retailer intermediation. Regulatory compliance is becoming a competitive advantage, as brands with robust traceability systems and ISO 22000 certifications can navigate tightening food safety standards more efficiently than smaller rivals. The fragmented structure suggests that consolidation is likely, with larger players acquiring niche brands to fill portfolio gaps and accelerate entry into high-growth segments like gluten-free, vegan, and premium.

Frozen Pizza Industry Leaders

Nestlé S.A.

General Mills Inc.

Dr. Oetker GmbH

Conagra Brands Inc.

Palermo Villa Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Palermo Villa, in partnership with Kellanova, introduced Cheez-It Frozen Pizza to expand their frozen pizza portfolio. The product features an ultra-thin crust with a Cheez-It flavored base, demonstrating innovation in the frozen pizza category. The company offers multiple varieties in their product line, including Italian Four Cheese and Pepperoni options, catering to different consumer preferences. The pizzas are positioned at competitive price points in the retail market.

- February 2025: Daiya enhanced its plant-based frozen pizza portfolio by introducing new recipes that incorporate a proprietary Oat Cream blend, improving texture and taste. The company plans to introduce Meatless Spicy Salami and Cheeseburger Pizza varieties to broaden its plant-based offerings.

- February 2025: Dr. Oetker Canada operates its manufacturing facility in London, Ontario, which produces 400,000 frozen pizzas daily using locally sourced ingredients. The facility employs 430 people and manufactures over 190 frozen pizza products, demonstrating the company's integration into the local supply chain.

Global Frozen Pizza Market Report Scope

| Thin Crust |

| Regular/Traditional Crust |

| Stuffed Crust. |

| Other Crust Types |

| Meat-Based (Includes Combination With Vegetables) |

| Vegetable |

| Vegan And Plant-Based Cheese |

| Free-Form |

| Conventional |

| Foodservice | |

| Retail | Supermarkets And Hypermarkets |

| Convenience Stores | |

| Online Retail | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Crust Type | Thin Crust | |

| Regular/Traditional Crust | ||

| Stuffed Crust. | ||

| Other Crust Types | ||

| By Topping | Meat-Based (Includes Combination With Vegetables) | |

| Vegetable | ||

| Vegan And Plant-Based Cheese | ||

| By Category | Free-Form | |

| Conventional | ||

| By Distribution Channel | Foodservice | |

| Retail | Supermarkets And Hypermarkets | |

| Convenience Stores | ||

| Online Retail | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the frozen pizza market by 2031?

It is forecast to reach USD 28.93 billion by 2031.

Which crust format is growing fastest within frozen pizza?

Stuffed crust is advancing at a 7.82% CAGR through 2031.

How quickly are vegan cheese frozen pizzas expanding?

They are growing at an 8.11% CAGR over 2026-2031.

What share of 2025 sales did thin crust pizzas hold?

Thin crust captured 58.15% of 2025 global sales.

Page last updated on: