Food Ultrasound Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

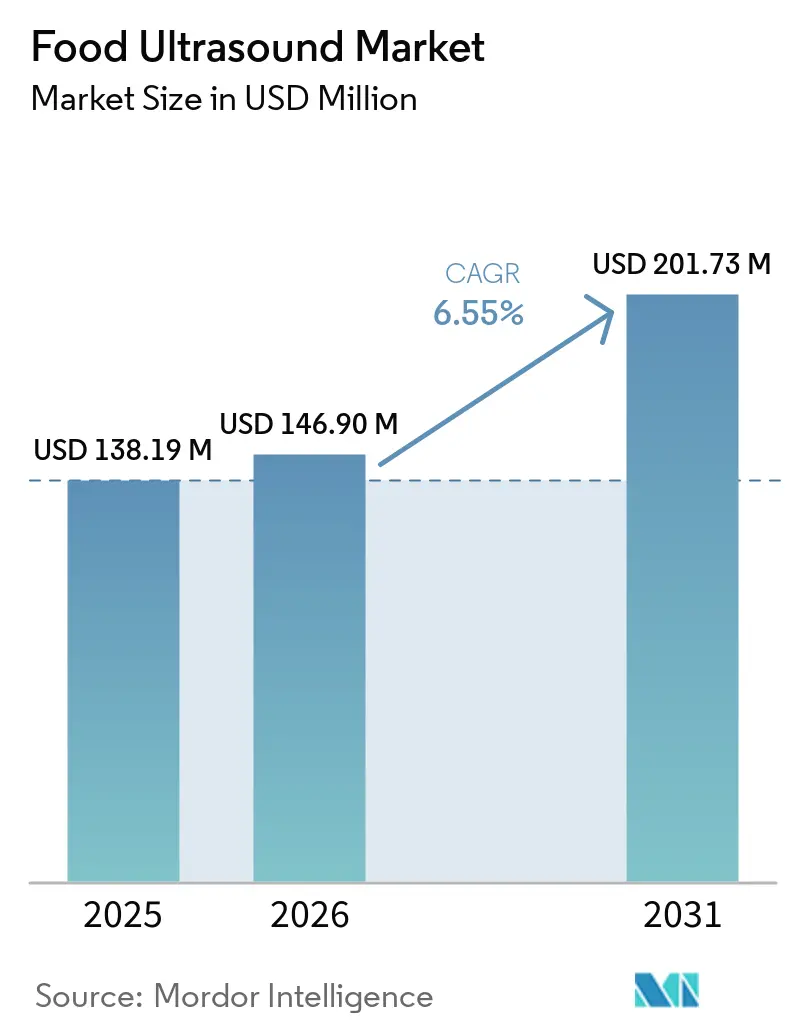

| Market Size (2026) | USD 146.90 Million |

| Market Size (2031) | USD 201.73 Million |

| Growth Rate (2026 - 2031) | 6.55% CAGR |

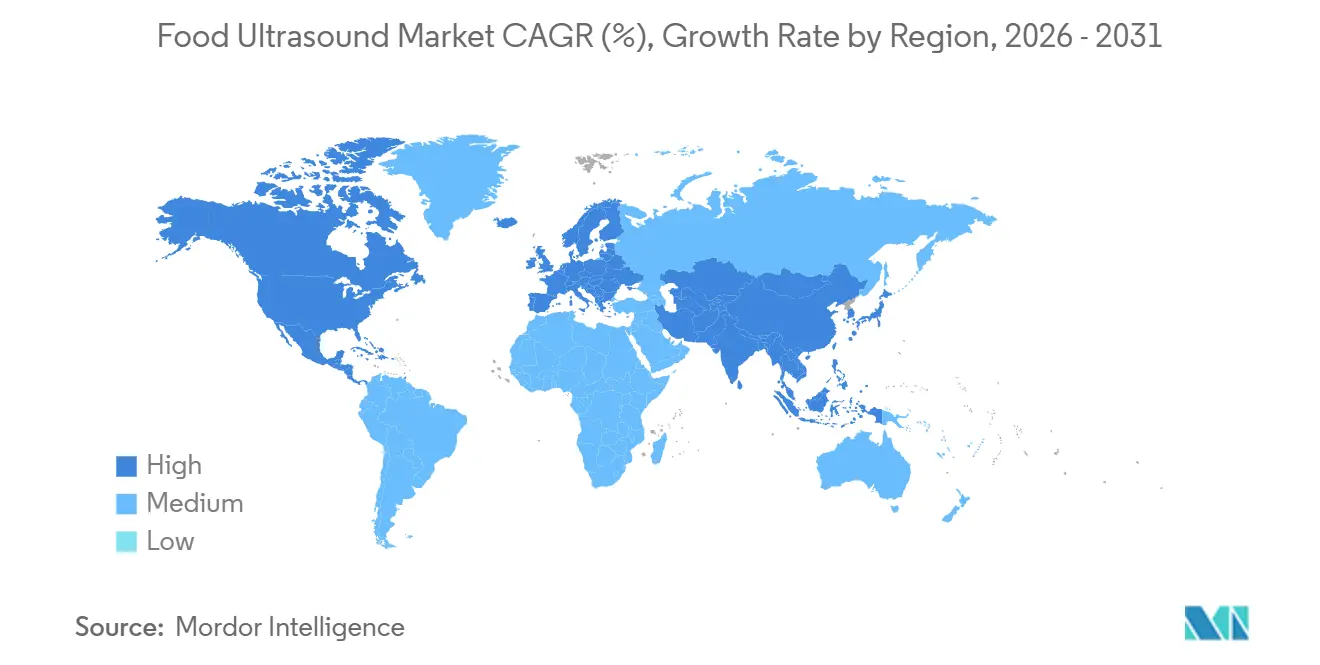

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

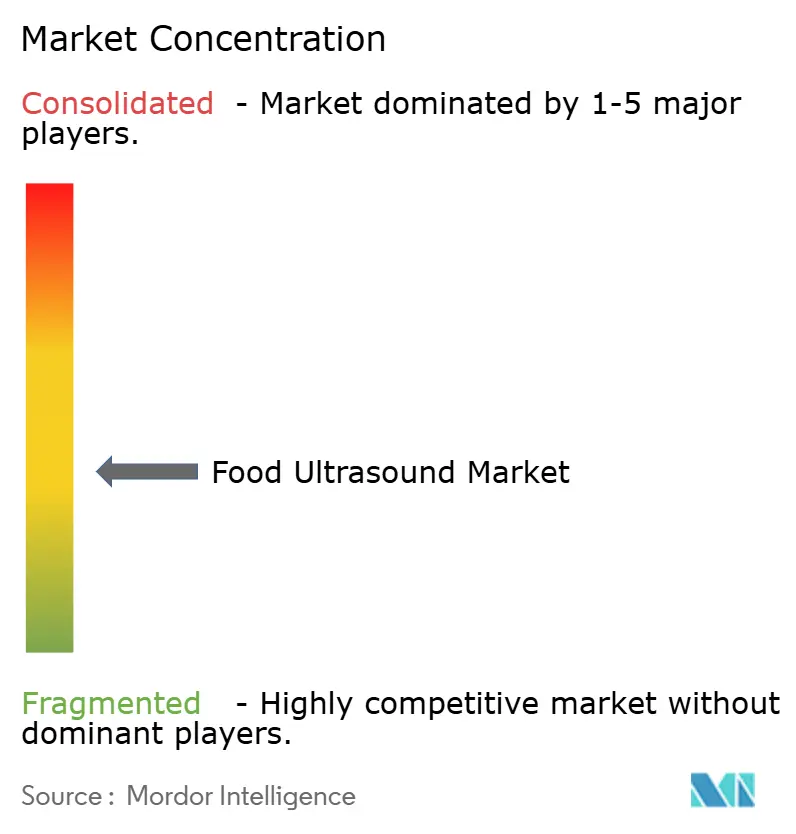

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Food Ultrasound Market Analysis by Mordor Intelligence

The food ultrasound market was valued at USD 138.19 million in 2025 and is projected to reach USD 201.73 million by 2031, growing at a CAGR of 6.55% during 2026-2031. In 2026, the market revenue is expected to reach USD 146.90 million, driven by the increasing adoption of processing methods that preserve nutritional integrity without relying on thermal energy. The shift from heat-based preservation to acoustically driven alternatives is influencing energy consumption and product differentiation strategies. For instance, a patented ultrasonic brewing sonoreactor developed at the University of New South Wales demonstrated a 75% reduction in energy consumption, as published in the Journal of Food Engineering (2026). This highlights the potential cost and sustainability benefits for industrial food processors. Ultrasonic food processing achieves these advantages by utilizing cavitation, the formation and collapse of microscopic bubbles, rather than heat, making it energy-efficient and non-destructive to heat-sensitive bioactive compounds.

Key Report Takeaways

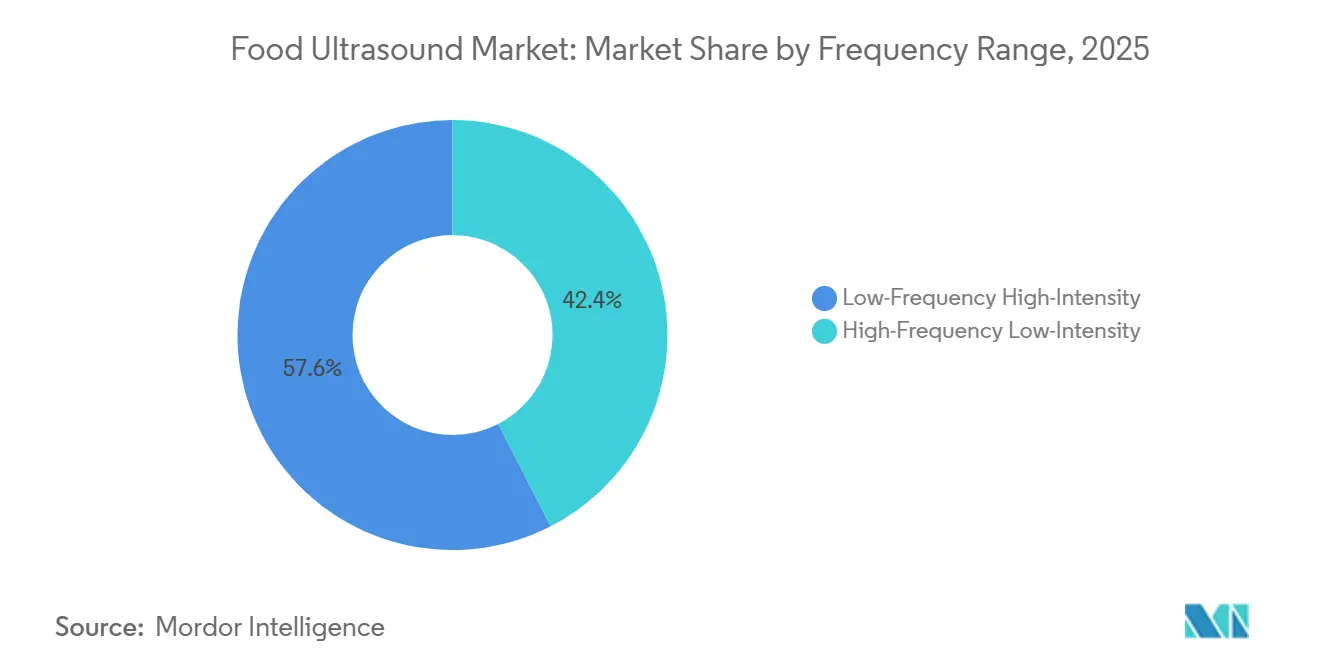

- By frequency range, the low-frequency high-intensity accounted for 57.56% of 2025 revenue, while high-frequency, low-intensity will post a 7.94% CAGR through 2031.

- By function, emulsification and homogenization led with 36.81% in 2025; quality assurance recorded the fastest CAGR of 7.53% to 2031.

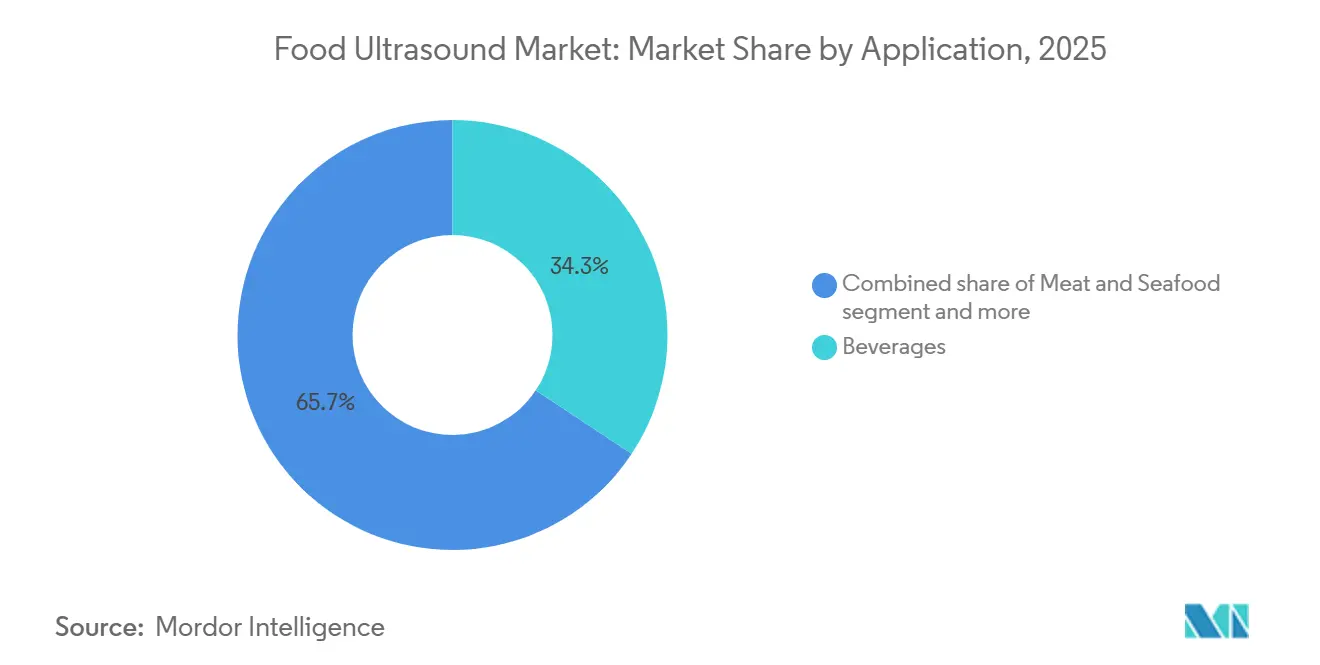

- By application, beverages accounted for 34.31% of 2025 demand, whereas meat and seafood is forecast to grow at a 8.76% CAGR through 2031.

- By geography, North America accounted for 40.75% of 2025 sales, while Asia-Pacific will expand at a 7.58% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Food Ultrasound Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of clean-label and minimal-additive formulations | +1.2% | Global; early leadership in North America and European Union | Short term (≤ 2 years) |

| Rising demand for non-thermal processing in shelf-life sensitive foods | +1.5% | Global; strongest in North America and European Union, rapid growth in Asia-Pacific | Short term (≤ 2 years) |

| Growing need for in-line quality control and defect detection | +0.8% | North America and European Union core, spill-over to Asia-Pacific | Medium term (2–4 years) |

| Plant-based and functional food processing complexity | +0.7% | North America, European Union, Asia-Pacific | Medium term (2–4 years) |

| Rising demand for sustainable and resource-efficient processing solutions | +0.6% | Global | Long term (≥ 4 years) |

| Stringent food safety and quality regulations | +0.5% | North America, European Union | Short to medium term (≤ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of clean-label and minimal-additive formulations

The growing demand for clean-label, low-additive formulations is driving the adoption of food ultrasound technologies. Food manufacturers are seeking processing methods that preserve product quality while reducing the use of artificial additives, preservatives, and chemical processing aids. As a non-thermal processing technology, food ultrasound supports processes such as emulsification, homogenization, extraction, and microbial control, while maintaining the natural taste, texture, and nutritional value of food products. The commercial significance of clean-label products is reflected in consumer purchasing trends, with Gen Z and Millennials, in particular, willing to pay 20–30% more for products labeled as organic, natural, high-protein, or free from artificial ingredients in 2025 [1]Source: Ingredion, "Less mystery, more meaning: Clean labels win consumer preference", ingredion.com. In response, food processors are increasingly adopting ultrasound-based solutions to facilitate clean-label product development, enhance ingredient functionality, and meet consumer demand for minimally processed foods.

Rising demand for non-thermal processing in shelf-life sensitive foods

The increasing demand for non-thermal processing in shelf-life-sensitive foods is driving the adoption of food ultrasound technology. Manufacturers are leveraging this technology to preserve product freshness, nutritional value, flavor, and texture without relying on traditional heat-based methods. Food ultrasound provides an effective non-thermal processing solution, enhancing microbial control, emulsification, homogenization, and extraction while reducing quality degradation. This technology works by utilizing high-frequency sound waves to create cavitation bubbles in liquids, which generate localized high temperatures and pressures, effectively disrupting microbial cells and facilitating various processing functions. With the growing consumer preference for minimally processed foods, producers are increasingly using ultrasound technologies to extend shelf life and improve product stability across categories such as beverages, dairy products, fresh produce, and ready-to-eat foods.

Plant-based and functional food processing complexity

The complexity of processing plant-based and functional foods is driving the adoption of food ultrasound technologies, as manufacturers seek advanced solutions to enhance texture, stability, emulsification, and ingredient functionality in sophisticated food formulations. Compared to conventional food products, plant-based meats, dairy alternatives, and functional foods often face challenges such as protein structuring, mouthfeel, ingredient dispersion, and shelf-life stability. Food ultrasound provides a non-thermal and efficient method to address these challenges while maintaining nutritional quality and supporting clean-label positioning. This need is further emphasized by strong consumer interest in plant-based products. According to a 2024 study by GFI, 71% of U.S. consumers aged 18–59 indicated they were at least somewhat likely to consume plant-based meat and/or dairy products in the future [2]Source: Good Food Institute, "U.S. foodservice market insights for plant-based foods", gfi.org. As demand for plant-based and functional foods grows, food processors are increasingly utilizing ultrasound technologies to improve product quality and production efficiency.

Rising demand for sustainable and resource-efficient processing solutions

The increasing demand for sustainable and resource-efficient processing solutions is driving the adoption of food ultrasound technologies. Food manufacturers are seeking methods to reduce energy consumption, processing time, water usage, and dependence on chemical additives while maintaining product quality. As a non-thermal and efficient processing technology, food ultrasound enhances processes such as extraction, emulsification, homogenization, and preservation, offering a lower environmental impact compared to some conventional methods. The emphasis on sustainability in consumer purchasing decisions is further supporting this trend. According to IFIC, 59% of Americans in 2025 consider it very important that their food is produced in an environmentally sustainable manner, an increase from 53% in 2021[3]Source: International Food Information Council (IFIC), "2025 IFIC Food & Health Survey", ific.org. As a result, food processors are increasingly investing in ultrasound-based solutions to align their production practices with sustainability objectives and changing consumer preferences.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost for industrial-scale retrofit and validation | -1.1% | Global; most acute in South America and Middle East and Africa | Short to medium term (≤ 4 years) |

| Competition from established processing technologies | -0.8% | North America, European Union | Medium term (2–4 years) |

| Process standardization gaps across diverse food matrices | -0.5% | Global | Long term (≥ 4 years) |

| Skilled operator and application engineering shortages | -0.4% | Global; most acute in Asia-Pacific and South America | Medium to long term (2+ years) |

| Source: Mordor Intelligence | |||

High capital cost for industrial-scale retrofit and validation

The high capital cost associated with industrial-scale retrofitting and validation is a significant restraint for the food ultrasound market. Implementing ultrasound technology necessitates substantial upfront investment in specialized equipment, system integration, facility modifications, and process validation. Additionally, food manufacturers face costs related to pilot testing, regulatory compliance, employee training, and performance verification prior to full-scale implementation. These financial and operational demands can hinder adoption, especially for small and medium-sized food processors, and may extend the return-on-investment period compared to traditional processing technologies.

Competition from established processing technologies

Established processing technologies pose a challenge to the growth of the food ultrasound market, as many food manufacturers continue to depend on traditional methods such as thermal pasteurization, high-pressure processing (HPP), homogenization, mechanical mixing, and conventional extraction systems. These methods are supported by proven performance, existing infrastructure, regulatory compliance, and broad industry acceptance, which diminishes the incentive for manufacturers to adopt ultrasound-based alternatives. Furthermore, concerns about integration complexity, validation processes, and uncertain return on investment often lead manufacturers to prioritize conventional technologies, especially in large-scale production settings where reliability and consistency are essential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Frequency Range: Power-Mode Dominance Coexists With High-Frequency Momentum

Low-frequency high-intensity ultrasound accounted for 57.56% of the 2025 market, highlighting its established role in applications such as emulsification, microbial inactivation, cutting, and cleaning. These functions collectively contribute to the majority of the equipment's deployed value. Typically operating in the 20–100 kHz range at intensities exceeding 10 W/cm², this technology leverages acoustic cavitation to produce mechanical, thermal, and chemical effects simultaneously. These effects are critical in various industrial processes, such as enhancing the stability of emulsions, effectively inactivating microbes to ensure product safety, precision cutting in manufacturing, and thorough cleaning of equipment. These capabilities justify its higher per-unit power consumption compared to diagnostic alternatives.

High-frequency low-intensity ultrasound is the fastest-growing frequency segment, with a CAGR of 7.94% projected for 2026–2031. This growth is driven by the increasing adoption of non-destructive quality sensing tools in automated food production lines. Operating above 100 kHz at intensities below 1 W/cm², this technology assesses physical properties such as fat content, texture, fermentation state, and foreign-body presence without altering the product. Its ability to provide real-time, accurate quality assessments without compromising product integrity makes it an essential tool in modern food processing, where efficiency and quality control are paramount.

By Function: Emulsification Leads on Scale; Sensing Reshapes the Growth Outlook

Emulsification and homogenization accounted for 36.81% of the 2025 market, driven by their established use in beverages, dairy products, sauces, and dressings, where achieving consistent and stable emulsions at industrial throughput rates is a fundamental production requirement. High-intensity ultrasound (HIU) technology produces droplet sizes below 200 nm with lower energy consumption compared to conventional high-pressure homogenizers. This advantage has been documented in peer-reviewed studies across various food matrices, including protein-polysaccharide complex emulsions. Microbial and enzyme inactivation, cleaning, and cutting collectively represent a significant portion of the remaining market, each with unique adoption patterns.

Quality assurance is the fastest-growing application, with a compound annual growth rate (CAGR) of 7.53% projected for 2026-2031, driven by increased investment in automated production line sensing technologies. Cutting applications benefit from established commercial platforms. For instance, Emerson's Branson Ultrasonics division offers frictionless portioning solutions for confectionery, bakery products, and frozen meals, providing advantages such as extended blade life and minimal product waste, as highlighted in Emerson's 2025 technical documentation. Additionally, Telsonic's sonotrodes, operating at frequencies of 20 kHz, 30 kHz, and 35 kHz, support inline rotary and robot-integrated cutting systems for pastry and layered food products.

By Food Application: Beverages Anchor Revenue; Meat and Seafood Drive Growth

The beverages segment accounted for 34.31% of the 2025 market, driven by the multifunctional benefits of ultrasound technology in liquid applications. These include emulsion stabilization, particle refinement, microbial reduction through cold processing, and flavor homogenization, all at throughput rates suitable for industrial beverage production. Ultrasonic homogenizers are particularly effective for juice and plant-based beverages, as they break down fruit pulp and pectin to prevent sedimentation while operating below 40°C, preserving heat-sensitive vitamins and anthocyanins.

The meat and seafood segment is projected to be the fastest-growing application, with a CAGR of 8.76% from 2026 to 2031. Growth is fueled by the demand for tenderization without the use of exogenous enzymes, accelerated marination, and protein modification for clean-label processed products. A 2025 study published in RSC Sustainable Food Technology on Bos indicus cattle demonstrated that high-intensity ultrasound at 150–262.5 W for 12–16 minutes reduces water loss and discoloration while enhancing tenderness. These outcomes align with the premium beef market's emphasis on chemical-free processing to support clean-label claims.

Geography Analysis

North America dominated the food ultrasound market, accounting for 40.75% of market revenue in 2026. This leadership is driven by a well-established food and beverage processing industry, widespread adoption of advanced manufacturing technologies, and increasing consumer demand for clean-label and minimally processed products. Food manufacturers in the region are investing in innovative processing solutions to enhance product quality, improve operational efficiency, and promote sustainability, fostering favorable conditions for the adoption of food ultrasound technologies.

Asia-Pacific is projected to be the fastest-growing regional market, with a CAGR of 7.58% during 2026–2031. Factors such as rapid urbanization, rising disposable incomes, and increasing consumption of processed and convenience foods are driving food manufacturers to modernize production facilities and adopt advanced processing technologies. Additionally, growing investments in food processing infrastructure and the expansion of domestic food industries in countries like China, India, Japan, and Australia are further contributing to market growth.

Europe, Latin America, and the Middle East and Africa are experiencing steady growth in the adoption of food ultrasound technologies. Food producers in these regions are increasingly focusing on improving processing efficiency, product quality, and sustainability. The rising interest in non-thermal processing methods, clean-label formulations, and resource-efficient manufacturing practices is driving the integration of ultrasound technologies across various food applications. Furthermore, ongoing innovations in food processing and heightened regulatory emphasis on sustainable production practices are creating additional growth opportunities in these regions.

Competitive Landscape

The ultrasonic food processing market reflects moderate fragmentation, indicating no single vendor holds a dominant position across all application areas. European precision ultrasonic specialists, including Hielscher Ultrasonics, Weber Ultrasonics, Telsonic, and SinapTec, compete based on transducer quality and depth in application engineering. In contrast, North American companies such as Emerson's Branson division and Dukane leverage their scale, extensive installed base, and long-standing food industry service infrastructure.

Chinese suppliers like Cheersonic and XIAOWEI focus on competitive pricing in commodity ultrasonic cutting and homogenization, gaining market share in Asia-Pacific and South America, where acquisition cost often takes precedence over total cost of ownership. Strategic differentiation in the market is increasingly driven by software and sensing integration rather than transducer hardware alone. Vendors incorporating IoT-enabled amplitude control, process logging, and closed-loop feedback systems, such as Emerson's Branson Polaris platform, are better positioned to secure long-term customer relationships. This approach shifts revenue streams from capital equipment sales to recurring software and maintenance services.

Opportunities for innovation exist in hybrid ultrasound systems that combine low-frequency inactivation with high-frequency sensing within a single flow-through reactor. Additionally, there is potential in validation documentation services designed to assist smaller food processors in meeting HACCP process authority requirements. Emerging disruptors in the market include companies developing ultrasonic solutions for plant-based protein extraction and ultrasonic-assisted fermentation systems. These areas are attracting interest from sustainable agri-food investors due to lower capital barriers and unique functional outcomes.

Food Ultrasound Industry Leaders

-

Hielscher Ultrasonics GmbH

-

Sonics & Materials, Inc.

-

Dukane

-

Weber Ultrasonics AG

-

Telsonic AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Emerson introduced the Branson Polaris Ultrasonic Welding Platform, a configurable and scalable ultrasonic welding system designed for modern manufacturing environments. The platform allows flexible integration of hardware and software components, enabling manufacturers to create customized welding solutions for applications in industries such as automotive, medical devices, electronics, consumer goods, food packaging, and bioplastics.

- April 2025: Fujitsu, in collaboration with Sonofai, Ishida Tec, and Tokai University, launched the SONOFAI T-01, the world's first automated inspection device capable of non-destructively assessing the fat content of frozen albacore tuna. The system uses ultrasound analysis combined with AI technology, leveraging Fujitsu’s ultrasound AI engine (part of its Kozuchi AI platform) to evaluate tuna quality in just 12 seconds. This represents a significant improvement over traditional manual tail-cut inspections, which require skilled workers and take considerably more time.

- March 2024: GEA introduced NiSoMate, a sensor-based inline monitoring system for homogenizers that provides real-time analysis of liquid products during processing. The system continuously measures product quality parameters such as density, consistency, and dilution using ultrasound-based sensor technology. This enables operators to adjust process conditions, such as homogenization pressure, instantly. NiSoMate replaces traditional lab sampling, reduces waste and energy consumption, and enhances process efficiency and product consistency.

Global Food Ultrasound Market Report Scope

| High-Frequency Low-Intensity |

| Low-Frequency High-Intensity |

| Quality Assurance |

| Microbial and Enzyme Inactivation |

| Emulsification and Homogenization |

| Cleaning |

| Cutting |

| Other Food Processing Functions |

| Meat and Seafood |

| Fruits and Vegetables |

| Dairy Products |

| Beverages |

| Bakery and Confectionery |

| Other Food Products |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Frequency Range | High-Frequency Low-Intensity | |

| Low-Frequency High-Intensity | ||

| By Function | Quality Assurance | |

| Microbial and Enzyme Inactivation | ||

| Emulsification and Homogenization | ||

| Cleaning | ||

| Cutting | ||

| Other Food Processing Functions | ||

| By Food Application | Meat and Seafood | |

| Fruits and Vegetables | ||

| Dairy Products | ||

| Beverages | ||

| Bakery and Confectionery | ||

| Other Food Products | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the size of the food ultrasound market in 2026?

The food ultrasound market is valued at USD 146.90 Million in 2026.

Which application segment leads the food ultrasound market?

In the food ultrasound market, the beverages segment leads with a 34.31% share in 2026.

Which region dominates the food ultrasound market?

North America dominates the food ultrasound market with a 40.75% share in 2026.

Which segment is growing fastest in the food ultrasound market?

In the food ultrasound market, meat and seafood applications are the fastest growing segment, registering a 8.76% CAGR (2026–2031).

Page last updated on: