Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

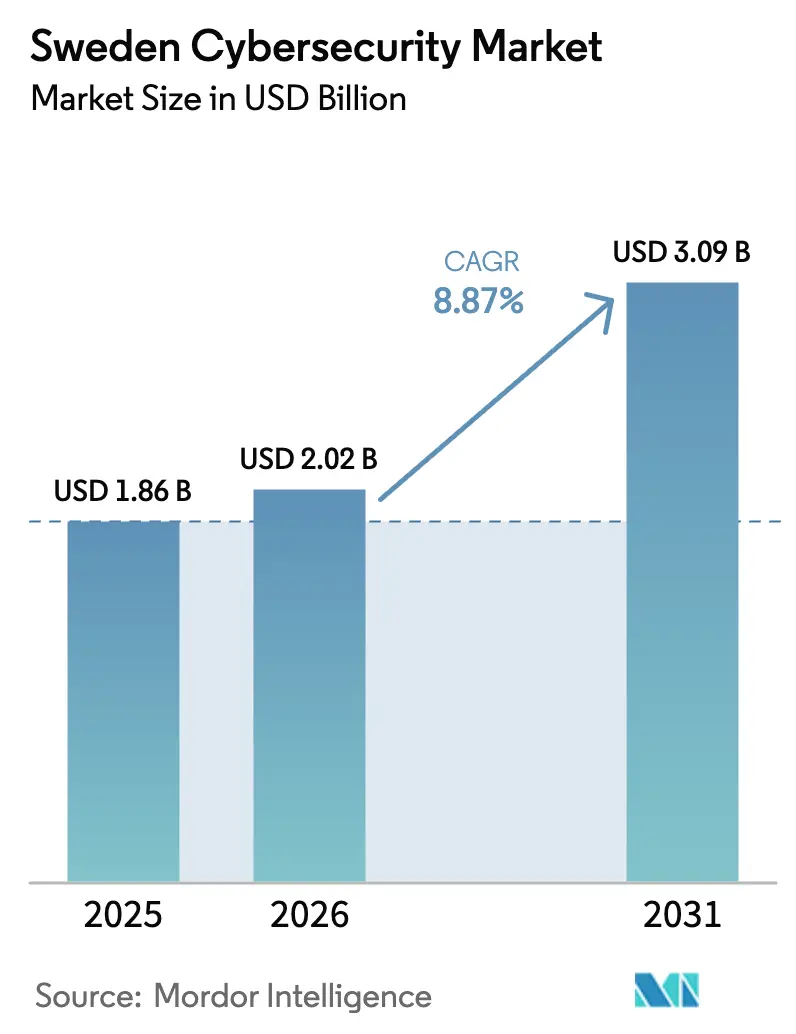

| Base Year Market Size (2025) | USD 1.86 Billion |

| Market Size (2026) | USD 2.02 Billion |

| Market Size (2031) | USD 3.09 Billion |

| Growth Rate (2026 - 2031) | 8.87% CAGR |

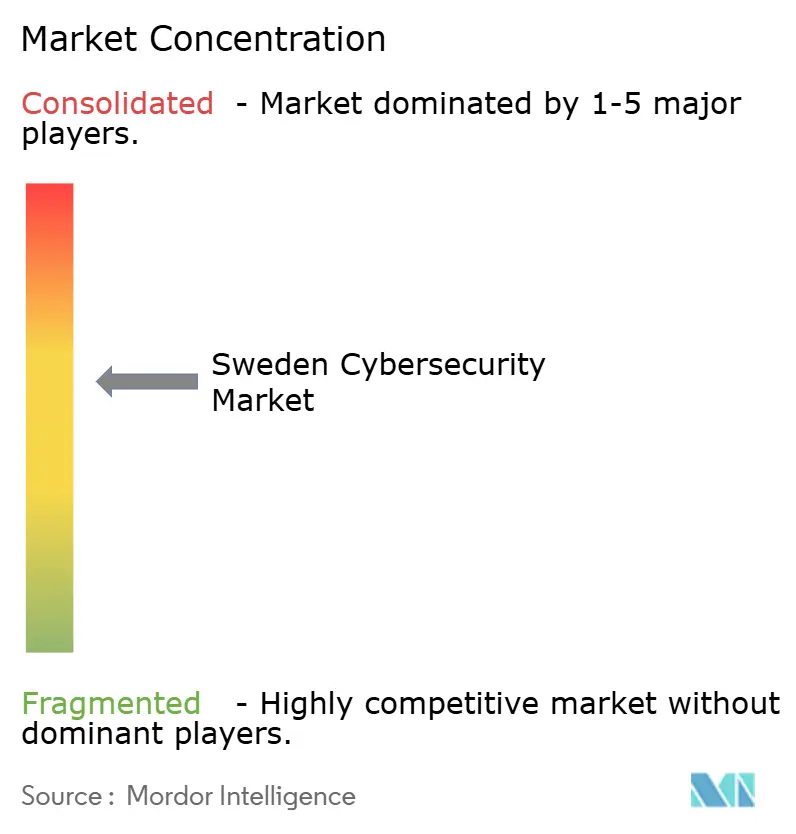

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sweden Cybersecurity Market Analysis by Mordor Intelligence

The Sweden cybersecurity market size is projected to be USD 1.86 billion in 2025, USD 2.02 billion in 2026, and reach USD 3.09 billion by 2031, growing at a CAGR of 8.87% from 2026 to 2031. Sweden’s transposition of the NIS2 Directive on 15 January 2026 has widened mandatory breach-reporting to roughly 3,000 entities, triggering a nationwide uplift in governance, risk, and compliance spending. NATO accession in 2024 heightened threat perceptions, leading the defense sector to ring-fence larger cyber budgets and spurring cross-border awards such as Clavister’s SEK 280 million (USD 26.7 million) appliance deal with the Norwegian Defence Materiel Agency. Cloud deployment dominates today’s architecture because pay-as-you-grow licensing aligns with Sweden’s cash-flow-oriented IT culture, while persistent skills shortages propel managed security services demand. Taken together, identity-centric controls, zero-trust adoption, and incident-response automation are expected to set the tone for new contracts through 2031.

Key Report Takeaways

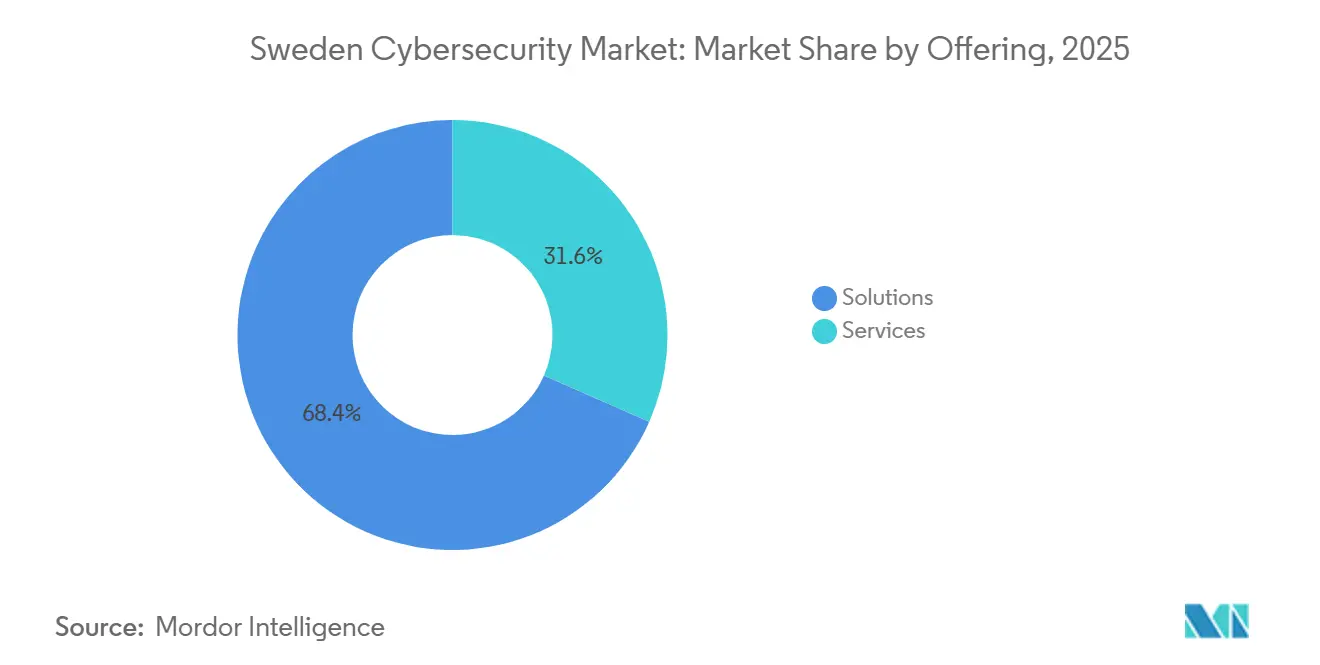

- By offering, solutions captured 68.38% revenue in 2025, while service is poised for the fastest 9.23% CAGR to 2031.

- By deployment, cloud held 63.23% of Sweden cybersecurity market share in 2025 and is expanding at an 9.02% CAGR through 2031.

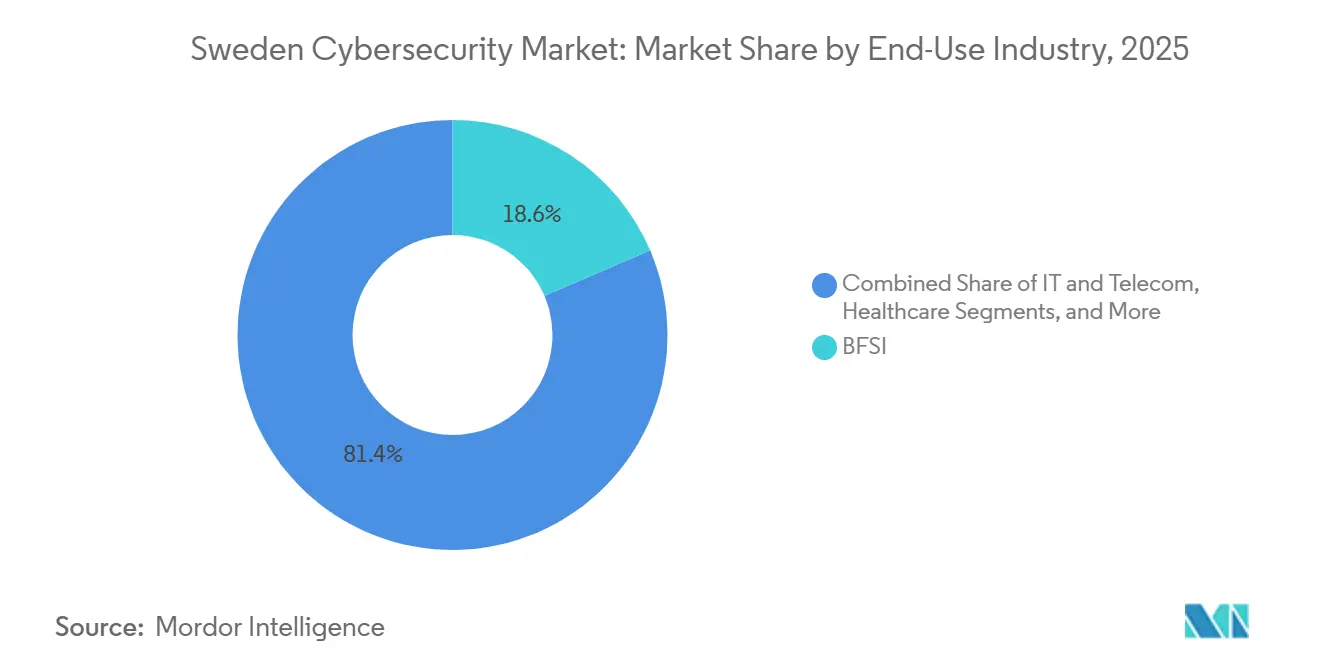

- By end user, BFSI led with 18.56% of Sweden cybersecurity market size in 2025; healthcare shows the quickest 10.11% CAGR to 2031.

- By enterprise size, large enterprises commanded 61.47% of the Sweden cybersecurity market size in 2025; SMEs record the highest 9.53% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Sweden Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Cybersecurity Compliance Mandates in Sweden | +2.3% | National, with concentrated enforcement in Stockholm, Gothenburg, Malmö | Short term (≤ 2 years) |

| Surge in Cloud Adoption Among Swedish Enterprises | +1.9% | National, with early adoption in IT and Telecom, BFSI sectors | Medium term (2-4 years) |

| Growing Remote Workforce and Endpoint Proliferation | +1.5% | National, with spillover to Nordic region | Medium term (2-4 years) |

| Strategic Focus on 5G Security in Telecom Ecosystem | +1.2% | National, with implications for EU telecom supply chains | Long term (≥ 4 years) |

| Sweden's Digitalization Grants for SME Cyber Upgrades | +0.9% | National, with priority regions in rural and mid-sized municipalities | Short term (≤ 2 years) |

| Rising Cybersecurity Talent Export Driving Managed Services Demand | +1.1% | National, with Nordic and European spillover | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Cybersecurity Compliance Mandates in Sweden

The Cybersecurity Act that transposed NIS2 on 15 January 2026 broadened incident-reporting to 3,000 operators across 14 sectors, compressing breach notification into a 24-hour window and imposing board-level accountability. Financial institutions simultaneously face Digital Operational Resilience Act rules that require yearly resilience tests for third-party ICT providers.[1]European Banking Authority, “Digital Operational Resilience Act Guidelines,” eba.europa.eu Manufacturers will soon come under the EU Cyber Resilience Act, mandating security-by-design in connected products. Together these statutes create multi-year procurement cycles favoring modular, API-driven platforms.

Surge in Cloud Adoption Among Swedish Enterprises

Cloud captured almost one-third of national IT budgets in 2025 as hybrid work and digital service delivery accelerated migration.[2]Microsoft, “Microsoft Expands Swedish Datacenter Regions for Sovereign Cloud,” microsoft.com Microsoft’s datacenter expansion offers sovereign-cloud options, allowing public bodies to keep workloads inside Swedish borders without losing hyperscale elasticity. Roughly 60% of large firms now operate on at least two providers, a pattern that reduces lock-in but complicates policy enforcement. As misconfigurations remain the dominant cause of cloud breaches, demand spikes for Cloud Security Posture Management and Cloud Workload Protection.

Growing Remote Workforce and Endpoint Proliferation

Hybrid work adoption hit 68% of knowledge workers in 2025, lifting the managed endpoint count by 40% in two years. The widened perimeter raises the profile of zero-trust architectures and endpoint detection and response solutions. CrowdStrike’s expanded Nordic partner roster now delivers enterprise-grade protection to mid-market customers. Internet of Things devices in industrial contexts add to exposure, with Swedish organizations logging an average recovery period of 8.07 months after endpoint-driven cyber incidents.

Strategic Focus on 5G Security in the Telecom Ecosystem

Huawei and ZTE remain barred from Swedish 5G networks following a 2024 appeals-court ruling, pushing operators toward trusted vendors such as Ericsson, Nokia, and Samsung. Ericsson embeds next-generation firewalls into its 5G core, partnering with Palo Alto Networks for real-time threat analytics. Sweden’s participation in EU 6G programs places quantum-resistant encryption and decentralized identity on the long-term roadmap.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Advanced Security Solutions for SMEs | -1.1% | National, with acute pressure in rural and mid-sized municipalities | Short term (≤ 2 years) |

| Shortage of Cybersecurity Professionals | -0.9% | National, with spillover to Nordic region | Long term (≥ 4 years) |

| Fragmented Data-Localization Debate | -0.6% | National, with implications for cross-border data flows | Medium term (2-4 years) |

| Open-Source Adoption Reducing Commercial Security Spend | -0.7% | National, with concentration in developer-heavy sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Security Solutions for SMEs

SMEs account for 99% of Swedish companies but spend only USD 150 per employee on cyber controls versus USD 450 at large enterprises. Upfront investments exceeding USD 50,000 for SIEM platforms remain prohibitive. Grants covering up to 50% of eligible outlays exist, yet paperwork deters small applicants. Subscription-based services ease cap-ex pressure but create tool overlap, breeding “subscription fatigue”.

Shortage of Cybersecurity Professionals

Sweden fields around 6,500 practitioners, 30% short of open roles. Universities have expanded enrollments, yet specialized skills cloud-native security or OT expertise remain scarce. Providers such as Truesec capitalise by offering 24 / 7 monitoring from the largest Nordic SOC. Red-hot overseas salary offers siphon 15% of graduates abroad within five years, thinning the local pool.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Accelerate as Talent Scarcity Fuels Outsourcing

Services revenue in the Sweden cybersecurity market expanded at 9.23% CAGR, outpacing overall growth as enterprises outsource 24 / 7 monitoring and incident response. Managed services providers plug the domestic talent gap, delivering economies of scale that internal teams rarely replicate. Solutions still controlled 68.38% of 2025 spending, anchored in identity, application, and cloud-security use cases. Convergence toward platform suites continues as buyers seek simplified procurement and unified management.

Sustained demand for governance and compliance tooling flows directly from fresh mandates. Integrated risk dashboards that map ISO 27001 and NIS2 controls into executive-friendly KPIs attract board interest. Zero-trust pivots elevate identity and access management to priority status, while legacy network security boxes migrate toward cloud-managed versions, lowering maintenance overhead.

By Deployment Mode: Cloud Dominance Reflects Infrastructure Modernization

Cloud accounts for 63.23% of 2025 outlays and will retain the growth lead through 2031 as elasticity, rapid provisioning, and Opex pricing remain irresistible to Swedish CFOs. The Sweden cybersecurity market size for cloud-delivered controls reached USD 1.18 billion in 2026. Hyperscalers’ Swedish regions satisfy data-residency clauses without performance trade-offs, removing a historic adoption brake.

On-premises equipment survives in air-gapped defense and critical-infrastructure zones where latency or classification bars cloud gateways. Hybrid architectures, now mainstream in 60% of large companies, increase policy fragmentation and force adoption of unified control planes. Continuous cloud configuration scanning has become table stakes because 70% of cloud breaches stem from misconfigurations.

By End-Use Industry: Healthcare Surges on Digital Mandates

BFSI generated the largest 18.56% spend slice in 2025, but hospital and life-science environments will clock the fastest 10.11% CAGR. Region Stockholm’s electronic health record overhaul magnifies vulnerabilities, prompting investments in encryption, privileged access, and zero-trust network segmentation. The Sweden cybersecurity market share of healthcare is set to enlarge as compliance and patient-safety stakes climb.

E-commerce and retail focus on payment fraud as online shopping penetration exceeds 85%, illustrated by Klarna’s AI-enabled risk engine deployment. Manufacturing leaders such as Volvo and ABB isolate operational technology from IT networks, deploying micro-segmentation to protect production uptime. Energy utilities, newly captured under NIS2, invest heavily in threat detection for supervisory control and data acquisition systems.

By Enterprise Size: SMEs Accelerate as Grants Lower Barriers

Large organizations commanded 61.47% of 2025 expenditure, but SMEs will outpace them at 9.53% CAGR through 2031. Grants covering half of eligible costs and the arrival of one-click, multi-tenant security platforms shrink historical barriers. The Sweden cybersecurity market size for SMEs is projected to climb from USD 0.72 billion in 2026 to USD 1.15 billion by 2031. Managed service bundles from Orange Cyberdefense or Nixu provide right-sized 24 / 7 coverage without personnel overhead.

Large enterprises increasingly rationalize vendor sprawl, moving from best-of-breed silos toward consolidated suites where licensing, SOC dashboards, and threat intel integrate natively. Even so, specialized tools survive for deep-packet inspection or OT anomaly detection, preserving wallet share for niche suppliers.

Geography Analysis

Stockholm, Gothenburg, and Malmö together generate roughly 70% of national spending as finance, tech, and public-sector buyers cluster in these metros. Stockholm anchors the startup scene, hosting 90 of the nation’s 201 cyber ventures and attracting USD 254 million in disclosed funding rounds.[3]Detectify, “Company Overview and Funding History,” detectify.com Government grants aim to raise maturity in smaller municipalities by subsidizing endpoint and cloud security.

Internationally, Sweden works through the EU’s Cybersecurity Competence Centre and coordinates Nordic intelligence sharing. NATO membership from 2024 pushed defense budgets higher, rewarding vendors holding high-assurance certifications. The nation also shapes pan-EU 6G security pilots, preserving a seat at the standards table.

Meanwhile, politically motivated distributed-denial-of-service campaigns have averaged 40 incidents annually since the NATO decision, lengthening mean-time-to-recovery to 8.07 months. Telcos must now block spoofed calls under new Swedish Post and Telecom Authority rules, catalyzing AI-enhanced traffic-analytics deployments.

Competitive Landscape

The Sweden cybersecurity market supports about 201 active vendors. The ten largest suppliers together command roughly major share of revenue, so no single firm can dictate pricing. Global platforms such as Palo Alto Networks, Fortinet, Cisco Systems, and CrowdStrike lead volume segments by bundling firewalls, endpoint analytics, and threat intelligence. Swedish specialists Clavister and Advenica win public sector deals by holding high-assurance certifications that foreign rivals lack. Truesec operates Northern Europe’s largest security operations center with more than 300 analysts, giving it scale in managed detection and response.

Buyers show a clear tilt toward platform consolidation that reduces console sprawl and simplifies license management. Global vendors answer by integrating cloud security, identity, and analytics into single subscriptions that fit Sweden’s preference for predictable Opex. Local challengers counter with deep Nordic threat models, multilingual support, and rapid product iterations. The chronic 30% talent shortfall pushes many enterprises to outsource monitoring, which lifts demand for managed service offerings from Truesec, Orange Cyberdefense, and Nixu. Artificial intelligence and automation tools that lower analyst workload have become key differentiators in competitive bids.

Merger activity is brisk, highlighted by Insight Partners’ 2024 purchase of Detectify and Truesec’s takeover of Foresights in the same year. Private capital continues to flow, as seen in EQT’s majority stake in Acronis, meaning growth funding is readily available for Swedish innovators. Strategic alliances are also expanding, for example Ericsson’s partnership with Palo Alto Networks that embeds firewalls inside 5G core networks. Compliance milestones such as the NIS2 transposition reward vendors that can document governance controls, sharpening the competitive divide between full-stack providers and point product makers.

Sweden Cybersecurity Industry Leaders

Palo Alto Networks Inc.

Check Point Software Technologies Ltd.

Fortinet Inc.

Cisco Systems Inc.

Trend Micro Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Clavister secured a SEK 280 million (USD 26.7 million) Norwegian defense order for network-security appliances.

- January 2026: Sweden’s Cybersecurity Act entered force, transposing NIS2 and expanding breach-reporting obligations.

- December 2025: Advenica won a SEK 58 million (USD 5.5 million) data-diode contract from a Swedish authority.

- June 2025: Brookfield Asset Management confirmed a SEK 95 billion (USD 9.95 billion) AI-center project in Strängnäs, doubling national hyperscale capacity and elevating demand for cloud-native defenses.

Sweden Cybersecurity Market Report Scope

The Cybersecurity Market encompasses global spending on solutions, software, and services designed to protect digital infrastructure, data, and operations across all industries, including cloud, network, endpoint, and application security; it includes enterprise, government, and SME segments but excludes physical security and pure consulting-only services, with the market evolving rapidly toward AI-driven automation, platform consolidation, and regulatory-driven transformation.

The Sweden Cybersecurity Market Report is Segmented by Offering (Solutions [Application Security, Cloud Security, Data Security, Identity and Access Management, Infrastructure Protection, Integrated Risk Management, Network Security, End Point Security], Services [Professional Services, Managed Services]), Deployment Mode (On-Premises, Cloud), End-Use Industry (IT and Telecom, BFSI, Healthcare, Industrial Manufacturing, Retail and E-commerce, Energy and Utilities, Aerospace, Military and Defense, Other End-Use Industries), and End-User Enterprise Size (Large Enterprises, Small and Medium Enterprises). The Market Forecasts are Provided in Terms of Value (USD).

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| End Point Security | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| On-Premises |

| Cloud |

By End-use Industry

| IT and Telecom |

| BFSI |

| Healthcare |

| Industrial Manufacturing |

| Retail and E-commerce |

| Energy and Utilities |

| Aerospace, Military and Defense |

| Other End-use Industries |

By End-User Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| End Point Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | On-Premises | |

| Cloud | ||

| By End-use Industry | IT and Telecom | |

| BFSI | ||

| Healthcare | ||

| Industrial Manufacturing | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Aerospace, Military and Defense | ||

| Other End-use Industries | ||

| By End-User Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

Key Questions Answered in the Report

How large will Sweden’s cybersecurity outlays be by 2031?

Spending is forecast to reach USD 3.09 billion by 2031, reflecting an 8.87% CAGR from 2026.

Which deployment model is growing fastest in Sweden?

Cloud-delivered security is set to advance at 9.02% CAGR, retaining the largest 63.23% share.

Why is healthcare the quickest-expanding vertical?

Digital health mandates, electronic records, and telemedicine raise compliance and data-protection stakes, driving a 10.11% CAGR.

How does the talent shortage shape purchase decisions?

A 30% skills gap steers many firms toward managed security services instead of building in-house teams.

What impact does NATO membership have on Sweden’s cyber market?

Elevated threat perceptions and defense-budget uplifts accelerate procurement of high-assurance security systems, especially for critical infrastructure.

Page last updated on: