Frozen Seafood Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

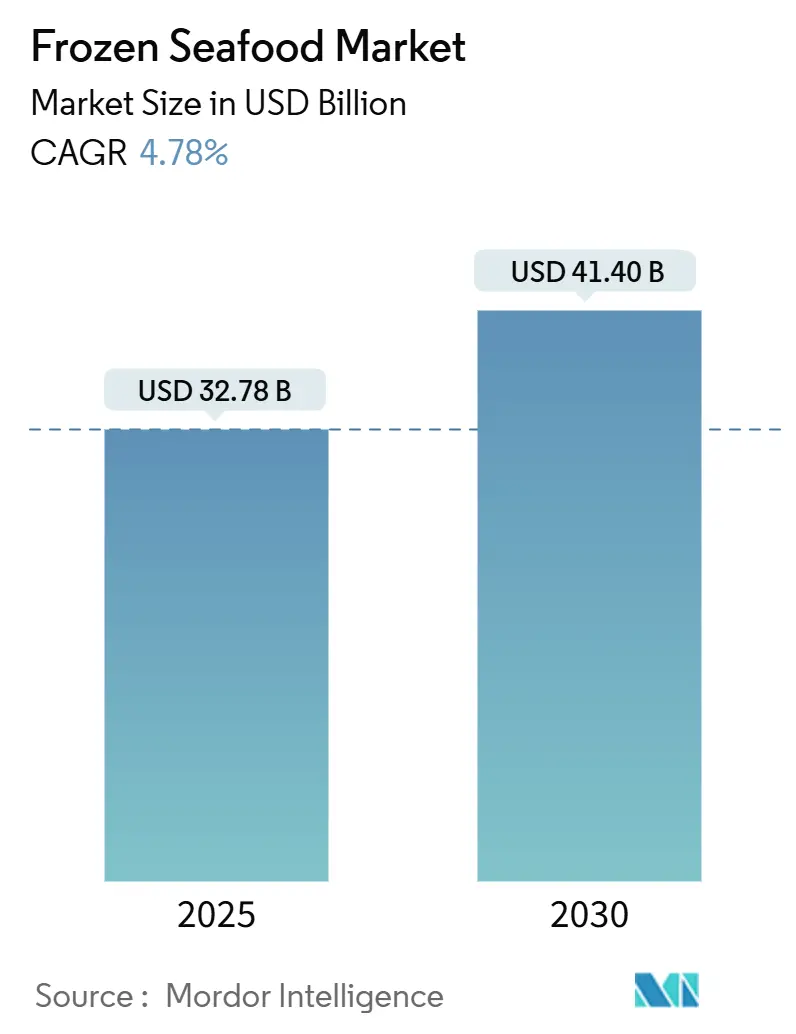

| Market Size (2025) | USD 32.78 Billion |

| Market Size (2030) | USD 41.40 Billion |

| Growth Rate (2025 - 2030) | 4.78% CAGR |

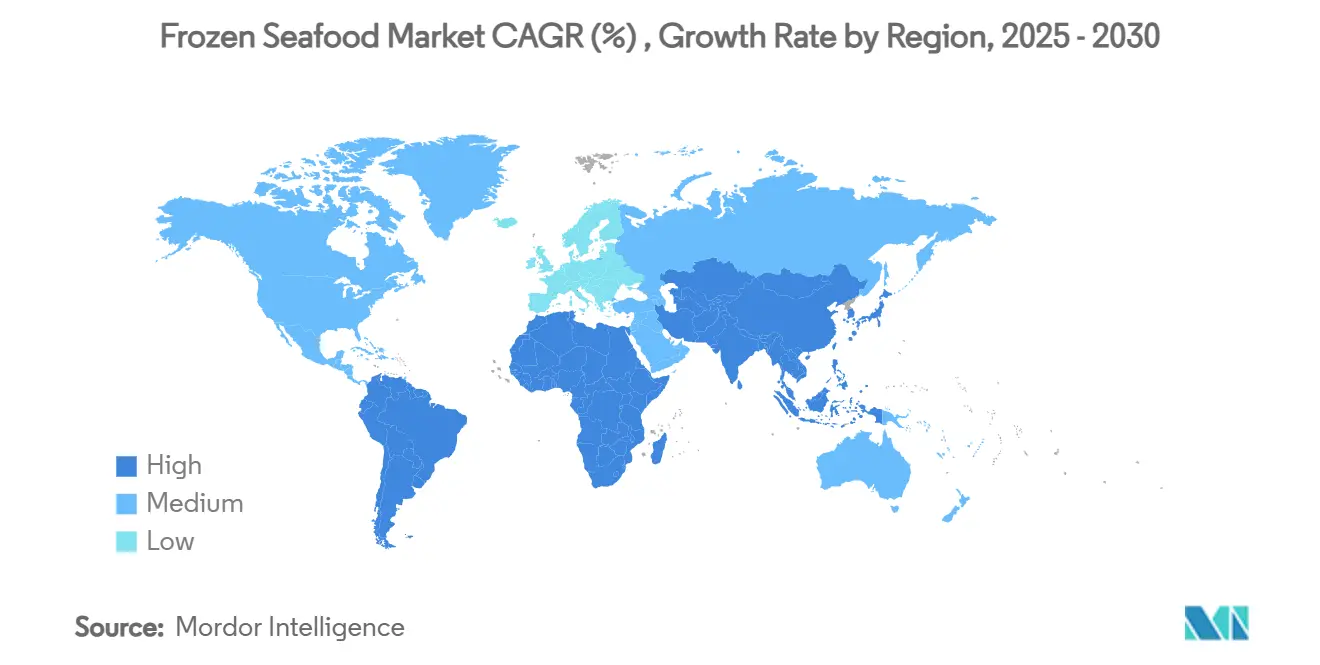

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Frozen Seafood Market Analysis by Mordor Intelligence

The Frozen Seafood Market size is estimated at USD 32.78 billion in 2025, and is expected to reach USD 41.40 billion by 2030, at a CAGR of 4.78% during the forecast period (2025-2030).

This growth trajectory reflects the sector's resilience amid evolving consumer preferences and technological advancements that are reshaping traditional seafood distribution models. The market's expansion is driven by sophisticated cold chain innovations, regulatory harmonization across key importing regions, and the emergence of Individual Quick Frozen (IQF) technology as a quality differentiator rather than merely a preservation method. The region's dual role as the world's largest aquaculture producer and fastest-growing consumer market creates unique supply-demand dynamics that influence global pricing and trade flows [1]Source: Food and Agriculture Organization, “State of World Fisheries and Aquaculture 2024,” fao.org.

Key Report Takeaways

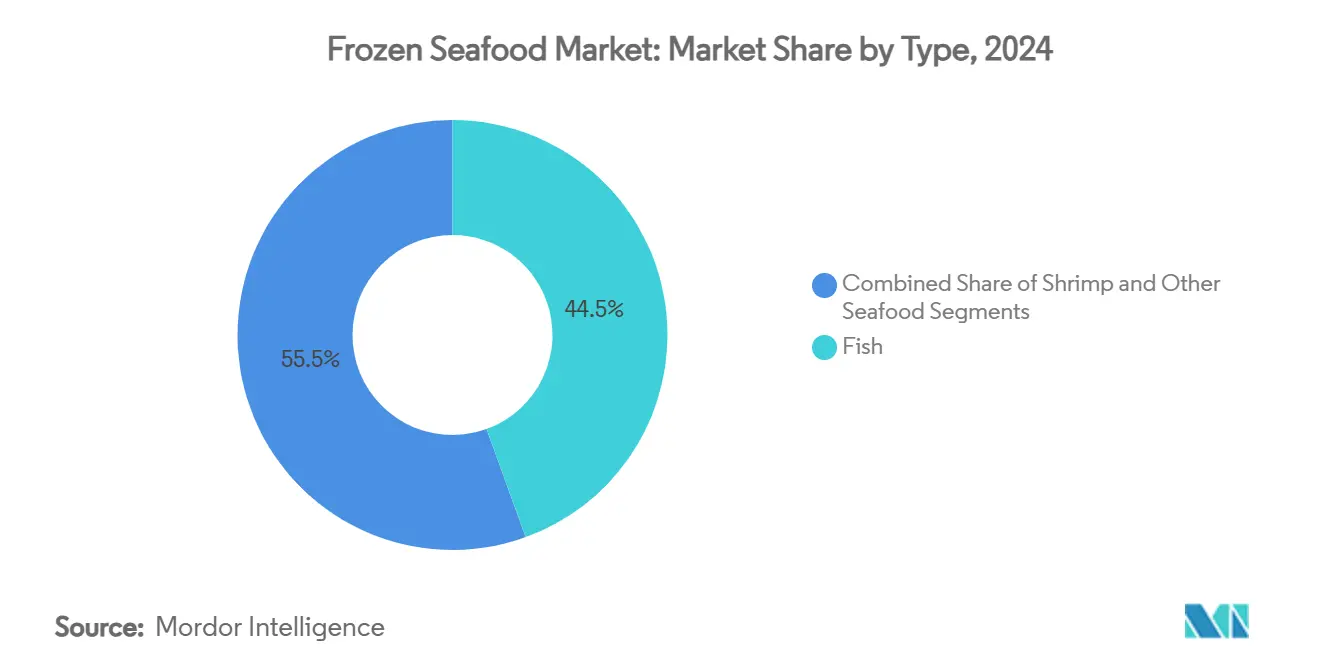

- By type, fish led with 44.46% of frozen seafood market share in 2024, while shrimp is projected to grow at a 5.75% CAGR through 2030.

- By freezing technology, block frozen held 43.32% of the frozen seafood market in 2024; IQF is expected to expand at a 5.84% CAGR to 2030.

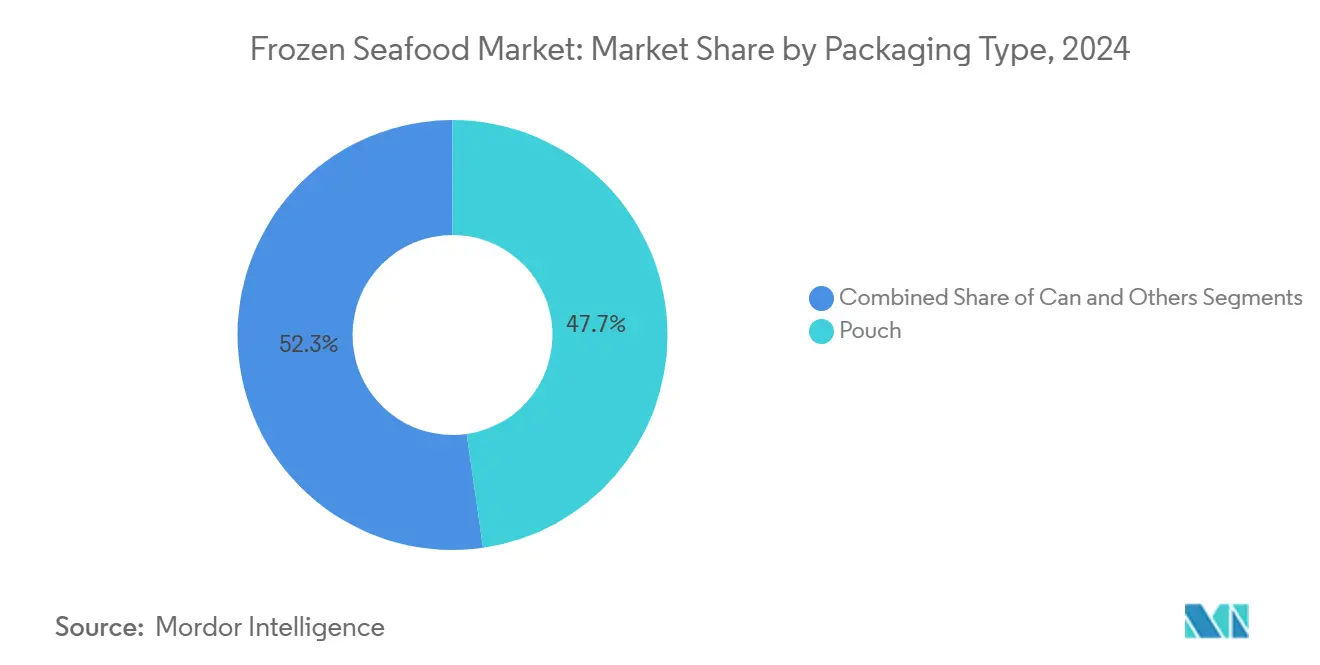

- By packaging, pouches captured 47.74% share of the frozen seafood market in 2024 and are set to rise at a 6.06% CAGR over 2025-2030.

- By distribution channel, off-trade outlets accounted for 68.46% of 2024 value; on-trade sales should grow fastest at a 5.98% CAGR through 2030.

- By geography, Asia-Pacific controlled 38.83% of 2024 revenue and is projected to post a 5.78% CAGR during the forecast period.

Global Frozen Seafood Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for convenient and time-saving food solutions | +1.2% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Increasing demand for extended shelf-life products | +0.8% | Global, particularly emerging markets in APAC and MEA | Long term (≥ 4 years) |

| Year-round availability of frozen seafood drives | +0.9% | Global, with seasonal variations in temperate regions | Long term (≥ 4 years) |

| Advanced freezing technologies transform food preservation | +1.1% | APAC core, spill-over to North America and Europe | Medium term (2-4 years) |

| Consumer preference for premium and organic products | +0.7% | North America and EU, expanding to urban APAC | Medium term (2-4 years) |

| Rising emphasis on food safety standards and compliance | +0.6% | Global, with stricter implementation in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Convenient and Time-saving Food Solutions

The increasing consumer preference for convenient purchasing options continues to shape the development and distribution strategies of frozen seafood products. Both individual consumers and foodservice establishments actively seek products that streamline their preparation processes and reduce kitchen time. E-commerce platforms have witnessed substantial growth in ready-to-cook frozen seafood meal sales, reflecting this shift in consumer behavior. The frozen format effectively addresses a common consumer pain point - food waste concerns that traditionally deterred many from purchasing fresh seafood. These combined factors have positively influenced seafood consumption patterns, with American consumers reporting higher seafood intake levels, primarily attributed to the availability of easier preparation methods.

Increasing Demand for Extended Shelf Life Products

The growing concerns over supply chain reliability have transformed extended shelf life from a mere convenience into a critical business necessity for both retailers and their customers. Modern packaging innovations, particularly vacuum skin packaging and modified atmosphere systems, are successfully extending product longevity while delivering quality standards that match fresh alternatives. This presents a compelling economic opportunity, especially in markets where cold chain infrastructure is limited. In these regions, frozen products can effectively bridge the gap by reaching consumers who previously had no access to fresh seafood, thereby creating new market opportunities and expanding the overall seafood consumption footprint.

Year-Round Availability of Frozen Seafood

Frozen processing serves as a crucial mechanism for stabilizing prices in wild-caught fisheries by effectively managing seasonal supply variations through strategic inventory management and demand balancing. The process enables fishing communities to process their peak-season catches for distribution throughout the year, ensuring their economic sustainability while delivering reliable supply to both consumers and foodservice businesses. This approach is particularly valuable for high-value species such as wild salmon, where seasonal availability continues to shrink due to shifting fishing patterns caused by climate changes. In the aquaculture sector, companies increasingly implement frozen processing methods to effectively manage their production cycles and maximize facility efficiency. The ability to adjust harvest timing has become a significant operational advantage, especially in markets characterized by frequent price and demand fluctuations.

Advanced Freezing Technologies Transform Food Preservation

Individual Quick Frozen (IQF) technology has transformed from a conventional preservation method into a sophisticated quality enhancement solution. The technology's precision in maintaining cellular structure and preventing ice crystal formation enables food processors to deliver superior products that command higher market prices. This advancement directly addresses the growing consumer preference for restaurant-quality frozen meals at home, allowing families to enjoy premium dining experiences in their own kitchens. The incorporation of AI-based temperature monitoring and predictive maintenance systems has revolutionized processing operations, delivering improved efficiency while simultaneously reducing energy consumption and minimizing waste generation across the production chain.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Perception of Lower Quality Compared to Fresh Seafood | -0.9% | Global, particularly pronounced in developed markets | Medium term (2-4 years) |

| Risk of Contamination and Food Safety Issues | -0.7% | Global, with heightened concerns in import-dependent regions | Short term (≤ 2 years) |

| High Logistics and Transportation Costs | -1.1% | Global, with acute impact on island nations and remote regions | Long term (≥ 4 years) |

| Exhaustive Investment for Cold Chain Setup | -0.8% | Emerging markets in APAC, MEA, and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Perception of Lower Quality Compared to Fresh Seafood

Consumer perception challenges remain, even though technological advances have significantly reduced quality differences between frozen and fresh seafood products. This perception issue is prominent in foodservice, where chefs and consumers prefer fresh products due to historical quality differences that modern freezing technology has now largely eliminated. Industry associations and retailers are implementing educational initiatives to change consumer understanding, with taste tests showing that properly frozen seafood using advanced 3D freezing technology can achieve comparable quality to fresh products. The pricing dynamics present an additional challenge, as frozen products must compete on value rather than premium positioning, which restricts margin expansion opportunities for processors.

Risk of Contamination and Food Safety Issues

Food safety concerns significantly influence how consumers perceive frozen seafood products compared to other protein options, even though scientific data consistently demonstrates lower contamination rates in properly processed frozen seafood. The intricate nature of global seafood supply chains, involving multiple touchpoints across different countries and handling processes, makes the industry more susceptible to contamination events. These incidents can substantially damage both the category's reputation and consumer confidence in frozen seafood products. When food safety incidents occur, regulatory bodies typically respond by implementing more rigorous inspection requirements and stricter import controls, which ultimately creates supply chain disruptions and adds considerable operational costs for businesses throughout the supply chain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Shrimp Drives Premium Growth

The global seafood market continues to demonstrate strong consumer preference for fish products, which currently hold a commanding 44.46% market share in 2024. This market leadership position stems from the broad diversity of fish species available and well-established consumer preferences across international markets. The industry has built comprehensive supply chains and processing infrastructure to address this consistent market demand, ensuring reliable product availability to consumers worldwide.

The shrimp segment presents a compelling growth story, with projections indicating a CAGR of 5.75% from 2025 to 2030. This growth trajectory is supported by notable advancements in automated processing systems and enhanced disease management protocols in aquaculture operations. Industry leaders like OctoFrost have demonstrated significant operational efficiencies, achieving a tenfold reduction in processing costs while maintaining premium quality standards through mechanical IQF processing. The segment's success is particularly evident in its strategic adaptation to convenience food formats and value-added processing, which generate higher profit margins compared to conventional fish products. In the European market, this trend is clearly visible, with vannamei shrimp maintaining market dominance, while Argentine red shrimp and black tiger shrimp navigate increasing competition from farm-raised alternatives.

By Freezing Technology: IQF Innovation Accelerates

Block freezing technology holds 43.32% market share in 2024, as food processors value its cost-effectiveness in bulk processing and storage efficiency for commercial applications. Individual Quick Frozen (IQF) technology demonstrates strong momentum with 5.84% CAGR growth, responding to increasing consumer demand for portion control and quality preservation, despite commanding premium prices. The performance gap between these technologies continues to narrow as manufacturers enhance IQF systems for better energy efficiency and cost-effectiveness.

Blast freezing and cryogenic systems serve distinct market segments where rapid freezing and superior output quality justify higher processing costs. IQF technology's market growth reflects its success in preserving product integrity and meeting consumer expectations for restaurant-quality frozen products at home. By effectively preventing ice crystal formation and maintaining cellular structure, IQF technology ensures consistent product quality throughout the freezing process.

By Packaging Type: Pouch Dominance Continues

The ready-to-eat meals market has witnessed pouch packaging emerge as the preferred choice, holding a substantial 47.74% market share in 2024 and demonstrating robust growth at a 6.06% CAGR. This format resonates with consumers who value convenience, portion control, and storage efficiency in their daily lives. The success of pouch packaging lies in its exceptional barrier properties that ensure longer shelf life while providing consumers with hassle-free preparation and serving options. While can packaging maintains its strong position in shelf-stable products and institutional applications, other formats such as vacuum-sealed bags and modified atmosphere packaging continue to serve specific market requirements.

Environmental consciousness has become a driving force in the packaging industry, with companies actively pursuing biodegradable materials and circular economy initiatives. In response to this shift, manufacturers are introducing innovative plant-based and compostable alternatives in the pouch segment, balancing environmental responsibility with product protection. The rise of e-commerce has further cemented pouch packaging's market position, as it offers superior product protection during transit while optimizing transportation costs through efficient space utilization. Additionally, the market is seeing advancements in barrier films and printing technologies, driven by consumers' preference for packaging that allows product visibility.

By Distribution Channel: On-Trade Recovery Accelerates

The frozen seafood market demonstrates a clear channel preference, with off-trade channels commanding a substantial 68.46% market share in 2024. These channels, which include supermarkets, hypermarkets, convenience stores, and online retail platforms, continue to serve as the primary access points for consumers seeking frozen seafood products. While supermarkets and hypermarkets maintain their position as market leaders due to their scale advantages and consumer shopping habits, online retail has emerged as the fastest-growing segment, supported by robust cold chain logistics and increasing consumer confidence in frozen food delivery.

In the on-trade segment, which encompasses foodservice establishments and restaurants, the market shows promising growth at 5.98% CAGR. This growth reflects a strategic shift in post-pandemic operations, where businesses increasingly recognize the advantages of frozen seafood. The adoption of frozen products helps these establishments optimize their inventory management, reduce operational waste, and maintain consistent quality standards across their menu offerings, making it a practical choice for foodservice operators looking to balance quality with operational efficiency.

Geography Analysis

Asia-Pacific dominates the global frozen seafood market, accounting for 38.83% of sales in 2024. According to the United States Department of Agriculture, China's frozen seafood imports reached 2.38 MMT in 2024 [2]Source: United States Department of Agriculture, “China Fishery Products Report,” usda.gov, demonstrating the region's significance as both a major producer and consumer. E-commerce companies have developed same-day delivery networks with freezer capabilities, enabling the distribution of wild-caught salmon to inland consumers beyond traditional coastal markets.

The region is projected to grow at a CAGR of 5.78% through 2030, driven by increasing disposable incomes and expanding aquaculture production. Government initiatives supporting cold-chain infrastructure development through digital economy programs strengthen market growth prospects in the region. The Indian fisheries sector has experienced significant growth and transformation from 2004 to 2024, encompassing technological advancements and policy reforms that have enhanced India's position in global fisheries and aquaculture. The Union Budget 2025-26 allocated the highest annual budgetary support of INR 27.04 billion for the fisheries sector, reinforcing India's position in aquaculture and seafood exports [3]Source: Government of India, “India’s Fisheries on the Rise,” pib.gov.in.

North America and Europe maintain stable market presence, with growth opportunities in premium and health-conscious segments. While 54% of U.S. consumers indicate increased seafood consumption compared to two years ago, overall volumes remain sensitive to inflation. South America, the Middle East, and Africa present growth potential due to expanding middle-class populations. Brazil experienced significant growth in farmed salmon demand in 2023, while tilapia continues to gain popularity as an affordable domestic option.

Competitive Landscape

Large companies in the frozen seafood market are integrating vertically from feed production to finished goods to ensure supply chain control and maximize profit margins. Premium segment players implement digital traceability systems and machine-vision grading technology to verify product origin and quality standards. The market maintains a fragmented structure with regional processors competing alongside multinational companies.

Companies are rapidly advancing in alternative protein development following the FDA's approval of cell-cultured salmon in 2025. This segment shows significant growth potential as companies develop products such as algae-based coatings and fish-skin collagen snacks to address sustainability demands. The implementation of AI-based demand forecasting and dynamic routing systems reduces waste and enables companies to capitalize on market fluctuations.

In 2025, the market experienced significant merger and acquisition activity as companies pursued scale advantages and geographic expansion. Notable transactions included Captain Fresh's acquisition of CenSea to strengthen U.S. distribution, Mowi's EUR 625 million acquisition of Nova Sea to increase Norwegian salmon production capacity, and Thai Union's USD 883 million purchase of MW Brands and John West, which increased its European market presence to over one-third of total sales. Companies differentiate themselves through specialized capabilities, including organic certification, sustainable sourcing, and direct-to-consumer distribution networks. Increasing regulatory requirements favor well-capitalized companies, indicating a trend toward market consolidation.

Frozen Seafood Industry Leaders

Nippon Suisan Kaisha, Ltd.

Mowi ASA

Thai Union Group PCL

Trident Seafoods Corp.

Austevoll Seafood ASA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Mowi agreed to acquire additional 46% stake in Nova Sea for NOK 7.4 billion (EUR 625 million), enhancing Norwegian salmon market position with expected synergies of NOK 400 million annually.

- December 2024: Pacific Seafood acquired Trident Seafoods' processing facilities in Kodiak: Star of Kodiak, Alkod, and Kodiak Near Island. The acquisition also includes the Plaza bunkhouse apartments for employee accommodation.

- October 2024: Scott & Jon's expanded frozen seafood portfolio with Lemon Butter Dill Salmon Bowl and Baja Fish Taco Bowl made with whitefish, targeting 83% of total frozen seafood category consumption through product diversification.

Global Frozen Seafood Market Report Scope

| Fish |

| Shrimp |

| Other Seafood |

| Block Frozen |

| Individual Quick Frozen (IQF) |

| Others |

| Can |

| Pouch |

| Others |

| On-Trade | |

| Off-Trade | Supermarkets and Hypermarkets |

| Convenience Stores | |

| Online Retail | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Type | Fish | |

| Shrimp | ||

| Other Seafood | ||

| By Freezing Technology | Block Frozen | |

| Individual Quick Frozen (IQF) | ||

| Others | ||

| By Packaging Type | Can | |

| Pouch | ||

| Others | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets and Hypermarkets | |

| Convenience Stores | ||

| Online Retail | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the frozen seafood market today?

The frozen seafood market is valued at USD 32.78 billion in 2025 and is projected to reach USD 41.40 billion by 2030.

Which product type is expanding fastest?

Shrimp is forecast to grow at a 5.75% CAGR, outpacing fish and other seafood categories through 2030.

What technology is driving premium product growth?

Individual Quick Frozen (IQF) systems deliver portion control and near-fresh quality, supporting a 5.84% CAGR for IQF-processed seafood.

Which region contributes the largest revenue?

Asia-Pacific accounts for 38.83% of 2024 sales and continues to post the highest regional CAGR at 5.78%.

How is the food-service sector influencing demand?

On-trade channels are recovering rapidly, with a 5.98% projected CAGR as restaurants adopt frozen formats for cost and inventory efficiency.

Page last updated on: