Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

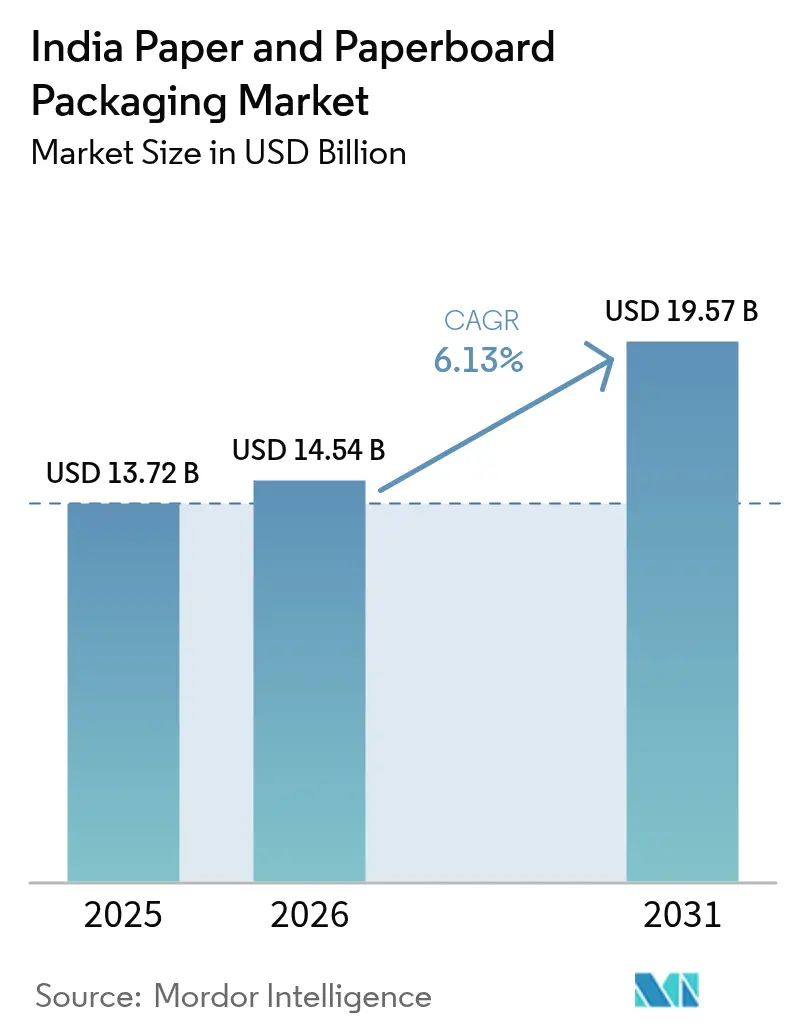

| Base Year Market Size (2025) | USD 13.72 Billion |

| Market Size (2026) | USD 14.54 Billion |

| Market Size (2031) | USD 19.57 Billion |

| Growth Rate (2026 - 2031) | 6.13% CAGR |

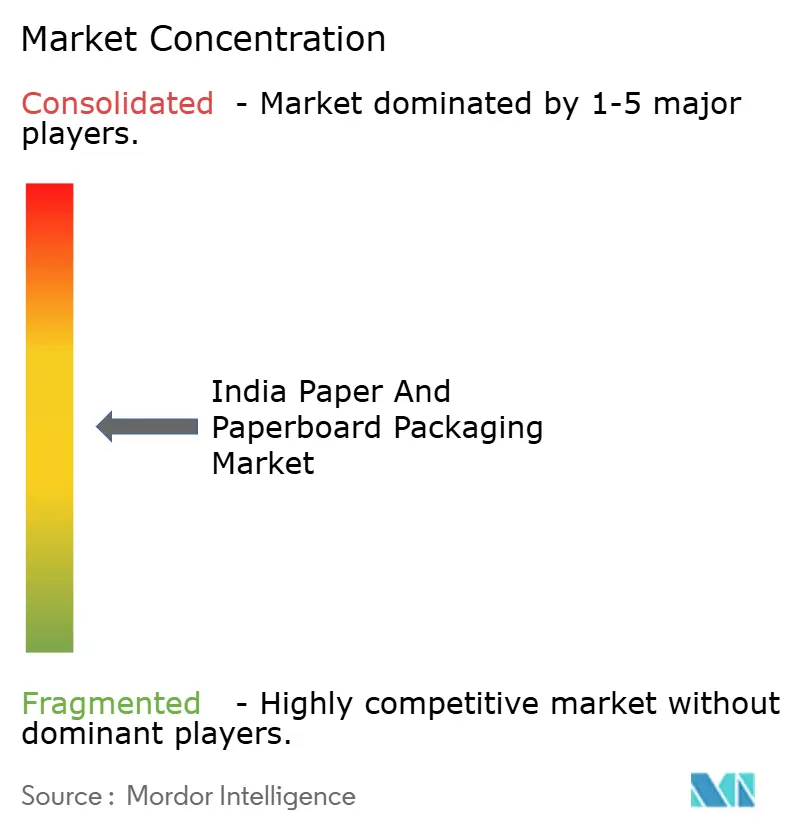

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Paper And Paperboard Packaging Market Analysis by Mordor Intelligence

The India paper and paperboard packaging market size is expected to grow from USD 13.72 billion in 2025 to USD 14.54 billion in 2026 and is forecast to reach USD 19.57 billion by 2031 at a 6.13% CAGR over 2026-2031. A nationwide ban on select single-use plastics, fast-rising e-commerce penetration and record investments in agro-residue pulping have become the core pillars supporting this trajectory. Order profiles are fragmenting as quick-commerce platforms favor right-sized corrugated shippers, while food and beverage brands move toward QR-code-enabled mono-material packs that simplify Extended Producer Responsibility audits. Integrated mills with captive pulp and biomass energy are widening their cost gap over converters that rely on volatile imported waste paper. At the same time, automated flexographic and digital presses allow nimble converters to win premium short-run work in cosmetics and pharmaceuticals despite higher raw-material costs.

Key Report Takeaways

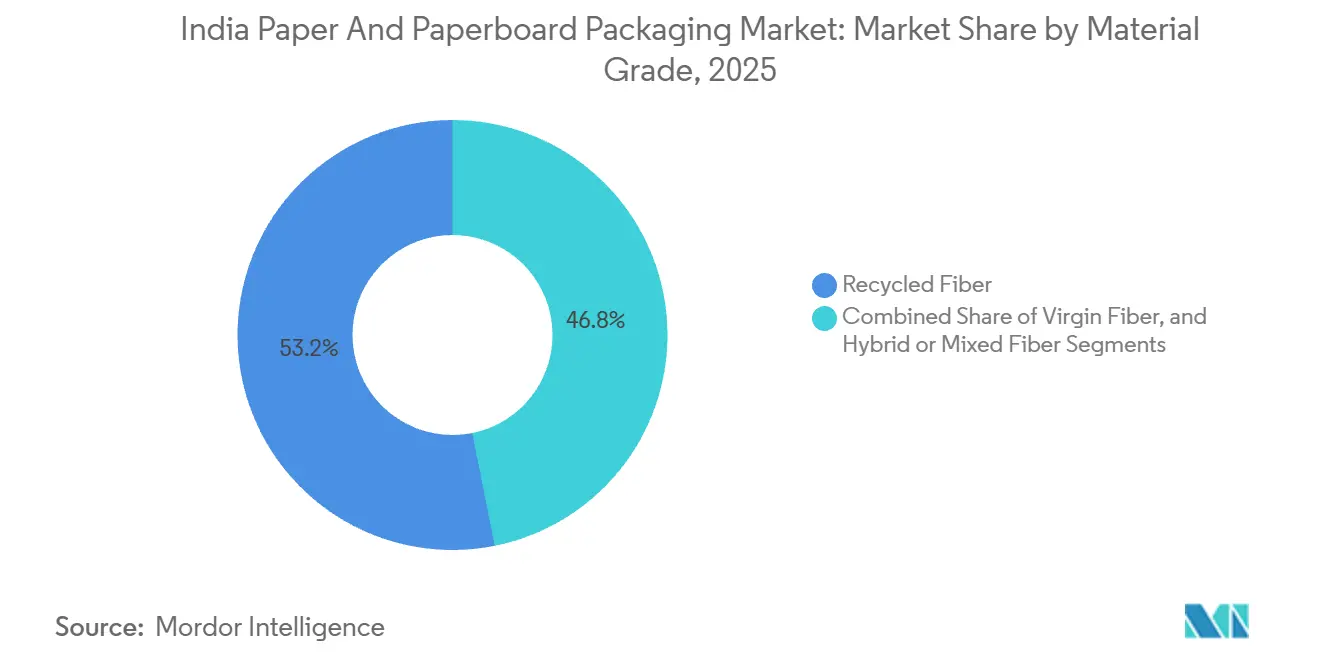

- By material grade, recycled fiber led with 53.16% of India paper and paperboard packaging market share in 2025, whereas hybrid or mixed fiber is projected to post the fastest 7.14% CAGR through 2031.

- By product type, corrugated packaging accounted for 48.24% of the India paper and paperboard packaging market size in 2025, while liquid cartons are set to expand at a 7.63% CAGR to 2031.

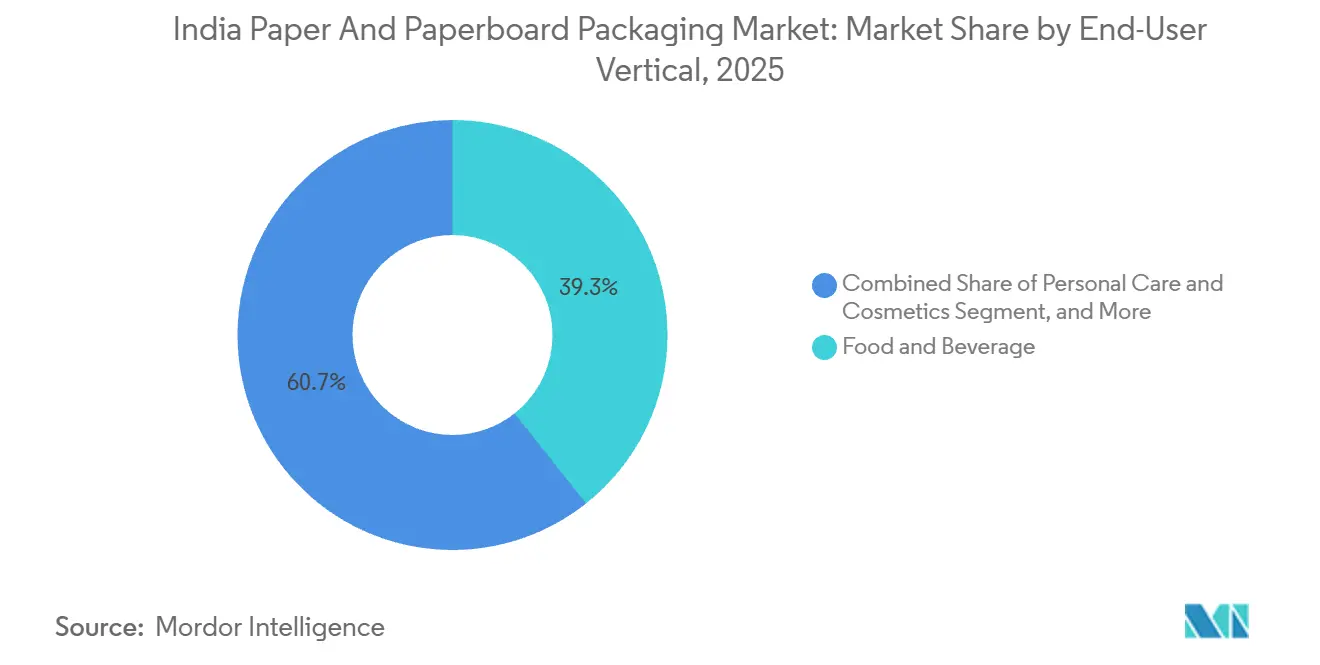

- By end-user vertical, food and beverage held 39.34% market share in 2025, whereas personal care and cosmetics is forecast to grow at an 8.12% CAGR during 2026-2031.

- By packaging format, secondary packaging represented 45.24% of the India paper and paperboard packaging market size in 2025 and is expected to grow at a 7.85% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Paper And Paperboard Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising E-commerce Corrugated Demand | +1.8% | National, with concentration in metro dark-store clusters and tier-2 quick-commerce hubs | Short term (≤ 2 years) |

| Food Brand Shift to Recyclable Mono-Material Packs | +1.3% | National, led by FMCG majors in Maharashtra, Tamil Nadu, Gujarat | Medium term (2-4 years) |

| Government Ban on Single-Use Plastics | +1.1% | National, with stricter enforcement in Delhi, Karnataka, Maharashtra | Medium term (2-4 years) |

| Emergence of Quick-Commerce Regional Hubs | +0.9% | Tier-2 and tier-3 cities including Jaipur, Lucknow, Coimbatore, Indore | Short term (≤ 2 years) |

| Automated High-Speed Flexo Printing Investments | +0.6% | National, concentrated in Gujarat, Tamil Nadu, Haryana converter clusters | Long term (≥ 4 years) |

| Agro-Residue Pulp Capacity Additions | +0.5% | Punjab, Haryana, Uttar Pradesh (wheat straw); Maharashtra, Karnataka (bagasse) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising E-commerce Corrugated Demand

Order-to-dispatch cycles in quick-commerce have compressed from hours to minutes, forcing converters near fulfillment hubs to keep pre-assembled shippers ready at all times. Average units per shipment are now closer to one SKU than the three to five typical in earlier e-retail models, effectively multiplying corrugated demand per rupee of merchandise sold. Tier-2 cities such as Jaipur, Lucknow, Coimbatore and Indore are expanding fastest because dark-store operators secure lower real-estate costs there, drawing regional converters to invest in rotary die-cutters and slitter-scorers. Right-weighting to cut excess void fill has become a key cost lever for platforms dispatching millions of micro-orders each month. The resulting boom in micro-flute boards that deliver crush resistance at lighter basis weights adds fresh momentum to the India paper and paperboard packaging market.

Food Brand Shift to Recyclable Mono-Material Packs

Extended Producer Responsibility rules mandate QR-code traceability from July 2025, pushing brand owners to redesign packs around a single substrate.[1]Ministry of Environment, Forest and Climate Change, “Plastic Waste Management Amendment Rules 2024,” moef.gov.in Carton makers responded with barrier-coated paperboard that withstands oil, moisture and oxygen without relying on multilayer plastic laminates. Although these substrates cost 8-12% more than polyethylene pouches, leading consumer-goods companies absorb the premium to avoid non-compliance fines and reputational risk. Retailers now favor matte cartons that showcase sustainability credentials, a shift that boosts print value per pack. Large converters securing multiyear supply agreements can therefore justify further automation and widen their competitive moat.

Government Ban on Single-Use Plastics

The prohibition on 19 single-use plastic items has positioned paper as the default replacement for carry bags, cutlery and food-service ware.[2]Press Information Bureau, “Single-Use Plastic Ban Enforcement,” pib.gov.in States with well-staffed inspection squads such as Delhi and Karnataka collected most of the INR 198 million in fines recorded by 2024, reinforcing compliance urgency. Demand for kraft grocery bags and molded-pulp trays that was negligible before the ban surged across modern retail formats. Mills are upgrading pulping chemistries to meet tighter migration limits for heavy metals in food-contact grades. While illicit plastic flows persist in informal retail, the regulatory direction cements a durable demand floor for fiber-based solutions.

Emergence of Quick-Commerce Regional Hubs

Platforms such as Blinkit and Zepto have opened micro-fulfillment centers in Jaipur, Lucknow, Coimbatore and Indore, each stocking 2,000-3,000 SKUs and promising 15-minute delivery windows. These hubs require customized shippers that optimize shelf density, prompting converters to site flexographic lines within 50 km of dark stores. Localized supply eliminates interstate freight delays and ensures same-day replenishment commitments. Durable secondary packs that survive multiple reverse-logistics cycles are gaining favor, increasing demand for high-burst board grades. Together, these trends create new profit pools for agile converters in emerging consumption centers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Volatility of Imported Waste Paper | -0.8% | National, acute in coastal states with port access (Gujarat, Maharashtra, Tamil Nadu) | Short term (≤ 2 years) |

| Chronic Containerboard Energy-Cost Inflation | -0.7% | National, most severe in states with coal-dependent grids (Chhattisgarh, Odisha, Jharkhand) | Medium term (2-4 years) |

| Delayed GST Refunds for SME Converters | -0.4% | National, disproportionately affects SMEs in Gujarat, Haryana, Uttar Pradesh | Medium term (2-4 years) |

| Digital Substitution in Billing and Publishing | -0.3% | National, concentrated in urban centers with high digital-payment adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Volatility of Imported Waste Paper

India imported roughly 1.5 million t of waste paper in FY 2023-24, yet domestic collection efficiency remains below 30%.[3]Ministry of Commerce and Industry, “Waste Paper Import Data FY 2023-24,” commerce.gov.in Bale prices swung 20-30% during 2024 after China’s National Sword policy rerouted shipments, forcing recycled-board mills to trade off margin versus volume. Standalone converters locked into annual price contracts resist cost pass-through, squeezing mill profitability. Some producers blend agro-residue pulp, but wheat-straw fibers lack the tensile strength required for heavy-duty liners. Until organized collection scales, volatility will continue to undercut recycled-fiber economics.

Chronic Containerboard Energy-Cost Inflation

Thermal-coal and grid tariffs rose 10-15% across India in 2024, lifting energy toward 20% of board production cost for mills without captive power. Integrated players such as ITC and JK Paper installed biomass cogeneration that burns agro-residue or black liquor, partially insulating them from fossil-fuel swings. Stand-alone converters purchasing finished board cannot hedge and consequently exit low-margin SKUs or consolidate with stronger rivals. Sustained inflation narrows the traditional price gap between recycled and virgin grades, subtly reshaping substrate decisions. Energy cost pressure therefore doubles as a consolidation catalyst within the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Grade: Hybrid Fiber Blends Gain Momentum

Recycled fiber controlled 53.16% of India paper and paperboard packaging market share in 2025, yet hybrid grades are forecast to deliver a 7.14% CAGR to 2031, outpacing all other material options. These blends combine agro-residue pulp with recycled furnish, providing crush strength while satisfying recycled-content criteria. The Directorate General of Trade Remedies began probing subsidized virgin imports from Chile and China in 2024, making domestically sourced hybrids more attractive. Imported waste-paper volatility further drives mills to secure agro-residue feedstock from wheat straw and bagasse, stabilizing cost curves. Policy incentives that reward stubble-burning reduction and circular-economy targets reinforce the transition toward hybrid boards.

Hybrid adoption also benefits converters: boards run clean on high-speed corrugators and accept water-based inks without extra primer, reducing downtime. Brand owners display recycled-content logos prominently, enhancing on-shelf perception without sacrificing box compression strength. Integrated mills with both pulp and converting assets therefore defend margins even in down cycles. Smaller firms can still participate by buying pre-trimmed hybrid sheets, though their cost base remains higher than that of vertically integrated rivals. Overall, hybrid grades advance both sustainability messaging and performance, securing their place in the growth mix of the India paper and paperboard packaging market.

By Product Type: Liquid Cartons Ride Dairy Upswing

Corrugated packaging dominated 48.24% of India paper and paperboard packaging market size in 2025, but liquid cartons are poised for the fastest 7.63% CAGR through 2031. Less than 10% of India’s milk output reaches consumers in packaged form, leaving vast headroom for aseptic cartons that permit ambient storage. SIG Combibloc’s USD 96 million plant in Ahmedabad can produce 4 billion packs a year, ensuring local supply for co-operatives modernizing distribution. Dairy processors in tier-2 cities value shelf-stable packs that bypass cold-chain costs, broadening market access and curbing spoilage.

Beyond dairy, fruit-based beverages and flavored milks adopt carton formats to differentiate from PET bottles. Folding cartons maintain relevance in pharmaceuticals and confectionery because anti-counterfeit features such as holographic foils fit easily on carton substrate. Paper bags continue to benefit from grocery bans on thin plastics, although reusable non-woven options slow their penetration. Rigid boxes, despite a niche volume base, capture premium margins in smartphones and luxury accessories. Collectively, this diversified demand profile consolidates liquid cartons and allied paperboard formats as structural growth pillars.

By End-User Vertical: Personal Care Leads Premiumization

Food and beverage held 39.34% of India paper and paperboard packaging market share in 2025, yet personal care and cosmetics is tipped to expand at an 8.12% CAGR during 2026-2031. A USD 28 billion domestic personal-care sector produced 186.6 billion packaging pieces in 2024, favoring matte-finish cartons with soft-touch lacquers and foil stamping. Brand owners localize designs for festivals, resulting in frequent changeovers that reward converters equipped with servo-driven presses. QR-code authentication printed inline also supports direct-to-consumer engagement campaigns.

Healthcare and pharmaceuticals demand tamper-evident seals and serialization, adding complexity that boosts per-unit revenue for folding-carton suppliers. Electronics require micro-flute corrugated inserts and molded-pulp cushioning to cut transit damage, expanding use of lightweight but high-strength board. Industrial and automotive parts ship in heavy-duty containers, though growth there follows broader manufacturing cycles. Consequently, while staples anchor volume, premium personal care and regulated pharma drive value growth for converters.

By Packaging Format: Secondary Packs Streamline Fulfillment

Secondary packaging represented 45.24% of India paper and paperboard packaging market share in 2025 and is expected to grow at a 7.85% CAGR through 2031. Omnichannel retailers standardize shipper sizes so automated sorters handle mixed-SKU orders without stoppages. Quick-commerce dark stores under 4,000 sq ft rely on knock-down boxes that pop open in seconds and nest flat when empty, conserving limited aisle space. Right-sized shippers also reduce void fill, lowering freight costs and improving eco-scores on retailer dashboards.

Primary packs still communicate brand identity and meet barrier performance needs, with coated boards replacing multilayer plastic in snacks and impulse foods. Tertiary packs such as pallet wraps remain commoditized, yet upcoming QR-code mandates spur limited demand for data-rich outer wraps. Converters installing inline digital printers can embed batch-level codes without extra handling steps, earning service premiums. As fulfillment models evolve, secondary format innovation stays crucial to efficiency gains across supply chains.

Geography Analysis

Western and southern coastal states dominate fiber inflows because ports at Mundra, Kandla, JNPT and Chennai handle nearly all imported waste paper. Gujarat and Tamil Nadu therefore house India’s densest converter clusters, serving FMCG factories located within 150 km of port gates. Integrated mills in Maharashtra leverage proximity to brand headquarters in Mumbai and Pune, shortening design-to-market cycles for new SKUs.

Punjab, Haryana, and Uttar Pradesh provide abundant wheat straw and rice husk, which are consumed by new agro-residue pulp lines. This aligns with efforts to mitigate stubble burning and ensure fiber security. Inland states without port access, such as Chhattisgarh and Madhya Pradesh, are shifting toward agro-based furnishes to avoid volatile bale prices, creating a north-central pulp corridor that counters the traditional west-coast bias.

Compliance readiness for QR-code traceability varies widely. Urban districts like Pune and Surat already pilot digital links between packaging batches and recycler receipts, whereas many rural blocks still build basic collection networks. Early-mover converters in metros gain preferred-supplier status for multinational brands, but tier-3 locations present greenfield potential for players willing to brave fragmented logistics, ensuring geographic diversification of the India paper and paperboard packaging market.

Competitive Landscape

The India paper and paperboard packaging market shows moderate fragmentation. ITC Limited and JK Paper Limited operate integrated pulp-to-carton chains, insulating margins against fiber and energy shocks that squeeze converters purchasing board on the spot market. Smurfit WestRock couples imported design know-how with localized right-sizing services for quick-commerce clients, reinforcing its value proposition beyond plain corrugated supply.

Automation is a key battleground. TCPL Packaging and Parksons Packaging each installed multi-color flexographic lines with inline foiling that slash changeover time, enabling profitable execution of cosmetics runs under 10,000 units. Sustainability certifications such as Forest Stewardship Council labels and ISO 22000 food-safety systems now influence tender awards, allowing credentialed suppliers to levy 5-8% premiums.

Cost inflation is driving consolidation, with several SME converters entering structured sale talks after energy and waste-paper spikes erased gross margins in 2024. Larger groups are focusing on tuck-in acquisitions that add territory coverage or specialized coatings. This indicates that market power will concentrate even as overall demand expands, shaping the future competitiveness of the India paper and paperboard packaging market.

India Paper And Paperboard Packaging Industry Leaders

Tetra-Pak India Private Limited

Oji India Packaging Private Limited

ITC Limited – Paperboards and Specialty Papers Division

Huhtamaki India Limited

Smurfit WestRock

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: SIG Combibloc’s aseptic carton plant in Ahmedabad reached full 4 billion-pack capacity after a EUR 90 million (USD 96 million) investment.

- October 2025: JK Paper Limited started a bleached chemi-thermomechanical pulp plant in Songadh, Gujarat, for USD 78 million, adding 75,000 t of high-brightness pulp.

- August 2025: TCPL Packaging Limited obtained ISO 22000 certification for its Gujarat food-contact board line.

- June 2025: Parksons Packaging Limited commissioned a seven-color flexographic press with inline foiling and embossing in Haryana.

India Paper And Paperboard Packaging Market Report Scope

The study tracks the demand for paper and paperboard packaging products like folding cartons, corrugated boxes, and others, which are frequently used for packaging food and beverage products, such as juices, milk, and cereals. There are numerous grades of paperboard packaging. Paperboard is the most common material used to make containers, like folding cartons. Paperboard requires pulping, optional bleaching, refining, sheet forming, drying, calendaring, and winding to manufacture paper.

The India Paper and Paperboard Packaging Market Report is Segmented by Material Grade (Virgin Fiber, Recycled Fiber, and Hybrid or Mixed Fiber), Product Type (Folding Cartons, Corrugated Packaging, Liquid Cartons, Paper Bags and Sacks, Rigid Boxes, and Other Product Types), End-User Vertical (Food and Beverage, Healthcare and Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Industrial and Automotive, and Other End-user Industries), and Packaging Format (Primary Packaging, Secondary Packaging, and Tertiary Packaging). The Market Forecasts are Provided in Terms of Value (USD).

By Material Grade

| Virgin Fiber |

| Recycled Fiber |

| Hybrid or Mixed Fiber |

By Product Type

| Folding Cartons |

| Corrugated Packaging |

| Liquid Cartons |

| Paper Bags and Sacks |

| Rigid Boxes |

| Other Product Types |

By End-User Vertical

| Food and Beverage |

| Healthcare and Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Industrial and Automotive |

| Other End-user Industries |

By Packaging Format

| Primary Packaging |

| Secondary Packaging |

| Tertiary Packaging |

| By Material Grade | Virgin Fiber |

| Recycled Fiber | |

| Hybrid or Mixed Fiber | |

| By Product Type | Folding Cartons |

| Corrugated Packaging | |

| Liquid Cartons | |

| Paper Bags and Sacks | |

| Rigid Boxes | |

| Other Product Types | |

| By End-User Vertical | Food and Beverage |

| Healthcare and Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Industrial and Automotive | |

| Other End-user Industries | |

| By Packaging Format | Primary Packaging |

| Secondary Packaging | |

| Tertiary Packaging |

Key Questions Answered in the Report

How big is the India paper and paperboard packaging market in 2026?

The market stands at USD 14.54 billion in 2026 and is projected to reach USD 19.57 billion by 2031.

Which segment grows the fastest through 2031?

Liquid cartons are forecast to expand at a 7.63% CAGR as dairy processors adopt ambient packaging.

Why are hybrid fiber boards gaining popularity?

They blend agro-residue virgin pulp with recycled furnish, delivering needed strength while meeting recycled-content mandates and avoiding anti-dumping duties.

What drives secondary packaging demand?

Omnichannel and quick-commerce fulfillment centers standardize shipper sizes for automated sortation, pushing secondary packs to a 7.85% CAGR.

How does the single-use plastic ban affect paper packaging?

The ban positions paper as the default substitute for carry bags and service ware, unlocking new volume for kraft bags and molded-pulp trays.

Page last updated on: