Pizza Foodservice Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 158.93 Billion |

| Market Size (2031) | USD 257.17 Billion |

| Growth Rate (2026 - 2031) | 10.10% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Pizza Foodservice Market Analysis by Mordor Intelligence

The pizza foodservice market size is expected to increase from USD 144.08 billion in 2025 to USD 158.93 billion in 2026 and reach USD 257.17 billion by 2031, growing at a CAGR of 10.10% over 2026-2031. The global surge is fueled by an increasing appetite for on-the-go meals, swift menu tweaks, and engaging dining experiences. Data from the U.S. Securities and Exchange Commission reveals that in 2024, U.S. consumers shelled out approximately USD 42.1 billion at quick-service pizza joints, up nearly two percent from the USD 41.3 billion spent the year prior [1]Source: U.S. Securities and Exchange Commission, "Domino's Pizza Inc. Form 10-K 2024", sec.gov. Operators are leveraging technological advancements, from automated make-lines to astute demand forecasting, to reduce labor demands and enhance efficiency. They're not stopping there; operators are adopting sustainable delivery methods, such as electric two-wheeler fleets and eco-friendly packaging. These choices aren't solely about cost savings; they're strategic moves to cultivate consumer trust. Flavor innovation plays a pivotal role, with fusion toppings resonating with a wider audience and commanding premium pricing.

Key Report Takeaways

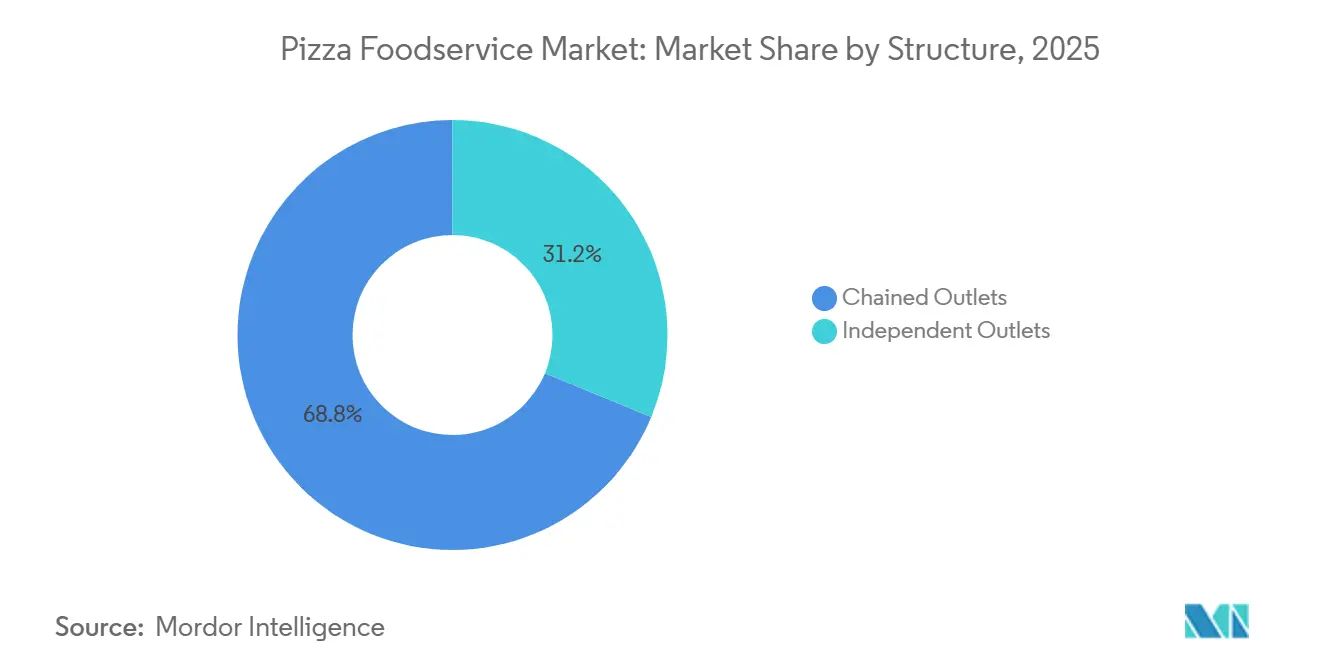

- By structure, chained outlets held 68.77% of the pizza foodservice market share in 2025, while independent outlets are expanding at a 10.13% CAGR through 2031.

- By service model, carry-out and take-away operations commanded 45.04% of the pizza foodservice market in 2025, and delivery-only ghost kitchens are forecast to post a 10.27% CAGR to 2031.

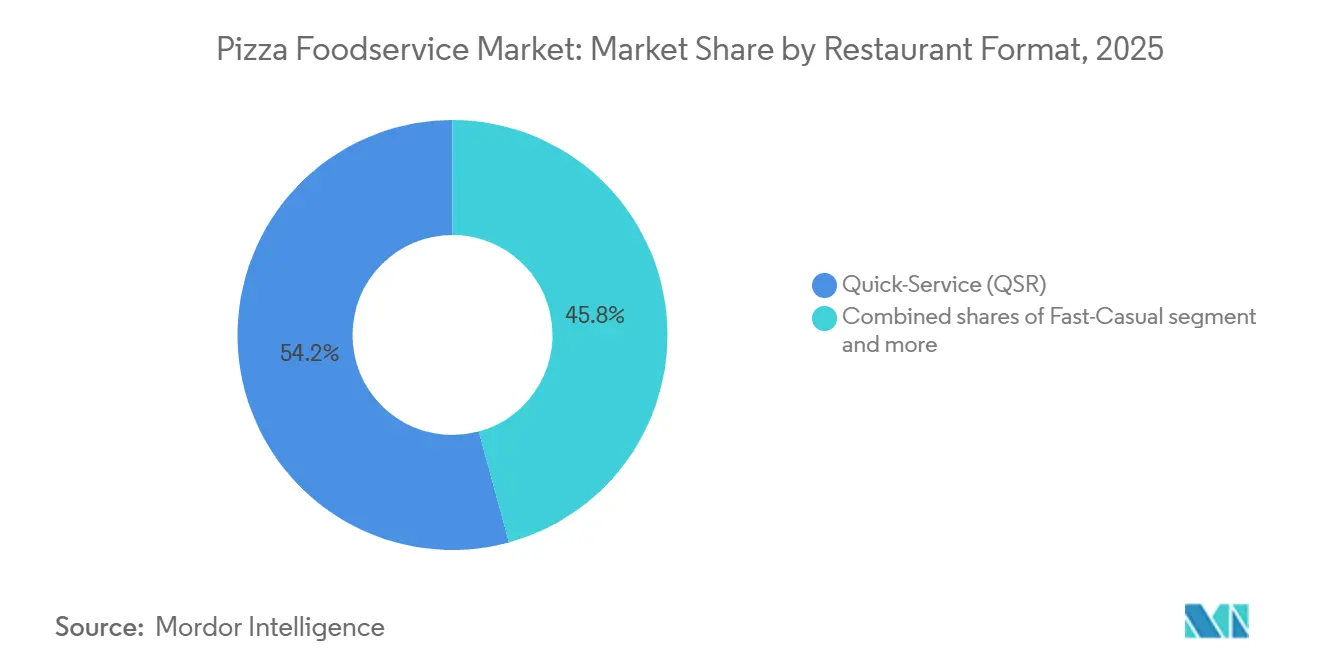

- By restaurant format, quick-service venues captured 54.24% of the 2025 pizza foodservice market size, yet fast-casual concepts are projected to grow at an 11.03% CAGR.

- By location, standalone stores represented 76.24% of the pizza foodservice market in 2025, whereas lodging-based outlets are advancing at 10.44% CAGR.

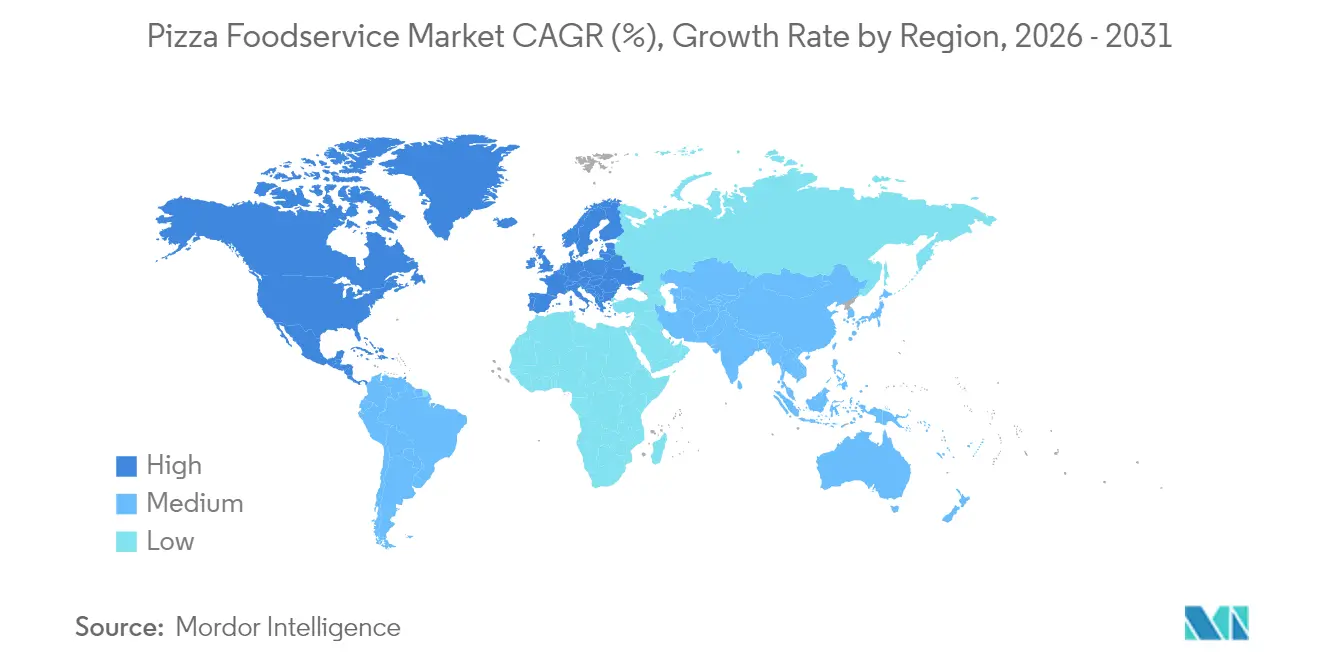

- By geography, North America led with 38.11% of the pizza foodservice market share in 2025, and Asia-Pacific is expected to register the fastest CAGR of 10.56% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pizza Foodservice Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global culinary trends: from fusion pizzas to AR packaging | +1.5% | Global, with early gains in North America, Asia-Pacific | Medium term (2-4 years) |

| Robot-driven and automated kitchen operations | +1.2% | North America and Europe, spill-over to Asia-Pacific | Long term (≥ 4 years) |

| Plant-based and functional ingredients | +0.8% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Digital innovation and interactive packaging | +0.6% | Asia-Pacific core, spill-over to North America | Long term (≥ 4 years) |

| Delivery platforms boost pizza ordering growth | +1.1% | Europe and North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Affordability increases pizza foodservice appeal | +0.7% | Global, with premium positioning in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Global culinary trends: from fusion pizzas to AR packaging

U.S. consumers are increasingly gravitating towards international flavors, reshaping pizza menus across the nation. Data from the U.S. Securities and Exchange Commission reveals that U.S. consumers spent about USD 16.9 billion on pizza deliveries in 2024, marking a modest rise from the USD 16.5 billion spent the year prior [2]Source: U.S. Securities and Exchange Commission, "Domino's Pizza Inc. Form 10-K 2024", sec.gov. Traditional Italian pizzas set the stage, but today's menu is a vibrant tapestry, weaving in influences from Mexican and Greek to Korean, Indian, and various regional fusions. These dishes, while tailored to local tastes, maintain a universal appeal. With the market reaching saturation, the emergence of fusion flavors provides both chains and independent pizzerias a unique opportunity to differentiate themselves. By embracing this trend, pizza chains are not only commanding premium prices but also drawing in a wider audience, including those who previously viewed pizza as monotonous.

Robot-driven and automated kitchen operations

Capriotti's Sandwich Shop has partnered with Piestro to introduce automated pizza kiosks that can craft, slice, and box pizzas in just three minutes. Over the next five years, Capriotti's plans to acquire up to 100 of these kiosks, aiming to enhance dinner service and boost revenue during typically slower hours. This initiative addresses labor shortages, improves consistency, and reduces operational costs, especially crucial with rising minimum wages in key markets. In a similar vein, Donatos Pizza unveiled its fully autonomous pizza restaurant in June 2025. Operated by HMS Host, the restaurant will run 24/7, utilizing advanced robotics and data science technologies to streamline the customer experience, from order placement to pizza delivery.

Plant-based and functional ingredients

Plant-based proteins are making a strong comeback in the U.S. foodservice sector, even outpacing sales figures from before the pandemic. Quick-service restaurants are at the forefront of this trend, leading in plant-based protein sales. Pizza operators, in particular, are capitalizing on this surge, effortlessly integrating cheese alternatives and plant-based meat toppings into their menus. This segment is thriving, thanks to the environmental and health awareness of younger consumers, enabling them to command premium prices on ingredients deemed nutritionally advantageous. However, challenges persist: achieving taste parity and staying price-competitive are significant obstacles. Success in this arena depends on building strategic partnerships with suppliers and smartly positioning items on the menu. Moreover, this plant-based trend aligns with broader sustainability efforts, allowing operators to meet corporate environmental objectives while responding to evolving consumer demands.

Digital innovation and interactive packaging

Digital innovation and interactive packaging are enhancing the customer experience in pizza foodservice by making ordering faster, more personalized, and engaging. QR codes, NFC tags, and smart boxes allow customers to access menus, promotions, loyalty rewards, and reheating instructions instantly from their phones. Augmented-reality packaging and gamified campaigns encourage repeat purchases and social media sharing, especially among younger consumers. Data collected through connected packaging also helps brands tailor offers and predict demand more accurately. Together, these technologies increase convenience, brand engagement, and customer retention for pizza chains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating costs of ingredients | -0.9% | Global, with an acute impact in emerging markets | Short term (≤ 2 years) |

| Competition from alternative fast foods intensifies | -0.6% | Global, concentrated in mature markets | Medium term (2-4 years) |

| Ensuring quality consistency across locations | -0.8% | Global, particularly challenging for rapid expansion | Medium term (2-4 years) |

| Health concerns limit traditional pizza consumption | -0.5% | North America and Europe, emerging in the Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fluctuating costs of ingredients

Key ingredients in pizza-making, such as tomatoes and olive oil, have seen dramatic price hikes over the past four years, reshaping the economics of the beloved dish. In 2024, the Bureau of Labor Statistics reported that the retail price of field-grown tomatoes in the U.S. climbed to USD 2.07 per pound, up from USD 1.99 the year prior [3]Source: Bureau of Labor Statistics, "Average Retail Food and Energy Prices, U.S. and Midwest Region", bls.gov. Labor costs are adding to the challenges. New York's minimum wage surged from USD 7.15 in 2007 to an eye-popping USD 16 in 2024. This leap has forced operators to rethink their pricing strategies, even if it means potentially alienating some customers. Consequently, in 2024, restaurant menu prices have seen an uptick, widening the gap between the costs of dining out and home-cooked meals. Operators are responding with tactics like menu engineering, optimizing portions, and broadening their supply chains. Yet, the shadow of persistent inflation looms large, threatening profitability for many.

Ensuring quality consistency across locations

Major restaurant chains are witnessing growth in same-store sales, even as the overall restaurant sales see an uptick. This trend underscores a shift in consumer preferences, leaning towards unique dining experiences and local authenticity, rather than the predictability offered by chain establishments. Over the last decade, a proliferation of restaurant locations has intensified competition, leading to a dilution of consumer spending among established brands. Furthermore, with menu saturation, operators grapple to distinguish themselves in traditional pizza categories while maintaining operational efficiency. While this landscape benefits independent operators and newcomers with unique value propositions, it compels established chains to not only innovate but to fundamentally transform the dining experience, moving beyond mere menu adjustments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Structure: Chains Leverage Scale While Independents Pursue Authenticity

In 2025, chained outlets dominated the market with a commanding 68.77% share. Their success stemmed from standardized operations, efficient supply chains, and robust brand recognition, enabling rapid scaling across diverse markets. Meanwhile, independent outlets are on the rise, boasting a projected CAGR of 10.13% through 2031. This growth is driven by a consumer shift towards authentic, locally-sourced experiences, a realm where chains struggle to compete. This trend underscores a broader market dichotomy: the benefits of scale versus the charm of personalization and community connection. Independent operators are leveraging social media and local partnerships to build loyalty, while chains invest heavily in technology and automation to maintain their cost advantage.

Franchise models are evolving to adapt to these market shifts. Take pizza, for example: it's ambitiously targeting 250-300 new stores by 2030, with a significant 80-90% of these being franchised. This approach combines the strength of a well-known brand with local oversight. Such a franchise strategy not only speeds up expansion but also ensures attentiveness to local market intricacies, though it demands strong support systems to maintain quality. The market is also seeing increased consolidation, highlighted by acquisitions like 1000 Degrees' purchase of My Pie, which aims to leverage operational synergies and expand market presence. These shifting dynamics suggest a market bifurcation: one side prioritizes large-scale efficiency, while the other celebrates hyper-local uniqueness, leaving mid-sized players in a strategic quandary.

By Service Model: Ghost Kitchens Navigate Post-Hype Reality

In 2025, carry-out and take-away operations seized a commanding 45.04% market share, highlighting a steadfast consumer preference for convenience and value, even in the face of economic shifts. While dine-in services cater to select occasions and demographics, delivery-only ghost kitchens are poised for a 10.27% CAGR expansion, navigating challenges that have tempered earlier industry forecasts. Even as diners returned to traditional restaurants post-pandemic, ghost kitchens, facing setbacks, are evolving. Many operators are now diversifying into catering and event services, broadening their revenue streams beyond just delivery.

This shift in service models signals a profound change in consumer behavior and operational economics, rather than mere transient trends. Take Domino's as a case in point: their venture into third-party delivery partnerships underscores how established chains are not only adopting aggregator platforms but also fostering direct customer relationships. This dual approach not only facilitates market growth but also protects existing channels, though it demands careful margin management and brand oversight. As operators shift their emphasis from mere expansion to profitability, the segmentation of service models is set for further refinement, with the most successful ones demonstrating strong unit economics and adept customer acquisition tactics.

By Restaurant Format: Fast-Casual Gains Premium Positioning

In 2025, quick-service restaurants (QSRs) maintained a robust 54.24% market share, capitalizing on operational efficiency and value-driven strategies amidst economic headwinds. Meanwhile, fast-casual dining surged ahead with a notable 11.03% CAGR, drawing in consumers willing to pay a premium for superior quality, customization, and distinctive experiences. While full-service and casual dining pizza outlets cater to specific occasions, they find themselves in a competitive tussle, challenged by the value propositions of QSRs and the convenience of fast-casual dining. This segmentation reflects a wider industry trend: a clear divide between value and premium offerings, with middle-market concepts feeling the pinch.

As we approach 2026, pizza lovers can anticipate a rise in toppings like olives, kimchi, and sauerkraut, along with an uptick in mentions of sourdough crusts. These culinary shifts predominantly benefit fast-casual operators, who skillfully navigate menu complexities while maintaining operational efficiency. This transformation in dining formats also highlights trends in the labor market. Fast-casual establishments, by providing better working conditions and growth prospects, are successfully luring top talent in a competitive landscape. Additionally, there's a noticeable split in technology adoption: QSRs focus on automation for efficiency, while fast-casual venues emphasize enhancing customization and the overall customer experience.

By Location: Standalone Dominance Faces Non-Traditional Growth

In 2025, standalone locations dominated the market, seizing 76.24% of the share. Their success stemmed from dedicated kitchen spaces, ample parking, and heightened brand visibility, all vital for traditional pizza operations. On the other hand, lodging locations are gaining momentum, boasting a notable 10.44% CAGR growth. Hotels and resorts, increasingly drawn to the pizza trend, are catering to a diverse guest demographic and even extending their service hours. Retail spots in shopping centers and travel hubs enjoy a consistent customer influx but face challenges with high rental costs and operational hurdles. Leisure venues, spanning entertainment spots to sports facilities, see lucrative opportunities during events but require nimble staffing and savvy inventory management.

This shift in location strategy highlights changing consumer behaviors and real estate trends, with an emphasis on flexibility and convenience. In a significant move, Casey's invested USD 1.145 billion in July 2024 to acquire 198 CEFCO convenience stores. This acquisition underscores pizza operators' strategy to venture into unconventional locales, aiming to capture fresh demand. By merging with convenience stores, pizza sales can now penetrate underserved markets and operate during extended hours, though this comes with the challenge of specialized equipment and customized operational procedures. In a parallel strategy, Mr. Gatti's teamed up with Walmart in July 2024, launching 92 units within retail spaces. This collaboration is a strategic play on foot traffic and the convenience factor. Such forward-thinking location strategies signal a market evolution, transitioning from traditional restaurant settings to a fusion of retail and hospitality partnerships.

Geography Analysis

In 2025, North America commanded a significant 38.11% share of the pizza foodservice market. This dominance was fueled by strong delivery networks, unwavering customer loyalty, and a robust cold-chain infrastructure. Recent USDA relaxations on pizza standards have given operators the green light to experiment with toppings beyond the classic tomato and cheese, accelerating recipe innovations. Yet, as ingredient costs climb and labor markets tighten, maintaining profit margins has become increasingly challenging. In response, many are turning to investments in kitchen robotics and adopting dynamic pricing strategies.

Asia-Pacific, with a projected growth rate of 10.56% CAGR, is emerging as a key player. In early 2024, a major Chinese chain celebrated a year-on-year revenue boost, driven by its ambitious plan to expand to over 600 stores by 2026. Western fast-food brands are making notable strides in the region, racking up sales of 268 billion yuan in 2023, with many brands operating over 10 outlets each. Localization is key, with strategies like introducing seafood toppings in coastal areas and crafting lower-cheese pies for lactose-sensitive diners proving effective.

Europe's pizza market is on a steady, albeit slow, growth trajectory, influenced by premiumization and sustainability trends. The UK's pizza sales approached the billion mark, buoyed by the rise of "fakeaway" kits that blend takeout convenience with home cooking. Meanwhile, urban expansion and rising disposable incomes are driving momentum in South America, the Middle East, and Africa. Partnerships are proving pivotal in global expansions, as evidenced by a South Korean mini-pie brand, backed by a Thai conglomerate, boasting 450 outlets across seven countries and eyeing a leap to 1,200 by year's end.

Competitive Landscape

The pizza foodservice market is moderately fragmented. Multinational chains leverage logistics on a grand scale, while independent operators thrive on their local appeal. In 2024, inflationary pressures and unpredictable demand led twenty prominent chains to file for bankruptcy. However, the top five players, armed with substantial purchasing power, navigate raw-material fluctuations adeptly and invest in proprietary applications. Digital platforms have emerged as pivotal battlegrounds. A major U.S. chain broadened its reach via a third-party aggregator, simultaneously enhancing incentives on its loyalty app to protect profit margins.

Another brand's commissary model, which supplies dough and toppings to franchisees for consistency, also boosts royalty collections. Collaborations in automation, from conveyorized smart ovens to self-driving delivery pods, highlight a dedication to labor optimization through capital investment. Independent operators are getting creative, sourcing hyper-locally and introducing unique menu items like kimchi-bacon slices and matcha-dessert pizzas. While corporate chains struggle to connect with communities, independents excel on social media.

Consolidators are actively reshaping the landscape: a regional franchisor with 400 units has acquired a rising artisan competitor, strategically placing them in convenience marts to cut overheads and enhance cross-promotion. The financing landscape is diverse. Private equity favors asset-light franchisors with positive same-store sales. In contrast, corporates facing margin squeezes contend with high debt costs. While public offerings remain scarce, strategic partnerships, particularly with infrastructure or retail landlords, not only offer growth capital but also ensure distribution agreements.

Pizza Foodservice Industry Leaders

-

Papa John's International, Inc.

-

Yum! Brands, Inc.

-

Domino's Pizza, Inc.

-

Little Caesar Enterprises, Inc.

-

MOD Super Fast Pizza, LLC.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Sofia’s Pizzeria, a family-owned establishment in San Antonio, debuted its inaugural restaurant in New Braunfels, right by the historic downtown. On Saturday, February 7, Sofia's welcomed patrons to savor its renowned offerings - from pizza slices to salads and pasta - all crafted with the same dedication and quality that garnered acclaim in San Antonio, as highlighted in their announcement.

- June 2025: Pizza chain Pizza Hut opened its first all-women-operated outlet in India. The store is located in Gangtok, empowering more women in the workforce and ensuring an ‘Equal Slice for Everyone’. From store function, food preparation, and customer service to day-to-day management, everything will be managed by the all-women team.

- April 2025: Domino's Pizza Inc. entered into a partnership with DoorDash in North America. The partnership will allow Domino's to reach new customers through DoorDash Marketplace, while continuing its delivery service by Domino's drivers. A pilot was conducted in select locations, with a nationwide U.S. launch, which began in May 2025, and across Canada later in 2025.

- March 2025: Domino’s Pizza India launched the Big Big 6-in-1 Pizza, a 24-slice offering designed for group dining. The new pizza featured six distinct flavors, catering to different preferences in a single order. The Big Big 6-in-1 Pizza was made available at an introductory price of INR 799 for the vegetarian variant and INR 899 for the non-vegetarian variant.

Global Pizza Foodservice Market Report Scope

Pizza foodservice is a pizza outlet that offers different types of pizza to consumers across the globe. Foodservice includes the businesses, institutions, and companies that prepare meals outside the home. The Pizza Foodservice Market is Segmented by Structure (Chained Outlets and Independent Outlets), Service Model (Delivery-Only (Ghost Kitchens), Dine-In, and Carry-Out/Take-Away), Restaurant Format (Quick-Service (QSR), Fast-Casual, and Full-Service/Casual Dining), Location (Leisure, Lodging, Retail, Standalone, and Travel), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Chained Outlets |

| Independent Outlets |

| Quick-Service (QSR) |

| Fast-Casual |

| Full-Service/Casual Dining |

| Delivery-only (Ghost Kitchens) |

| Dine-in |

| Carry-out/Take-away |

| Leisure |

| Lodging |

| Retail |

| Standalone |

| Travel |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | India |

| Japan | |

| Australia | |

| China | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Structure | Chained Outlets | |

| Independent Outlets | ||

| By Restaurant Format | Quick-Service (QSR) | |

| Fast-Casual | ||

| Full-Service/Casual Dining | ||

| By Service Model | Delivery-only (Ghost Kitchens) | |

| Dine-in | ||

| Carry-out/Take-away | ||

| By Location | Leisure | |

| Lodging | ||

| Retail | ||

| Standalone | ||

| Travel | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| Japan | ||

| Australia | ||

| China | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the global pizza foodservice market in 2026?

The pizza foodservice market size is USD 158.93 billion in 2026, with a 10.10% CAGR forecast to 2031.

Which region is expanding the fastest for pizza chains?

Asia-Pacific leads growth, projected at a 10.56% CAGR through 2031, driven by urbanization and rising incomes.

How are operators addressing labor shortages?

Chains invest in robotic dough presses, automated kiosks, and AI scheduling to curb labor expenses and boost consistency.

Why is sustainability critical for pizza operations?

Electric delivery fleets and recyclable packaging cut operating costs and attract eco-conscious younger diners, supporting brand loyalty and modest price premiums.

Page last updated on: