Licensed Sports Merchandise Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

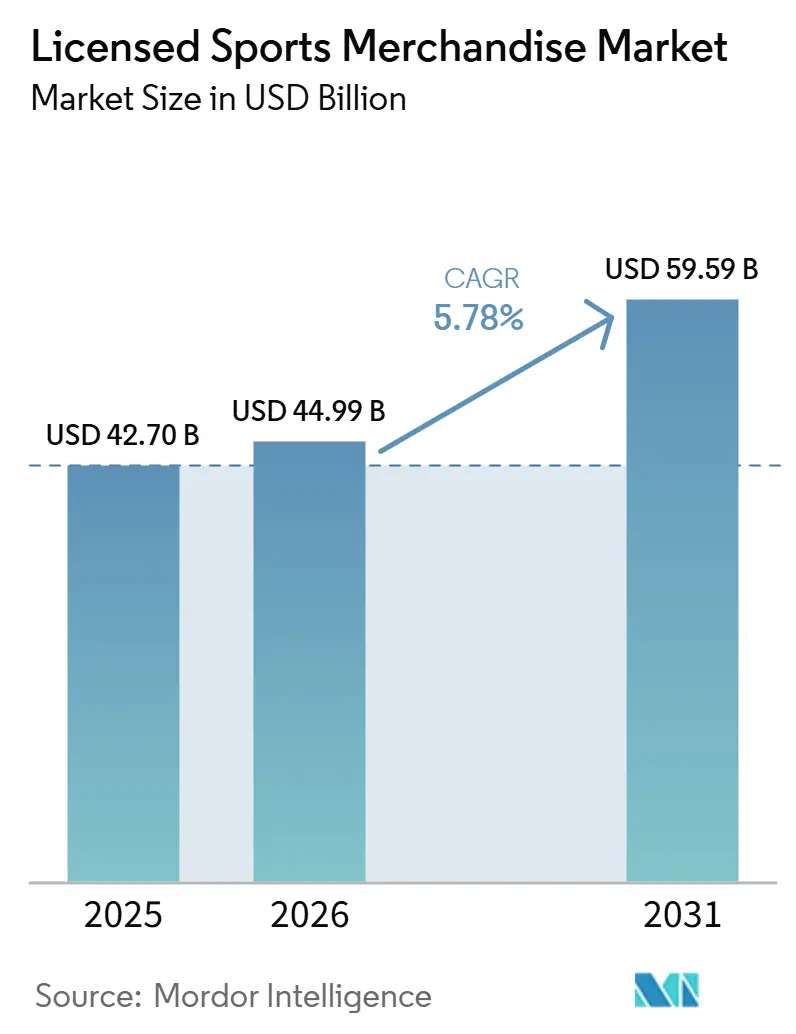

| Market Size (2026) | USD 44.99 Billion |

| Market Size (2031) | USD 59.59 Billion |

| Growth Rate (2026 - 2031) | 5.78% CAGR |

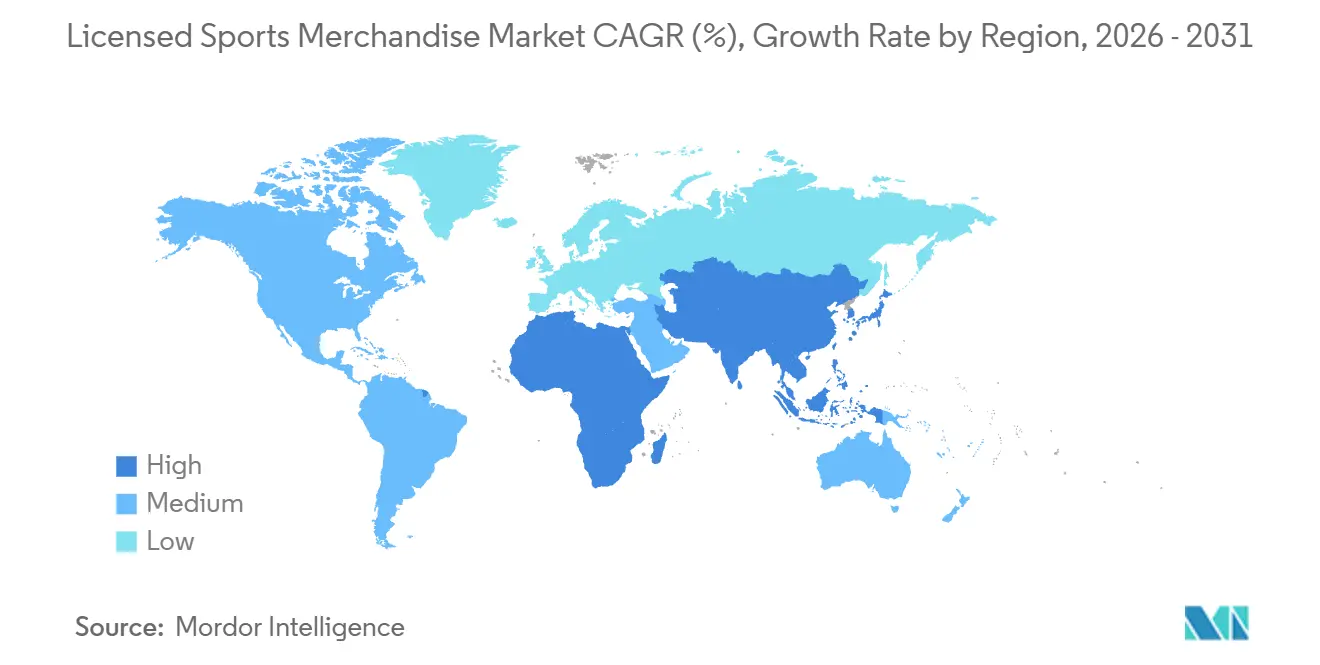

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Licensed Sports Merchandise Market Analysis by Mordor Intelligence

The licensed sports merchandise market size is projected to expand from USD 42.70 billion in 2025 and USD 44.99 billion in 2026 to USD 59.59 billion by 2031, registering a CAGR of 5.78% between 2026 and 2031. Digital streaming has significantly expanded the global reach of major sports leagues, enabling increased cross-border jersey sales and facilitating real-time product launches tied to key moments in sports. Luxury fashion brands are increasingly collaborating with sports clubs and athletes to design exclusive capsule collections, elevating licensed merchandise from basic souvenirs to high-value investment pieces. Esports franchises, which represent competitive video gaming organizations, have established partnerships with the same apparel providers as traditional sports leagues, thereby attracting new fan segments to the licensed sports merchandise market. Retailers with vertically integrated operations, such as Fanatics, utilize first-party customer data to implement targeted product launches, while blockchain-based authentication systems play a critical role in restoring consumer trust following high-profile counterfeit incidents.

Key Report Takeaways

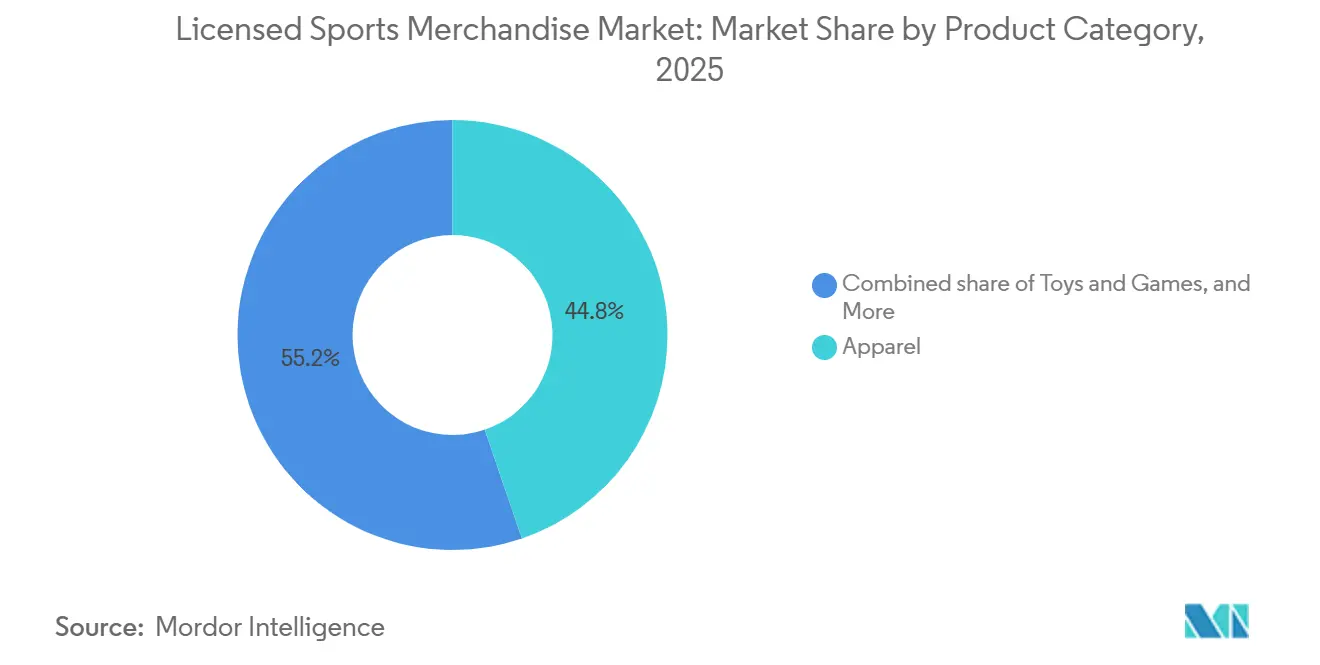

- By product category, apparel led with 44.76% of licensed sports merchandise market share in 2025; toys and games are projected to advance at a 6.81% CAGR through 2031.

- By sports type, football retained 33.12% revenue share in 2025, while basketball is forecast to post the fastest 6.97% CAGR to 2031.

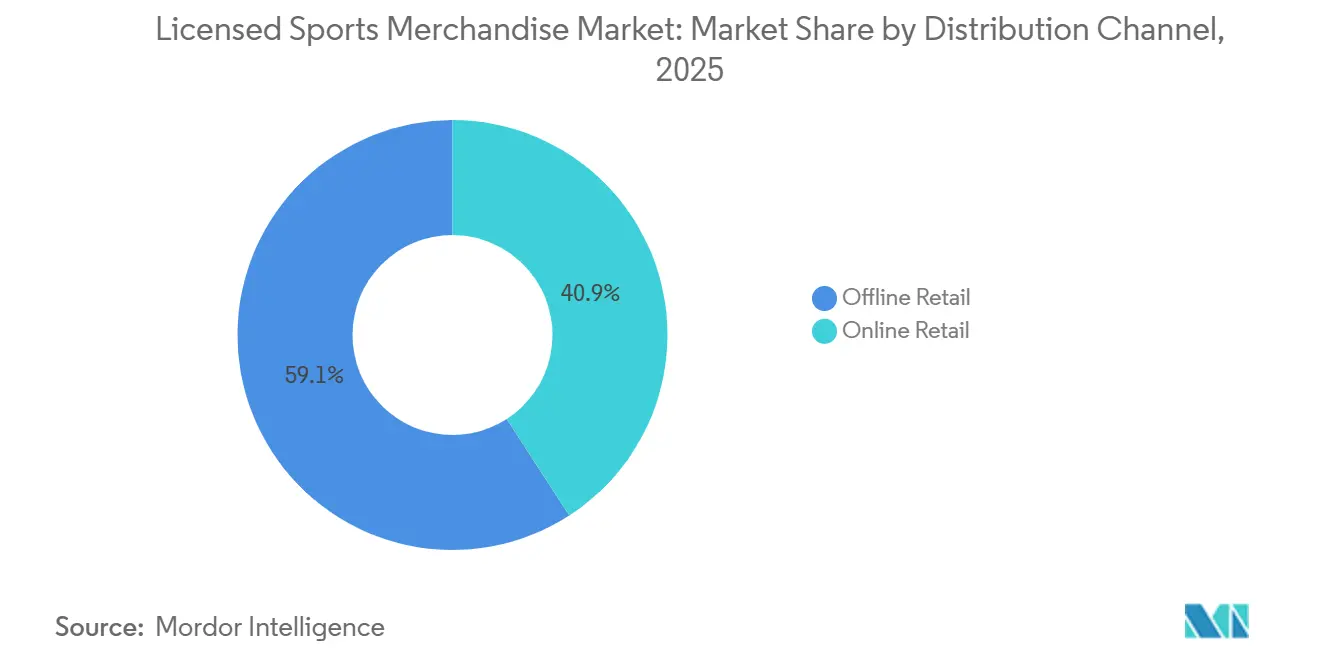

- By distribution channel, offline retail captured 59.14% of the licensed sports merchandise market size in 2025, yet online retail is set to grow at 6.90% per year through 2031.

- By end user, adults accounted for 82.84% of 2025 spending, but the kids segment is projected to climb at 6.93% CAGR over 2026-2031.

- By geography, North America contributed 61.42% of global revenue in 2025, whereas Asia-Pacific is expected to expand at 7.81% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Licensed Sports Merchandise Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global popularity of major sports leagues | +0.8% | Global, with acceleration in Asia-Pacific and Middle East | Medium term (2-4 years) |

| Expansion of esports into mainstream merchandising | +0.7% | North America and Europe core, spillover to Asia-Pacific | Short term (≤ 2 years) |

| Innovative product designs attracting collectors | +0.6% | Global, premium segments in North America and Europe | Long term (≥ 4 years) |

| Partnerships with luxury fashion houses | +0.5% | Europe and North America, emerging in Middle East | Medium term (2-4 years) |

| Digital streaming boosting international fanbase | +0.4% | Asia-Pacific, Latin America, Middle East and Africa | Short term (≤ 2 years) |

| Themed merchandise for seasonal tournaments | +0.3% | Global, peaks during FIFA World Cup, Olympics, IPL | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising global popularity of major sports leagues

The National Football League (NFL) hosted several international games during a recent season, drawing substantial in-person audiences. This initiative led to a notable year-over-year increase in international viewership, which was directly linked to higher overseas sales of jerseys and licensed headwear. Formula 1 entered into a long-term sponsorship agreement with LVMH (Moët Hennessy Louis Vuitton), valued at a significant annual amount. This partnership integrated Louis Vuitton branding into race-day merchandise and pit-lane apparel, positioned at premium luxury price points. The National Basketball Association (NBA) opened flagship stores in Manila and Mexico City, capitalizing on the popularity of local sports stars to convert streaming audiences into merchandise buyers. India’s cricket economy generated considerable revenue in a recent year, showing consistent growth compared to the previous year. Indian Premier League (IPL) franchises collectively earned over INR 6,797 crore during fiscal 2024. In China, the government set a CNY 5 trillion target for its sports industry by 2025, with the 2024 output reaching CNY 3.8421 trillion. This reflects the effectiveness of government-backed infrastructure investments in boosting consumer spending on licensed goods [1]Source: China National Bureau of Statistics, “Sports Industry Output Data,” stats.gov.cn.

Expansion of esports into mainstream merchandising

Esports organizations such as 100 Thieves, Fnatic, and FaZe Clan have established apparel partnerships with Adidas AG, Nike Incorporated, and ASOS. These collaborations have transitioned team jerseys from niche online stores to mainstream retail channels that traditionally focused on sports merchandise. Fanatics Incorporated launched dedicated esports storefronts in 2025, utilizing the same licensing and fulfillment infrastructure used for the National Football League (NFL) to support competitive gaming leagues. The intersection of gaming influencers and athletic brands is increasingly blurring category boundaries. For example, Nike Incorporated collaborated with League of Legends to release limited-edition sneakers, which sold out within hours. This trend is particularly prominent in North America and Europe, where esports viewership among the 18-to-34 demographic rivals that of traditional sports. This has created a merchandising pipeline that bypasses traditional retail gatekeepers and opens new revenue opportunities in markets with high purchasing power. Additionally, the growing popularity of esports has led to a significant increase in merchandise sales, with some regions reporting growth rates exceeding 20% annually.

Innovative product designs attracting collectors

Funko Incorporated reported that its Jason Kelce Pop! figure was the top-selling collectible in 2024, highlighting how athlete-specific designs can drive impulse purchases beyond core fan bases. In the United States sports memorabilia market, the trend of Kidults, which refers to adults purchasing toys and collectibles, continues to grow, supported by expanded licensing agreements. Mitchell and Ness, acquired by Fanatics in 2024, specializes in producing throwback jerseys that command premium prices by leveraging nostalgia for retired players and defunct franchises. The market for personalized sporting equipment and apparel is projected to grow rapidly at an annual rate of over 10% through 2031, driven by advancements in digital printing technologies. These technologies enable on-demand customization, which reduces inventory risks while simultaneously increasing perceived value for consumers. Additionally, the shift from mass-produced replicas to limited-edition collaborations is further exemplified by Nike's Kobe Protro releases, which often resell at multiples of their retail price within just days of launch.

Partnerships with luxury fashion houses

LVMH's 10-year Formula 1 sponsorship, valued at approximately USD 100 million annually, includes co-branded merchandise lines that integrate Louis Vuitton luggage and apparel with race-day gear, enhancing the perceived value of licensed products. Puma SE has collaborated with luxury streetwear labels to launch limited-edition football kits, retailing at three times the price of standard replicas and targeting collectors who view sports merchandise as investment pieces. Adidas Aktiengesellschaft (Adidas AG) partnered with high-fashion designers to relaunch the Predator boot in 2024, combining performance engineering with runway-inspired aesthetics to attract non-athletes purchasing for style rather than functionality. These partnerships are primarily concentrated in Europe and North America, where disposable income supports premium pricing, but are gradually expanding into Middle Eastern markets as sovereign wealth funds invest in sports franchises and related retail ventures. The luxury crossover is transforming margin structures, with co-branded items achieving gross margins 20% to 30% higher than standard licensed apparel.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High licensing fees burdening manufacturers | -0.5% | Global, most acute in North America and Europe | Long term (≥ 4 years) |

| Counterfeit products eroding brand trust | -0.4% | Global, concentrated in Asia-Pacific and online channels | Medium term (2-4 years) |

| Short product lifecycles after seasons end | -0.3% | Global, peaks in North America and Europe | Short term (≤ 2 years) |

| Supply chain disruptions delaying launches | -0.2% | Global, legacy bottlenecks in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High licensing fees burdening manufacturers

In 2024, National Football League (NFL) licensing revenue reached USD 3.8 billion, with individual team agreements often including minimum guarantees that transfer the risk of unsold inventory to manufacturers. Major League Baseball (MLB) generates over USD 300 million annually in licensing fees, which are typically passed on to retailers through higher wholesale prices, leading to a reduction in gross margins. Smaller manufacturers face significant challenges in obtaining premium licenses, as sports leagues generally prioritize partnerships with well-established companies that possess strong distribution networks and sufficient financial reserves to handle fluctuations in demand. The licensing fee structure motivates manufacturers to focus on increasing sales volumes to recover fixed costs, rather than investing in innovative, limited-edition, or customized products. This situation is particularly evident in North America and Europe, where mature markets restrict pricing flexibility, and retailers are reluctant to absorb higher costs. As a result, the market has become increasingly divided, with a small number of large licensees controlling the majority of retail shelf space, while smaller, niche players are turning to direct-to-consumer channels to bypass traditional licensing agreements.

Counterfeit products eroding brand trust

Nike Incorporated reported losses exceeding USD 450 million in 2024 due to counterfeit merchandise, with fake jerseys and sneakers flooding online marketplaces and undermining the exclusivity of genuine products. Both Adidas Aktiengesellschaft (AG) and Nike have adopted blockchain-based authentication systems that embed unique digital identifiers into tags and labels, allowing consumers to verify product authenticity via smartphone applications. Despite these efforts, counterfeiters have started replicating these authentication features, escalating the competition between brands and counterfeiters, and increasing production costs without fully addressing the counterfeit problem. The Asia-Pacific region remains the leading source of counterfeit sports merchandise, with cross-border e-commerce platforms enabling direct shipments to consumers in North America and Europe. The impact on brand trust is particularly pronounced in the collectibles segment, where authenticity is a critical value driver, as a single high-profile counterfeit incident can significantly depress prices across an entire category. Regulatory measures, such as the European Union's Digital Services Act, aim to hold platforms accountable for facilitating counterfeit sales; however, enforcement of these regulations varies across jurisdictions. In total, over 214,507 counterfeit items were seized, including jerseys, t-shirts, hats, jewelry, and other memorabilia [2]Source: U.S. Immigration and Custom Enforcement, “$39.5M in counterfeit sports merchandise seized ahead of Super Bowl LIX,” ice.gov.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Apparel Anchors Revenue While Toys Capture Collectors

In 2025, apparel accounted for 44.76% of the market share, driven by the increasing popularity of jersey sales transitioning from game-day attire to everyday streetwear. The Toys and Games segment is projected to grow at an annual rate of 6.81% through 2031. Funko Incorporated reported that its Jason Kelce Pop! figure was the top-selling collectible in 2024. The company is focusing on expanding its presence in the sports memorabilia market by increasing its licensing agreements with various organizations. In the footwear segment, signature athlete lines, such as Nike's Jordan Brand, continue to drive growth. This trend highlights how performance footwear can achieve premium pricing when endorsed by well-known celebrities. Headwear remains an important category, with New Era Cap holding the exclusive sideline cap contract for the National Football League (NFL), ensuring consistent demand from both fans and players.

The Equipment and Accessories segment also attracts consumer spending, as items like balls, gloves, and training aids are frequently purchased alongside apparel. Personalized sporting equipment further contributes to the growth of this segment. Apparel continues to dominate the market due to its dual role as functional sportswear and a means of expressing personal identity. Additionally, the rapid growth of the Toys and Games segment reflects a shift from one-time purchases to long-term collecting behaviors, which help generate recurring revenue streams. This shift underscores the evolving consumer preference for collectibles that hold sentimental and monetary value over time.

By Sports: Football Dominates Yet Basketball Accelerates Internationally

Football, also referred to as soccer, accounted for 33.12% of sport-specific revenue in 2025, primarily driven by leagues such as the English Premier League, La Liga, and Serie A. These leagues collectively license merchandise to over 200 countries, showcasing their extensive global reach. In comparison, basketball is expected to grow at an annual rate of 6.97% through 2031, supported by the National Basketball Association (NBA). The NBA has been expanding its global footprint by opening flagship stores in cities such as Manila and Mexico City and licensing Name, Image, and Likeness (NIL) jerseys for college athletes, further enhancing its market appeal.

India's cricket economy generated significant revenue in a recent year, with cricket contributing the largest share to the nation’s sports economy. Indian Premier League (IPL) franchises reported substantial earnings during the same period, with a considerable portion derived from jersey sales and branded merchandise. In North America, baseball maintains a dedicated fanbase, with Major League Baseball (MLB) generating notable annual licensing fees. However, its growth remains constrained due to limited international market penetration. American football has expanded its global presence through the National Football League’s (NFL) recent international games, which drew large crowds and achieved higher international viewership compared to the previous year. The “Others” category, encompassing sports such as hockey, motorsports, tennis, and combat sports, serves smaller but loyal fanbases, creating niche opportunities for merchandise. For instance, Formula 1 secured a long-term sponsorship agreement with Louis Vuitton Moët Hennessy (LVMH), valued at a significant annual amount, incorporating Louis Vuitton branding into race-day merchandise positioned at premium price points.

By Distribution Channel: Offline Holds Share as Online Surges

In 2025, offline retail accounted for 59.14% of the market share, supported by stadium concessions, specialty sporting goods stores, and department store partnerships. These channels offer tactile product experiences and immediate consumer satisfaction. However, online retail is projected to grow at an annual rate of 6.90% through 2031. Sports and recreation e-commerce transactions saw significant year-over-year growth between late 2024 and late 2025. Fanatics Incorporated, which operates online platforms for the National Football League (NFL), Major League Baseball (MLB), and National Basketball Association (NBA), anticipated that the league’s official online store would generate substantial revenue by the mid-2020s. This underscores the potential of league-branded storefronts to secure a significant portion of online spending.

Furthermore, the International Trade Administration estimates that global business-to-consumer e-commerce revenue will grow at a compound annual growth rate (CAGR) of 14.4% [3]Source: International Trade Administration, “2024 eCommerce Size & Sales Forecast,” trade.gov. Additionally, Fanatics Incorporated projected that the league’s official online store would generate significant revenue, contributing to the overall growth of the online retail market. The increasing adoption of online platforms highlights the shift in consumer preferences and spending patterns, with a growing emphasis on convenience and accessibility in the retail landscape.

By End User: Adults Dominate Spending While Kids Segment Grows

Adults accounted for 82.84% of end-user demand in 2025, driven by higher disposable income and the growing trend of "kidults," referring to adults purchasing toys and collectibles. This group contributed USD 9.3 billion, or 25%, of the United States toy revenue in 2022. Meanwhile, the Kids or Children segment is projected to grow at an annual rate of 6.93% through 2031, supported by youth sports participation platforms like GameChanger. GameChanger, owned by DICK'S Sporting Goods, generated over USD 100 million in revenue during fiscal 2024 and had more than 9 million unique active users in the same period. The platform provides a direct channel to parents purchasing team uniforms, equipment, and branded merchandise.

In the United States, Name, Image, and Likeness (NIL) regulations now allow college athletes to license their jerseys, creating a new revenue stream that appeals to younger fans who follow collegiate sports more closely than professional leagues. In India, the athlete endorsement market grew by 32% to INR 1,224 crore in 2024, with cricket stars like Virat Kohli and Rohit Sharma driving youth merchandise sales through social media campaigns and brand partnerships. The Kids or Children segment benefits from parental willingness to invest in youth sports participation, which is perceived as both recreational and developmental. Additionally, gifting occasions such as birthdays, holidays, and team celebrations create predictable demand cycles. In contrast, adult collectors exhibit purchasing behaviors similar to luxury goods buyers, focusing on limited-edition releases, autographed memorabilia, and vintage items that appreciate in value. The convergence of these segments is evident in multi-generational product lines, such as matching parent-child jerseys, which encourage incremental spending by appealing to family identity rather than individual fandom.

Geography Analysis

North America emerged as the leading segment in the global sports merchandise market in 2025, contributing 61.42% of the total revenue. This leadership position is attributed to the presence of well-established professional leagues, such as the National Football League (NFL), Major League Baseball (MLB), and the National Basketball Association (NBA), which drive consistent demand for licensed merchandise. Additionally, the region benefits from high per-capita spending on sports-related products and a robust, vertically integrated retail infrastructure that ensures efficient distribution. However, the maturity of the North American market has led to limited pricing power, compelling retailers to prioritize convenience and customer experience over product innovation. Companies like Fanatics and DICK'S Sporting Goods, which operate with vertically integrated models, are better positioned to thrive in this competitive environment compared to traditional wholesale distributors.

The Asia-Pacific region is the fastest-growing segment in the sports merchandise market, with an anticipated annual growth rate of 7.81% through 2031. This growth is driven by factors such as China’s objective of developing a multitrillion-dollar sports industry and India’s expanding cricket-focused economy. In China, the growing middle class is expected to provide a substantial consumer base with increased discretionary income for licensed sports merchandise. Similarly, in India, the sports merchandise market is gaining traction, as demonstrated by rising unit sales on platforms like FanCode and playR during recent Indian Premier League seasons. These trends underscore the region’s increasing demand for sports-related products and its potential to emerge as a significant player in the global market.

Other regions are also making notable contributions to the sports merchandise market. Europe benefits from football's deep cultural integration, with leagues such as the English Premier League (EPL), La Liga, and Bundesliga licensing merchandise in over 200 countries. South America is experiencing rapid growth, particularly in Brazil and Argentina, where football fandom drives strong demand for jerseys and other merchandise. Additionally, Formula 1's expansion into new circuits within the region is further boosting merchandise sales. The Middle East and Africa, while smaller in market size, are witnessing fast-paced growth driven by sovereign wealth fund investments in sports franchises and related retail ventures. Furthermore, the rise of digital streaming platforms is enabling access to previously untapped fanbases, bypassing the limitations of traditional broadcast models and creating new opportunities for merchandise sales.

Competitive Landscape

The licensed sports merchandise market is primarily controlled by vertically integrated retailers and brand licensors who manage distribution channels, licensing agreements, and direct-to-consumer platforms. Fanatics Incorporated, a prominent player in this market, operates e-commerce platforms for major leagues such as the National Football League (NFL), Major League Baseball (MLB), and National Basketball Association (NBA). The company solidified its position by entering a long-term partnership with World Wrestling Entertainment (WWE) in 2025 and acquiring Mitchell & Ness in 2024 to expand into the throwback jersey segment. These initiatives have positioned Fanatics as a key infrastructure provider for digital merchandise sales.

Nike Incorporated reported notable revenue growth in its Jordan Brand during 2024, highlighting the potential of signature athlete lines to compete with entire sports categories. Adidas AG and Puma SE are renewing multi-year contracts with football clubs and basketball stars to sustain their market share. However, they face growing competition from Chinese companies such as Anta Sports Products Limited and Li-Ning Company Limited. These firms increased their global market share in 2024 compared to 2022 by offering competitive pricing and expanding retail operations across Southeast Asia.

DICK'S Sporting Goods, operating hundreds of retail locations, generated significant revenue from vertical and licensed brands, which accounted for a substantial portion of its total sales. The company's ScoreCard loyalty program, with millions of enrolled members, played a crucial role in driving repeat purchases, demonstrating the effectiveness of customer data platforms in converting foot traffic into sales. Strategic trends in the market reveal a division between premium and mass-market approaches. For example, luxury fashion partnerships, such as LVMH's (Moët Hennessy Louis Vuitton) long-term Formula 1 sponsorship valued at nearly USD 100 million annually, have elevated licensed products into high-value collectibles. At the same time, direct-to-consumer channels are bypassing traditional wholesale margins and leveraging first-party data to enhance product development and inventory management.

Licensed Sports Merchandise Industry Leaders

Fanatics Inc.

DICK'S Sporting Goods, Inc.

Rally House

New Wave Group AB

New Era Cap

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Nike and the National Football League (NFL) have introduced the Rivalries program, which will feature new uniforms and fan gear inspired by local communities for rivalry games over the next four seasons. This initiative emphasizes community engagement while creating new merchandise categories tied to specific matchups and regional identities.

- March 2025: Nike, in partnership with TOGETHXR, introduced the "Everyone Watches Women's Sports" collection. This initiative aims to enhance the visibility of women's sports and increase recognition for female athletes. The collaboration highlights the growing focus on women's sports merchandise, emphasizing its status as a fast-growing market segment.

- March 2025: Adidas announced its third collaboration with Liverpool Football Club, set to begin in the 2025/26 season. This multi-year partnership includes match kits, training apparel, and cultural wear for all teams and staff members, with the first kits scheduled for release in August 2025.

- January 2025: Adidas partnered with the Mercedes-AMG PETRONAS F1 Team through a multi-year agreement, producing a complete range of apparel, footwear, and accessories. The collaboration aimed to engage new generations of fans by introducing lifestyle products that combined motorsport and fashion elements.

Global Licensed Sports Merchandise Market Report Scope

The licensed sports merchandise market comprises officially authorized products featuring team, league, or athlete branding, sold across retail and digital channels to fans seeking authenticated apparel, equipment, collectibles, and accessories that generate royalty revenue.The market is segmented by product category, it includes apparel, footwear, headwear, equipment and accessories, and toys and games. By sports, it covers football/soccer, basketball, baseball, American football, and others. By distribution channel, the segmentation includes offline retail and online retail. By end user, the market is divided into adults and children. Geographically, the market spans North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Apparel |

| Footwear |

| Headwear |

| Equipment and Accessories |

| Toys and Games |

| Football/Soccer |

| Basketball |

| Baseball |

| American Football |

| Others |

| Offline Retail |

| Online Retail |

| Adults |

| Kids / Children |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Singapore | |

| Indonesia | |

| Thailand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Category | Apparel | |

| Footwear | ||

| Headwear | ||

| Equipment and Accessories | ||

| Toys and Games | ||

| By Sports | Football/Soccer | |

| Basketball | ||

| Baseball | ||

| American Football | ||

| Others | ||

| By Distribution Channel | Offline Retail | |

| Online Retail | ||

| By End User | Adults | |

| Kids / Children | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Singapore | ||

| Indonesia | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will global spending on officially licensed team products be by 2031?

The licensed sports merchandise market size is projected to reach USD 59.59 billion by 2031, reflecting a 5.78% CAGR from 2026.

Which product category is growing fastest after jerseys?

Toys and games are set to expand 6.81% annually through 2031, driven by adult collectors and esports figurines

Which region offers the strongest growth opportunity for brands?

Asia-Pacific is expected to register an 7.81% CAGR as China and India scale licensed sports programs

How are digital channels changing merchandise sales?

Online transactions grew 6.90% year over year in November 2025, and mobile now accounts for two-thirds of traffic, forcing brands to refine app-based shopping

What role do luxury houses play in sports licensing?

Partnerships with firms such as LVMH push average selling prices higher and position select items as collectibles rather than simple fan gear

Page last updated on: