Food Certification Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 6.75 Billion |

| Market Size (2031) | USD 8.72 Billion |

| Growth Rate (2026 - 2031) | 5.26% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Food Certification Market Analysis by Mordor Intelligence

The global food certification market size was valued at USD 6.41 billion in 2025 and estimated to grow from USD 6.75 billion in 2026 to reach USD 8.72 billion by 2031, at a CAGR of 5.26% during the forecast period (2026-2031). This growth is driven by increasing complexity in global food supply chains, heightened regulatory scrutiny, and mandatory certification requirements, particularly for halal products and novel foods in the European Union. Increased corporate outsourcing of research and development and quality assurance work, growing international trade flows, and rising demand for regulated materials and processes further support the market expansion. The food industry's rapid digitalization has led to increased adoption of digital solutions for accurate food safety data recording and improved compliance. Consumer awareness regarding food safety and preference for properly labeled products has also contributed to market growth, along with rising concerns about artificial products and the increasing prevalence of foodborne illnesses. The implementation of stringent food safety regulations across regions has necessitated that businesses obtain various certifications to maintain market access and consumer trust. Additionally, the growing emphasis on sustainable and ethical food production practices has increased the demand for specialized certifications, while the rise in cross-border food trade has made international food safety standards more crucial than ever. As the global food industry continues to evolve, food certification will remain a fundamental component in ensuring food safety, maintaining consumer confidence, and facilitating international trade.

Key Report Takeaways

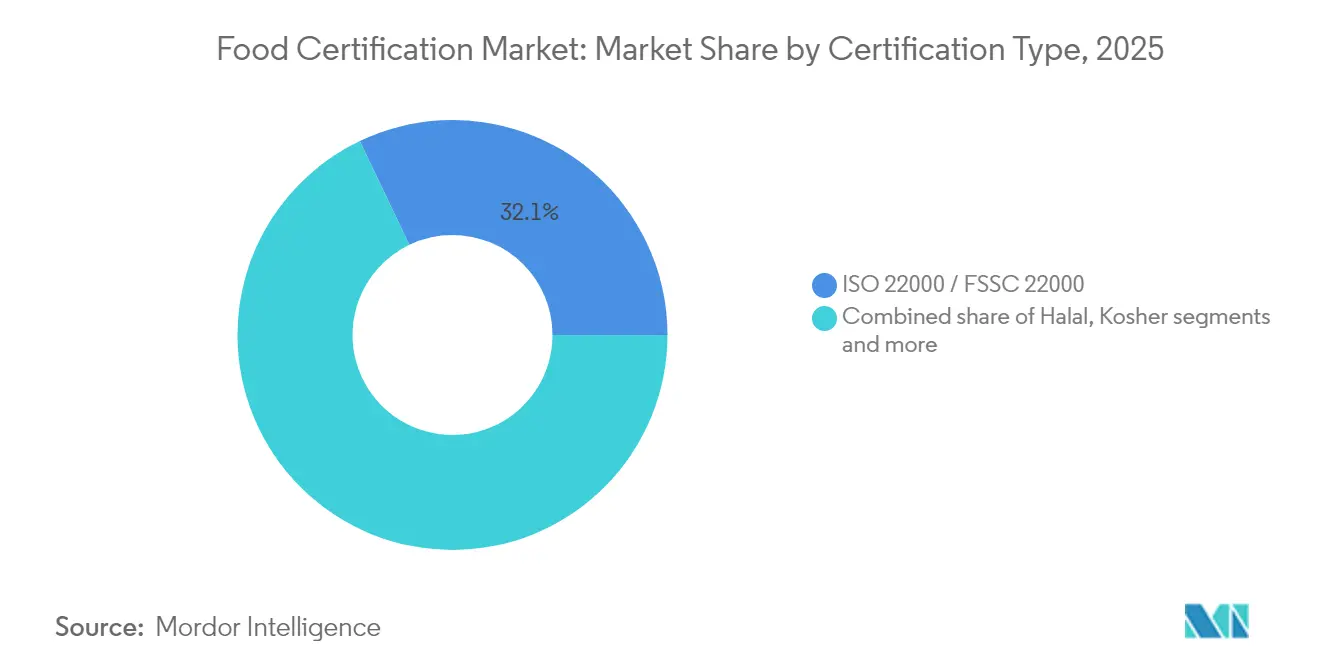

- By certification type, ISO 22000/FSSC 22000 led with 32.10% of food certification market share in 2025, while halal certification is projected to accelerate at a 7.52% CAGR through 2031

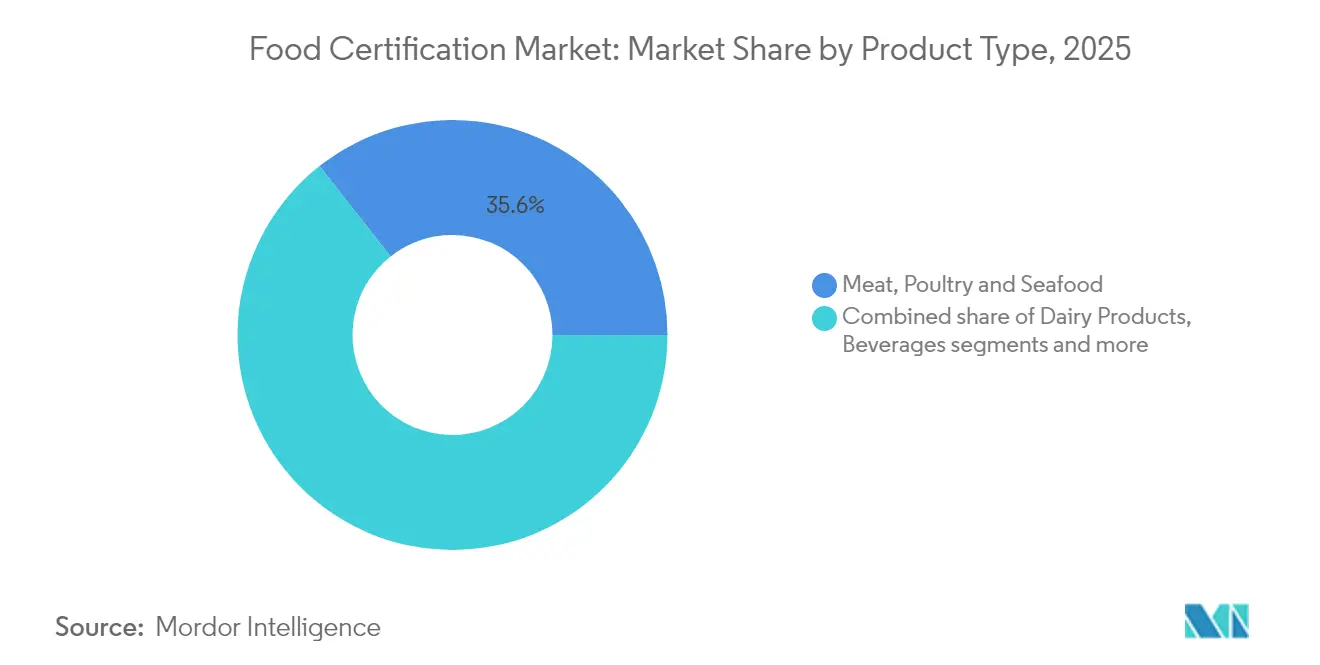

- By product type, meat, poultry, and seafood commanded 35.62% share of the food certification market size in 2025; free-from and allergen-free foods are expected to expand at a 7.48% CAGR to 2031

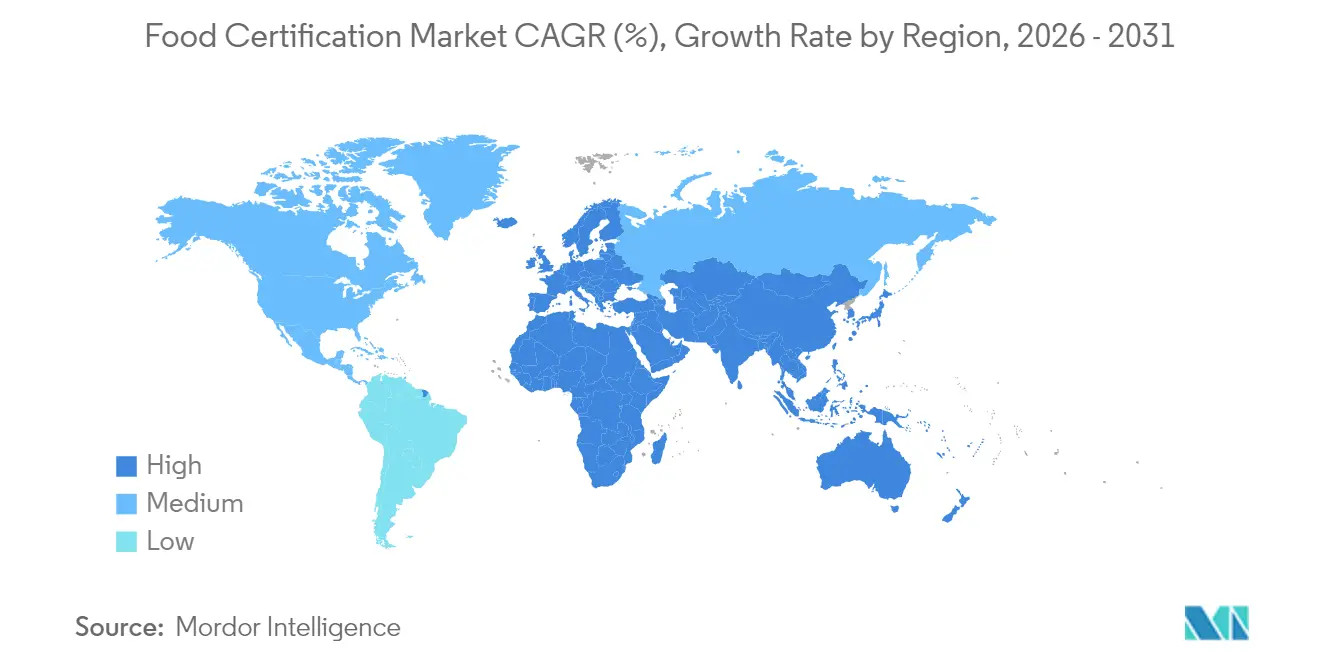

- By geography, Europe accounted for 33.74% of the food certification market size in 2025, whereas Asia-Pacific is set to record the fastest 7.24% CAGR between 2026-2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Food Certification Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer demand for food-safety and transparency | +1.2% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Stringent government regulations and compliance requirements | +1.8% | Global, particularly Asia-Pacific and Europe | Long term (≥ 4 years) |

| Expanding cross-border food trade drives multi-standard adoption | +0.9% | Global, emphasis on emerging markets | Medium term (2-4 years) |

| Growing popularity of clean-label and transparency movements | +0.7% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Expansion of private label and contract manufacturing | +0.6% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Technological advancements in auditing and traceability | +0.4% | Global, led by developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising consumer demand for food-safety and transparency

The increasing consumer awareness about food safety and transparency is significantly driving the food certification market, with consumers actively seeking detailed information about food sources, production methods, and ingredient authenticity. Social media and digital platforms have enhanced consumer access to food safety information, leading to heightened scrutiny of food products and their certifications. Recent food safety incidents have reinforced the importance of third-party certifications, as evidenced by BRCGS data showing that 91% of consumers are influenced by third-party verification for gluten-free products, while 76% prefer products certified by recognized coeliac associations [1]Source: BRCGS, “Gluten-Free Certification Program,” brcgs.com . This heightened awareness has prompted food manufacturers to adopt certification standards, implement transparent labeling practices, and invest in food safety certifications to maintain consumer trust and market share. The trend is further strengthened by the growing population of health-conscious consumers creating demand for certified organic, non-GMO, and allergen-free products. Food manufacturers are responding to this demand by obtaining multiple certifications to address various consumer concerns and regulatory requirements. The integration of blockchain technology and digital traceability solutions is further enhancing the credibility and transparency of food certification systems.

Stringent government regulations and compliance requirements

Government regulations and compliance requirements for food safety and quality standards continue to strengthen globally, particularly in North America and Europe. The implementation of regulations such as the Food Safety Modernization Act (FSMA) in the United States and the General Food Law in the European Union mandates food businesses to obtain certifications like HACCP, ISO 22000, and FSSC 22000. The increasing number of foodborne illnesses, with WHO reporting in October 2024, approximately 600 million people falling ill and 420,000 deaths annually from contaminated food, has prompted governments to enforce stricter food safety measures [2]Source: World Health Organization, “Food Safety,” who.int. This has compelled food manufacturers and processors to invest in certification programs to demonstrate compliance. Furthermore, the rise in international food trade has emphasized the need for standardized certifications to ensure compliance with importing countries' regulations, creating new compliance requirements while driving market growth through mandatory certification requirements.

Expanding cross-border food trade drives multi-standard adoption

The growth in international food trade requires manufacturers to obtain multiple certifications to access different markets. Companies must comply with various regulatory standards, including FDA regulations in the United States, FSSC 22000 in European markets, and CCC certification in China. The World Trade Organization's Sanitary and Phytosanitary Agreement establishes baseline standards for food safety and certification processes across borders. The growth of cross-border food trade and e-commerce has created a regulatory environment where multi-certification approaches are necessary for market access and global expansion. Food companies must adapt to diverse certification standards due to increasing consumer demand for imported products and varying regional food safety regulations. According to WTO data in 2024, international trade accounts for 25% of global food production, with food and agricultural trade valued at USD 2.3 trillion [3]Source: World Trade Organization, “25 Years of SPS Agreement,” wto.org. Multi-certification requirements have become essential for food producers aiming to access global markets. This complex certification landscape is expected to continue shaping international food trade dynamics in the coming years, making it crucial for companies to develop comprehensive certification strategies.

Growing popularity of clean label and transparency movements

The clean label movement is driving significant changes in the food certification market, as consumers increasingly demand products with recognizable ingredients and transparent production processes. This consumer awareness has intensified the need for verified information about product ingredients, sourcing, and manufacturing methods. Food manufacturers are responding by obtaining various certifications, including organic, non-GMO, and clean label certifications, to validate their product claims. The USDA's Strengthening Organic Enforcement rule exemplifies this trend, mandating certification for companies in the organic supply chain and eliminating loopholes that previously allowed non-compliant ingredients. The trend has particularly gained momentum in developed markets like North America and Europe, where consumers actively seek products with minimal processing and natural ingredients. Companies are adapting to these demands, as demonstrated by Little Sesame obtaining clean label certification in September 2024, which verifies products are free from artificial additives, preservatives, and unnecessary chemicals including glyphosate, arsenic, and pesticide residues [4]Source: Eat Little Sesame, “Little Sesame Is Officially Clean Label Certified,” eatlittlesesame.com . This transparency imperative is creating new certification categories and enabling premium pricing for verified clean-label products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of certification and renewal | -1.1% | Global, impacting SMEs in developing markets | Short term (≤ 2 years) |

| Lack of harmonization across certification standards | -0.8% | Global, strongest on cross-border trade | Medium term (2-4 years) |

| Shortage of qualified food auditors slows site approvals | -0.6% | Global, most acute in North America and Europe | Medium term (2-4 years) |

| Fraudulent or misleading certification claims | -0.3% | Global, regions with weak enforcement | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High cost of certification and renewal

The high costs associated with food certification and renewal processes create significant barriers, particularly for small and medium enterprises (SMEs). Organizations must allocate substantial financial resources for initial certification, including application fees, audit expenses, and implementation of required systems. The recurring costs for periodic renewals, surveillance audits, and maintaining compliance with evolving standards further strain company budgets. This challenge is particularly evident in developing markets, where certification fees can represent a disproportionate share of company revenues. For instance, Indonesian micro and small enterprises face multiple obstacles in meeting halal certification requirements, including high costs, lack of process knowledge, and inadequate facilities. Similarly, Malaysian SMEs struggle with certification acquisition due to financial constraints and knowledge gaps. These financial burdens can deter potential market entrants and may force existing certified companies to discontinue their certifications, ultimately constraining market growth.

Shortage of qualified food auditors slows site approvals

The food certification market faces significant operational challenges due to the limited availability of qualified food auditors, creating bottlenecks in certification processes and increasing the risk of foodborne illnesses and regulatory lapses. The shortage of experienced professionals extends the time required for site inspections and approvals, particularly affecting developing regions where certification demand is growing rapidly. The extensive training requirements and increasing complexity of food safety standards make it difficult to expand the qualified auditor pool quickly. This scarcity has led to notable food safety incidents and recalls linked to inadequate oversight. The resulting delays in site approvals increase costs for food manufacturers and potentially affect their market entry timing, highlighting the critical need for more qualified professionals in the industry. The gap between auditor supply and certification demand continues to widen as global food trade expands and regulatory requirements become more stringent. Furthermore, the increasing consumer awareness about food safety and quality has amplified the pressure on certification bodies to maintain thorough inspection processes despite resource constraints. Therefore, addressing the auditor shortage through enhanced training programs and industry partnerships has become crucial for maintaining food safety standards and meeting market demands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Certification Type: Standards Consolidation Drives Market Leadership

ISO 22000/FSSC 22000 certification dominates the market with a 32.10% share in 2025, supported by its Global Food Safety Initiative recognition and implementation across 35,000 organizations worldwide, according to NSF. The certification's prominence is attributed to its comprehensive framework, which integrates ISO 22000:2018 requirements with sector-specific prerequisites. The upcoming FSSC 22000 Version 6, effective April 2024, strengthens this position by introducing enhanced requirements for food safety culture, quality control, and equipment management documentation. BRCGS certification maintains its market strength through its Issue 9 standard, while IFS and GMP+/FSA certifications cater to specialized market segments.

Halal certification emerges as the fastest-growing segment, projecting a 7.52% CAGR through 2031, with Indonesia's mandatory certification law resulting in over 5 million certified products by October 2024. The certification landscape continues to evolve with kosher certification maintaining steady demand in traditional markets, while other certifications, including organic and sustainability standards, experience growth driven by increasing consumer demand for transparency and environmental responsibility. This diversification in certification types reflects the industry's response to evolving consumer preferences and regulatory requirements across global markets.

By Product Type: Protein Products Lead While Specialty Foods Accelerate

Meat, poultry, and seafood products command a dominant 35.62% market share in 2025, driven by complex safety requirements and regulatory oversight. The USDA's proposed Salmonella framework for raw poultry products introduces new adulterant standards, while the National Marine Fisheries Service has revised seafood inspection regulations to enhance program uniformity and reliability. The sector's growth aligns with expanding global trade and evolving consumer preferences for certified products.

The food safety testing market shows significant growth across various segments, with free-from and allergen-free foods projected to grow at 7.48% CAGR through 2031. This growth is supported by regulatory initiatives like the USDA's Allergen Verification Sampling Program, which tests for 14 allergens, including the 'Big 9' and gluten, in ready-to-eat products. The market also sees enhanced oversight in infant foods, exemplified by China's new procedures for priority review of special medical purpose foods and updated infant formula registration guidelines, while segments like beverages, bakery, and confectionery products continue to develop under increasing safety standards.

Geography Analysis

Europe holds the dominant market position with a 33.74% share in 2025, underpinned by the European Food Safety Authority's comprehensive regulatory framework. The region's commitment to consumer protection is evident through the implementation of Regulation 2025/351 on plastic food contact materials, effective March 2025, which establishes stricter purity requirements and migration limits. Additionally, the European Food Safety Authority's updated guidance for novel food applications, effective February 2025, has improved the efficiency of risk assessment processes.

The Asia-Pacific region demonstrates the strongest growth trajectory with a projected CAGR of 7.24% through 2031. This growth is driven by significant regulatory developments, such as India's FSSAI re-operationalized food labeling and display standards implemented in January 2023. These standards have strengthened consumer protection through enhanced labeling requirements for fortified foods, while the adoption of blockchain-based traceability systems further supports regional market expansion.

North America maintains a significant market presence through FDA regulations and USDA oversight. South America's market growth is exemplified by Argentina's food import reforms, which streamline trade processes for countries with high sanitary standards while maintaining safety requirements. The Middle East and Africa region continues to develop through expanded halal certification requirements and enhanced regulatory frameworks, contributing to steady market progression.

Competitive Landscape

The global food certification market demonstrates moderate fragmentation, with a mix of domestic and international players competing for market share. Key industry leaders include Eurofins Scientific SE, Bureau Veritas Group, Intertek Group PLC, SGS S.A., and NSF International. These companies actively pursue mergers and acquisitions to maintain their market dominance and expand their global presence. A recent example is Amtivo Group's acquisition of the United Kingdom's Food Certification Ltd in January 2024, which enhanced their food safety certification capabilities.

Companies are increasingly differentiating themselves through technological innovation and digital solutions. DNV's My Story™ digital product passport exemplifies this trend, enabling transparent sharing of verified sustainability and safety certifications. The integration of artificial intelligence in food authentication processes is improving fraud detection capabilities, offering superior speed and accuracy compared to traditional statistical methods. These technological advancements are reshaping certification processes and creating new opportunities for market growth.

The competitive landscape is significantly influenced by regulatory requirements, with companies making substantial investments to comply with evolving standards such as FSSC 22000 Version 6 and emerging digital certification frameworks. This focus on compliance and standards adherence remains crucial for maintaining market position and ensuring service quality in the food certification industry. Market players that successfully adapt to these regulatory changes often gain competitive advantages and strengthen their industry position.

Food Certification Industry Leaders

Eurofins Scientific SE

Bureau Veritas Group

Intertek Group PLC

SGS S.A.

NSF International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: SGS partnered with The PLEDGE on Food Waste Certification to embed waste-reduction metrics in audited food-service outlets

- December 2024: SGS formed a strategic alliance with HEYTEA, covering laboratory testing and a proprietary tea-health label across 4,300 stores.

- October 2024: Merieux NutriSciences acquired Bureau Veritas’ food testing arm, adding 34 labs in 15 nations.

- May 2024: USB Certification and Standard Group partnered to expand BRCGS schemes within Greater China’s packaged-food sector.

Global Food Certification Market Report Scope

The food certification market is based on an accredited and approved certification body. Control Union Certifications provide third-party certification audits against the main food safety. The report on the food certification market offers key insights into the latest developments. The food certification market is segmented into end-user industry, type, and geography. By end-user industry, the market is segmented into meat, poultry and seafood products, dairy products, infant food, beverages, bakery and confectionery, and other end-user industries. The market is also segmented by type into ISO 22000 - Food Safety Management System, BRCGS., Halal certification, GMP+/FSA, and other certifications. Also, the study provides an analysis of the food certification market in emerging and established markets across the globe, including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

| ISO 22000/FSSC 22000 |

| BRCGS |

| SQF |

| IFS |

| Halal |

| Kosher |

| GMP+/FSA |

| Others |

| Meat, Poultry and Seafood Products |

| Dairy Products |

| Infant Foods |

| Beverages |

| Bakery and Confectionery Products |

| Free-From/Allergen-Free Foods |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Russia | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| Rest of Middle East and Africa |

| By Certification Type | ISO 22000/FSSC 22000 | |

| BRCGS | ||

| SQF | ||

| IFS | ||

| Halal | ||

| Kosher | ||

| GMP+/FSA | ||

| Others | ||

| By Product Type | Meat, Poultry and Seafood Products | |

| Dairy Products | ||

| Infant Foods | ||

| Beverages | ||

| Bakery and Confectionery Products | ||

| Free-From/Allergen-Free Foods | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Russia | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the food certification market?

The food certification market stands at USD 6.75 billion in 2026 and is projected to reach USD 8.72 billion by 2031.

Which certification type holds the largest food certification market share?

ISO 22000/FSSC 22000 leads with 32.10% share as of 2025, owing to its global retailer acceptance.

Why is halal certification growing faster than other segments?

Mandatory halal laws in Indonesia and Gulf states, coupled with rising Muslim consumer spending, are driving a 7.52% CAGR through 2031.

Which region is expanding most rapidly in the food certification market?

Asia-Pacific is forecast to grow at a 7.24% CAGR owing to labeling reforms in India, China’s infant-formula rules, and widespread halal requirements.

Page last updated on: