Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 135.71 Billion |

| Market Size (2031) | USD 199.46 Billion |

| Growth Rate (2026 - 2031) | 8.01% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Health And Fitness Club Market Analysis by Mordor Intelligence

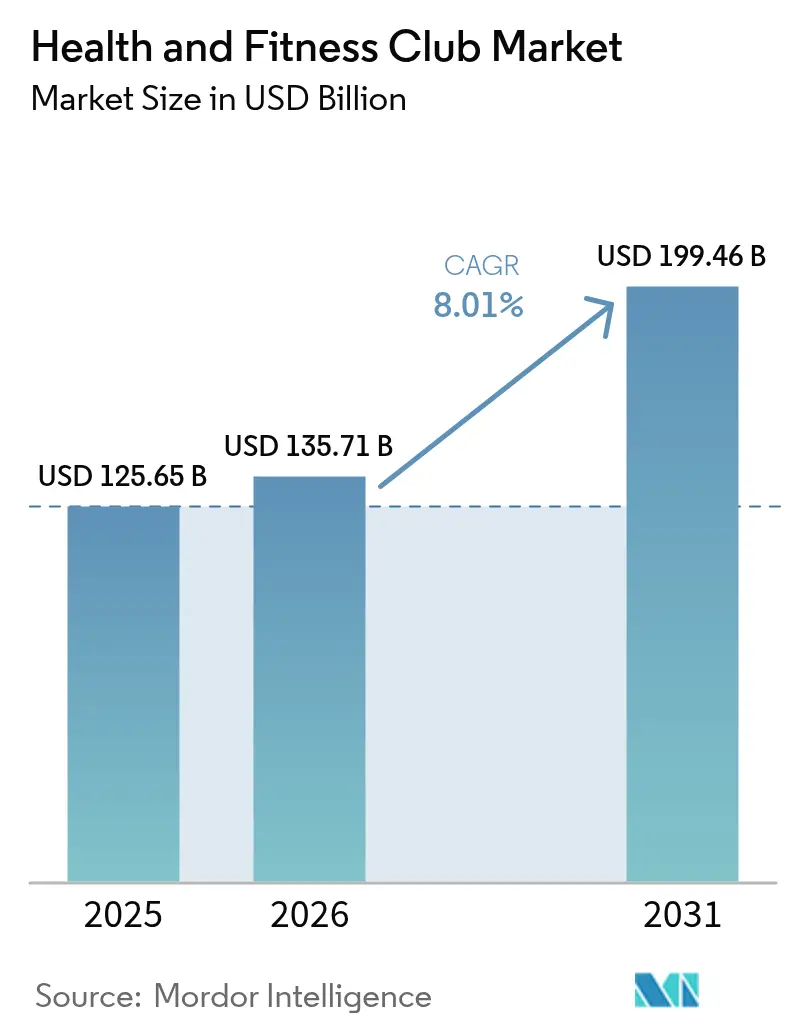

The Health And Fitness Club Market size was valued at USD 125.65 billion in 2025 and estimated to grow from USD 135.71 billion in 2026 to reach USD 199.46 billion by 2031, at a CAGR of 8.01% during the forecast period (2026-2031). This growth trajectory reflects the convergence of escalating obesity rates, government health initiatives, and technological integration, reshaping how consumers approach fitness and active lifestyle choices. The CDC's Active People, Healthy Nation initiative[1]Centers for Disease Control and Prevention, "Active People, Healthy Nation", www.cdc.gov, targeting 27 million Americans by 2027, combined with the HHS multimillion-dollar "Take Back Your Health" campaign, creates unprecedented policy momentum supporting fitness club expansion

Key Report Takeaways

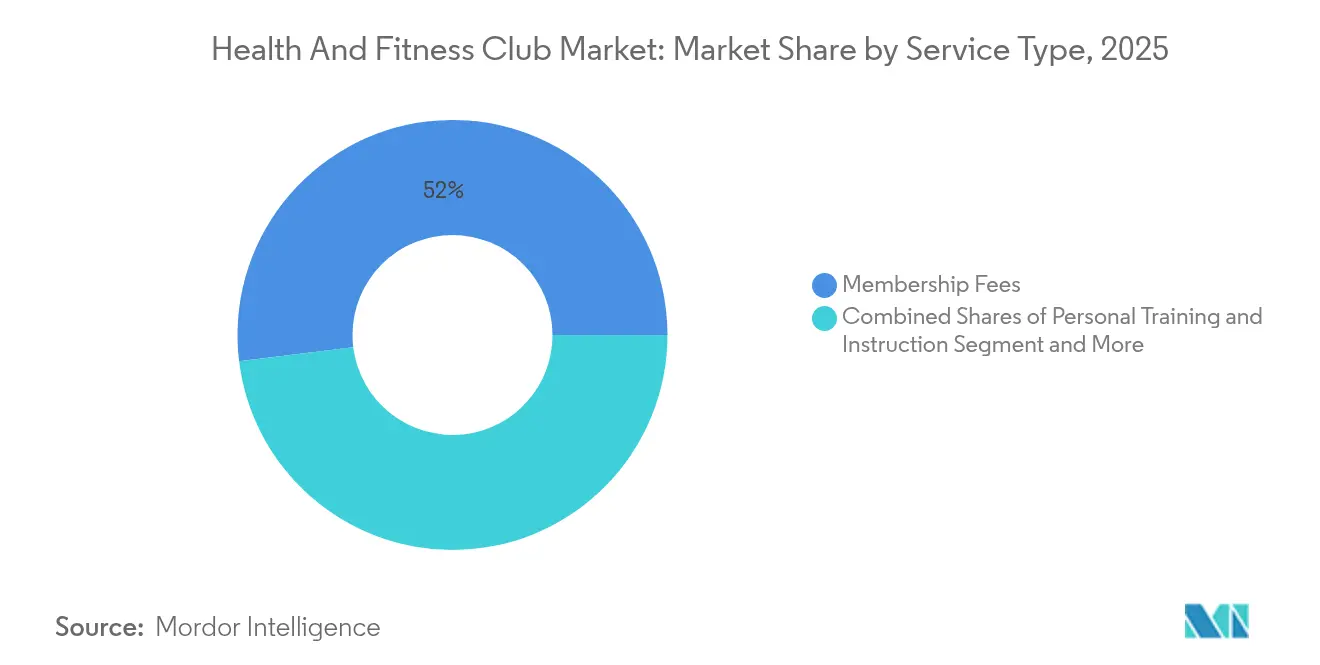

- By service type, membership fees captured 51.95% of the health and fitness club market share in 2025, while personal training and instruction services are projected to expand at an 7.78% CAGR through 2031.

- By business model, independent clubs accounted for 66.55% of the market in 2025, whereas chained clubs are set to grow at an 9.57% CAGR over 2026-2031.

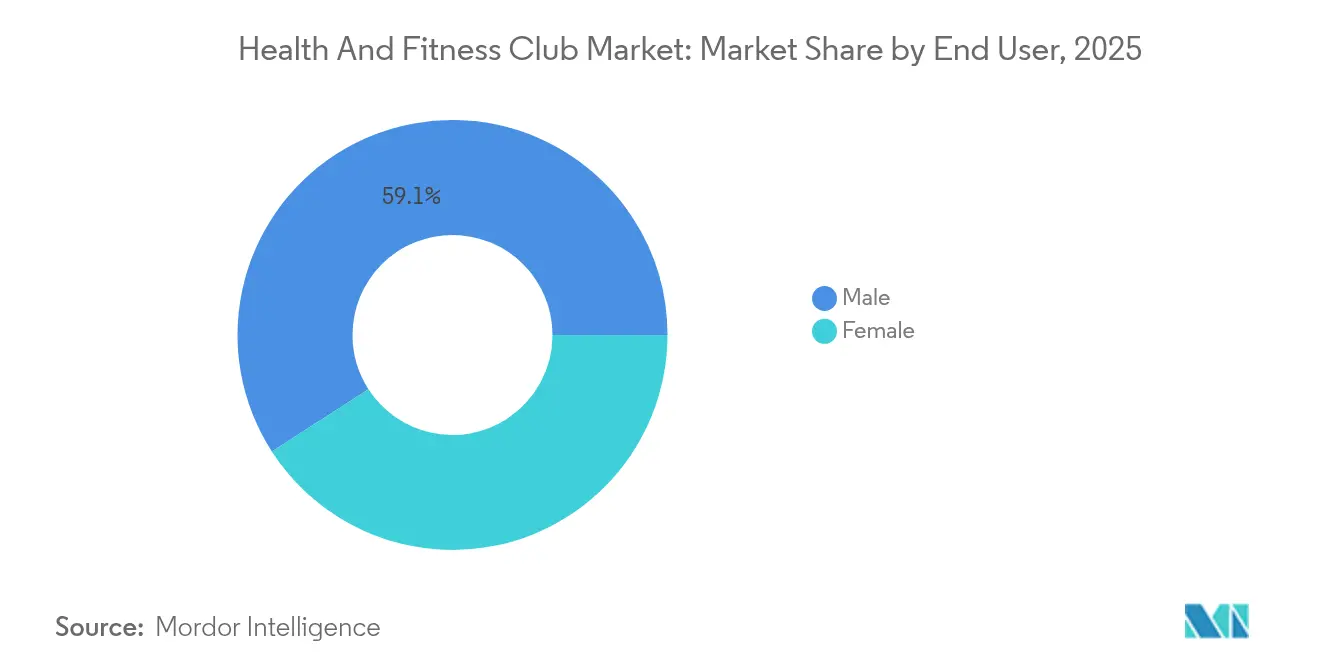

- By end-user, male members represented 59.12% of 2025 revenue, yet the female segment is slated to log 10.79% CAGR.

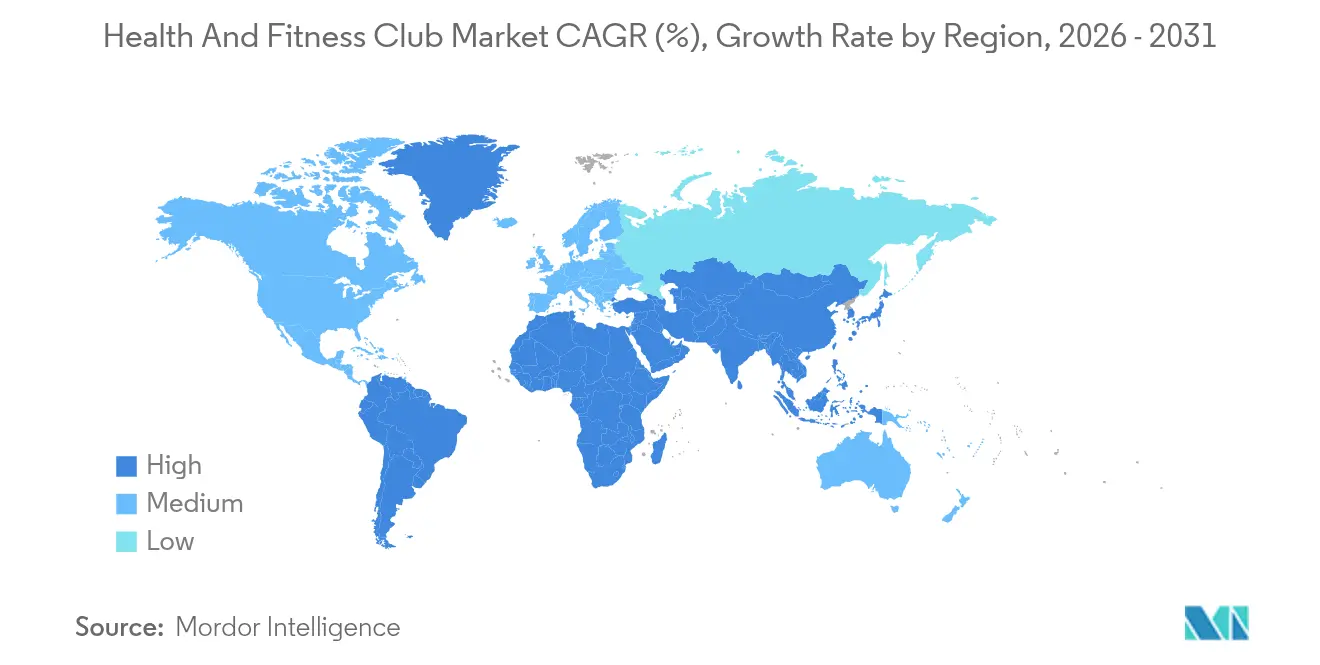

- By geography, North America led with a 34.72% share in 2025, and Middle East and Africa is forecast to post a 10.23% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Health And Fitness Club Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Obesity and Lifestyle Diseases | +2.1% | Global, with highest impact in North America and Europe | Long term (≥ 4 years) |

| Growing Health Awareness and Wellness Trends | +1.8% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Integration of Technology and Digital Fitness Solutions | +1.6% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Corporate Wellness Programs and Fitness in Work Culture | +1.4% | North America & EU, emerging in APAC urban centers | Medium term (2-4 years) |

| Government Initiatives and Public Health Campaigns | +1.2% | Global, with strongest impact in US, EU, and China | Long term (≥ 4 years) |

| Expansion of Fitness Franchises and Personalized Services | +1.0% | APAC core, spill-over to MEA and Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Obesity and Lifestyle Diseases

The obesity epidemic creates sustained demand pressure across health and fitness markets. According to the Government of the UK[2],Government of the UK, "Obesity Profile: short statistical commentary May 2024", www.gov.uk data from 2023, 69.2% of men and 58.6% of women in the United Kingdom were overweight. Southern US states are witnessing the highest prevalence of obesity, unveiling concentrated market opportunities for fitness club expansion in these underserved regions. This trend highlights the potential for fitness businesses to address the growing demand for health and wellness solutions in these areas. According to 2024 data from the Centers for Disease Control and Prevention, the annual economic burden of obesity-related healthcare costs hits a staggering USD 173 billion. This hefty figure propels both individuals and employers to invest in preventive fitness solutions. As a result, there's a noticeable shift, with more consumers opting to join gyms and fitness centers. Additionally, fitness clubs in these regions can leverage this demand by offering tailored programs and services to cater to the specific needs of the local population.

Growing Health Awareness and Wellness Trends

Health club operators anticipate a surge in memberships, driven by a shift in consumer perception. Fitness is now viewed as a vital component of health, rather than a luxury. This shift is further supported by increasing awareness of the long-term health benefits of regular physical activity, including improved cardiovascular health, enhanced mental well-being, and reduced risk of chronic diseases. Additionally, rising sports participation across the world, physical activity, and fitness focus are increasing. According to the Sports England[3]Sports England, "Number of people participating in Fitness Classes In the United Kingdom", www.sportsengland.org data from 2024, 6,695.5 thousand people in the United Kingdom participated in fitness classes twice a month. As members gravitate towards holistic wellness, clubs are responding by merging mental health benefits with traditional fitness offerings. This evolution underscores the growing demand for comprehensive wellness experiences that cater to both physical and mental health needs. Meanwhile, corporate wellness programs are gaining traction, with employers acknowledging their role in boosting productivity and curbing healthcare costs. Additionally, fitness clubs are forging retail partnerships, broadening their revenue horizons by integrating products related to nutrition, recovery, and overall lifestyle. These partnerships enable clubs to offer a more diverse range of services and products, enhancing customer engagement and loyalty.

Integration of Technology and Digital Fitness Solutions

AI-powered fitness technology transforms member engagement through personalized workout programs and biometric data analysis, with the AI fitness market expanding across the world. Wearable technology integration enables continuous health monitoring and creates data-driven coaching opportunities that enhance member retention and premium service pricing. The rise of hybrid fitness models combining AI coaching with human trainers addresses the convenience demand while maintaining the social interaction elements that differentiate physical clubs from home workouts. Smart gym equipment deployment allows clubs to optimize space utilization and provide real-time performance feedback, creating competitive advantages in member acquisition. Digital fitness platforms serve as complementary rather than competitive services, with successful clubs leveraging technology to enhance rather than replace human-centered fitness experiences.

Corporate Wellness Programs and Fitness in Work Culture

Workplace fitness initiatives expand beyond traditional gym membership reimbursements toward comprehensive wellness ecosystems that include on-site fitness facilities, virtual training programs, and health coaching services. The White House partnership with major sports leagues and players' unions creates institutional momentum for corporate wellness program adoption across industries, according to the U.S. Department of Health and Human Services. Employee health benefit packages increasingly feature fitness club partnerships as recruitment and retention tools, particularly in competitive labor markets where wellness benefits differentiate employers. Remote work trends create demand for flexible fitness solutions that accommodate distributed workforces, driving corporate contracts for multi-location gym access and virtual fitness programming. The integration of fitness metrics into corporate health insurance premium calculations incentivizes both employers and employees to prioritize fitness club participation.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Operational and Membership Costs | -1.5% | Global, with highest impact in developed markets | Short term (≤ 2 years) |

| Market Saturation in Developed Regions | -1.2% | North America & EU primarily | Medium term (2-4 years) |

| Changing Consumer Preferences and Time Constraints | -0.9% | Global, with urban concentration | Short term (≤ 2 years) |

| Impact of Digital Fitness and At-Home Workouts | -0.8% | Developed markets with high internet penetration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Operational and Membership Costs

Rising operational expenses from equipment maintenance, facility leases, and staffing costs pressure profit margins while limiting membership accessibility for price-sensitive consumers. Planet Fitness's USD 800 million securitized financing facility demonstrates the capital intensity required for large-scale operations, with proceeds allocated to debt refinancing and expansion funding. Membership pricing increases, implemented for the first time in over two decades by major chains, test consumer price elasticity amid inflationary pressures across the economy. Energy costs for climate control, lighting, and equipment operation create ongoing expense volatility that affects pricing strategies and market positioning. The challenge of balancing premium service offerings with affordable membership rates constrains market expansion in middle-income demographics, creating opportunities for value-oriented fitness concepts.

Market Saturation in Developed Regions

Established markets in North America and Europe face facility density limitations as prime real estate becomes scarce and expensive, forcing operators to explore alternative locations and formats. The competitive intensity in saturated markets drives margin compression as clubs compete through amenities, pricing, and service differentiation rather than geographic expansion. Luxury gym operators like Equinox and Life Time adapt by occupying large retail spaces, indicating market evolution toward experience-based differentiation rather than location convenience. Market maturity creates consolidation pressure, with smaller independent operators struggling to compete against well-capitalized chains that achieve economies of scale in equipment procurement, marketing, and operational efficiency. The saturation challenge drives innovation in club formats, including smaller footprint concepts, specialized fitness studios, and hybrid retail-fitness models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Membership Fees Drive Revenue While Personal Training Accelerates

Membership fees represent 51.95% of market share in 2025, reflecting the subscription-based foundation of fitness club business models, while personal training and instruction services demonstrate the fastest growth at 7.78% CAGR through 2031. The dominance of membership revenue creates predictable cash flow streams that support facility investments and operational stability, yet the accelerating personal training segment indicates consumer willingness to pay premium rates for customized fitness experiences. Other service types, including group classes, nutrition counseling, and wellness services, contribute supplementary revenue streams that enhance member engagement and reduce churn rates.

The shift toward personal training growth reflects broader consumer preferences for individualized health solutions, supported by the integration of AI-powered coaching tools that enhance trainer effectiveness and member outcomes. Corporate wellness contracts increasingly demand personalized fitness programming for employees, creating B2B opportunities for clubs that can scale individual training services.

By Business Model: Independent Clubs Dominate Despite Chain Acceleration

Independent clubs maintain 66.55% market share in 2025, leveraging local market knowledge and community relationships to compete against standardized chain operations, while chained clubs expand at 9.57% CAGR through 2031, driven by franchise scalability and operational efficiency. The independent club advantage stems from flexibility in programming, pricing, and facility customization that addresses specific demographic needs and local preferences. Chained clubs achieve growth through systematic expansion, standardized training programs, and centralized marketing that reduces individual location risks and accelerates market penetration.

The Orangetheory Fitness and Self Esteem Brands merger in March 2024 exemplifies chain consolidation strategies, creating a USD 3.5 billion entity with 7,000 locations that leverages brand recognition and operational synergies. Franchise models enable rapid geographic expansion with reduced capital requirements, particularly attractive for international market entry, where local partners provide market knowledge and regulatory compliance. Independent clubs respond through specialization strategies, focusing on niche markets such as senior fitness, rehabilitation services, or premium wellness experiences that chains cannot easily replicate.

By End-User: Male Dominance Shifts Toward Female Growth

Male consumers represent 59.12% of market share in 2025, reflecting traditional fitness club demographics, while female participation accelerates at 10.79% CAGR through 2031, indicating a significant demographic transition within the fitness industry. The male market dominance stems from historical weightlifting and strength training focus in traditional gym environments, yet evolving facility designs and programming increasingly accommodate diverse fitness preferences. Female market growth reflects expanding wellness awareness, group fitness popularity, and specialized programming for women's health needs, including prenatal and postnatal fitness services.

The demographic shift creates opportunities for clubs to redesign spaces and services that appeal to female consumers, including enhanced privacy features, childcare services, and wellness programming beyond traditional exercise equipment. Corporate wellness programs increasingly target female employees through flexible scheduling, family-friendly amenities, and holistic health services that address work-life balance challenges. The integration of mental health and stress management programming appeals particularly to female consumers who seek comprehensive wellness solutions rather than exercise-only experiences

Geography Analysis

In 2025, North America commands a dominant 34.72% market share, bolstered by its well-established fitness infrastructure, proactive government health initiatives, and the widespread embrace of corporate wellness programs. These factors collectively fuel a robust demand across diverse demographic segments. Additionally, Canada and Mexico play pivotal roles in this growth narrative, driven by cross-border franchise expansions and heightened health awareness campaigns. The region's maturity presents ripe consolidation opportunities, with industry giants like Planet Fitness actively pursuing acquisitions and franchise conversions to harness economies of scale. With 40.3% of U.S. adults classified as obese, as reported by the Centers for Disease Control and Prevention (2023), rising obesity rates ensure sustained demand, driving market expansion despite economic headwinds.

Meanwhile, the Middle East & Africa is on a rapid ascent, charting a projected CAGR of 10.23% through 2031. This growth surge is attributed to urbanization, increasing disposable incomes, and a heightened awareness of health and wellness, especially among the youth. Key players like the UAE, Saudi Arabia, and South Africa are capitalizing on this momentum, thanks to government-led initiatives championing active lifestyles, a surge in boutique and premium fitness concepts, and a growing inclination towards lifestyle-centric wellness solutions. The region's dynamic economic and demographic shifts pave the way for varied business models, ranging from upscale wellness clubs in metropolitan hubs to budget-friendly fitness options in burgeoning urban locales.

Europe and Asia-Pacific are witnessing steady growth, albeit driven by distinct market dynamics. Europe's growth is underpinned by government health campaigns, an aging demographic, and a deeply ingrained wellness culture. Countries like Germany, the UK, and France are at the forefront, boasting high membership penetration and premium offerings. In contrast, Eastern European nations, notably Poland, are experiencing a growth spurt, fueled by rising disposable incomes and heightened health consciousness. Asia-Pacific, with its vast potential, sees China, India, and Southeast Asia as key growth engines, driven by urbanization and a burgeoning middle class. Innovative fitness concepts, from budget-friendly gyms in Japan to boutique wellness clubs in Southeast Asia, are sprouting across both established and emerging markets. Furthermore, a growing emphasis on sustainability and environmental stewardship is reshaping club operations in both regions, leading to a broader adoption of green practices and renewable energy solutions.

Regulatory Landscape

Regulation for health and fitness clubs continues to tighten around consumer protection, safety, and data handling, increasing documentation and compliance requirements for operators. In the United States, state-level oversight increasingly focuses on contract practices (including cancellation and disclosure rules) and on the handling of biometric data collected through access systems and connected fitness technologies, as reflected in the Health & Fitness Association (HFA) 2026 State of the States legislative review.

In Europe, EN 17229:2026 (published March 25, 2026) formalizes fitness-club requirements for amenities and operations, including documented risk assessments, emergency response planning, supervision expectations, and explicit user information protocols for specific conditions, such as high-temperature environments above 26 degrees Celsius. Safety standards for equipment run in parallel through established series such as EN ISO 20957 for indoor equipment, alongside ongoing standardization activity for outdoor fitness equipment (including BSI work on BS EN 16630 in January 2026). In Australia, the Australian Capital Territory introduced the Fair Trading (Australian Consumer Law) Fitness Industry Code of Practice 2026, reinforcing consumer-contract and conduct expectations for fitness providers.

Competitive Landscape

The health and fitness club market is fragmented, offering opportunities for regional consolidation and niche market strategies targeting diverse consumer segments. Market leaders employ differentiated positioning strategies, including product launches, expansions, partnerships, mergers, and acquisitions. Prominent players in the market include Planet Fitness, Equinox Holdings Inc., 24-Hour Fitness Worldwide Inc., Life Time Group Holdings, Inc., and RSG Group GmbH, each leveraging unique approaches to maintain their competitive edge.

Technology integration has emerged as a critical competitive advantage in the market. AI-driven fitness solutions, wearable device compatibility, and mobile app functionalities are enhancing member engagement and improving retention rates. These technological advancements not only improve the customer experience but also enable operators to streamline operations and gather valuable data insights, further strengthening their market position.

Franchise models are driving rapid geographic expansion with reduced capital requirements, making them particularly attractive for international market entry. Local partners in these markets provide essential regulatory compliance and market knowledge, ensuring smoother operations. The competitive landscape increasingly rewards operators who balance standardization for operational efficiency with customization to meet local market preferences, fostering sustainable growth in an increasingly crowded marketplace.

Health And Fitness Club Industry Leaders

-

Planet fitness

-

Equinox Holdings Inc.

-

RSG Group GmbH

-

Leejam Sports Ltd.

-

Fitness International LLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

International expansion into underpenetrated urban markets remains a clear whitespace opportunity, supported by active brand entry and multi-site growth plans. In 2026, Crunch Fitness disclosed a global build-out plan for approximately 100 gyms and opened its first India club in Noida, highlighting how scalable operating models and franchise-led deployment are being used to reach new member pools beyond saturated North American and European corridors.

Operators are also working to lift addressable spend per member by bundling traditional training with recovery, mental wellness, and technology-enabled personalization. The American College of Sports Medicine (ACSM) ranked exercise for mental health as a top fitness trend for 2026, which aligns with additions such as red light therapy and compression therapy. On the operations side, adoption is shifting toward predictive analytics and AI-driven automation for member engagement and churn management, supporting differentiation for chained clubs and tech-forward independents that can integrate digital tools while preserving in-club coaching and community.

Recent Industry Developments

- July 2026: RSG Group GmbH opened a new McFIT club in Bochum, Germany, showcasing the McFIT The Original design concept. The update indicates continued investment in refreshed club formats and brand standardization, supporting consistent rollout across both company-owned sites and future franchise partners.

- June 2026: Equinox announced its first Georgia fitness center location in Buckhead Village (Atlanta), with an opening planned for 2027. The move extends luxury club expansion into high-income submarkets beyond the brand’s traditional coastal strongholds and reinforces premium positioning through selective geographic growth.

- November 2024: Leejam Sports opened four new centers in Saudi Arabia, including its first-ever Ladies' Center in Al-Rass (Qassim Province), alongside new Men's and Ladies' Centers in Al-Qunfidah (Makkah Province). These openings expand gender-segmented capacity and broaden access in secondary cities, strengthening network density where organized fitness participation is rising.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenues earned by health and fitness clubs from operating physical facilities where members and walk-in customers use fitness equipment and participate in paid services like instruction and training.

Scope exclusions: We exclude at-home digital-only fitness subscriptions, one-off sports event participation fees, and sales of fitness equipment or apparel that are not sold as part of a club service.

Segmentation Overview

-

By Service Type

- Membership Fees

- Personal Training & Instruction

- Other Service Type

-

By Business Model

- Independent Clubs

- Chained Clubs

-

By End-User

- Male

- Female

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

- Middle East & Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

For desk research, we start by mapping the demand pool for gyms and clubs using public economic and demographic indicators, then we link those signals with industry operating metrics.

The main public inputs include income and urbanization indicators from the World Bank and OECD, labor statistics from agencies such as the US Bureau of Labor Statistics, and health participation signals from the World Health Organization.

To keep the market model tied to how clubs earn revenue, we also reviewed filings and investor materials from listed operators, reputable business press coverage, and relevant trade association publications that discuss membership behavior and pricing. Paid subscriptions were used selectively for company financials and intelligence, news and financials, and patent databases to understand product-service innovation around training formats and recovery offerings. The desk research sources mentioned are not exhaustive, and we also checked other public references to support data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was done through structured conversations and short surveys with club operators, franchisors, equipment and service partners, and local industry experts across APAC, EMEA, and the Americas. We used these inputs to pressure-test key assumptions such as average membership pricing, churn patterns, service attach rates (for personal training and classes), and how penetration differs between mature and emerging cities. When desk sources were thin, we re-checked the numbers with a second set of respondents to keep the final totals realistic.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 18% | APAC: 45% |

| Mid tier: 49% | Functional/Unit leaders: 38% | EMEA: 34% |

| Smaller Players: 21% | Managers: 44% | Americas: 21% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs the addressable revenue pool by combining country-level fitness participation, the urban adult population, and likely paid club penetration. We then convert this into market value using observed membership pricing and add-on service spend.

The totals are checked with selective bottom-up approximations, such as rolling up sampled operator revenues in key cities, using membership counts times average revenue per member, and validating price ranges through channel checks.

In this market, several inputs move the forecast most directly: membership fee levels by city tier, the share of members buying personal training or group classes, club count growth and closure rates, average visit frequency (used as a proxy for retention), and inflation-led pricing adjustments. Forecasts were built using scenario analysis supported by expert views, since churn, discretionary spending, and local competition can change quickly, and then the scenarios were blended into one central case. Where bottom-up evidence was missing for smaller markets, we applied conservative penetration bands and only widened them after primary checks confirmed similar operating conditions.

Data Validation & Update Cycle

Outputs are validated by comparing the model with independent signals such as reported operator revenue trends, broad consumer spending direction, and regional participation changes. Large jumps are flagged, then the underlying assumptions are reviewed line by line. Follow-up calls are triggered when a pricing or penetration input looks out of place relative to what respondents report.

Before sign-off, the work goes through multiple analyst reviews to keep formulas, conversions, and market boundaries consistent across countries. Reports are refreshed annually, and interim updates are made when material events occur, such as a sharp change in consumer spending or a major shift in club openings. Right before delivery, we run a final pass to ensure the latest public indicators and interview learnings are reflected.

Mordor Intelligence's Health and Fitness Club Market Size Measured Against Other Published Estimates

Published market sizes for health and fitness clubs do not always match because the service boundary is drawn differently, and because some models lean heavily on broad consumer wellness spending instead of club revenue. Differences in starting year, inflation handling, and whether franchised revenue is treated as operator revenue or system revenue can also widen the spread.

The table shows a fairly tight cluster around 2026 values, and the gap tends to widen with longer forecasts. In Mordor Intelligence's model, the value is counted as club revenues tied to membership fees, personal training and instruction, and other in-club offerings, which avoids folding in home fitness subscriptions or stand-alone equipment sales that can inflate totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 135.71 B (2026) | |

| Global Consultancy A | USD 142.62 B (2026) | Uses a different segmentation lens and base-year anchoring, and the total can drift upward if broader wellness participation is translated into club spending using higher penetration and price ramps. |

| Trade Publisher B | USD 121.58 B (2026) | Often applies a narrower revenue capture approach and may exclude parts of non-membership service revenue, such as paid instruction upsells, which can pull the 2026 total down. |

Overall, the spread is best explained by what each source counts as club revenue and how aggressively membership pricing and penetration are projected forward. Our steps stay traceable to membership economics, service attach, and reasonable penetration bands, so decision-makers can follow how each assumption moves the final number.

Key Questions Answered in the Report

What is the current and forecast size of the health and fitness club market?

The market is valued at USD 135.71 billion in 2026 and is projected to reach USD 199.46 billion by 2031, growing at 8.01% CAGR.

Which region will grow the fastest through 2031?

Middle East and Africa is expected to record the highest pace, expanding at a 10.23% CAGR over the forecast period.

How is technology reshaping fitness clubs?

AI-enabled equipment and wearable integrations deliver personalized coaching and real-time feedback, raising member retention and supporting premium pricing tiers.

What demographic shift is influencing club strategies?

Female membership is forecast to rise at an 10.79% CAGR, narrowing the historical gap with male participants.

Page last updated on: