3D Food Printing Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.17 Billion |

| Market Size (2031) | USD 4.62 Billion |

| Growth Rate (2026 - 2031) | 15.61% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

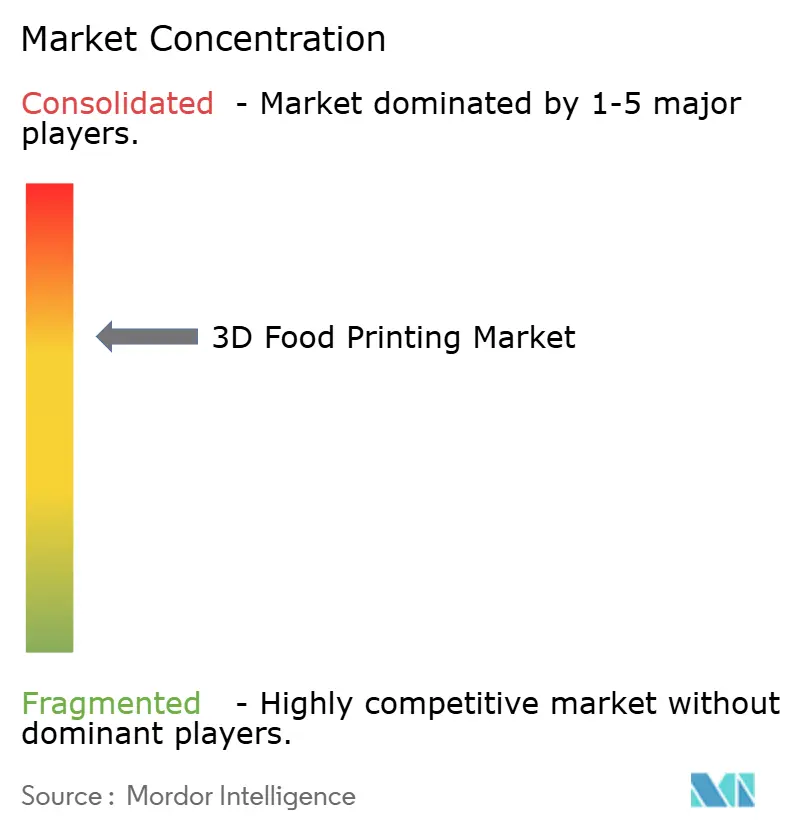

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

3D Food Printing Market Analysis by Mordor Intelligence

The 3D food printing market size is valued at USD 1.17 billion in 2026, growing from the 2025 value of USD 1.05 billion, and is forecast to climb to USD 4.62 billion by 2031, advancing at a 15.61% CAGR. The strong growth trajectory reflects regulatory breakthroughs, deeper venture capital participation, and broader use cases that are moving the technology from pilot kitchens into mainstream commercial settings. Rising demand for personalized nutrition, proven ability to reduce food waste through precise portioning, and institutional support for alternative proteins underpin sustained revenue expansion. At the same time, equipment makers and ingredient suppliers are adopting recurring-revenue models, which improve visibility for investors and speed up product iteration. North American players continue to benefit from early regulatory clarity, yet Asia-Pacific nations are closing the gap thanks to government-backed research and development consortia and streamlined approval pathways.

Key Report Takeaways

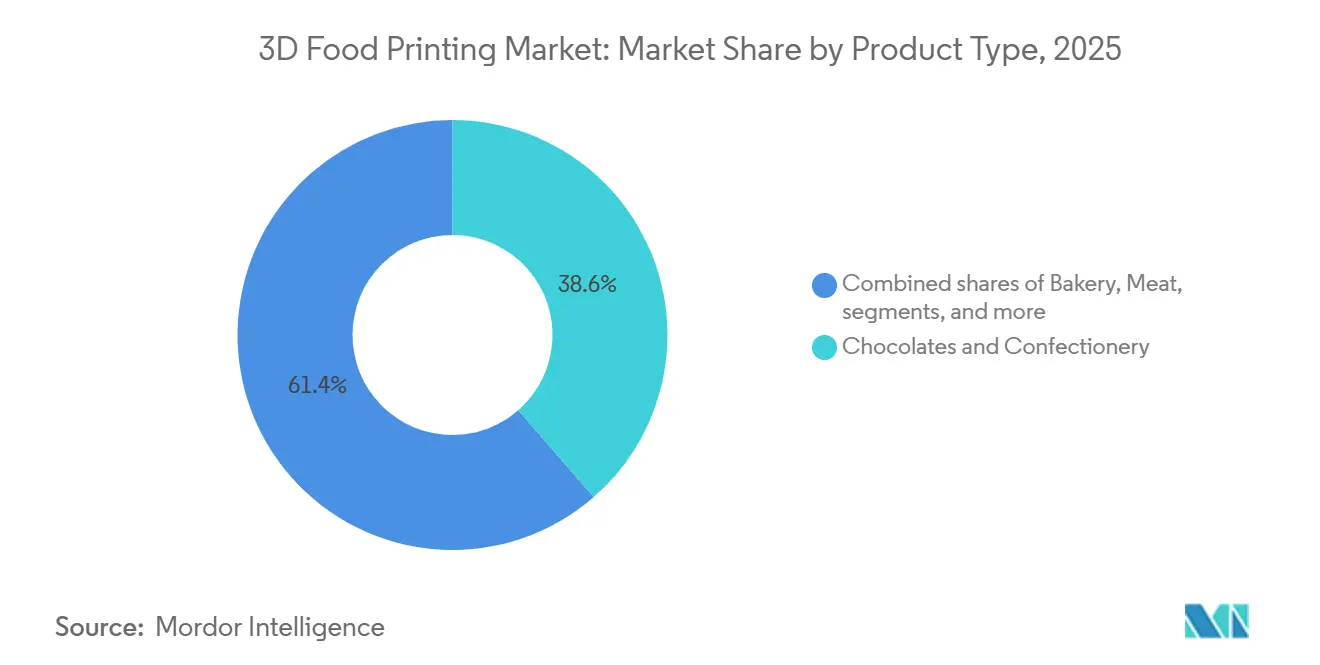

- By product type, chocolates and confectionery held 38.58% of the 3D food printing market share in 2025, while meat and seafood are projected to expand at an 18.02% CAGR to 2031.

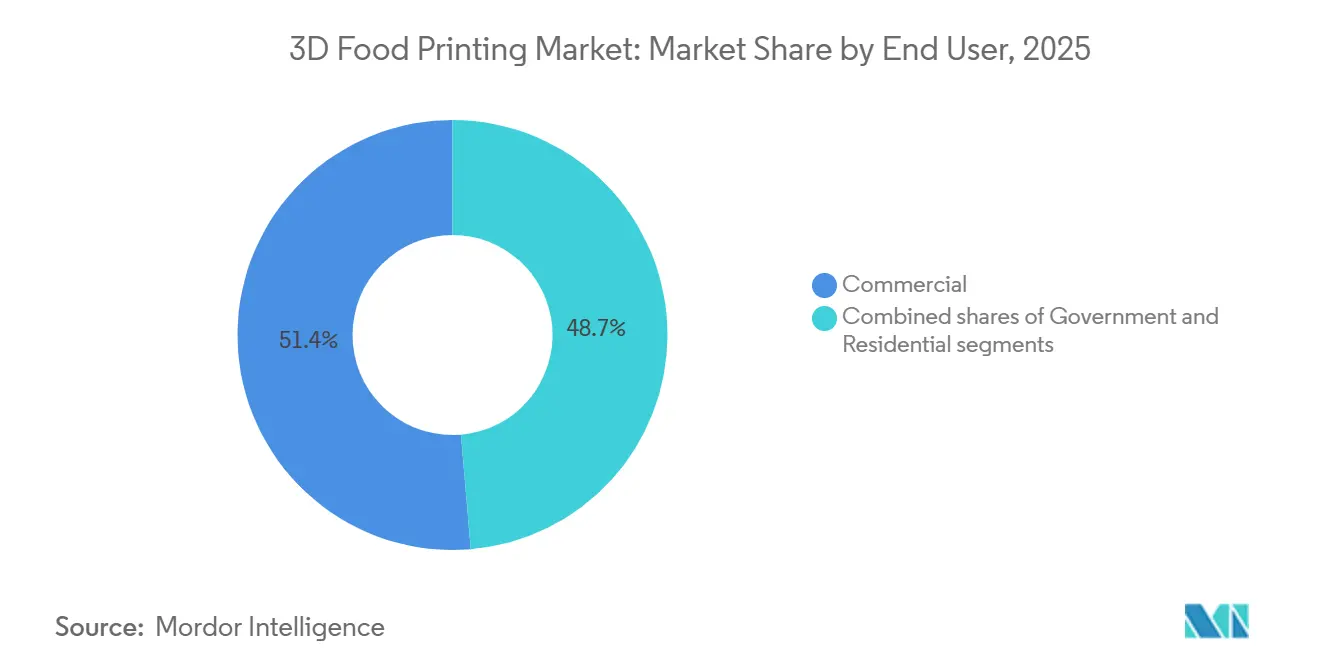

- By end user, commercial operators captured 51.35% of revenue in 2025, whereas the residential segment is projected to rise at a 17.23% CAGR through 2031.

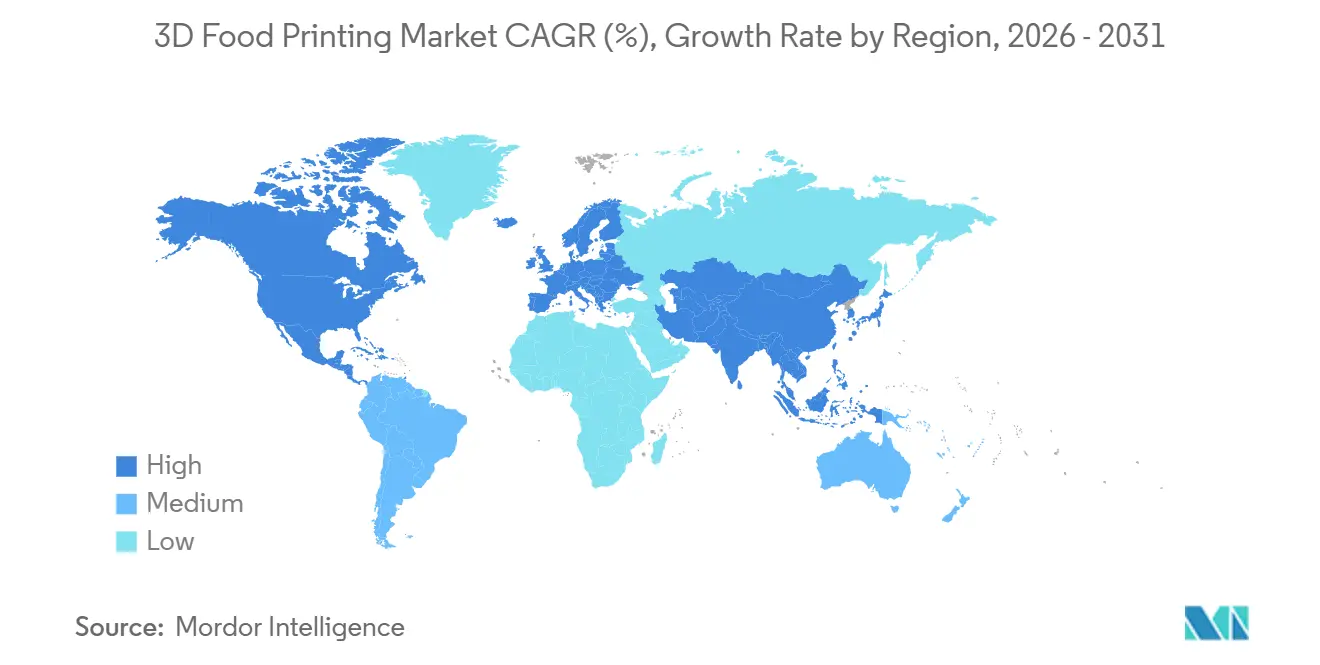

- By geography, North America controlled 41.12% of sales in 2025, yet Asia-Pacific is positioned to post a 17.85% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global 3D Food Printing Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Personalized Nutrition and Customized Foods | +3.2% | Global, with early gains in North America, Western Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Food Waste Reduction Through Precise Portioning and On-Demand Production | +2.1% | Global, particularly Europe (sustainability mandates) and Japan (resource efficiency culture) | Long term (≥ 4 years) |

| Innovations in Bio-Printing for Meat, Seafood, and Nutrient-Rich Products | +4.5% | North America, Israel, Singapore, and select EU markets with regulatory clarity | Medium term (2-4 years) |

| Busy Lifestyles Drive Need for Quick, Indulgent Snacks | +1.8% | North America, Western Europe, and affluent Asia-Pacific metros | Short term (≤ 2 years) |

| Growth in Plant-Based Alternatives Using 3D Printing | +2.7% | North America, Europe, and Asia-Pacific urban centers | Medium term (2-4 years) |

| Rising Technology Innovations by Manufacturers | +3.0% | Global, led by innovation hubs in Israel, Japan, United States, and Germany | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for personalized nutrition and customized foods

3D food printers are transforming personalized nutrition, shifting it from a marketing concept to a practical reality. Yamagata University has developed 3D food printers that use soft gel materials to create texture-modified meals for elderly patients with swallowing difficulties. This innovation highlights the capabilities of digital design: modifying hardness, nutrient density, and allergen content within a single production run. This technology addresses a critical gap in institutional food services, where accommodating residents with specific dietary needs, such as diabetes, allergies, or dysphagia, traditionally required separate kitchen workflows, increasing labor costs. However, the applications of this technology extend beyond eldercare. Hospitals and specialty clinics can now efficiently provide meals customized to individual patient requirements, adhering to therapeutic diets without the need for parallel production lines. Musashi Engineering leads the market with its FOODMASTER 3D printer, integrated with proprietary Mu-SLICER software. The company emphasizes the printer's ability to precisely control both extrusion and motion simultaneously, ensuring the production of stable, high-quality food shapes tailored to specific customer needs. This shift from conventional batch production to mass customization is redefining the economics of niche food segments, enabling the profitable service of smaller patient or consumer groups that were previously unviable.

Innovations in bio-printing for meat, seafood, and nutrient-rich products

Bio-printing has progressed from academic research to commercially scalable programs, driven by regulatory approvals that have unlocked previously stalled capital investments. In December 2023, Aleph Farms obtained preliminary approval from the Israeli Health Ministry to produce and sell cultivated beef steaks. These steaks are developed from cells sourced from a fertilized egg of a Black Angus cow. Following final label approval and inspection, these products are expected to reach consumers. This milestone is crucial as it establishes the technical and regulatory framework for 3D-bioprinted whole-muscle cuts, which yield higher profit margins compared to ground or less structured cell-based products. Concurrently, Revo Foods and Paleo are leading a EUR 2.2 million (USD 2.4 million) EU-funded initiative to create 3D-printed vegan salmon. Their efforts focus on the hybrid plant-cell segment, where combining cultivated fats with plant proteins enables faster market entry and reduces production costs compared to fully cell-cultured seafood. This approach highlights how early adopters are diversifying across pure cultivated, hybrid, and plant-based protein platforms to optimize revenue as cell-culture economics continue to develop. Additionally, Aleph Farms partnered with BioRaptor in May 2024 to leverage AI-driven bioprocess optimization for scaling cultivated meat production. This collaboration emphasizes the critical role of computational tools in achieving cost competitiveness with conventional meat.

Food waste reduction through precise portioning and on-demand production

On-demand production through 3D printing resolves a critical inefficiency in food supply chains: the disparity between forecast-based batch manufacturing and actual consumption, which results in waste across retail, foodservice, and household levels. Musashi Engineering, in collaboration with Aichi Industrial Science and Technology Center and MP Gokyo Food & Chemical, has developed feedstocks using underutilized resources, such as roasted sweet potato skins and low-value fish species. This innovation demonstrates how 3D printers can convert surplus or irregular raw materials into marketable products. This capability is especially significant in Japan, where industrial policies emphasize resource efficiency, and food manufacturers face increasing pressure to reduce organic waste. Additionally, the technology enables precise portioning, addressing the over-production inherent in fixed-batch processes and allowing operators to print only the required quantity for immediate use. A public demonstration at Japan's National Museum of Emerging Science in December 2024 featured 3D-printed sushi made from surimi and rice, showcasing the potential to reduce food loss by transforming low-cost ingredients into premium-format dishes. The strategic benefit lies in decoupling production volume from inventory risk, a shift that supports both commercial kitchens operating on tight margins and institutions striving to meet sustainability mandates.

Growth in plant-based alternatives using 3D printing

In some Western markets, the growth of plant-based protein adoption has slowed, mainly due to taste and texture differences compared to animal-based products. This challenge creates an opportunity for 3D printing technology to produce structured, meat-like formats that traditional extrusion and molding methods cannot achieve. In February 2024, Steakholder Foods signed a memorandum of understanding with Wyler Farm to implement industrial-scale 3D printing for plant-based beef steaks. By leveraging Steakholder's advanced Meat Printer MX200 and proprietary beef-steak premix, the partnership aims to produce whole-muscle analogs at a commercial scale. This collaboration is significant as it combines a technology innovator with an established tofu manufacturer, enabling faster market entry without the need to build a distribution network from scratch. In October 2024, Steakholder received its first purchase order from Wyler Farm under a commercial cooperation agreement. The premix blends will support a new plant-based product line, "Whaat Meat?! by Steakholder," targeting retail, restaurant, and catering channels in Israel. The shift from Research and Development collaboration to purchase orders marks a critical milestone, indicating that 3D-printed plant-based products are entering commercial production. Additionally, recurring revenue models are emerging, centered on proprietary premix supplies and royalty agreements tied to end-product sales.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Costs of 3D Printers and Materials | -2.8% | Global, with acute impact in price-sensitive emerging markets and small foodservice operators | Short term (≤ 2 years) |

| Regulatory Hurdles on Food Safety, Hygiene, and Labeling | -2.3% | Fragmented across jurisdictions; highest impact in EU (novel food approvals) and markets without clear frameworks | Medium term (2-4 years) |

| Consumer Unfamiliarity and Skepticism Toward 3D-Printed Food | -1.5% | Broad, with higher resistance in conservative food cultures and older demographics | Long term (≥ 4 years) |

| Supply Chain Issues for Specialized Inks and Powders | -1.2% | Global, with bottlenecks in regions lacking local ingredient suppliers or cold-chain logistics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High initial costs of 3D printers and materials

Capital intensity remains a major obstacle to the broader adoption of industrial 3D food printers. These systems require significant upfront investments, which small and mid-sized operators struggle to justify without clear payback timelines. Steakholder Foods' financial results for the first half of 2024 illustrate the scale of this challenge. Despite cutting research and development expenses by 54% year-over-year to USD 1.6 million, the company reported a net loss of USD 4.4 million and consumed an equivalent amount in operating cash, highlighting the prolonged cash burn associated with commercializing capital-intensive food technology platforms. End users face similar economic challenges: commercial-grade systems, necessary for consistent throughput and food-safe operations, often cost more than USD 100,000. Furthermore, proprietary food-grade inks and premix blends are priced at a premium due to limited supplier competition. LaserCook Inc., established in August 2023, is introducing a laser-based 3D food printer that uses laser irradiation to solidify specific regions of a liquid feedstock. The company claims its system offers lower costs and reduced mechanical complexity compared to the screw-extrusion systems provided by Apptec[1]Source: apptec, "10 new realizations I learned through developing a 3D food printer", apptec.co.jp. This innovation reflects efforts by equipment manufacturers to pursue disruptive cost-reduction strategies. However, the market remains dominated by higher-priced legacy platforms. Strategically, for manufacturers to penetrate markets beyond premium hospitality and institutional food services, they will need to adopt equipment leasing models or achieve significant reductions in hardware costs.

Regulatory hurdles on food safety, hygiene, and labeling

Regulatory fragmentation across jurisdictions adds complexity to compliance, delaying product launches and increasing market entry costs. This challenge is particularly significant for novel protein formats that do not align with existing food categories. While the Food and Drug Administration and United States Department of Agriculture have introduced a joint framework for cell-cultured products, labeling requirements and state-level restrictions remain unsettled. For example, Florida enacted a ban on cultivated meat sales in 2024. In Europe, the European Food Safety Authority's novel food approval process involves lengthy reviews and extensive data requirements, which smaller companies often struggle to meet, creating a barrier to entry. Aleph Farms achieved regulatory approval in Israel in January 2024, marking a significant milestone. However, the company must still secure label approval and pass final inspections before beginning commercial sales, highlighting that successful regulatory submissions do not ensure immediate market access. In May 2024, Singapore's regulatory-friendly environment enabled GOOD Meat to launch its retail cultivated chicken, demonstrating how streamlined approval processes can attract investment and accelerate commercialization. The strategic takeaway is that companies are leveraging geographic arbitrage, prioritizing markets with clear regulatory frameworks while delaying entry into regions with uncertain or restrictive policies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Structured Proteins Challenge Confectionery Dominance

Meat and seafood segments are forecast to grow at 18.02% CAGR from 2026 to 2031, outpacing all other product categories despite chocolates and confectionery holding a 38.58% share in 2025. This divergence reflects a fundamental shift in value capture: confectionery applications monetize established consumer acceptance and low technical barriers, while structured protein formats target the higher-margin opportunity in alternative meat and seafood, where 3D printing solves texture and appearance challenges that extrusion cannot address. Aleph Farms' January 2024 regulatory approval for cultivated beef steaks validates the technical pathway for bioprinted whole-muscle cuts, which command premium pricing relative to ground or unstructured cell-based products.

Bakery applications remain a steady contributor, leveraging 3D printing to produce complex shapes and intricate designs that differentiate premium offerings in hospitality and retail. Yamagata University's development of 3D food printers for eldercare foods, which can produce visually appealing texture-modified dishes resembling regular meals, illustrates the technology's versatility beyond protein and confectionery. Other product types, including sauces, dairy analogs, and functional foods, represent emerging opportunities where 3D printing enables precise nutrient layering and customized formulations. Musashi Engineering's collaboration with Tokyo Medical and Dental University and a chef specializing in dysphagia-friendly French cuisine produced 2D and 3D mousse forms aimed at improving nutrition and meal enjoyment for elderly patients, demonstrating that niche applications can drive adoption in institutional settings, as noted by Musashi Engineering[2]Source: Musashi Engineering, “3D Food Printer Overview,” Musashi Engineering, musashi-engineering.co.jp. The strategic implication is that incumbents in confectionery must defend share by accelerating innovation in customization and design complexity, while disruptors in meat and seafood race to achieve cost parity with conventional proteins before capital markets lose patience.

By End User: Residential Segment Accelerates as Commercial Matures

In 2025, commercial kitchens accounted for 51.35% of global revenue, driven by restaurants and hotels leveraging labor savings and menu differentiation. Fine-dining venues, as early adopters, print intricate dessert sculptures during off-peak hours, boosting average ticket values without increasing staff. This trend highlights how commercial kitchens are utilizing 3D food printing technology to enhance operational efficiency and offer unique menu items that attract customers. In H1 2024, Steakholder Foods inked four commercial contracts, notably with Taiwan’s Industrial Technology Research Institute, creating a repeatable model that integrates hardware, premix, and royalties. These agreements demonstrate the growing adoption of 3D food printing solutions in commercial settings, emphasizing their scalability and profitability.

Forecasted to achieve a 17.23% CAGR through 2031, the residential channel sees consumer appliances becoming smaller and more affordable. LaserCook’s innovative design, featuring fewer moving parts, positions its retail units as attainable for upscale kitchen enthusiasts. This development reflects the increasing accessibility of 3D food printing technology for households, enabling consumers to experiment with personalized meal preparation. With a focus on portion control, allergy management, and culinary creativity, the value propositions are drawing the 3D food printing market into households. While government and space-agency applications are niche, their endorsement underscores the technology's longevity, nutritional stability, and waste management systems, paving the way for civilian adoption. These use cases validate the technology's potential for broader applications, including sustainable food production and resource optimization in constrained environments.

Geography Analysis

From 2026 to 2031, the Asia-Pacific region is expected to grow at a CAGR of 17.85%, surpassing all other regions. This growth is driven by Japan's government-supported Research and Development consortia, China's rapid commercialization efforts, and Singapore's favorable regulatory policies, creating an ideal environment for 3D food printing adoption. In May 2024, GOOD Meat achieved a milestone by launching the world's first retail sale of cultivated chicken in Singapore. Priced at SGD 7.20 (USD 5.30) for a 120-gram package, this development highlights how streamlined approval processes can enable jurisdictions to outpace Western markets in delivering 3D-printed and cultivated foods to consumers. Japan's Soft3D Co-Creation Consortium, established to advance 3D food printer R&D in collaboration with food industry stakeholders, has demonstrated significant progress. Public showcases, such as the 2024 sushi exhibition at Miraikan's National Museum of Emerging Science, emphasize the technology's potential to minimize food waste and transform low-cost ingredients into premium products. China and India are strengthening their alternative protein infrastructures, with local manufacturers and suppliers emerging to serve domestic markets at competitive prices. Australia's foodservice industry is exploring 3D printing for high-end hospitality applications, while South Korea is updating its regulatory framework to accommodate cell-cultured and 3D-printed foods.

In 2025, North America held a 41.12% market share, supported by its well-established foodservice infrastructure, early regulatory clarity under the FDA-USDA joint framework for cell-cultured products, and substantial venture capital investments in food technology startups. Steakholder Foods' 2024 partnerships with Wyler Farm and Taiwan's Industrial Technology Research Institute illustrate North America's strategy to target both domestic and Asia-Pacific markets. By utilizing proprietary technologies, these companies are not only driving equipment sales but also generating recurring revenue from ingredient supplies. The United States remains the largest single-country market, fueled by adoption in premium restaurants, hotels, and institutional food services. However, state-level regulatory inconsistencies, such as Florida's 2024 ban on cultivated meat sales, create compliance challenges that could hinder market growth. Canada and Mexico are emerging as secondary markets, with Canadian companies focusing on 3D printing for specialized diets and Mexican foodservice chains experimenting with menu customization.

Europe's 3D food printing market is shaped by strict novel food regulations enforced by the European Food Safety Authority. These regulations, which require lengthy reviews and extensive data submissions, tend to favor established players over startups. Germany, the United Kingdom, France, and Italy are leading adoption efforts. German engineering firms are supplying industrial 3D printers to foodservice operators across Europe, while United Kingdom, hospitality chains are testing customization for seasonal menus. In South America, the Middle East, and Africa, the 3D food printing market is still in its early stages. Challenges such as limited infrastructure, high equipment costs, and low consumer awareness hinder adoption. However, interest is beginning to grow in urban areas and premium hospitality segments.

Competitive Landscape

As firms strive to secure intellectual property and establish distribution alliances, competitive dynamics continue to evolve within a moderately to highly consolidated market. Steakholder Foods integrates printer hardware with proprietary premix blends, creating a recurring revenue stream that offsets the cyclical nature of hardware sales. Aleph Farms, specializing in cultivated beef steaks, focuses on licensing its core bioprinting processes to regional producers. This strategy positions the company as a technology enabler, prioritizing innovation and scalability over end-to-end manufacturing.

LaserCook Inc. has introduced laser-solidification printers, which are set to disrupt cost structures and challenge established players reliant on extrusion-based architectures. Musashi Engineering differentiates itself through its Mu-SLICER software, highlighting the growing importance of firmware and slicer algorithms in determining throughput and shape accuracy, alongside traditional mechanical design. Ingredient suppliers are increasingly asserting their bargaining power by owning formulations that influence critical factors such as mouthfeel and nutritional value, signaling the potential for future vertical mergers within the industry.

Private capital remains abundant; however, investors are increasingly demanding greater transparency regarding consumable margins and regulatory pathways. Partnerships between hardware manufacturers and major food conglomerates are accelerating go-to-market strategies, but the risk of patent litigation is rising as overlaps in print-head geometries and feedstock recipes become more common. Consequently, the global 3D food printing market is navigating a delicate balance between aggressive innovation and strategic portfolio management to ensure the protection of long-term enterprise value.

3D Food Printing Industry Leaders

-

BeeHex

-

byFlow

-

Systems And Materials Research Corporation (SMRC)

-

Natural Machines

-

TNO

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Italian researchers, through the ENEA-led Nutri3D project, are developing sustainable snacks using lab-cultured plant cells and fruit processing residues, formed into nutrient-rich prototypes like snack bars and "honey pearls" via 3D printing.

- November 2024: Revo Foods announced a partnership with Paleo on a EUR 2.2 million (USD 2.4 million) EU-funded project to develop 3D-printed vegan salmon, targeting the commercialization of plant-based seafood alternatives using advanced bioprinting technology. The project represents a significant institutional investment in hybrid plant-cell platforms as a hedge against protein supply volatility.

- July 2024: Redefine Meat commercially launched the world's first whole cuts of new meat in Rehovot, Israel. It is the first-ever category of plant-based whole cuts that achieve a product quality comparable to high-quality animal meat.

- February 2024: Steakholder Foods signed a memorandum of understanding with Wyler Farm to deploy industrial-scale 3D printing for plant-based beef steaks, leveraging Steakholder's Meat Printer MX200 and proprietary beef-steak premix to produce whole-muscle analogs at commercial throughput. The partnership pairs a technology provider with an established tofu manufacturer, accelerating market entry by bypassing the need to build distribution from scratch.

Global 3D Food Printing Market Report Scope

3D food printing is the process of manufacturing food products using a variety of additive manufacturing techniques. Most commonly, food-grade syringes hold the printing material, which is then deposited through a food-grade nozzle layer by layer. The food 3D printing market is segmented by product type, end user, and geography. The market is segmented by product type into chocolates and confectionery, bakery, meat and seafood, and other product types. By end user, the market is segmented into government, commercial, and residential. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD).

| Chocolates and Confectionery |

| Bakery |

| Meat & Seafood |

| Other Product Types |

| Government |

| Commercial |

| Residential |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Product Type | Chocolates and Confectionery | |

| Bakery | ||

| Meat & Seafood | ||

| Other Product Types | ||

| By End User | Government | |

| Commercial | ||

| Residential | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the 3D food printing market?

The market stands at USD 1.17 billion in 2026 and is on track to reach USD 4.62 billion by 2031.

Which segment is growing fastest within 3D food printing?

Meat and seafood products are projected to post an 18.02% CAGR from 2026 to 2031.

Which region shows the highest growth potential?

Asia-Pacific is forecast to grow at 17.85% CAGR through 2031 due to supportive regulations and funding.

How are companies generating recurring revenue?

Leading firms bundle printers with proprietary premix supplies and royalty agreements tied to product sales.

Page last updated on: