Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

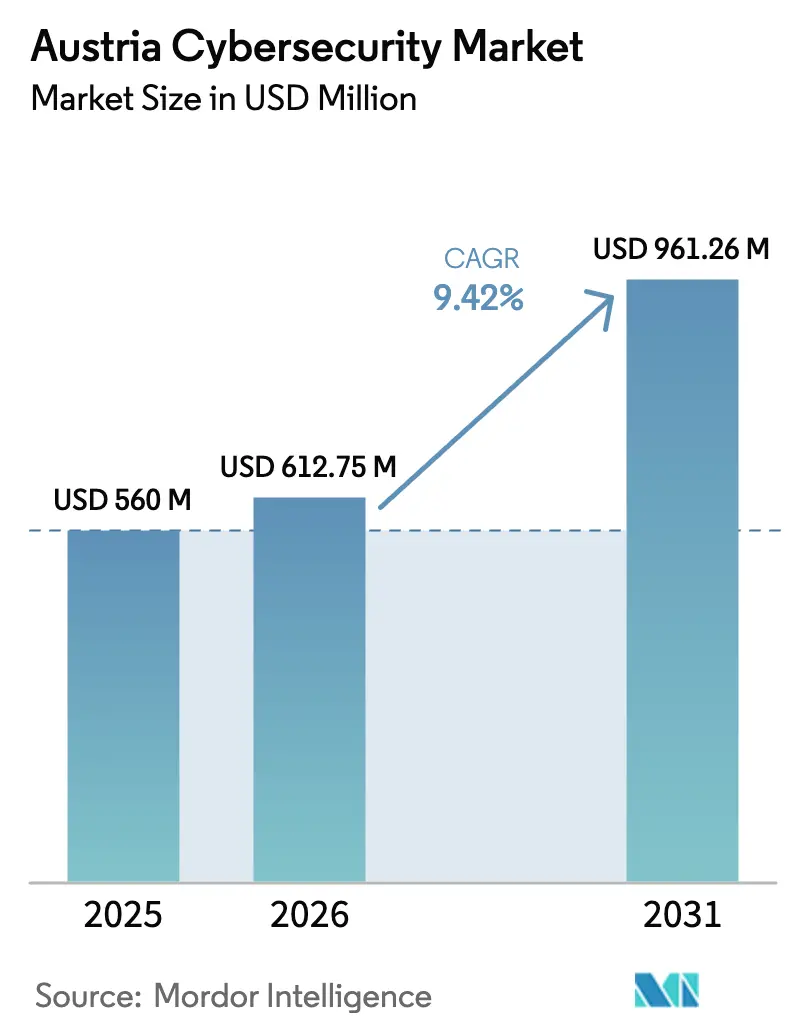

| Base Year Market Size (2025) | USD 560 Million |

| Market Size (2026) | USD 612.75 Million |

| Market Size (2031) | USD 961.26 Million |

| Growth Rate (2026 - 2031) | 9.42% CAGR |

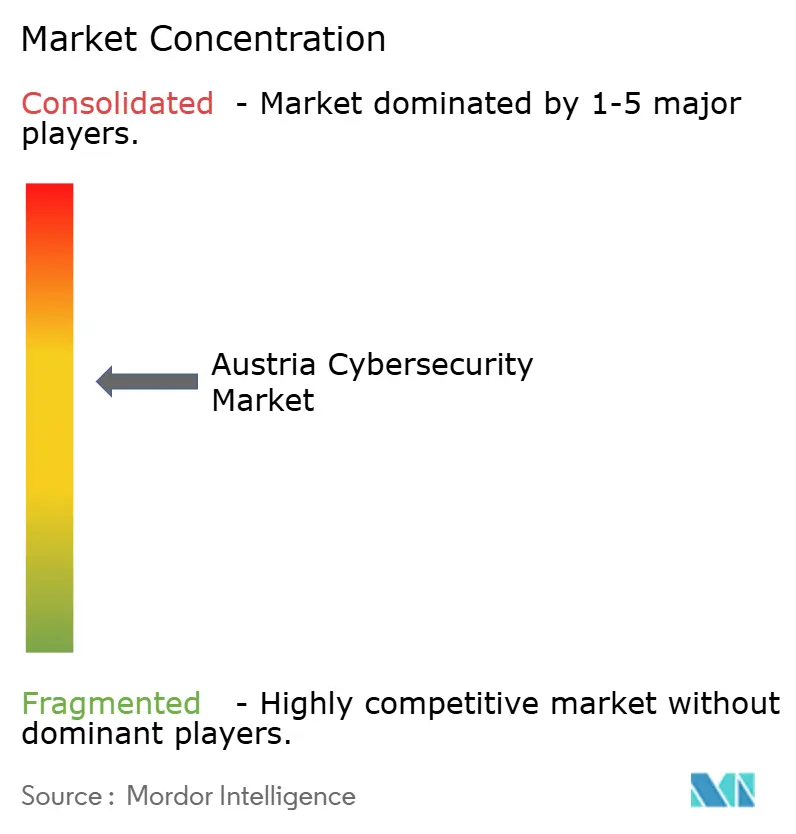

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Austria Cybersecurity Market Analysis by Mordor Intelligence

The Austria cybersecurity market size was valued at USD 560 million in 2025 and estimated to grow from USD 612.75 million in 2026 to reach USD 961.26 million by 2031, at a CAGR of 9.42% during the forecast period (2026-2031). Austria’s status as an EU digital hub, its €1.8 billion commitment to digital infrastructure under the EU Recovery Plan, and imminent NIS2 and DORA compliance deadlines are steering budgets toward integrated, regulation-ready security platforms. Financial institutions, energy operators, and healthcare providers are increasing cloud-first security deployments, while AI-powered threat-detection start-ups draw new venture funding. Rising cyberattacks on municipal agencies and industrial firms are forcing even cautious sectors to adopt zero-trust frameworks. Fragmented vendor competition, a talent shortfall, and tight SME budgets temper growth but also propel demand for managed services and automation. [1]Republik Österreich, “EU-Aufbauplan – Bundeskanzleramt,” bundeskanzleramt.gv.at

Key Report Takeaways

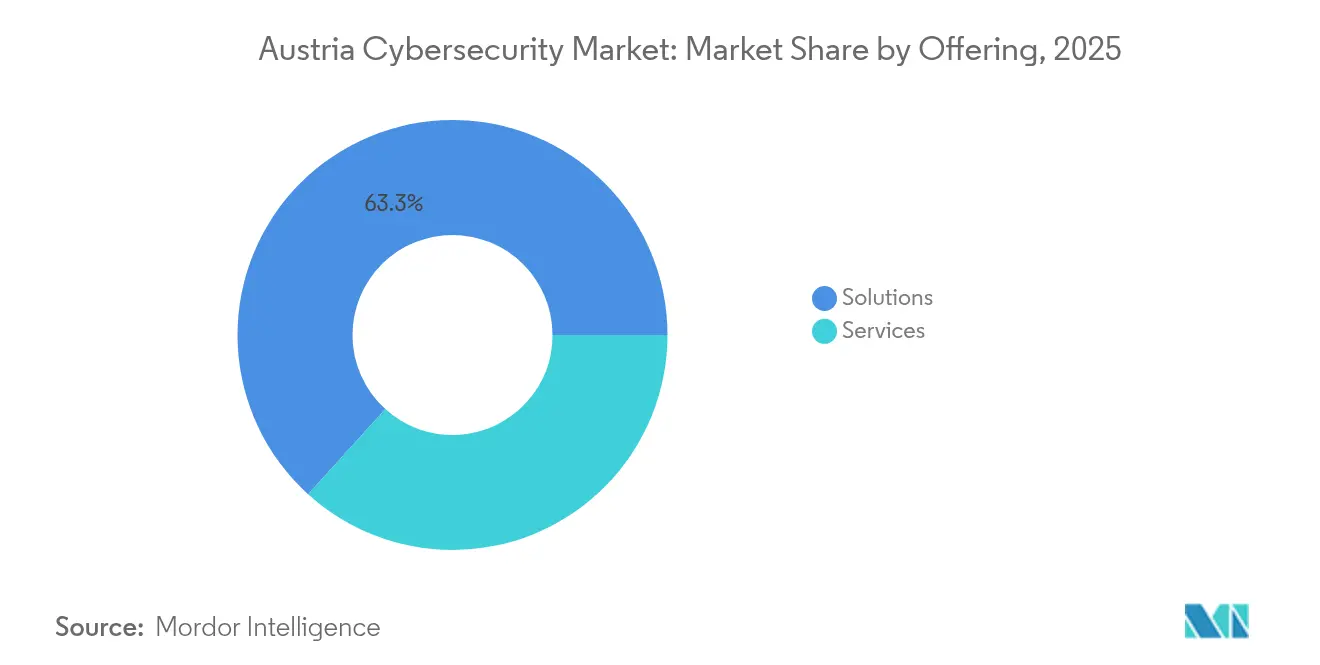

- By offering, solutions segment held 63.28% of the Austria cybersecurity market share in 2025; Cloud Security is projected to expand at a 11.85% CAGR to 2031.

- By deployment mode, the cloud segment captured 70.35% revenue in 2025, while on-premise remains vital for regulated industrial assets.

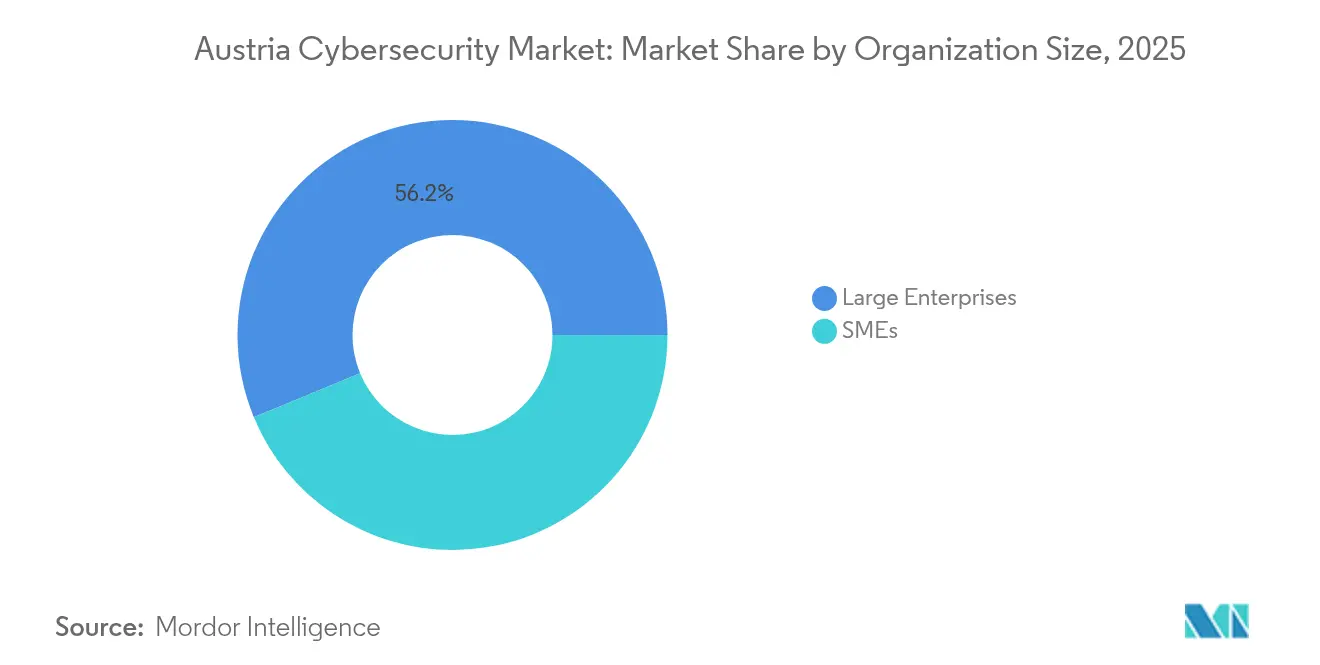

- By organization size, Large Enterprises accounted for 56.24% share of the Austria cybersecurity market size in 2025; SMEs lead growth at an 11.05% CAGR through 2031.

- By end user, BFSI led with 23.62% revenue share in 2025; Healthcare is accelerating at a 12.45% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Austria Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-driven threat-detection adoption | 2.80% | Austria, with spillover to CEE region | Medium term (2-4 years) |

| Rising malware & phishing incidents | 2.10% | National, concentrated in Vienna and industrial regions | Short term (≤ 2 years) |

| Demand for cyber-savvy boards | 1.60% | National, strongest in BFSI and large enterprises | Long term (≥ 4 years) |

| EU NIS2 Directive compliance pressure | 3.20% | Austria-wide, aligned with EU implementation | Short term (≤ 2 years) |

| Government investment in cybersecurity infrastructure | 2.40% | National, concentrated in critical infrastructure sectors | Medium term (2-4 years) |

| Energy sector digitization and smart grid security | 1.90% | National, focused on energy transition regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-driven threat-detection adoption

More than half of Austria’s AI companies focus on industrial use cases that now include autonomous threat detection, giving local vendors a performance edge in spotting advanced intrusions. Flagship start-up CyberTrap secured public-sector contracts abroad with deception-based AI, proving Austrian technology can scale internationally. National funding channels, such as the new AI Advisory Board, and recent mega-rounds like Magic AI’s EUR 117 million financing, strengthen an ecosystem that blends academic talent with security engineering. Although enterprises need time to train models and integrate toolsets, the resulting uplift in detection speed and accuracy supports a clear medium-term boost to Austria cybersecurity market adoption. [2]AI Landscape Austria, “Why Austria,” ai-landscape.at

Rising malware and phishing incidents

Cyberattacks against Austrian public utilities, municipalities, and insurers jumped 143% between 2022 and 2024, forcing organizations to migrate from perimeter defenses to layered monitoring and response. Daily attack frequency is highest in manufacturing and energy, sectors that anchor Austria’s export economy. With 22% of firms enduring near-constant probing, spending on endpoint detection and incident-response orchestration is prioritised ahead of discretionary IT upgrades. The immediate threat environment contributes a short-term spike in Austria cybersecurity market purchases of SaaS-based SOC services.

Demand for cyber-savvy boards

One-third of Austrian board directors now list cybersecurity oversight among their core duties as NIS2 and DORA extend personal liability for lapses. Banks already demonstrate this shift: supervisory boards regularly review resilience metrics and sanction tabletop breach drills. Public-sector IT provider BRZ applies similar governance to digital citizen-services, making risk dashboards routine for executive committees. Board-level education programs and specialist recruitment mark the early phase of a structural, long-term uplift in strategic security spending.

EU NIS2 Directive compliance pressure

NIS2 thrusts roughly 4,000 Austrian companies—40 times more than the original NIS regime—into mandatory risk-management and breach-reporting obligations. Penalties of up to €10 million or 2% of global turnover spur large technology refreshes, particularly in cloud security and identity management. Because the transposition is expected only by autumn 2025, many firms are engaging turnkey platform vendors to meet tight deadlines. The directive therefore dominates near-term Austria cybersecurity market demand curves.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of skilled cybersecurity workforce | -1.80% | National, acute in Vienna tech hub | Long term (≥ 4 years) |

| SME budget constraints for advanced security | -1.20% | National, concentrated in rural regions | Medium term (2-4 years) |

| Legacy OT-system integration challenges | -0.90% | Industrial regions, manufacturing centers | Long term (≥ 4 years) |

| Complexity of multi-cloud environments | -0.70% | Large enterprises, cloud-first organizations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of skilled cybersecurity workforce

Almost 9 in 10 Austrian organizations say they need extra security personnel to meet NIS2 requirements. Median salaries for senior analysts already exceed EUR 130,000, pushing employers to outsource 24/7 monitoring. Government programs offer coding bootcamps and school workshops, yet the talent pipeline still lags projected 30% job growth by 2029. Over the long term, automation and managed services are expected to soften but not remove this drag on Austria cybersecurity market expansion.

SME budget constraints for advanced security

SMEs comprise 99.6% of Austrian companies, but more than 40% have suffered cyber incidents without funds for comprehensive defenses. Although public grants subsidize initial security audits, ongoing protection—such as zero-trust and XDR platforms—remains out of reach for many. Providers are countering with subscription-priced, cloud-native stacks, yet the affordability gap persists in medium-term projections. [3]AI Landscape Austria, “Why Austria,” ai-landscape.at

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Integrated solutions dominate a compliance-driven landscape

Solutions controlled 63.28% of the Austria cybersecurity market in 2025, buoyed by consolidated platforms that fold network, endpoint, and identity protection into one policy engine. Cloud Security posted the fastest 11.85% CAGR, mirroring nationwide cloud migration for line-of-business apps and reflecting regulatory insistence on cloud event logging. Application and data-layer defenses are recording double-digit growth as GDPR enforcement tightens, while infrastructure and network appliances continue to safeguard energy and utility grids. Demand for integrated risk-management modules, able to report NIS2 and DORA metrics in a single dashboard, is rising among both banks and government agencies.

Services made up 36.72% of 2025 revenue, led by managed detection and response centres that compensate for domestic talent shortages. Public provider BRZ operates a national CERT model for federal ministries, showcasing appetite for 24/7 remote monitoring. Consulting remains brisk for gap assessments and certification support, but outcome-based MDR contracts are gaining momentum with SMEs eager to transfer operational risk. The Austria cybersecurity industry increasingly treats service subscriptions as an OPEX alternative to large upfront licensing.

By Deployment Mode: Cloud-first strategies reshape security blueprints

Cloud deployments captured 70.35% of spending in 2025 and are on a 11.78% CAGR trajectory as enterprises pursue scalability and centralised policy control. Many organisations already label new workloads “cloud-preferred” and allocate extra budget for posture management, CASB, and SaaS threat-prevention tools. The Austria cybersecurity market size tied to multi-cloud governance is projected to keep expanding through 2031 as firms juggle Amazon Web Services for elasticity, Microsoft Azure for productivity suites, and European sovereign clouds for sensitive data.

On-premises environments retain 29.65% share, anchored by utilities, defense contractors, and semiconductor fabs requiring air-gapped resilience. Rather than pure on-premises strategies, these operators blend local data lakes with secure cloud analytics to meet performance and sovereignty goals. Consequently, vendor road maps increasingly revolve around hybrid mesh architectures that move policy execution closer to workloads regardless of location.

By Organization Size: SME acceleration reshapes growth math

Large Enterprises held 56.24% of the Austria cybersecurity market share in 2025 thanks to deep compliance budgets, formal SOC teams, and global supply-chain exposure. Banks and insurers, for example, now roll out zero-trust blueprints spanning 12-country networks while tracking operational resilience indicators for supervisors. These organisations also pilot AI-assisted forensics to cut mean-time-to-detect by double digits.

SMEs are the fastest-growing cohort at 11.05% CAGR. The Austria cybersecurity market size attributed to mid-tier exporters, industrial parts makers, and digital agencies is benefiting from SaaS subscription models, managed SOC packages, and government vouchers for security audits. Vendors that bundle endpoint, email, and backup protection into one licence resonate strongly with this segment, where IT staff often juggle multiple roles.

By End User: Healthcare digitization lifts future demand

BFSI contributed 23.62% of revenue in 2025. All major Austrian banks now integrate security telemetry into trading platforms and mobile wallets, reinforcing customer trust amid rising fintech competition. DORA timelines prompt fresh investments in cross-border incident reporting and cryptographic key management.

Healthcare is sprinting ahead at a 12.45% CAGR. Hospitals expanding digital patient apps, remote diagnostics, and connected devices must protect sensitive electronic health records, pushing them to adopt micro-segmentation and secure access gateways. Industrial & defense automation, retail omnichannel roll-outs, and smart-grid upgrades in energy & utilities keep orders steady for threat-intelligence feeds and OT-specific firewalls.

Geography Analysis

Vienna hosts roughly half of Austria’s 300-plus AI and cybersecurity start-ups, making the capital the nerve centre for product innovation and 24/7 SOC operations. Its proximity to EU institutions and Central European partners also supports cross-border pilot projects under Horizon Europe. Graz and Linz follow as specialised hubs for industrial cybersecurity research and embedded-system protection. Cyberattack logs from 2024 show that incidents spread far beyond the capital, striking municipalities in Lower Austria, Carinthia, and Styria, which in turn stimulates regional demand for cyber-insurance and managed response services.

Austria’s national recovery programme sets aside €1.8 billion for broadband, cloud, and data-centre capacity, ensuring nationwide reach of modern security controls. Simultaneously, the NCC-AT links local companies to the EU-wide competence framework, giving them early access to research funding and standards alignment. Strategic participation in G7 resilience exercises and ENISA working groups positions Austrian suppliers as interface points for neighbours in Central and Eastern Europe, adding export revenue potential to the domestic Austria cybersecurity market.

Infrastructure modernisation plans for energy transition (ÖNIP) include mandatory cyber-resilience scoring for grid operators. Similar requirements extend to rail and public-transport projects, creating steady workflows for integrators across federal provinces. As a result, regional budgets increasingly earmark at least 6% of total IT spend for cybersecurity solutions that comply with both EU directives and national privacy statutes.

Regulatory Landscape

Austria's cybersecurity compliance environment is being reset by the national implementation of the EU NIS2 Directive via the Network and Information Systems Act 2026 (NISG 2026), published in December 2025 and entering into force on 1 October 2026. The law expands the regulated perimeter, strengthening risk-management, incident handling, and governance requirements while increasing the need for auditable controls across cloud security, identity, and integrated risk management.

Supervision and coordination are being centralized through the Bundesamt fuer Cybersicherheit, established under the Federal Ministry of the Interior. In parallel, responsibilities for NIS authority functions shifted from the Federal Chancellery to the Ministry of the Interior's Department IV/S/2 on 1 April 2025. The compliance clock is explicit: affected entities must register between 1 October 2026 and 31 December 2026 and submit a self-declaration on risk-management measures, including supply chain security, by 30 September 2027.

Value Chain Analysis

The Austria cybersecurity value chain covers global platform vendors and Austrian niche suppliers, which flow through local distributors and system integrators into enterprise and public-sector deployments. Procurement is increasingly shaped by regulated end users (BFSI, energy, healthcare, and government), with buying preferences shifting toward consolidated suites (network, endpoint, IAM, and cloud controls) supported by professional services for gap assessments, implementation, and certification support.

Downstream, managed security service providers and 24/7 monitoring centers are becoming key delivery nodes as organizations address talent shortages and operationalize continuous detection and response. On the public-sector coordination side, operational cybersecurity interfaces include the Federal Ministry of the Interior structure, GovCERT Austria, and the Cyberlagezentrum. Under NISG 2026, supply chain security is pushed deeper into the control set, increasing demand for third-party risk management, vendor assurance, and security testing as recurring service lines across the ecosystem.

Competitive Landscape

The vendor field remains moderately fragmented: no single supplier exceeds a 10% share, and the top five combined account for well under 50%. Multinationals such as IBM, Cisco, and Fortinet compete head-to-head with niche Austrian players including IKARUS, CyberTrap, and newcomer SignPath. The Austria cybersecurity market therefore rewards specialisation: deception-based analytics, quantum-resistant encryption, and code-signing automation each attract high-margin contracts in their niches.

Platform convergence is a visible trend. Cisco doubled European security product revenue after bundling secure access, XDR, and zero-trust into a single suite, mirroring client preference for fewer dashboards. Austrian integrators respond by packaging imported toolsets into managed service wrappers tuned to local compliance reporting.

Startup dynamism is strong. Dream, founded by former Chancellor Sebastian Kurz, secured USD 100 million to build AI language models designed for sovereign cybersecurity applications, while Arnika, an open-source VPN extension led by CANCOM Austria and AIT, brings quantum-safe protocols to critical-infrastructure operators. With European defense budgets ascending, dual-use security-and-surveillance firms such as HENSOLDT are also deepening their Austrian partnership networks.

Austria Cybersecurity Industry Leaders

Palo Alto Networks Inc.

Cisco Systems Inc.

Fortinet Inc.

IBM Corporation

RadarServices Smart IT-Security GmbH

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A gap remains between widespread baseline controls and lower uptake of advanced management practices across Austrian enterprises. Adoption is high for baseline measures such as data backup (90.51%) and network access control (76.68%), while gaps versus EU averages persist in more mature disciplines such as ICT risk assessments (32.48%) and security tests (33.76%). For vendors and service providers, this creates room to package continuous assessment, automated testing, and evidence-ready reporting into subscription offerings that fit SME budgets.

Regulatory milestones turn this whitespace into procurement programs with defined timelines, particularly for organizations brought into scope by NISG 2026. Mandatory registration runs from 1 October 2026 to 31 December 2026, and self-declarations covering risk management measures, explicitly including supply chain security, are due by 30 September 2027. These deadlines are driving demand for third-party risk tooling, audit support, and managed services that can industrialize compliance operations across distributed hybrid and multi-cloud environments.

Recent Industry Developments

- June 2026: AIRGAPNET GmbH secured a seven-figure investment to fund production, product development, and international expansion of its physical network separation technology. The capital infusion supports hardware-enforced segmentation for critical infrastructure and reinforces Austria's niche in domestically sourced security architectures.

- May 2026: KPMG/KSÖ published the 11th edition of the Cybersecurity in Austria study, surveying 1,396 domestic companies on cybercrime experiences. The report updates the risk landscape for policy makers and vendors targeting Austria's market.

- April 2026: Exclusive Networks Austria was recognized as Palo Alto Networks EMEA Distributor of the Year 2025. The award points to channel strength and momentum for vendor alignment in Austria's cybersecurity market.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Austria cybersecurity market is the spending in Austria on security software, hardware, and services that protect networks, endpoints, identities, applications, and data across on-premises and cloud environments.

Scope exclusions: We exclude general IT outsourcing, telecom connectivity spend, and non-security IT infrastructure unless it is sold and used mainly for cybersecurity outcomes.

Segmentation Overview

- By Offering

- Solutions

- Application Security

- Cloud Security

- Data Security

- Identity and Access Management

- Infrastructure Protection

- Integrated Risk Management

- Network Security Equipment

- Endpoint Security

- Other Solutions

- Services

- Professional Services

- Managed Services

- Solutions

- By Deployment Mode

- Cloud

- On-premise

- By Organization Size

- SMEs

- Large Enterprises

- By End User

- BFSI

- Healthcare

- IT and Telecom

- Industrial and Defense

- Retail

- Energy and Utilities

- Manufacturing

- Others

Data Sources, Market Sizing, and Validation

Desk Research

Desk research helped us set the market boundaries and build reliable starting points for demand and supply signals in Austria. We used public sources such as Eurostat, Statistics Austria, ENISA publications, Austrian CERT advisories, and EU-level rules and guidance (for example, NIS2 and DORA texts and timelines) to understand exposure, compliance pull, and investment cycles.

To translate this into a sizing model, we also reviewed company annual reports, investor decks, and reputable press coverage of security incidents and public tenders. Select paid subscriptions were used only for company financials and structured news screening, plus patent databases to check where new security capabilities are being built. The sources listed here are illustrative and not exhaustive, and we relied on other public and paid references for cross-checks and clarification.

Primary Interviews and Surveys

Primary work was used to test what desk research cannot show clearly, especially pricing movement, service attach rates, and how cloud security is being adopted in Austrian enterprises and government-linked bodies. We spoke with a mix of solution providers, managed service teams, distributors, system integrators, and buyer-side security leaders to validate assumptions across key industries in the country. Responses were also used to confirm procurement cycles, the split between new deployments and renewals, and realistic adoption timing for compliance-driven programs.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 14% | APAC: 46% |

| Mid tier: 52% | Functional/Unit leaders: 30% | EMEA: 33% |

| Smaller Players: 14% | Managers: 56% | Americas: 21% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs Austria cybersecurity demand from the addressable IT spend pool, then applies security intensity factors by industry and deployment shift. We corroborate totals with selective bottom-up checks such as sampled vendor revenue splits, partner channel checks, and a simple volume times average selling price approach for common tools and managed services, which helps reduce over-counting.

Key model inputs include the pace of cloud adoption, managed security service penetration in mid-market firms, incident frequency and severity signals that drive urgent spending, compliance timelines tied to EU and national requirements, and observed pricing patterns for subscriptions and services. When data gaps appear for smaller vendors or bundled contracts, we apply conservative allocation rules based on interview feedback, and we only count the security portion that can be reasonably separated.

For forecasting, we use scenario-based analysis supported by trend smoothing for stable categories. The scenarios are anchored to expected regulation readiness, macro IT budget outlook, and hiring constraints for security roles. Assumptions are reviewed with experts so the growth path reflects what can be implemented on the ground, not only what is planned.

Data Validation & Update Cycle

Outputs are checked through multiple passes so the totals align with real-world signals. We compare category splits against independent indicators such as tender activity, reported incident patterns, and the implied security share of IT budgets, then we investigate any large variances before sign-off.

A second analyst review is used to challenge key assumptions like cloud security mix, service attach rates, and currency conversion timing. Reports are refreshed annually, with interim updates when material events occur, such as major regulation changes, large breaches that shift spending, or visible pricing resets. Before delivery, an analyst performs a final update pass so clients receive the latest view available at that time.

Mordor Intelligence's Austria Cybersecurity Market Size Compared With Other Published Estimates

Different publishers often show different market sizes because the counted spend is not always the same, even when the market name looks identical. The gaps usually come from how services are treated, whether adjacent IT security related items are bundled in, and how aggressive the growth path is assumed to be.

Some external estimates fold in broader IT security and continuity services as a single bucket, then they back-cast values from a global share assumption. In Mordor Intelligence, only cybersecurity solutions and services sold for threat prevention, detection, response, and compliance are counted, and general IT operations work is left out unless it is clearly security-specific.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 560.00 M (2025) | |

| Industry Research Publisher A | USD 549.80 M (2024) | Uses a different base year and a broader service list that can blend cyber consulting and business continuity work, which shifts the starting value and lowers the implied growth rate. |

| Industry Research Publisher B | USD 860.30 M (2031) | Publishes only an end-year figure and applies a smoother CAGR from an earlier start year, which can understate pricing changes and timing effects from compliance-driven buying cycles. |

The table shows that most of the spread can be explained by scope choices and time anchors, not just math. By keeping inclusions tied to observable security buying categories and validating assumptions like service attach and subscription pricing through interviews, the final market size stays traceable to repeatable inputs.

Key Questions Answered in the Report

What is the current size of the Austria cybersecurity market?

The market is valued at USD 612.75 million in 2026 and is on track to reach USD 961.26 million by 2031.

Which segment is growing fastest within the Austria cybersecurity market?

Cloud Security leads with a 11.85% CAGR, reflecting extensive national cloud-first strategies.

How will the NIS2 Directive influence spending?

NIS2 expands mandatory security coverage to about 4,000 Austrian organizations, driving a short-term surge in compliance-oriented platform purchases

Why is healthcare a high-growth end-user segment?

Digital patient portals and connected medical devices elevate data-protection requirements, pushing healthcare cybersecurity outlays at a 12.45% CAGR.

What are the main challenges restraining the Austria cybersecurity market?

A shortage of skilled professionals and budget limitations among SMEs are the top restraints, together shaving roughly 3% off potential CAGR.

Which regions within Austria show heightened demand?

Vienna dominates due to its start-up ecosystem and headquarters concentration, while industrial provinces such as Styria and Upper Austria drive OT-centric security projects.

Page last updated on: