Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 101.86 Billion |

| Market Size (2026) | USD 105.74 Billion |

| Market Size (2031) | USD 127.39 Billion |

| Growth Rate (2026 - 2031) | 3.80% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Frozen Food Market Analysis by Mordor Intelligence

The North America frozen food market was valued at USD 101.86 billion in 2025 and is expected to reach USD 105.74 billion in 2026 and USD 127.39 billion by 2031, growing at a CAGR of 3.80%. North America's appetite for frozen food is surging, propelled by a confluence of regional factors. One of the primary factors is the region's fast-paced lifestyle, coupled with an uptick in women's workforce participation, amplifying the demand for convenient meal solutions. As a result, consumers are gravitating towards ready-to-eat and ready-to-cook frozen meals that seamlessly fit into their hectic routines. Bolstering this trend is the region's robust cold chain infrastructure and the omnipresence of modern retail outlets, like supermarkets and hypermarkets, ensuring a broad spectrum of frozen products is readily available. Heightened health awareness among North Americans is steering them towards the rising trend of clean-label and organic frozen foods, further shaping market dynamics. On another front, technological strides in food preservation and packaging are not only enhancing the quality and shelf life of frozen items but also amplifying their allure.

Key Report Takeaways

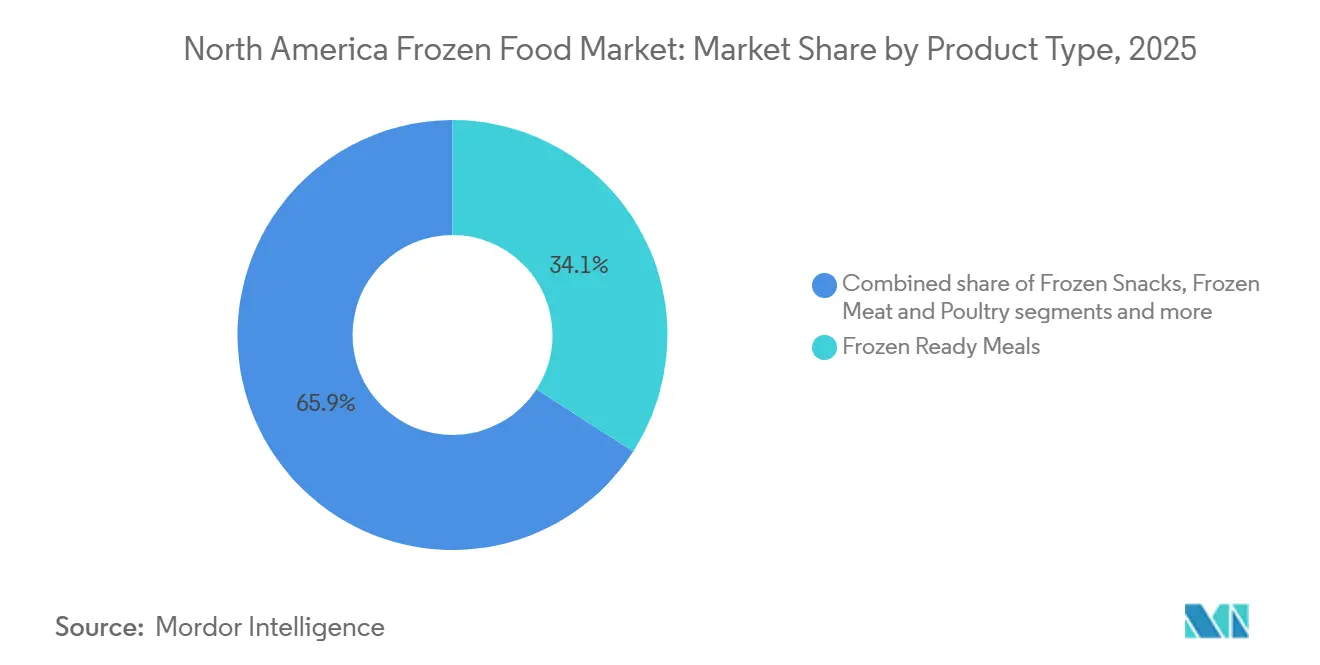

- By product type, frozen ready meals led with 34.12% of the North America frozen food market share in 2025; frozen snacks are projected to grow the fastest at a 6.21% CAGR through 2031.

- By category, the ready-to-eat segment captured 58.43% share of the North America frozen food market size in 2025, while ready-to-cook products are on track for a 6.52% CAGR between 2026-2031.

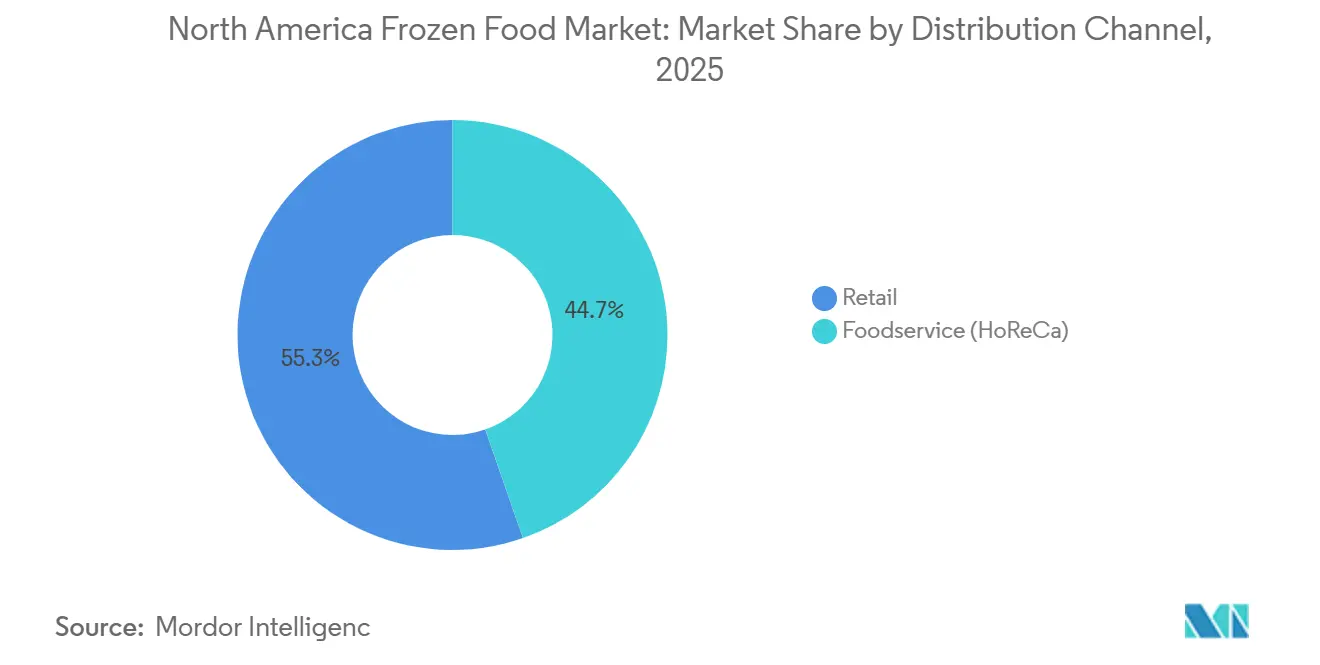

- By distribution channel, retail held 55.32% of the North America frozen food market share in 2025; foodservice (HoReCa) will register the highest growth at an 8.73% CAGR from 2026-2031.

- By geography, the United States dominated with 84.46% revenue share in 2025, whereas Mexico is set to expand the fastest at a 4.86% CAGR from 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Frozen Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for convenience meal solutions among U.S. Millennials and Gen Z | +1.2% | United States, Canada | Medium term (2-4 years) |

| Innovation in plant-based frozen entrées boosting health-positioned offerings | +0.8% | United States, Canada, Mexico | Long term (≥ 4 years) |

| Targeted marketing and advertisements elevating frozen food sales | +0.6% | North America | Short term (≤ 2 years) |

| Technological advancements in freezing and packaging | +0.5% | North America | Medium term (2-4 years) |

| Growing ethnic and global cuisine options | +0.4% | United States, Canada, Mexico | Medium term (2-4 years) |

| Increasing frozen aisles in retail channels | +0.3% | North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising demand for convenience meal solutions among U.S. Millennials and Gen Z

Millennials and Generation Z are significantly influencing the U.S. frozen food market due to their preference for convenient, time-saving meal options that align with their fast-paced and flexible lifestyles. As these generations transition through key life stages, such as living independently and forming households, frozen foods are increasingly perceived as practical everyday solutions rather than occasional purchases. According to the United States Census Bureau, millennials, the largest generational group in the United States as of 2024, account for approximately 74.19 million people, highlighting the substantial demand from this demographic[1]Source: United States Census Bureau, "National Population by Characteristics: 2020-2024", census.gov. Shifting eating habits, characterized by irregular schedules and a preference for smaller, customizable meals, have driven the growing popularity of frozen entrées and snack-style formats that serve as complete meals. In response, food manufacturers are diversifying their offerings by introducing premium, chef-inspired recipes, globally influenced flavors, and higher-quality ingredients. Product innovation now focuses on portion flexibility, enhanced nutritional profiles, and packaging designed for convenience and sustainability.

Innovation in plant-based frozen entrées boosting health-positioned offerings

The United States frozen food market is experiencing significant growth in plant-based frozen entrées, particularly those emphasizing health and wellness. Consumers are increasingly prioritizing frozen meal solutions that strike a balance between convenience and nutritional value, catering to diverse dietary preferences. To meet this demand, manufacturers are adopting advanced culinary techniques and utilizing high-quality ingredients to create flavorful, nutrient-rich plant-based meals. Reflecting this trend, in July 2024, Korean plant-based brand Unlimeat expanded its footprint in the U.S. by launching five products across 149 Giant and Martin’s stores. This included Korean-inspired plant-based meat alternatives and ready-to-eat options like frozen kimbap, enhancing consumer access to globally influenced, sustainable frozen food options. Increasing awareness of the environmental impact of food choices continues to drive demand for plant-based frozen products, highlighting a broader shift toward sustainable and health-focused offerings within the category. Additionally, the rising influence of GLP-1–based weight management has boosted interest in portion-controlled and calorie-conscious frozen meals. In response to this trend, Conagra introduced GLP-1–friendly labeling on its Healthy Choice frozen meals in January 2025. These initiatives have helped reposition frozen foods as a practical option for health-conscious consumers, improving the category's perception and encouraging wider adoption among wellness-focused segments.

Targeted marketing and advertisements elevating frozen food sales

Brand-led communication strategies are transforming perceptions of frozen foods, particularly among Millennials and Gen Z, by emphasizing digital-first engagement. Leading companies are allocating significant budgets to modern marketing channels; for example, Conagra Brands invested USD 289.6 million in advertising and promotional activities in 2024. Social media has emerged as a key platform for these efforts, allowing brands to connect with younger audiences through influencers, short-form video content, and lifestyle-oriented messaging. According to the International Food Information Council’s 2024 Food and Health Survey, 54% of consumers encounter food-related content on social media, underscoring its growing impact on purchasing decisions. Marketing narratives are increasingly tailored to address consumer priorities, including health, convenience, and efficiency. Campaigns often highlight innovations like Individual Quick Freezing (IQF), which preserves taste, texture, and nutritional value, positioning frozen foods as a practical alternative to fresh options. Industry-led educational initiatives, such as the “Frozen Food Revolution” cited by Procurement Resource, aim to address lingering concerns about quality and freshness at the retail level. By combining these efforts with data-driven targeting and personalized messaging, brands are successfully re-engaging health-conscious consumers who had previously moved away from frozen food categories.

Technological advancements in freezing and packaging

Advanced freezing and packaging technologies are significantly enhancing the quality, efficiency, and sustainability of frozen foods. For example, Individual Quick Freezing (IQF) rapidly freezes products individually, preserving natural cell integrity and resulting in better flavor, texture, and appearance after reheating. Modified Atmosphere Packaging (MAP) extends shelf life by regulating internal gas levels, reducing moisture loss and freezer burn, while also enabling manufacturers to decrease plastic usage, aligning with sustainability goals. Cryogenic freezing, which utilizes liquid nitrogen or carbon dioxide, supports high-throughput production in limited facility spaces, improves energy efficiency, and maintains product quality by minimizing ice crystal formation across various food categories, including proteins, produce, bakery items, and ready meals. Additionally, digital and smart manufacturing solutions are increasingly integrated into frozen food operations. For instance, platforms like JBT’s OmniBlu leverage real-time data monitoring and analytics to optimize process control, minimize equipment downtime, and enable more informed decision-making. As environmental responsibility becomes a priority in the food industry, adopting these advanced technologies is essential. Frozen food producers are utilizing innovation to meet growing consumer demands for quality, transparency, and sustainability while enhancing production efficiency and reducing environmental impact.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Perceived nutritional inferiority vs fresh produce among affluent consumers | -0.6% | United States, Canada | Medium term (2-4 years) |

| Rising competition from fresh meal kits and delivery services | -0.4% | Urban centers across North America | Medium term (2-4 years) |

| Negative perceptions around ultra-processed frozen products | -0.5% | United States, Canada | Long term (≥ 4 years) |

| Energy costs for freezing and storage | -0.2% | North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Perceived nutritional inferiority vs fresh produce among affluent consumers

Frozen fruits and vegetables provide convenience and an extended shelf life but are often viewed by affluent consumers as less nutritious compared to fresh produce. This perception is driven by concerns about nutrient loss during processing and storage, the use of additives, and the belief that these products undergo extensive processing. Millennials, in particular, are highly attentive to food quality and sourcing, showing a preference for products they perceive as more "natural" or minimally processed. Their purchasing decisions are heavily influenced by these factors, reflecting broader consumer trends. According to the International Food Information Council Food and Health Survey 2024, 62% of consumers prioritize health benefits over price when selecting food [2]Source: International Food Information Council, "2024 IFIC Food & Health SURVEY", ific.org. This statistic underscores the significant role that perceived health and quality play in shaping consumer behavior within the frozen food market. Addressing these concerns is crucial for increasing adoption and acceptance, particularly among health-conscious consumers who demand transparency and assurance regarding the nutritional value and processing methods of frozen products.

Rising competition from fresh meal kits and delivery services

The increasing adoption of meal-kit subscriptions and food delivery applications poses a significant challenge to the North American frozen food market, particularly among high-income consumers. These services provide pre-portioned, restaurant-quality meals that are easy to prepare and often feature sustainable, visually appealing packaging. This positions them as premium alternatives to traditional frozen foods. Their customizable options, diverse flavor profiles, and perceived freshness further diminish the appeal of frozen products. Moreover, the ongoing growth of these services pressures frozen food manufacturers to enhance product quality while maintaining cost efficiency. The rising costs of essential raw materials, such as proteins and vegetables, add to the difficulty of offering competitively priced products. Consequently, the frozen food market faces heightened competition from solutions that combine convenience, perceived freshness, and a premium experience, threatening its position within the ready-to-eat and ready-to-cook meal segment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Premium Ready Meals Redefine Value

In 2025, frozen ready meals accounted for 34.12% of the North American frozen food market, driven by their convenience and appeal to busy lifestyles. The segment continues to grow through product improvements, including enhanced pasta textures, richer sauces, and compatibility with modern cooking appliances such as air fryers. Frozen snacks, including products like dumplings and pizza bites, are expected to witness the fastest growth, with a projected CAGR of 6.21% from 2026 to 2031. This growth is attributed to the increasing trend of snacks being used as meal replacements. While the meat and poultry category remains a significant contributor to overall sales, seafood is emerging as a faster-growing segment due to rising consumer demand for convenient, lean protein options.

The frozen fruit and vegetable category maintains a stable position in the market, despite ongoing concerns about quality perceptions. Brands are addressing these challenges through innovations such as farm-to-package traceability using QR codes and flash-steaming techniques that help retain nutrients. Health-focused product development continues to influence market trends. For example, in May 2024, Nestlé launched Vital Pursuit, a frozen food line in the U.S. tailored for users of GLP-1 weight management therapies and other weight-conscious consumers. These products emphasize high protein content, ample fiber, essential micronutrients, and portion sizes designed to support appetite control and dietary goals.

By Category: Ready-to-Cook Gains Momentum

In 2025, ready-to-eat (RTE) meals accounted for 58.43% of the frozen food market, highlighting their strong appeal among time-constrained consumers. These products incorporate innovations such as microwave-ready trays, self-venting films, and pre-portioned seasoning packets to enhance convenience and meal quality. The inclusion of air-fryer cooking instructions addresses the growing adoption of this appliance, particularly among Gen Z. RTE meals remain a preferred choice for busy professionals and families seeking quick, hassle-free meal solutions. Additionally, improvements in nutritional profiles and ingredient transparency align these products with evolving consumer expectations, making them a versatile option for various consumer groups.

The ready-to-cook (RTC) segment is projected to grow at a 6.52% CAGR, driven by consumers who prefer a hands-on approach to meal preparation. These products provide greater flexibility in ingredients and portion sizes, enabling meal customization. Innovations such as improved batter adhesion, steam-bag vegetables, and grill-from-frozen capabilities ensure quality comparable to fresh produce. Health-conscious consumers are increasingly attracted to this segment, as active involvement in cooking allows better control over sodium, fat, and nutrient intake. RTC products have also benefited from advancements in packaging, portion control, and globally inspired flavor options, enhancing both convenience and culinary variety. This segment caters to consumers seeking a balance between convenience and the satisfaction of preparing meals tailored to their preferences.

By Distribution Channel: Retail Dominates However Foodservice Sees Rapid Growth

In 2025, retail channels represented 55.32% of the North American frozen food market, with supermarkets and hypermarkets maintaining a dominant position. These outlets benefit from broad product assortments, immediate availability, and cross-category promotional strategies. Their large store formats feature dedicated frozen sections, organized into specific aisles for ready meals, vegetables, meats, and desserts. While these formats remain prominent, consumer shopping behaviors are increasingly diversifying across multiple retail outlets. Convenience stores are gaining importance by catering to quick, on-the-go purchases, such as single-serve burritos and breakfast items, targeting urban professionals and students who prioritize speed and accessibility.

The foodservice (HoReCa) segment is expanding at a CAGR of 8.73%, driven by rising labor costs, operational challenges, and the demand for efficiency in busy kitchens. Frozen products are increasingly utilized in this sector to reduce preparation time, minimize food waste, and ensure consistent food safety standards. Beyond operational efficiency, frozen foods support menu diversification and help stabilize supply chains, making them particularly valuable for quick-service restaurants, catering services, and institutional dining. The growing consumer preference for convenient, affordable, and reliable meal options continues to fuel growth in this segment.

Geography Analysis

In 2025, the United States accounted for 84.46% of the North American frozen food market. This dominance is attributed to widespread household freezer ownership, extensive retail networks, and consistent consumer demand for high-quality frozen products. Within the U.S., the Midwest and Northeast regions report the highest per capita consumption, reflecting regional preferences and access to frozen food options. Changing consumer preferences toward nutritious frozen vegetables and portion-controlled meals are influencing product development, as manufacturers aim to cater to health-conscious consumers. Market growth is further supported by advancements in freezing technologies, improved cold chain logistics, and efforts to reduce food waste through frozen storage solutions, which are increasingly recognized as sustainable practices.

Mexico is projected to grow at a 4.86% CAGR through 2031, driven by the expansion of supermarket chains, rising e-commerce penetration, and the increasing prevalence of urban dual-income households adopting frozen ready meals and plant-based snacks. According to the USDA, Mexico’s food processing industry contributed 4% of the national GDP in 2024, highlighting strong domestic frozen food manufacturing capabilities [3]Source: United States Department of Agriculture, "Food Processing Ingredients Annual", usdamexico.org. The growth of the frozen food market in Mexico is further bolstered by investments in cold storage facilities, modernized retail infrastructure, and the adoption of Western eating habits among urban consumers. These factors are enabling greater accessibility and convenience for consumers, particularly in urban areas where time-saving meal options are in high demand.

Canada holds a significant share of the regional market, with consumer demand centered on organic, clean-label products and sustainability initiatives, such as recyclable packaging and locally sourced ingredients. The market benefits from stringent food safety regulations, advanced cold chain systems, and a growing preference for premium frozen options, which cater to consumers seeking high-quality and environmentally friendly products. Other North American regions contribute to the market through niche and ethnic product offerings, catering to diverse populations and local culinary preferences. These regions play a vital role in addressing the unique demands of multicultural communities, further enriching the overall market landscape.

Regulatory Landscape

Frozen food manufacturers and distributors in North America work under food safety and labeling oversight led by the US Food and Drug Administration (FDA), the Canadian Food Inspection Agency (CFIA) and Health Canada, and Mexico’s competent authorities. Compliance requirements span preventive controls, allergen management, sanitation, and bilingual labeling in Canada. In the United States, the FDA Human Foods Program published its 2026 priority deliverables agenda centered on microbiological food safety, nutrition, and food chemical safety, which keeps attention on formulations and labeling clarity for frozen ready meals, snacks, and processed proteins.

Supply chain transparency also remains a key compliance theme, but the enforcement timeline shifted in 2026. The FY2026 Agriculture, Rural Development, Food and Drug Administration, and Related Agencies Appropriations Act restricts FDA from enforcing the FSMA Food Traceability Rule (21 CFR Part 1, Subpart S) until July 20, 2028, while FDA continues stakeholder engagement and guidance work ahead of eventual compliance. In Canada, Health Canada’s 2026-2028 Forward Regulatory Plan and the registration of SOR/2026-96 (Regulations Amending Certain Regulations Made Under the Food and Drugs Act) point to continued modernization of the regulatory framework affecting ingredient use, labeling, and compliance processes for packaged frozen foods sold nationally.

Competitive Landscape

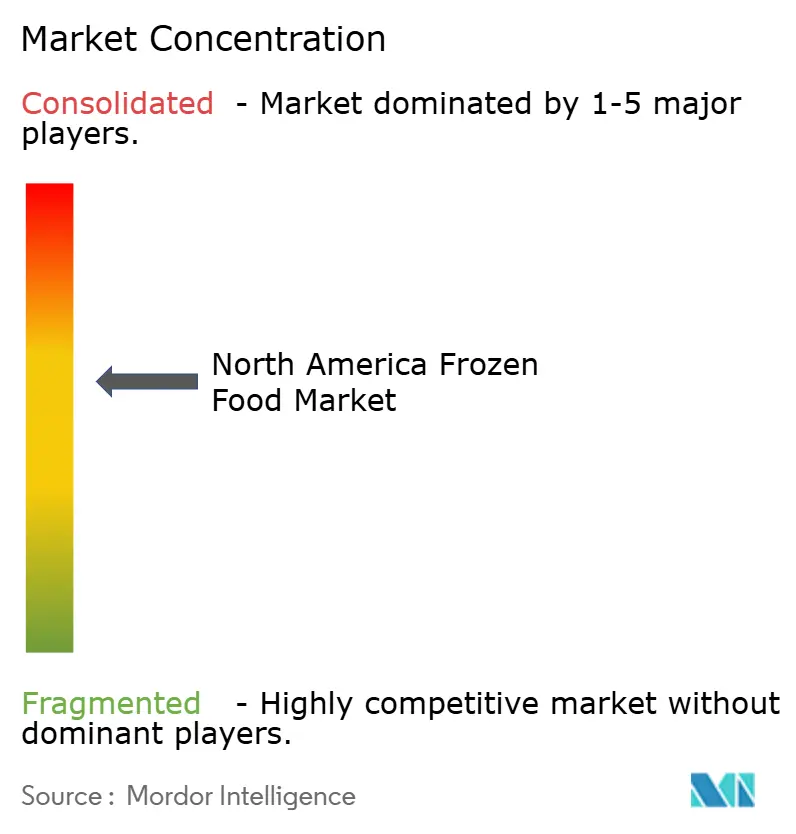

The North American frozen food market exhibits moderate concentration, with major players such as Conagra, Tyson, Nestlé, and McCain commanding a significant share of revenue. However, these incumbents face ongoing challenges from the growth of plant-based competitors and the expansion of private-label offerings. Competitive strategies in the market diverge between innovation and efficiency. Multinational companies focus on research and development initiatives, such as isochoric freezing and clean-label reformulations, as well as mergers and acquisitions to address portfolio gaps. In contrast, regional processors prioritize cost competitiveness through vertical integration and proximity to agricultural inputs.

Growth opportunities are concentrated in three key areas: ultra-premium frozen meals targeting affluent consumers willing to spend USD 12-15 per entrée for chef-designed recipes; ethnic cuisines co-branded with culinary experts from diaspora communities; and hybrid ready-to-cook kits that combine the convenience of frozen foods with the customization of meal kits. Technological advancements are centered on improving freezing precision and packaging innovation. Brands that minimize drip loss and extend shelf life gain favor with retailers by reducing shrinkage and increasing product turnover.

Compliance with FDA food safety standards and CFIA bilingual labeling requirements remains essential. However, the lack of harmonized definitions for ultra-processed foods creates strategic uncertainty. Some brands adopt "clean label" positioning, while others avoid engaging in this debate. The next area of competitive differentiation lies in vertical integration within cold-chain logistics. Companies that manage warehousing and last-mile delivery can provide retailers with guaranteed fill rates and shorter lead times, a critical advantage during periods of seasonal demand spikes and supply chain disruptions.

North America Frozen Food Industry Leaders

-

Conagra Brands Inc.

-

Nestlé S.A

-

McCain Foods Limited

-

Kraft Heinz Company

-

Tyson Foods, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Investment into North American frozen supply and manufacturing capacity points to opportunities for players that can secure inputs, reduce bottlenecks, and serve both retail and foodservice with consistent fill rates. In March 2026, Conagra Brands announced a multi-year USD 220 million expansion of its Fayetteville, Arkansas manufacturing operations to increase chicken production capacity for frozen brands such as Banquet, Healthy Choice, and Hungry-Man, highlighting the value of in-house protein capacity for high-velocity frozen meals. Upstream, Agristo broke ground in July 2026 on a 630,000-square-foot, USD 1 billion potato production facility in Grand Forks, North Dakota, adding long-cycle capacity that supports demand for frozen potato products and strengthens domestic processing near agricultural hubs.

Cold chain digitization and freezer-aisle execution also create traction for retailers, 3PLs, and technology providers seeking to reduce shrink, improve availability, and shorten the cycle from product development to shelf. In March 2026, Kroger began testing an autonomous, AI-driven inventory system for live freezer warehouse environments to address visibility gaps that can limit on-shelf availability and weaken promotion performance for frozen categories. On the product side, health and convenience positioning already visible in-market provides a clearer route to differentiated assortments, including GLP-1 oriented labeling moves such as Conagra’s Healthy Choice labeling initiative announced in January 2025 and plant-based global flavors such as Unlimeat’s July 2024 US retail rollout, spanning the United States, Canada, and Mexico.

Recent Industry Developments

- July 2026: Conagra Brands reported its fiscal year 2026 fourth-quarter results, highlighting a year-over-year net sales increase in its Refrigerated and Frozen segment. The update underscored the scale of the frozen portfolio within a major branded supplier and supported continued investment focus across frozen meals and adjacent categories.

- November 2025: McCain Foods entered into an agreement to acquire Penobscot McCrum LLC, including its potato processing facility in Washburn, Maine. The deal expands McCain’s North American processing footprint and strengthens supply availability for frozen potato products.

- October 2024: Delimex expanded beyond taquitos with the launch of Crispy Quesadillas in Char-Grilled Chicken and Chipotle Chicken varieties. The products leverage Kraft Heinz’s 360CRISP technology to deliver a crisper microwave-ready texture, supporting premium convenience positioning in frozen handhelds.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the North America frozen food market covers packaged and bulk food items that are commercially frozen and kept at or below -18 C, and then sold through retail or foodservice channels in the United States, Canada, and Mexico.

Scope exclusions: Chilled prepared foods that are not stored in a freezer, home-frozen items, and frozen novelties sold from vending-style cabinets are not counted.

Segmentation Overview

-

By Product Type

- Frozen Fruits and Vegetables

- Frozen Meat and Poultry

- Frozen Seafood

- Frozen Ready Meals

- Frozen Bakery and Desserts

- Frozen Snacks

- Others

-

By Category

- Ready-To-Eat

- Ready-To-Cook

-

By Distribution Channel

- Foodservice (HoReCa)

-

Retail

- Supermarkets and Hypermarkets

- Convenience Stores

- Online Stores

- Other Retail Formats

-

By Geography

- United States

- Canada

- Mexico

- Rest of North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the cold chain food landscape and to anchor the model to repeatable public data points. We referred to sources such as USDA (including ERS and AMS series), the US Census Bureau, Statistics Canada, and Government of Canada trade statistics to understand category movement and cross-border flows that affect supply availability.

To make sure the story reflects real market behavior, we also reviewed inputs such as retailer and brand owner public filings, investor presentations, and reputable press coverage of freezer aisle trends, promotions, and product launches. In parallel, paid subscriptions for company financials and intelligence, plus shipment-level import and export data, were used selectively to check scale for major routes and to avoid missing structural changes. This desk source list is illustrative only, and many other public references were also used for collection, validation, and clarification.

Primary Interviews and Surveys

Primary conversations helped us validate what is actually counted as frozen food in the commercial chain, and how category mix has been shifting across the United States, Canada, and Mexico. We spoke with manufacturers, ingredient and packaging partners, distributors, and channel-side participants to pressure-test assumptions on pricing, mix, and demand drivers, and then we re-checked open questions until ranges narrowed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 13% | |

| Mid tier: 43% | Functional/Unit leaders: 36% | |

| Smaller Players: 18% | Managers: 51% |

Market-Sizing & Forecasting

The core sizing starts with a top-down build where household food spend, frozen-category penetration, and retail and foodservice channel shares are translated into a North America value pool for frozen items stored at freezer temperatures. Once the total is built, it is corroborated with selective bottom-up approximations, such as sampled category volumes multiplied by typical price bands, plus supplier and distributor checks that help us adjust totals where desk data is thin.

In practice, the model responds to a few market fingerprints that are easy to track year to year. These include freezer aisle share trends versus fresh and chilled alternatives, price per pound or per pack movement by major frozen categories, private label versus branded mix, and the balance between at-home consumption and foodservice demand. Trade flows for frozen meat, seafood, and vegetables are also monitored because they can change supply and pricing quickly, and those changes show up in interview feedback.

For forecasting, scenario analysis is used with a simple set of drivers, and the driver paths are confirmed through expert inputs before being locked. When there are gaps in category-level detail, the missing pieces are backfilled using conservative mix splits and then revisited during validation so the final totals stay consistent with observable channel and trade signals.

Data Validation & Update Cycle

Outputs are checked through triangulation across independent signals, and then unusual jumps are investigated before numbers are signed off. We compare the final series against category consumption indicators, trade and supply cues, and pricing direction, and then we re-contact sources when a variance looks too large to be explained by normal seasonality or mix.

The work is reviewed in multiple steps so key assumptions, conversions, and scope boundaries are consistent across countries and channels. Reports are refreshed annually, and interim updates are made when material events occur that can move pricing, availability, or demand. Before delivery, a fresh analyst pass is completed so clients receive the most recent and internally consistent view.

Mordor Intelligence's North America Frozen Food Market Sizing Compared With Other Published Estimates

It is common to see different published numbers for the North America frozen food market, even when the topic name looks the same. The gaps usually come from differences in what gets counted as frozen food, which geographies are included, and how pricing and channel mix are handled in the base year.

Trade-flow direction for frozen meat, seafood, and vegetables, together with observed retail pricing movement for freezer categories, are practical checks that keep Mordor Intelligence aligned to a freezer-temperature scope (at or below -18 C) and away from chilled convenience foods that can inflate totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 101.86 B (2025) | |

| Global Consultancy A | USD 103.45 B (2024) | Uses a different base year and can apply broader category splits that may treat ready-to-eat and ready-to-cook groupings as a single pool, which can shift mix and pricing assumptions versus a strict freezer-only definition. |

| Regional Consultancy B | USD 179.97 B (2023) | The much larger value suggests adjacent chilled or wider packaged food categories may be included, and the estimate is sensitive to how currency timing and channel coverage are handled across retail and foodservice. |

The table indicates that year alignment and scope discipline explain most of the spread, before any forecasting differences are even considered. When freezer-temperature boundaries, channel splits, and practical price checks are applied consistently, the resulting market value is easier to trace back to clear drivers and to replicate during updates.

Key Questions Answered in the Report

What is the current value of the North America frozen food market?

The North America frozen food market size equals USD 105.74 billion in 2026 and is projected to reach USD 127.39 billion by 2031.

Which product segment is growing fastest?

Frozen Snacks are set to advance at a 6.21% CAGR through 2031 as portion-controlled, on-the-go formats resonate with Gen Z and GLP-1 users.

Why is foodservice demand for frozen foods accelerating?

Labor shortages and 15-20% wage inflation make pre-portioned frozen inputs economically attractive, pushing foodservice growth to an 8.73% CAGR.

Which geography shows the fastest growth outlook?

Mexico is forecast to post a 4.86% CAGR through 2031, spurred by urbanization and supermarket freezer-aisle expansion.

Page last updated on: