Organic Ice Cream Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2025) | USD 2.01 Billion |

| Market Size (2030) | USD 3.57 Billion |

| Growth Rate (2026 - 2031) | 10.07% CAGR |

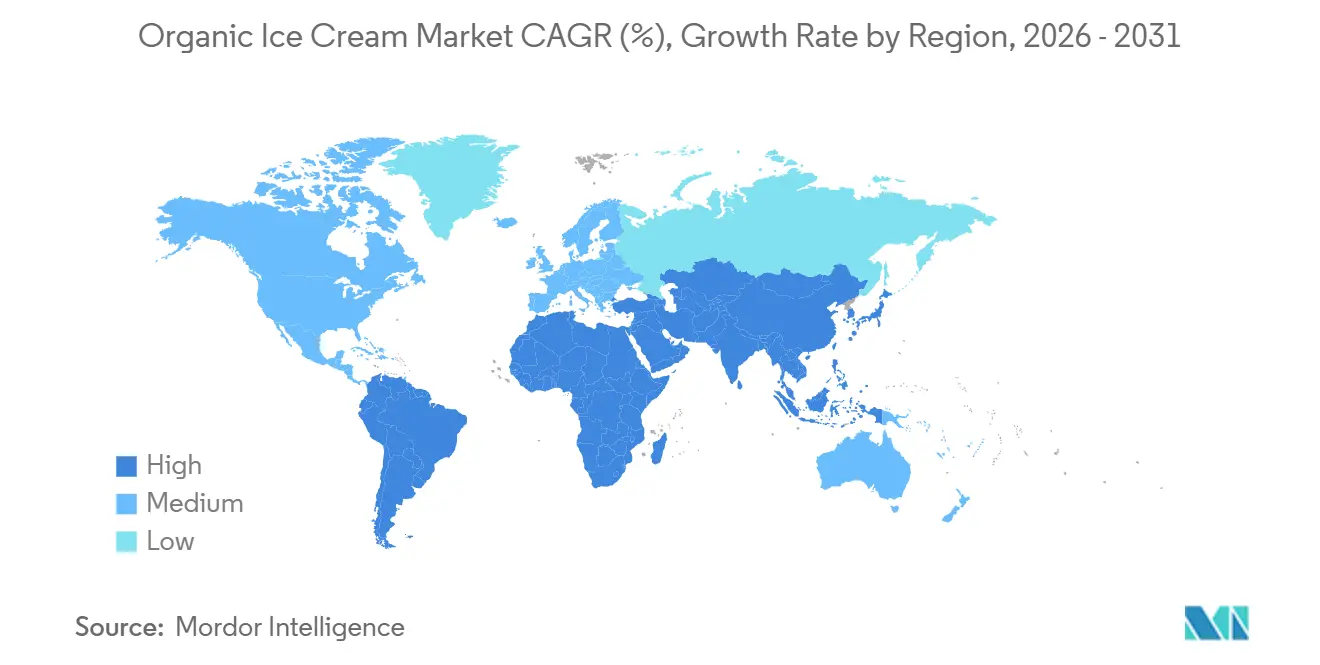

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Organic Ice Cream Market Analysis by Mordor Intelligence

The organic ice cream market size was valued at USD 1.82 billion in 2025 and estimated to grow from USD 2.01 billion in 2026 to reach USD 3.57 billion by 2031, at a CAGR of 10.07% during the forecast period (2026-2031). This sharp expansion reflects a lasting shift in frozen-dessert habits, as shoppers favor certified organic ingredients, short ingredient lists, and transparent sourcing. Consumer readiness to pay sizeable premiums for natural claims, coupled with tighter organic dairy supply and rapid launches of lactose-free and plant-based lines, keeps demand outpacing capacity. Producers also benefit from stronger food-safety regulations that elevate trust in certified products, while flavor innovation centered on organic fruits, botanicals, and inclusions broadens appeal. At the same time, input-cost inflation and dairy-supply volatility pressure gross margins, prompting larger players to scale through mergers, backward integration, and precision-fermentation partnerships.

Key Report Takeaways

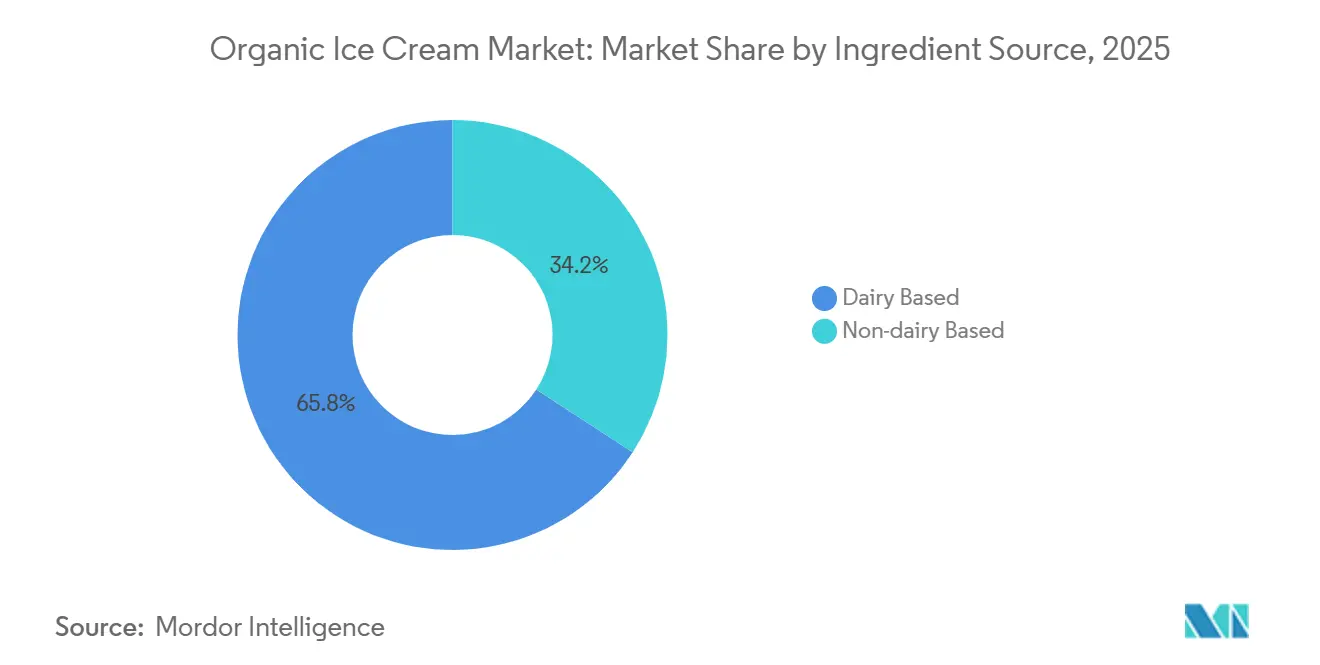

- By ingredient source, dairy-based products led with 65.83% of the organic ice cream market share in 2025, whereas non-dairy alternatives are forecast to post an 11.86% CAGR to 2031.

- By flavor, vanilla dominated with 31.37% share in 2025; fruit-flavored variants are poised to grow at a 10.75% CAGR through 2031.

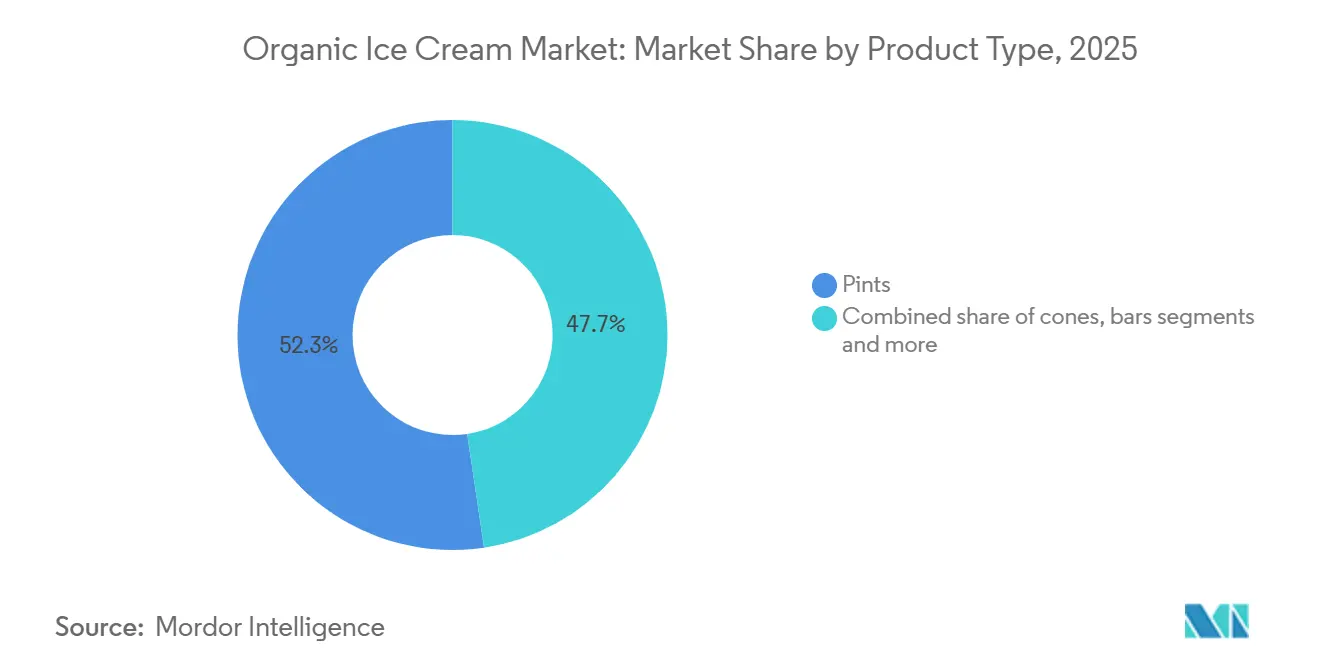

- By product type, pints captured 52.34% revenue in 2025, while bars are on track for a 10.64% CAGR to 2031.

- By distribution channel, retail accounted for 84.72% of the organic ice cream market in 2025; foodservice is the fastest-growing channel, with a 11.35% CAGR to 2031.

- Regionally, North America accounted for 38.64% of global revenue in 2025; Asia-Pacific is forecast to lead growth with a 11.59% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Organic Ice Cream Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Organic dairy sourcing as a premium trust signal | +1.8% | North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Premiumization and indulgent organic products | +1.5% | North America, Europe, affluent Asia-Pacific metros | Short term (≤ 2 years) |

| Flavor innovation using organic inclusions | +1.2% | Global | Medium term (2-4 years) |

| Growth of lactose-free organic dairy variants | +1.4% | North America, Europe, emerging Asia-Pacific cities | Short term (≤ 2 years) |

| Strengthening food-safety and certification standards | +1.0% | Global | Long term (≥ 4 years) |

| Artisanal small-batch organic positioning | +0.9% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Organic dairy sourcing as a premium trust signal

Certified organic dairy sourcing has emerged as a decisive brand differentiator, particularly as consumers scrutinize supply-chain transparency and animal welfare practices. The global organic farmland base reached 98.9 million hectares in 2023, representing 2.1% of total agricultural land, with Oceania (53.2 million hectares), Europe (19.5 million hectares), and Latin America (10.3 million hectares) leading in certified acreage according to The Research Institute of Organic Agriculture FiBL[1]Source: Research Institute of Organic Agriculture, “The World of Organic Agriculture 2025,” fibl.org. Organic dairy cows in Argentina increased 5.7% to 4,618 head in 2024, supporting export-oriented organic ice cream ingredient supply chains targeting North America and Europe, according to SENASA Argentina. U.S. organic milk exports surged 102.6% year-over-year in the first nine months of 2025, though 74% of shipments remained within North America under USMCA tariff-free provisions, limiting immediate impact on Asia-Pacific ingredient availability, as per NODPA[2]Source: Northeast Organic Dairy Producers Alliance, “Pay and Feed Prices, January 2026,” nodpa.com. This dynamic creates a two-tier market: established North American and European brands leverage domestic organic dairy networks to reinforce provenance claims, while Asia-Pacific entrants face higher import costs or must develop nascent local organic dairy infrastructure. Global consumers indicate a willingness to pay more for natural or all-natural claims and for packaged foods with natural ingredients.

Flavor Innovation using organic inclusions

Flavor innovation anchored in organic inclusions is driving differentiation and repeat purchase, particularly as vanilla's 31.37% share in 2025 signals saturation risk for single-note offerings. Fruit-flavored variants are accelerating at 10.75% CAGR through 2031, propelled by organic berry, mango, passion fruit, and exotic inclusions that command premium pricing and appeal to adventurous consumers. Organic vanilla pricing volatility, driven by cyclone damage in Madagascar and supply concentration, has incentivized formulators to diversify into organic cocoa, coffee, matcha, and botanical extracts sourced from certified fair-trade cooperatives. Whitey's Ice Cream introduced dairy-free pea protein flavors in February 2026, incorporating organic fruit purees and adaptogens to target wellness-oriented consumers. The technical challenge lies in maintaining flavor stability and color vibrancy without synthetic preservatives or artificial colors; natural vegetable-derived colors (carrot, beet, turmeric) and fermentation-derived flavor enhancers are gaining traction as clean-label alternatives, though they introduce cost premiums and processing complexity, according to the Institute of Food Technologists. Inclusion innovation extends to texture: organic cookie dough, brownie chunks, and nut-based swirls must meet organic certification standards while delivering indulgent sensory cues that justify premium pricing.

Growth of lactose-free organic dairy variants

Lactose-free organic ice cream is capturing dual demand from lactose-intolerant consumers and health-conscious buyers seeking digestive wellness benefits. Valio introduced its Eila® lactose-free milk powder range in June 2025, offering skimmed, semi-skimmed, and whole milk variants with naturally sweeter taste profiles (due to lactose hydrolysis into glucose and galactose) that enable sugar reduction without artificial sweeteners, addressing clean-label and reduced-sugar mandates simultaneously. Lactaid launched a lactose-free chocolate peanut butter ice cream in May 2025, leveraging lactase enzyme technology to retain dairy's creamy mouthfeel while eliminating lactose-induced digestive discomfort. The segment's appeal extends beyond diagnosed lactose intolerance among the global adult population to include consumers who perceive lactose-free as inherently healthier or easier to digest, even without clinical necessity. Technical formulation advantages include reduced risk of lactose crystallization (which causes grittiness in conventional ice cream) and naturally enhanced sweetness, allowing formulators to lower added sugar by 10-15% while maintaining sensory acceptance. Regulatory frameworks under the USDA National Organic Program (NOP) and the EU Regulation 2018/848 permit the use of lactase enzymes in organic products, provided the enzymes are produced via non-GMO processes, facilitating broader adoption.

Strengthening food safety and organic certification standards

Tightening organic certification standards and food safety protocols are reshaping competitive dynamics by raising entry barriers while simultaneously expanding market access for compliant producers. The European Union's full implementation of Regulation 2018/848 in 2024 introduced stricter controls on contamination thresholds, traceability documentation, and group certification schemes, forcing smaller producers to invest in upgraded record-keeping systems and third-party audits or exit the certified organic market entirely. The USDA National Organic Program (NOP) continues to refine its National List of Allowed and Prohibited Substances through National Organic Standards Board (NOSB) deliberations, with recent scrutiny on natural stabilizers, processing aids, and packaging materials that directly affect ice cream formulation flexibility, carrageenan, for instance, remains on the allowed list despite periodic challenges, while synthetic emulsifiers face ongoing restriction advocacy that could force reformulation cycles. Regulatory harmonization efforts among USDA NOP, EU organic frameworks, and emerging Asia-Pacific standards (China's GB/T, India's NPOP, Japan's JAS) remain incomplete, creating certification arbitrage opportunities in which producers target the least restrictive regime for ingredient sourcing while claiming equivalence for export markets. Food safety incidents in conventional dairy supply chains, including pathogen outbreaks and antibiotic residue detections, are accelerating consumer migration to organic alternatives perceived as inherently safer due to prohibited-substance restrictions and mandatory traceability, though organic certification addresses production methods rather than microbial safety, creating a perception-reality gap that savvy brands exploit through dual messaging on organic purity and HACCP compliance. The certification infrastructure itself is consolidating: third-party certifiers are merging to achieve audit scale economies, while blockchain-enabled traceability platforms are emerging to streamline compliance documentation and enhance supply-chain transparency, reducing certification costs for large producers but widening the compliance gap for artisanal operators lacking IT infrastructure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of certified organic dairy and ingredients | -1.6% | North America, Europe, emerging Asia-Pacific | Short term (≤ 2 years) |

| Shorter shelf life due to clean-label formulations | -1.1% | Global | Medium term (2-4 years) |

| Fragmented organic standards across regions | -0.8% | Global | Long term (≥ 4 years) |

| Limited organic milk supply | -1.3% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High cost of certified organic dairy and ingredients

Certified organic dairy commands substantial cost premiums, compressing manufacturer margins and limiting mass-market penetration. Pennsylvania organic milk averaged USD 38.43 per hundredweight in December 2024, while Northeast regional pay prices ranged from USD 35-45 per hundredweight for grain and pasture-fed organic milk, USD 38-50+ for grass-fed, and USD 50-60 for regenerative organic or A2A2 certified milk, according to the USDA. Dutch organic milk processor guaranteed prices stood at EUR 63.50 per 100 kilograms (USD 65.08) in January 2025, down slightly from December but still reflecting elevated input costs driven by organic feed grain inflation. Organic feed corn traded at USD 8.23 per bushel and organic feed soybeans at USD 22.57 per bushel in November 2025, well above conventional equivalents, according to the USDA AMS[3]Source: United States Department of Agriculture, “Organic Dairy Fluid Overview,” ams.usda.gov . Retail pricing reflects these upstream pressures: organic ice cream (48-64 ounce packages) averaged USD 8.42 nationally in March 2026, a USD 4.08 premium over conventional products, limiting purchase frequency among price-sensitive households. Brands unable to secure long-term organic ingredient contracts or pass through cost increases face margin erosion, while smaller artisanal producers struggle to achieve procurement scale economies, constraining market entry and expansion.

Shorter shelf life due to clean-label formulations

Clean-label organic formulations sacrifice shelf-life robustness for ingredient simplicity, introducing distribution and waste management challenges. Conventional ice cream relies on synthetic emulsifiers (mono- and diglycerides, polysorbates) and stabilizers (modified starches, carrageenan, cellulose gum) to control ice crystal growth, manage unfrozen water mobility, and maintain textural stability during temperature fluctuations common in retail freezers and home storage. Organic certification under USDA NOP and EU 2018/848 restricts many synthetic additives, forcing formulators to substitute with natural hydrocolloids (locust bean gum, guar, pectin, tapioca starch) and plant-derived emulsifiers (lecithin, chickpea broth) that offer narrower functional performance windows. The trade-off is acute: clean-label formulations with 0.2% stabilizer/emulsifier blends exhibit greater susceptibility to heat shock, ice crystal coarsening, and fat separation than conventional products with 0.6% blends, reducing shelf life by 20-30% under identical storage conditions. This constraint is particularly problematic for export-oriented brands targeting Asia-Pacific, where extended cold-chain transit times, high-altitude distribution (Himalayan regions, Andean markets), and inconsistent retail freezer temperatures accelerate quality degradation. Manufacturers must balance consumer demand for short ingredient lists against operational realities of distribution infrastructure, often segmenting product lines by channel—premium clean-label pints for local specialty retail versus stabilizer-enhanced formulations for national supermarket chains and export markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Source: Non-Dairy Surge Challenges Dairy Dominance

Dairy-based organic ice cream commanded 65.83% market share in 2025, underpinned by consumer familiarity, superior creaminess from milkfat, and established organic dairy supply chains in North America and Europe. Traditional organic dairy formulations leverage butterfat content (10-16%) to deliver an indulgent mouthfeel and flavor-carrying capacity, remaining the sensory benchmark for premium frozen desserts. Regulatory compliance frameworks under USDA NOP and EU Regulation 2018/848 permit organic certification for both dairy and non-dairy products, provided that all agricultural ingredients meet organic production standards and that processing aids (enzymes, cultures) derive from non-GMO sources. Whitey's Ice Cream introduced pea protein-based organic flavors in February 2026, positioning them as high-protein (8-10 grams per serving) to attract fitness-oriented consumers. The technical challenge for non-dairy organic formulations lies in replicating dairy's fat globule structure and protein matrix. Plant proteins lack casein's emulsifying properties and require higher stabilizer loads or precision fermentation ingredients (such as Perfect Day's whey protein) to achieve comparable texture and freeze-thaw stability. Patent activity reflects this innovation focus: China leads global ice cream patents with over 40% of active filings, followed by Western multinationals Unilever and Nestlé, with plant-based base formulations, natural stabilizers, and energy-efficient freezing processes dominating recent applications.

Non-dairy organic variants are expanding at 11.86% CAGR through 2031, driven by plant-based bases including oat, pea protein, cashew, almond, and hemp milk that appeal to vegan, lactose-intolerant, and environmentally conscious consumers. Unilever's Ben & Jerry's reformulated its non-dairy line with oat bases in 2024, capitalizing on oat milk's neutral flavor profile and creamy texture that more closely mimics dairy than earlier coconut or almond formulations. The non-dairy segment faces ingredient sourcing constraints, organic oat, almond, and pea protein supplies are concentrated in North America and Europe, with limited certified production in Asia-Pacific, elevating import dependency and cost for regional manufacturers. Conversely, dairy-based organic ice cream confronts supply volatility: Pennsylvania organic milk production volumes fell 24% from October to December 2024 due to drought and feed scarcity, tightening cream availability for ice cream manufacturers. This supply-demand imbalance is pushing dairy-based brands toward vertical integration strategies (direct farm partnerships, cooperative ownership) to secure consistent organic milk flows, while non-dairy entrants leverage flexible ingredient sourcing across multiple plant-base platforms to mitigate single-commodity risk.

By Flavor: Fruit Variants Outpace Vanilla's Mature Base

Vanilla captured 31.37% flavor share in 2025, reflecting its role as the foundational profile for mix-ins, toppings, and multi-flavor pints, yet its growth trajectory is moderating as consumers seek novelty and functional benefits beyond classic offerings. Vanilla's enduring share reflects its versatility and lower formulation risk, but brands over-indexed to vanilla face commoditization pressure and must differentiate via bean origin (Madagascar, Tahitian, Mexican), extraction method (cold-pressed, alcohol-free), or stacked certifications (organic, fair trade, regenerative) to justify premium pricing in an increasingly crowded segment. Flavor innovation is increasingly tied to functional positioning: organic matcha ice cream delivers antioxidant claims, coffee variants incorporate fair-trade certified beans, and adaptogen-infused flavors (ashwagandha, reishi mushroom) target wellness-oriented buyers. Straus Family Creamery's gluten-free organic cookie dough launch in January 2025 exemplifies cross-functional innovation, addressing allergen concerns while maintaining indulgent flavor delivery.

Fruit-flavored organic ice cream is accelerating at 10.75% CAGR through 2031, propelled by organic berry (strawberry, blueberry, raspberry), tropical (mango, passion fruit, guava), and stone fruit (peach, cherry) variants that leverage seasonal harvest cycles and regional sourcing narratives. Chocolate remains a stable secondary segment, benefiting from organic cocoa certification growth in Latin America (Ecuador, Peru, Dominican Republic) and West Africa, though cocoa price volatility and ethical sourcing scrutiny require brands to maintain transparent supply-chain documentation. Other flavors, encompassing coffee, matcha, salted caramel, and botanical infusions (lavender, rose, earl grey), are gaining traction in specialty channels and artisanal brands targeting experiential consumers willing to pay premiums for limited-edition releases and hyper-seasonal offerings. The technical complexity of fruit-flavored organic formulations centers on color and flavor stability, natural fruit purees and juices oxidize and degrade faster than synthetic flavors, requiring careful pH management, antioxidant addition (ascorbic acid from organic sources), and cold-chain discipline to preserve vibrancy through shelf life.

By Product Type: Bars Gain as Portion Control Meets Indulgence

Pints dominated product-type sales at 52.34% share in 2025, driven by at-home consumption preferences, multi-serve household formats, and retailer shelf-space allocation favoring larger package sizes with higher absolute revenue per SKU. Bars are expanding at 10.64% CAGR through 2031, reflecting consumer demand for portion-controlled indulgence, on-the-go convenience, and single-serve formats that align with calorie-conscious eating patterns without sacrificing organic and premium positioning. Cones and other formats (sandwiches, cups, novelties) serve niche occasions, cones appeal to nostalgic and experiential consumers seeking artisanal gelato-style presentations, while sandwich formats target children and value-oriented households.

The bar segment's growth is underpinned by innovation in coatings, inclusions, and functional claims. Organic chocolate coatings (dark, milk, white) must meet dual certification (organic cocoa, organic dairy or plant-based milk), while inclusions (nuts, cookie pieces, caramel swirls) require organic ingredient sourcing and allergen management to meet clean-label standards. Unilever's Magnum brand, now part of The Magnum Ice Cream Company following the 2025 separation, introduced a vegan raspberry swirl bar with pea protein in 2023, targeting flexitarian consumers and demonstrating technical feasibility of plant-based coatings and fillings. Bars also benefit from lower cold-chain complexity than pints, individual wrapping and smaller thermal mass reduce temperature fluctuation sensitivity during retail display and consumer transport, extending effective shelf life and reducing waste. However, bars face higher per-unit packaging costs and lower gross margin per ounce compared to pints, requiring brands to optimize production scale, automate wrapping and coating processes, and leverage multi-SKU production runs to maintain profitability. The format's premiumization potential is evident in artisanal brands offering hand-dipped organic bars with exotic coatings (matcha white chocolate, salted caramel dark chocolate) at USD 4-6 per bar, positioning ice cream bars as accessible luxury rather than commodity treats.

By Distribution Channel: Retail Dominance with Foodservice Growth

Retail channels accounted for 84.72% of organic ice cream sales in 2025, encompassing supermarkets/hypermarkets, specialty stores, convenience stores, and online retail platforms that collectively provide broad consumer access, promotional visibility, and private-label competition. Supermarkets and hypermarkets dominate retail distribution, offering extensive freezer space, frequent promotional activity (buy-one-get-one, temporary price reductions), and co-location with complementary products (toppings, cones, dessert sauces) that drive impulse purchases and basket building. Specialty stores (natural food retailers and organic-focused chains such as Whole Foods and Sprouts) command premium pricing and attract core organic consumers willing to pay for curated assortments, knowledgeable staff, and mission-aligned brands. Online retail is expanding rapidly, accelerated by pandemic-driven e-commerce adoption and last-mile cold-chain innovations (insulated packaging, dry ice, scheduled delivery windows) that maintain product integrity during home delivery. Convenience stores serve immediate consumption occasions and impulse purchase, though limited freezer space constrains SKU variety and favors single-serve formats (bars, cones) over multi-serve pints.

Foodservice channels, restaurants, cafés, dessert parlors, catering, are growing at 11.35% CAGR through 2031, rebounding from pandemic-era closures and benefiting from rising consumer expectations for organic and clean-label menu options. Restaurants are integrating organic ice cream into dessert menus to reinforce farm-to-table positioning and justify premium check averages, while specialty dessert parlors (gelaterias, ice cream shops) are differentiating via organic certification, local dairy partnerships, and artisanal small-batch production. Froneri's acquisition of Nestlé's ice cream operations in China, Malaysia, and Thailand in February 2026 positions the joint venture to expand foodservice penetration across Asia-Pacific, where dining-out occasions are recovering and consumers increasingly associate organic ingredients with food safety and quality. The foodservice channel's appeal for organic brands lies in direct consumer engagement, storytelling opportunities (menu descriptions, staff training), and higher per-serving pricing that offsets ingredient cost premiums, a scoop of organic ice cream in a café setting commands USD 5-8 versus USD 0.50-1.00 per serving for retail pints. However, foodservice requires dedicated sales infrastructure, smaller package formats (3-gallon tubs, pre-portioned cups), and consistent quality across varied storage and scooping conditions, elevating operational complexity for manufacturers accustomed to retail-focused distribution models.

Geography Analysis

North America accounted for 38.64% of global organic ice cream revenue in 2025, underpinned by the United States’ well-established organic dairy ecosystem, strong consumer familiarity with organic labeling, and extensive retail penetration across supermarkets, specialty outlets, and e-commerce platforms. Regulatory clarity through the USDA National Organic Program (NOP), combined with the long-standing credibility of the USDA Organic seal, continues to reinforce consumer trust and support premium pricing. Canada is seeing steady expansion as provincial organic standards align with federal frameworks, while Mexico’s rising middle class and growing health awareness are boosting demand for both imported and locally produced organic frozen desserts. The region also remains highly innovation-driven, with brands introducing new certified and specialty offerings that emphasize product differentiation and justify higher price points.

Asia-Pacific is projected to be the fastest-growing region, with a CAGR of 11.59% through 2031, fueled by rising disposable incomes, rapid urbanization, and improving cold-chain logistics. Increasing awareness of food safety and health benefits is accelerating demand across major markets such as China, India, Japan, and Australia. Strategic investments and consolidation activity highlight the region’s potential, as multinational players expand their presence through acquisitions and partnerships that combine global branding with local production and distribution capabilities. However, growth is tempered by regulatory fragmentation, as countries maintain distinct organic certification systems, increasing compliance complexity for exporters. Additionally, limited domestic organic dairy supply means many producers rely on imported ingredients, exposing the market to higher costs and currency risks.

Europe remains a significant contributor to the organic ice cream market, supported by stringent regulatory standards, high per-capita organic consumption, and a strong preference for locally sourced and artisanal products. Markets such as Germany, France, Austria, and the Netherlands drive demand, while established certification systems and cross-border regulatory alignment facilitate trade despite post-Brexit complexities affecting the UK. In contrast, South America and the Middle East & Africa are still emerging markets. South America shows long-term promise with improving organic agriculture infrastructure and growing urban demand, though consumption remains concentrated in major cities and constrained by distribution challenges. Meanwhile, the Middle East and Africa are characterized by limited organic production and certification systems, with demand largely centered in affluent urban areas and driven by imports. Across these regions, future growth will depend on infrastructure development, regulatory progress, and increasing consumer awareness of organic products.

Competitive Landscape

The organic ice cream sector exhibits moderate concentration, with a handful of multinational food conglomerates (Unilever, Danone, Nestlé via Froneri JV) commanding substantial market share alongside a fragmented long tail of regional and artisanal brands leveraging local sourcing, small-batch production, and direct-to-consumer distribution. Consolidation accelerated in 2025-2026 as large players divested non-core ice cream assets to pure-play operators: Nestlé sold its remaining ice cream business to Froneri in February 2026, transferring operations in China, Malaysia, Thailand, Canada, Chile, and Peru, and enabling Froneri to scale as one of the two largest global ice cream companies (alongside Unilever's separated Magnum Ice Cream Company). Froneri raised EUR 3.6 billion (USD 3.9 billion) in new equity in October 2025, valuing the joint venture at EUR 15 billion (USD 16.3 billion) including debt, and signaling capacity for further M&A-led transformation and brand portfolio expansion. In 2025, Unilever completed the separation of its ice cream division into The Magnum Ice Cream Company, which subsequently acquired a 61.9% stake in Kwality Wall's India to strengthen its presence in a fast-growing, under-penetrated market.

Strategic patterns emphasize vertical integration (securing organic dairy supply via farm partnerships and cooperatives), portfolio premiumization (organic, lactose-free, plant-based line extensions), and channel diversification (expanding foodservice penetration alongside retail dominance). White-space opportunities exist for regenerative organic certification, hyper-local distribution models (farm-to-freezer direct sales, subscription services), and functional positioning (high-protein, probiotic, adaptogen-infused variants) that large incumbents are slower to address due to scale and complexity constraints. Patent activity underscores technology-driven competition: China leads global ice cream patents with over 40% of active filings, followed by Western multinationals Unilever and Nestlé, with innovation focused on plant-based base formulations, natural stabilizers replacing synthetic emulsifiers, energy-efficient freezing processes, and automated production systems.

Smaller organic-focused brands (Straus Family Creamery, Alec's Ice Cream, Stonyfield Farm, Organic Valley) differentiate via transparent sourcing narratives, regenerative agriculture partnerships, and stacked certifications (organic, fair trade, non-GMO, B Corp) that justify premium pricing and build brand loyalty among mission-aligned consumers. Emerging disruptors include precision fermentation ingredient suppliers (Perfect Day) enabling lactose-free organic dairy proteins without animal agriculture, and plant-based specialists (Oatly, NadaMoo!, Coconut Bliss) leveraging proprietary formulations and direct-to-consumer e-commerce to bypass traditional retail gatekeepers. Competitive intensity is highest in North America and Europe, where retail shelf space is finite, promotional spending is elevated, and private-label organic ice cream from retailers (Whole Foods 365, Trader Joe's) competes on price and convenience, compressing branded manufacturers' margins and forcing continuous innovation to maintain differentiation.

Organic Ice Cream Industry Leaders

Alden’s Organic

Oatly Group AB

Danone S.A.

Nestlé S.A.

Unilever

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Nestlé announced the sale of its remaining ice cream business to Froneri, the 50-50 joint venture Nestlé co-owns with PAI Partners, in a phased integration during 2026-early 2027. The transaction transfers Nestlé's direct ice cream operations in China, Malaysia, Thailand, Canada, Chile, and Peru to Froneri, consolidating regional assets under a pure-play operator while Nestlé retains its 50% ownership stake in the joint venture.

- June 2025: Valio introduced its Eila® lactose-free milk powder range, including skimmed, semi-skimmed, and whole milk variants designed for ice cream formulation. The products leverage lactose hydrolysis technology to deliver naturally sweeter taste profiles without added sugars or artificial sweeteners, enabling sugar reduction, addressing clean-label mandates, and preventing lactose crystallization and grittiness in frozen desserts.

- May 2025: Alec's Ice Cream has introduced Culture Cup, a single-serve ice cream product made with A2 milk from regenerative organic farms. Each Culture Cup contains ice cream topped with a dark chocolate shell and includes prebiotics, probiotics, and less than 10g of unrefined cane sugar. The product maintains a calorie count below 160 while incorporating ingredients sourced through sustainable practices.

- January 2025: Straus Family Creamery introduced Gluten-Free Cookie Dough to its organic ice cream product line. The ice cream is produced using organic milk and cream from family farms in Northern California.

Global Organic Ice Cream Market Report Scope

Organic ice cream is ice cream made using organically sourced ingredients, such as milk, cream, and sweeteners, produced without synthetic pesticides, hormones, or artificial additives. The organic ice cream market is segmented by ingredient source, flavor, product type, distribution channel, and geography. By ingredient source, the market includes dairy-based and non-dairy-based products. By flavor, the market covers vanilla, chocolate, fruit-flavored, and other variants. Based on product type, the market is categorized into pints, cones, bars, and other formats. By distribution channel, the market is segmented into foodservice and retail. By geography, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East and Africa, with market size and forecasts provided for each region. For each segment, market sizing and forecasts have been done on the basis of value (USD million) and volume (Tons).

| Dairy Based |

| Non-dairy Based |

| Vanilla |

| Chocolate |

| Fruit-Flavored |

| Others |

| Pints |

| Cones |

| Bars |

| Others |

| Foodservice | |

| Retail | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Ingredient Source | Dairy Based | |

| Non-dairy Based | ||

| By Flavor | Vanilla | |

| Chocolate | ||

| Fruit-Flavored | ||

| Others | ||

| By Product Type | Pints | |

| Cones | ||

| Bars | ||

| Others | ||

| By Distribution Channel | Foodservice | |

| Retail | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the organic ice cream market in 2031?

The organic ice cream market size is expected to reach USD 3.57 billion by 2031.

Which region will grow the fastest to 2031?

Asia-Pacific is forecast to expand at an 11.59% CAGR, the highest among all regions.

What ingredient source is gaining share most rapidly?

Non-dairy alternatives such as oat and pea bases are projected to grow at an 11.86% CAGR, narrowing the gap with traditional dairy.

Why are organic ice cream bars gaining traction?

Bars offer portion control and on-the-go convenience, supporting a 10.64% CAGR through 2031.

How are manufacturers addressing high organic milk costs?

Strategies include vertical integration with certified farms, precision-fermentation partnerships, and premium pricing backed by indulgent flavors.

Page last updated on: