Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

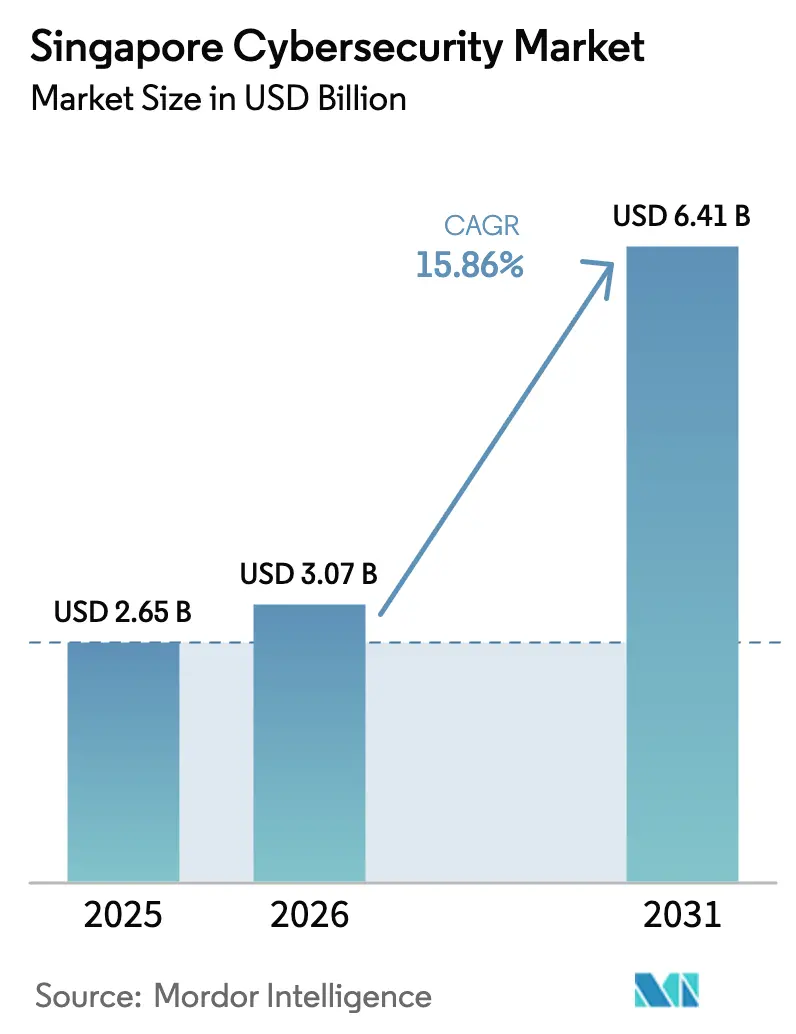

| Base Year Market Size (2025) | USD 2.65 Billion |

| Market Size (2026) | USD 3.07 Billion |

| Market Size (2031) | USD 6.41 Billion |

| Growth Rate (2026 - 2031) | 15.86% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Cybersecurity Market Analysis by Mordor Intelligence

Singapore Cybersecurity market size in 2026 is estimated at USD 3.07 billion, growing from 2025 value of USD 2.65 billion with 2031 projections showing USD 6.41 billion, growing at 15.86% CAGR over 2026-2031 and confirming the city-state’s status as Southeast Asia’s digital command center[1]Cyber Security Agency of Singapore, “Singapore Cyber Landscape 2024,” csa.gov.sg. Corporate boards attribute the growth to elevated threat volumes—cybercrime already formed 49.2% of all offences logged in 2023—and to the rising density of hyperscale data-center investments that surpassed 1.4 GW of active or committed IT load by mid-2024. Procurement teams now judge offerings on delivered risk reduction rather than feature counts, with 67% of large enterprises insisting on key-risk indicators in 2024 contracts. A pronounced shift toward converged IT-OT defence reflects automated port terminals and smart factories that prefer one security control plane over siloed stacks. Zero-trust policies, mandated across critical infrastructure, have already trimmed unauthorized-privilege cases at banks by 42% since mid-2023.

Key Report Takeaways

- By offering, Services held a 59.60% Singapore Cybersecurity market share in 2025, while cloud security solutions are poised to deliver a 15.52% CAGR to 2031.

- By deployment mode, On-premises retained 54.30% share of the Singapore Cybersecurity market size in 2025; cloud deployments are forecast to expand at a 16.93% CAGR through 2031.

- By end-user enterprise size, large enterprises commanded 77.60% of spending in 2025; SME demand is set for an 18.09% CAGR over the forecast horizon.

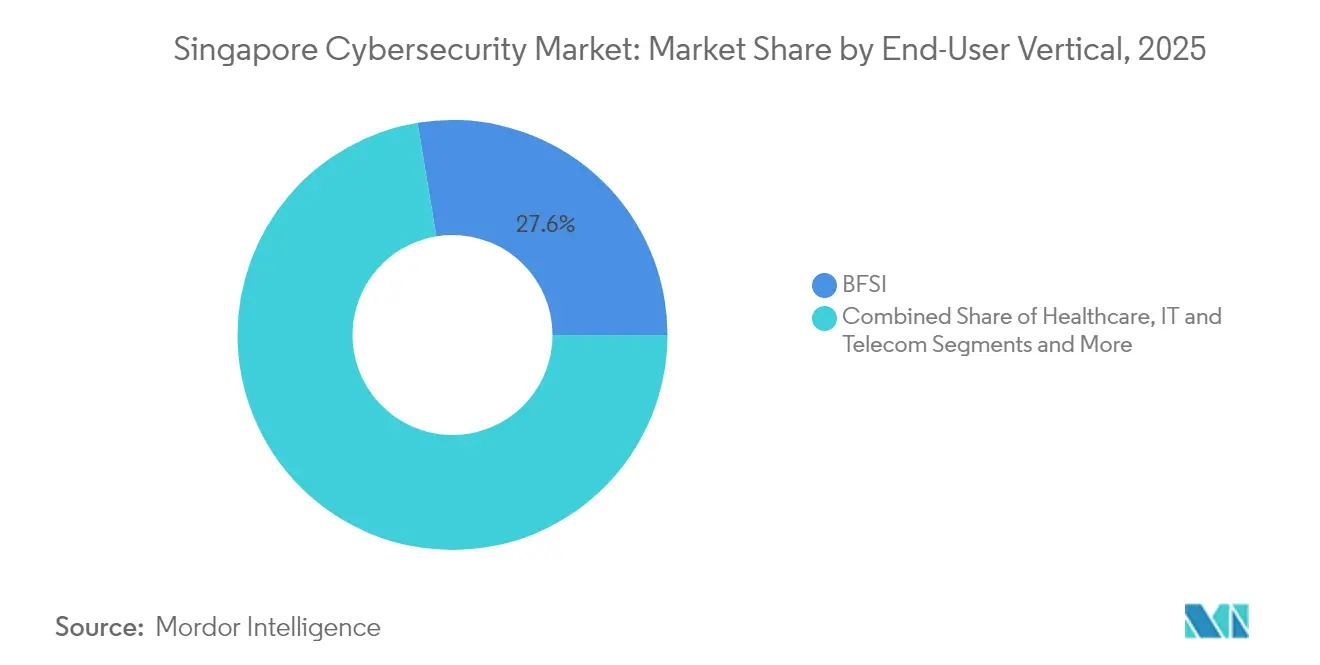

- By end-user vertical, BFSI led with 27.60% revenue share of the Singapore Cybersecurity market size in 2025, whereas healthcare spending is projected to grow at 18.74% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Singapore Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nationwide zero-trust architecture mandates | +3.2% | National, finance and government | Medium term (2-4 years) |

| Accelerated digital-bank licenses | +2.8% | Financial district | Short term (≤ 2 years) |

| SGX-listed firms’ disclosure rules | +1.5% | CBD | Short term (≤ 2 years) |

| Heightened OT-security demand | +2.5% | Western Singapore | Medium term (2-4 years) |

| Roll-out of 5G standalone networks | +1.8% | National | Medium term (2-4 years) |

| R&D tax-incentives | +1.2% | Innovation hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Nationwide Zero-Trust Architecture Mandates from Government

Regulators now compel every critical information-infrastructure owner to file a zero-trust roadmap, and 96% had submitted plans by November 2024. Financial institutions responded by micro-segmenting traffic, cutting unauthorized-privilege cases by 42% within one year of go-live. Budget cycles allocate up to 28% of security outlays to identity analytics, underscoring demand for context-aware access controls. Streamlined multi-agency design reviews compressed policy-approval windows to 34 days, halving historical delays and allowing vendors to accelerate revenue recognition. Together, these moves place zero-trust enforcement at the heart of every major tender, giving suppliers that support adaptive trust scoring a decisive edge.

Accelerated Digital-Bank Licences Driving Next-Gen BFSI Security Spend

Digital full-bank licensees accumulated SGD 1.8 billion in deposits by end-2024, equal to 4% of Singapore’s retail savings pool. Each new entrant channelled roughly 22% of operating expenditure into cybersecurity during its first year, an intensity mirrored by incumbents whose resilience investments grew 36% to SGD 491 million in 2024. Pilot deployments of post-quantum cryptography already protect 12% of domestic interbank traffic. Competitive parity now hinges on rapid threat-intelligence ingestion and automated compliance evidence, redirecting budgets toward managed detection and response platforms rather than standalone appliances. The banking cluster’s early adoption curves ripple through payments, wealth management and capital-markets systems, magnifying total addressable demand for the Singapore Cybersecurity market.

SGX-Listed Firms’ Mandatory Cyber-Incident Disclosure Rules

The Singapore Exchange oversees 714 issuers worth SGD 776 billion and plans to enforce four-business-day cyber-incident notification, a pilot regime that surfaced 14 reportable events in 2024. Listed firms lifted spending on automated breach-impact assessment tools by 31% after the trial, shrinking board-notification lag to 20 hours. Faster, transparent disclosure reduces rumor-driven price swings and places quantitative integrity metrics on investor dashboards. Vendors offering validated forensic data pipelines and template-driven regulatory reports find accelerated decision cycles. Over time the rules institutionalize cybersecurity as an ESG checkpoint, anchoring recurring demand across 714 corporate budgets and reinforcing the Singapore Cybersecurity market.

Heightened OT-Security Demand from Tuas Mega-Port and Jurong Island Revamp

Phase 1 of Tuas Mega-Port processed 3 million TEUs in 2024, each crane and automated guided vehicle streaming up to 2 GB of telemetry per hour that requires round-the-clock OT-SOC coverage. Jurong Island hosts more than 100 petrochemical plants that contributed SGD 81 billion in manufacturing output during 2023, and 87% of new OT devices were certified to IEC 62443 by mid-2024. Operators prefer unified IT-OT control planes to handle both process safety and cyber threats, elevating demand for deep-packet inspection sensors tuned to proprietary protocols. Capital-project consortia now embed security clauses worth 2%–3% of total build cost, locking in multiyear run-rate for managed OT-incident response. These industrial deployments, clustered in western Singapore, materially boost service hours sold into the Singapore Cybersecurity market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarce CREST-certified talent | –2.5% | National | Medium term (2-4 years) |

| Fragmented SME market | –1.5% | Suburban parks | Short term (≤ 2 years) |

| Data-sovereignty clauses | –1.2% | National | Medium term (2-4 years) |

| High compliance overlap | –0.8% | Regulated industries | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Scarce Pool of CREST-Certified Talent Inflates Service Costs

Only 530 CREST-certified professionals operated locally in 2024 against demand for 1,200, equating to a 56% gap. Median senior-analyst pay climbed 14% to SGD 117,000, compressing margins for managed security service providers. MSSPs used automation to trim Tier-1 ticket volumes by 35%, yet many still absorb wage inflation by passing through higher seat-licence prices. Persistent scarcity delays large rollouts, elongating go-live timelines and dampening short-term revenue conversion. Unless training pipelines expand materially, talent supply will continue to limit the Singapore Cybersecurity market’s ability to scale at the forecast rate.

Fragmented SME Market Still Anchored on Legacy Antivirus

SMEs represent 99% of Singapore firms but 58% remain dependent on standalone antivirus, with only 21% adopting multi-factor authentication. Average security budgets seldom exceed SGD 10,000, making price the dominant buying criterion. Government subsidies such as the CISO-as-a-Service grant averaged SGD 18,500 yet reached only 350 projects in the first year. Low cyber-insurance penetration—12% of eligible policies in 2024—further blunts incentives to modernise. The volume of small, non-recurring deals raises customer-acquisition costs and constrains vendor margins, moderating growth of the Singapore Cybersecurity market among micro-enterprises.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Dominate While Cloud Security Accelerates

Services contributed 59.60% to the Singapore Cybersecurity market share in 2025, helped by managed security service revenues of SGD 2.3 billion. Average mean-time-to-detect dropped from eight hours in 2022 to two hours in 2024, proving the return on 24/7 monitoring investments. Providers that integrate cross-border threat-intelligence achieved 92% renewal, outpacing the sector median of 84%. Clients increasingly bundle insurance broking and incident-response retainers with monitoring, creating annuity-like revenue for MSSPs. These factors sustain robust double-digit expansion for the Singapore Cybersecurity market.

Cloud security is on track for a 15.52% CAGR through 2031, riding on 84% enterprise cloud-workload penetration. Updated MAS rules expanded mandatory control objectives from eight to 11, intensifying due-diligence cycles yet enlarging addressable spend. Vendors that pair posture management with auto-remediation now execute 37 policy updates per client each month, triple 2022 volumes. Consumption-based pricing fits well with rapid scale-out during peak e-commerce seasons. As a result, cloud-native solutions will continue to outpace appliance refreshes inside the Singapore Cybersecurity market.

By Deployment Mode: Cloud Momentum Gathers Even as On-Premise Leads

On-premise installations still held 54.30% of the Singapore Cybersecurity market share in 2025, with 71% of financial-sector databases co-located in trusted facilities. Tier-4 floor space reached 660,000 m², providing large banks and payment networks with latency-controlled environments. Hybrid forensics workflows lowered evidence-processing time by 27%, validating a staged migration path for regulated workloads. Accordingly, most incumbents continue to refresh perimeter hardware even while piloting cloud-first applications.

Cloud deployments promise a 16.93% CAGR, buoyed by an extra 300 MW of hyperscale IT load planned for 2025-2027. Operators meeting the Green Data Centre standard report PUE below 1.3, releasing energy budgets for in-rack security accelerators. New bulk-licence tariffs priced per CPU-second reduced monthly invoice volatility by 18%, easing CFO concerns. Faster provisioning times allow startups to activate SOC infrastructure in hours rather than weeks. These advantages will keep cloud adoption at the forefront of the Singapore Cybersecurity market.

By End-User Vertical: Healthcare Emerges as High-Growth Challenger to BFSI

BFSI retained the largest Singapore Cybersecurity market share at 27.60% in 2025, having executed 4,712 cyber drill scenarios during the year . Synthetic-transaction monitoring sliced fraud losses by SGD 14 million, breaking a multi-year surge. Immutable backups now cover 82% of banks, insuring rapid recovery under adverse conditions. Vendor selection criteria prioritize zero-downtime upgrades and audited crypto-modules, prolonging refresh cycles yet enlarging per-node spend. BFSI therefore remains an anchor tenant for the Singapore Cybersecurity market.

Healthcare exhibits a 18.74% CAGR outlook, having logged 4.3 million digital hospital visits in 2024 —double 2022 volume. Farrer Park Hospital’s AI-powered SOC cut mean-time-to-respond to 12 minutes compared with a national average of 46 minutes. Medical-device vulnerability disclosures grew 28%, signaling proactive risk management as tele-ICUs proliferate. Cloud-native data-loss-prevention suites and secure-API gateways rise in priority as hospitals unify electronic medical records. Consequently, healthcare is set to be the fastest-growing vertical inside the Singapore Cybersecurity market.

By End-User Enterprise Size: Enterprise Dominance Persists While SME Uptake Quickens

Large enterprises commanded 77.60% of the Singapore Cybersecurity market size in 2025, with SGX-listed issuers alone investing SGD 1.96 billion in security capital and operating expenditure. Board reports now integrate cyber resilience into ESG dashboards for 63% of issuers, up from 38% three years earlier. Secure-by-design hardware purchases shrank end-of-life e-waste by 12%, an ancillary sustainability gain that resonates with investors. With regulators tightening benchmarks annually, large-cap spending shows little elasticity, undergirding baseline growth for the Singapore Cybersecurity market.

SME budgets are still modest but are expanding at an 18.09% CAGR thanks to IMDA’s CTO-as-a-Service programme that enrolled 1,600 subscribers by Q4 2024. Browser-based dashboards now cut initial configuration to 3.5 hours, replacing appliance rollouts that once took 18 hours. Cyber-insurance holders deploying multi-factor authentication filed 27% fewer ransomware claims, encouraging insurers to offer premium rebates. Together, simplified user experiences and risk-transfer incentives make SMEs the next frontier of the Singapore Cybersecurity market.

Geography Analysis

Singapore’s central business district continues to anchor the Singapore Cybersecurity market, housing headquarters of more than 200 regional banks and insurers that together spend over SGD 1.2 billion on security each year. Mandatory four-day breach-disclosure rules at SGX-listed firms compressed remediation lead times, pushing managed detection demand higher in the CBD. High-density office towers also host distributed SOC centres that offer 24/7 coverage for ASEAN clients, concentrating skilled labour and premium colocation facilities.

Western Singapore, stretching from Tuas Port to Jurong Island, represents the fastest-expanding subregion. The port’s automated container terminals generate terabytes of OT telemetry that require protocol-aware intrusion detection, while petrochemical complexes on Jurong Island integrate IEC 62443-certified controllers. These projects favour suppliers that can certify both marine and process-safety environments, creating niche opportunities for OT-specialist MSSPs. Supporting infrastructure such as the JL-NTU Maritime AI lab further boosts pilot activity, deepening regional share of the Singapore Cybersecurity market.

Northern and eastern districts benefit from near-total 5G standalone coverage that attained 95% population reach in 2024. Edge-compute nodes collocated at suburban exchanges host low-latency security analytics for telemedicine, smart-transport and drone-delivery pilots. Community hospitals and polyclinics in the east now process fully digital EMR traffic, prompting incremental licensing of API-security gateways. Meanwhile, suburban innovation parks house many SMEs targeted by CTO-as-a-Service grants, raising micro-segmentation and email-security orders. Collectively these zones ensure balanced geographic demand across the Singapore Cybersecurity market.

Competitive Landscape

Ensign InfoSecurity recorded SGD 281 million revenue in 2024, a 20% jump that lifted its customer-retention rate to 94%, well above the 86% industry median. Palo Alto Networks booked Asia-Pacific orders worth USD 1.36 billion, citing “high-double-digit millions” from Singapore as zero-trust deals closed ahead of regulatory deadlines. Local analytics start-up Seconize secured 68 paid government pilots through the Open Innovation Platform, spotlighting appetite for AI-native vulnerability scoring.

Strategic alliances shape the mid-tier: StarHub’s Cybersecurity Services arm reported SGD 104 million revenue, with 40% stemming from bundled 5G edge-security packages. The Singapore Manufacturing Federation recorded an 18% reduction in procurement lead-time for Industry 4.0 adopters using these telecom-plus-security bundles. Identity provider Okta enlarged its active local customer base by 47% to 310, driven by stricter MAS authentication guidance.

Price pressure remains intense in the SME segment where Check Point’s average bundle fell to USD 6,400 in 2024, 5% lower year on year. To defend margins MSSPs automated 62% of Tier-1 tasks, reallocating analysts toward consultancy upsells[3]Association of Information Security Professionals, “Operations Study 2024,” aisp.sg . API-first security platforms report 33% integration-cost savings versus appliance models, a gap highlighted in Cisco’s 2024 Singapore Partner Economics paper. The combined moves underscore a healthy but competitive Singapore Cybersecurity market.

Singapore Cybersecurity Industry Leaders

Horangi Cyber Security

wizlynx Pte Ltd

Attila Cybertech Pte Ltd

Tech Security

Tenable Singapore

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Singtel activated 700 MHz 5G spectrum that lifts median indoor download speeds to 600 Mbps, enabling AI-driven 4K surveillance without backhaul links.

- February 2025: Ensign InfoSecurity ranked sixth globally in MSSP Alert’s Top 250 while confirming a 94% renewal rate.

- November 2024: Semperis raised USD 125 million Series C funding and pledged to train 1,000 local engineers in identity-attack mitigation.

- October 2024: PSA started a USD 647.5 million supply-chain hub whose robotics arm will emit 2 TB sensor data daily, demanding high-throughput OT-security analytics.

Singapore Cybersecurity Market Report Scope

Cybersecurity solutions help organizations detect, monitor, report, and counter cyber threats to maintain data confidentiality. The adoption of cybersecurity solutions is expected to grow in line with the rising internet penetration among developing and developed countries. The need for cybersecurity has increased as every system in today's world is connected to the Internet, making data more accessible to cybercriminals.

The Singapore cybersecurity market is segmented by offerings (solutions [application security, cloud security, data security, identity access management, infrastructure protection, integrated risk management, network security, end-point security, and other solution types] and services [professional services and managed services]), by deployment (On-premise, and cloud), by organization size (SMEs, large enterprises), by end-user vertical (BFSI, healthcare, IT and telecom, industrial and defense, retail, energy and utilities, manufacturing, and other end-user industries). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security Equipment | |

| Endpoint Security | |

| Other Services | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| On-Premise |

| Cloud |

By End-User Vertical

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defense |

| Manufacturing |

| Retail and E-commerce |

| Energy and Utilities |

| Others |

By End-User Enterprise Size

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security Equipment | ||

| Endpoint Security | ||

| Other Services | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | On-Premise | |

| Cloud | ||

| By End-User Vertical | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defense | ||

| Manufacturing | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Others | ||

| By End-User Enterprise Size | Small and Medium Enterprises (SMEs) | |

| Large Enterprises | ||

Key Questions Answered in the Report

What is the current Singapore Cybersecurity market size and growth rate?

The Singapore Cybersecurity market size is USD 3.07 billion in 2026 and is forecast to reach USD 6.41 billion by 2031, reflecting a 15.86% CAGR.

Which industry segment spends the most on cybersecurity?

Banking, financial services and insurance accounts for 27.60% of total spending, driven by stringent MAS regulations and new digital-bank licences.

How extensive is 5G coverage in Singapore and why does it matter for security?

5G standalone networks cover 95% of the population, enabling low-latency services that require cloud-native security functions to protect micro-service cores.

How large is the local cybersecurity talent shortfall?

Singapore had 17,100 practitioners for 18,000 roles in 2024, with only 530 CREST-certified experts, leaving a 900-position gap.

Why are SMEs a rising opportunity in the Singapore Cybersecurity market?

Government grants and cyber-insurance incentives are lifting SME adoption, supporting an 18.09% CAGR in SME cybersecurity spending through 2031.

Page last updated on: