Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.42 Billion |

| Market Size (2026) | USD 2.52 Billion |

| Market Size (2031) | USD 3.09 Billion |

| Growth Rate (2026 - 2031) | 4.13% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Paperboard Packaging Market Analysis by Mordor Intelligence

The Egypt Paperboard Packaging market size was valued at USD 2.42 billion in 2025 and estimated to grow from USD 2.52 billion in 2026 to reach USD 3.09 billion by 2031, at a CAGR of 4.13% during the forecast period (2026-2031). Strong processed-food export gains, widening e-commerce penetration, and policy shifts favoring fiber-based formats underpin sustained demand across corrugated boxes, folding cartons, and liquid cartons. Export-oriented food processors require temperature-stable, contamination-free packaging that complies with Gulf and European regulations, while online retailers seek lightweight, brandable shipping containers that protect products during last-mile delivery. Rising private-sector investment of EGP 133.1 billion in Q1 FY2024/25 channels capital toward logistics hubs, fulfillment centers, and converting plants that enlarge the domestic converting base. Meanwhile, bans on single-use plastic bags in the Red Sea governorate and Sharm El-Sheikh are accelerating the substitution toward recyclable paperboard along Egypt’s tourism corridors.[1]Zeinab El-Gundy, “Egypt in the process of going plastic-free,” Ahram Online, ahram.org.eg Currency stability following the March 2024 float and USD 35 billion UAE injection bolsters investor confidence, yet mills remain exposed to higher electricity tariffs after the COVID-era industrial discount was revoked in June 2025.

Key Report Takeaways

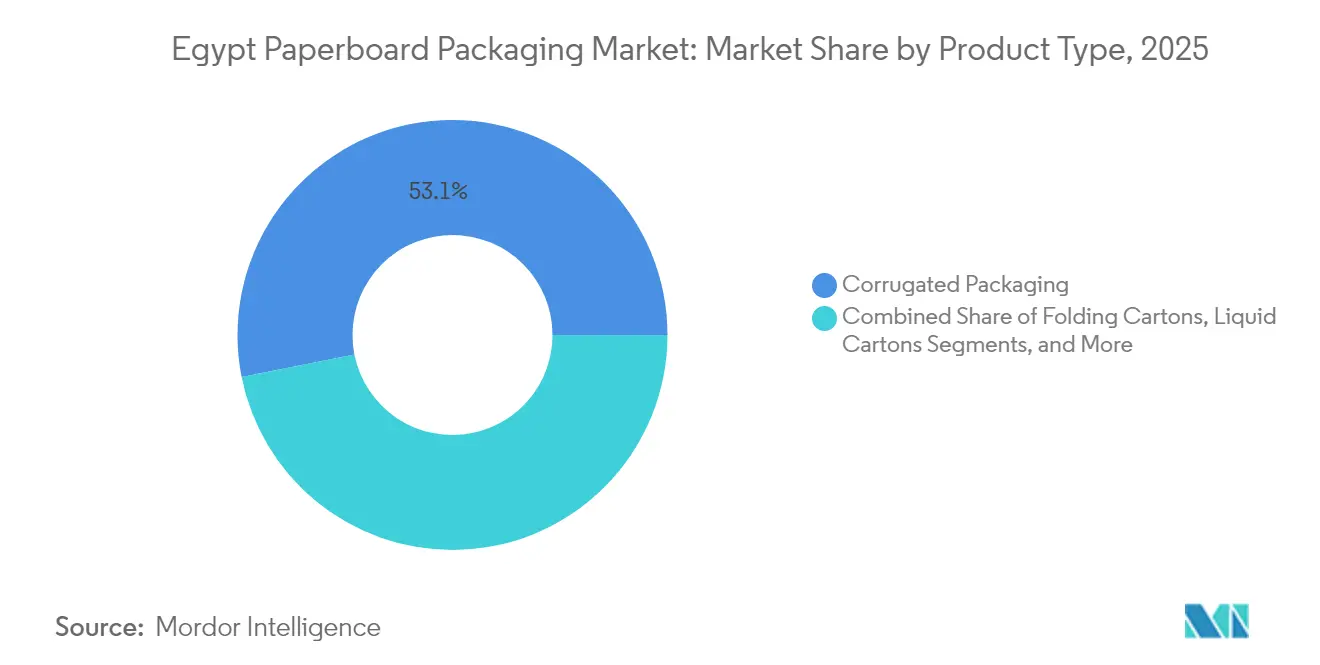

- By product type, corrugated packaging captured 53.12% of the Egypt paperboard Packaging market share in 2025.

- By material grade, the Egypt Paperboard Packaging market size for mixed fiber is projected to expand at a 5.05% CAGR between 2026-2031.

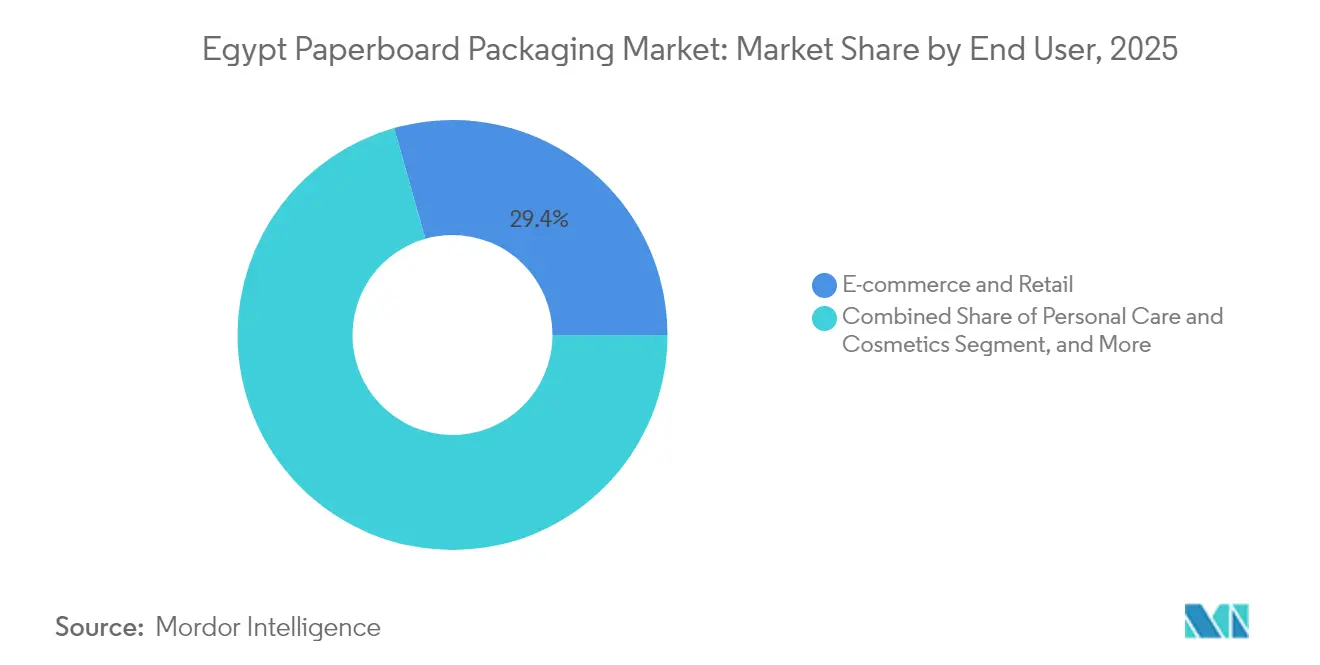

- By end-user, e-commerce and retail captured 29.38% of the Egypt paperboard Packaging market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Egypt Paperboard Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Processed-food export boom | +1.2% | Nile Delta, Alexandria | Medium term (2-4 years) |

| E-commerce last-mile acceleration | +0.8% | Cairo, Alexandria, Giza | Short term (≤ 2 years) |

| Plastic-bag bans | +0.6% | Red Sea, national rollout | Long term (≥ 4 years) |

| Green-manufacturing incentives | +0.4% | Industrial zones, Suez Canal Economic Zone | Long term (≥ 4 years) |

| Import tariffs on empty cartons | +0.3% | National | Medium term (2-4 years) |

| Smart digital printing adoption | +0.2% | Urban consumer markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Processed-food export boom

Egypt’s processed-food exports surged 21% year over year to USD 6.1 billion in 2024, stimulating upstream demand for corrugated shippers, liquid cartons, and folding cartons that satisfy transport, barrier, and regulatory requirements for frozen potatoes, edible oils, and fruit juices. Arab destinations absorbed 54% of shipments, often favoring stackable, moisture-resistant corrugated cases, while EU buyers worth USD 1.168 billion mandated high-grade, multilayer paperboard with traceability features. The Food Export Council’s training programs and trade-fair support extend processors’ reach into new markets, sustaining the Egypt Paperboard Packaging market through 2030.

E-commerce last-mile acceleration

Digital commerce revenue expansion hinges on rising smartphone adoption and domestic logistics expansion, prompting retailers to standardize corrugated shipper dimensions, integrate QR-based authentication, and adopt custom inserts that reduce in-transit damage. Private investment climbed 30% year over year to EGP 133.1 billion in Q1 FY2024/25, much of it financing warehouses and delivery fleets that consume high volumes of folding cartons and mailers. Sustainability-minded online brands prefer recyclable substrates, driving growth in the Egyptian Paperboard Packaging market across urban hubs.

Plastic-bag bans

The Red Sea governorate’s 2019 decree and Sharm El-Sheikh’s sweeping ban, ahead of COP27, exemplify the tightening of rules that restrict petroleum-based carrier bags and food-service disposables. Hospitality chains, grocers, and souvenir stores are migrating to kraft paper sacks, molded pulp trays, and coated folding cartons, gradually expanding fiber demand nationwide.

Green-manufacturing incentives

Fiscal incentives offered by Egypt’s Sovereign Fund and the Suez Canal Economic Zone encourage the development of low-carbon production, recycling plants, and waste-to-energy facilities. Such programs reduce project-financing costs for mills installing biomass boilers or solar rooftops, underpinning capacity additions that reinforce the growth trajectory of the Egyptian Paperboard Packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pound depreciation inflating pulp costs | -0.7% | National | Short term (≤ 2 years) |

| Fragmented collection infrastructure | -0.5% | Rural areas | Long term (≥ 4 years) |

| Volatile energy tariffs | -0.4% | Industrial zones | Medium term (2-4 years) |

| Reusable plastic crates in produce logistics | -0.2% | Agricultural chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Currency-driven pulp inflation

The pound’s sharp devaluation in early 2024 increased imported pulp costs in local terms, reducing gross margins for mills that rely on Scandinavian, Brazilian, and North American fiber. Mondi booked a EUR 32 million currency loss in H1 2024, underscoring the exposure faced by global producers operating in Egypt.

Collection-system fragmentation

Only 35% of rural solid waste is formally collected, which constrains the recovered-fiber pool available to local recyclers and compels converters to import supplementary material despite high freight charges.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Corrugated leadership amid export logistics needs

Corrugated solutions generated 53.12% of the Egyptian paperboard Packaging market share in 2025, reflecting their versatility across processed foods, electronics, and industrial commodities. The Egypt Paperboard Packaging market size for corrugated boxes is expected to expand in tandem with the growth of export-processing zones along the Nile Delta. Local converters continue to add high-speed flexo lines and rotary die-cutters, which shorten lead times for multicolor shippers targeting Gulf retailers.

Liquid cartons are projected to post the fastest 5.55% CAGR through 2031, buoyed by rising domestic juice and UHT milk consumption, as well as export-oriented beverage processors adopting aseptic technology. SIG’s April 2025 launch of Egypt’s first closed-loop collection and recycling system for beverage cartons brings end-of-life solutions into the mainstream. Folding cartons continue to meet demand in the pharmaceuticals and personal care sectors, where precision creasing and premium graphics remain essential.

By Material Grade: Recycled fiber prominence with mixed-grade upswing

Recycled fiber held 52.05% of Egypt's Paperboard Packaging market share in 2025, supported by the Waste Management Law’s producer-responsibility provisions and steadily rising recovered-paper imports. Yet feedstock shortages persist, prompting mills to optimize furnish blends and invest in OCC sorting lines. Mixed fiber, blending virgin and recycled stock, is projected to log a 5.05% CAGR as converters balance performance, food-contact safety, and cost.

Virgin fiber remains indispensable for liquid cartons and heavy-duty corrugated grades requiring high ring-crush strength. Domestic capacity additions are limited, so mills hedge supply risk through long-term pulp contracts and on-site deinked pulp facilities that partially offset dollar-denominated raw material exposure.

By End User: E-commerce reigns while cosmetics accelerate

The e-commerce and retail segment commanded 29.38% of 2025 revenue, driven by Cairo-centric last-mile networks and consumers’ preference for return-ready, branded boxes that heighten unboxing appeal. Automated fulfillment centers utilize machine-erected corrugated trays, paper void-fill, and tamper-evident seals to reduce labor costs and shrink damage claims, thereby fueling the growth of the Egyptian Paperboard Packaging market.

Personal care and cosmetics applications are expected to advance at a 5.29% CAGR as local brands scale and international players co-pack region-specific SKUs in Egypt to leverage tariff advantages. High-gloss folding cartons, window patching, and digital embellishments differentiate products on pharmacy and hypermarket shelves, lifting average selling prices and converting margins.

Geography Analysis

Cairo’s metropolitan cluster accounts for the largest slice of consumption, driven by its 20 million residents, dense e-commerce volumes, and proximity to printing hubs. Alexandria’s port ecosystem supports high outbound container volumes of food, chemicals, and manufactured goods, anchoring corrugated demand among exporters. The Suez Canal Economic Zone is emerging as a green-industry enclave, offering subsidized land leases and streamlined customs, which makes it a favored site for new paperboard mills and recyclers.

Upper Egypt’s agricultural governorates foster demand for produce trays and wax-free fruit cartons. Nevertheless, low waste-collection coverage restricts OCC availability, prompting pilot community-collection projects funded by development banks. Red Sea tourism corridors, having banned single-use plastics, generate specialty kraft shopping bags and coated salad-box demand across hotels and resorts, advancing the Egypt Paperboard Packaging market.

Exports to Arab partners, which account for 54% of processed-food shipments, require Arabic-language graphics and Halal-certified materials, while EU shipments necessitate FSC certification and migration-compliant inks, prompting converters to secure chain-of-custody audits. Emerging East-African markets are opening to Egyptian suppliers leveraging competitive freight rates via the soon-to-be-expanded Safaga Port.

Competitive Landscape

The Egyptian paperboard Packaging market features a medium concentration, with the top five producers holding roughly a 50% collective share. Integrated multinationals such as Mondi, International Paper, and Smurfit Kappa (formerly WestRock) operate kraft liner production and corrugating plants, benefiting from scale economies and captive pulp.[3]PaperAge staff, “Smurfit WestRock Reports Third-Quarter 2024 Financial Results,” paperage.com Regional groups like Indevco and Uniboard focus on lightweight corrugated and specialty folding cartons. Local champions Misr Cartonboard and El-Ahram Printing capitalize on proximity to FMCG clients and short lead times.

Capacity expansions dominate strategy. Mondi’s January 2024 purchase of Lafarge Cement Egypt’s paper-bag assets resulted in an additional 180 million bags of annual throughput, securing long-term contracts in the cement sector. SIG partnered with Plastic Bank and Carta Misr to establish an end-to-end beverage carton recycling chain, enhancing brand sustainability credentials while unlocking PCR fibers. Tetra Pak piloted QR-enabled traceability solutions, and Smurfit WestRock installed high-efficiency corrugators that cut energy intensity by 15%.

Rising input-cost pressure spurs efficiency moves: mills deploy AI-based predictive maintenance, switch to natural-gas-fired boilers, and sign 20-year solar PPAs to hedge tariff hikes. Digital printing adoption accelerates the use of short-run, versioned packaging for cosmetics and online sellers, differentiating converters that invest in single-pass inkjet or toner platforms.

Egypt Paperboard Packaging Industry Leaders

Huhtamaki Egypt L.L.C.

International Paper Company

Smurfit WestRock plc

Mondi plc

Tetra Pak Egypt Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: SIG inaugurated Egypt’s first closed-loop recycling network for aseptic beverage cartons, integrating blockchain-tracked collection with local fiber repulping.

- June 2025: Egypt’s Cabinet withdrew industrial power subsidies, lifting paperboard production costs by 10–15 piastres/kWh.

- February 2025: Processed-food exports hit USD 6.1 billion for 2024, up 21% year over year, sustaining robust demand for corrugated and liquid-carton formats.

- March 2024: The currency float and USD 35 billion UAE investment stabilized the EGP around 50 per USD, reducing FX volatility for import-reliant converters.

Egypt Paperboard Packaging Market Report Scope

Paperboard packaging refers to packaging materials made from thick paper. It is versatile, recyclable, and can be printed upon, making it suitable for a wide range of products in the food, beverage, cosmetics, pharmaceutical, electronics, and other manufacturing industries for the purpose of strength, aesthetics, and sustainability.

The Egyptian paperboard packaging market is segmented by product type (corrugated and solid fiber boxes, folding cartons, and other product types) and end-user industry (food, beverage, healthcare and pharmaceutical, household and personal care, and other end-user industries). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Product Type

| Folding Cartons |

| Corrugated Packaging |

| Liquid Cartons |

| Other Product Types |

By Material Grade

| Virgin Fiber |

| Recycled Fiber |

| Mixed Fiber |

By End-User

| Food |

| Beverage |

| Healthcare and Pharmaceutical |

| Household and Personal Care |

| E-commerce and Retail |

| Industrial and Electronics |

| By Product Type | Folding Cartons |

| Corrugated Packaging | |

| Liquid Cartons | |

| Other Product Types | |

| By Material Grade | Virgin Fiber |

| Recycled Fiber | |

| Mixed Fiber | |

| By End-User | Food |

| Beverage | |

| Healthcare and Pharmaceutical | |

| Household and Personal Care | |

| E-commerce and Retail | |

| Industrial and Electronics |

Key Questions Answered in the Report

How big is the Egypt Paperboard Packaging market in 2026?

The market is valued at USD 2.52 billion in 2026 and is forecast to grow at a 4.13% CAGR to 2031.

Which product type leads demand?

Corrugated packaging leads with 53.12% 2025 share, driven by export logistics and e-commerce shipping needs.

Why are liquid cartons growing fastest?

Rising juice and dairy processing plus SIG’s new recycling network support a 5.55% CAGR in liquid cartons.

How significant is recycled fiber in Egypt?

Recycled fiber represents 52.05% of 2025 volume, backed by waste-management reforms and cost advantages.

What regulatory trends favor paperboard?

Single-use plastic-bag bans and green-procurement policies in Red Sea and national programs encourage fiber substitution.

Which end-user segment offers the highest growth?

Personal care and cosmetics packaging is projected to expand at 5.29% CAGR through 2031 due to rising domestic production and exports.

Page last updated on: