Meal Kit Delivery Services Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

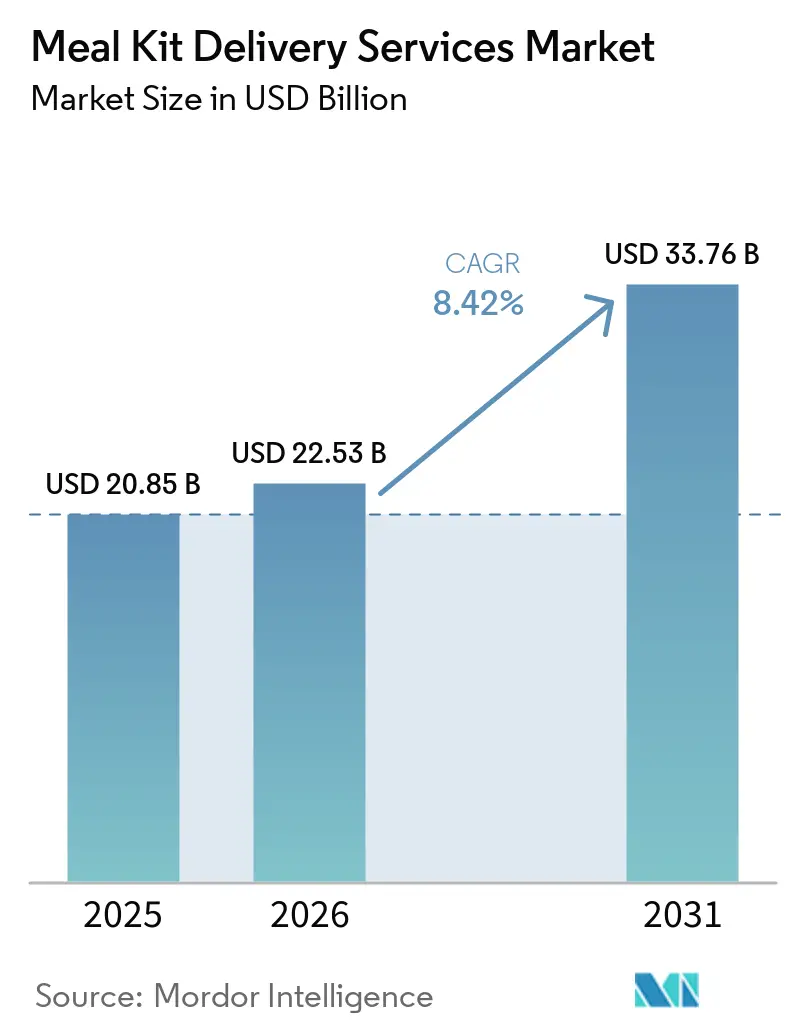

| Market Size (2026) | USD 22.53 Billion |

| Market Size (2031) | USD 33.76 Billion |

| Growth Rate (2026 - 2031) | 8.42% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

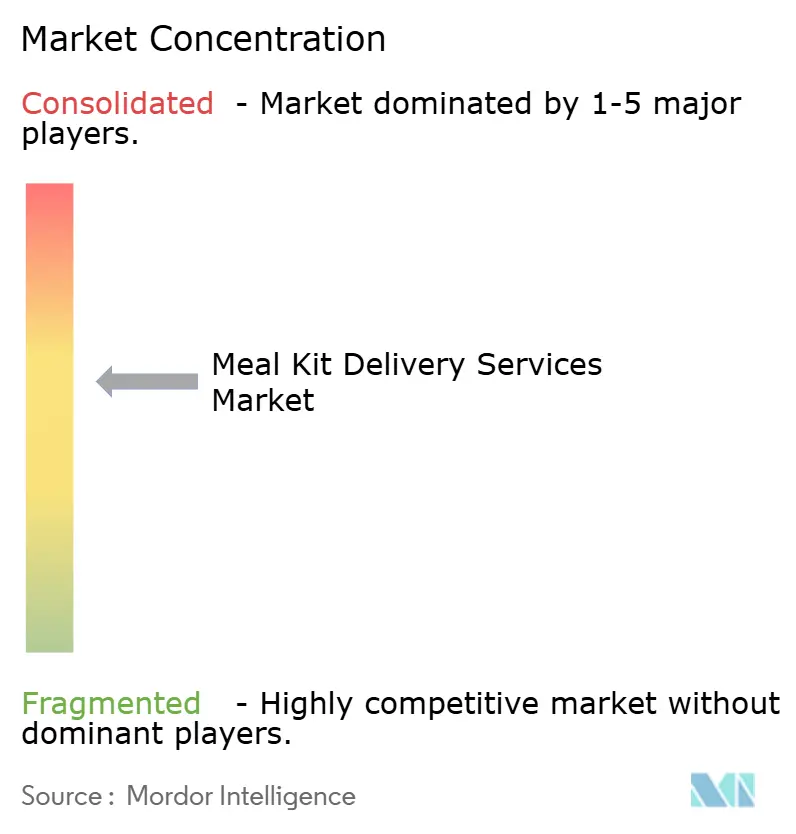

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Meal Kit Delivery Services Market Analysis by Mordor Intelligence

The meal kit delivery services market size is expected to grow from USD 20.85 billion in 2025 to USD 22.53 billion in 2026 and is forecast to reach USD 33.76 billion by 2031 at a 8.42% CAGR over 2026-2031. The global meal kit delivery services market is driven by evolving consumer lifestyles, a growing demand for convenience, and an increasing preference for home-cooked meals without the need for meal planning or grocery shopping. Factors such as busy work schedules, urbanization, and the rise in dual-income households have led consumers to adopt subscription-based meal solutions that provide pre-portioned ingredients and simple recipes. Additionally, rising health awareness is boosting demand for meal kits offering calorie-controlled, organic, plant-based, high-protein, and allergen-friendly options tailored to various dietary needs. The expansion of e-commerce, increased smartphone usage, and the adoption of digital payment systems have improved the accessibility of online meal ordering. Advancements in cold-chain logistics and packaging technologies have further enhanced product freshness and delivery efficiency. Moreover, consumers are increasingly seeking culinary variety and premium dining experiences at home, encouraging meal kit providers to introduce chef-designed recipes, international cuisines, and customizable menus. Efforts to reduce food waste through precise ingredient portioning, along with strategic collaborations between meal kit providers, retailers, and food manufacturers, are also contributing to market growth by expanding customer reach and improving service offerings.

Key Report Takeaways

- By offering, ready-to-cook held 68.34% of the global meal kit delivery services market share in 2025, while ready-to-eat is forecast to expand at an 8.91% CAGR from 2026 to 2031.

- By meal type, non-vegetarian held 53.53% of the global meal kit delivery services market share in 2025, while vegan is projected to grow at a 9.15% CAGR through 2031.

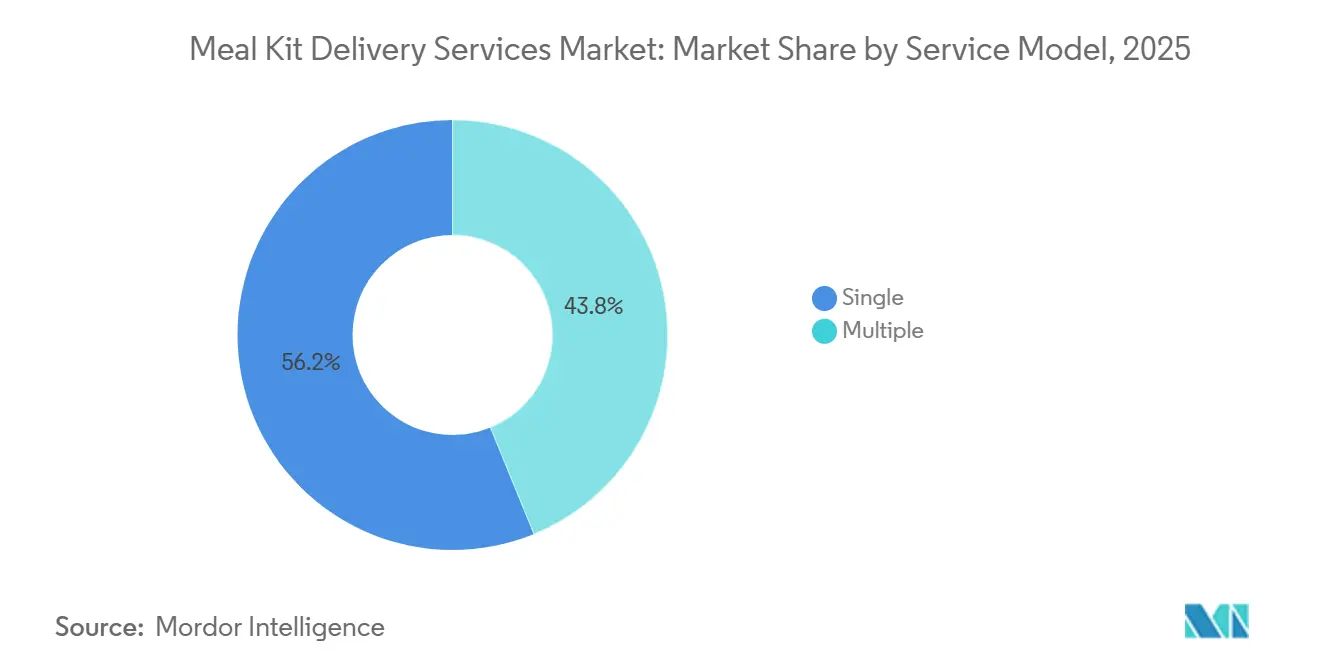

- By service model, single-plan deliveries accounted for 56.19% of the global meal kit delivery services market share in 2025, while multiple-delivery plans are expected to advance at an 8.84% CAGR from 2026 to 2031.

- By fulfillment channel, online retail captured 65.58% of the global meal kit delivery services market share in 2025 and also recorded the highest projected CAGR at 9.43% through 2031.

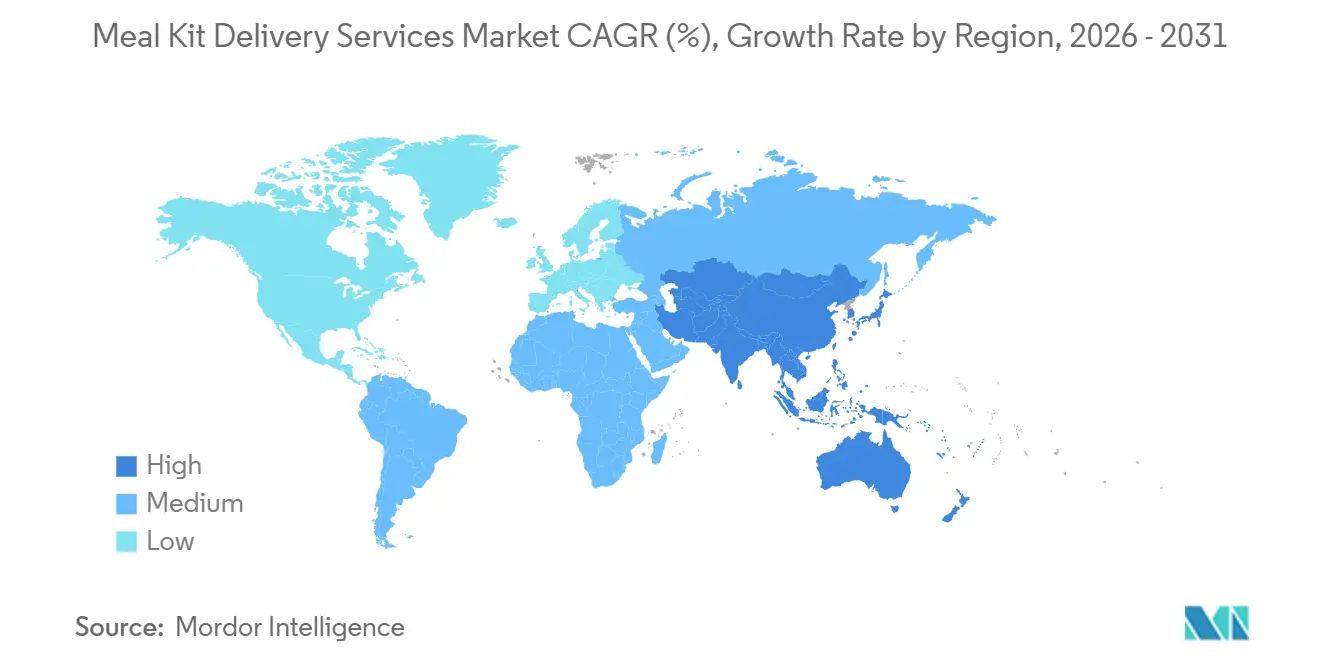

- By geography, North America held 41.63% of the global meal kit delivery services market share in 2025, while Asia-Pacific is forecast to grow at a 9.29% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Meal Kit Delivery Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing consumer preference for convenient home cooking | +1.8% | Global, led by North America and Western Europe | Short term (≤ 2 years) |

| Rising demand for healthy and portion-controlled meals | +1.5% | Global, concentrated in North America and United Kingdom | Medium term (2–4 years) |

| Expansion of specialized dietary and lifestyle meal options | +1.3% | North America, Western Europe, urban Asia-Pacific | Medium term (2–4 years) |

| Advancements in digital ordering platforms and subscription management | +1.4% | Global, with accelerated adoption in Asia-Pacific | Medium term (2–4 years) |

| Expansion of premium, gourmet, and chef-curated meal kits | +1.0% | North America, United Kingdom, Germany, Australia | Long term (≥ 4 years) |

| Growing adoption of sustainable packaging and food waste reduction | +0.6% | Europe, North America, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing consumer preference for convenient home cooking

The increasing preference for convenient home cooking is a key driver of the global meal kit delivery services market. Consumers are seeking solutions that combine the satisfaction of preparing fresh meals with the convenience of pre-portioned ingredients and easy-to-follow recipes. Factors such as busy lifestyles, limited time, and growing awareness of healthy eating have led households to opt for meal kits that simplify meal planning and grocery shopping while enabling home-cooked dining experiences. This trend is further supported by the desire to control ingredient quality, minimize food waste, and explore diverse cuisines with minimal preparation. Consumer sentiment underscores the sustained popularity of home cooking. According to HelloFresh's 2025–2026 State of Home Cooking Report, 93% of Americans plan to cook as much as or more than they did in the previous year over the next 12 months, reflecting the ongoing demand for convenient cooking solutions. As meal kit providers continue to enhance menu variety, offer dietary customization, and provide flexible subscription options, the growing preference for hassle-free home cooking is expected to drive consistent market growth globally.

Rising demand for healthy and portion-controlled meals

The growing demand for healthy and portion-controlled meals is a key factor driving the global meal kit delivery services market. Consumers are increasingly focused on weight management, improving nutrition, and reducing the risk of lifestyle-related diseases. Meal kit services cater to these needs by providing balanced recipes with pre-measured ingredients, clear nutritional information, and options customized to dietary preferences such as low-calorie, high-protein, and diabetic-friendly meals. The convenience of receiving nutritionally planned meals supports healthier eating habits while helping to prevent overeating and reduce food waste. The rising prevalence of obesity further reinforces this trend. According to the 2025 FACT SHEET – Obesity in America, published by the Centers for Disease Control and Prevention, obesity affects 40.3% of the United States population, with severe obesity impacting 9.4%[1]Source: American Society for Metabolic & Bariatric Surgery, "2025 FACT SHEET -- OBESITY IN AMERICA," asmbs.org. These concerning statistics are driving consumers to seek healthier meal solutions that emphasize portion control and balanced nutrition, thereby boosting the adoption of meal kit delivery services globally.

Expansion of specialized dietary and lifestyle meal options

The growth in specialized dietary and lifestyle meal options is a significant driver of the global meal kit delivery services market. Consumers are increasingly seeking meal solutions that align with their health goals, ethical values, and nutritional needs. To meet this demand, meal kit providers are expanding their offerings to include plant-based, vegan, ketogenic, gluten-free, low-carbohydrate, high-protein, and other customized meal plans. These options allow consumers to maintain specific eating patterns without the challenges of meal planning or ingredient sourcing. This emphasis on personalization enhances customer satisfaction, improves subscription retention rates, and attracts a broader consumer base with varied dietary preferences. According to the 2025 IFIC Food & Health Survey, 3% of Americans follow a plant-based diet, and 1% adhere to a vegan diet[2]Source: International Food Information Council, "2025 IFIC Food & Health Survey," ific.org. Additionally, according to the same report, 5% of Americans follow a ketogenic or high-fat diet[3]Source: International Food Information Council, "2025 IFIC Food & Health Survey," ific.org. The rising adoption of these specialized dietary lifestyles is prompting meal kit companies to continually diversify their offerings. This approach makes tailored nutrition more accessible and supports sustained growth in the global meal kit delivery services market.

Advancements in digital ordering platforms and subscription management

Advancements in digital ordering platforms and subscription management are playing a crucial role in driving the global meal kit delivery services market by enhancing convenience and personalization in meal selection, purchasing, and delivery. Meal kit providers are utilizing intuitive mobile applications, AI-powered recommendation systems, and user-friendly websites to enable customers to customize menus, adjust serving sizes, manage delivery schedules, pause or modify subscriptions, and make secure digital payments with ease. Key features such as personalized recipe suggestions based on dietary preferences, automated recurring orders, real-time delivery tracking, and flexible subscription plans have significantly improved customer engagement and retention rates. Additionally, the integration of data analytics helps companies better understand consumer preferences, optimize inventory management, and minimize food waste, thereby delivering a more tailored customer experience. As digital commerce continues to grow and consumers increasingly demand seamless online services, ongoing innovations in ordering platforms and subscription management are fostering customer loyalty and driving the global adoption of meal kit delivery services.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited shelf life of fresh ingredients | -1.2% | Global, more acute in markets lacking dense urban delivery networks | Short term (≤ 2 years) |

| Complex cold chain and last-mile delivery requirements | -1.0% | Asia-Pacific emerging markets, South America, Middle East and Africa | Medium term (2–4 years) |

| Consumer preference for traditional grocery shopping and fresh ingredient selection | -0.8% | Mature markets: United States, Germany, United Kingdom | Short term (≤ 2 years) |

| Price sensitivity and premium perception | -1.1% | Global, led by cost-of-living pressures in Europe and North America | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Consumer preference for traditional grocery shopping and fresh ingredient selection

Consumer preference for traditional grocery shopping and for personally selecting fresh ingredients continues to be a significant restraint on the global meal kit delivery services market. Many consumers prioritize the ability to evaluate the freshness, quality, and appearance of produce, meat, seafood, and other perishables before purchasing, an experience that meal kit subscriptions cannot fully replicate. Shopping at local supermarkets, farmers' markets, and neighborhood grocery stores also offers greater flexibility to compare prices, select preferred brands, purchase specific quantities, and make spontaneous meal decisions based on seasonal availability or promotional offers. Additionally, some consumers value the social and recreational aspects of grocery shopping and prefer to create their own recipes rather than adhere to pre-planned meal kits. Concerns regarding packaging waste, subscription commitments, and the inability to make last-minute ingredient substitutions further deter certain customer groups from adopting meal kit services. Consequently, the sustained popularity of conventional grocery shopping limits the growth potential of meal kit delivery services across various consumer segments.

Price sensitivity and premium perception

Price sensitivity and the perception of meal kits as a premium-priced service continue to hinder the growth of the global meal kit delivery services market. While meal kits provide convenience, recipe guidance, and pre-portioned ingredients, many consumers compare their per-meal cost to purchasing ingredients from supermarkets. Supermarkets often offer more economical options through bulk buying, private-label products, and promotional discounts. Budget-conscious households, particularly during periods of inflation and economic uncertainty, may view recurring meal kit subscriptions as discretionary rather than essential. Additional costs, such as delivery charges and subscription fees, along with limited pricing flexibility, further deter adoption among cost-sensitive consumers. This challenge is especially significant in price-conscious emerging markets, where affordability often takes precedence over convenience in food purchasing decisions. As a result, the perception that meal kits cater primarily to higher-income consumers restricts broader market penetration and remains a significant barrier to sustained global market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Ready-to-Eat Closes the Gap on Cook-at-Home Dominance

Ready-to-cook products accounted for 68.34% of the meal kit delivery market value in 2025, driven by the growing demand for convenient home cooking solutions. These products reduce meal preparation time while preserving the experience of cooking with fresh ingredients. Consumers with busy lifestyles are increasingly opting for pre-portioned ingredients and step-by-step recipes that eliminate the need for grocery shopping, simplify meal planning, and minimize food waste, all without compromising nutritional quality or taste. Rising health consciousness has further fueled demand for balanced and customizable meal kits, including options such as organic, high-protein, plant-based, gluten-free, and low-calorie meals. Additionally, the growing interest in culinary exploration has encouraged consumers to try chef-inspired recipes and international cuisines, which often require specialty ingredients. Technological advancements in digital ordering platforms, flexible subscription models, and cold-chain logistics have enhanced customer convenience, ensured product freshness, and improved delivery reliability. Furthermore, increasing awareness of sustainable consumption, through reduced food waste and optimized ingredient portions, has supported the adoption of ready-to-cook meal kits across households globally.

Ready-to-eat products are projected to grow at a CAGR of 8.91% during 2026-2031, driven by the rising demand for maximum convenience among consumers with demanding work schedules, limited cooking skills, and fast-paced urban lifestyles. Fully prepared meals requiring little or no preparation provide an appealing solution for individuals seeking nutritious food without the time investment in cooking or cleaning. The growing demand for healthy, restaurant-quality meals with transparent nutritional labeling has prompted providers to expand offerings catering to dietary preferences such as high-protein, low-carbohydrate, vegan, diabetic-friendly, and calorie-controlled diets. The expansion of online food delivery platforms, mobile applications, and subscription-based meal services has improved accessibility and ordering convenience, enhancing customer retention. Innovations in food preservation, modified atmosphere packaging, and refrigerated logistics have extended product shelf life while maintaining freshness and taste. Additionally, the increasing number of single-person households, aging populations, students, and working professionals continues to drive demand for ready-to-eat meal delivery services, supporting sustained global market growth.

By Meal Type: Non-Vegetarian Leads, Vegan Accelerates Fastest

Non-vegetarian products maintained a dominant 53.53% market share in 2025, driven by strong consumer demand for protein-rich meals that combine convenience with restaurant-quality taste and nutritional value. Growing awareness of the benefits of lean proteins in supporting muscle development, weight management, and overall wellness has encouraged consumers to opt for meal kits featuring chicken, beef, pork, seafood, and other animal-based proteins. The increasing prevalence of busy lifestyles and limited time for meal preparation has further fueled demand for pre-portioned ingredients and easy-to-follow recipes, simplifying cooking while ensuring freshness and consistent quality. Additionally, consumers are showing heightened interest in premium meat cuts, sustainably sourced seafood, free-range poultry, and globally inspired recipes, prompting meal kit providers to diversify their product offerings. Advancements in refrigerated logistics, cold-chain infrastructure, and vacuum-sealed packaging have improved the safe transportation and shelf life of perishable proteins, boosting consumer confidence in home-delivered non-vegetarian meal kits.

Vegan meal kits are expected to grow at a 9.15% CAGR from 2026 to 2031, driven by the increasing adoption of plant-based lifestyles, growing health consciousness, and heightened awareness of environmental sustainability and animal welfare. Consumers are seeking convenient meal solutions that provide balanced nutrition without the need to independently source and prepare a variety of plant-based ingredients. In response, meal kit providers are offering diverse vegan recipes featuring legumes, whole grains, vegetables, nuts, seeds, and innovative plant-based protein alternatives, appealing to both dedicated vegans and flexitarian consumers. Rising concerns about the environmental impact of livestock production, along with growing interest in reducing carbon footprints, have further bolstered demand for vegan meal solutions. Advances in plant-based food innovation have enhanced the taste, texture, and nutritional quality of vegan ingredients, making these meal kits more attractive to mainstream consumers.

By Service Model: Single Plans Hold Ground, Multiple Offerings Gain Share

In 2025, single-plan deliveries accounted for a 56.19% market share, driven by consumer preferences for simplicity, affordability, and a hassle-free subscription experience. First-time users and budget-conscious households often favor standardized meal plans, which eliminate the complexity of choosing from numerous options while providing predictable pricing and consistent weekly deliveries. This model allows meal kit providers to optimize procurement, inventory management, and meal production, leading to reduced operational costs and enhanced supply chain efficiency. Additionally, standardized menus help minimize food waste and improve demand forecasting, enabling companies to maintain competitive pricing without compromising quality. Consumers with routine eating habits or minimal dietary restrictions value the convenience of curated meal selections that require little decision-making. The combination of operational efficiency, cost-effectiveness, and ease of use continues to drive the adoption of single-plan service models, particularly among smaller households, new subscribers, and value-focused consumers.

Multiple-delivery service plans are projected to grow at a CAGR of 8.84% from 2026 to 2031, fueled by increasing consumer demand for flexibility, personalization, and meal options tailored to diverse dietary preferences and household needs. Modern consumers expect meal kit providers to cater to a wide range of lifestyles, including vegetarian, vegan, ketogenic, and gluten-free diets, as well as family-friendly, high-protein, low-calorie, and gourmet meal options. By offering multiple subscription plans, companies can attract a broader customer base and enhance customer satisfaction through greater choice and customization. Flexible plans that allow users to adjust meal preferences, serving sizes, delivery frequency, and subscription schedules contribute to improved retention rates and reduced cancellations. Furthermore, advancements in digital ordering platforms, artificial intelligence, and customer analytics enable providers to recommend personalized meal plans based on purchasing behavior and nutritional preferences. As consumer expectations increasingly shift toward individualized food experiences, the availability of multiple service plans has emerged as a critical competitive advantage, driving growth in the global meal kit delivery services market.

By Fulfillment Channel: Online Retail Consolidates Both Share and Growth

Online retail accounted for 65.58% of the fulfillment channel value in 2025 and is also the fastest-growing channel, with a 9.43% CAGR during 2026-2031. This growth is driven by increasing internet penetration, widespread smartphone adoption, and the rising preference for convenient digital shopping experiences. Consumers are increasingly drawn to online platforms that enable them to browse menus, customize meal preferences, manage subscriptions, schedule deliveries, and make secure payments through a single interface. Features such as flexible ordering options, AI-powered meal recommendations, loyalty programs, and real-time order tracking further enhance customer convenience and engagement. The development of e-commerce infrastructure, coupled with same-day and next-day delivery capabilities and advanced cold-chain logistics, has improved the reliability and freshness of delivered meal kits, encouraging repeat purchases. Additionally, digital marketing strategies, subscription discounts, and personalized promotions have proven effective in acquiring and retaining customers.

The offline retail fulfillment channel is gaining momentum as supermarkets, hypermarkets, specialty food stores, and grocery chains expand their ready-to-cook and ready-to-eat meal kit offerings to meet evolving consumer preferences. Many shoppers prefer purchasing meal kits during routine grocery trips, as this allows them to inspect packaging, verify freshness, compare product options, and make immediate purchasing decisions without waiting for home delivery. Retail stores also encourage impulse purchases through appealing in-store displays and promotional campaigns, while eliminating subscription commitments that may deter some consumers. Collaborations between meal kit brands and established retail chains have significantly enhanced product accessibility and market visibility, particularly among consumers unfamiliar with subscription-based services. Retailers are also introducing exclusive meal kit ranges featuring local ingredients, seasonal recipes, and private-label offerings, which help differentiate their product portfolios. The convenience of same-day availability, combined with the growing retail distribution network, continues to support the expansion of the offline fulfillment channel within the global meal kit delivery services market.

Geography Analysis

North America accounted for 41.63% of the global meal kit delivery market in 2025, driven by strong consumer demand for convenient and time-saving meal solutions. This demand is supported by busy lifestyles, high disposable incomes, and the widespread adoption of e-commerce. The region benefits from a well-established subscription economy, enabling consumers to access customizable meal plans through digital platforms. Increasing health awareness has fueled demand for nutritionally balanced, portion-controlled, organic, and specialized meal kits catering to vegan, ketogenic, gluten-free, and high-protein diets. Additionally, the rise in dual-income and single-person households has amplified the need for convenient meal preparation options that minimize grocery shopping time and food waste. Market growth is further supported by continuous innovation from leading meal kit providers, the expansion of ready-to-eat offerings, advancements in cold-chain logistics, and partnerships with supermarkets and retailers. Strong internet penetration, efficient last-mile delivery networks, and consumers' willingness to pay for premium convenience solidify North America's position as a leading market for meal kit delivery services.

Asia-Pacific is the fastest-growing region in the meal kit delivery market, with a 9.29% CAGR projected for 2026-2031. This growth is driven by increasing urbanization, expanding middle-class populations, rising disposable incomes, and widespread smartphone adoption in countries such as China, Japan, South Korea, India, and Australia. Consumers are increasingly turning to digital food purchasing platforms as demanding work schedules and long commutes heighten the need for convenient meal solutions. The rapid development of food delivery ecosystems and digital payment infrastructure has made meal kits more accessible in metropolitan areas. Providers are introducing regionally inspired recipes and locally sourced ingredients to cater to diverse culinary preferences while offering healthier alternatives to dining out. Growing health consciousness, interest in home cooking, and the popularity of premium convenience foods are further driving market expansion. Improvements in cold-chain logistics, increasing e-commerce penetration, and investments by domestic and international meal kit companies are accelerating adoption across the region.

The meal kit delivery market in Europe, South America, and the Middle East and Africa is influenced by evolving consumer lifestyles, growing digital retail penetration, and rising demand for convenient, high-quality meal solutions. In Europe, strong environmental awareness, demand for sustainable packaging, preference for organic ingredients, and the adoption of plant-based and health-focused diets are driving the popularity of meal kit subscriptions. In South America, expanding internet access, rising urban populations, improving disposable incomes, and increasing acceptance of online grocery shopping are creating opportunities for meal kit providers, particularly in major metropolitan areas. Meanwhile, the Middle East and Africa is experiencing growth due to rapid urbanization, an expanding expatriate population, greater workforce participation by women, and increasing investments in e-commerce infrastructure and temperature-controlled logistics. Across these regions, consumers are seeking greater convenience, dietary customization, and premium food experiences. Meal kit providers are responding by expanding localized menus, offering flexible subscription models, and forming retail partnerships to enhance market penetration.

Competitive Landscape

The global meal kit delivery services market features a mix of established operators, regional providers, and niche specialists competing through diverse product offerings, digital capabilities, and supply chain efficiency. Leading companies are expanding their portfolios to include budget-friendly, premium, organic, family-oriented, and ready-to-eat options, aiming to cater to a wider consumer base. Investments in vertically integrated sourcing, automated fulfillment centers, and advanced demand forecasting are being made to enhance operational efficiency, reduce costs, and improve customer retention. Geographic expansion strategies are becoming more selective, with providers concentrating on high-growth markets while optimizing operations in less profitable regions to ensure long-term profitability.

Competition in the market is increasingly focused on infrastructure development and business-to-business fulfillment capabilities. Beyond direct-to-consumer subscription models, service providers are now supporting grocery retailers, private-label brands, and emerging meal kit companies through shared production facilities, logistics networks, and white-label fulfillment services. This asset-light operating model reduces entry barriers for new participants and facilitates the integration of meal kits into supermarket and omnichannel retail ecosystems. Strategic investments in fulfillment technology, cold-chain logistics, and scalable manufacturing capabilities are enabling companies to enhance service reliability and expand distribution across multiple sales channels.

Innovation continues to be a critical competitive factor, with companies focusing on personalized nutrition, digital engagement, and premium consumer experiences. Providers are fostering customer loyalty by offering AI-powered meal recommendations, personalized subscription management, flexible delivery schedules, and dynamic menu rotations tailored to individual preferences. Collaborations with professional chefs, nutrition experts, and culinary creators are further differentiating offerings through exclusive recipes and premium dining experiences. The competitive landscape is evolving toward comprehensive food and nutrition platforms that integrate meal planning, health-focused solutions, and digital wellness services. These initiatives are helping providers strengthen subscriber retention, diversify revenue streams, and move beyond traditional meal kit subscription models.

Meal Kit Delivery Services Industry Leaders

-

Gousto Group Ltd.

-

Marley Spoon AG

-

Blue Apron Holdings, Inc.

-

The Kroger Co.

-

HelloFresh SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: HelloFresh became the Official Meal Kit Provider of the BottleRock Napa Valley Music Festival, marking its first sponsorship of a major music festival. The collaboration included a dedicated performance stage, live cooking demonstrations by celebrity chefs, recipe sampling, exclusive merchandise, and interactive culinary activities for attendees. To extend the festival experience, HelloFresh introduced a limited-time collection of globally inspired recipes for subscribers, paired with curated music playlists timed to each recipe's preparation. This partnership aimed to enhance brand engagement by integrating food, music, and home cooking, while highlighting HelloFresh's diverse international recipe offerings and improving customer experience through interactive initiatives.

- August 2025: HelloFresh announced a USD 70 million investment to advance product innovation within its meal kit portfolio. This investment aims to expand menu variety, enhance ingredient quality, increase healthy and diet-specific meal options, introduce quick-preparation meals for added convenience, and improve personalization through AI-driven recommendations. The company added over 100 new weekly menu choices, larger protein portions, premium seafood and steak options, and more than 25 quick and easy meal options. This initiative is part of a broader efficiency strategy designed to reallocate resources toward customer-focused innovation, strengthening the company's competitive position and supporting long-term growth in the meal kit delivery market.

- August 2025: Wonder incorporated Blue Apron meal kits into its app, enabling customers to order meal kits alongside prepared restaurant meals through a unified platform. This integration eliminated the need for a traditional subscription, allowing one-time purchases with delivery available in as little as three days, thereby enhancing convenience and accessibility. The initiative aims to establish the platform as a comprehensive mealtime solution by combining restaurant delivery services with at-home cooking options. Furthermore, the company improved the meal kit offering by introducing 15-minute recipes, reducing shipping fees, and maintaining price stability, while continuing to operate the standalone nationwide meal kit service under the Blue Apron brand.

Global Meal Kit Delivery Services Market Report Scope

| Ready to Cook |

| Ready to Eat |

| Non-Vegetarian |

| Vegetarian |

| Vegan |

| Single |

| Multiple |

| Online Retail |

| Offline Retail |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Offering | Ready to Cook | |

| Ready to Eat | ||

| By Meal Type | Non-Vegetarian | |

| Vegetarian | ||

| Vegan | ||

| By Service Model | Single | |

| Multiple | ||

| By Fulfillment Channel | Online Retail | |

| Offline Retail | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What will the meal kit delivery services market be worth by 2031?

The meal kit delivery services market is projected to reach USD 33.76 billion by 2031, rising from USD 22.53 billion in 2026 at an 8.42% CAGR.

Which region leads meal kit delivery services in 2025, and which one grows fastest?

North America led with 41.63% share in 2025, while Asia-Pacific is projected to grow the fastest at a 9.29% CAGR from 2026 to 2031.

Which meal kit format holds the largest share, and which one grows fastest?

Ready-to-cook remained the largest format with 68.34% share in 2025, while ready-to-eat is expected to post the fastest growth at an 8.91% CAGR.

Which dietary segment is expanding the fastest in meal kits?

Vegan meal kits are projected to grow the fastest at a 9.15% CAGR through 2031, even as non-vegetarian offerings held the largest 2025 share at 53.53%.

Page last updated on: