Nordics Cybersecurity Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

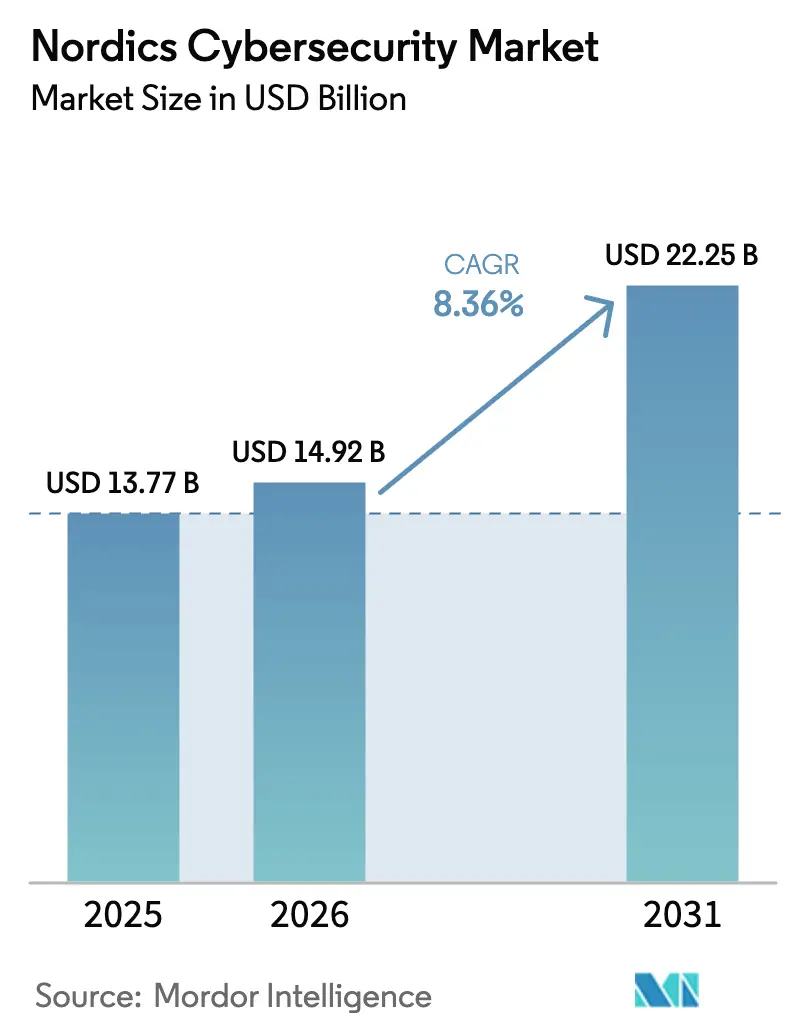

| Base Year Market Size (2025) | USD 13.77 Billion |

| Market Size (2026) | USD 14.92 Billion |

| Market Size (2031) | USD 22.25 Billion |

| Growth Rate (2026 - 2031) | 8.36% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nordics Cybersecurity Market Analysis by Mordor Intelligence

Nordics cybersecurity market size in 2026 is estimated at USD 14.92 billion, growing from 2025 value of USD 13.77 billion with 2031 projections showing USD 22.25 billion, growing at 8.36% CAGR over 2026-2031. Heightened geopolitical pressure, especially after Finland’s 2023 NATO accession and Sweden’s ongoing integration, channels fresh capital toward critical-infrastructure protection, managed XDR platforms, and AI-driven security operations. Government stimulus under the Nordic Defence Cooperation framework spurs joint procurement, while country-level “security-by-design” mandates hasten adoption of integrated risk management tools that automate incident reporting within 24 hours. Demand is also fueled by 5G-enabled Industry 4.0 programs that expand OT attack surfaces, compelling energy, manufacturing, and automotive verticals to converge IT and OT defenses. Vendor consolidation accelerates as end users trim tool sprawl, with platform suppliers promising mean-time-to-detection cuts of 40-60% and sizable operational-cost savings.

Key Report Takeaways

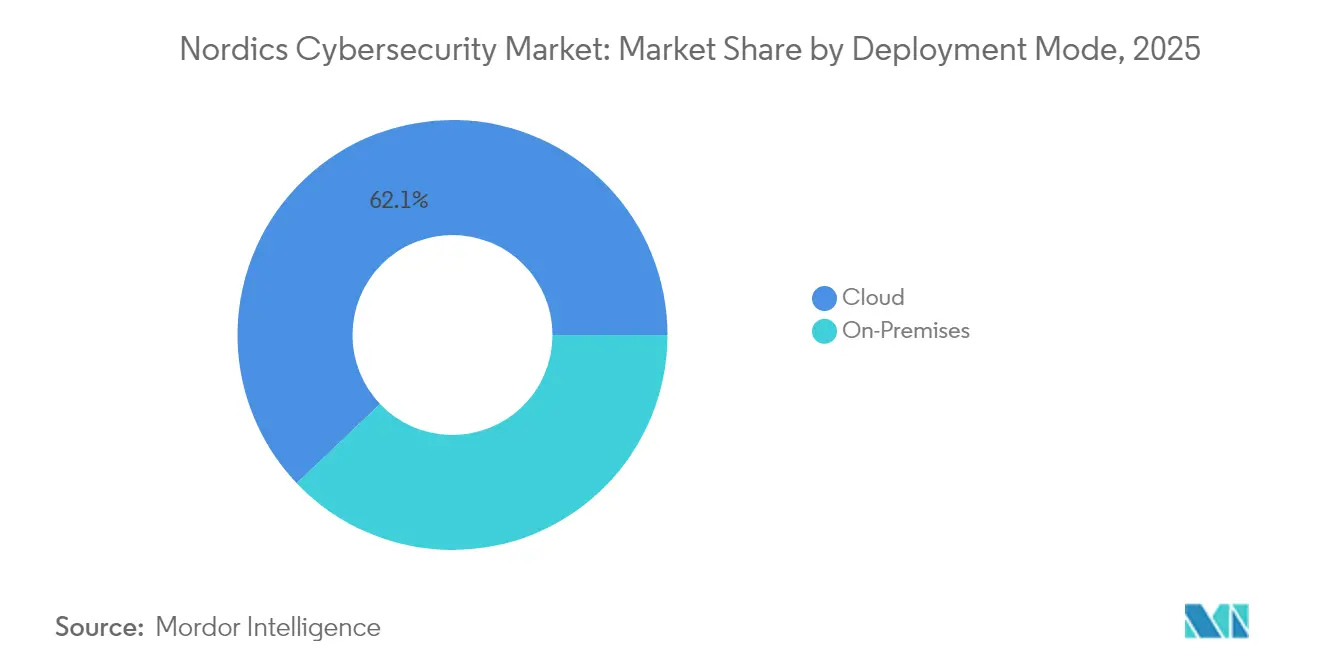

- By offering, cloud security led with 25.62% of Nordics cybersecurity market share in 2025, whereas integrated risk management is projected to grow at a 14.86% CAGR to 2031.

- By deployment mode, cloud deployment accounted for 62.10% share of the Nordics cybersecurity market size in 2025 and is expanding at a 13.02% CAGR through 2031.

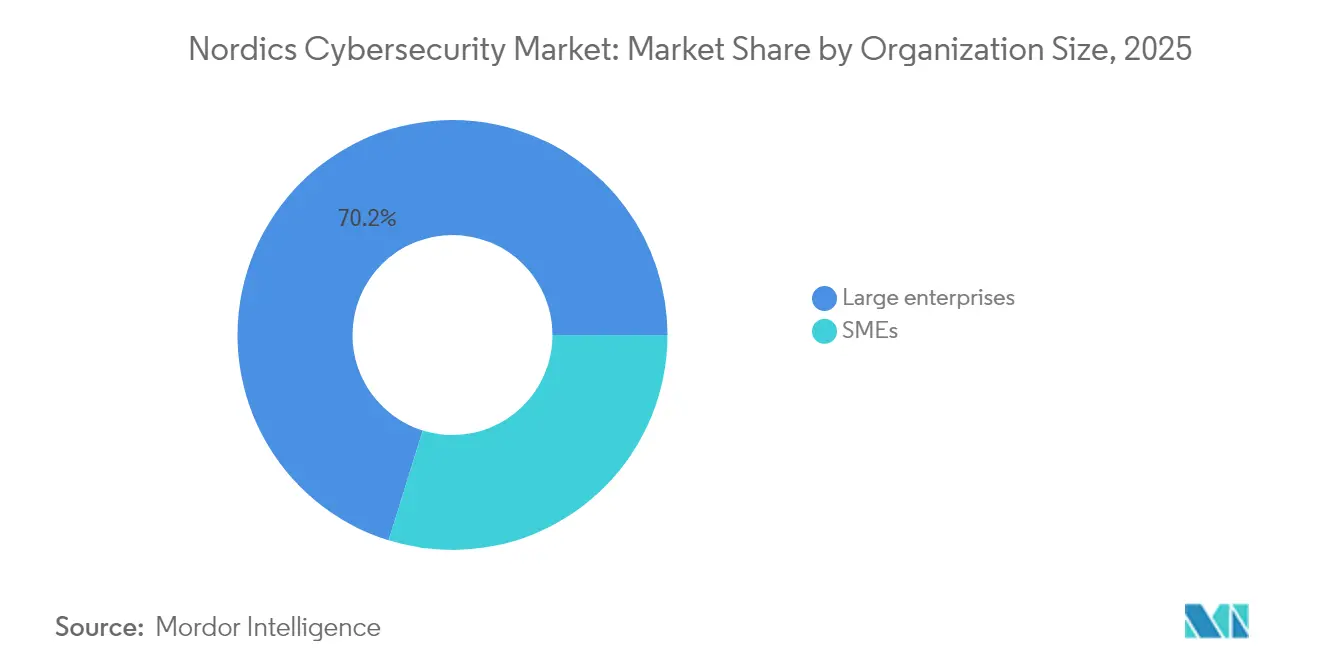

- By organisation size, large enterprises held 70.20% of the Nordics cybersecurity market share in 2025, while SMEs post the quickest 11.21% CAGR to 2031.

- By end-user vertical, BFSI captured 23.10% share of the Nordics cybersecurity market size in 2025; Industrial and Defence is climbing at a 12.31% CAGR.

- By country, Sweden commanded 38.65% market share in 2025, whereas Norway exhibits the fastest 9.82% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Nordics Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating roll-out of 5G-enabled Industry 4.0 production lines | 1.80% | Sweden, Finland core with spillover to Norway, Denmark | Medium term (2-4 years) |

| Public-sector "security-by-design" mandates under NIS2 & DORA | 2.10% | Global Nordic region | Short term (≤ 2 years) |

| Vendor consolidation to managed XDR platforms | 1.40% | Sweden, Norway primary markets | Medium term (2-4 years) |

| AI-driven automated SOC & SecOps tooling | 1.60% | Denmark, Sweden technology hubs | Short term (≤ 2 years) |

| Shift to cloud-native ERP modernisation in BFSI | 0.90% | Sweden, Denmark financial centers | Medium term (2-4 years) |

| NATO accession–linked defence cyber funding surge | 1.20% | Finland, Sweden defense sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating roll-out of 5G-enabled Industry 4.0 production lines

Real-time connected robotics, machine-vision inspection, and predictive-maintenance workloads running across private 5G networks have multiplied OT entry points that legacy perimeter controls never addressed. Swedish automakers and Finnish electronics assemblers therefore allocate bigger budgets to zero-trust micro-segmentation, 5G-aware intrusion detection, and protocol translation gateways capable of bridging Modbus, OPC-UA, and IP traffic. Integrators report that each brownfield manufacturing site requires six to nine months of phased security retrofits, while co-developed security frameworks between IT and OT teams checkpoint every automation sprint. The resulting demand spike benefits Nordic vendors with deep OT know-how and global platform leaders that bundle 5G policy engines into consolidated firewalls, thereby raising average contract values and locking in multi-year managed-service revenues.

Public-sector “security-by-design” mandates under NIS2 and DORA

NIS2 obliges organisations exceeding 250 employees or EUR 50 million turnover to file breach reports within 24 hours and to pass yearly risk-maturity audits, while DORA layers mandatory threat-led penetration tests for financial entities. Denmark enacted the rules in March 2025 covering nearly 1,500 entities, and Norway’s Digital Security Act applies fines up to 4% of global turnover for non-compliance. Compliance deadlines compress procurement cycles, pushing high-growth orders for policy-automation software, evidence-tracking modules, and managed compliance services. Nordic banks deploy resilience dashboards that map system dependencies against DORA stress-scenarios and auto-populate regulators’ templates, cutting audit preparation by 70%.

Vendor consolidation to managed XDR platforms

CISOs faced with double-digit tool counts and scarce Nordic-language analysts increasingly favour single-stack XDR suites that fuse SIEM, SOAR, EDR, and NDR data under one analytics plane. Consolidation momentum quickened in 2024 when Logpoint added Danish AI specialist Muninn, providing regionally trained language models that lower false positives on Scandinavian log formats. Norwegian power utilities now negotiate multi-year XDR service contracts that include 24/7 SOC outsourcing and threat-hunting retainer hours. Enterprises cite mean-time-to-detect cuts from 14 hours to under 5 hours, freeing staff for red-team simulations and board-level risk reviews.

AI-driven automated SOC and SecOps tooling

The Nordics will need roughly 300,000 additional security professionals by 2029, but local graduate pipelines fall short. AI-enhanced orchestration tackles repetitive triage tasks, correlating asset inventories, CVE feeds, and MITRE ATTandCK heat maps to surface high-certainty alerts. Danish cloud-software firms report 50-70% drops in false alarms after deploying ML-led playbooks that auto-quarantine suspect endpoints and launch no-code forensics jobs. Deepfake voice identification modules now sit on inbound-call systems at Swedish banks to catch fraud that tripled in 2024, while AI-assisted e-discovery tools shorten GDPR data-subject-access responses to hours instead of days.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute shortage of Nordic-language cyber talent | -1.90% | Regional, most severe in Finland, Norway | Long term (≥ 4 years) |

| High electricity prices limiting on-prem crypto workloads | -0.80% | Denmark, Sweden energy-intensive sectors | Medium term (2-4 years) |

| SME under-investment below 5% of IT budget | -1.10% | Regional SME sector | Short term (≤ 2 years) |

| Fragmented legacy operational tech in utilities | -0.70% | Norway, Finland utilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Acute shortage of Nordic-language cyber talent

Vacancy ratios top 40% for roles requiring Swedish or Finnish language skills, and salary inflation tops 12% annually for mid-level security architects. Public agencies postpone SOC modernisation projects, while private-sector firms spend on international contractors who lack regional compliance fluency. Training programs sponsored by telecom operators add only 2,000 graduates yearly, leaving a persistent gap. This scarcity propels uptake of autonomous attack-surface monitoring and managed detection services embedded with local-language playbooks, yet long-term talent constraints continue to cap deployment velocity for bespoke security programmes.

High electricity prices limiting on-prem crypto workloads

Nordic electricity futures rose 31% between 2024 and 2025 after hydro output dipped below 20-year averages. Data-centre operators running on-prem HSM clusters face OPEX spikes, prompting moves to cloud-based key-management services that promise 30% lower per-transaction cost yet raise data-sovereignty debates. Danish pharma manufacturers are deferring rollouts of domestic quantum-safe cryptography pilots until wholesale power rates stabilise, slowing certain high-security workload migrations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Acceleration Reshapes Architecture

Cloud deployment commanded 62.10% share of the Nordics cybersecurity market size in 2025, equating to USD 8.55 billion. Cost-benefit analyses show 30-40% security infrastructure savings when shifting to shared-responsibility models, while threat telemetry coverage broadens through SaaS audit APIs. Nordic ministries migrate citizen-service portals to private-cloud zones, stipulating that workloads remain within Schengen borders, thereby elevating interest in regionally hosted cloud-native security stacks.

On-prem environments persist in energy, defence, and high-assurance manufacturing, where deterministic latency and air-gap policies remain non-negotiable. Statnett’s OT control-room overhaul illustrates hybrid practice: administrative IT logs ship to a public-cloud SIEM, whereas grid-control enclaves retain on-prem collectors protected by host-based firewalls. Over the forecast period, as utilities modernise substations and automate patch-management, cloud-delivered security analytics will gradually absorb visibility, but sovereign-cloud constructs will still anchor final-mile compliance for classified data.

By Organization Size: SME Growth Challenges Enterprise Dominance

Large enterprises held 70.20% of 2025 revenues as board-level risk appetites justify multi-million-euro security stack renewals and 24/7 SOC staffing. Fortune-500-scale Nordic multinationals funnel budgets into AI-enhanced threat-hunting and red-team labs. Conversely, SMEs add momentum with 11.21% CAGR as digital invoicing mandates, e-ID integration, and NIS2 reporting pull them into regulated territory.

Budget-constrained SMEs favour subscription bundles that wrap endpoint, email, and vulnerability scanning in one console, often procured via telecom resellers who already invoice broadband connectivity. Vendor roadmaps now include “click-to-comply” wizards tailored to local Data Protection Authorities, further easing adoption. While average SME deal size remains modest, volume scales quickly, and low churn underpins predictable recurring revenue that diversifies vendor portfolios beyond enterprise concentration risk.

By End-user Vertical: Industrial and Defence Surge Challenges BFSI Leadership

BFSI retained 23.10% of 2025 spending as banks invest in anti-fraud analytics, mobile-banking hardening, and DORA-mandated resilience testing. Nordic lenders use model-risk frameworks to ration cybersecurity outlays across open-banking APIs, real-time payments, and cloud-native micro-services that underpin anything-as-a-service retail products.

Industrial and Defence, projected at a 12.31% CAGR, benefits from NATO-aligned cyber ranges, renewable-energy OT visibility, and drone-command network protection. Energy majors allocate double-digit shares of capex to identity segregation, sensor telemetry, and encrypted telemetry backhaul, while defence primes co-develop fortified DevSecOps pipelines for classified systems. Healthcare, telecoms, and public administration each notch mid-single-digit growth as e-health records, 5G rollout schedules, and citizen-ID schemes expand their threat surfaces.

Geography Analysis

Sweden’s 38.65% revenue share comes from its digital-government maturity, export-heavy manufacturing, and deep fintech stack. The state’s EUR 5.3 billion IT-transformation program backs electronic-ID expansion and national-cloud investments, ensuring continuous demand for identity governance, SIEM, and zero-trust architecture services. Swedish start-ups like Detectify and Outpost24 supply attack-surface management SaaS consumed globally, cementing the country as an innovation beacon.

Norway leads growth with 9.82% CAGR. Its NOK 20 million federal cyber-modernisation fund, plus multi-year commitments from Equinor, Statnett, and the USD 1.6 trillion Government Pension Fund, inject steady projects around OT segmentation, sovereign-cloud logs, and AI-aided SOC correlation. Critical-infrastructure directives require event telemetry retention for five years, driving storage and analytics subscription revenue and nudging utilities toward unified OT-IT observability.

Denmark and Finland round out the region. Denmark’s fintech and shipping clusters adopt secure-access-service-edge (SASE) to safeguard distributed workforces and maritime IoT. The relaunch of the National Cyber Security Council and EUR 100 million earmarked for cyber resilience accelerates SME onboarding to managed services. Finland leverages decades of telecom RandD and its NATO gateway role to prototype quantum-resistant encryption, 6G threat-modelling, and classified sovereign-cloud testbeds that will cascade into civil markets. Collective geographic growth remains underpinned by unified Nordic standards bodies that exchange best practice, harmonising buyer requirements and shortening vendor sales cycles.

Competitive Landscape

The Nordics cybersecurity market hosts a layered vendor mix comprising US platform giants and home-grown specialists. Fortinet, Palo Alto Networks, and CrowdStrike anchor the high-end platform tier; Fortinet posted USD 5.96 billion 2024 revenue and guides to USD 6.65-6.85 billion for 2025. Their single-pane consoles resonate with enterprises seeking to rationalise overlapping point products.

Regional champions WithSecure, Mnemonic, Arctic Security, and Logpoint leverage cultural proximity, Nordic-language threat intel, and privacy-by-design credentials. Logpoint’s 2024 acquisition of Muninn infused AI-driven anomaly detection into its SIEM, boosting upsell potential to existing public-sector accounts. Telecom-linked players like Telenor Cyberdefence widen managed-service footprints by folding in Combitech’s OT expertise, signalling a march toward bundled SASE plus managed SOC offers.

M&A intensity is forecast to stay elevated as investors chase platform plays that weld threat-intelligence feeds, identity analytics, and compliance automation. Vendors differentiating through sovereign-cloud hosting, quantum-safe crypto, or OT-specific protocol mastery will command valuation premiums. Buyers show heightened preference for vendor viability and roadmap clarity, rewarding suppliers with broad partner ecosystems and in-region support desks.

Nordics Cybersecurity Industry Leaders

International Business Machines Corporation

Cisco Systems, Inc.

Fortinet, Inc.

WithSecure Corporation

Dell Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Allurity finalised acquisitions of Infigo and Onevinn, lifting headcount to 700 across 18 countries.

- April 2025: Socket bought Danish static-analysis firm Coana, deepening supply-chain code security capabilities.

- May 2025: Fortinet posted USD 1.54 billion Q1 revenue, up 14% YoY, underpinned by Unified SASE expansion.

- January 2025: CrowdStrike and GuidePoint Security crossed USD 1 billion in combined sales, highlighting surging appetite for Falcon Next-Gen SIEM.

Nordics Cybersecurity Market Report Scope

Cybersecurity solutions help an organization monitor, detect, report, and counter cyber threats, which are internet-based attempts to damage or disrupt information systems and hack critical information using spyware, malware, and phishing to maintain data confidentiality.

The Nordics cybersecurity market is segmented by offerings (solutions [application security, cloud security, data security, identity access management, infrastructure protection, integrated risk management, network security, end-point security, and other solution types] and services [professional services and managed services]), by deployment (On-premise, and cloud), by organization size (SMEs, large enterprises), by end-user vertical (BFSI, healthcare, IT and telecom, industrial and defense, retail, energy and utilities, manufacturing, and other end-user industries), by country (Denmark, Norway, Sweden, Finland). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security Equipment | |

| Endpoint Security | |

| Other Solutions | |

| Services | Professional Services |

| Managed Services |

| Cloud |

| On-premise |

| SMEs |

| Large Enterprises |

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defence |

| Retail |

| Energy and Utilities |

| Manufacturing |

| Others |

| Denmark |

| Norway |

| Sweden |

| Finland |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security Equipment | ||

| Endpoint Security | ||

| Other Solutions | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | Cloud | |

| On-premise | ||

| By Organisation Size | SMEs | |

| Large Enterprises | ||

| By End-User Vertical | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defence | ||

| Retail | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Others | ||

| By Country | Denmark | |

| Norway | ||

| Sweden | ||

| Finland | ||

Key Questions Answered in the Report

What is the current value of the Nordics cybersecurity market?

The Nordics cybersecurity market size stands at USD 14.92 billion in 2026 and is set to reach USD 22.25 billion by 2031.

Which regulatory frameworks are having the greatest impact on cybersecurity spending in the Nordics?

Mandatory compliance with the European Union’s NIS2 directive and the Digital Operational Resilience Act (DORA) is accelerating security investments across both public and private sectors, especially in Denmark and Norway where fines for non-compliance reach up to 4% of annual turnover

What is the biggest restraint on market growth?

A severe shortage of Nordic-language cybersecurity talent—Sweden alone needs nearly 300,000 additional professionals by 2029—continues to delay project timelines and keeps labor costs high

Which country shows the fastest market growth through 2031?

Norway leads with a projected 9.82% CAGR, propelled by large-scale energy digitization projects and fresh government funding tied to the Digital Security Act

How is vendor consolidation shaping the competitive landscape?

Regional specialists and global platform vendors are merging or acquiring AI-driven capabilities—such as Logpoint’s purchase of Muninn—to offer unified XDR suites and address talent shortages, while Fortinet continues to expand revenue, guiding up to USD 6.85 billion for 2025

Page last updated on: