Fitness And Recreational Sports Centers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

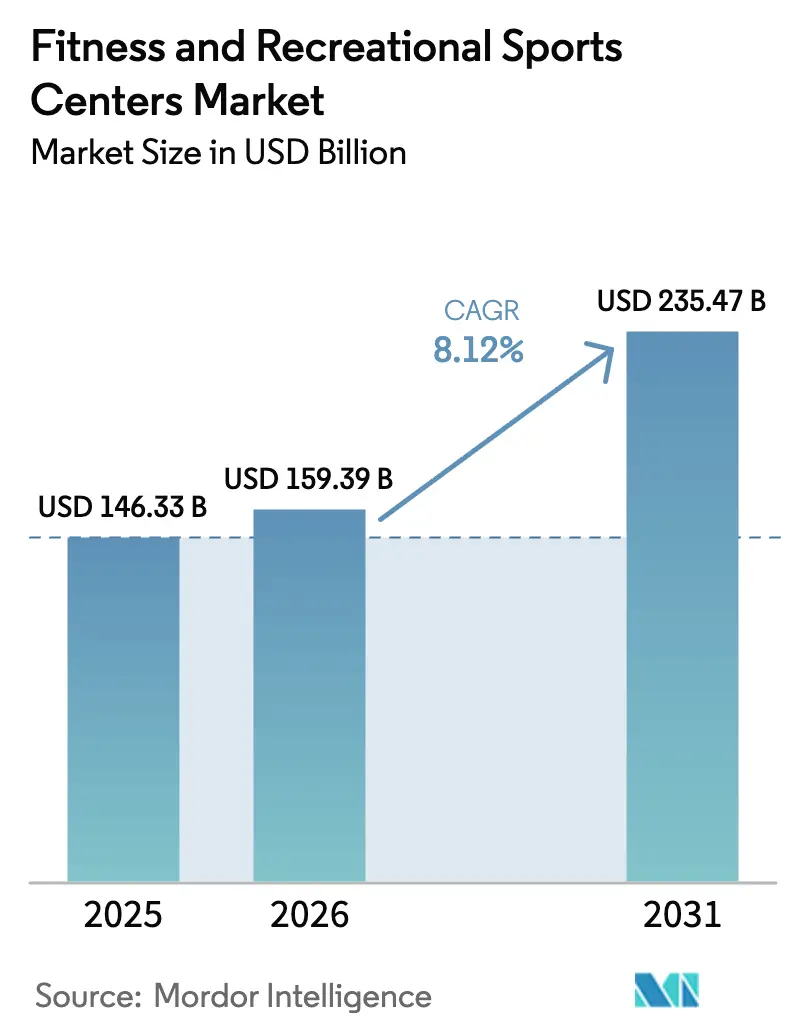

| Market Size (2026) | USD 159.39 Billion |

| Market Size (2031) | USD 235.47 Billion |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

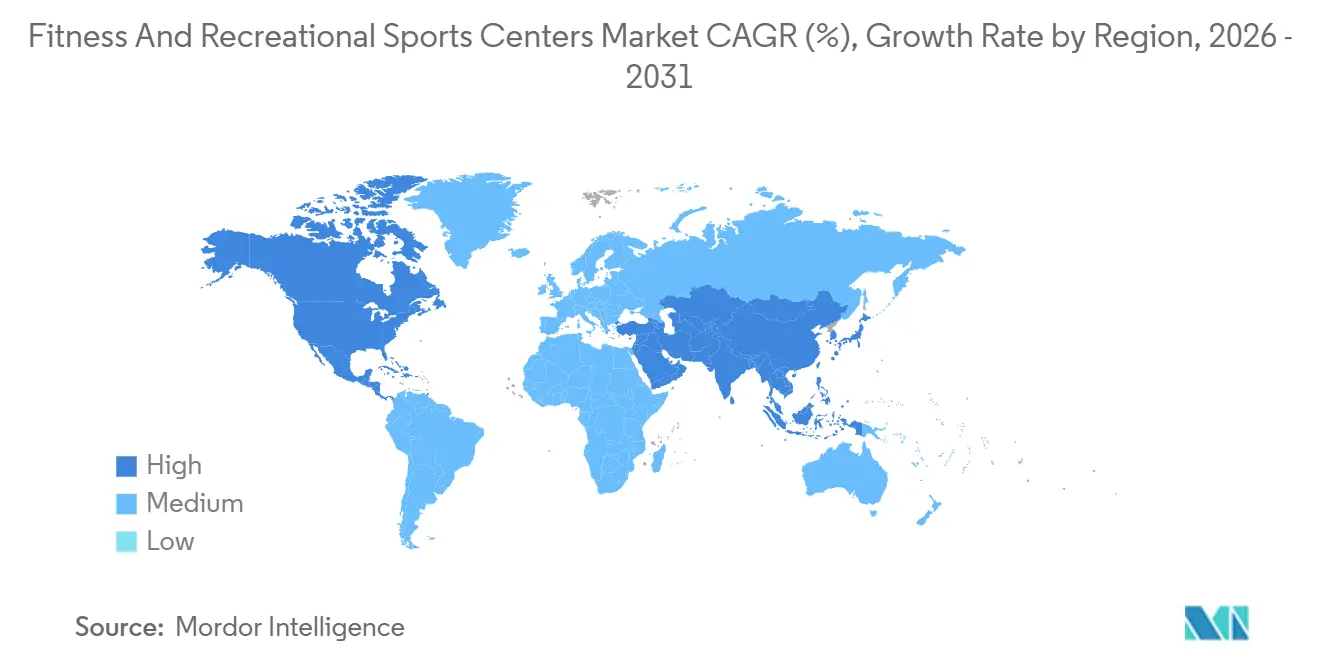

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fitness And Recreational Sports Centers Market Analysis by Mordor Intelligence

The Fitness and Recreational Sports Centres Market size was valued at USD 146.33 billion in 2025 and estimated to grow from USD 159.39 billion in 2026 to reach USD 235.47 billion by 2031, at a CAGR of 8.12% during the forecast period (2026 to 2031). The robust expansion stems from consumers directing a growing share of household budgets toward preventive health, spurred by government mandates that reward regular physical activity. Operators that certify member engagement now tap quasi-public revenue streams, shielding cash flows from cyclical shocks. Format fragmentation is sharpening competitive tactics; boutique studios command premium pricing, while big-box chains defend scale through budget memberships. Digital integration is turning facilities into data platforms, enabling algorithmic capacity planning and outcome-based pricing. The parallel growth of corporate wellness programs and senior preventive care is widening procurement opportunities as employers and insurers co-fund utilization-linked contracts.

Key Report Takeaways

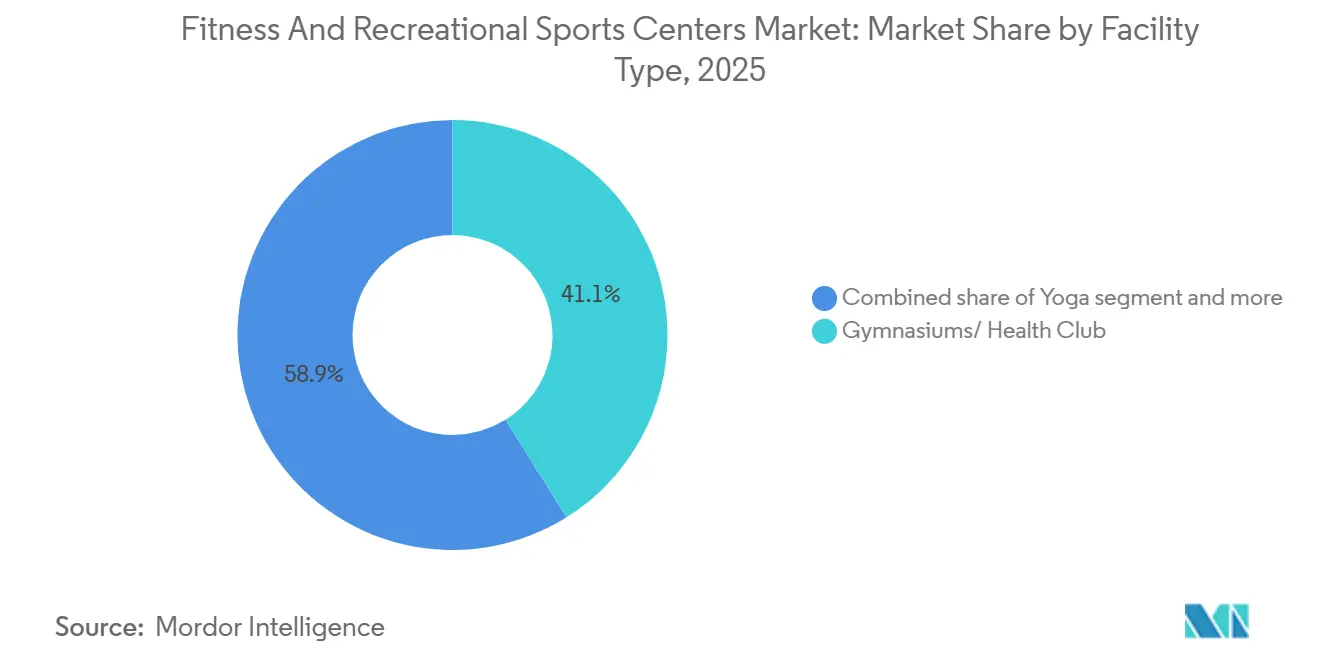

- By facility type, gymnasiums and health clubs captured 41.15% of the fitness and recreational sports centers market share in 2025, whereas yoga studios are on track to post an 8.53% CAGR to 2031.

- By end-user, adults generated 46.26% of revenue in 2025, while the kids and children segment is projected to expand at a 9.24% CAGR through 2031.

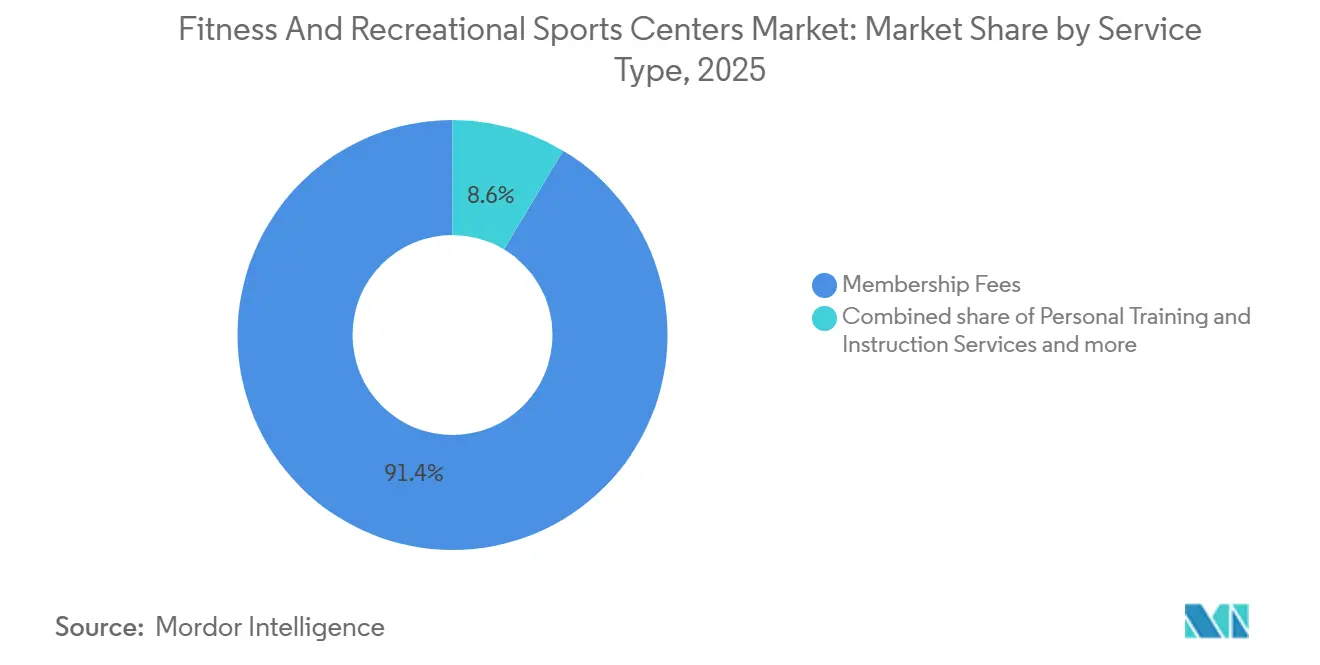

- By service type, memberships contributed 91.35% of revenue in 2025, yet personal training and instruction are advancing at an 8.75% CAGR to 2031.

- By geography, North America led with a 38.44% share in 2025; Asia-Pacific is forecast to accelerate at a 9.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fitness And Recreational Sports Centers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Health and Wellness Awareness | +1.8% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Growth of Boutique and Specialized Formats | +1.5% | North America, Europe, Asia-Pacific urban hubs | Short term (≤ 2 years) |

| Expansion of Corporate Wellness Programs | +1.2% | North America, Europe, Singapore, Japan, Australia | Medium term (2-4 years) |

| Digital Integration and Smart Fitness | +1.0% | Global, led by North America and Asia-Pacific tech centers | Short term (≤ 2 years) |

| Aging Population and Preventive Adoption | +0.9% | Europe, North America, Japan, South Korea | Long term (≥ 4 years) |

| Rising Participation in Amateur Sports | +0.7% | Asia-Pacific, South America, Middle East and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Health and Wellness Awareness

Household spending patterns are shifting as preventive healthcare increasingly aligns with curative medical expenses, repositioning fitness centers from optional lifestyle services to essential health infrastructure. The Centers for Disease Control and Prevention (CDC) Active People, Healthy Nation initiative aims to engage 27 million participants by 2027, encouraging gym operators to adopt biometric tracking technologies to support compliance and public health reporting[1]Source: Centers for Disease Control and Prevention, “Active People, Healthy Nation,” CDC.GOV. In 2024, the World Health Organization estimated that physical inactivity costs the global economy USD 300 billion each year in healthcare spending, prompting governments in countries such as Germany, Singapore, and Australia to test tax credits tied to verified gym attendance[2]Source: World Health Organization, “Physical Activity,” WHO.INT. This policy shift effectively reframes membership fees as quasi-public funding, reducing operators’ dependence on discretionary consumer spending and helping stabilize revenues during economic slowdowns.

Growth of Boutique and Specialized Fitness Formats

Boutique fitness studios are capturing disproportionate revenue growth by unbundling the traditional gym model into instructor-led, format-specific classes that command price premiums of 40–60% over big-box memberships. Xponential Fitness operated 3,150 studios globally as of Q3 2024 and reported system-wide sales of USD 405.8 million, a 9% increase year over year. Brands such as Club Pilates, CycleBar, and StretchLab target distinct biomechanical niches. Its franchise model shifts real estate risk to licensees while centralizing instructor certification and data-driven class scheduling, enabling rapid expansion without balance-sheet strain. Yoga studios are projected to grow at an 8.53% CAGR through 2031, the fastest among facility types, as corporate wellness programs increasingly pair mindfulness with strength training to address burnout. At the same time, F45 Training and Orangetheory Fitness have scaled HIIT formats by integrating wearable heart-rate monitors that gamify performance, using real-time data and leaderboards to drive engagement, retention, and network effects.

Expansion of Corporate Wellness Programs

Employers are incorporating fitness subsidies into total compensation packages to mitigate healthcare cost inflation and reduce absenteeism, a trend that helps stabilize facility utilization during economic volatility. PwC's 2024 workforce survey found that 68% of multinational corporations now offer gym reimbursements or on-site fitness facilities, up from 42% in 2020. Fortune 500 companies allocate an average of USD 800 per employee annually to wellness benefits. Life Time Fitness reported that corporate partnerships accounted for 22% of new memberships in 2024, with contracts structured around utilization thresholds that tie pricing to documented employee engagement rather than flat per-capita fees. This shift from headcount-based to outcome-based pricing rewards operators who invest in biometric tracking and digital check-in systems that generate audit-ready attendance data. Singapore's Health Promotion Board expanded its corporate wellness grant in 2025, covering up to 50% of fitness program costs for employers who demonstrate measurable reductions in employee body mass index or blood pressure metrics[3]Source: Health Promotion Board, “Corporate Wellness Grants,” HPB.GOV.SG. Such public-private co-funding models are emerging in Japan, Australia, and the Netherlands, creating procurement tailwinds for chains that can navigate multi-stakeholder contracting and compliance reporting.

Digital Integration and Smart Fitness Adoption

Connected equipment and wearable integration are reshaping gyms into data-driven platforms, allowing operators to monetize performance insights while tailoring retention strategies at the individual level. In 2024, Planet Fitness announced plans to retrofit 1,200 locations with IoT-enabled cardio equipment compatible with Apple Watch, Fitbit, and Garmin, enabling members to track workouts across locations and receive algorithm-generated exercise recommendations. This level of interoperability helps address a major cause of churn, uneven equipment access, by supporting dynamic capacity management and nudging members toward underutilized time slots through push notifications. Peloton has similarly shifted its focus from hardware-led growth to B2B partnerships, installing connected bikes and treadmills in 800 hotel gyms and 200 corporate fitness centers by mid-2024 to generate recurring software licensing revenue amid softer direct-to-consumer demand. Boutique studios are also adopting smart mirrors and AI-based form-correction tools, which provide real-time biomechanical feedback, supporting premium pricing and reducing injury-related liability. At the same time, biometric check-in systems using facial recognition or fingerprint scans are being integrated with payment platforms, streamlining onboarding and cutting front-desk labor costs by 30–40%, a meaningful margin advantage in high-rent urban locations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Investment Requirements | -1.1% | Global, most acute in high-rent urban markets | Short term (≤ 2 years) |

| Limited Availability of Skilled Trainers and Staff | -0.8% | North America, Europe, Asia-Pacific developed markets | Medium term (2-4 years) |

| Regulatory and Licensing Challenges | -0.6% | Europe, Asia-Pacific, South America | Medium term (2-4 years) |

| Seasonal and Regional Fluctuations in Demand | -0.4% | North America, Europe, seasonal tourism markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Investment Requirements

High upfront facility launch costs, covering real estate, equipment, and technology infrastructure, create significant barriers to entry, concentrating market share among well-capitalized chains and limiting expansion into secondary cities. A mid-sized gym spanning 10,000–15,000 square feet typically requires an initial investment of USD 500,000 to USD 1.5 million, with cardio and strength equipment accounting for roughly 30-40% of the total costs, based on industry benchmarks from equipment manufacturers and real estate consultants. While boutique studios involve lower overall capital outlays, their per-square-foot costs are higher due to specialized requirements, such as flooring, mirrors, and audio systems. For example, a 2,000-square-foot yoga studio generally requires USD 150,000–300,000 in build-out capital. Long-term lease agreements in prime urban areas often span 10 years and include personal guarantees, exposing franchisees to sustained downside risk if membership growth falls short. Additional costs associated with smart-gym upgrades, including IoT-enabled equipment, biometric access systems, and integrated payment platforms, can add USD 100,000-250,000 to renovation budgets, making them difficult to justify for budget operators without clear evidence of improved retention. Although equipment financing and sale-leaseback models are becoming more common, interest-rate volatility in 2024–2025 has pushed borrowing costs higher, squeezing returns on new locations and slowing expansion plans for regional chains.

Regulatory and Licensing Challenges

Fragmented regulatory frameworks across countries impose significant administrative burdens and can slow market entry, especially for chains seeking multi-country expansion. Within the European Union, fitness facility standards vary widely: Germany mandates annual inspections by TÜV-certified auditors, France requires on-site CPR-trained staff throughout operating hours, and Spain enforces ventilation standards based on occupancy levels. ISO 9001 quality certifications are increasingly necessary for operators pursuing public-sector contracts or health insurance reimbursements, but the 12-18 month audit process and consulting fees of USD 20,000-50,000 often deter smaller, independent operators. In India, licensing requirements differ by state. Maharashtra demands fire-safety approvals that can take 6–9 months, while Karnataka requires environmental clearances for facilities over 5,000 square feet. In China, the General Administration of Sport ties operating licenses to instructor-to-member ratios (at least one certified trainer per 100 members) and mandates the presence of emergency medical equipment, such as automated external defibrillators, in facilities larger than 2,000 square meters, favoring operators with state backing. Liability insurance costs are also rising in North America and Europe, driven by litigation related to equipment injuries and lapses in supervision. For a mid-sized gym, annual premiums typically range from USD 10,000 to USD 30,000, adding to the financial burden of regulatory compliance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Facility Type: Boutique Formats Reshape Traditional Gym Dominance

Gymnasiums and health clubs held a 41.15% share of the market in 2025, driven by their ability to provide extensive equipment and multi-generational programming under one roof. Meanwhile, yoga studios are growing at an 8.53% CAGR through 2031, the fastest among facility types, as corporate wellness programs increasingly combine mindfulness training with traditional strength conditioning. Xponential Fitness, which franchises Club Pilates, CycleBar, StretchLab, and YogaSix, operated 3,150 studios globally by Q3 2024 and reported system-wide sales of USD 405.8 million, up 9% year over year, demonstrating how specialized formats support premium pricing and rapid franchise growth. Aerobic dance studios, including Zumba, barre, and dance cardio formats, are benefiting from TikTok-driven virality, where user-generated choreography videos spur trial memberships among Gen Z and millennial consumers. Handball facilities remain concentrated in Europe and South America, where municipal co-funding lowers operator capital requirements, while racquet sports are experiencing a resurgence, driven by pickleball’s 158% participation growth in the U.S. from 2020 to 2024, prompting operators to repurpose underutilized tennis courts (SFIA)[4]Source: Sports & Fitness Industry Association, “2024 Participation Report,” SFIA.ORG.

Swimming facilities are expanding in Middle Eastern markets, where extreme heat limits outdoor exercise. Saudi Arabia’s Vision 2030 sports strategy allocated USD 1.3 billion to aquatic center construction, aiming for 40% female participation in line with social-reform goals. Skating rinks face high energy costs for refrigeration, limiting profitability outside cold climates, yet operators in Canada and Scandinavia are maximizing utilization through multi-use programming such as hockey leagues, figure skating, and public sessions. The “Others” segment, including climbing gyms, trampoline parks, and functional-training studios, is attracting venture capital, with climbing gyms benefiting from the sport’s inclusion in the 2024 Paris Olympics, which boosted mainstream visibility. Planet Fitness, with 2,600 locations and 19.7 million members in Q3 2024, highlights the continued strength of low-cost, high-volume models. However, the company’s USD 1.1 billion revenue reflects average monthly dues of USD 10–25, limiting per-member profitability compared with boutique chains that can charge USD 150–300 per month.

By End-User: Pediatric Fitness Outpaces Adult Growth

The kids and children segment is expected to grow at a 9.24% CAGR through 2031, outpacing adult growth as municipalities introduce physical education alternatives and insurers pilot pediatric obesity-prevention reimbursement programs. Adults accounted for 46.26% of end-user revenue in 2025, driven by employer wellness subsidies and the increasing adoption of preventive fitness among older populations. However, youth programming is emerging as a key differentiator for operators seeking recession-resilient revenue streams. The CDC recommends 60 minutes of daily physical activity for children aged 6–17, yet only 24% of U.S. youth met this target in 2024, creating opportunities for school-gym partnerships and after-school programs. Life Time Fitness expanded its junior academy offerings in 2024, adding swim lessons, youth sports leagues, and STEM-integrated fitness camps with monthly fees ranging from USD 200 to USD 500, which is double the typical adult membership rate. The company also provides childcare that allows parents to work out.

Operators in the pediatric segment face stricter regulatory oversight, including mandatory background checks for instructors, child-to-staff ratios (typically 10:1 for ages 6-12), and facility requirements that separate youth zones from adult areas. India’s Fit India Movement prioritized school fitness infrastructure in 2024, allocating USD 150 million to upgrade 10,000 government schools with gym equipment and certified physical education teachers, creating opportunities for private operators to provide training and curriculum support. In Japan, declining birth rates have shifted focus toward senior programming, yet urban centers like Tokyo and Osaka are seeing a rise in boutique kids’ fitness studios offering parkour, martial arts, and obstacle-course training in response to parental demand for structured after-school activities. Growth in the adult segment is anchored by preventive fitness uptake among the 50-plus cohort, with operators incorporating telehealth consultations and chronic-disease management programs to capture Medicare and national health insurance reimbursements, allowing revenue streams to extend beyond traditional membership fees.

By Service Type: Personal Training Gains Share Amid Membership Commoditization

Membership fees accounted for 91.35% of service-type revenue in 2025, yet personal training and instructional services are growing at an 8.75% CAGR through 2031, reflecting consumers’ willingness to pay for outcome-focused programs as digital-only offerings diminish the value of equipment-access memberships. In North America, personal training sessions typically range from USD 50 to USD 150 per hour, while boutique studios offer small-group sessions (3–6 participants) at USD 30-60 per person to balance revenue with instructor capacity. Operators are increasingly integrating AI-powered form-correction tools and wearable technology to justify premium pricing, allowing trainers to manage larger client rosters without compromising personalized programming.

The “Other Service Type” segment, including nutrition counseling, physical therapy, spa treatments, and retail products such as apparel and supplements, is also expanding, providing non-dues revenue to offset membership commoditization. Equinox reported in 2024 that these ancillary services contributed 18% of total revenue, with in-house spa and nutrition offerings generating an average of USD 120 per member per month above base dues. Hybrid membership models, combining unlimited facility access with a set number of personal training sessions, are becoming more common, supported by algorithmic scheduling that maximizes trainer utilization and reduces idle time during off-peak hours. Certification bodies like NASM and ACE are expanding specialized credentials, covering areas such as pre- and post-natal fitness, sports-specific conditioning, and geriatric training, allowing trainers to charge higher rates and protect against commoditization (nasm.org; acefitness.org). Premium operators are increasingly adopting outcome-based pricing, where clients pay for measurable progress such as strength gains or body-composition changes rather than session time, creating margin upside for those investing in biometric tracking and data analytics.

Geography Analysis

North America accounted for 38.44% of the global market in 2025, driven by high per-capita gym spending, averaging USD 60-80 per month, and employer-sponsored wellness programs that help stabilize demand during economic uncertainty. The United States drives the bulk of regional revenue, with a clear split between low-cost operators, such as Planet Fitness, which charges USD 10–25 per month, and premium brands like Life Time, where monthly fees range from USD 150 to USD 300. In Canada, GoodLife Fitness operates more than 400 locations and is deepening its focus on corporate wellness partnerships. Meanwhile, in Mexico, growth is being seen in manufacturing centers such as Monterrey and Guadalajara, where multinational employers are subsidizing gym access to attract and retain skilled workers.

Europe presents a fragmented landscape, with fitness penetration differing sharply by country. The UK supports more than 7,000 gyms and around 11 million members, Germany maintains a robust health-club culture reinforced by employer wellness policies, and Southern European markets such as Spain and Italy are growing faster from a lower spending base as household incomes recover. Budget operators are gaining scale: PureGym runs over 500 locations across the UK and Europe with 24-hour, no-contract models, while Netherlands-based Basic-Fit expanded to more than 1,300 clubs across six countries by 2024, using centralized procurement and marketing to pressure independent operators. However, varying national regulations, ranging from Germany’s TÜV inspections to France’s staffing requirements and Spain’s ventilation standards, raise compliance costs and tend to favor larger chains with dedicated regulatory capabilities.

Asia-Pacific is the fastest-growing region, projected to expand at a 9.43% CAGR through 2031, driven by urbanization, rising incomes, and state-led investment in sports infrastructure. China anchors regional growth, supported by the State Council’s USD 687 billion sports industry target by 2025 and a base of more than 500 million regular exercisers, with operators benefiting from land-lease incentives near transit hubs. India’s fitness market reached USD 2.6 billion in 2024 and is growing 8–10% annually under the Fit India Movement, which links licensing to accessibility and air-quality standards. Japan’s USD 4 billion market emphasizes aging-population services, including fall-prevention programs tied to national health insurance reimbursements, while Australia’s AUD 3.1 billion industry is expanding functional training formats. In South America, Brazil’s market contracted in 2024 amid inflation and currency pressure, though Chile and Colombia are seeing steady middle-class demand via flexible pricing and hybrid models. The Middle East and Africa are benefiting from government-backed wellness initiatives, notably Saudi Arabia’s Vision 2030 investment in aquatic facilities and the UAE’s corporate wellness mandates, while growth in Africa remains concentrated in major urban centers such as Johannesburg and Cape Town due to infrastructure constraints elsewhere.

Competitive Landscape

The fitness and recreational sports centers market remains highly fragmented, with no single operator holding more than 5% of the global share. This structure leaves meaningful room for regional players to tailor programming to local preferences and secure favorable municipal real estate arrangements. Planet Fitness, with 19.7 million members across 2,600 locations in Q3 2024 and USD 1.1 billion in revenue, exemplifies the high-volume, low-touch model built on minimal staffing and low monthly fees. At the opposite end, Life Time serves 777,000 members through 172 luxury athletic resorts, generating USD 2.4 billion in revenue in 2023 by bundling personal training, spa services, childcare, and premium amenities that support monthly dues of USD 150 to USD 300.

Xponential Fitness occupies a middle ground through its franchise-led strategy, operating 3,150 studios globally and posting system-wide sales of USD 405.8 million in Q3 2024. While shifting real-estate risk to franchisees, it retains centralized control over instructor certification and data-driven class scheduling, allowing for efficient scaling without heavy balance-sheet exposure. Technology is increasingly shaping competitive advantage. Planet Fitness’s rollout of IoT-enabled cardio equipment in 2024, compatible with Apple Watch, Fitbit, and Garmin devices, aims to reduce churn by allowing members to track workouts across locations and by enabling operators to manage crowding through algorithmic capacity planning. At the same time, newer formats such as climbing gyms and functional-training studios are attracting venture capital, aided by heightened visibility from climbing’s inclusion in the 2024 Paris Olympics.

Established operators are also pushing deeper into ancillary services to counter membership commoditization: Equinox reported that spa, nutrition, and related offerings contributed 18% of total revenue in 2024, adding roughly USD 120 per member each month beyond base dues. Corporate wellness partnerships are further reshaping competition, with Life Time noting that 22% of new memberships in 2024 came through employer contracts tied to measured utilization rather than flat fees. As regulatory requirements tighten, certifications such as ISO 9001 are becoming prerequisites for public-sector and insurer-linked revenue streams, though the time and cost of compliance continue to disadvantage smaller independents. Secondary cities offer untapped potential due to lower real-estate costs and limited incumbent presence, but high upfront capital needs and shortages of qualified trainers remain key constraints on rapid expansion.

Fitness And Recreational Sports Centers Industry Leaders

Planet Fitness

Life Time Fitness

Basic-Fit

LA Fitness

Anytime Fitness

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Planet Fitness announced a USD 800 million capital allocation plan through 2026, targeting 1,200 location retrofits with IoT-enabled cardio equipment that syncs with Apple Watch, Fitbit, and Garmin wearables, enabling cross-facility workout tracking and algorithmic capacity planning to reduce peak-hour congestion.

- September 2024: Life Time Fitness opened its 172nd luxury athletic resort in Coral Gables, Florida, featuring a 50-meter Olympic pool, 40,000 square feet of strength and cardio equipment, and integrated spa and coworking spaces. The USD 60 million facility targets high-net-worth individuals with monthly memberships priced at USD 250 to USD 350, reflecting the company's strategy to capture premium-tier demand in affluent submarkets.

- August 2024: Xponential Fitness completed the acquisition of BFT (Body Fit Training) for USD 28 million, adding 200 international studios to its portfolio and expanding its functional-training footprint in Australia and Southeast Asia. The deal underscores the company's strategy to consolidate boutique fitness brands and leverage centralized marketing and instructor certification to drive franchisee profitability.

- July 2024: Basic-Fit announced a EUR 150 million (approximately USD 162 million) expansion plan to open 100 new clubs across Germany, France, and Spain by end-2025, targeting secondary cities where budget fitness penetration remains below 5%. The Netherlands-based chain operates 1,300-plus locations and is leveraging economies of scale in equipment procurement to undercut local independents.

Global Fitness And Recreational Sports Centers Market Report Scope

Sports and Fitness Center is an off-site facility operated by a third party that is open to the public and has amenities to improve and maintain physical health, which includes cardio and strength training equipment, free weights, group fitness classes, and locker rooms with showers. This report aims to provide a detailed analysis of the fitness and recreational sports centers market. It focuses on the market dynamics, emerging trends in the segments and regional markets, and insights into the various product and application types. Also, it analyzes the key players and the competitive landscape. The fitness and recreational sports centers market is segmented by type, which includes gymnasiums, yoga, aerobic dance, handball sports, racquet sports, skating, swimming, and others, by age group, which includes 35 and younger, 35-54, and 55 and older, by end-user which includes men and women, and by geography which includes North America, Asia-Pacific, Europe, South America, and the Middle East. The report offers market size and forecasts for the fitness and recreational sports centers market in terms of revenue (USD) for all the above segments.

| Gymnasiums/ Health Club |

| Yoga |

| Aerobic Dance |

| Handball Sports |

| Racquet Sports |

| Skating |

| Swimming |

| Others |

| Adults |

| Kids/Children |

| Membership Fees |

| Personal Training and Instruction Services |

| Other Service Type |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Facility Type | Gymnasiums/ Health Club | |

| Yoga | ||

| Aerobic Dance | ||

| Handball Sports | ||

| Racquet Sports | ||

| Skating | ||

| Swimming | ||

| Others | ||

| By End-User | Adults | |

| Kids/Children | ||

| By Service Type | Membership Fees | |

| Personal Training and Instruction Services | ||

| Other Service Type | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the fitness and recreational sports centers market today?

Global revenue reached USD 159.39 billion in 2026 and is set to climb to USD 235.47 billion by 2031 at an 8.12% CAGR.

Which region will grow the fastest through 2031?

Asia-Pacific is forecast to post a 9.43% CAGR, supported by China’s sports infrastructure goals and India’s Fit India policies that lower licensing barriers.

Which facility format is expanding most quickly?

Yoga studios lead with an 8.53% CAGR through 2031 as corporations bundle mindfulness with traditional exercise in wellness contracts.

Why are personal training services gaining share?

Consumers are paying for measurable outcomes; sessions priced at USD 50–150 per hour outpace basic memberships as AI tools let trainers handle more clients.

What role do corporate wellness programs play?

Two-thirds of multinationals now subsidize gym use, and utilization-based contracts supply stable traffic and diversified revenue for operators.

Page last updated on: