Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

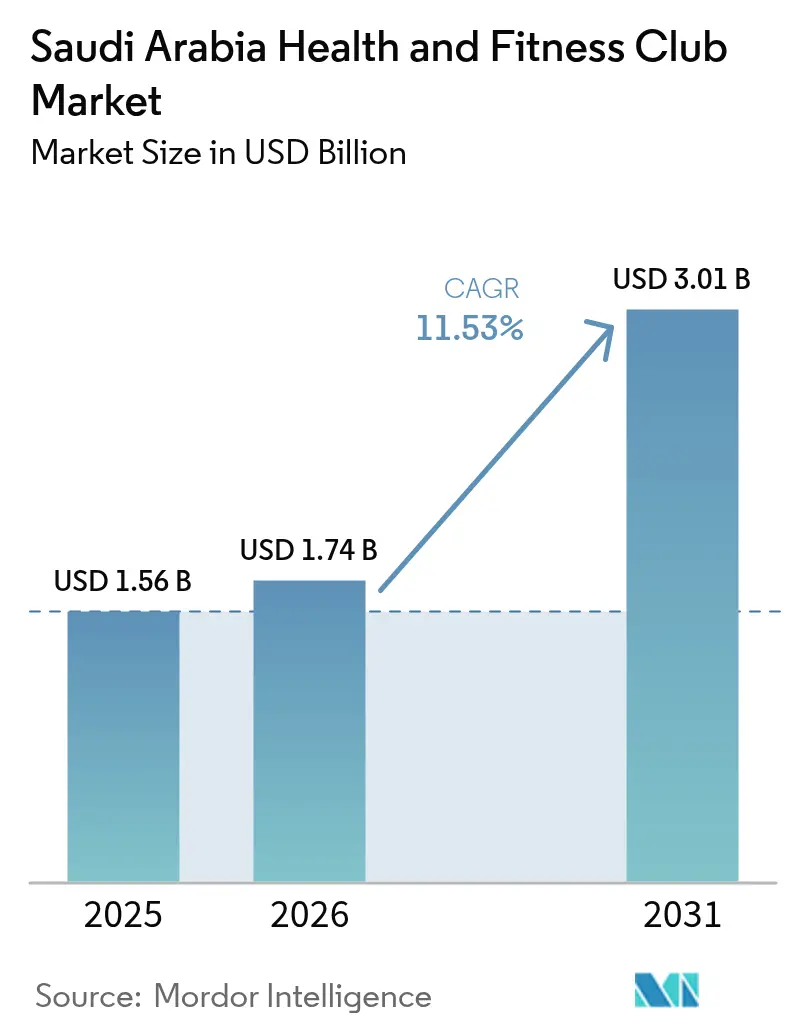

| Base Year Market Size (2025) | USD 1.56 Billion |

| Market Size (2026) | USD 1.74 Billion |

| Market Size (2031) | USD 3.01 Billion |

| Growth Rate (2026 - 2031) | 11.53% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Saudi Arabia Health And Fitness Club Market Analysis by Mordor Intelligence

Saudi Arabia health and fitness club market size in 2026 is estimated at USD 1.74 billion, growing from 2025 value of USD 1.56 billion with 2031 projections showing USD 3.01 billion, growing at 11.53% CAGR over 2026-2031. This growth is primarily fueled by the increasing awareness of health and wellness among the population, as more individuals prioritize physical fitness and adopt healthier lifestyles. The market's expansion is further supported by rising disposable incomes, enabling consumers to spend more on fitness-related services and memberships. Government initiatives, such as Saudi Vision 2030, play a pivotal role in promoting physical activity and encouraging the establishment of fitness facilities across the country. These initiatives aim to reduce lifestyle-related diseases and improve the overall well-being of the population, thereby driving demand for health and fitness clubs. Additionally, the market is benefiting from the growing presence of international fitness brands and the introduction of innovative services, such as personalized training programs, virtual fitness classes, and wellness-focused offerings. The increasing penetration of digital fitness platforms and mobile applications is also contributing to the market's growth, as they provide convenient and flexible fitness solutions to consumers.

Key Report Takeaways

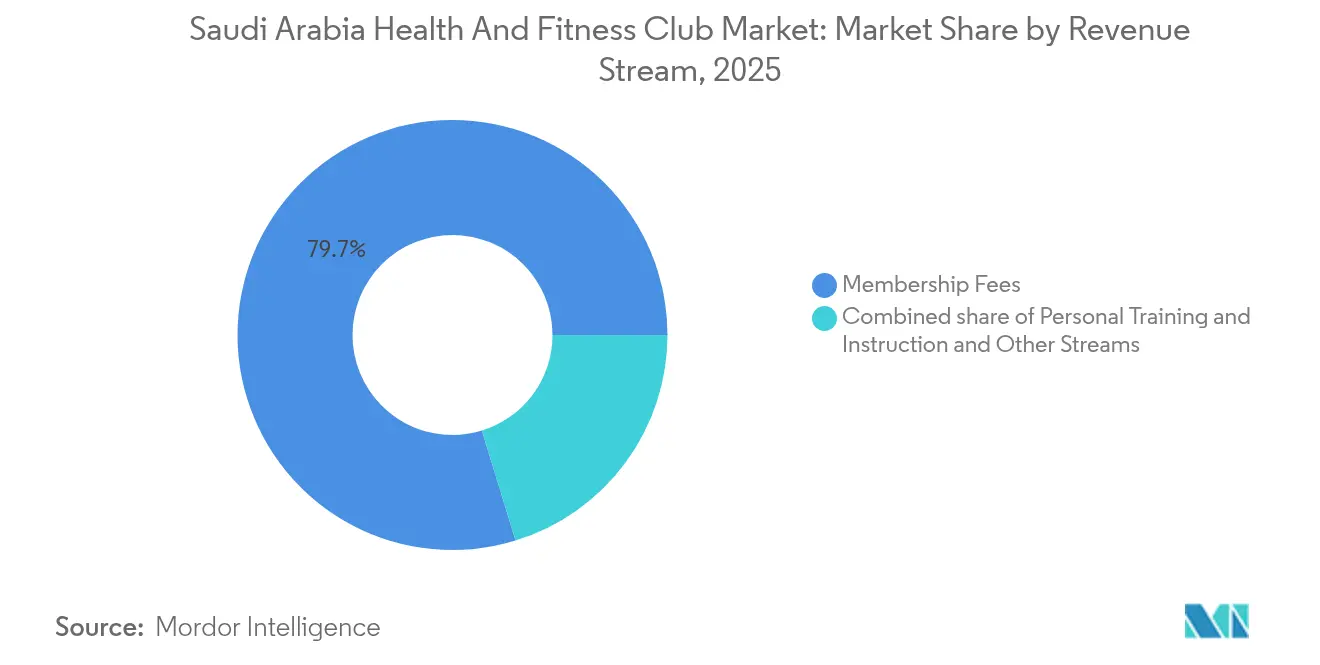

- By revenue stream, Membership Fees held 79.74% of the Saudi Arabia health and fitness club market share in 2025, whereas Personal Training and Instruction is advancing at a 12.95% CAGR through 2031.

- By end user, men accounted for 77.62% of participation in 2025; women represent the fastest growing cohort with a 13.05% CAGR to 2031.

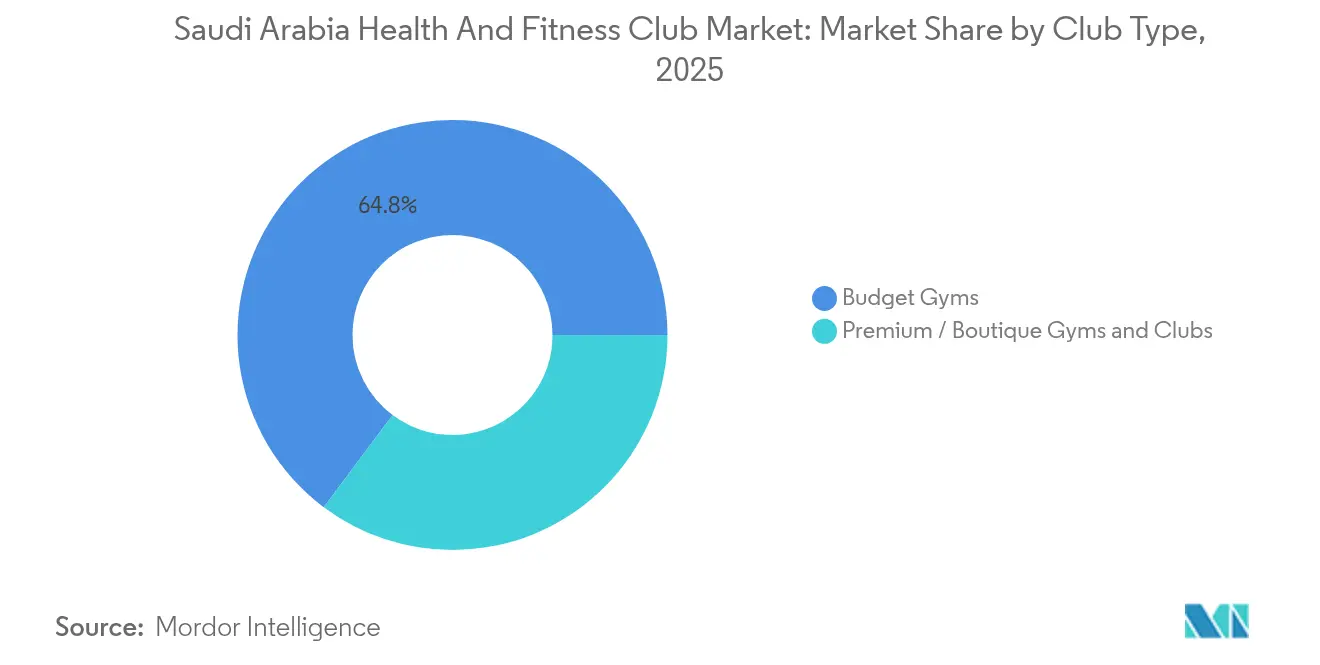

- By club type, Budget Gyms captured 64.78% revenue in 2025, while Premium/Boutique Gyms and Clubs are expanding at a 13.32% CAGR during 2026-2031.

- By structure, independent operators commanded 66.74% share in 2025 and chained facilities are scaling at a 12.67% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Health And Fitness Club Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government support and vision 2030 reforms | +2.8% | National, with concentrated gains in Riyadh, Jeddah, Dammam | Long term (≥ 4 years) |

| Growth of gym culture and penetration of gym brands | +2.1% | Urban centers, expanding to secondary cities | Medium term (2-4 years) |

| Rising awareness and increasing obesity among consumers | +1.9% | National, with higher impact in metropolitan areas | Medium term (2-4 years) |

| Urbanization and lifestyle changes | +1.6% | Major cities and emerging urban centers | Long term (≥ 4 years) |

| Variety in fitness offerings | +1.4% | Premium segments in Riyadh, Jeddah, Eastern Province | Short term (≤ 2 years) |

| Corporate wellness mandates in large employers | +1.3% | Industrial hubs, major corporate centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government support and vision 2030 reforms

The Saudi Arabian health and fitness club market is significantly driven by government support and the ambitious Vision 2030 reforms. These reforms aim to diversify the economy and reduce dependence on oil revenues by promoting sectors like health, wellness, and fitness. Vision 2030's Health Sector Transformation Program fundamentally reshapes fitness infrastructure through unprecedented public investment and regulatory modernization. The government has introduced various initiatives to encourage physical activity and healthy lifestyles among citizens, aligning with the Vision 2030 objective of increasing the participation rate in sports and physical activities. Additionally, substantial investments in infrastructure, such as the development of fitness centers, gyms, and recreational facilities, are further propelling the market. These efforts are complemented by public awareness campaigns and partnerships with private entities to foster a culture of health and fitness across the nation. The government's proactive approach and strategic reforms are creating a conducive environment for the growth of the health and fitness club market in Saudi Arabia.

Growth of gym culture and penetration of gym brands

In Saudi Arabia, physical activity has shifted from being a leisure activity to becoming an essential part of everyday routines. The 2024 Physical Activity Statistics Bulletin, published by the General Authority for Statistics (GASTAT), highlights that 58.5% of Saudi residents aged 18 and older actively participate in physical activities for at least 150 minutes each week [1]Source: General Authority for Statistics, "General Authority for Statistics Announces Physical Activity Statistics for Saudi Arabia in 2024", mos.gov.sa. This growing focus on health and fitness has significantly increased the demand for gyms and fitness centers across the country. To address this rising demand, market players are actively introducing strategic innovations and expanding their presence in the region. Prominent fitness chains are not only entering the Saudi market but are also establishing a strong foothold by opening new facilities. International fitness brands, including Gold's Gym, World Gym, Landmark Fitness, and Curves, are forming franchise partnerships to cater to the growing appetite for fitness services. These collaborations aim to provide high-quality fitness solutions and capitalize on the increasing health awareness among Saudi residents. The fitness industry in Saudi Arabia is witnessing rapid growth as both local and international players work to meet the evolving needs of the market.

Rising awareness and increasing obesity among consumers

In Saudi Arabia, the rising prevalence of obesity is driving the demand for targeted fitness solutions and specialized health programs. This growing health concern has prompted corporate wellness initiatives to adopt strategies aimed at improving employee well-being. For instance, Aramco offers its employees free access to recreational facilities, including gyms and swimming pools, to address workforce health challenges. Such initiatives reflect a broader trend within the corporate sector to prioritize health and wellness. Additionally, there is a noticeable increase in consumer participation in rigorous exercise routines, driven by the goals of weight management and improved stamina. This shift indicates a rising health consciousness among the population, as individuals actively seek to adopt healthier lifestyles. According to data from The General Authority for Statistics (Saudi Arabia), the obesity rate among individuals aged 15 and older has reached 23.1% in 2024, while 45.1% of this demographic is classified as overweight. Among children aged 2 to 14 years, 14.6% are categorized as obese, and 33.3% are considered overweight [2]Source: General Authority for Statistics, "GASTAT publishes the results of Health Determinants Statistics Publication in Saudi Arabia 2024", stats.gov.sa. These statistics highlight the urgent need for interventions, including public health campaigns, community-based fitness programs, and educational initiatives to promote healthier eating habits and active lifestyles.

Urbanization and lifestyle changes

Urbanization and changing lifestyles are significant drivers of the Saudi Arabia Health and Fitness Club Market. According to World Bank data, Saudi Arabia's urbanization rate reached 85% in 2024 [3]Source: World Bank, "Urban population (% of total population) - Saudi Arabia", data.worldbank.org, underscoring the rapid pace of urban development and the increasing concentration of the population in cities. This urban expansion has not only transformed the country's demographic landscape but also exposed a larger segment of the population to global health and wellness trends. As urban areas grow, residents are becoming more aware of the importance of maintaining a healthy lifestyle to counteract the challenges posed by sedentary jobs and modern living conditions. The shift towards urban living has also led to a rise in disposable incomes and access to fitness facilities, further driving the adoption of fitness routines. Consequently, health and fitness clubs are witnessing increased memberships as individuals seek structured environments to achieve their wellness goals. This growing demand for fitness facilities and services highlights urbanization as a critical factor propelling the Saudi Arabia Health and Fitness Club Market forward.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for home gyms and recreational activities | -1.8% | Urban areas with higher disposable income | Short term (≤ 2 years) |

| High membership prices in premium gyms | -1.5% | Premium segments in major cities | Medium term (2-4 years) |

| Shortage of certified Saudi fitness professionals | -1.2% | National, more acute in secondary cities | Long term (≥ 4 years) |

| Cultural barriers in smaller, conservative cities | -0.9% | Rural and conservative regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging demand for home gyms and recreational activities

The market faces a significant restraint due to the surging demand for home gyms and recreational activities. Consumers are increasingly opting for home-based fitness solutions, driven by convenience, cost-effectiveness, and the ability to customize their workout routines. The availability of online fitness platforms and mobile applications offering personalized workout plans and real-time tracking has further accelerated this shift. Additionally, recreational activities, including outdoor sports, hiking, and community fitness events, are gaining popularity, diverting consumer interest away from traditional fitness clubs. The growing awareness of health and wellness has also encouraged individuals to explore alternative fitness options that align with their personal preferences and schedules. These factors collectively pose a challenge to the growth of health and fitness clubs in the region, as they struggle to compete with the flexibility, accessibility, and cost advantages offered by alternative fitness solutions.

High membership prices in premium gyms

Premium gyms in Saudi Arabia charge high membership fees, which act as a significant restraint in the health and fitness club market. These elevated costs limit accessibility for a large portion of the population, particularly middle-income and low-income groups. As a result, many individuals are unable to afford memberships at such facilities, thereby restricting the market's growth potential. This pricing structure also creates a competitive disadvantage for premium gyms compared to more affordable fitness options, such as budget gyms or home workout solutions. The high membership prices further emphasize the need for market players to explore strategies like flexible pricing models or promotional offers to attract a broader customer base and mitigate this restraint. Additionally, the high costs associated with premium gyms often deter first-time gym-goers, who may perceive the investment as risky without prior experience or assurance of consistent usage. This challenge is compounded by the presence of alternative fitness trends, such as outdoor activities and digital fitness platforms, which offer cost-effective solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Revenue Stream: Membership Fees Drive Market Foundation

Membership fees are the largest contributor to revenue generation in the Saudi Arabia health and fitness club market, accounting for a substantial 79.74% market share in 2025. This dominant position highlights the widespread adoption of subscription-based business models among fitness operators in the region. The preference for membership fees reflects consumers’ long-term commitment to fitness clubs and the operators’ strategic focus on securing steady, predictable income streams. This revenue model provides stability to fitness businesses, allowing them to invest in facilities, equipment, and services that enhance member experience. The large market share also indicates that the majority of consumers in Saudi Arabia prefer accessing fitness services through memberships rather than pay-per-use options. As a result, the fitness industry in Saudi Arabia is strongly anchored on this model, supporting sustained growth and service innovation.

On the other hand, personal training and instruction is emerging as the fastest-growing segment within the Saudi Arabia health and fitness market, with a robust CAGR of 12.95% expected between 2026 and 2031. This rapid growth is fueled by increasing consumer demand for personalized fitness solutions tailored to individual goals and needs. Cultural preferences in Saudi Arabia also play a significant role, as many consumers favor guided instruction from qualified professionals to ensure effective and safe workouts. The rise in health awareness and the pursuit of fitness goals have further strengthened interest in personal training services. Additionally, fitness clubs are increasingly focusing on offering specialized training programs and one-on-one coaching to differentiate themselves in a competitive market.

By End User: Women's Participation Accelerates Market Evolution

Men hold the largest market share in the Saudi Arabia health and fitness club market, accounting for 77.62% of the market in 2025. This substantial share reflects longstanding participation trends rooted in traditional cultural norms that have historically favored male involvement in fitness activities. The dominance of men in the fitness sector is also linked to social factors and access to fitness facilities tailored primarily for male users. This pattern has shaped the development of fitness clubs and their programming, focusing largely on male preferences and fitness needs. The strong market presence of men underscores the entrenched cultural attitudes towards gender roles within the country’s fitness landscape. Despite ongoing social changes, male participation remains dominant, providing a stable customer base for fitness operators.

Conversely, women represent the fastest-growing segment in the Saudi fitness club market, with a notable CAGR of 13.05% projected from 2026 to 2031. This rapid expansion is largely attributed to the strategic initiatives outlined in Saudi Arabia’s Vision 2030, which emphasizes enhancing female workforce participation and empowering women’s social engagement. The development of specialized fitness facilities catering exclusively to women is a key driver behind this growth, addressing cultural sensitivities and increasing access. Rising health awareness and changing societal attitudes are further encouraging more women to embrace fitness activities. Additionally, the government’s supportive policies and investments in women’s fitness infrastructure contribute to expanding female participation.

By Club Type: Premium Segment Outpaces Budget Growth

Budget gyms hold the largest market share in the Saudi Arabia health and fitness club market, commanding 64.78% in 2025. This significant share highlights the predominance of price-sensitive consumer behavior within the region, where affordability remains a key factor in fitness club selection. The large market presence of budget gyms reflects the current developmental stage of the fitness industry, with many consumers prioritizing access and value over premium features. These gyms cater to a broad base of users who seek essential fitness services without the added cost of luxury amenities. The success of budget gyms underscores the importance of economical pricing structures in capturing the majority of fitness club members. As the fitness market continues to evolve, budget gyms remain a critical segment driving widespread participation.

In contrast, premium and boutique gyms and clubs are experiencing the fastest growth in the Saudi fitness market, with a CAGR of 13.32% projected from 2026 to 2031. This rapid expansion reflects a growing consumer willingness to invest in differentiated and enhanced fitness experiences that go beyond basic offerings. Premium gyms attract clients looking for specialized services, personalized attention, and upscale facilities, creating a niche for luxury-oriented fitness enthusiasts. The rising demand for innovative fitness classes, advanced equipment, and tailored wellness programs further fuels this segment’s expansion. As disposable incomes increase and lifestyle aspirations shift, more consumers are gravitating toward premium fitness options.

By Structure: Independent Operators Face Chain Competition

Independent operators hold the largest market share in the Saudi Arabia health and fitness club market, capturing 66.74% of the market in 2025. This dominance reflects the fragmented nature of the market, where many entrepreneurial fitness businesses have emerged to meet growing consumer demand. The prevalence of independent gyms and clubs indicates a landscape characterized by localized, smaller-scale operations rather than consolidated chains. These operators often enjoy flexibility in tailoring services to specific community needs and preferences, which has helped build a loyal customer base. The significant market share of independent operators underscores the entrepreneurial spirit driving the sector’s development. Despite increasing competition from larger chains, independent businesses remain a critical force within the market structure.

On the other hand, chained operations are the fastest-growing segment in the Saudi fitness market, forecasted to achieve a CAGR of 12.67% between 2026 and 2031. Chains benefit from their ability to leverage operational scale, which allows for more efficient cost management and resource allocation. Brand recognition also plays a crucial role in attracting new members, as well-known chains often inspire greater consumer confidence and trust. Moreover, standardized service delivery across locations ensures a consistent customer experience, which is attractive to fitness consumers seeking quality assurance. The superior growth velocity of chained operations highlights a trend toward market consolidation and professionalization. As chains continue expanding their presence, they are positioned to capture increasing market share from fragmented independents.

Geography Analysis

Saudi Arabia's fitness market is heavily concentrated in Riyadh, Jeddah, and the Eastern Province. These regions dominate the market landscape due to higher urbanization rates and greater disposable incomes. Riyadh leads the market, driven by substantial government investments and infrastructure projects. Key initiatives include a SAR 2 billion investment in the Sports Boulevard project and the Jawharat Riyadh retail development, which integrates fitness into lifestyle destinations. Additionally, Riyadh benefits from its position as a corporate hub, with government entities and multinational corporations fostering a strong demand for corporate wellness programs. The city is also at the forefront of technological advancements in fitness, with initiatives like the Saudi Sports for All Federation's digital engagement programs and smart gym concepts such as B_fit, which incorporates AI-powered fitness solutions.

Jeddah and the Western Province exhibit significant market potential, supported by cultural openness and international connectivity. Operators like NuYu have successfully established women-only fitness facilities, setting a benchmark for market development. The region's growing tourism infrastructure, fueled by investments in projects like the Red Sea initiative, further enhances its fitness market prospects. For instance, Equinox is developing luxury resort facilities that combine fitness with hospitality experiences, catering to both residents and tourists. Jeddah also has a thriving corporate wellness sector, with startups like GetMuv originating in the city and expanding their services to major employers across the Kingdom, showcasing the region's dynamic contribution to the fitness market.

The Eastern Province leverages its industrial concentration and the presence of major employers like Aramco to strengthen its fitness market. Aramco plays a pivotal role by providing extensive employee wellness infrastructure, including gyms, swimming pools, and sports courts, which cater to the recreational needs of its workforce. This comprehensive approach to wellness not only supports employee health but also contributes to the region's fitness market growth. By capitalizing on its industrial base and robust wellness initiatives, the Eastern Province continues to solidify its position as a key player in Saudi Arabia's expanding fitness landscape.

Competitive Landscape

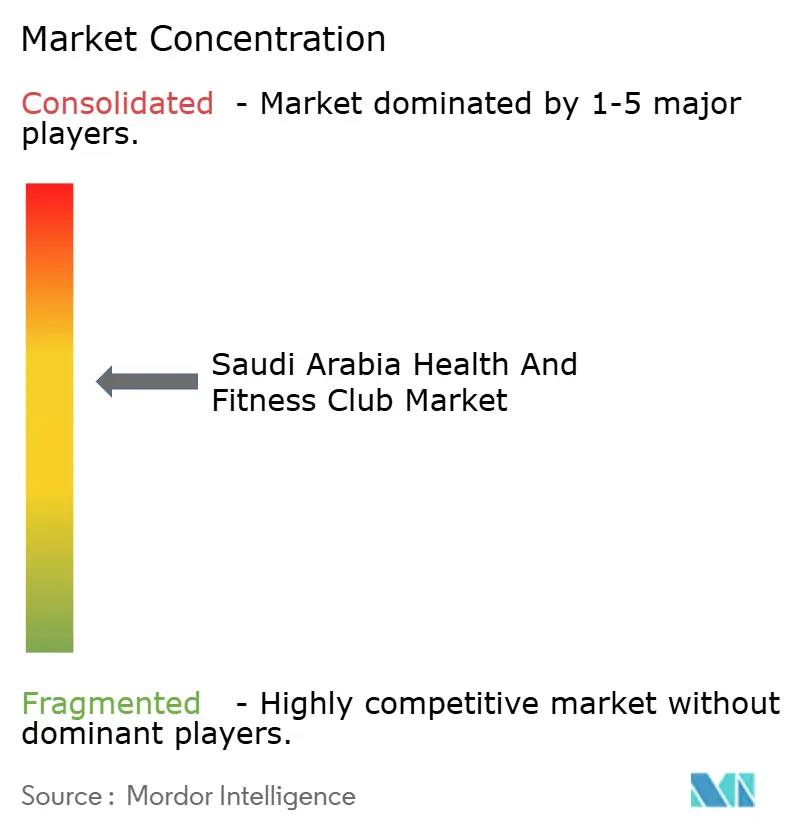

The Saudi Arabia health and fitness club market demonstrates a moderate level of concentration, characterized by fragmented competitive dynamics. The market's concentration score of 6 indicates a balanced mix of established players and smaller, emerging competitors. This fragmentation creates opportunities for new entrants while also posing challenges for existing players to maintain their market share. The competitive environment is shaped by factors such as pricing strategies, service offerings, and the ability to cater to evolving consumer preferences. The growing awareness of health and wellness among the Saudi population has further fueled the demand for fitness services, intensifying competition among market participants.

The market is witnessing increased competition as both domestic and international players strive to expand their presence. Key players are focusing on diversifying their service portfolios, incorporating advanced fitness technologies, and offering personalized fitness programs to attract and retain customers. Companies are also leveraging strategic partnerships and collaborations to enhance their market position and gain a competitive edge. Additionally, the adoption of digital platforms for customer engagement and the introduction of niche fitness programs are becoming prominent strategies among smaller players to differentiate themselves in the market. These efforts are aimed at addressing the evolving needs of consumers and capitalizing on the growing fitness trend in the country.

Despite the fragmented nature of the market, established players hold a significant share due to their strong brand presence and extensive network of fitness clubs. However, smaller players are increasingly adopting innovative approaches to compete effectively. The competitive landscape is expected to evolve further during the forecast period, driven by changing consumer preferences, technological advancements, and government initiatives promoting health and wellness in the country. The Saudi Vision 2030 initiative, which emphasizes improving the quality of life and encouraging physical activity, is likely to play a pivotal role in shaping the market dynamics. As a result, the market is poised for growth, with both existing and new players actively contributing to its development.

Saudi Arabia Health And Fitness Club Industry Leaders

-

Leejam Sports Company

-

RSG Group LLC

-

Landmark Group

-

NuYu Fitness

-

Amwal Al Khaleej (BodyMasters)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Gymnation, a prominent operator in the Middle East, has inaugurated its largest club yet in the Qurtubah district of Riyadh. Spanning 77,000 square feet, the club boasts Saudi Arabia's largest ladies-only reformer Pilates studio, a private reformer Pilates room, and an outdoor roof terrace designed for both fitness and social events. The facility caters to both male and female members.

- February 2025: Leejam Sports Company opened a new women's fitness center in Riyadh's An Nasim Al Gharbi district on Hassan bin Thabit Street. Operating under the "Fitness Time - Ladies" brand, the center features modern facilities, premium exercise equipment, and well-designed training spaces.

- December 2024: Leejam Sports Company launched two new fitness centers in Riyadh. The first center, located on Mohammed bin Abdulaziz Al-Dughaither Street in the Al Sahafa district, operates under the "Fitness Time - Ladies" brand and features state-of-the-art equipment and well-designed exercise spaces. The second center, situated on King Abdulaziz Road in the Al Arid district, operates under the "Fitness Time Xpress" brand.

- October 2024: Armah Sports has purchased fitness equipment worth SAR 1.9 million from Pulse Fitness & Sports Co. as part of its strategic initiative to expand operations and address the growing demand for women's B_FIT centers.

Saudi Arabia Health And Fitness Club Market Report Scope

A health and fitness club is usually a commercial establishment with members who pay a fee to use its health and fitness facilities and equipment.

The health and fitness club market is segmented by revenue stream and end-user. The market is segmented by revenue stream into membership fees, personal training and instruction services, and other revenue streams. By end user, the market is segmented into men and women. For each segment, the market sizing and forecasts are done based on the value (USD).

By Revenue Stream

| Membership Fees |

| Personal Training and Instruction |

| Other Revenue Streams |

By End User

| Men |

| Women |

By Club Type

| Budget Gyms |

| Premium / Boutique Gyms and Clubs |

By Structure

| Independent |

| Chained |

| By Revenue Stream | Membership Fees |

| Personal Training and Instruction | |

| Other Revenue Streams | |

| By End User | Men |

| Women | |

| By Club Type | Budget Gyms |

| Premium / Boutique Gyms and Clubs | |

| By Structure | Independent |

| Chained |

Key Questions Answered in the Report

How fast is the Saudi Arabia health and fitness club market expected to grow through 2031?

It is forecast to expand at an 11.53% CAGR, rising from USD 1.74 billion in 2026 to USD 3.01 billion by 2031.

Which revenue stream will add the most absolute value by 2031?

Personal Training and Instruction, growing at 12.95% CAGR, is projected to contribute the largest incremental revenue.

What segment shows the highest growth among end users?

Women’s participation is increasing at a 13.05% CAGR as gender-specific facilities multiply.

How will Vision 2030 influence future club openings?

Government infrastructure and licensing reforms make new site development easier, especially in emerging urban centers.

Page last updated on: