Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

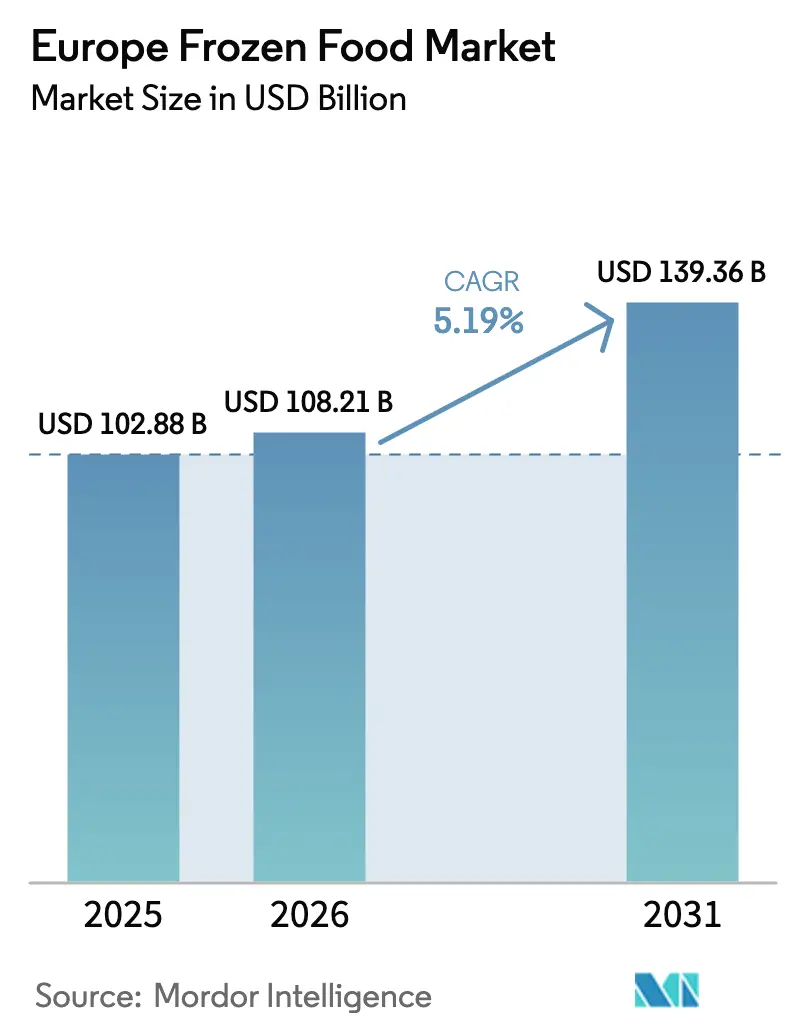

| Base Year Market Size (2025) | USD 102.88 Billion |

| Market Size (2026) | USD 108.21 Billion |

| Market Size (2031) | USD 139.36 Billion |

| Growth Rate (2026 - 2031) | 5.19% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Frozen Food Market Analysis by Mordor Intelligence

The Europe frozen food market size is expected to grow from USD 102.88 billion in 2025 to USD 108.21 billion in 2026 and is forecast to reach USD 139.36 billion by 2031 at 5.19% CAGR over 2026-2031. Rising demand for convenient meal solutions and advancements in individual quick-freezing (IQF) technology are driving market growth. Retailers are increasingly focusing on private-label products, while the launch of plant-based lines, premium frozen bakery goods, and health-focused offerings is expanding consumer interest. Innovations in cold-chain logistics are reducing energy consumption and cutting food waste, further accelerating market expansion. Ultrafast grocery delivery services are prioritizing frozen items as key contributors to profitability. In 2025, the European Food Safety Authority (EFSA) introduced guidelines that simplify the process of launching new products, adding momentum to the sector. Geographically, Germany leads as the largest market, France shows the fastest growth, and the Nordic countries are shaping category trends with their strong emphasis on sustainability.

Key Report Takeaways

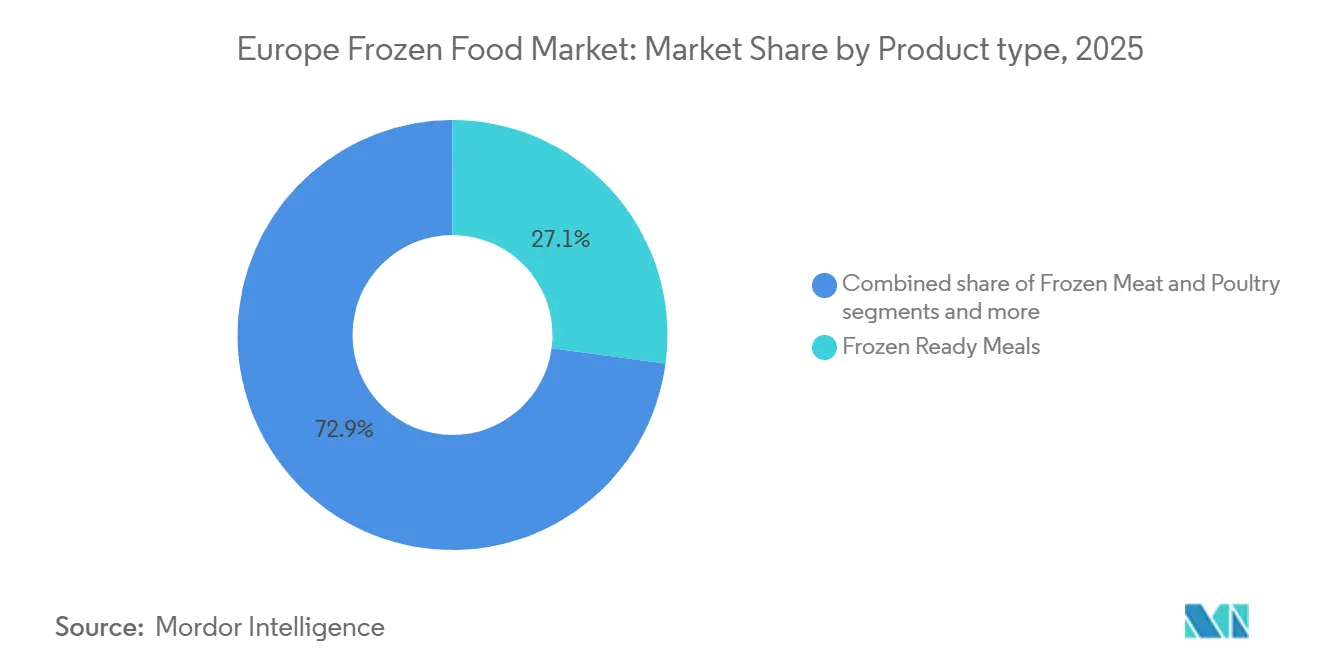

- By product type, frozen ready meals held 27.12% of the Frozen food market share in 2025, while frozen snacks and appetizers are forecast to expand at an 8.16% CAGR through 2031.

- By product category, ready-to-eat formats captured 61.38% of 2025 volume, whereas ready-to-cook is advancing at a 7.42% CAGR through 2031.

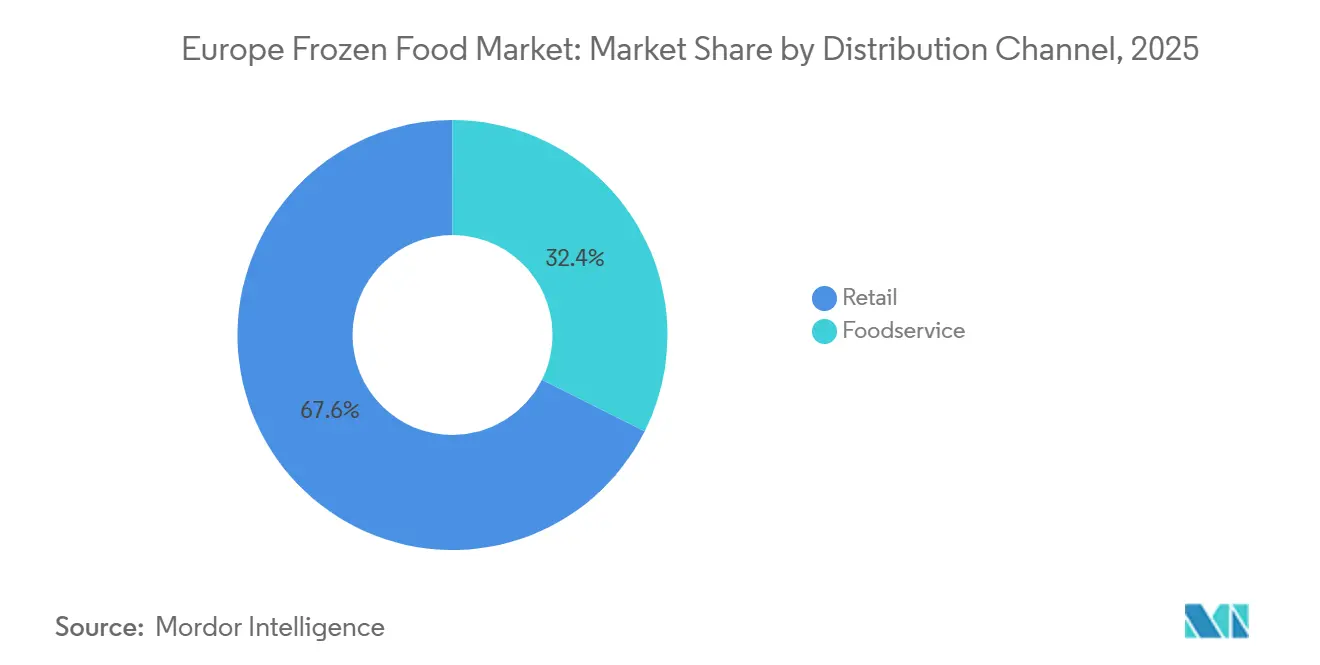

- By distribution channel, retail accounted for 67.62% of 2025 revenue, yet foodservice is projected to rise at a 9.31% CAGR through 2031.

- By geography, Germany commanded 23.53% of 2025 sales, while France is projected to post the fastest 5.61% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Frozen Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of dual-income households supporting quick meal consumption | +1.2% | Western Europe (Germany, UK, France, Netherlands), spreading to Spain and Italy | Medium term (2-4 years) |

| Increasing demand for healthier, organic, and plant-based frozen foods | +0.9% | UK, Germany, Netherlands, Denmark; emerging in France and Belgium | Long term (≥ 4 years) |

| Technological advancements improving freezing quality and shelf life | +0.7% | Regional, with early adoption in Germany, Netherlands, UK | Long term (≥ 4 years) |

| Rising foodservice and hospitality sector usage of frozen ingredients | +1.4% | Western Europe (Germany, France, UK, Spain), expanding to Eastern Europe | Short term (≤ 2 years) |

| Longer shelf life reducing food waste and increasing consumer acceptance | +0.8% | EU-wide, particularly Germany, France, Netherlands | Medium term (2-4 years) |

| Premiumization and innovation in frozen ready meals and ethnic cuisines | +1.0% | UK, Germany, France, with spillover to Belgium and Netherlands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth of dual-income households supporting quick meal consumption

The growth of dual-income households is a key driver supporting the rising demand for frozen foods in Europe. With both adults in many households engaged in full-time employment, consumers are increasingly seeking convenient and time-saving meal solutions. According to the Office for National Statistics, in the United Kingdom, 59.2% of households with at least one person aged 16–64 had all adults in employment during July–September 2025, highlighting the prevalence of fully employed households[1]Source: Office for National Statistics, “Working and workless households in the UK: July to September 2025”, ons.gov.uk. Busy lifestyles and limited time for cooking are encouraging the adoption of ready-to-eat and ready-to-cook frozen meals, snacks, and desserts. Retailers and manufacturers are responding by expanding their frozen product portfolios with diverse, high-quality, and nutritious options. This trend is further supported by urbanization, changing family dynamics, and the desire for quick yet wholesome meal solutions.

Increasing demand for healthier, organic, and plant-based frozen foods

The increasing demand for healthier, organic, and plant-based frozen foods is a major driver of the Europe frozen food market. Consumers are becoming more health-conscious and seeking products that align with nutritious and sustainable lifestyles. Around 26% of EU consumers report eating organic products as part of their healthy diet considerations, according to the European Food Safety Authority survey in 2024, highlighting the growing preference for certified organic options[2]Source: European Food Safety Authority, “Food safety in the EU”, efsa.europa.eu. This trend is encouraging manufacturers to expand frozen product portfolios to include plant-based meals, organic vegetables, and minimally processed options. Retailers are also promoting these products through dedicated sections and marketing campaigns that emphasize health, sustainability, and clean-label benefits. The shift toward healthier and environmentally conscious consumption is influencing product innovation, packaging, and ingredient sourcing within the frozen food segment.

Technological advancements improving freezing quality and shelf life

Technological advancements in freezing and storage methods are significantly driving the growth of the Europe frozen food market. Modern freezing techniques, such as blast freezing, IQF (individually quick frozen), and cryogenic methods, help preserve the taste, texture, and nutritional value of products, ensuring higher quality for consumers. Improved cold chain infrastructure and temperature-controlled logistics have enhanced product shelf life, reduced food waste, and enabled wider geographic distribution. Automation and smart freezing technologies also allow manufacturers to scale production efficiently while maintaining consistency and safety standards. These innovations support the introduction of premium and delicate frozen items, including ready-to-cook meals, seafood, and plant-based products, without compromising quality. Retailers benefit from longer shelf life and reduced spoilage, which also improves operational efficiency.

Rising foodservice and hospitality sector usage of frozen ingredients

The rising usage of frozen ingredients in the foodservice and hospitality sector is a significant driver of the Europe frozen food market. Increasing tourism and travel across Europe have boosted demand from hotels, restaurants, and catering services for convenient, high-quality, and easily stored frozen products. According to Eurostat, the European Union recorded over 3.0 billion nights spent in tourist accommodation in 2024, marking the strongest tourism performance on record, which underscores the growing scale and activity of the hospitality sector[3]Source: Eurostat, “EU sees record number of tourism nights in 2024”, ec.europa.eu. Frozen ingredients help foodservice operators reduce preparation time, minimize food waste, and maintain consistent quality across high-volume operations. The sector is increasingly relying on ready-to-use frozen vegetables, seafood, meats, and ready-to-cook meals to meet the demands of busy kitchens and varied menus. Innovation in frozen products, including premium and plant-based options, further supports their adoption in foodservice.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High energy consumption and operational costs for freezing and storage | -0.9% | EU-wide, acute in Germany, UK, France due to industrial electricity pricing | Short term (≤ 2 years) |

| Negative consumer perception regarding nutritional value of frozen foods | -0.4% | Southern Europe (Spain, Italy), diminishing in Northern Europe | Medium term (2-4 years) |

| Cold chain and distribution challenges in certain regions | -0.5% | Southern and Eastern Europe (Spain, Italy, Russia), rural areas | Medium term (2-4 years) |

| Fluctuating raw material and logistics costs impacting margins | -0.7% | EU-wide, particularly affecting protein and vegetable processors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High energy consumption and operational costs for freezing and storage

High energy consumption and operational costs remain a significant restraint for the Europe frozen food market. Maintaining low temperatures throughout production, storage, and distribution requires substantial electricity usage, which increases operational expenses for manufacturers and retailers. Rising energy prices and the need for advanced refrigeration systems further add to the cost burden, affecting profitability, particularly for small and mid-sized players. Cold chain logistics also demand continuous monitoring and specialized infrastructure, which can limit expansion into new regions or smaller markets. These costs may be partially passed on to consumers, potentially affecting price sensitivity and demand. Additionally, investments in energy-efficient technologies and sustainable refrigeration methods require significant capital outlay.

Negative consumer perception regarding nutritional value of frozen foods

Negative consumer perception regarding the nutritional value of frozen foods continues to act as a restraint on the Europe frozen food market. Many consumers associate frozen products with lower freshness, artificial additives, or reduced nutrient content compared with fresh alternatives, which can limit adoption among health-conscious buyers. Misconceptions about preservatives and processed ingredients further contribute to hesitation in purchasing frozen meals, vegetables, and ready-to-eat products. Despite technological advancements in freezing that preserve taste and nutrients, consumer awareness of these benefits remains limited in some regions. Marketing efforts and educational campaigns by manufacturers are helping to address these concerns, but widespread perception challenges persist. This negative image can affect brand preference and slow the growth of certain product categories, particularly premium or health-oriented frozen foods.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ready Meals Lead, Snacks Accelerate

Frozen ready meals accounted for the largest share of the Europe frozen food market in 2025, capturing 27.12% of total market value. The segment’s dominance is largely driven by growing consumer demand for convenient and time-saving meal solutions, particularly among busy urban households and dual-income families. Ready meals offer a wide variety of options, including traditional cuisine, international flavors, and health-focused alternatives, which appeal to a broad range of consumer preferences. Supermarkets and grocery retailers play a key role in promoting these products by providing dedicated frozen meal sections and attractive packaging. Additionally, increasing awareness about portion-controlled and nutritious ready meals has further strengthened their market position.

Frozen snacks and appetizers are projected to be the fastest-growing segment in the Europe frozen food market, expanding at a CAGR of 8.16% through 2031. Growth in this segment is driven by rising consumer interest in bite-sized, on-the-go, and shareable food options that complement busy lifestyles. The increasing popularity of casual dining, social gatherings, and party culture is further fueling demand for frozen snack varieties. Innovation in flavors, healthier formulations, and premium ingredients has attracted a wider consumer base. Retailers are also expanding shelf space and promoting frozen snacks through multi-pack offerings and impulse-buy displays.

By Product Category: Ready-to-Eat Dominates, Ready-to-Cook Gains

Ready-to-eat formats accounted for the largest share of the Europe frozen food market in 2025, capturing 61.38% of total volume. The strong dominance of this segment is primarily driven by increasing consumer demand for convenience and minimal meal preparation time. Busy lifestyles, rising urbanization, and the growing number of working professionals have encouraged greater reliance on fully prepared frozen meals. Ready-to-eat products also benefit from wide availability across supermarkets, hypermarkets, and online retail channels, making them easily accessible to consumers. Continuous innovation in product quality, taste, and nutritional value has helped improve consumer perception of frozen ready meals.

Ready-to-cook formats are projected to be the fastest-growing segment in the Europe frozen food market, advancing at a CAGR of 7.42% through 2031. Growth in this segment is supported by increasing consumer interest in home cooking combined with the convenience of pre-prepared ingredients. Ready-to-cook frozen products allow consumers to customize meals while reducing preparation time and food waste. The segment is also benefiting from rising demand for healthier and fresher meal options that offer greater control over cooking methods and ingredients. Manufacturers are expanding product offerings to include diverse cuisines, premium ingredients, and clean-label formulations to attract health-conscious consumers.

By Distribution Channel: Retail Anchors, Foodservice Surges

Retail distribution accounted for the largest share of the Europe frozen food market in 2025, contributing 67.62% of total revenue. The dominance of the retail segment is largely driven by strong consumer preference for purchasing frozen products through supermarkets, hypermarkets, convenience stores, and online grocery platforms. Wide product availability, promotional pricing strategies, and private label expansion have further strengthened retail sales performance. Retail outlets provide consumers with access to a broad assortment of frozen ready meals, vegetables, seafood, snacks, and desserts under one roof. The growth of e-commerce grocery platforms has also enhanced convenience, allowing consumers to order frozen products for home delivery.

Foodservice is projected to be the fastest-growing distribution channel in the Europe frozen food market, expanding at a CAGR of 9.31% through 2031. The segment’s growth is supported by the recovery and expansion of restaurants, quick-service outlets, catering services, and hospitality establishments. Frozen food products are widely used in foodservice operations due to their extended shelf life, consistent quality, and ease of storage. The ability to reduce preparation time and minimize food waste makes frozen ingredients particularly attractive to commercial kitchens. Rising tourism, urban dining culture, and increasing demand for quick-service meals are further fueling demand within this channel.

Geography Analysis

Germany accounted for the largest share of the Europe frozen food market in 2025, contributing 23.53% of total sales. The country’s strong position is supported by a well-developed retail infrastructure and high consumer acceptance of frozen food products. German consumers value convenience, quality, and food safety, all of which align closely with the benefits offered by frozen formats. The widespread presence of discount retailers and supermarket chains has enhanced product accessibility and competitive pricing. In addition, strong cold chain logistics and advanced storage facilities ensure consistent product availability across urban and rural areas. Continuous product innovation and private-label expansion further reinforce Germany’s leading role in the regional frozen food market.

France is projected to be the fastest-growing country in the Europe frozen food market, registering a CAGR of 5.61% over 2026–2031. Growth in France is driven by increasing demand for convenient meal solutions among busy households and working professionals. The rising popularity of frozen ready meals, vegetables, and bakery products is supporting steady market expansion. Retailers are expanding frozen product assortments and introducing premium and health-focused options to attract a broader consumer base. Improvements in cold storage infrastructure and online grocery penetration are also contributing to growth. As consumer lifestyles continue to evolve toward convenience-oriented consumption, France is expected to maintain strong growth momentum during the forecast period.

Other European countries, including the United Kingdom, Spain, and Italy, also represent significant markets within the region. The United Kingdom benefits from high frozen food penetration and strong demand for ready meals and frozen snacks. Spain is witnessing steady growth supported by expanding retail chains and increasing adoption of frozen seafood and convenience foods. Italy’s market is driven by demand for frozen pizza, vegetables, and bakery products, alongside growing modern retail formats. In these countries, changing lifestyles, urbanization, and rising dual-income households are encouraging higher consumption of frozen products. Collectively, these markets contribute substantially to overall regional revenue and provide stable growth opportunities across multiple frozen food categories.

Competitive Landscape

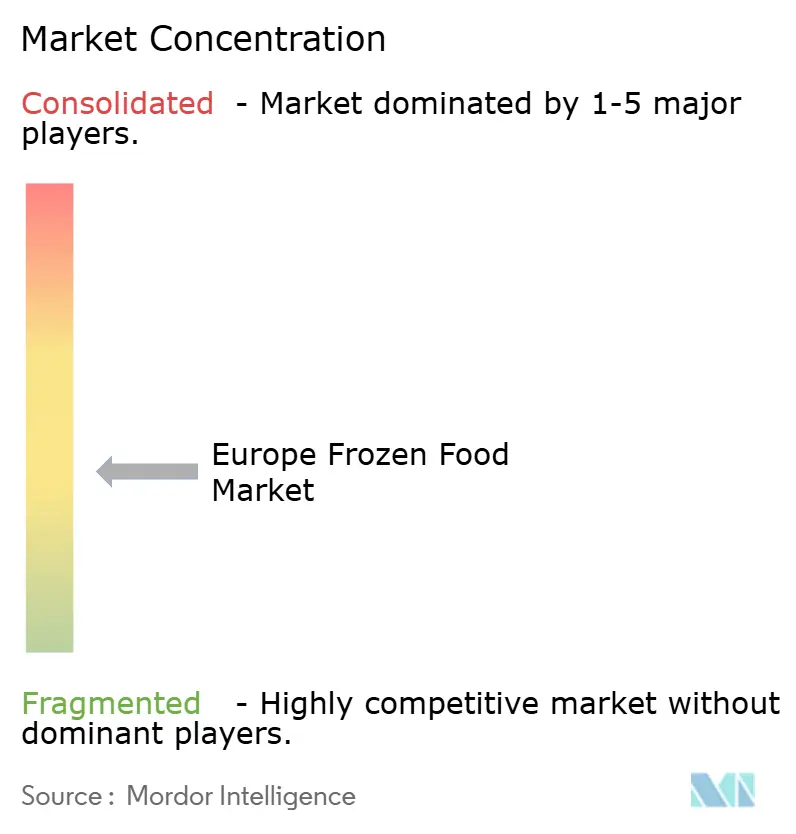

The European frozen food market exhibits low concentration, indicating significant opportunities for new entrants to compete alongside established players. The competitive landscape is shaped by key companies such as Nomad Foods Ltd., Nestlé S.A., Dr. Oetker KG, Unilever PLC, and Conagra Brands Inc., which leverage extensive product portfolios, disciplined mergers and acquisitions, and strong brand recognition to maintain their market presence. These companies continue to invest in product innovation and portfolio diversification to address changing consumer preferences for convenience and health-oriented frozen foods. Sustainability initiatives, including responsible sourcing and eco-friendly packaging, are also becoming central to competitive strategies.

Competition in the market is further intensified by the growing presence of regional and private-label brands that offer competitively priced alternatives. Retailers are increasingly expanding their own frozen food offerings, creating additional pressure on branded manufacturers to differentiate through quality, innovation, and premium positioning. Smaller and mid-sized companies are gaining traction by focusing on niche categories such as plant-based meals, organic frozen products, and ethnic cuisines. Technological advancements in freezing and packaging are also enabling newer entrants to improve product quality and shelf life. As consumers seek greater variety and value, companies are investing in faster product development cycles and localized offerings.

Strategic collaborations and investments in supply chain optimization are becoming key priorities among market participants seeking long-term growth. Companies are strengthening cold chain logistics and digital distribution capabilities to enhance product availability and reduce operational inefficiencies. Expansion into e-commerce and direct-to-consumer channels is also reshaping competition, allowing brands to reach wider consumer bases. Furthermore, increasing emphasis on clean-label ingredients and transparent sourcing is influencing product development strategies across the industry. Market players are also exploring acquisitions and partnerships to expand geographic presence and strengthen category expertise.

Europe Frozen Food Industry Leaders

Nestlé S.A.

Dr. Oetker KG

Unilever PLC

Conagra Brands Inc.

Nomad Foods Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: BOSH! expanded its frozen portfolio by launching a new range of plant-based frozen ready meals, pizzas, and seasonings in UK retail, reflecting the growing demand for convenient vegan and plant-based meal solutions. The expansion focuses on delivering flavor-driven, protein-rich meals inspired by the brand’s established recipes, aimed at increasing accessibility and attracting a wider consumer base seeking healthier and sustainable frozen food options.

- November 2025: Seabrook entered the frozen category with the launch of frozen crinkle-cut French fries and related potato snack products, extending its established flavour portfolio beyond traditional crisps. The move demonstrates brand diversification into adjacent frozen food segments to capture new consumption occasions and leverage existing brand recognition.

- October 2025: Booker introduced a new frozen desserts range targeting the foodservice, aimed at expanding product variety for hospitality operators and convenience retailers. The development focuses on offering ready-to-serve dessert options that help operators improve menu flexibility while reducing preparation time and operational complexity.

- March 2025: UK supermarkets now stock Yo!'s new line of Japanese-inspired frozen ready meals. Shoppers can find offerings like Chicken Teriyaki, Korean Style BBQ Beef, and the classic Chicken Katsu, all prominently featured at Tesco outlets.

Europe Frozen Food Market Report Scope

Frozen food products refer to packaged food that is subjected to rapid freezing and is kept frozen until used. The Europe frozen food market is segmented by product category, product type, distribution channel, and geography. By product category, the market is bifurcated into ready-to-eat, and ready-to-cook. By product type, the market is segmented into frozen fruits and vegetables, frozen meat and fish, frozen-cooked ready meals, frozen desserts, frozen snacks, and other product types. Based on distribution channels, the market is fragmented into foodservice and retail. By geography, the market is segmented into Spain, Italy, the United Kingdom, Germany, France, Russia, and the Rest of Europe. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million) and volume (Tons).

By Product Type

| Frozen Fruits & Vegetables |

| Frozen Meat & Poultry |

| Frozen Fish & Seafood |

| Frozen Ready Meals |

| Frozen Bakery & Confectionery |

| Frozen Desserts & Ice Cream |

| Frozen Snacks & Appetizers |

| Other Product Types |

By Product Category

| Ready-to-Eat |

| Ready-to-Cook |

By Distribution Channel

| Foodservice (HoReCa) | |

| Retail | Supermarkets & Hypermarkets |

| Convenience Stores | |

| Online Stores | |

| Other Retail Formats |

By Geography

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| Denmark |

| Russia |

| Netherlands |

| Belgium |

| Rest of Europe |

| By Product Type | Frozen Fruits & Vegetables | |

| Frozen Meat & Poultry | ||

| Frozen Fish & Seafood | ||

| Frozen Ready Meals | ||

| Frozen Bakery & Confectionery | ||

| Frozen Desserts & Ice Cream | ||

| Frozen Snacks & Appetizers | ||

| Other Product Types | ||

| By Product Category | Ready-to-Eat | |

| Ready-to-Cook | ||

| By Distribution Channel | Foodservice (HoReCa) | |

| Retail | Supermarkets & Hypermarkets | |

| Convenience Stores | ||

| Online Stores | ||

| Other Retail Formats | ||

| By Geography | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Denmark | ||

| Russia | ||

| Netherlands | ||

| Belgium | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the projected value of frozen food sales in Europe by 2031?

Sales are forecast to reach USD 139.36 billion by 2031, reflecting a 5.19% CAGR from 2026 to 2031.

Which product type is expanding the fastest?

Frozen snacks and appetizers are growing at an 8.16% CAGR, outpacing all other product types through 2031.

Why is France expected to grow quicker than Germany?

France is on a 5.61% CAGR trajectory because retailers are adding freezer space and consumers are adopting premium frozen options later than their German counterparts.

How are energy costs affecting processors?

Elevated electricity prices and the EU F-gas phase-down raise short-term costs, but large players are investing in natural-refrigerant systems that cut lifetime operating expenses.

Which consumer trend most benefits premium frozen ready meals?

Growth in dual-income households with limited cooking time drives demand for chef-branded, organic, and high-quality ready meals that deliver convenience without compromising perceived quality.

Page last updated on: