Fitness Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

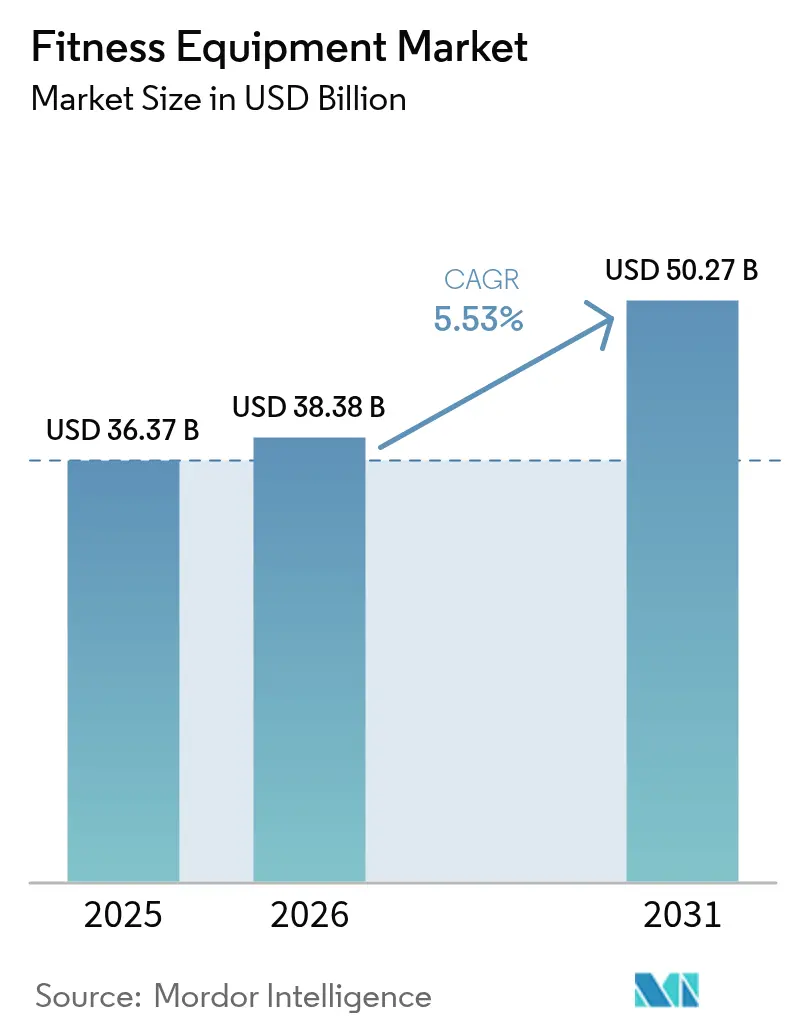

| Market Size (2026) | USD 38.38 Billion |

| Market Size (2031) | USD 50.27 Billion |

| Growth Rate (2026 - 2031) | 5.53% CAGR |

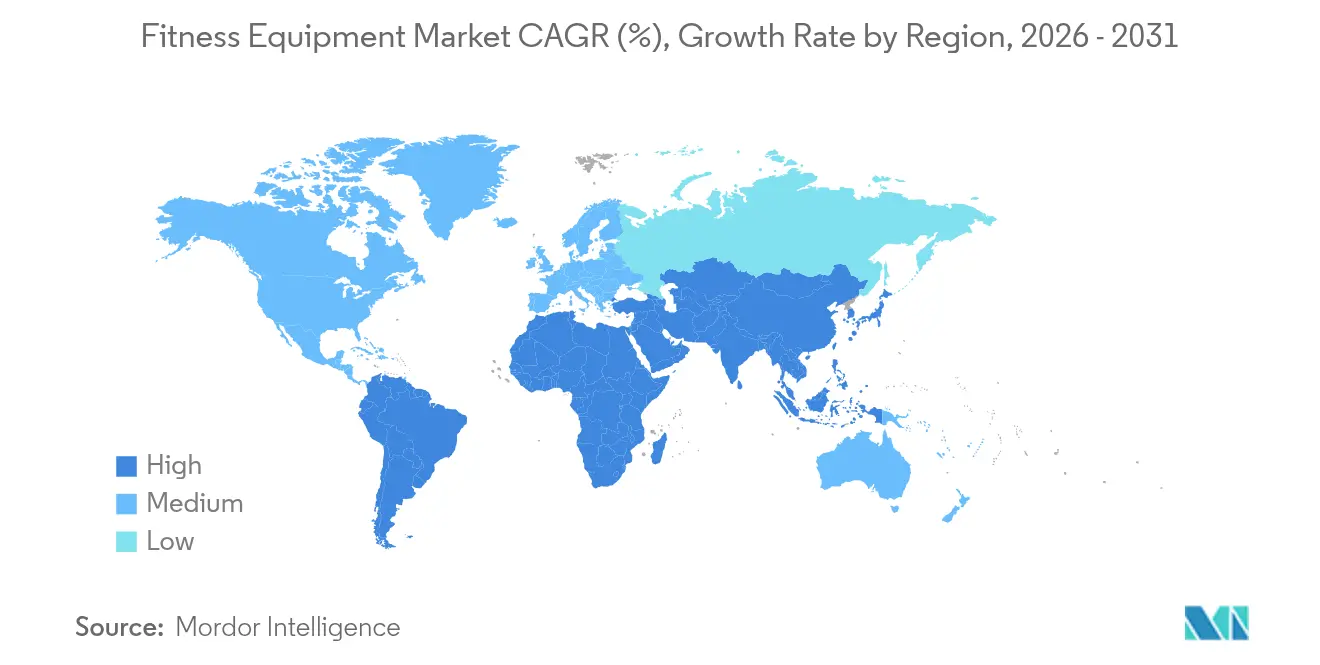

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Fitness Equipment Market Analysis by Mordor Intelligence

The fitness equipment market size was valued at USD 36.37 billion in 2025 and estimated to grow from USD 38.38 billion in 2026 to reach USD 50.27 billion by 2031, at a CAGR of 5.53% during the forecast period (2026-2031). The increasing prevalence of global obesity, the rising economic burden of physical inactivity, and policy initiatives promoting preventive healthcare are fueling market demand. Manufacturers are leveraging the growing consumer preference for data-driven, personalized workout experiences by incorporating digital features into traditional fitness equipment designs. Additionally, health insurers and employers are increasingly subsidizing equipment purchases to mitigate long-term healthcare costs. In the Asia-Pacific region, rapid urbanization and rising disposable incomes are significantly contributing to first-time equipment purchases. Meanwhile, in Europe, the mature market infrastructure is driving demand for replacement cycles and technology upgrades in the fitness equipment market. The competitive landscape remains moderately intense, providing opportunities for niche brands to gain market share. Companies specializing in eco-friendly designs or connected hardware ecosystems are particularly well-positioned to capitalize on evolving consumer preferences and technological advancements in the fitness equipment market.

Key Report Takeaways

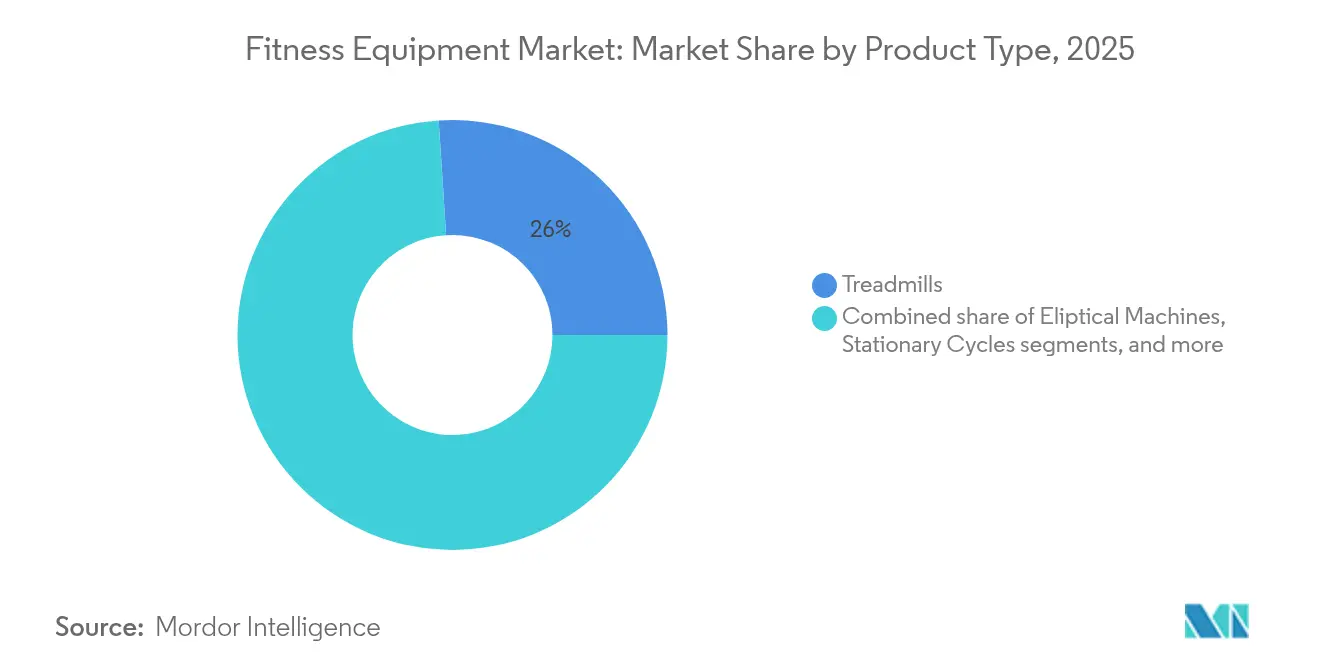

- By product type, treadmills led with 26.02% of fitness equipment market share in 2025, while strength training equipment is forecast to grow at 5.86% CAGR to 2031.

- By category, the conventional segment held 74.85% revenue share in 2025, and smart/connected devices are set to expand at a 6.18% CAGR through 2031.

- By end use, the commercial segment accounted for 76.92% of the fitness equipment market size in 2025, whereas the residential segment is advancing at 7.06% CAGR through 2031.

- By price range, the mass segment captured 67.92% share of the fitness equipment market size in 2025, and the premium segment is projected to climb 6.74% CAGR through 2031.

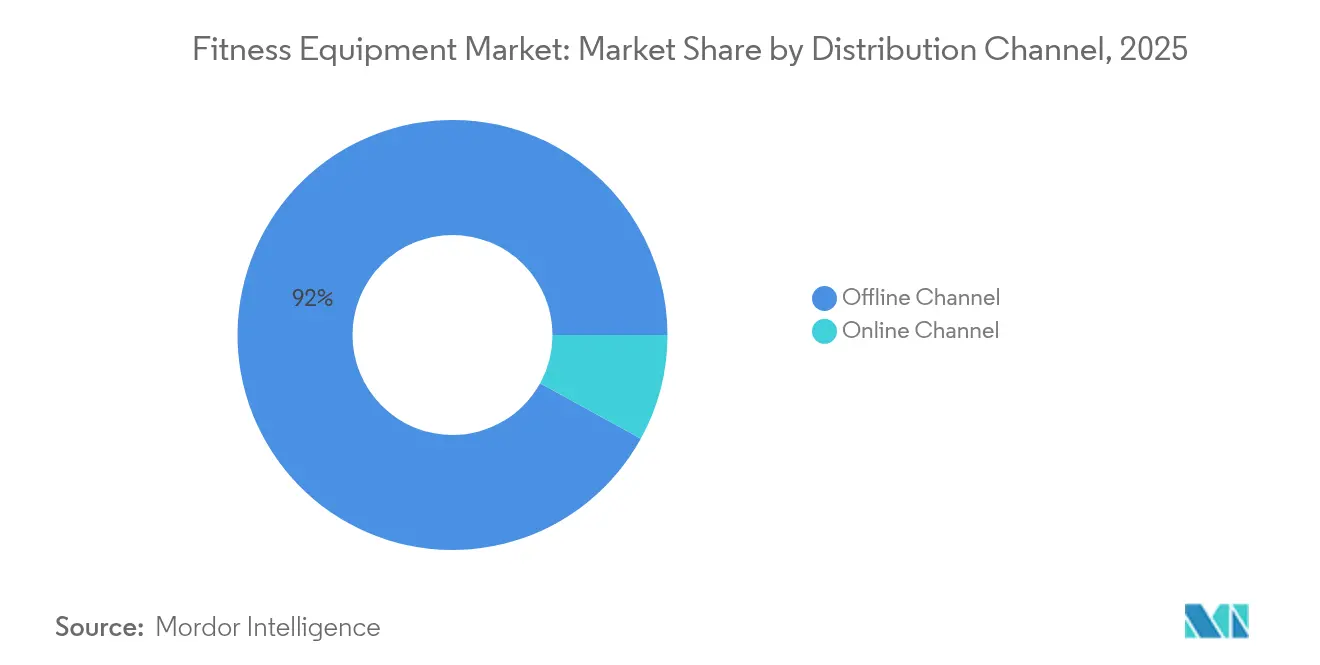

- By distribution channel, offline retail dominated with 91.98% of sales in 2025, and the online retail channel is growing at 6.92% CAGR through 2031.

- By geography, Europe commanded 39.05% revenue share in 2025, and Asia-Pacific is set to register the fastest 7.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fitness Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising influence of healthy lifestyle | +1.2% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Increasing prevalence of obesity and lifestyle diseases | +1.8% | Global, particularly acute in North America, Europe, and urban Asia-Pacific | Long term (≥ 4 years) |

| Technological advancements in equipments production | +0.9% | Global, led by North America and Europe innovation hubs | Short term (≤ 2 years) |

| Rising popularity of home fitness | +1.1% | Global, with highest penetration in developed markets | Medium term (2-4 years) |

| Hybrid and flexible fitness models | +0.7% | Primarily North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Influence of social media and fitness influencers | +0.6% | Global, strongest in markets with high social media penetration | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising influence of healthy lifestyle

Wellness has evolved from a passing trend into a fundamental aspect of daily life, driving consistent growth in fitness equipment demand across diverse demographic groups. The American College of Sports Medicine's 2025 fitness trends survey highlights wearable technology as the top global trend, reflecting its widespread adoption. Traditional strength training and high-intensity interval training also remain prominent, emphasizing the continued reliance on equipment-based fitness routines. This shift is particularly evident among younger demographics, who increasingly consider fitness equipment an essential component of home infrastructure rather than a discretionary purchase. The growing focus on sustainability in modern lifestyles further drives the need for eco-friendly equipment designs and energy-efficient technologies, reflecting a broader commitment to environmentally conscious health and wellness practices in the fitness equipment market.

Increasing prevalence of obesity and lifestyle diseases

The global obesity epidemic has escalated significantly, with over 1 billion individuals now living with obesity—a figure that has doubled since 1990. This surge has created an unprecedented demand for effective intervention solutions. According to the WHO's European Regional Obesity Report, in 2024, 35 million children under the age of five were classified as overweight. Additionally, in 2022, over 390 million children and adolescents aged 5 to 19 were overweight, including 160 million living with obesity[1]Source: World Health Organization, "Obesity and Overweight", www.who.int. The economic consequences are profound, as the WHO projects nearly 500 million new cases of non-communicable diseases by 2030, which could cost the global economy approximately USD 300 billion. Healthcare systems are increasingly integrating structured exercise programs into medical interventions, marking a shift where fitness equipment is no longer seen as solely recreational but as a critical healthcare tool in the fitness equipment market.

Technological advancements in equipments production

AI integration, biometric monitoring, and adaptive resistance systems are transforming the fitness equipment landscape by enabling real-time workout personalization. EGYM exemplifies this innovation with its Smart Strength Squat systems, which feature guided training protocols designed to optimize user performance. Additionally, its Fitness Hub platforms leverage advanced 3D camera technology to deliver immediate and precise movement analysis, enhancing training efficiency. Technogym's Kinesis Personal system incorporates FullGravity Technology, enabling tri-dimensional movement patterns that closely replicate functional training scenarios, while its 15.6-inch touchscreen interfaces provide an engaging and immersive user experience. The integration of IoT connectivity further enhances functionality by allowing equipment to seamlessly sync with health apps, wearable devices, and virtual coaching platforms, creating interconnected and comprehensive fitness ecosystems in the fitness equipment market. On the manufacturing side, advancements in automation and precision engineering are driving mass customization, enabling equipment to be tailored to diverse user requirements with greater efficiency and accuracy.

Rising popularity of home fitness

Home fitness has evolved into a permanent consumer behavior, supported by sustained demand for fitness equipment. According to data from UN Comtrade, the value of the United Kingdom's imports of exercise, gymnastics, athletics, and other sports equipment reached 1.1 billion British Pounds in 2024, marking an increase of 101.9 million British Pounds (+10.03 percent) compared to 2023. This growth highlights a significant shift driven by convenience, cost efficiency, and advancements in home fitness technology that now rival professional gym setups[2]Source: UN Comtrade, "Value of articles and equipment for physical exercise, gymnastics, athletics and other sports imported to United Kingdom (UK) from 2015 to 2024", www.trademap.org. The elimination of commute times, gym membership fees, and rigid schedules has been pivotal in driving consumer adoption. Additionally, space-saving equipment designs cater to urban living constraints, making home fitness more accessible. The market is also witnessing increased penetration through family-oriented fitness solutions, with equipment designed to accommodate multiple user profiles and age groups. This trend is fostering household-level adoption, transitioning the focus from individual purchases to collective family engagement in fitness activities in the fitness equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced fitness equipment | -0.8% | Global, most acute in emerging markets and price-sensitive segments | Medium term (2-4 years) |

| Preference for outdoor activities | -0.5% | Primarily temperate climate regions, seasonal impact in others | Short term (≤ 2 years) |

| Space constraints for home equipment | -0.6% | Urban centers globally, particularly acute in Asia-Pacific dense cities | Long term (≥ 4 years) |

| Maintenance complexity and high after-sales costs | -0.4% | Global, with higher impact in regions with limited service infrastructure | Medium term |

| Source: Mordor Intelligence | |||

High cost of advanced fitness equipment

The high pricing of technologically advanced fitness equipment continues to create substantial barriers to market penetration, particularly in price-sensitive segments and emerging economies where limited disposable incomes restrict adoption rates. In 2024, the mass market segment accounts for 68.46% of the market share but remains constrained by affordability challenges. These challenges are most evident among middle-income consumers, who represent the largest potential growth segment but face financial limitations. Additionally, rising manufacturing costs, driven by persistent supply chain disruptions and component shortages, are intensifying pricing pressures across the industry. Manufacturers are increasingly tasked with finding a balance between incorporating advanced features and ensuring market accessibility. Furthermore, the U.S. Consumer Product Safety Commission's updated safety standards for stationary activity centers, set to take effect in July 2025, are expected to increase compliance costs, further impacting equipment pricing. While financing options and subscription models are emerging as potential solutions to improve affordability, their effectiveness is limited by regulatory complexities and stringent credit requirements, which continue to hinder broader market access in the fitness equipment market.

Preference for outdoor activities

The increasing focus on outdoor physical activities is creating a significant challenge for the adoption of indoor fitness equipment. This trend is particularly evident in regions with favorable climates and well-developed outdoor infrastructures, which offer cost-free alternatives to equipment-based exercise. Government-driven urban planning initiatives, such as the development of walkable cities, expanded cycling networks, and outdoor fitness parks, are intensifying competition for home and commercial fitness equipment manufacturers. Outdoor exercise also provides psychological benefits, including stress reduction and mood enhancement, which are difficult for indoor equipment to replicate, especially among environmentally conscious consumers who prioritize sustainable and nature-oriented activities. Furthermore, seasonal variations in outdoor activity preferences lead to demand fluctuations, complicating inventory management and sales forecasting for manufacturers. Additionally, the evolving impacts of climate change are expected to influence regional outdoor exercise patterns, adding another layer of complexity to market dynamics in the fitness equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Treadmill Dominance and Strength Training Surge

In 2025, treadmills maintain a leading 26.02% market share, highlighting their broad appeal across various age groups and fitness levels. This dominance is attributed to their versatility, supporting activities such as walking, running, rehabilitation, fitness maintenance, and performance training. The equipment's ability to deliver controlled, measurable exercise experiences that can be easily tracked and adjusted appeals to goal-driven consumers who prioritize tangible fitness outcomes. Additionally, the established familiarity with treadmills reduces purchase hesitation among consumers. The Australian Government's focus on safety standards for exercise equipment, as seen in its exercise bike safety guide, underscores the importance of safety features in treadmill design.

Strength training equipment is projected to be the fastest-growing segment, with a 5.86% CAGR forecasted for 2026-2031. This growth is driven by a significant consumer shift toward muscle-building and functional fitness, emphasizing resistance-based workouts. The increasing focus on strength training aligns with advancements in fitness science, which highlight its critical role in improving metabolic health, maintaining bone density, and preventing injuries, particularly among aging populations. The segment benefits from a wide variety of equipment, ranging from free weights to advanced resistance machines, enabling manufacturers to cater to diverse price points and spatial requirements in the fitness equipment market.

By Category: Conventional Stability and Smart Equipment Innovation

In 2025, conventional equipment commands a dominant 74.85% market share, underscoring its appeal to consumers prioritizing mechanical reliability, reduced maintenance, and cost-effectiveness. These attributes resonate with budget-conscious buyers and commercial entities that value durability over digital enhancements. The segment's robustness stems from its reliance on tried-and-true technology, ensuring consistent performance devoid of concerns like software updates, connectivity hiccups, or the looming threat of digital obsolescence—issues often associated with smart equipment in the fitness equipment market.

Smart and connected equipment is on a rapid ascent, projected to grow at a 6.18% CAGR from 2026 to 2031. This surge is fueled by a growing consumer appetite for tailored, data-centric fitness experiences that seamlessly weave into larger health and wellness frameworks. A testament to this segment's sophistication and its divergence from conventional counterparts is EGYM's 2025 rollout, showcasing AI-driven workout personalization and 3D movement analysis via cameras. The connected equipment realm is riding the wave of a broader movement towards health data amalgamation in the fitness equipment market.

By End Use: Commercial Foundation and Residential Revolution

In 2025, commercial end use dominates the market with a commanding 76.92% share, driven by substantial investments in fitness equipment by gyms, fitness centers, corporate wellness programs, and healthcare institutions. These entities demand equipment that offers durability, multi-user functionality, and professional-grade performance to meet the rigorous requirements of their operations. The segment's dominance is attributed to the high-volume and high-value nature of commercial purchases, where a single facility may procure dozens of equipment units, creating significant revenue opportunities for manufacturers. Commercial fitness equipment is designed with enhanced durability, extended warranties, and specialized service support, which justify its premium pricing and ensure reliable performance under intensive usage in the fitness equipment market.

The residential segment is experiencing rapid growth, with a projected CAGR of 7.06% from 2026 to 2031. This growth highlights a lasting shift in consumer behavior toward home-based fitness solutions in the fitness equipment market, driven by the need for convenience, privacy, and long-term cost savings compared to traditional gym memberships. Several factors contribute to this expansion, including the development of space-efficient equipment designs, advancements in technology integration, and the availability of home fitness content and services that now rival the experience offered by commercial gyms.

By Distribution Channel: Offline Dominance and Digital Transformation

In 2025, offline channels command a dominant 91.98% market share, underscoring consumers' preference for hands-on product evaluations and consultations, especially for high-stakes purchases like complex equipment. This segment thrives on the tactile assessment of fitness equipment, where consumers prioritize comfort, functionality, and build quality, knowing these choices impact their long-term fitness journeys. Offline channels not only ensure immediate product availability but also offer professional installation and local service support, enhancing the purchase experience and alleviating perceived risks in the fitness equipment market.

Online channels, however, are on a rapid ascent, projected to grow at a 6.92% CAGR from 2026 to 2031. This surge is fueled by advancements in product visualization, in-depth customer reviews, and improved delivery and installation services, all aimed at overcoming traditional online shopping hurdles for sizable, intricate products. Manufacturers are increasingly adopting direct-to-consumer strategies, sidestepping retailer margins and gaining enhanced customer data and relationship management insights. The e-commerce boom is further bolstered by the trend of connected equipment, where digital integration resonates with tech-savvy consumers, making online purchases feel intuitive in the fitness equipment market.

By Price Range: Mass Market Foundation and Premium Acceleration

In 2025, mass segment commands a dominant 67.92% share, catering to budget-conscious consumers and fundamental fitness needs. These cost-effective solutions prioritize essential functionality over advanced features or luxury materials. The segment's strength lies in its accessibility and widespread market appeal, targeting the largest demographic that desires reliable fitness equipment without the hurdles of premium pricing. By leveraging economies of scale in manufacturing, standardized component sourcing, and a streamlined feature set, mass market products manage to keep production costs low while upholding acceptable quality standards in the fitness equipment market.

Meanwhile, the premium equipment segment is on a faster trajectory, boasting a 6.74% CAGR for 2026-2031. This growth is fueled by affluent consumers who are drawn to advanced features, superior build quality, and unique experiences. These attributes not only justify the higher price points but also promise enhanced performance and durability. The premium segment stands out by integrating technological advancements, showcasing features like AI-driven personalization, sophisticated biometric monitoring, and engaging digital experiences that set them apart in the market. This shift in consumer behavior underscores a broader trend: fitness is evolving from a mere recreational activity to a vital lifestyle component. As a result, affluent consumers now prioritize quality and durability in their purchasing decisions in the fitness equipment market.

Geography Analysis

In 2025, Europe holds the largest market share at 39.05%, driven by its advanced fitness infrastructure, high disposable income levels, and robust healthcare systems that emphasize preventive care. Regulatory frameworks across the region actively promote physical activity as a public health priority, further strengthening the market. The region benefits from a well-established gym culture and government initiatives encouraging physical activity. A 2023 WHO/OECD report highlighted that increasing physical activity could save the EU nearly EUR 8 billion annually in healthcare costs, reinforcing policy support for fitness equipment adoption. Decades of fitness culture development have positioned Europe as a market leader, with countries like Germany, Italy, and France facing significant economic burdens due to insufficient physical activity. This creates both a lucrative market opportunity and a pressing policy focus to address these challenges within the fitness equipment industry.

Asia-Pacific is emerging as the fastest-growing region, with a projected CAGR of 7.22% for the 2026-2031 period. The region's growth is fueled by rapid urbanization, rising disposable incomes, increasing health consciousness, and government-led initiatives promoting physical activity. These factors are driving demand across markets with varying levels of development. A notable example of this growth trajectory is Johnson Health Tech's USD 100 million investment in a new factory in Vietnam, scheduled to begin construction in Q1 2025 and commence operations by 2026. This investment underscores the region's dual role as a manufacturing hub and a growing consumption center in the fitness equipment industry.

North America represents a mature market characterized by widespread home fitness adoption and a preference for premium equipment. High disposable incomes and extensive fitness infrastructure support this trend across the fitness equipment industry. The region pioneered the connected fitness segment, with companies like Peloton initially defining the category. However, market saturation and rising competition have introduced challenges for such players. In South America, urbanization and the expansion of the middle class are driving emerging market dynamics. Meanwhile, Africa and Western Asia exhibit significant growth potential, although infrastructure limitations and economic volatility remain key constraints. Globally, the obesity epidemic, affecting over 1 billion people as reported by the World Health Organization, drives universal demand for fitness solutions. However, market accessibility is shaped by factors such as purchasing power and the pace of infrastructure development.

Regulatory Landscape

Safety and performance compliance for fitness equipment is increasingly anchored in harmonized standards and regulator-led requirements for stationary training equipment. ISO 20957-1:2024 (stationary training equipment, general safety requirements and test methods) has a corrected version published in February 2026, giving manufacturers an updated baseline when selling into multiple regions. ASTM standards, including ASTM F2276-23 (consumer safety specification for fitness equipment) and ASTM F2571-15(2020) (test methods and evaluation), continue to shape expectations around stability, structural integrity, and labeling for adult-use categories.

Region-specific rulemaking and trade administration are also influencing compliance costs and sourcing decisions. In the United States, the Consumer Product Safety Commission issued a July 2026 compliance directive for children's home fitness equipment (ages 3 to 12), increasing the focus on verifying locking and child-safety design features. China implemented GB/T 17498.1-2026 for indoor stationary fitness equipment safety, tightening local conformity requirements for products manufactured or sold into the market, while changes in the U.S. Harmonized Tariff Schedule and Section 232 coverage (including updates affecting HTS 9506.91.00 gym and exercise equipment in 2026) add planning complexity for importers and global brands managing landed cost and documentation.

Competitive Landscape

The Fitness Equipment Market is moderately consolidated, characterized by a mix of global leaders and emerging regional players that shape a competitive landscape. Prominent players such as Technogym S.p.A., Johnson Health Tech Co. Ltd., Life Fitness LLC, Core Health & Fitness LLC, and Peloton Interactive Inc. maintain dominance in the commercial and connected equipment segments by driving innovation and forming strategic alliances.

Technology integration remains a critical differentiator in the market. Companies like EGYM are at the forefront, utilizing AI-powered workout customization and 3D camera movement analysis to deliver advanced solutions and gain a competitive edge. The fragmented nature of the market presents significant opportunities for specialized players to cater to specific user groups, geographic regions, or technology-driven niches in the fitness equipment industry.

The fitness equipment industry dynamics reveal a growing shift toward ecosystem-based approaches. Equipment manufacturers are increasingly diversifying into content creation, service offerings, and data analytics to establish recurring revenue streams and strengthen customer retention. Emerging disruptors are challenging traditional retail-dependent incumbents by adopting direct-to-consumer models and subscription-based services. In response, established players are leveraging strategic partnerships, such as Peloton's collaboration with Costco, to expand their reach and tap into new customer segments.

Fitness Equipment Industry Leaders

-

Technogym S.p.A.

-

Johnson Health Tech Co. Ltd.

-

Life Fitness LLC

-

Core Health & Fitness LLC

-

Peloton Interactive Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Connected ecosystems are creating room for differentiated hardware bundles that combine equipment, coaching, and club-operator tooling, particularly where personalization and measurement drive purchase decisions. Technogym's July 2026 launch of the Technogym AI Ecosystem, built on data from more than 38 million connected users, shows how competitive advantage is moving toward software, content, and analytics layered on top of conventional cardio and strength footprints. This shift aligns with demand for data-driven, personalized training experiences and supports opportunities for manufacturers and gym operators to monetize recurring services (programming, insights, and performance tracking) rather than depending only on one-time equipment sales.

Category expansion beyond traditional cardio and strength is also opening new product lanes for residential and light-commercial settings, where space constraints shape buying behavior. NordicTrack and iFIT's Ultra 1 Reformer, released in July 2026 in Australia, indicates that connected Pilates is moving deeper into equipment roadmaps, widening addressable use cases for at-home studios and multi-user households. Alongside this, consolidation and platform roll-ups, including Interactive Strength Inc.'s July 2026 definitive agreement to acquire STEPR, reflect ongoing efforts to pair branded hardware with software experiences and distribution reach, supporting more integrated portfolios across price tiers and channels.

Recent Industry Developments

- May 2026: Technogym reported Q1 2026 consolidated revenue of EUR 237 million, marking 10.1% year-over-year growth. The update reinforced the company's continued investment capacity across connected products and services, influencing competitive intensity in premium commercial and smart/connected segments.

- October 2025: Johnson Fitness & Wellness partnered with Tonal to retail Tonal's all-in-one strength training system through its U.S. store network. The partnership strengthened omnichannel access to connected strength equipment and increased competitive pressure on incumbents that rely on proprietary retail or direct-to-consumer distribution.

- May 2024: Johnson Health Tech acquired the BowFlex and Schwinn Fitness residential brands along with the JRNY digital fitness platform. This transaction expanded its home-fitness portfolio and added a content and software layer that supports ecosystem-based differentiation across equipment categories.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers fitness equipment sold for structured physical activity, including cardio and strength machines, and related equipment used in homes and commercial facilities. Values are counted as equipment revenues in USD across major regions and typical sales channels.

Scope exclusions: We exclude consumables and non-equipment wellness services that do not involve the sale of fitness equipment hardware.

Segmentation Overview

-

By Product Type

- Treadmills

- Eliptical Machines

- Stationary Cycles

- Rowing Machines

- Strength Training Equipment

- Other Product Types

-

By Category

- Conventional

- Smart/Connected Equipment

-

By End Use

- Residential

- Commercial

-

By Price Range

- Mass

- Premium

-

By Distribution Channel

- Offline Channel

- Online Channel

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build a clean fact base on demand drivers, pricing direction, and channel mix for fitness equipment. We relied on public sources such as the World Health Organization for physical activity and obesity indicators, the US CDC for health behavior context, and World Bank macro series for income and inflation signals that affect discretionary purchases.

To connect demand to supply, we also reviewed trade and manufacturing signals from sources such as UN Comtrade, national statistics offices, and customs dashboards where available, along with patent databases to sense product innovation and feature adoption. These inputs were paired with company filings, investor presentations, and reputable press coverage to understand product mix shifts (connected features, replacement cycles, and commercial reopening effects) and to sanity-check directional assumptions. The sources listed here are illustrative, and many other public materials were also used for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what the model could not reliably infer from public data, especially mix changes across residential and commercial buyers and how pricing is moving by equipment type. We spoke with a spread of stakeholders across manufacturing, distribution, and buyer-side roles, and we made sure regional perspectives were covered so that assumptions on adoption and replacement timing were not built from one geography alone.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 14% | APAC: 44% |

| Mid tier: 56% | Functional/Unit leaders: 31% | EMEA: 32% |

| Smaller Players: 14% | Managers: 55% | Americas: 24% |

Market-Sizing & Forecasting

The sizing starts with a top-down build that reconstructs the demand pool by linking fitness participation and facility footprints to likely equipment replacement and first-time purchase needs, which are then translated into value using observed price bands. The total is then checked with selective bottom-up approximations, such as sampled average selling price (ASP) by equipment type multiplied by estimated unit volumes from channel discussions, before final totals are adjusted.

Key inputs used in the model include obesity and physical inactivity indicators, household income and consumer inflation, commercial gym openings and refurbishment cycles, online versus offline sales mix, and the share shift toward connected or feature-led equipment that can change ASPs. For forecasting, scenario analysis is applied around the main swing factors, and then the year-by-year path is smoothed using expert-agreed adoption and replacement timing assumptions so the curve does not overreact to one-time spikes. Where bottom-up signals are incomplete for smaller channels or informal retail, gaps are handled through conservative share assumptions that are later pressure-tested in interviews.

Data Validation & Update Cycle

We validate outputs by triangulating the modeled totals against independent signals, including macro trends, trade flow direction, and channel checks from interviews, followed by a second-pass review to confirm that country and regional sums behave logically. Outliers are flagged for rework when price, growth, or mix shifts look inconsistent with the supporting evidence, and respondents are re-contacted when a key assumption moves beyond a reasonable range.

Reports are refreshed annually, and interim updates are made when material events occur that can shift demand or pricing quickly. Before delivery, an analyst completes a fresh review so clients receive the most current view that matches the latest available data.

Mordor Intelligence's Fitness Equipment Market Market Sizing Compared With Other Published Estimates

Published market values for fitness equipment can look far apart because each publisher decides what to count as equipment revenue, how to treat connected features, and which sales routes are visible enough to include. Differences in base year selection also matter, since pricing and demand patterns have moved a lot across recent years.

Key gaps usually come from scope choices and the evidence used to convert unit activity into value. Some estimates lean heavily on factory-gate reporting or include services bundled with hardware, and others apply broad ASP inflation without checking if mix is shifting from entry products to premium connected models, or the other way around. Currency conversion timing and refresh cadence can further widen the spread when inflation is uneven across regions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 38.38 B (2026) | |

| Trade Publisher A | USD 36.37 B (2025) | Uses a prior base year, so the value reflects earlier pricing and demand conditions, and it may not fully capture recent mix changes across home and commercial buying. |

| Global Consultancy B | USD 15.81 B (2026) | Counts factory-gate values and can include manufacturer-sold services, which changes the boundary versus retail value capture and can understate multi-channel equipment revenues. |

Trade flow direction, replacement timing discussed by channel participants, and observed price-band movement are the checks that keep Mordor Intelligence tied to an equipment-only demand pool in 2026, rather than a manufacturing-only or services-included boundary. When these boundary choices are made explicit, the spread in the table becomes easier to interpret and the number is simpler to reuse in planning.

Key Questions Answered in the Report

What is the current value of the fitness equipment market?

The fitness equipment market size stands at USD 38.38 billion in 2026 and is expected to reach USD 50.27 billion by 2031.

Which region leads the global fitness equipment market?

Europe holds the leading 39.05% share, supported by well-established gym networks and preventive-health policies.

Which product category is growing the fastest?

Strength-training equipment is forecast to expand at a 5.86% CAGR between 2026 and 2031.

How quickly is the residential segment growing?

Home installations are advancing at 7.06% CAGR as consumers embed permanent workout spaces in their living environments.

Page last updated on: