Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

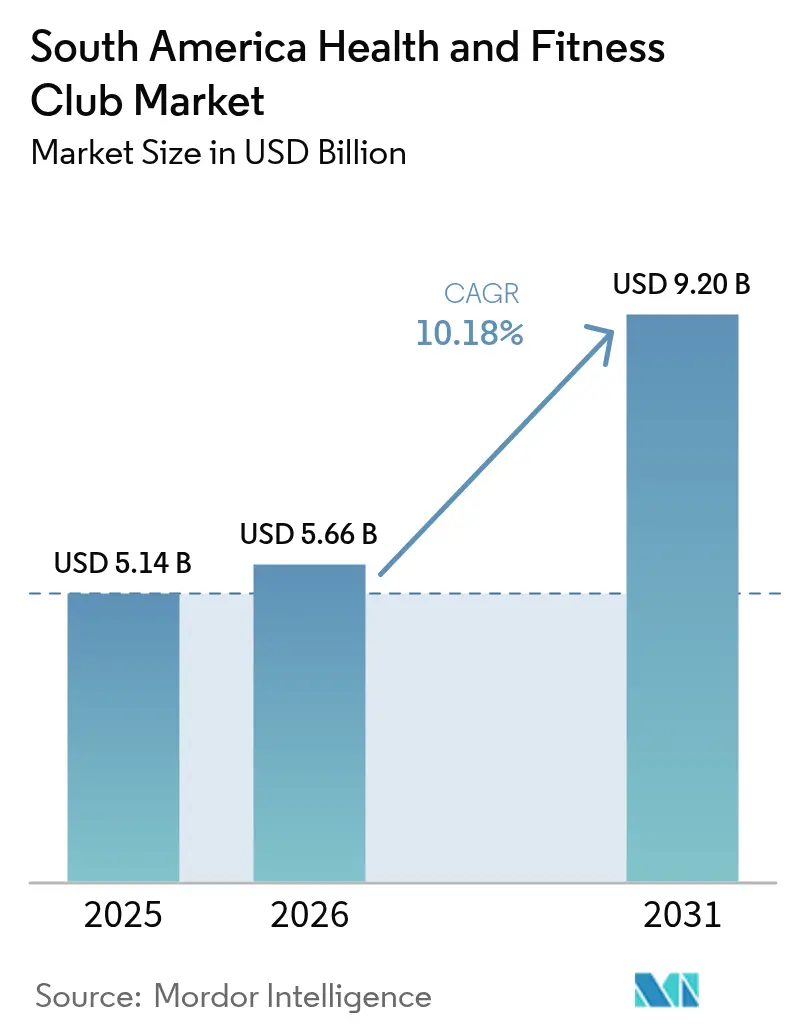

| Base Year Market Size (2025) | USD 5.14 Billion |

| Market Size (2026) | USD 5.66 Billion |

| Market Size (2031) | USD 9.2 Billion |

| Growth Rate (2026 - 2031) | 10.18% CAGR |

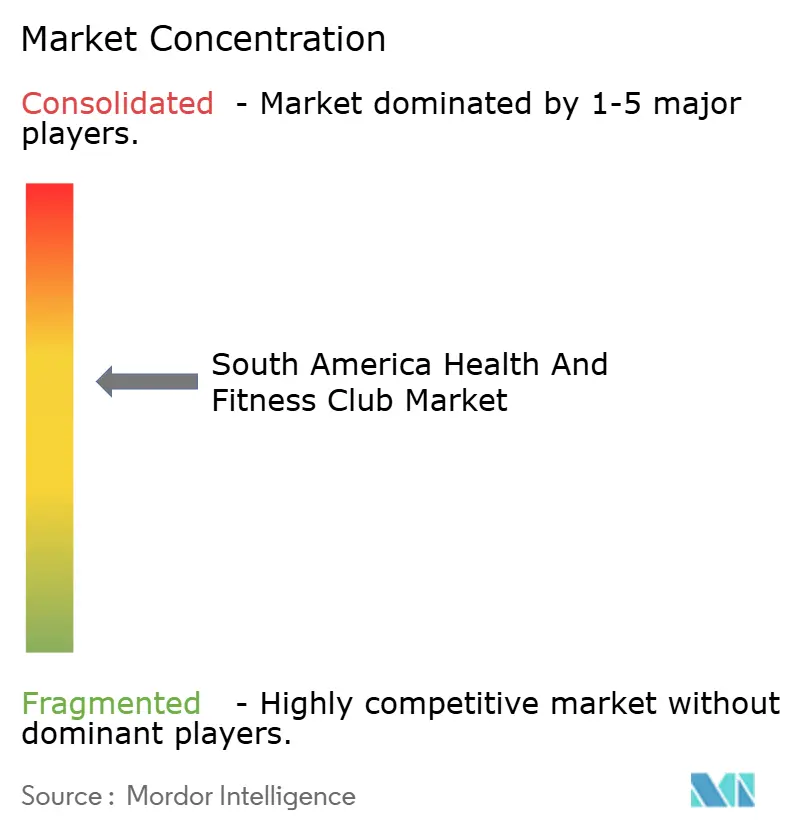

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South America Health And Fitness Club Market Analysis by Mordor Intelligence

The South American health and fitness club market size was valued at USD 5.14 billion in 2025 and estimated to grow from USD 5.66 billion in 2026 to reach USD 9.2 billion by 2031, at a CAGR of 10.18% during the forecast period (2026-2031). Demand is driven by a region-wide shift toward preventive health, expanding middle-income cohorts, and the introduction of scalable budget-friendly gym formats. Besides, public-sector obesity control campaigns, the professionalization of personal training, and steadily rising corporate wellness budgets further widen the addressable base. Brazil’s first-mover advantage in digital-fitness integration, Peru’s double-digit catch-up growth, and a wave of Pan-American university programs supplying trained instructors strengthen the ecosystem. Moreover, competitive dynamics remain fluid as international chains acquire local independents. However, in 2025, Brazil's Administrative Council for Economic Defense (CADE) levied fines exceeding BRL 300,000 on gym sector entities for engaging in anticompetitive practices, demonstrating the regulatory body's dedication to ensuring fair competition.

Key Report Takeaways

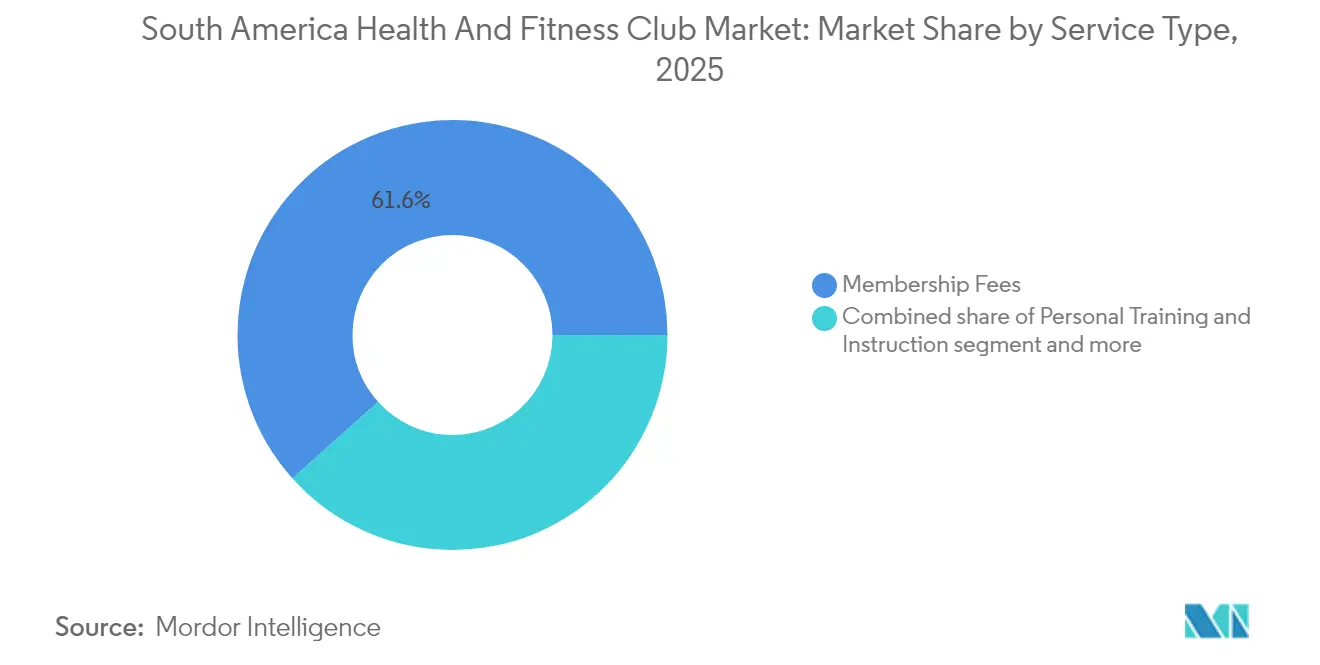

- By service type, membership fees led with 61.64% of the South American health and fitness club market share in 2025, whereas personal training and instruction services are advancing at an 11.36% CAGR through 2031.

- By outlet format, independent clubs held 67.82% share of the South American health and fitness club market size in 2025, while chained outlets are expanding at an 11.68% CAGR in the same period.

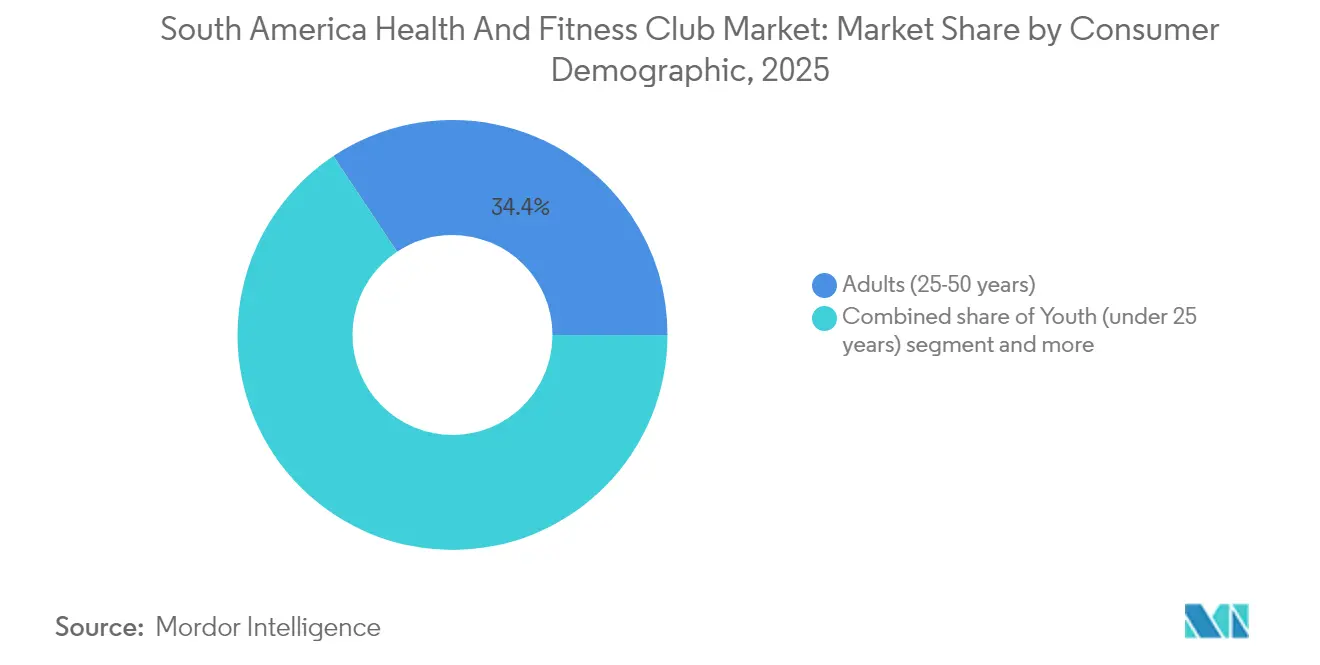

- By consumer demographic, adults aged 25-50 commanded 34.35% of the South American health and fitness club market size in 2025; the under-25 cohort shows the fastest 10.87% CAGR to 2031.

- By geography, Brazil captured 52.21% revenue share in 2025, whereas Peru is projected to grow at an 11.14% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Health And Fitness Club Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing focus on preventive health and fitness | +2.8% | Brazil, Argentina, Chile, Colombia | Medium term (2-4 years) |

| Prevalence of lifestyle diseases | +2.4% | Brazil, Argentina, Colombia, Peru | Long term (≥ 4 years) |

| Surge in digital-fitness adoption | +2.1% | Brazil, Mexico, Argentina | Short term (≤ 2 years) |

| Innovation in fitness offerings | +1.9% | Brazil, Chile, Peru, Colombia | Medium term (2-4 years) |

| Expansion of budget-friendly gym chains | +1.7% | Brazil, Peru, Argentina, Colombia | Long term (≥ 4 years) |

| Rising popularity of group fitness activities | +1.6% | Brazil, Argentina, Chile | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing focus on preventive health and fitness

Government-led health initiatives are driving significant changes in the fitness industry, positioning fitness clubs as critical components of community health strategies. Colombia’s Ministry of Health mandates adults to engage in either 150 minutes of moderate or 75 minutes of vigorous physical activity weekly, integrating fitness into national health policies [1]Source: Ministry of Health and Social Protection of Colombia, "Physical Activity", minsalud.gov.co. This aligns with the Pan American Health Organization’s strategic plan to combat the region's escalating obesity rates. In 2022, 67.5% of adults were classified as obese, with projections indicating this figure could rise to 73.2% by 2030 without intervention. These public health challenges are prompting policy reforms that support the fitness club sector. For instance, Brazil’s National Cancer Institute advocates physical activity as a preventive measure against cancer. Similarly, Argentina’s Ministry of Health incorporates physical activity promotion into its National School Health Program, fostering early fitness habits that could lead to sustained demand for fitness club memberships. These coordinated efforts are creating a regulatory framework where fitness clubs transition from discretionary services to essential public health resources. Brands like Smart Fit are leveraging this environment, expanding their presence as accessible health hubs. Together, these initiatives are fostering a supportive ecosystem that promotes widespread fitness adoption, driving sustained growth in the health and fitness club market across South America.

Rising popularity of group fitness activities

The increasing demand for group fitness activities is reshaping the dynamics of the health and fitness club market in South America. These activities not only enhance physical well-being but also foster a sense of community and engagement among participants. Classes such as Zumba, Brazilian Jiu-Jitsu, yoga, Pilates, and CrossFit are leading this shift, combining social interaction with structured, motivating workouts. This trend aligns with consumer preferences for inclusive and dynamic fitness experiences, moving beyond solitary gym visits. Companies like Megatlon and Bodytech have strategically leveraged this trend by offering extensive group class portfolios, creating vibrant, high-energy environments that appeal to millennials and Gen X demographics. Additionally, the communal aspect of group fitness strengthens member retention, as peer support and consistent attendance become integral. Operators are capitalizing on this by providing flexible class schedules and thematic sessions. Beyond traditional gym settings, cities such as São Paulo and Rio de Janeiro are experiencing a surge in outdoor and unconventional fitness experiences, including rooftop spin classes and beach boot camps, catering to individuals seeking novelty and social engagement. Digital integration further complements this trend, with live-streamed group sessions expanding access beyond physical locations. The growing participation in group fitness is driving market growth, enhancing competitiveness and vibrancy across the health and fitness sector in the region.

Innovation in fitness offerings

Boutique fitness innovations are reshaping the competitive dynamics of the health and fitness club market in South America by introducing specialized and community-focused approaches. CrossFit has established a strong foothold in Brazil's major cities, with affiliates such as Eros CrossFit in Pelotas and Taura Zona Sul CrossFit in Porto Alegre showcasing the rising demand for high-intensity, socially-driven fitness experiences. Bio Ritmo is driving premium innovation, with plans to expand into Chile, Peru, and Panama by 2025. The company targets affluent consumers through upscale facility designs and exclusive programming, enabling premium pricing strategies. Additionally, educational advancements are enhancing the talent pipeline. For example, Universidad San Ignacio de Loyola in Peru has launched a Sports and Physical Activity Sciences program, featuring advanced biomechanics labs and global partnerships. This initiative strengthens operators' ability to integrate specialized expertise. These developments collectively create differentiation and competitive advantages, allowing fitness operators to attract higher-value customers. By combining technology with tailored offerings, they are positioning themselves for sustainable growth in South America’s dynamic fitness landscape.

Expansion of budget-friendly gym chains

Budget-friendly gym chains are driving significant growth by making fitness more accessible to South America's expanding middle class. A 2024 survey by J. Wallin Opinion Research, commissioned by the Health & Fitness Association, found that 61% of Latin Americans in select urban areas work out at least twice a week. Notably, 55% of these active individuals prefer gyms and fitness facilities [2]Source: Health & Fitness Association, "2024 Latin America Fitness Consumer Survey", healthandfitness.org. Chains like Smart Fit are at the forefront of this movement, aggressively setting up in urban and less-explored areas. For instance, Smart Fit has strategically expanded its operations, reaching 736 gyms in Brazil, 339 in Mexico, and 454 across 13 other Latin American countries by 2024. They attract budget-conscious consumers with affordable memberships and strategic site selection. Smart Fit's approach melds physical gyms with digital fitness, using proprietary apps to boost customer loyalty. This push towards accessible fitness has led to consistent membership growth, even during economic ups and downs, aligning with the survey's findings on exercise frequency. Furthermore, these budget gyms emphasize convenience and community, crucial for member retention in a competitive landscape. Consequently, the budget segment is not just a player but a driving force in South America's fitness market, working in tandem with premium and boutique offerings.

Restaints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited access to modern fitness facilities outside major cities | -1.4% | Rural areas across Brazil, Argentina, Colombia | Long term (≥ 4 years) |

| Intense market competition from alternative fitness formats | -1.1% | Urban centers in Brazil, Argentina, Chile | Short term (≤ 2 years) |

| High informality driving price wars | -0.9% | Brazil, Peru, Colombia | Medium term (2-4 years) |

| Technology access gaps | -0.8% | Rural and secondary markets across region | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited access to modern fitness facilities outside major cities

The health and fitness club industry in South America faces significant challenges due to the geographic concentration of modern fitness facilities, which limits access beyond major urban centers. For instance, in Brazil’s Northeast region, chains like Selfit, despite generating BRL 300 million in revenue, primarily serve urban populations, leaving rural areas underserved. This urban-centric focus is further hindered by regulatory obstacles, such as Sportlife Chile’s municipal permitting delays, which impede timely facility openings and highlight broader bureaucratic barriers in secondary markets. In Paraguay, stringent health professional registration regulations create compliance challenges for clubs employing physiotherapists or offering therapeutic services, increasing operational burdens [3]Source: General Directorate for the Control of Professions, Establishments, and Health Technology, "Regulations for the registration and qualification of health professionals", controldeprofesiones.mspbs.gov.py. Economic disparities between urban and rural areas reduce consumer spending power in less populated markets, while higher logistics costs for fitness equipment and maintenance deter chains from expanding. These infrastructural and regulatory constraints disproportionately affect independent fitness clubs, which often lack the scale to justify investments in low-density regions. This dynamic not only complicates market penetration but also reinforces urban market dominance. As a result, the unequal distribution of fitness infrastructure restricts broad-based market access, limiting the growth potential of the industry in South America.

Intense market competition from alternative fitness formats

Traditional gyms in South America are facing intense competition from alternative fitness formats, resulting in pricing pressures and membership retention challenges. A survey conducted by the Health and Fitness Association in 2024 highlights that 42.8% of Latin Americans prefer outdoor activities, driven by benefits such as mental clarity and cost-effectiveness. This trend reflects the increasing popularity of non-gym-based exercises. Digital fitness platforms are also gaining traction due to their convenience and flexibility. However, 53% of individuals who have never been gym members express an intent to join a physical club within the next year, indicating that these alternatives may act as trial phases rather than permanent substitutes. Competitive pressures have already led to significant market exits, such as Bodytech's withdrawal from Peru in 2024 after 16 years, as it struggled to compete with low-cost rivals like Smart Fit, which offers similar services at reduced prices. Additionally, corporate wellness programs are reshaping the landscape by providing subsidized fitness access. While this may reduce direct membership sales, it creates a dependency on B2B contracts, which are susceptible to economic fluctuations. These dynamics collectively compel traditional fitness operators in South America to innovate and diversify their offerings to remain relevant in the region's evolving fitness ecosystem.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Personal Training Drives Premium Growth

In 2025, membership fees dominate the service type segmentation with a 61.64% market share, highlighting the scalability and predictable revenue streams of the subscription-based business model. This approach has enabled operators like Smart Fit to expand operations across 15 countries. Personal training and instruction services represent the fastest-growing segment, with an 11.36% CAGR projected from 2026 to 2031. This growth is driven by increasing consumer demand for personalized fitness solutions and premium service offerings, which enhance member retention and lifetime value. The "Others" category, which includes services such as nutrition counseling, wellness programs, and specialized classes, provides operators with opportunities to differentiate and capture premium market segments.

In 2025, Wellhub's Trainiac program, which doubled its partner personal trainer network, reflects the segment's strong momentum. This initiative not only creates new revenue streams for fitness professionals but also addresses the growing demand for customized programming. Similarly, Universidad San Ignacio de Loyola in Peru has contributed to the professionalization of the instruction services segment by launching a comprehensive Sports and Physical Activity Sciences program. This program includes specialized tracks in exercise prescription and personal training, integrating fitness instruction with formal education systems. The growth trajectory indicates that successful operators are increasingly adopting hybrid models. By combining scalable membership revenues with high-margin personal services and leveraging digital platforms to deliver personalized programming at scale, they maintain the human touch that supports premium pricing and fosters member loyalty.

By Outlet Format: Chain Consolidation Accelerates

Independent clubs hold a 67.82% market share in 2025, highlighting the historically fragmented nature of the fitness industry in South America and the dominance of local operators who effectively address regional preferences and regulatory requirements. However, chained clubs are rapidly expanding at a CAGR of 11.68% during the forecast period (2026-2031), driven by consolidation trends and competitive advantages such as standardized operations, bulk purchasing power, and strong brand recognition, which enable large-scale market penetration and member acquisition.

Smart Fit's Guinness World Record recognition for its Latin American expansion exemplifies the growing momentum of the chain model. By 2024, the company operated 1,743 gyms and served 5.2 million members across 15 countries. Smart Fit's acquisition of Bodytech's former locations in Peru in 2024 demonstrates how chains can quickly capture market share through strategic asset purchases and member transfers, leveraging existing infrastructure while implementing standardized operational models. However, independent operators face mounting pressure to differentiate through specialized programming, local community engagement, or niche positioning. Many also explore franchise partnerships or management agreements to gain chain-like benefits while retaining local ownership and operational flexibility.

By Consumer Demographic: Youth Segment Leads Digital Adoption

Adults aged 25-50 command a 34.35% share of the market in 2025, underscoring their peak earning power, health consciousness, and established exercise habits that bolster membership and retention rates. Meanwhile, the under-25 youth segment is poised for the most significant growth, projected at an 10.87% CAGR from 2026 to 2031. This surge is largely attributed to their digital-native inclinations, the sway of social media, and a penchant for tech-integrated fitness solutions. On the other hand, seniors aged 50 and above, while a smaller segment, present a stable market. Their distinct needs, ranging from low-impact programming and rehabilitation services to social interaction, open avenues for specialized facility designs and tailored programming.

Institutional initiatives are driving the youth segment's expansion, such as Argentina's National School Health Program. By weaving physical activity promotion into school curricula, the program aims to instill lifelong fitness habits in children and adolescents. Furthermore, corporate wellness programs are increasingly targeting younger employees. A notable example is Fundação Tiradentes, which extends Wellhub/Gympass services to military personnel and their dependents, highlighting the potential of institutional partnerships in boosting youth engagement. As the demographic landscape shifts younger, operators are compelled to channel investments into digital platforms, social programming, and adaptable membership models. These models cater to the irregular schedules and budgetary constraints of younger members, all while harnessing the power of social media and peer influence for member acquisition and retention.

Geography Analysis

In 2025, Brazil solidifies its status as the regional leader, commanding a 52.21% market share. This dominance is driven by Smart Fit, which operates 736 gyms, and a well-developed fitness infrastructure that enables specialized operators to generate hundreds of millions in revenue. Government health initiatives, led by INCA, along with comprehensive corporate wellness programs, drive both B2C and B2B demand in the country. Smart Fit's contribution of 52% of UNICEF Brazil's face-to-face fundraising through 211 gym locations highlights the sector's strong community integration in 2023. The market's maturity is further reflected in digital platforms like TotalPass, which aggregates over 3,500 partner gyms and offers app-based access to diverse fitness modalities.

Peru is positioned as the fastest-growing market, with an expected CAGR of 11.14% from 2026 to 2031. This growth is attributed to market restructuring following Bodytech's exit and Smart Fit's aggressive expansion strategy, which includes premium Bio Ritmo locations in shopping centers such as El Polo in 2024. Smart Fit's 75 locations provide extensive coverage, while the market presents significant consolidation opportunities for specialized operators to capture premium segments. Argentina, Chile, and Colombia represent mature markets with established regulatory frameworks and increasing health awareness, supported by government initiatives like Colombia's Ministry of Health guidelines, which recommend 150 minutes of moderate exercise weekly for adults.

The "Rest of South America" category includes emerging markets with substantial growth potential, though these markets face varying regulatory environments and economic conditions. For instance, Paraguay is implementing health professional registration requirements to establish compliance frameworks for fitness facilities offering therapeutic services. Meanwhile, other countries benefit from PAHO's regional obesity prevention initiatives, which encourage government support for physical activity promotion. Geographic expansion strategies by major chains, such as Bio Ritmo's planned entry into Chile and Panama, reflect confidence in the region's growth prospects. At the same time, local operators continue to serve niche markets by offering culturally relevant programs that complement the offerings of international chains.

Competitive Landscape

Leading players in the health and fitness club market in South America are leveraging strategic initiatives to strengthen their competitive positioning. For instance, Smart Fit, a prominent operator, manages 1,743 gyms across 15 countries and serves 5.2 million members as of 2024. The company’s approach combines geographic expansion with investments in digital platforms and premium brands like Bio Ritmo, enabling it to effectively address diverse consumer segments. While the market demonstrates moderate consolidation, it continues to offer significant opportunities for mergers and acquisitions, fostering a competitive environment that drives innovation and price competitiveness. Regulatory oversight remains stringent; Brazil’s antitrust authority CADE in 2025 imposed fines exceeding BRL 300,000 on gym sector entities for anticompetitive practices, ensuring fair competition and balanced market dynamics.

Despite the dominance of large chains, untapped potential exists in underserved secondary cities. These regions, often characterized by infrastructure gaps, may not attract larger players but provide opportunities for local operators. By adopting cost-effective models and building strong community connections, smaller gyms can address unique regional needs and pricing sensitivities, contributing to the market’s overall diversity. However, operators must carefully navigate regulatory and infrastructure challenges when expanding into these areas to maintain competitive positioning.

The industry is also evolving toward hybrid models that integrate physical gyms with digital services, creating a significant competitive advantage. Operators who successfully combine technology with the social and motivational aspects of fitness can enhance member engagement, leading to higher lifetime value and improved retention rates. This integration is not merely about technological advancements; it redefines the membership experience by enabling seamless transitions between in-person and virtual workouts. Such adaptability is essential for staying relevant in South America’s rapidly digitizing fitness ecosystem.

South America Health And Fitness Club Industry Leaders

-

Bio Ritmo Participações S.A.

-

Bodytech

-

RSG Group GmbH

-

Planet Fitness Franchising, LLC

-

Purpose Brands

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Bio Ritmo, a premium gym chain under the Smart Fit Group, announced the launch of its inaugural concept gym, which integrated wellness, innovation, and tailored services. Located in the Ibirapuera Shopping Mall in São Paulo's southern district, the facility represented an investment exceeding BRL 10 million. It featured cutting-edge equipment from Italy's Technogym, upscale amenities, individualized spaces, a dedicated recovery room, and extensive technical support.

- August 2025: Gold's Gym entered Brazil through a master franchise agreement that outlined plans for 60 locations over the next decade. The flagship gym was scheduled to open in 2026, followed by additional branches in São Paulo, Rio de Janeiro, and Brasilia. Beyond Brazil, Gold's Gym secured commitments for over 200 new sites globally and sought additional master partners, targeting expansions in Argentina, Colombia, Chile, and Mexico.

- September 2024: Bio Ritmo, a premium fitness brand under the Smart Fit Group, expanded its international presence. By December, the brand had launched four new gyms in Chile, Peru, and Panama. By December 2024, Bio Ritmo had outlined plans for Brazil, targeting four additional locations. These included the brand's inaugural gym in São Paulo's eastern Anália Franco neighborhood and a new unit at Shopping Ibirapuera in the city's south. Additionally, in collaboration with insurance giant Porto Seguro, the brand introduced its sixth corporate-style gym.

South America Health And Fitness Club Market Report Scope

South America health and fitness market is segmented by service type and geography. By service type, the market is segmented into membership fees, total admission fees, and personal training and instruction services. By geography, the South America region is classified into Brazil, Argentina, Colombia and rest of South America.

By Service Type

| Membership Fees |

| Personal Training and Instruction Service |

| Others |

By Outlet Format

| Chained Clubs |

| Independent Clubs |

By Consumer Demographic

| Adults (25-50 years) |

| Youth (under 25 years) |

| Seniors (50+ years) |

By Country

| Brazil |

| Argentina |

| Colombia |

| Chile |

| Peru |

| Rest of South America |

| By Service Type | Membership Fees |

| Personal Training and Instruction Service | |

| Others | |

| By Outlet Format | Chained Clubs |

| Independent Clubs | |

| By Consumer Demographic | Adults (25-50 years) |

| Youth (under 25 years) | |

| Seniors (50+ years) | |

| By Country | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

How large is the South America health and fitness club market in 2026?

It is valued at USD 5.66 billion and is forecast to reach USD 9.2 billion by 2031.

What is the growth rate for fitness clubs in Peru?

Peru is projected to grow at an 11.14% CAGR between 2026 and 2031, the fastest in the region.

Which service type is expanding the fastest?

Personal training and instruction services are advancing at an 11.36% CAGR owing to rising demand for customized guidance.

What demographic offers the highest growth potential?

Consumers under 25 years old are expanding memberships at an 10.87% CAGR due to tech-integrated offerings and university partnerships.

Page last updated on: