Promotional Scented Paperboard Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

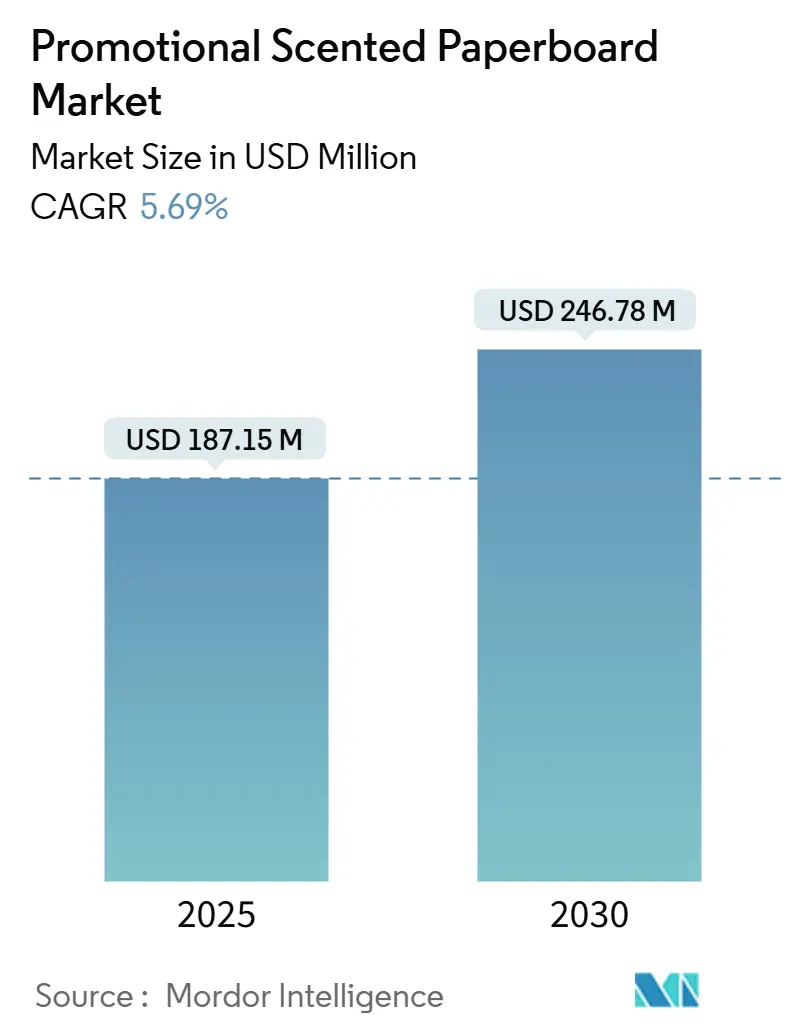

| Market Size (2025) | USD 187.15 Million |

| Market Size (2030) | USD 246.78 Million |

| Growth Rate (2025 - 2030) | 5.69% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Promotional Scented Paperboard Market Analysis by Mordor Intelligence

The promotional scented paperboard market size reached USD 187.15 million in 2025 and is projected to climb to USD 246.78 million by 2030, translating into a 5.69% CAGR over the forecast period. Robust demand stems from brand-owner efforts to create tactile, multisensory interactions that stand out in media-rich retail environments, while e-commerce players apply fragrance inserts to improve unboxing satisfaction and curb product returns. Sustainability legislation, especially Europe’s plastic-free sampling mandate, is accelerating the migration from polymer sachets to recyclable fiber substrates that carry encapsulated aromas.[1]Publications Office of the European Union, “Regulation (EU) 2025/40 on Packaging and Packaging Waste,” eur-lex.europa.eu Parallel advances in solvent-free micro-encapsulation bring down environmental footprints and support scale manufacturing efficiencies. Competitive intensity is rising as vertically integrated paperboard producers leverage broad converting networks, whereas specialist fragrance-sampler firms focus on high-margin, short-run jobs for luxury and direct-to-consumer brands.

Key Report Takeaways

- By coating technology, the promotional scented paperboard market size for the digital press fragrance capsules is projected to grow at a 6.37% CAGR between 2025-2030.

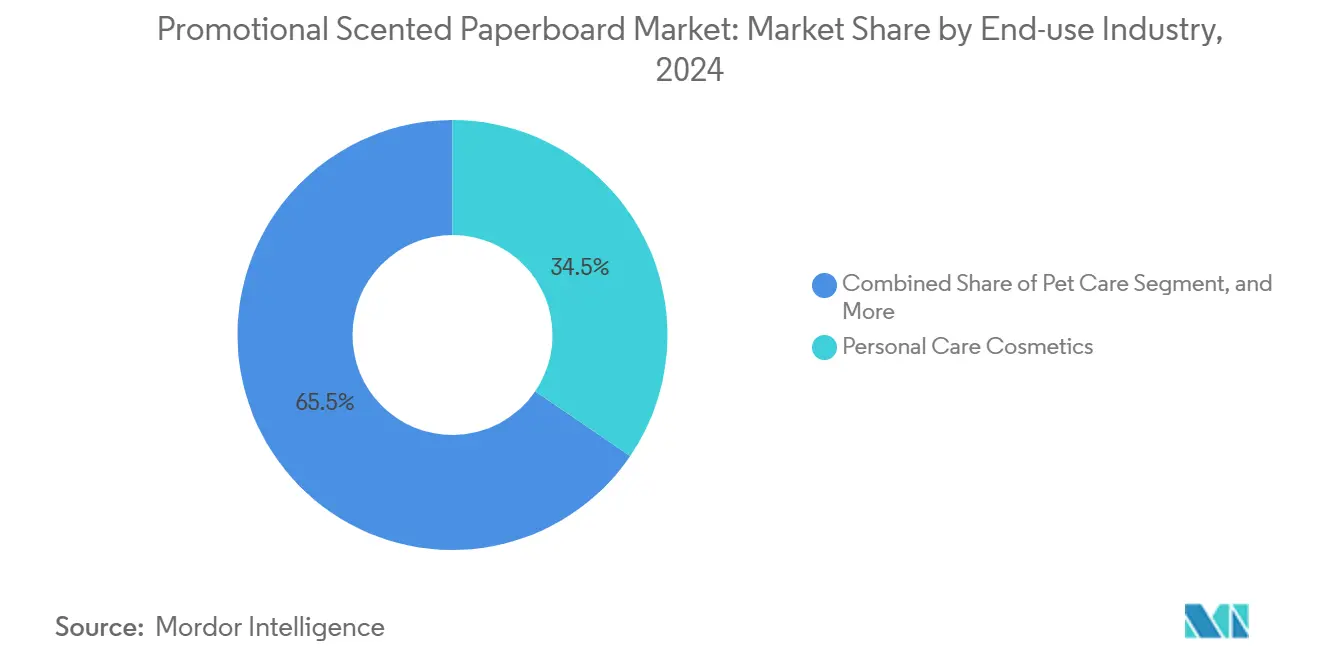

- By end-use industry, personal care and cosmetics captured 34.52% of the promotional scented paperboard market share in 2024.

- By distribution channel, the promotional scented paperboard market size for the online print platforms is projected to grow at a 6.54% CAGR between 2025-2030.

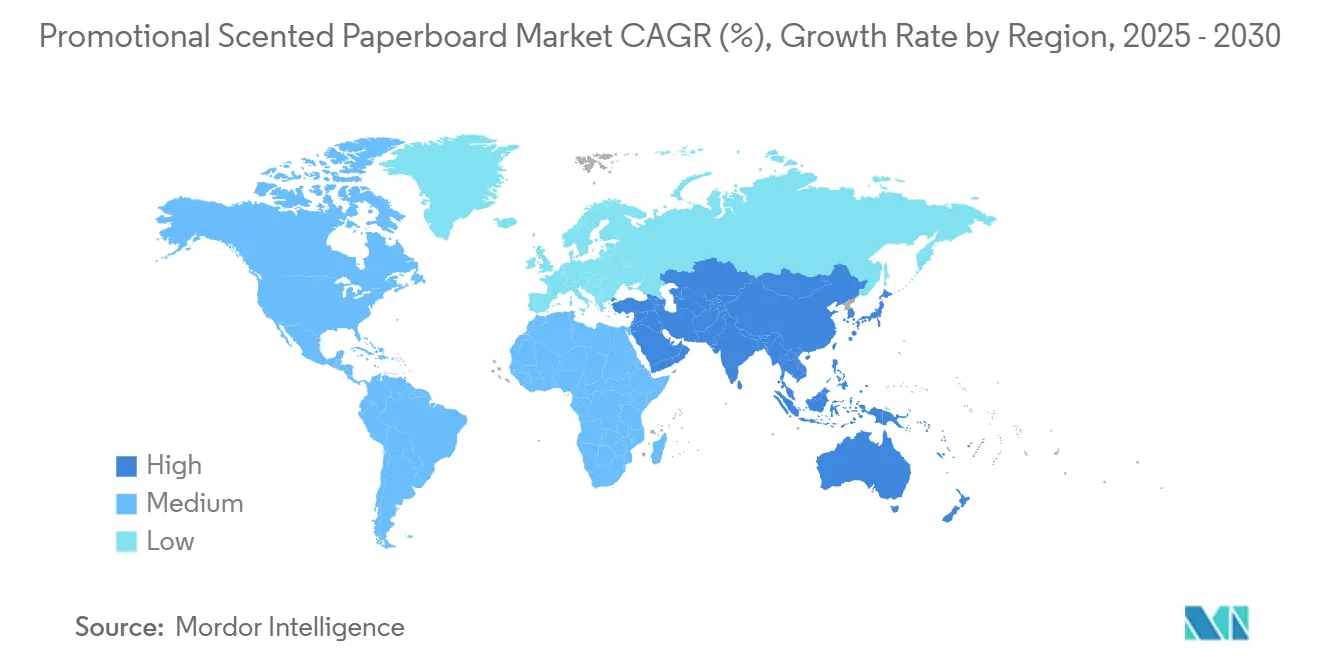

- By geography, Europe captured 33.18% of the promotional scented paperboard market share in 2024.

Global Promotional Scented Paperboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for multisensory marketing in saturated FMCG categories | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| E-commerce brands using scented inserts to reduce product return rates | +0.8% | Global, led by Asia-Pacific and North America | Short term (≤ 2 years) |

| Rapid adoption of solvent-free micro-encapsulation coatings | +0.6% | Europe and North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Brand-owner compliance with plastic-free sampling mandates (EU) | +0.4% | Europe primary, spillover to other developed markets | Long term (≥ 4 years) |

| Programmatic printing enabling SKU-level fragrance versioning | +0.3% | North America and Europe, gradual Asia-Pacific adoption | Long term (≥ 4 years) |

| Growing availability of bio-based aroma encapsulants | +0.2% | Global, with early adoption in Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Multisensory Marketing in Saturated FMCG Categories

Intensifying brand competition in mature consumer markets is pushing marketers to exploit the neurological power of scent. Controlled studies show that olfactory stimuli prompt faster recall and deeper emotional engagement than visual cues alone, a benefit that lifts direct-mail response rates and strengthens brand recall. Scented paperboard therefore acts as a physical media bridge, bringing digital-first brands into the consumer’s home and prolonging attention spans that once belonged to magazine spreads. Luxury labels in personal care and fine spirits champion the format as a premium touchpoint that aligns with their experiential branding ethos. Consequently, the promotional scented paperboard market is attracting R&D investment into finer capsule dispersion and color-accurate printable coatings that maintain graphics integrity while delivering consistent fragrance release. The approach also dovetails with omnichannel campaigns because the insert can carry QR codes that link offline sensory moments with online conversion paths.

E-commerce Brands Using Scented Inserts to Reduce Product Return Rates

High return ratios erode profitability for online sellers, particularly in beauty and fashion where sensory mismatch drives dissatisfaction. Peer-reviewed research finds that premium packaging signals quality and lowers the likelihood of returns by moderating consumer expectations.[2]Carl Marcus Wallenburg et al., “On Packaging and Product Returns in Online Retail—Mailing Boxes or Sending Signals?” Journal of Business Logistics, onlinelibrary.wiley.com Fragrant paperboard inserts amplify this effect by delivering the intangible scent aspect otherwise absent from virtual shopping. Subscription box providers apply seasonal fragrance cards that double as loyalty coupons, turning shipping expenses into revenue-generating engagement tools. Reduced reverse-logistics costs and improved customer lifetime value create a quantifiable ROI that sustains adoption even when per-unit packaging costs are higher. Fast-growing Asian marketplaces are piloting capsule-on-demand printing so sellers can rotate scents monthly without carrying large inventories, supporting agile merchandising calendars.

Rapid Adoption of Solvent-Free Micro-encapsulation Coatings

Regulatory pressure on volatile organic compounds (VOCs) is prompting printers to replace solvent carriers with water or UV-curable systems. Microfluidic encapsulation now produces monodisperse capsules that embed fragrance oils within hydrophilic shells, minimizing evaporation and improving shelf stability. Energy savings arise because ovens for solvent flash-off become redundant, while worker exposure to hazardous emissions falls sharply, lowering compliance and insurance costs. European converters were early adopters due to strict air-quality directives, but the technology is spilling into North America and Asia-Pacific as sustainability becomes a brand equity factor. Production lines equipped with closed-loop viscosity sensors ensure uniform lay-down weights, enabling cost-effective runs for mass personal-care sachets and boutique gift cards alike. Consequently the promotional scented paperboard market gains environmental credentials without compromising olfactory performance.

Brand-Owner Compliance with Plastic-Free Sampling Mandates (EU)

Regulation (EU) 2025/40 obliges all packaging placed on the European market to be recyclable by 2030 and sets recycled-content thresholds that conventional plastic sachets cannot meet. Fragrance, cosmetics, and detergent makers are replacing single-use polymers with fiber substrates coated in biodegradable encapsulants. The directive’s harmonized labeling scheme eases cross-border distribution and simplifies audits, encouraging multinational brands to standardize on scented paperboard formats for pan-regional campaigns. Converter investments in curtain-coating lines and precision die-cutting machines aim to scale production before the 2030 compliance deadline. Spill-over effects are appearing in North America and parts of Asia where retailers adopt voluntary plastic-reduction pledges that mirror EU rules, further enlarging the promotional scented paperboard market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining magazine circulation limiting legacy sampling volumes | -0.7% | Global, most severe in North America and Europe | Short term (≤ 2 years) |

| Supply-side volatility in natural aromatic feedstocks | -0.5% | Global, with acute impact in regions dependent on imports | Medium term (2-4 years) |

| Occupational exposure limits for aldehydes tightening | -0.4% | North America and Europe, expanding globally | Long term (≥ 4 years) |

| Limited recyclability of heavily varnished boards | -0.3% | Europe and developed markets with strict recycling mandates | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Declining Magazine Circulation Limiting Legacy Sampling Volumes

Print magazine readership continues to erode as advertisers pivot to digital channels. The contraction removes a distribution mainstay that once delivered millions of fragrance strips each month, thereby compressing baseline run-rates for coated paperboard converters. Employment data show persistent downsizing in printing and publishing occupations, confirming structural change. Although publishers experiment with augmented-reality covers and special-edition inserts, the aggregate volume shortfall will not reverse. Fragrance and luxury brands are reallocating sampling budgets toward direct mail, pop-up stores, and e-commerce packaging, activities that fragment order sizes and raise logistical complexity. Overcapacity risk looms for presses configured solely for high-volume magazine insert work, spurring consolidation and asset redeployment.

Supply-Side Volatility in Natural Aromatic Feedstocks

Essential oils such as lavender, rose, and sandalwood depend on climatic conditions and geopolitical stability in key producing regions. Extreme weather events and export restrictions impose unpredictable cost spikes that ripple through the capsule formulation budget. Blockchain-enabled traceability platforms improve transparency but also add compliance costs as suppliers document origin, fair-trade status, and carbon footprints. Synthetic or biotech-fermented aroma molecules promise supply security, yet regulatory approvals and consumer perception hurdles slow their penetration. Large integrated players hedge risk through multi-origin procurement and aroma competence centers, whereas smaller converters face margin squeeze and may shift toward standardized fragrance libraries with more predictable availability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Coating Technology: Digital Innovation Drives Customization

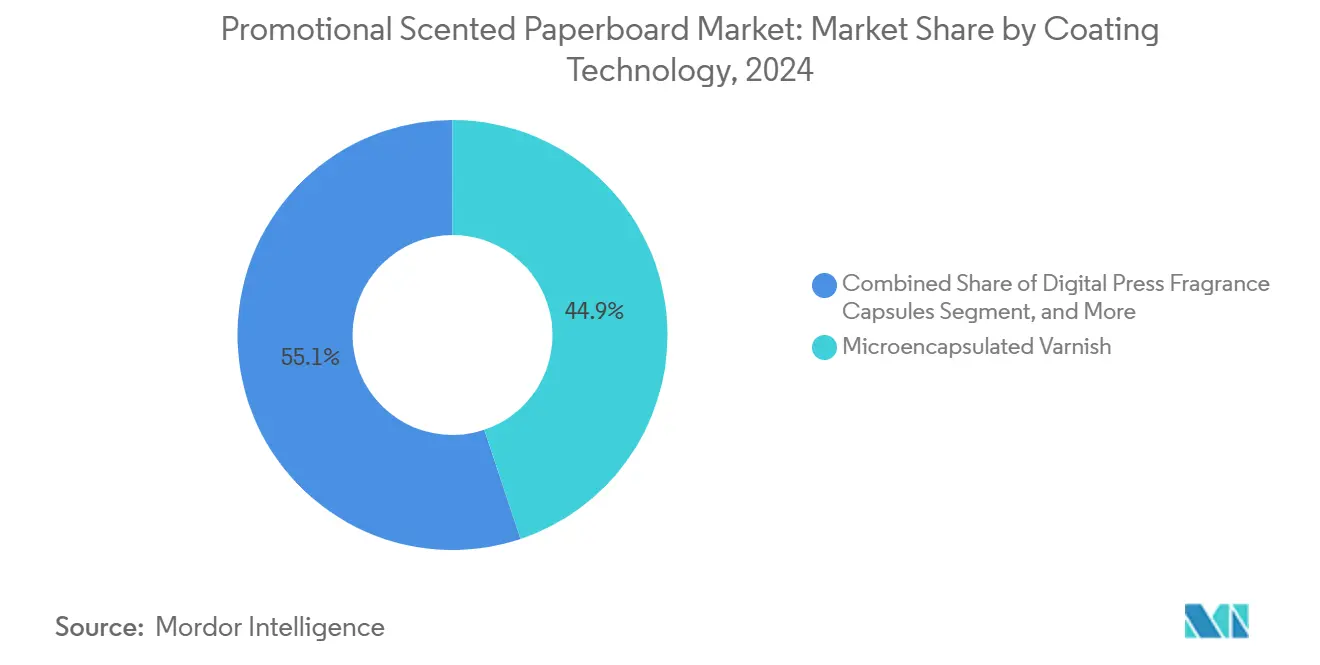

Microencapsulated varnish retained 44.86% of the promotional scented paperboard market share in 2024 because its proven coat-weight consistency and compatibility with offset presses support high-volume catalog, direct-mail, and retail display jobs. The segment’s scale economies keep unit costs favorable, anchoring the promotional scented paperboard market in mass FMCG campaigns. Digital press fragrance capsules are on track for a 6.37% CAGR to 2030, stimulated by the brand's need for SKU-level scent versioning and lower minimum order quantities. The promotional scented paperboard market size allocated to digital platforms is increasing as agile manufacturing replaces monolithic press runs for seasonal promotions.

Programmatic inkjet arrays jet fragrance micro-particles only where needed, cutting raw material waste and enabling variable scent placement within the same sheet. Water-based and UV flexo coats fill niches demanding food-contact compliance or ultra-fast line speeds, while scratch-and-sniff offset inks remain relevant for coupon books and children’s publications because of their playful consumer interaction. Continuous R&D in shell morphology and binder chemistry enhances fragrance longevity, allowing luxury brands to confidently deploy scented direct marketing without the risk of premature scent fade.

By Fragrance Type: Woody Scents Challenge Floral Dominance

Floral notes led the frame with 27.21% of promotional scented paperboard market size in 2024, supported by broad cross-gender acceptance and well-established essential oil supply chains. Woody and musky accords, however, are forecast to compound at 6.28% annually, propelled by demand for gender-neutral and premium positioning. Fruity compositions retain resonance in food and beverage promotions, whereas herbal and green variants satisfy wellness-centric consumers. Gourmand profiles serve confectionery and coffee gifting, tightening the emotional association between aroma and taste.

Sequential-release capsule architectures now enable top notes to disperse immediately while base notes unfold hours later, matching consumer curiosity with enduring memory cues. EU Regulation 2023/1545 lists 56 additional allergens that trigger labelling when thresholds are breached, encouraging formulators to swap troublesome molecules for hypoallergenic synthetics.[3]European Commission, “Regulation 2023/1545,” eur-lex.europa.euConsequently, encapsulation partners are offering regulatory screening as a service, helping brands navigate compliance, extend market access, and maintain fragrance creativity.

By End-Use Industry: Luxury Segments Outpace Traditional Applications

Personal care and cosmetics generated 34.52% of promotional scented paperboard market size in 2024, still functioning as the anchor vertical because fragrance discovery is integral to product trial. Luxury goods and publishing are advancing at a 6.43% CAGR, despite falling magazine volumes, as high-spend categories harness the exclusivity of limited-edition scented inserts mailed directly to priority clients. Food and beverage companies employ flavor-cognate aromas to reinforce taste cues in holiday promotions. Household-cleaning brands experiment with linen and citrus scents that communicate freshness upon shelf inspection.

Apparel labels pilot aromatic hang-tags and lookbooks that evoke brand narratives, while pet-care suppliers test odor-masking packaging. These emerging use cases diversify revenue streams and reduce reliance on legacy printed media. Brands value data capture opportunities such as embedded NFC chips that track consumer interaction, uniting olfactory and digital analytics within a single substrate.

By Distribution Channel: Digital Platforms Reshape Traditional Models

Direct sales via integrated printers and converters retained a 48.34% share of the promotional scented paperboard market size in 2024 because complex projects often require end-to-end design, coating, and die-cut expertise. Online print portals, expected to clock a 6.54% CAGR, democratize access for small and medium brands by offering design templates and transparent pricing. Real-time quotation engines slash pre-press lead times, enabling designers to upload artwork and fragrance choices in hours rather than weeks.

Specialty fragrance samplers cater to luxury and indie cosmetics, where low defect tolerances and hand finishing justify premium service fees. Hybrid models are appearing in which converters operate branded e-commerce front ends while fulfilling orders in automated plants. Geolocation algorithms pair customers with the nearest certified coating line, cutting freight emissions and lead times, reinforcing sustainability narratives that are central to the promotional scented paperboard market proposition.

Geography Analysis

Europe retained 33.18% revenue leadership in 2024, underwritten by stringent circular-economy rules and robust luxury-goods clusters in France, Italy, and Germany. Brands there allocate larger budgets to sensory sampling, and converters benefit from regional design houses seeking sustainable substrates. Northern European regulators’ scrutiny of recyclability pushes coating suppliers to accelerate water-based barrier innovations, ensuring the promotional scented paperboard market stays aligned with upcoming fiber-yield benchmarks.

Asia-Pacific, progressing at a 6.15% CAGR, is bolstered by rising disposable incomes, booming cross-border e-commerce, and social-commerce influencers who showcase sensory unboxing rituals. China’s fast-fashion and K-beauty sectors integrate scent cards within parcel liners, engaging customers post-checkout. Regional converters add capacity in Vietnam and Indonesia where labor and pulp costs remain competitive, shortening supply chains to East Asian brand owners and mitigating freight risk.

North America’s growth plateaus yet remains significant as direct-to-consumer brands prioritize customer retention. The United States advances allergen-labelling frameworks similar to EU rules, driving early adoption of compliant encapsulants. Canada’s Extended Producer Responsibility statutes nudge retailers to co-invest in take-back programs that favor recyclable paperboard over composite plastics. Latin American markets, notably Brazil and Mexico, observe heightened adoption as regional cosmetics champions replicate European sustainability playbooks. The Middle East and Africa are nascent but promising; luxury-mall developments in the Gulf spur niche fragrance sampling in high-end retail.

Competitive Landscape

The promotional scented paperboard market exhibits moderate concentration, with the combined share of the five largest participants holding around 45%. Smurfit Westrock’s July 2024 merger fused extensive boxboard assets with fragrance-compatible coating lines, delivering procurement scale and global distribution reach. Graphic Packaging’s USD 8.8 billion 2024 revenue underpins R&D in solvent-free flexo coatings and digital finishing modules that attract FMCG contracts.

Arcade Beauty and Scentisphere differentiate through fragrance formulation heritage and boutique prototyping services catering to prestige cosmetic houses. Clearwater Paper’s 2024 acquisition of Graphic Packaging’s Augusta mill signals continuing industry consolidation aimed at recycled-fiber leadership. Mativ Holdings leverages efficiency gains to enter specialty aroma substrates for electronics packaging, diversifying end-market exposure. Competitive advantages increasingly rest on regulatory foresight, life-cycle assessment capabilities, and the speed with which companies can switch fragrance payloads in response to campaign analytics.

Strategic initiatives in 2024-2025 include capital expenditure on closed-loop ventilation for aldehyde mitigation, investment in bio-polymer capsule startups, and partnerships with digital-press makers to embed scent modules within high-speed lines. Intellectual-property portfolios around microfluidic capsule fabrication give early movers a defensible edge. Yet rising customer demand for transparency presses large converters to open-source certain formulations or adopt blockchain for ingredient traceability, leveling some competitive differentials.

Promotional Scented Paperboard Industry Leaders

Smurfit Westrock PLC

Graphic Packaging International, LLC

Arcade Beauty, Inc.

Scentisphere LLC

Edelmann GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Smurfit Westrock reported Q4 2024 net sales of USD 7.5 billion with adjusted EBITDA of USD 1,166 million, completing a USD 400 million synergy program that strengthens capacity across global paperboard applications.

- December 2024: FDA issued final guidance on cosmetic facility registration and product listing under MoCRA 2022, introducing new compliance steps for scented paperboard sampling.

- October 2024: EU Regulation 2023/1545 set phased fragrance-allergen labelling deadlines of Jul 2026 and Jul 2028, guiding scented sampling compliance.

- September 2024: EPA released an occupational exposure assessment for formaldehyde, foreshadowing tighter factory limits for fragrance coating lines.

Global Promotional Scented Paperboard Market Report Scope

| Microencapsulated Varnish |

| Scratch-and-Sniff Offset Ink |

| Encapsulated UV Flexo Coating |

| Water-based Aroma Coating |

| Digital Press Fragrance Capsules |

| Floral |

| Fruity |

| Herbal and Green |

| Gourmand |

| Woody and Musky |

| Personal Care and Cosmetics |

| Food and Beverage |

| Household and Homecare |

| Pet Care |

| Luxury goods and Publishing (magazine inserts) |

| Apparel and Footwear |

| Direct (Printers and Convertors) |

| Specialty Fragrance Samplers |

| Online Print Platforms |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Coating Technology | Microencapsulated Varnish | ||

| Scratch-and-Sniff Offset Ink | |||

| Encapsulated UV Flexo Coating | |||

| Water-based Aroma Coating | |||

| Digital Press Fragrance Capsules | |||

| By Fragrance Type | Floral | ||

| Fruity | |||

| Herbal and Green | |||

| Gourmand | |||

| Woody and Musky | |||

| By End-use Industry | Personal Care and Cosmetics | ||

| Food and Beverage | |||

| Household and Homecare | |||

| Pet Care | |||

| Luxury goods and Publishing (magazine inserts) | |||

| Apparel and Footwear | |||

| By Distribution Channel | Direct (Printers and Convertors) | ||

| Specialty Fragrance Samplers | |||

| Online Print Platforms | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of promotional scented paperboard worldwide?

The promotional scented paperboard market size stands at USD 187.15 million in 2025.

How fast is demand for scented paperboard expected to grow?

Revenue is projected to rise at a 5.69% CAGR, reaching USD 246.78 million by 2030.

Which end-use category spends the most on scented paperboard today?

Personal care and cosmetics currently generate 34.52% of sales.

Why are e-commerce brands adding fragrance inserts?

Inserts enhance the unboxing experience and have been shown to lower product return rates, improving profitability.

What regional market is expanding the quickest?

Asia-Pacific leads with a forecast 6.15% CAGR through 2030 due to rising online retail and middle-class spending.

How will EU plastic-free rules influence sampling?

Regulation (EU) 2025/40 obliges recyclable formats, steering brands toward paperboard solutions that comply with 2030 targets.

Page last updated on: