Market Overview

| Study Period | 2021 - 2031 |

|---|---|

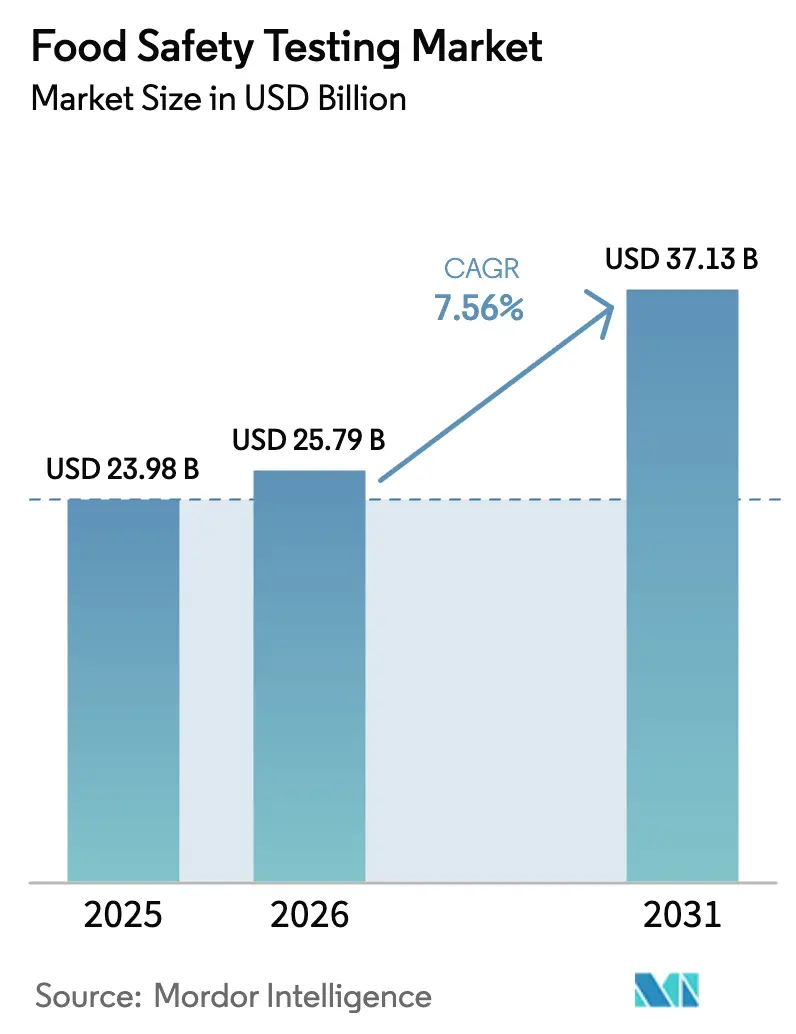

| Market Size (2026) | USD 25.79 Billion |

| Market Size (2031) | USD 37.13 Billion |

| Growth Rate (2026 - 2031) | 7.56% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Food Safety Testing Market Analysis by Mordor Intelligence

The food safety testing market size was USD 23.98 billion in 2025, is valued at USD 25.79 billion in 2026, and is forecast to reach USD 37.13 billion by 2031, rising at a 7.56% CAGR. As regulators worldwide demand real-time digital traceability, same-day molecular diagnostics, and transparent data sharing, the focus is shifting from episodic compliance to predictive risk mitigation. By 2026, the U.S. FDA's "New Era of Smarter Food Safety" blueprint mandates interoperable electronic records for high-risk foods. Meanwhile, Europe's 2025 revision of Regulation (EC) No 178/2002 is tightening retailer liability, leading to more frequent on-site rapid testing. Laboratories are now investing in advanced technologies, including whole-genome sequencing, cloud-based LIMS, and multi-residue LC-MS/MS workflows, enabling them to detect pesticides, mycotoxins, and PFAS in a single run. Concurrently, nations like China, India, and Japan are bolstering advanced testing capacities across the Asia-Pacific by investing in PCR-equipped inspection stations and blockchain pilots.

Key Report Takeaways

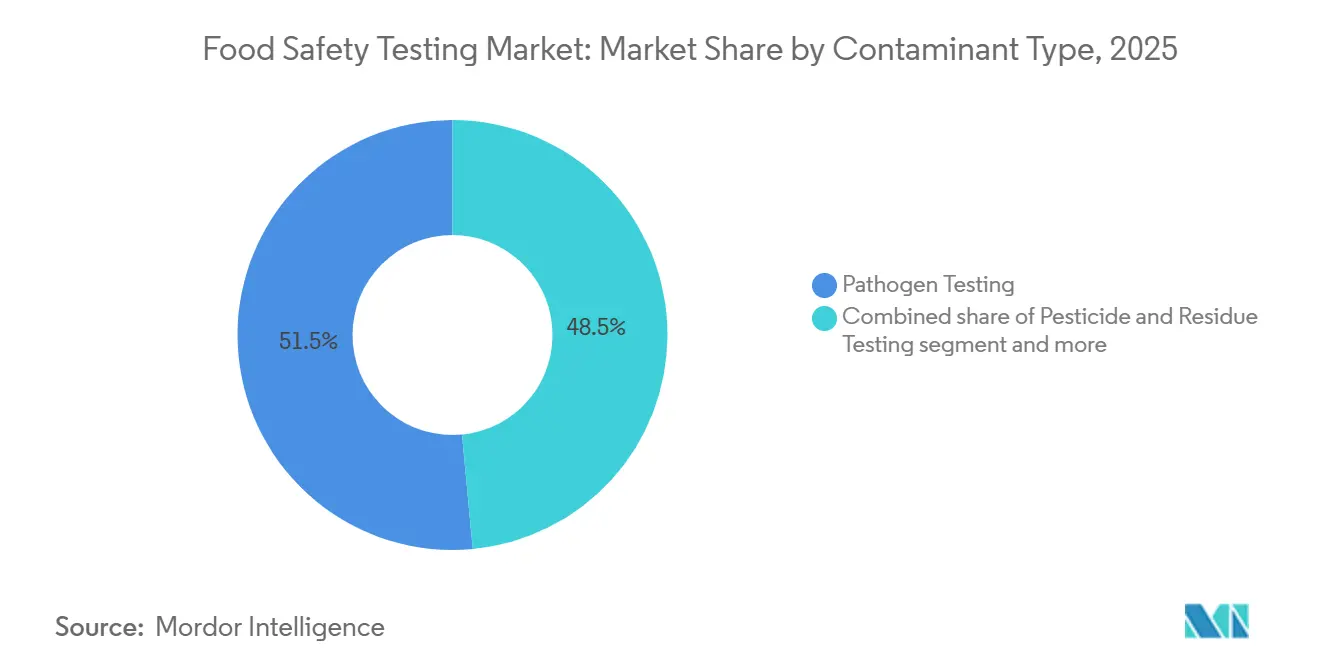

- By contaminant type, pathogen testing led with a 51.50% food safety testing market share in 2025; GMO screening is projected to grow at an 8.35% CAGR through 2031.

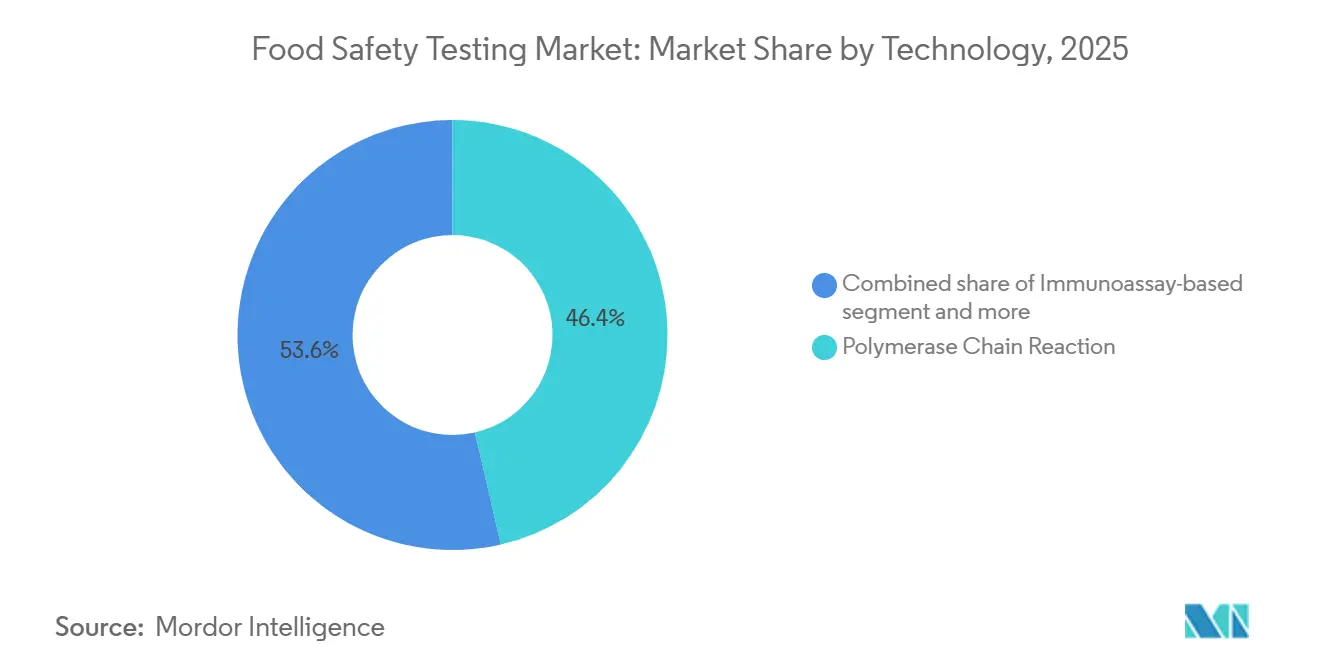

- By technology, PCR platforms captured 46.40% of 2025 revenue, while chromatography and spectrometry are advancing at an 8.53% CAGR to 2031.

- By application, the food segment commanded 83.66% of 2025 revenue; pet food and animal feed are expanding at an 8.13% CAGR through 2031.

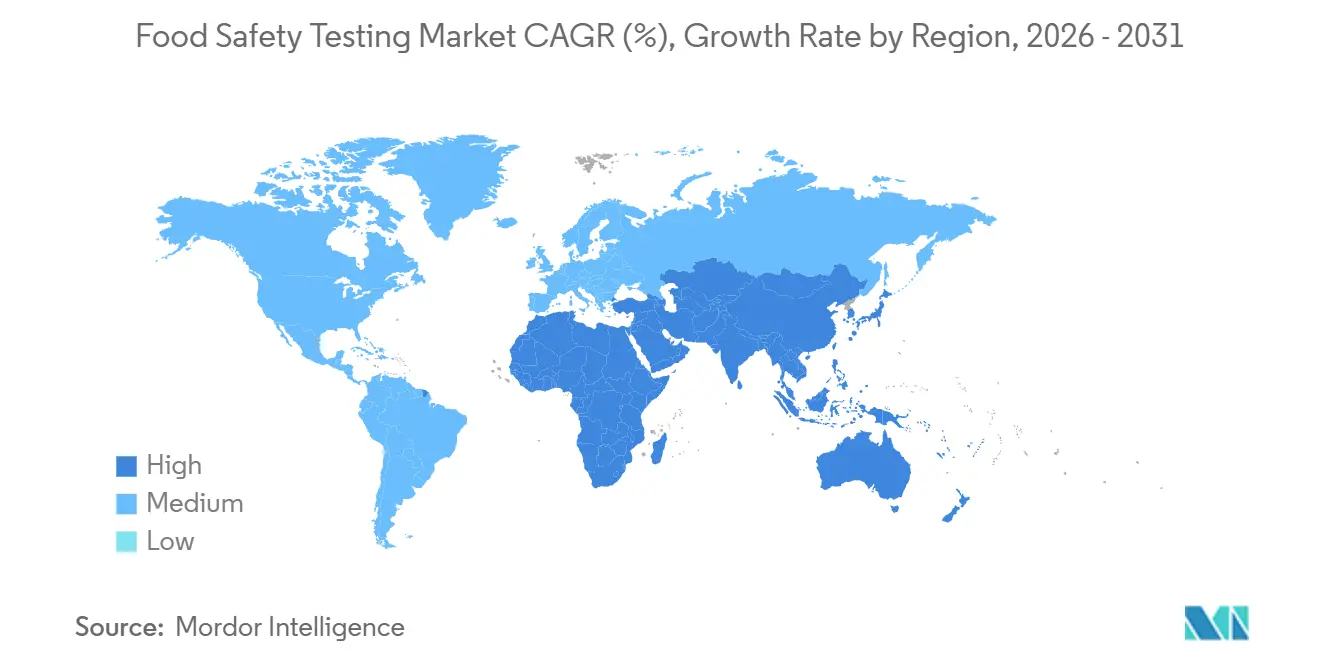

- By geography, North America accounted for 33.91% of the 2025 revenue, whereas the Asia-Pacific region is forecast to register an 8.45% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Food Safety Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent global food-safety regulations and enforcement | +1.8% | North America, Europe | Medium term (2-4 years) |

| Rising food-borne illness incidence and costly recalls | +1.5% | North America, Asia-Pacific | Short term (≤2 years) |

| Expanding cross-border food trade and complex supply chains | +1.2% | Global, strong in Asia-Pacific and Middle East | Long term (≥4 years) |

| Whole-genome sequencing and predictive analytics adoption | +1.4% | North America, Europe | Medium term (2-4 years) |

| Retailer liability clauses driving on-site rapid testing uptake | +1.0% | Europe, North America | Short term (≤2 years) |

| Cold-chain-resilient pathogen variants requiring high-sensitivity tests | +0.9% | Tropical and subtropical regions | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Stringent global food-safety regulations and enforcement

Global regulatory frameworks are becoming increasingly stringent, driving the demand for advanced and frequent food testing solutions across the food safety testing market. The FDA's Human Foods Program (HFP), launched in October 2024, has outlined strategic priorities for fiscal year 2025, focusing on microbiological food safety, chemical safety, and nutrition.[1]Source: U.S. Food and Drug Administration, "Human Food Program (HFP) FY 2025 Priority Deliverables", fda.gov Governments are shifting from periodic audits to continuous digital monitoring. Under FSMA Section 204, U.S. suppliers of leafy greens, nut butters, and finfish are now required to electronically record lot-level PCR results, effectively mandating testing at every stage. This regulation ensures traceability and enhances food safety by identifying contamination risks early in the supply chain. In 2025, the European Food Safety Authority tightened its standards, reducing the Listeria monocytogenes threshold in ready-to-eat foods from 100 CFU/g to 10 CFU/g, which spurred a surge in demand for high-sensitivity PCR assays. This change reflects the growing emphasis on minimizing health risks associated with foodborne pathogens. That same year, India mandated third-party testing for packaged foods in modern retail, hastening the push for ISO/IEC 17025 accreditation. This move aims to standardize testing protocols and improve consumer trust in food quality. These regulations now require a turnaround time of 24 hours or less, leading laboratories to automate sample preparation and implement cloud-based LIMS. The adoption of these technologies not only improves efficiency but also ensures compliance with stringent timelines. Overall, these stringent regulations are providing a significant boost to the food safety testing market.

Rising food-borne illness incidence and costly recalls

In 2025, the U.S. CDC reported more than a thousand outbreaks. Salmonella and E. coli were responsible for the majority of these cases. These outbreaks highlight the growing public health and economic challenges posed by foodborne pathogens. A 2025 report from the U.S. Government Accountability Office (GAO) highlighted the urgency, estimating the annual economic toll of foodborne illnesses on the United States at around USD 75 billion, factoring in medical costs, lost productivity, and premature deaths[3]Source: U.S. Government Accountability Office, "Food Safety: Status of Foodborne Illness in the U.S.", gao.gov. A significant dairy recall in Europe that year further emphasized the financial stakes, with costs amounting to EUR 180 million. In response, retailers have begun incorporating indemnity clauses into their contracts, effectively shifting recall responsibilities upstream to suppliers and manufacturers. This shift underscores the growing importance of pathogen screening before shipment to mitigate risks. A 2025 report from WHO highlighted that while low- and middle-income countries grapple with a disproportionate disease burden, they often lack the necessary testing capacities to address these challenges effectively. Consequently, multinational exporters are increasingly investing in third-party validations and certifications to ensure compliance with global safety standards, thereby protecting their global brands, maintaining consumer trust, and safeguarding profit margins.

Expanding cross-border food trade and complex supply chains

In 2025, the food trade reached an impressive USD 1.9 trillion, with developing economies contributing 42% to the exports. Multi-ingredient products, often sourced from 15 different countries, face significant traceability challenges due to complex supply chains and varying regulatory standards across nations. The 2025 National Trade Estimate Report by the United States Trade Representative underscores the hurdles posed by food safety regulations and technical trade barriers in global food commerce[2]Source: United States Trade Representative, "2025 National Trade Estimate Report on Foreign Trade Barriers of the President of the United States on the Trade Agreements Program", ustr.gov. While the African Continental Free Trade Area strives for standard harmonization to simplify trade, its inconsistent implementation forces importers to conduct independent tests on African shipments, adding both time and cost. China's Belt and Road initiatives heighten cold-chain vulnerabilities in Central Asia. Here, inadequate infrastructure and extreme weather elevate spoilage risks, leading to a spike in demand for portable PCR tests at border crossings to ensure food safety. Blockchain initiatives, such as Walmart's food ledger, are transforming recall processes. By linking pathogen certificates to each batch, these advanced systems cut trace-back times from days to mere seconds, bolstering transparency and efficiency in food safety management.

Whole-genome sequencing and predictive analytics adoption

In 2025, GenomeTrakr processed over 500,000 isolates, achieving 24-hour outbreak source matching, which significantly enhanced the speed and accuracy of foodborne illness investigations. Sequencing costs dropped to USD 50 per bacterial genome, making routine surveillance more accessible and practical for a wider range of laboratories beyond just elite facilities. Predictive AI, by overlaying WGS data with environmental sensors, demonstrated its potential in proactive food safety measures; an ECDC pilot accurately forecasted Salmonella hotspots in poultry facilities with an 82% success rate, showcasing its utility in preventing outbreaks. Despite ongoing hesitancy in data-sharing due to concerns over privacy and competition, vertically integrated firms gained an analytics advantage by leveraging proprietary data. Nevertheless, the widespread adoption of WGS is consistently elevating standards and driving innovation in the food safety testing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital costs for advanced test equipment and labs | -0.8% | Emerging markets, SME labs | Medium term (2-4 years) |

| Shortage of trained food-microbiology professionals | -0.6% | North America, Europe | Long term (≥4 years) |

| Cyber-security and data-privacy risks in cloud-based LIMS | -0.4% | Global, strictest in Europe and United States | Short term (≤2 years) |

| Climate-driven emergence of novel contaminants complicating validations | -0.5% | Tropical and subtropical regions | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High capital costs for advanced test equipment and labs

LC-MS/MS systems and high-throughput PCR platforms come with a price tag of USD 150,000-500,000, and users can expect to pay an additional 10-15% annually for service contracts. An ILAC survey revealed that 62% of laboratories in sub-Saharan Africa and South Asia identify equipment costs as the primary hurdle to achieving ISO/IEC 17025 accreditation. While leasing and pay-per-test subscriptions offer a more accessible entry point, Eurofins introduced a sequencing subscription in 2025, allowing costs to be distributed over monthly payments. However, method validation remains a lengthy process, taking 6-12 months and costing between USD 50,000-100,000 in consumables, which in turn delays technology refresh cycles. As a result, the capital-intensive nature of these systems constrains expansion efforts in regions sensitive to pricing.

Shortage of trained food-microbiology professionals

In 2025, U.S. labs grappled with a 23% vacancy rate for molecular diagnostics microbiologists, as clinical sectors outbid food testing for talent due to higher salaries and better career growth opportunities. Europe faces a shortfall of 8,000 professionals by 2028, driven by declining interest in food-microbiology careers, as university enrollment in related programs has plummeted by 14% from 2020 to 2024. While automation offers some relief, evidenced by Thermo Fisher’s SureTect cartridges reducing onboarding time from 12 weeks to just two weeks, interpreting WGS trees still requires graduate-level expertise, which remains a bottleneck. These skill shortages not only delay result validation and compliance reporting but also strain lab capacity, impacting the overall efficiency of operations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Contaminant Type: Pathogen Testing Dominates, GMO Screening Accelerates

In 2025, pathogen assays led the food safety testing market, accounting for 51.50% of total revenue. This dominance stemmed from mandatory checks for Salmonella, Listeria, and E. coli across meat, dairy, and fresh-produce supply chains. The segment's growth is bolstered by regulators tightening microbial thresholds and retailers demanding same-day certificates to ensure compliance with food safety standards. Laboratories are streamlining operations, automating enrichment and PCR processes, and reducing turnaround times from two days to a mere eight hours. These advancements not only enhance efficiency but also help businesses meet the increasing demand for rapid and reliable testing. Consequently, the pathogen detection market is set for consistent growth, driven by these stringent compliance requirements and the need for robust food safety measures.

While GMO screening occupies a smaller niche, it boasts the fastest growth rate, with an anticipated 8.35% CAGR through 2031. This surge is largely attributed to EU importers enforcing a strict 0.9% labeling threshold and Asia-Pacific exporters eyeing the premium European grocery market, where compliance with stringent regulations is critical for market entry. Varied global regulations on gene-editing technologies keep the demand for multiplex PCR kits high, as they can identify both approved and unintended genetic events, ensuring adherence to diverse regulatory frameworks. Additionally, while second-tier segments like pesticide residue testing are evolving, utilizing LC-MS/MS suites to cover over 700 compounds thanks to Codex limit reductions, mycotoxin screenings see a spike during cereal droughts, which increase the risk of contamination. Allergen verifications are broadening, especially with new mandates for sesame and mustard in Canada and Australia, reflecting the growing emphasis on consumer safety. Furthermore, testing for heavy metals and veterinary drug residues ensures steady revenue from seafood and livestock export certifications, offering a buffer against policy fluctuations and supporting the global trade of safe and compliant food products.

By Technology: PCR Leads, Chromatography Gains on Multi-Residue Demand

In 2025, PCR platforms captured 46.40% of the food safety testing market revenue, driven by their superior detection thresholds, specificity, and adaptability to various pathogens and GMOs. These platforms are highly efficient in identifying contaminants at sub-cycle levels, ensuring accuracy and reliability in results. Mid-range real-time instruments, now priced below USD 40,000, have become accessible, allowing regional labs to widely embrace molecular diagnostics. With automation advancements, labs now achieve a 4-hour sample-to-answer turnaround, cutting labor costs by 30% and significantly improving operational efficiency. This stronghold underscores PCR's pivotal role in swift, dependable testing, especially with tightening regulatory demands aimed at ensuring food safety and compliance.

Chromatography and spectrometry are on the rise, boasting an 8.53% CAGR, with LC-MS/MS leading as the preferred choice for screening multiple pesticide residues and mycotoxins. These technologies provide unmatched sensitivity and precision, making them indispensable for detecting contaminants in complex food matrices. Agilent’s 6495D triple-quadrupole system, capable of detecting PFAS at parts-per-trillion levels, aligns with the new compliance standards in the U.S. and Europe, addressing growing concerns over chemical contaminants. For field applications, immunoassays and lateral-flow devices remain popular, providing portability and ease of use at a cost of USD 5-15 per sample, catering to smallholders and budget-limited labs. Meanwhile, cutting-edge technologies like biosensors, next-gen sequencing, and CRISPR diagnostics are securing regulatory nods in Europe. These innovations promise to revolutionize the market by potentially reducing reagent costs to or below PCR levels within five years, despite some validation hurdles. Their adoption could further enhance testing efficiency and affordability, meeting the evolving needs of the food safety testing landscape.

By Application: Food Anchors Revenue, Pet Food Surges

In 2025, food applications dominated the revenue landscape, accounting for a significant 83.66%. Leading the charge were sectors like meat and poultry, dairy, fresh produce, and processed foods. The meat and poultry segment commands a notable share of the food safety testing market, driven by USDA FSIS's daily mandates for Salmonella and E. coli screenings on ground products. This ensures compliance with stringent safety standards and minimizes the risk of foodborne illnesses. Meanwhile, dairy processors are not only testing for pathogens but are also layering in antibiotic residue tests, ensuring compliance with EU's veterinary drug limits. These measures reflect the growing emphasis on quality assurance and regulatory adherence in the dairy sector. Recent Cyclospora outbreaks linked to imported berries have heightened testing demands for fruit exporters, as they aim to safeguard consumer health and maintain export standards. Additionally, multi-line snack facilities are increasingly adopting allergen verification programs to cater to the rising prevalence of food allergies and ensure product safety for sensitive consumers.

While pet food and animal feed represent a smaller segment, they're witnessing a robust growth at an 8.13% CAGR. This surge is largely driven by premium brands pursuing pathogen-free certifications and pet owners seeking human-grade assurances, reflecting a shift in consumer preferences toward higher-quality pet products. With the FDA's Animal Feed Regulatory Program Standards coming into full effect in 2024, manufacturers are now mandated to conduct weekly Salmonella PCR tests on both raw inputs and finished treats. This regulatory push ensures consistent safety standards across the supply chain. Furthermore, livestock feed mills are intensifying mycotoxin testing to safeguard conversion ratios, leading to a consistent demand for aflatoxin and DON assays. These testing measures are critical for maintaining livestock health and optimizing feed efficiency. This growth trajectory not only diversifies suppliers' revenue streams but also mitigates their reliance on more mature food testing categories, enabling them to tap into emerging opportunities within the pet food and animal feed market.

Geography Analysis

In 2025, North America accounted for 33.91% of global revenue, bolstered by FSMA enforcement and a USD 300 million USDA initiative funding advanced PCR and LC-MS/MS systems. The Food Safety Modernization Act (FSMA) has driven significant investments in food safety technologies, ensuring compliance with stringent regulations. Canada’s push for digital traceability in meat, seafood, and dairy is accelerating the adoption of cloud-based LIMS, enabling better tracking and quality assurance across the supply chain. Meanwhile, Mexico's expansion of accredited labs aims to enhance fresh-produce exports by meeting international safety standards and boosting competitiveness in global markets. While growth persists, it's tempered as installed capacities mature and consolidation curtails price competition, leading to a more stabilized market environment.

Asia-Pacific is poised for an 8.45% CAGR through 2031. In 2025, China introduced 1,200 new inspection stations, transitioning from culture methods to PCR, which significantly improved the speed and accuracy of pathogen detection. Concurrently, India mandated quarterly pathogen audits for dairy cooperatives targeting export markets, ensuring compliance with international safety standards and enhancing the reputation of Indian dairy products globally. Japan's blockchain-driven traceability trials for imported seafood, which mitigate recall risks by providing end-to-end visibility, are now being emulated by South Korea and Singapore, showcasing the region's focus on leveraging technology for food safety. In China, local instrument manufacturers are gaining traction by offering PCR systems at half the price of their Western counterparts, creating a competitive landscape and increasing accessibility to advanced testing solutions. Additionally, mergers, like SGS's lab acquisitions in 2025, are hastening scale in India, enabling better service coverage and operational efficiency. Southeast Asia's enhancements to cold-chain infrastructure are driving a surge in demand for portable rapid tests at border checkpoints, ensuring the quality and safety of perishable goods during transit.

Europe's adherence to stringent EFSA standards is pushing retailers to take on upstream liabilities, leading to a rise in on-site rapid testing at logistics hubs to ensure compliance and minimize risks. The post-Brexit landscape sees U.K. exporters navigating dual testing requirements, a challenge turned advantage for multi-jurisdictional entities like Eurofins and Intertek, which are well-positioned to offer comprehensive testing solutions. Eastern European nations are channeling EU cohesion funds to modernize laboratories, with notable capacity expansions in Poland and the Czech Republic, enhancing their ability to meet growing demand for food safety testing. In South America, labs focusing on pesticide residues and mycotoxins are scaling up to bolster Brazil's soy and beef exports, ensuring compliance with international standards and strengthening their position in global markets. The Middle East is establishing centralized hubs, highlighted by Dubai Municipality's 40% expansion of LC-MS/MS capacity in 2025, which enhances the region's ability to conduct high-throughput testing and support its growing food trade. Africa's growth story is mixed; while South Africa's citrus export checks fuel demand for advanced testing solutions, Nigeria and Egypt remain reliant on externally funded initiatives, limiting their ability to independently scale food safety infrastructure.

Regulatory Landscape

Food safety testing demand is being shaped by regulators and standards bodies moving toward faster verification, stronger traceability, and broader chemical-risk oversight. In the United States, the FDA Human Foods Program (HFP), launched in October 2024, set out 2026 priority deliverables that include reforms to the GRAS framework, raising the compliance bar for ingredient safety substantiation alongside traditional pathogen controls. Separately, the USDA FSIS announced new scientific capacity moves in April 2026, including the establishment of a National Food Safety Center in Urbandale, Iowa, and expanded capabilities at the new Science Center in Athens, Georgia, reinforcing government laboratory capacity that supports enforcement and method adoption.

In Europe, the EU advanced harmonization of laboratory practices through Commission Implementing Regulation (EU) 2026/765 (enacted April 1, 2026), which sets updated methods for sampling, analysis, and interpretation of pesticide residues in food and feed (with application starting January 1, 2027). Internationally, Codex Alimentarius Commission outcomes at its 49th Session in July 2026, including guidance on precautionary allergen labeling and emergency labeling provisions, provide a reference point that many national regulators and import programs translate into testing and documentation requirements, particularly for allergen and labeling verification.

Value Chain Analysis

The value chain for food safety testing spans method and reagent developers, instrument suppliers (PCR and LC-MS/MS platforms), sample-collection logistics, laboratory operators (central labs and mobile/on-site units), data systems (LIMS and traceability platforms), and end users across food, pet food, and animal feed. Regulatory method-setting is increasingly a direct upstream input to lab workflows, illustrated by the EU adoption of Commission Implementing Regulation (EU) 2026/765 in April 2026 for pesticide-residue sampling and analysis. This requires laboratories to align SOPs, QA controls, and reporting formats ahead of the January 1, 2027 application date. On the demand side, export and import programs tie market access to recognized lab capability and accreditation (for example, ISO/IEC 17025), making turnaround time, chain-of-custody, and defensible interpretive criteria core service differentiators.

Bottlenecks in customs and border settings also show where testing capacity and regulatory transitions are out of sync. In early 2026, Vietnam faced severe port and border congestion after new inspection procedures outpaced available testing capacity. The government responded with Resolution No.09/2026/NQ-CP on February 4, 2026, temporarily suspending Decree 46 and adjusting the timeline until April 15, 2026. Disruptions like this shift work toward third-party labs and increase testing at logistics nodes, while extended timelines elsewhere (for example, the US FDA Food Traceability Rule compliance date extended by 30 months to July 2028) give supply-chain participants more time to integrate testing results with electronic traceability records and data-sharing processes.

Competitive Landscape

The food safety testing market exhibits moderate concentration. In 2025, Eurofins Scientific bolstered its global presence by adding 12 regional labs and acquiring FoodChain ID’s European network in November, solidifying its leadership with over 900 facilities worldwide. This expansion has enabled Eurofins to cater to a broader client base and enhance its service offerings, further strengthening its competitive position. SGS SA, blending geographic reach with digital innovation, rolled out a blockchain traceability platform in collaboration with IBM, debuting with industry giants Nestlé and Unilever. This platform enhances transparency and traceability across the supply chain, addressing growing consumer demand for food safety and quality assurance. Bureau Veritas and Intertek are enhancing their regional footprints through strategic acquisitions, highlighted by Bureau Veritas’s takeover of Fera Science’s U.K. division and Intertek’s USD 22 million expansion in Shanghai. These moves aim to improve service accessibility and meet the rising demand for food safety testing in key markets.

Technology disruptors are heightening competition. Neogen unveiled a battery-powered PCR system in January 2026 that delivers Listeria results in 90 minutes, with wireless data uploads, targeting on-site meat plants. This innovation addresses the need for rapid and reliable testing solutions in the meat processing industry, where timely detection of pathogens is critical. Mérieux NutriSciences is capitalizing on environmental monitoring, introducing a subscription model that pairs quarterly swabbing with WGS, generating USD 18 million in its inaugural year. This model not only generates recurring revenue but also provides clients with a proactive approach to food safety management. Meanwhile, Agilent and Thermo Fisher are fortifying their positions by vertically integrating, offering bundled solutions of instruments, reagents, and data software to safeguard their profit margins. This strategy ensures a seamless experience for customers while maintaining cost efficiency and operational control.

Patent filings from 2024-2025 reveal a clear trend in research and development investments: 42% centered on rapid molecular diagnostics, 28% on multi-residue methods, and 18% on blockchain traceability. These trends highlight the industry's focus on advancing testing technologies to meet evolving regulatory standards and consumer expectations. ISO/IEC 17025 accreditation, a significant market entry barrier in emerging economies, demands an investment of USD 50,000-150,000 and a commitment of 12-18 months to achieve. This accreditation ensures the reliability and accuracy of testing laboratories, making it a critical factor for companies aiming to establish credibility and trust in the market.

Food Safety Testing Industry Leaders

-

SGS Group

-

Eurofins Scientific SE

-

Bureau Veritas Group

-

Intertek Group Plc

-

ALS Global

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity sits at the intersection of faster microbiological decision-making and digital workflow integration, as regulators and customers push for shorter time-to-release and stronger documentation. The FDA Human Foods Program 2026 priority deliverables, including GRAS system reform initiatives, expand the need for defensible chemical-safety dossiers and associated analytical verification, supporting demand for multi-residue LC-MS/MS and modern data systems that can link results to ingredients, lots, and suppliers. In parallel, technology upgrades that remove enrichment steps or add higher-resolution characterization strengthen use cases in environmental monitoring and root-cause analysis; for example, Neogen received AOAC Performance Tested Methods certification in April 2026 for its Listeria Right Now rapid environmental monitoring test, and bioMerieyux introduced GENE-UP TYPER SLM in June 2026 to support faster Salmonella strain characterization.

Capacity build-outs and regional hubs also create whitespace, especially where trade growth collides with limited accredited lab infrastructure. AmSpec’s February 2026 opening of a new laboratory in Dubai Science Park with LC-MS/MS, ICP-MS, and RT-PCR expands third-party capacity in a logistics-heavy corridor that serves food imports and re-exports. Kersia’s May 2026 Centre for Food Safety Excellence in Seneffe, Belgium adds an R&D and training anchor that can accelerate hygiene validation and implementation in industrial settings. At the same time, GAO findings on persistent gaps in meeting mandated inspection targets point to sustained demand for scalable private-sector testing and documentation services that can support domestic compliance and cross-border shipments when regulator capacity is constrained.

Recent Industry Developments

- June 2026: bioMerieyux launched GENE-UP TYPER SLM, a real-time PCR solution for rapid Salmonella strain characterization and root-cause analysis support. The addition of strain-level insights strengthens outbreak investigations and supplier corrective actions beyond presence-absence screening. It also raises the value of molecular platforms for manufacturers seeking faster, more actionable results across multi-site operations.

- April 2026: SGS launched a new laboratory in Antananarivo, Madagascar, offering food microbiology and water testing services. The local footprint supports exporters and importers that need internationally aligned testing without routing samples to distant regional hubs. It also expands SGS’s ability to serve emerging-market supply chains where border and port clearance can depend on timely lab certificates.

- October 2024: SGS North America expanded its testing capabilities for food safety and quality assurance across the North American food, pet food, and nutraceutical markets. The move increased service breadth for customers facing tighter pathogen, residue, and labeling requirements across categories. It also reinforced TIC providers’ role as outsourced capacity for brands managing recall risk and retailer documentation demands.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the food safety testing market covers revenues earned from analytical testing services used to detect biological, chemical, or physical hazards in food, beverages, pet food, and feed before products are released to the market.

Scope exclusions: equipment and instrument sales, routine in-process factory checks, and water or environmental monitoring that sits outside the food production line are not counted.

Segmentation Overview

-

By Contaminant Type

- Pathogen Testing

- Pesticide and Residue Testing

- Mycotoxin Testing

- GMO Testing

- Allergen Testing

- Other Contaminant Testing

-

By Technology

- Polymerase Chain Reaction

- Immunoassay-based

- Chromatography and Spectrometry

- Others

-

By Application

- Pet Food and Animal Feed

-

Food

- Meat and Poultry

- Dairy

- Fruits and Vegetables

- Processed Food

- Crops

- Other Foods

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Netherlands

- Poland

- Belgium

- Sweden

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to set the market boundary and to build initial demand and supply signals that a junior analyst can recheck. Public sources such as the US FDA, USDA, CDC, EFSA, and Codex Alimentarius were reviewed to understand testing requirements, common hazards, and how often official alerts and recalls occur.

We also reviewed customs and inspection releases where relevant, along with peer-reviewed food science journals for typical contaminant prevalence and accepted methods. For commercialization signals, we used company annual reports and investor presentations, association websites, and reputable press coverage on lab expansions and new method adoption. In a few places, paid subscriptions for company financials and patent databases were used to speed up revenue mapping and technology trend checks. These examples are illustrative only, and many other public sources were also consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on lab leaders, quality and food safety heads at manufacturers, and procurement and compliance teams across major regions, so assumptions from desk research could be confirmed or adjusted. The conversations were used to validate testing frequency, the outsourcing share, typical turnaround needs, and how pricing shifts with method choice and accreditation requirements. Inputs were then triangulated across food categories and contaminant priorities to keep the model consistent across regions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 13% | APAC: 53% |

| Mid tier: 57% | Functional/Unit leaders: 36% | EMEA: 29% |

| Smaller Players: 14% | Managers: 51% | Americas: 18% |

Market-Sizing & Forecasting

Sizing started with a top-down build that reconstructs the demand pool using food production and trade flows, recall and alert intensity, and regulated testing requirements by product category. Those demand signals were converted into test volumes using practical frequency assumptions shared by experts, and then translated into value using service pricing by method and panel (for example pathogen, allergen, pesticide residues, mycotoxins, and GMO), before results are rolled up to the global total.

Selective bottom-up checks were then used to keep totals realistic, including roll-ups from a sample of testing service revenues, capacity and utilization discussions with labs, and channel checks on common price bands for rapid methods versus lab-based confirmation. Where disclosures were incomplete, gaps were handled by applying region-specific utilization ranges and mix assumptions that were rechecked with interviews.

Forecasts were produced using scenario analysis supported by short trend fits on a few key drivers, including packaged food output, cross-border food trade, method shift toward faster molecular testing, and the pace of new safety rules and enforcement. A base case was finalized after expert feedback on how quickly testing frequency and outsourcing are likely to change.

Data Validation & Update Cycle

Results were validated through triangulation across independent signals, so implied test volume, average pricing, and regional mix stayed within believable ranges. Large variances are flagged, and then rechecked against the underlying inputs, followed by an internal review pass where assumptions and calculations are replicated before sign off.

The model is refreshed each year, and interim checks are triggered when material events occur, such as major outbreaks, new enforcement actions, or large lab capacity additions. Before delivery, a final update pass is completed so clients receive the most current view based on the latest public releases and expert feedback.

Mordor Intelligence's Food Safety Testing Market Estimate Compared With Other Published Estimates

Published values for food safety testing often vary because each publisher draws the line differently on what is counted, and because price and volume assumptions can be refreshed at different times. Differences also show up when one estimate leans heavily on a single region or a single food category, which can shift the total even if the growth story sounds similar.

In this study, the biggest gap driver is usually whether revenues are counted only for testing services on finished food, beverage, pet food, and feed before release, or whether adjacent items like equipment sales and broader environmental monitoring are also blended in. Other spreads come from how testing frequency is assumed during normal periods versus outbreak periods, how method mix is priced as rapid tools expand, and whether currency conversion is taken at an annual average or at a point in time, which can move a global total noticeably, a scope choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 23.98 B (2025) | |

| Global Consultancy A | USD 26.27 B (2025) | This figure appears to use a wider counted universe, where some spend tied to broader compliance programs and a more aggressive method mix uplift can inflate the service value captured in the same year. |

| Industry Publisher B | USD 25.40 B (2025) | This estimate looks closer in level, but it likely applies a different base year alignment and refresh timing for pricing, which can shift the 2025 number when rapid testing adoption is assumed to rise faster. |

Across the three numbers, the spread is explained less by demand direction and more by what is included and how price and mix are updated. By keeping the count tied to finished product testing services and by rechecking frequency and pricing assumptions with field inputs, the final total stays traceable to clear drivers and repeatable steps.

Key Questions Answered in the Report

What is the current value of the food safety testing market?

The market is worth USD 25.79 billion in 2026 and is projected to hit USD 37.13 billion by 2031.

Which contaminant type generates the largest revenue?

In 2025, pathogen testing delivered 51.50% of total revenue, reflecting strict Salmonella, Listeria, and E. coli mandates.

Which technology segment is growing fastest?

Chromatography and spectrometry are advancing at an 8.53% CAGR as labs adopt multi-residue LC-MS/MS for pesticides and PFAS.

Why is Asia-Pacific the fastest-growing region?

Government investment in inspection stations, mandatory quarterly audits, and blockchain traceability pilots drive an 8.45% CAGR through 2031.

Page last updated on: